Embed Size (px)

Citation preview

Japan’s Trade Strategy in the 21st Century and Economic Partnership

with Latin American Countries Revisited Prof. Yorizumi WATANABE

Faculty of Policy Management

KEIO UNIVERSITY (SFC)

Brasilia, December 1 2017

Yorizumi Watanabe, Keio University 1

Outline of Today’s Presentation

• Point of Departure: Two Major Concerns

• 1. Mega-Regions and Mega-FTAs i.e. TPP, RCEP+JCK/FTA, Japan-EU FTA, TTIP

• 2. Japan’s Bilateral FTA/EPA Policy

• 3. TPP/12 & TPP/11: a Bumpy Road towards “the Golden Standard”

• 4. The Japan-Mexico EPA(2005) as a Model for Future Japan-Latin America Economic Partnership

• 5. Bilateral Relations between Japan and Brazil

• 6. Concluding Remarks

Two Major Sources of Uncertainty BREXIT & Trump Shock

Why Brexit matters ?: Major Japanese Companies Presence in the UK company Sales in the

EU(Oku Yen) British Employee

Export to the EU

Toyota 23,233 3,000 75% of the UK production to the EU

SONY 18,813 5,000 Headquarters function for the EU

Nissan 17,481 8,000 80% of the UK production to the EU

Canon 10,743 2,800 Camera, Multi-function equipment

Hitachi 9,511 5,000 8000 OkuYen awarded order trains

Toshiba 5,599 n.a. Headquarters Function for the EU

Ricoh 5,310 3,000 Overall sales in the EU

Mitsubishi Electric

3,699 n.a.. Air conditioning system in the EU

KonicaMinolta 3,197 1,300 Multifunction office equipment

Takeda Pharma. 3,093 n.a. Experiments for the entire EU market

Nomura HD 1,458 2,500 Supporting M&A、security, banking 4

US Withdrawal from the TPP (Jan. 23 2017)

5

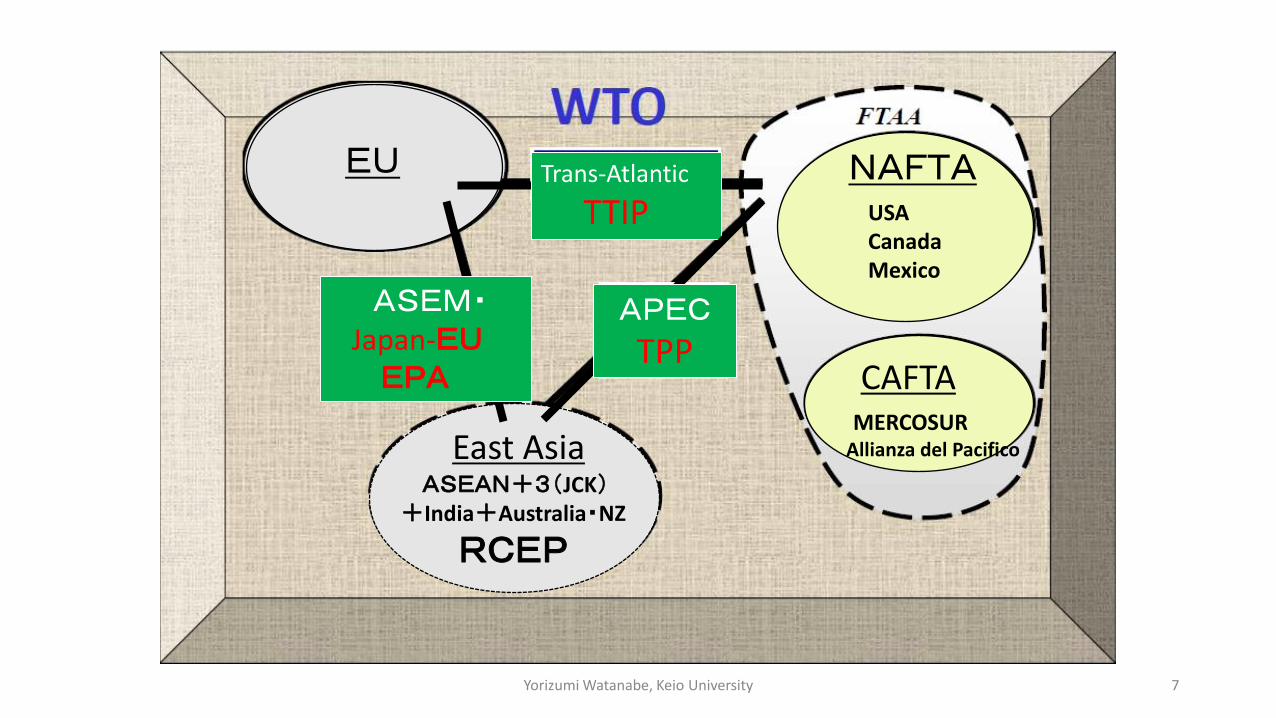

1. Mega-Regions and Mega-FTAs; TPP, RCEP+JCK/FTA, Japan-EU FTA, TTIP Existing Mega-FTAs and other Mega-FTAs under Negotiation

NAFTA USA Canada Mexico

CAFTA MERCOSUR Allianza del Pacifico East Asia

ASEAN+3(JCK) +India+Australia・NZ

RCEP

EU Trans-Atlantic

TTIP

ASEM・ Japan-EU EPA

APEC

TPP

Yorizumi Watanabe, Keio University 7

Membership and Economic Importance of the Mega-FTAs

Trade (2012)

Trade (2012)

GDP (2011)

GDP (2011)

Billion US $

Share (%)

Billion US $

Share (%)

JCK FTA 6,619

17.9 14,280.9 20.4

RCEP 10,470 28.4 19,929.9 28.5

TPP 9,545 25.9 26,593.4 38.0

TTIP 15,602 42.3 32,686.5 46.8

World 36,890 100.0 69,899.2 100.0

Yorizumi Watanabe, Keio University 8

Slide 9

RCEP 28% JCK 20%

TPP 38%

TTIP 47%

2. Japan’s FTA/EPA Policy

Unification of supply chain networks in the East Asia region

ASEAN

Australi

a

NZ

Japan

China

South Korea

India

.

• In order to increase exports to growth markets both inside and outside the East Asia

region, the unification of corporate supply chains is essential.

• At present, each EPA has its own set of regulations (e.g. rules of origin), and the

differences between these regulations hinder corporate activities. By unifying these

regulations into a single set of simple, easy-to-use rules for corporations, RCEP will

facilitate the establishment of an trans-national supply chain network.

Example 1: a Japanese automobile

company based in Thailand imports

engines and transmissions from

Japan, assembles them in Thailand,

and exports them to Australia.

Example 2: A Japanese auto-parts

manufacturer based in Thailand

imports parts from Japan,

manufactures airbags in Thailand

using these parts, and exports

these airbags to India.

Example 3: a Japanese elevator

manufacturer based in Thailand

imports hoists from China,

manufactures elevators in Thailand,

and exports them to India.

11

The significance of participation in RCEP

C C

• Transaction volumes of intermediate goods have risen rapidly among ASEAN

states. This reflects the increasing sophistication of production networks in

East Asia.

12

Change in quality of Japan-ASEAN-China trade

Japan

East Asia

China

Source: created from RIETE-TID 2011

*width of arrow represents trade value (1billion dollars); color denotes share of intermediate goods.

East Asia

Japan

China

*width of arrow represents trade value (1billion dollars); color denotes share of intermediate goods.

Source: created from RIETE-TID 2011

Japan’s FTA/EPA Strategy in Asia-Pacific & beyond • De-facto Business-driven Integration through Supply-chain and

Production Networks

• FTA/EPAs to consolidate the merits of the De-facto Integration

• From Bilateral FTA/EPAs to Wider Regional FTA/EPAs: (ASEAN+1)x5, ASEAN+3, ASEAN+6=RCEP, Japan-China-Korea EPA

• Beyond Regional FTA/EPAs ⇒⇒⇒ the TPP as an inter-regional FTA

Yorizumi Watanabe, Keio University 13

14

Japan’s EPAs: achievements so far (as of Nov. 2017)

• Japan-Singapore EPA (in force since 2002.11)

• Japan-Mexico EPA (negotiations started in 2002.11, in force since 2005.4)

• Japan-Malaysia EPA (in force since 2006.7)

• Japan-Chile EPA (negotiations started in 2006.2, in force since 2007.9 )

• Japan-Thailand EPA (agreement in substance 2005.9, in force 2007.11)

• Japan-Indonesia EPA (negotiations started in2005.7, in force 2008.7)

• Japan-Brunei EPA (negotiations started in 2006.6, in force 2008.7)

• Japan-ASEAN EPA (negotiations started in 2005.4, in force 2008.12)

• Japan-Philippines EPA (agreement in substance 2004.11, in force 2008.12)

• Japan-Switzerland EPA (negotiations started in 2007.5, in force 2009.2)

• Japan-Vietnam EPA (negotiations started in 2007.1, in force 2009.10)

• Japan-India EPA (negotiations started in 2007.1, in force 2011.8)

• Japan-Peru EPA (negotiations started in 2009.5, in force 2012.3)

• Japan-Australia EPA (negotiations started in 2007.4, agreement in substance in 2014.04, in force 2015.01)

• Japan-Mongolia EPA (negotiation started in 2012.6, signed in 2015.02, in force 2016.06)

• Japan-EU EPA (negotiation started in 2013.03, agreement in principle reached in 2017.07)

• Japan-Korea EPA (negotiations started in 2003.12, suspended in 2004.11)

• Japan-GCC EPA (negotiations started in 2006.9)

• Japan-Canada EPA (negotiation started in 2012. 10)

• Japan-Colombia EPA (negotiation started in 2012. 12)

• Japan-Turkey EPA (negotiation started in 2014.12)

15

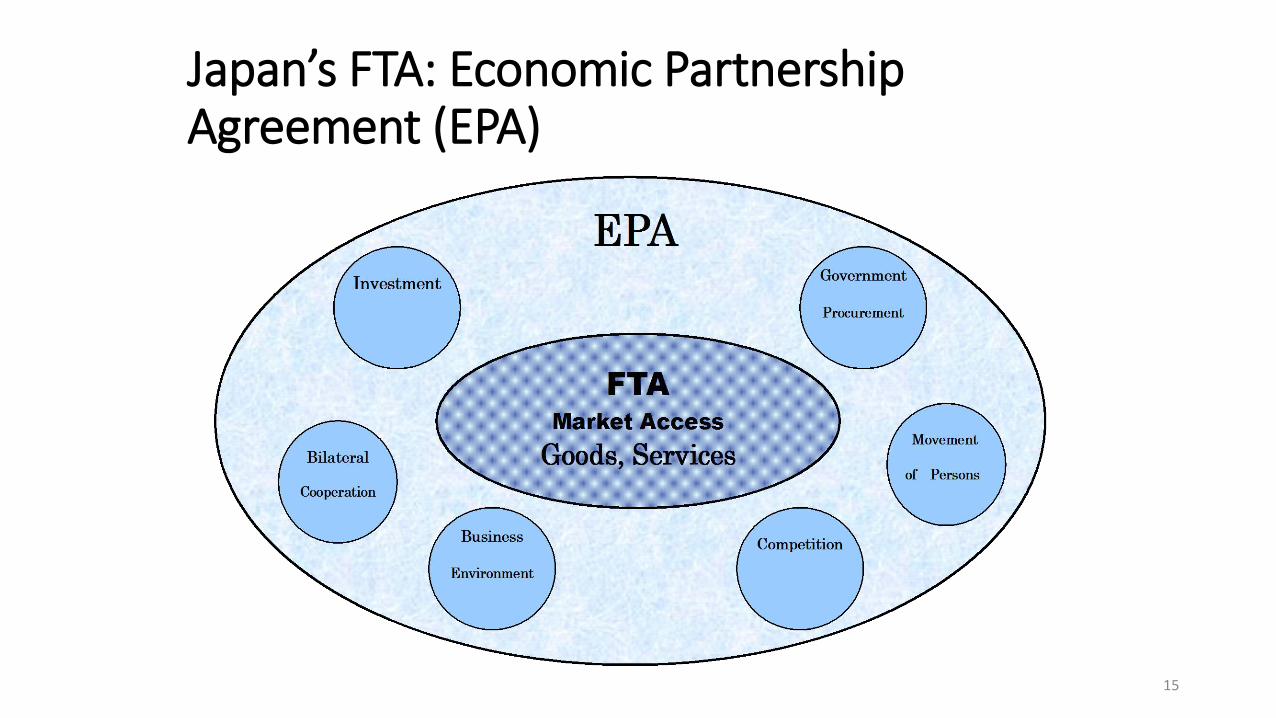

Japan’s FTA: Economic Partnership Agreement (EPA)

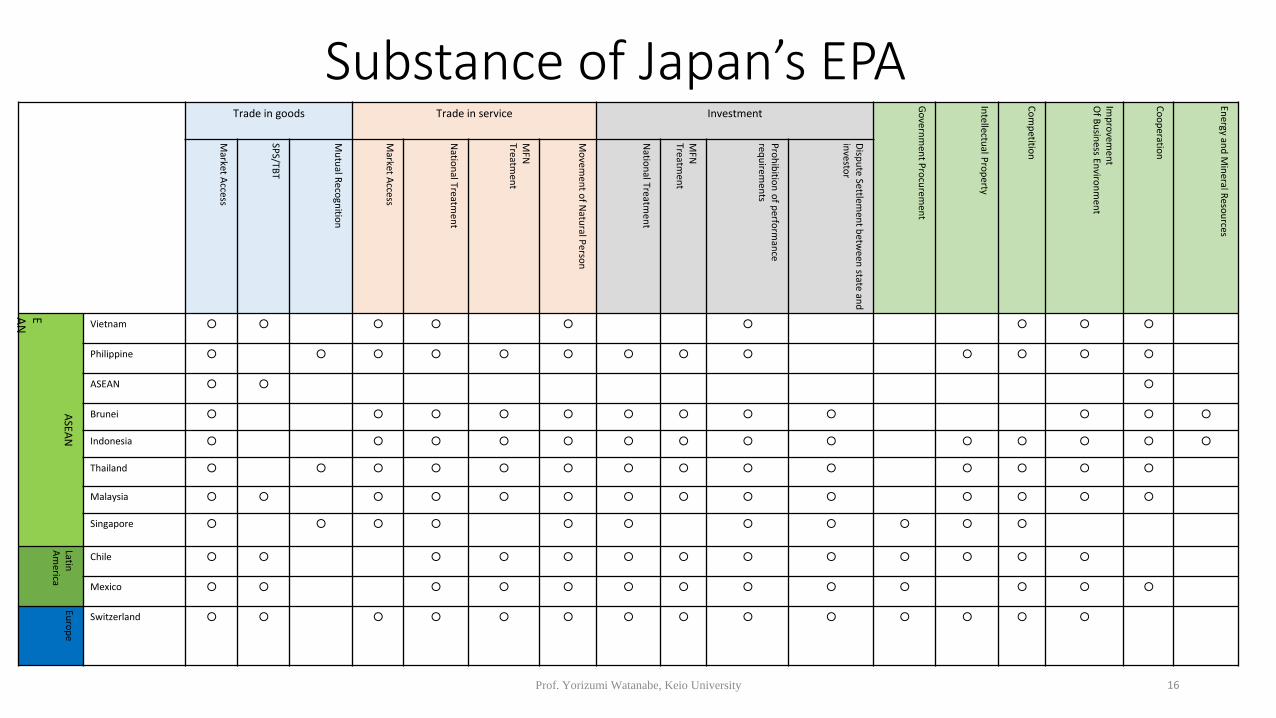

Substance of Japan’s EPA Trade in goods Trade in service Investment

Go

vernm

ent P

rocu

remen

t

Intellectu

al Pro

perty

Co

mp

etition

Imp

rovem

ent

Of B

usin

ess Enviro

nm

ent

Co

op

eration

En

ergy and

Min

eral Reso

urces

Market A

ccess

SPS/TB

T

Mu

tual R

ecogn

ition

Market A

ccess

Natio

nal Treatm

ent

MFN

Treatm

ent

Mo

vemen

t of N

atural P

erson

Natio

nal Treatm

ent

MFN

Treatm

ent

Pro

hib

ition

of p

erform

ance

requ

iremen

ts D

ispu

te Settlemen

t betw

een state an

d

investo

r

ASEA

N

E AN

Vietnam ○ ○ ○ ○ ○ ○ ○ ○ ○

Philippine ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

ASEAN ○ ○ ○

Brunei ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Indonesia ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Thailand ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Malaysia ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Singapore ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Latin

Am

erica

Chile ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Mexico ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

Euro

pe

Switzerland ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○ ○

16 Prof. Yorizumi Watanabe, Keio University

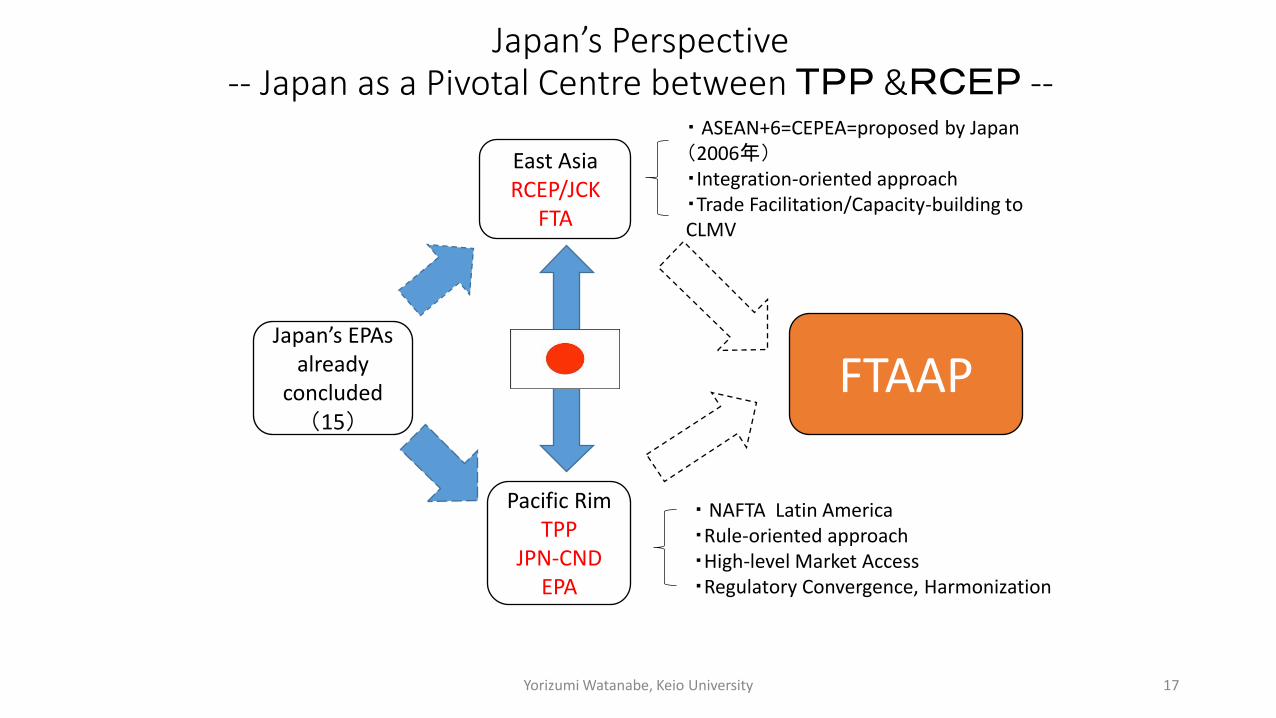

Japan’s Perspective -- Japan as a Pivotal Centre between TPP &RCEP --

East Asia RCEP/JCK

FTA

Japan’s EPAs already

concluded(15)

FTAAP

Pacific Rim TPP

JPN-CND EPA

・ ASEAN+6=CEPEA=proposed by Japan(2006年) ・Integration-oriented approach ・Trade Facilitation/Capacity-building to CLMV

・ NAFTA Latin America ・Rule-oriented approach ・High-level Market Access ・Regulatory Convergence, Harmonization

17 Yorizumi Watanabe, Keio University

Yorizumi Watanabe, Keio University 18

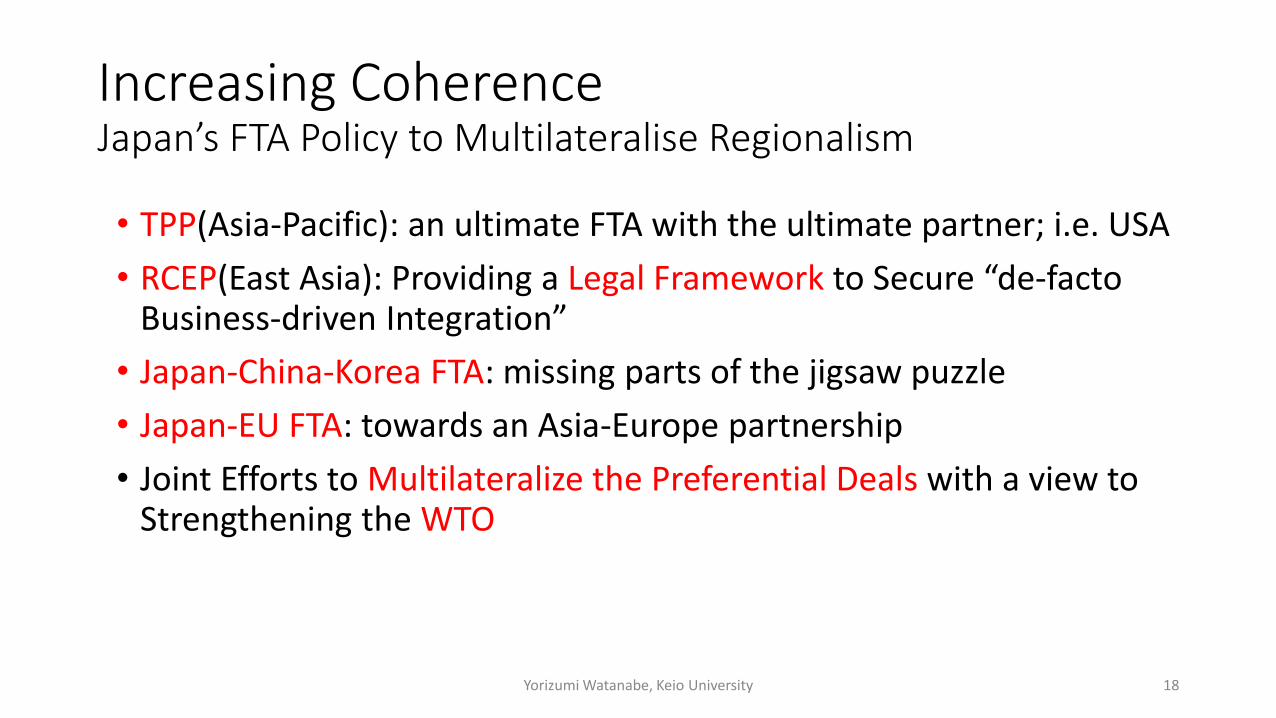

Increasing Coherence Japan’s FTA Policy to Multilateralise Regionalism

• TPP(Asia-Pacific): an ultimate FTA with the ultimate partner; i.e. USA

• RCEP(East Asia): Providing a Legal Framework to Secure “de-facto Business-driven Integration”

• Japan-China-Korea FTA: missing parts of the jigsaw puzzle

• Japan-EU FTA: towards an Asia-Europe partnership

• Joint Efforts to Multilateralize the Preferential Deals with a view to Strengthening the WTO

NAFTA USA Canada Mexico

CAFTA MERCOSUR Allianza del Pacifico East Asia

ASEAN+3(JCK) +India+Australia・NZ

RCEP

EU Trans-Atlantic

TTIP

ASEM・ Japan-EU EPA

APEC

TPP

Yorizumi Watanabe, Keio University 19

3. TPP/12 & TPP/11: A Bumpy Road to Agree on “the Golden Standard”

Agenda of the TPP Trans-Pacific Strategic Economic Partnership Agreement -”P4”: a comprehensive FTA including elimination of all tariffs among Chile, Brunei, New Zealand, and Singapore -TPP/12: ・Participants: US, Canada, Mexico, Peru, Chile, Vietnam, Malaysia, Singapore, Brunei, Australia and New Zealand, Japan

・ Goal: agreed in Oct. 2015, signed in Feb. 2016, BUT US withdrew in Jan. 2017⇒TPP/11 ・ Negotiating Agenda: 30 chapters including 4 cross-cutting issues

• Competition (SOEs)

• Market Access for goods (sugar, beef, rice,..)

• Cooperation and Capacity building

• Cross-border services

• Customs

• E-commerce

• Environment

• Financial services

• Government Procurement

• Intellectual Property Rights

• Investment (ISDS)

• Labour

• Legal issues

• Rules of Origin (textiles and apparel) • Sanitary and Phytosanitary Standards(SPS) • Technical Barriers to Trade (TBT) • Telecommunications • Temporary Entry • Textiles and apparel • Trade remedies • Regulatory coherence • Competitiveness and business facilitation • SMEs • Development

22 Yorizumi Watanabe

Japan and the TPP

• President Obama Visit in Tokyo, November 2009: a wake-up call

• PM Kan(DPJ) on the TPP at the Diet, October 2010: a strategic failure provoking strong opposition against the TPP, inter alia, from Agriculture Lobby

• PM Noda(DPJ) to step forward, November 2011/2012: influence on China (ASEAN+3 ⇒ ASEAN+6/RCEP) and the EU (FTA with Japan)

• Canada, Mexico joined TPP Negotiations 2012

• PM Abe (LDP) to join TPP Negotiations, March 2013

• Japan-US Agreement on Bilateral Talks on Cars & NTMs, April 2013

• Japan joined TPP Negotiations, July 2013

Yorizumi Watanabe, Keio University 23

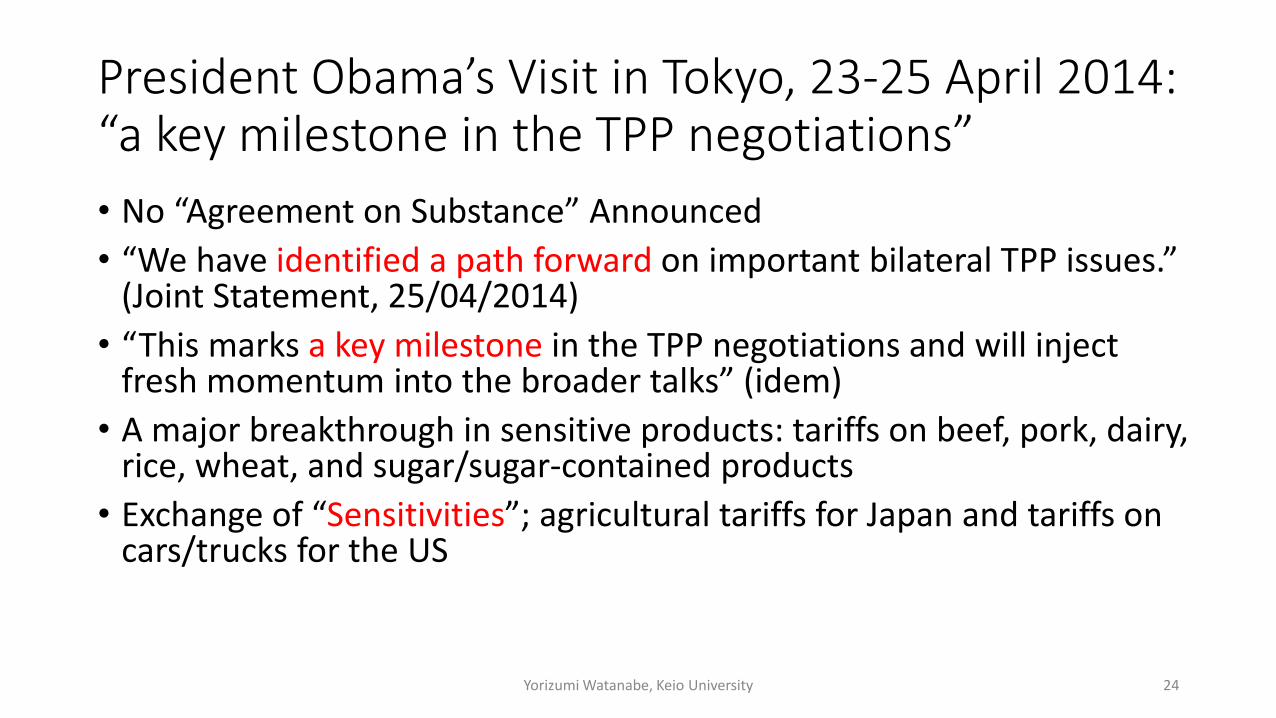

President Obama’s Visit in Tokyo, 23-25 April 2014: “a key milestone in the TPP negotiations”

• No “Agreement on Substance” Announced

• “We have identified a path forward on important bilateral TPP issues.” (Joint Statement, 25/04/2014)

• “This marks a key milestone in the TPP negotiations and will inject fresh momentum into the broader talks” (idem)

• A major breakthrough in sensitive products: tariffs on beef, pork, dairy, rice, wheat, and sugar/sugar-contained products

• Exchange of “Sensitivities”; agricultural tariffs for Japan and tariffs on cars/trucks for the US

Yorizumi Watanabe, Keio University 24

カナダ 0%

メキシコ 0% 豪州 0%

NZ 0%

シンガポール 0%

マレーシア 0%

ベトナム 0%

中国 0% 韓国 0% インド

0% 香港 0% 台湾 0%

EU 0%

その他 0%

カナダ 0%

メキシコ 0%

NZ 0%

シンガポール 0%

マレーシア 0%

ベトナム 0%

その他ASEAN 0% 中国 0% 韓国 0% インド

0%

台湾 0%

EU 0%

その他 0%

U.S. 27.5%

Canada 1.4%

Mexico 0.4%

Australia 5.9%

NZ 0.2%

Singapore 3.5%

Malaysia 1.3%

Vietnam 0.8%

Other ASEAN countries

6.2% China 9.0%

South Korea 2.5%

India 1.5%

Hong Kong 1.8%

Taiwan 1.3%

EU 22.9%

Other 14.0%

TPP

41.0%

RCEP 30.8%

U.S. 17.6%

Canada 1.3%

Mexico 1.3%

Chile 0.2%

Peru 0.1%

Australia 2.3%

NZ 0.2%

Singapore 2.9%

Malaysia 2.2%

Vietnam 1.3% Other ASEAN

countries 9.7%

China 18.1%

South Korea 7.7%

India 1.3%

Taiwan 5.8%

Hong Kong 5.1%

EU 10.2%

Other 12.5%

RCEP

45.8%

TPP

29.6%

Trade data: Trade Statistics of Japan

(Ministry of Finance, 2012)

Japan→world

(2012)

89,812,800

million yen

Japan→world

(2012)

63,747,600

million yen

Proportion of Japanese exports by region, in

2012

Proportion of Japanese FDI by region, in 2012

Approx. 45.8% of exports by value were exported to states engaged in RCEP

negotiations.

Approx. 30.8% of foreign direct investment was invested in states engaged in RCEP

negotiations.

*Individual figures for Peru, Chile, Brunei, and Papua New Guinea are excluded,

since they have not published stock results. However, total figures by region include

those states that have not published their results.

Source: Japanese foreign assets and liabilities balance (Ministry of Finance)

Direct investment (assets) balance statistics, by region (Bank of Japan)

25

The significance to Japan of the Pacific-Asia region

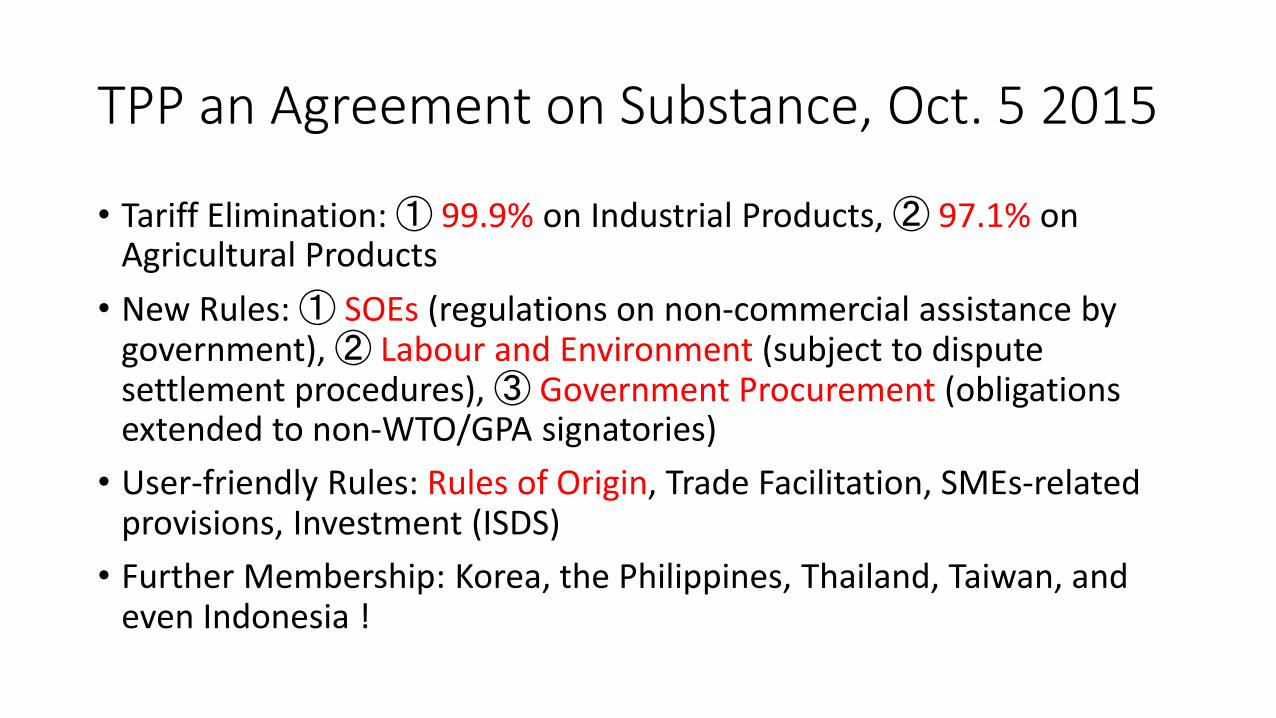

TPP an Agreement on Substance, Oct. 5 2015

• Tariff Elimination: ① 99.9% on Industrial Products, ② 97.1% on Agricultural Products

• New Rules: ① SOEs (regulations on non-commercial assistance by government), ② Labour and Environment (subject to dispute settlement procedures), ③ Government Procurement (obligations extended to non-WTO/GPA signatories)

• User-friendly Rules: Rules of Origin, Trade Facilitation, SMEs-related provisions, Investment (ISDS)

• Further Membership: Korea, the Philippines, Thailand, Taiwan, and even Indonesia !

Tariff Elimination in the TPP Negotiations: Tariff Offer by Japan (81% of agri-tariffs)

95%: tariffs maintained on 412 products (rice, sugar, wheat, dairy products, beef/port, etc)

Provided that the tariffs to be eliminated on leather products, wine, chocolate, cockies, salt, tobacco, beef tongue, etc

93.5%: tariff maintained on 586 products (rice, wheat, dairy, beef/pork, sugar, pineapple, etc.)

89.7%: tariffs maintained on 929 products that Japan has never offered zero-duty

88.4%: the highest level of tariff concession by Japan’s EPA (the Japan-Philippines EPA)

27 Yorizumi Watanabe

Rules of Origin in TPP (most generous accumulation rule to facilitate supply chain) • ASEAN CEPT scheme: 40%

• NAFTA scheme: 62.5% (in case of auto/auto-parts)

• Completed Passenger Vehicle: 55% (exceptions where special considerations provided to such items as; tempered glass, car-body for passenger vehicle, car-body of commercial vehicle, bumper, door, axle)

• Car Parts/Components: Change in Tariff Classification Criteria or Value-added Criteria (45~55%)

⇒⇒⇒ some shift of production might take place from non-TPP countries to TPP member countries

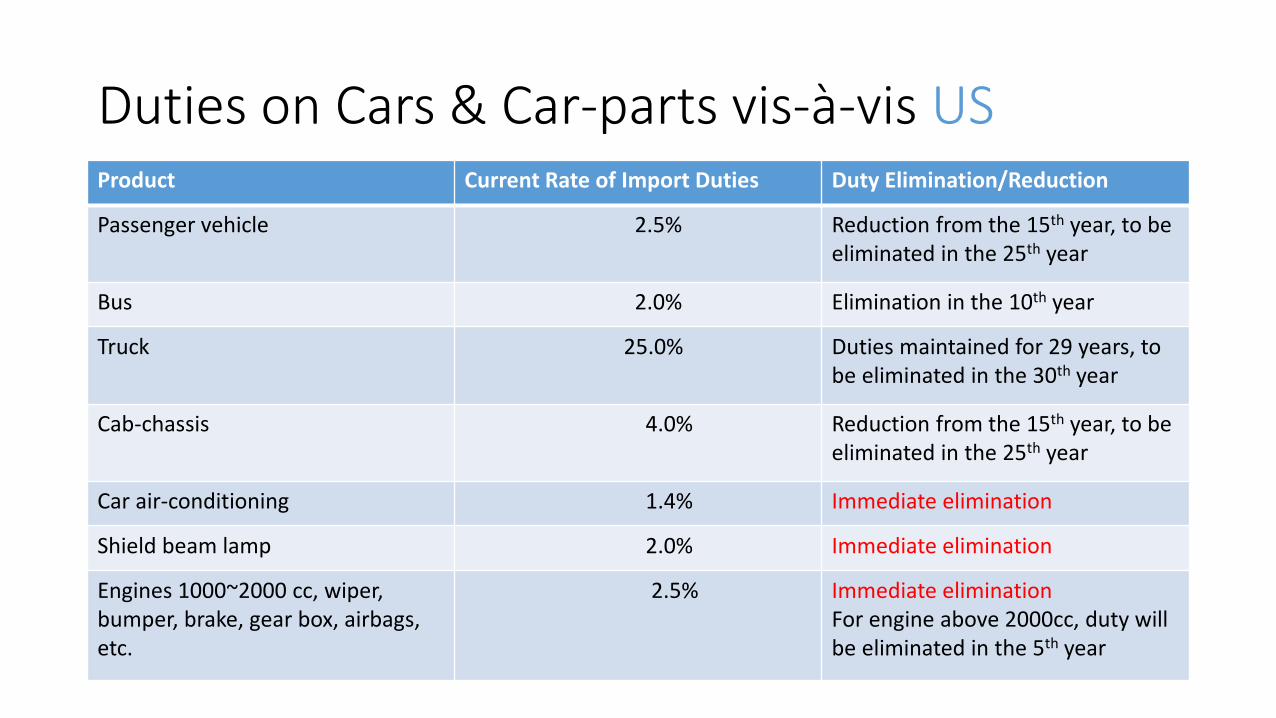

Duties on Cars & Car-parts vis-à-vis US Product Current Rate of Import Duties Duty Elimination/Reduction

Passenger vehicle 2.5% Reduction from the 15th year, to be eliminated in the 25th year

Bus 2.0% Elimination in the 10th year

Truck 25.0% Duties maintained for 29 years, to be eliminated in the 30th year

Cab-chassis 4.0% Reduction from the 15th year, to be eliminated in the 25th year

Car air-conditioning 1.4% Immediate elimination

Shield beam lamp 2.0% Immediate elimination

Engines 1000~2000 cc, wiper, bumper, brake, gear box, airbags, etc.

2.5% Immediate elimination For engine above 2000cc, duty will be eliminated in the 5th year

Duties on Cars & Car-parts vis-à-vis Canada

Product Current Rate of Import Duties Duty Elimination/Reduction

Passenger vehicle 6.1% To be eliminated in the 5th year

Bus 6.1% To be eliminated in the 11th year

Large gasoline truck 6.1% To be eliminated in the 6th year

Truck 6.1% To be eliminated in the 11th year

Car air-conditioning, car body, brake, suspension, steering gear, etc.

6.0% Immediate elimination

tire 7.0% To be eliminated in the 4th year

Duties on Cars & Car-parts vis-à-vis Mexico

Product Current Rate of Import Duties Duty Elimination/Reduction

Passenger vehicle 15~30% Immediate elimination

Bus 15~30% Phasing-out over 10 years

Small truck 15~30% Immediate elimination

Medium-sized & large truck 30% Phasing-out over 10 years

Used car 50% Reduction at coming-into-force

Engine parts 5% Immediate elimination

Shock-absorber parts 5% To be eliminated in the 5th year

Duties on Cars & Car-parts vis-à-vis Others

Country Product Current Rate of Import Duties

Duty Elimination/Reduction

New Zealand Passenger vehicle 10% Immediate elimination

New Zealand Bus 5% Immediate elimination

New Zealand Truck 5% Immediate elimination

Peru Passenger vehicle 9% Immediate elimination

Viet Nam Passenger vehicle above 3000cc

77/80 % To be eliminated in the 10th year

Viet Nam Passenger vehicle below 3000cc

77~83% To be eliminated in the 13th year

Viet Nam Truck 10~80% To be eliminated in the 12th ~13th year

4. The Japan-Mexico EPA(2005) and Beyond The Renewed Partnership between Japan and Mexico as a model for future Japan-Latin America Economic Relations

Japan-Mexico Renewed Partnership • 2002.7 Joint Study Group concluded its work • 2002.11 Negotiation started on the Officials’ Level • 2003.10 President Fox’s State Visit to Tokyo (negotiation broken down) • 2003.11 Negotiation resumed (”Compare-notes”) • 2004.3 Agreement on Substance reached • 2004.9 Agreement signed (PM Koizumi & President Fox, Mexico City) • 2005.4 Coming-into-effect of the Agreement • 2007.4 Coming-into-effect of the Protocol for Improved Market Access • 2008.9 Negotiation for Amendment started • 2011.2 Agreement reached on Amendment of the Agreement • 2011.9 Signature on the Amended Agreement • 2012.4 Coming-into-force of the Amended Agreement

Yorizumi Watanabe, Keio University 34

Increase in Bilateral Trade between Japan and Mexico (2004-2013) ☆Two-way Trade: JPY 785 billion (2004) ⇒ JPY 1,358 billion (2013)

Mexico ⇒ Japan • Pork: 32,712 t (2004) ⇒ 57,379 t (2013) • Beef: 1,772 t (2004) ⇒ 14,272 t (2013)

Japan ⇒ Mexico • Automobile: JPY 82.7billion (2004) ⇒ JPY135.3 billion (2013) • Auto Parts: JPY 58.3 billion (2004) ⇒ JPY 137.2 billion (2013)

☆Self-declaration for Certification in Rules-of-Origin ☆Improvement of Business Environment ☆Government Procurement

Yorizumi Watanabe, Keio University 35

Japanese Companies in Mexico (2004-2015)

310 326367 384 366 399 428

464546

679

814

957

0

100

200

300

400

500

600

700

800

900

1000

World Car Production Top 15 (2005-2014) RANKING 2005 million unit 2013 million unit 2014 million unit

1 USA 11.9 China 22.1 China 23.7

2 Japan 10.8 USA 11.1 USA 11.7

3 Germany 5.8 Japan 9.6 Japan 9.8

4 China 5.7 Germany 5.7 Germany 5.9

5 ROK 3.7 ROK 4.5 ROK 4.5

6 France 3.5 India 3.9 India 3.8

7 Spain 2.8 Brazil 3.7 Mexico 3.4

8 Canada 2.7 Mexico 3.1 Brazil 3.1

9 Brazil 2.5 Thailand 2.5 Spain 2.4

10 UK 1.8 Canada 2.4 Canada 2.4

11 Mexico 1.7 Spain 2.2 Russia 1.9

12 India 1.6 Russia 2.2 Thailand 1.9

13 Russia 1.4 France 1.7 France 1.8

14 Thailand 1.1 UK 1.6 UK 1.6

15 Italy 1.0 Indonesia 1.2 Indonesia 1.3

Multilateralizing Regionalism

• Convergence of Liberalization Efforts in 3 Mega FTAs, i.e. TPP, TTIP, and the Japan-EU EPA

• A New Momentum to reinforce the Trade Multilateralism embodied in the WTO

• Japan and the Mexico/US should demonstrate leadership in TPP and beyond

Yorizumi Watanabe, Keio University 38

5. The Bilateral Relations between Japan and Brazil

The Bilateral Economic Relations between Japan and Brazil • Japan’s Export to Brazil: US$ 5.9 billion, 2.6% of Brazil’s Total Import

(MDIC,2014)

• Japan’s Import from Brazil: US$ 6.7 billion, 3% of Brazil’s Total Export (MDIC, 2014)

• FDI from Japan: US$ 3.8 billion (DECAM, 2014), 450+Japanese Companies

• Untapped Potentiality: rich agriculture, natural resources, energy, growing market with young population, etc.

• MERCOSUR since 1995: Pros & Cons

• Proposal on “Japan-Brazil Economic Partnership Agreement” by Japan’s Keidanren and CNI of Brazil, Aug.-Sept. 2015

6. Conclusions TPP provides a momentum to free trade arrangements such as RCEP, JCK FTA and ASEAN Economic Community.

In the absence of WTO/DDA development on rule-making, the TPP rules could become “model rules” in such area as Investment, Competition, and Government Procurement etc.

Japan is interested in high-quality rules as well as high-level market access liberalization with the like-minded countries like Pacific Alliance Members across Asia-Pacific and beyond. Japan and Brazil should explore all the possibilities to establish a FTA between them.

Thank you for Your Attention --- Free Trade for a Better Future ---

42 Yorizumi Watanabe, Keio University

![INDIRECT EXPROPRIATION UNDER NAFTA AND DR-CAFTA: … · 2006] INDIRECT EXPROPRIATION UNDER NAFTA AND DR-CAFTA 933 NAFTA and DR-CAFTA. Part II explains how three earlier NAFTA tribunals](https://img.dokumen.tips/doc/110x75/5ec6d30ffb2475648e7b2fba/indirect-expropriation-under-nafta-and-dr-cafta-2006-indirect-expropriation-under.jpg)