Embed Size (px)

Citation preview

Japanese Banks:Risks and Opportunities

Jonathan Cornish, Managing Director

19 September 2013

Agenda

Macro Environment

Risks and Opportunities for Japan’s Banks

www.fitchratings.com

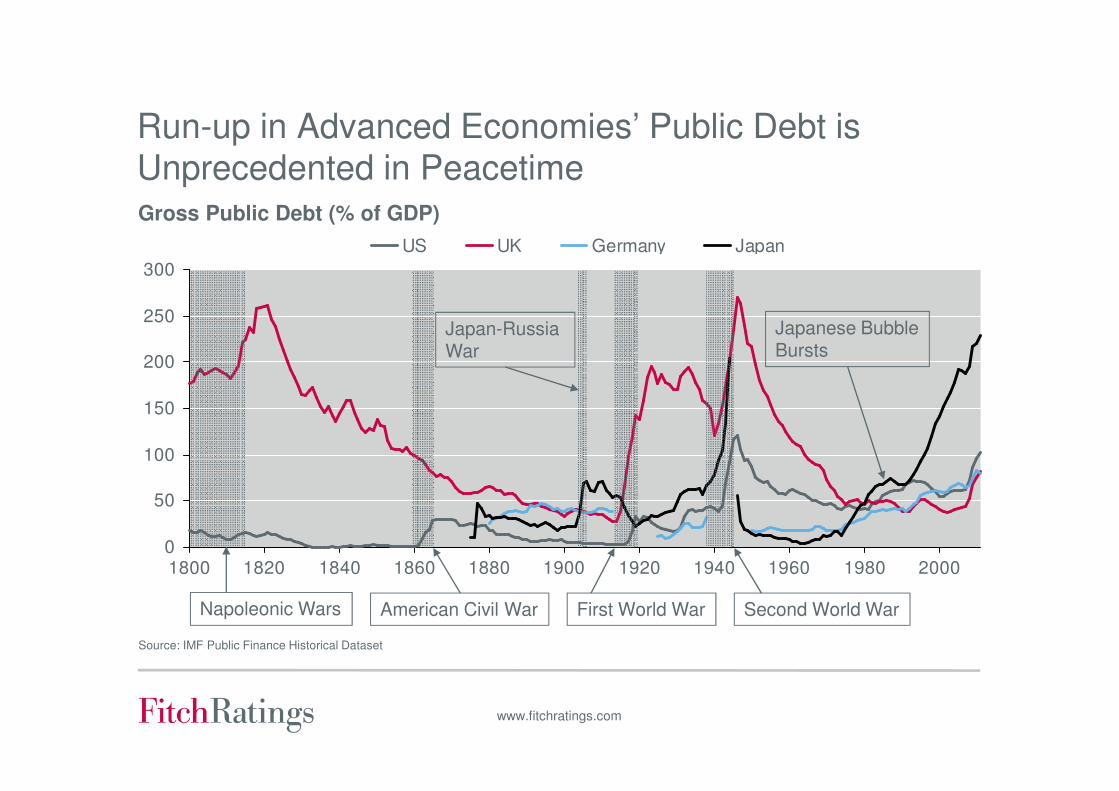

Run-up in Advanced Economies’ Public Debt is Unprecedented in PeacetimeGross Public Debt (% of GDP)

0

50

100

150

200

250

300

1800 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

US UK Germany Japan

Japan-Russia War

Japanese BubbleBursts

Source: IMF Public Finance Historical Dataset

Napoleonic Wars American Civil War First World War Second World War

www.fitchratings.com

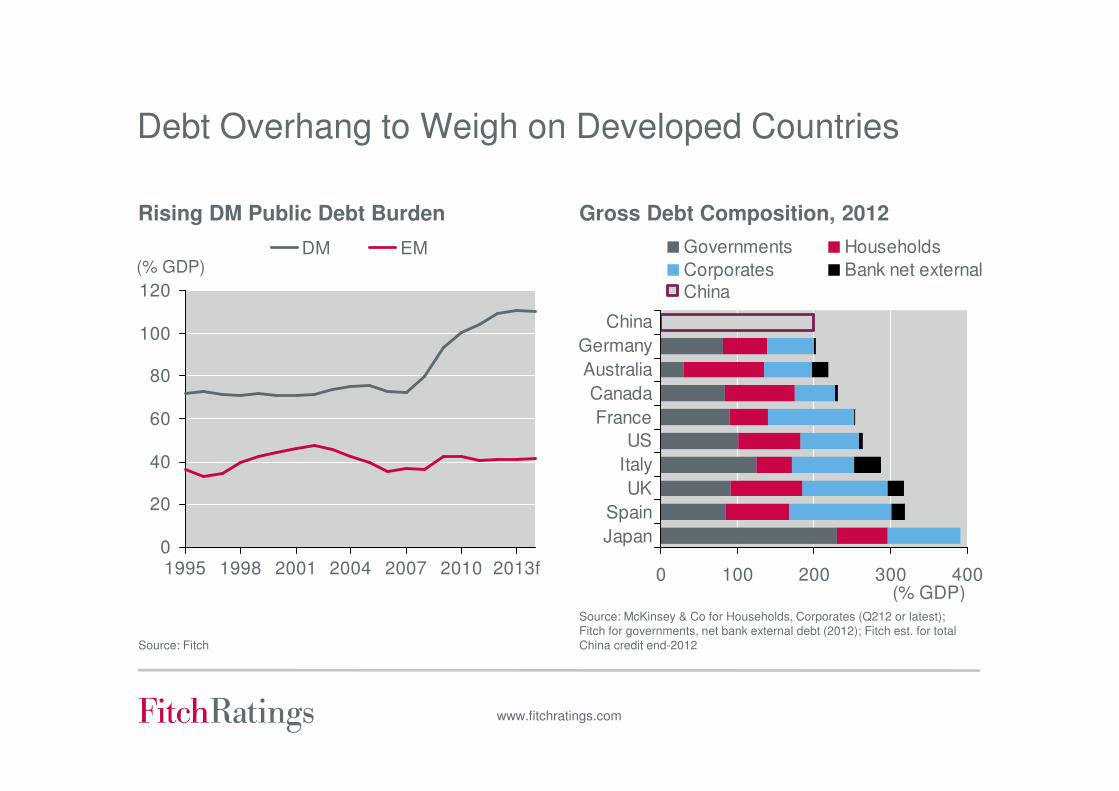

Debt Overhang to Weigh on Developed Countries

Rising DM Public Debt Burden

0

20

40

60

80

100

120

1995 1998 2001 2004 2007 2010 2013f

DM EM(% GDP)

Source: Fitch

Source: McKinsey & Co for Households, Corporates (Q212 or latest); Fitch for governments, net bank external debt (2012); Fitch est. for total China credit end-2012

0 100 200 300 400

Japan

Spain

UK

Italy

US

France

Canada

Australia

Germany

China

Governments Households

Corporates Bank net external

China

(% GDP)

Gross Debt Composition, 2012

www.fitchratings.com

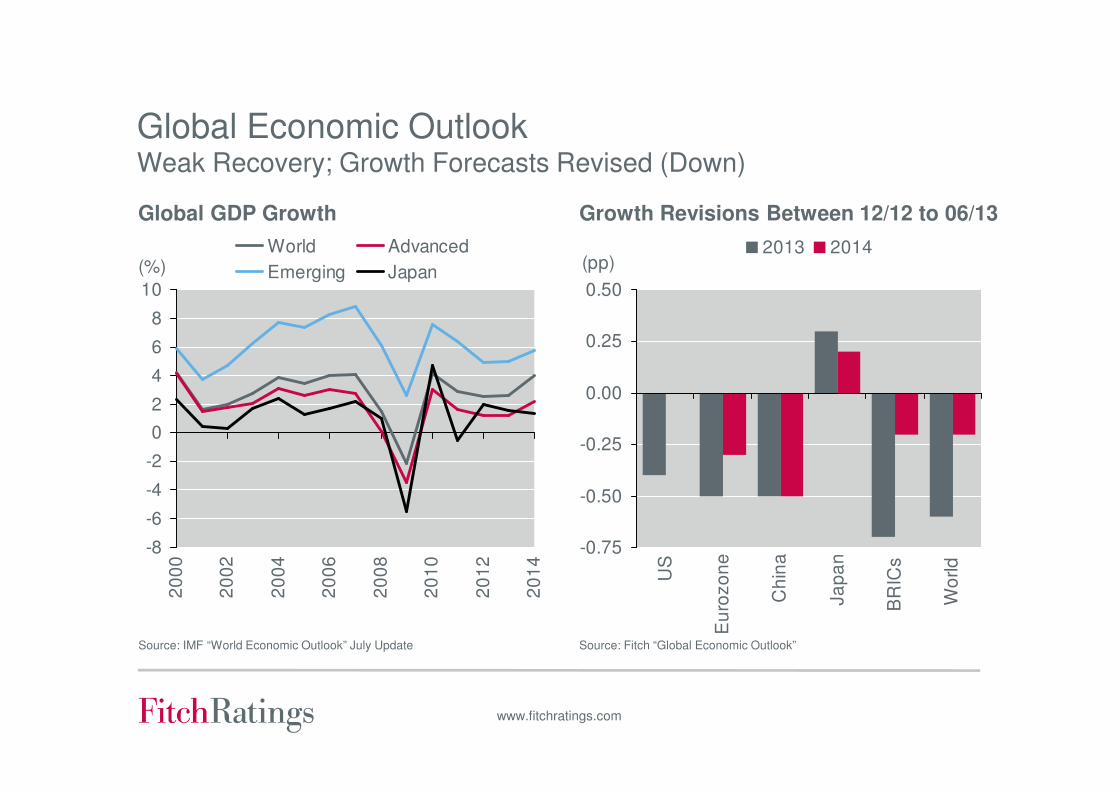

Global Economic OutlookWeak Recovery; Growth Forecasts Revised (Down)

Global GDP Growth

Source: IMF “World Economic Outlook” July Update Source: Fitch “Global Economic Outlook”

-0.75

-0.50

-0.25

0.00

0.25

0.50

US

Eu

rozo

ne

Ch

ina

Ja

pa

n

BR

ICs

Wo

rld

2013 2014(pp)

Growth Revisions Between 12/12 to 06/13

-8

-6

-4

-2

0

2

4

6

8

10

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

World Advanced

Emerging Japan(%)

www.fitchratings.com

Abenomics: Can Wages, Investment Grow Sustainably?Business Confidence

Source: CEIC, Fitch Source: CEIC, Fitch

Wages Growth

-4

-3

-2

-1

0

1

2

12/06 12/07 12/08 12/09 12/10 12/11 12/12

Nominal Real(% yoy)

-30

-20

-10

0

10

20

30

12/06 12/07 12/08 12/09 12/10 12/11 12/1225

30

35

40

45

50

55

Sentix (LHS)

Shoko Chukin (RHS)(Index) (Index)

www.fitchratings.com

Changing of Competitive Landscape

• EU/US bank deleveraging

• Political pressure to boost lending in home markets

• Many of the more “international banks” have support-driven IDRs …

• … but resolution regimes will lead to the erosion of sovereign support in the future

• Anticipate further improvement in financial profiles

- Capital now sound, but regulation driving even larger buffers

- Profit still subdued

• Selective pull-back or restraint (mostly by EU banks) from APAC markets so far …

• … but expected to expand again in APAC over the medium term

• APAC banks have been looking abroad in the region

• Expansion organically and inorganically

• Portfolio restructuring (expansion or divestment)

• Interest also in new frontier EM countries

• Varying degrees of financial capability and track record

- Less attention on Basel 3 concerns, as the region is generally already compliant (or expected to be)

www.fitchratings.com

Key Macro Prudential Risk Indicators for APAC

Country BSI Mar 07 Sep 07 Oct 08 Nov 09 Jun 10 Nov 10 Jun 11 Dec 11 Aug 12 Jan 13

Mongolia 3 3

China bb 1 1 1 1 3 3 3 3 3 3

Hong Kong a 1 1 1 1 1 3 3 3 3 3

Indonesia bb 1 1 1 1 2 2 2 3 3 3

Sri Lanka 1 1 1 1 1 1 1 3 3 3

Vietnam b 2 2 2 2 3 3 3 2 2 2

Australia aa 3 3 3 3 2 2 2 2 2 1

Korea bbb 1 3 3 3 2 2 2 1 1 1

Singapore aa 1 1 1 1 1 1 1 2 2 2

India bb 2 2 2 2 2 1 1 1 1 1

Taiwan bbb 1 1 1 1 1 1 1 1 1 1

Thailand bbb 1 1 1 1 1 1 1 1 1 1

Japan a 1 1 1 1 1 1 1 1 1 1

MPI: 3 = high vulnerability to potential systemic stress, 1 = low vulnerabilityBSI: Weighted average of Bank Viability Ratings in SystemSource: Fitch Macro-Prudential Risk Monitor

www.fitchratings.com

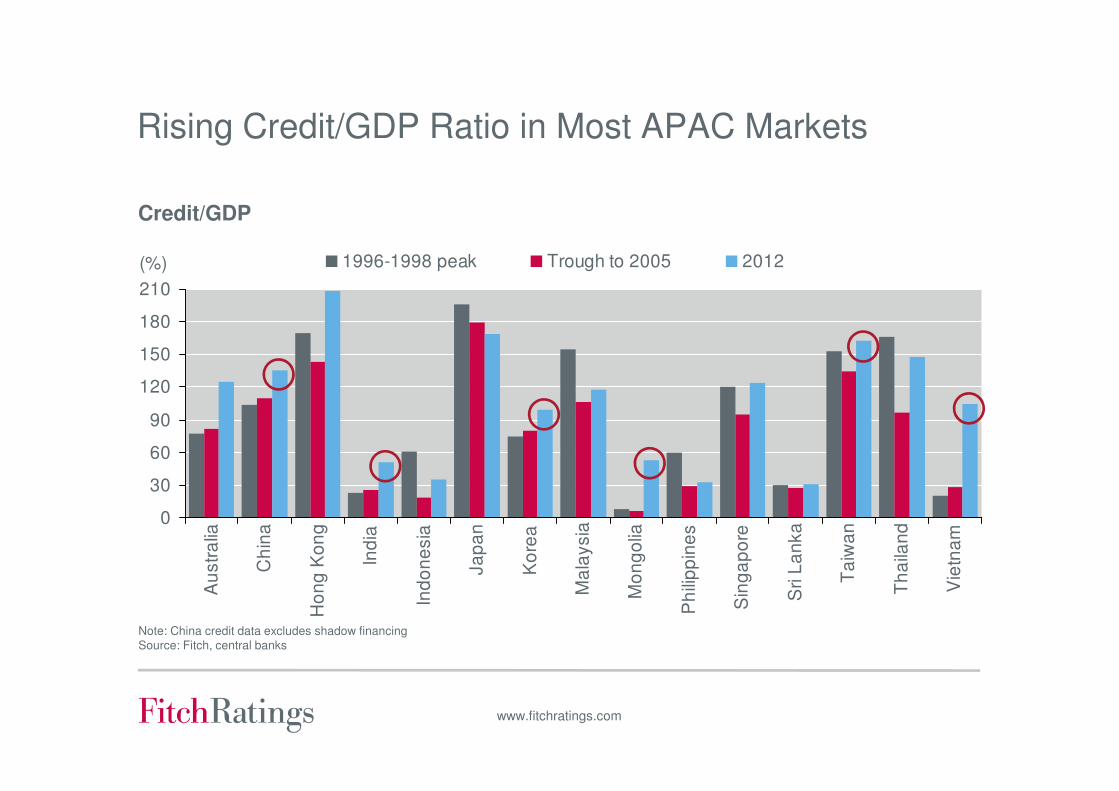

Rising Credit/GDP Ratio in Most APAC Markets

0

30

60

90

120

150

180

210

Au

str

alia

Ch

ina

Ho

ng

Ko

ng

Ind

ia

Ind

on

esia

Ja

pa

n

Ko

rea

Ma

laysia

Mo

ng

olia

Ph

ilip

pin

es

Sin

ga

po

re

Sri L

an

ka

Ta

iwa

n

Th

aila

nd

Vie

tna

m

(%) 1996-1998 peak Trough to 2005 2012

Note: China credit data excludes shadow financingSource: Fitch, central banks

Credit/GDP

Agenda

Macro Environment

Risks and Opportunities for Japan’s Banks

www.fitchratings.com

2006 2007 2008 2009 2010 2011 2012 2013

LT SRF

A-

A

A+

BBB+

2006 2007 2008 2009 2010 2011 2012 2013

LT SRF

BBB+

A-

A

A+

Japan’s Mega Banks: What’s Driving the Ratings …

• Fundamental improvements led

to VR upgrades

• Further improvements expected

(meeting future Basel 3 thresholds)

• Standalone profiles not uniform

• Mizuho’s IDR still support-driven

• Stable Outlook predicated on…

• Strong domestic franchises

• Executing stated plans to de-risk

• Pro-actively managing market risk

• Moderate offshore expansion (no

major increase in risk appetite)

BTMU: VR = a; IDR = A

SMFG: VR = a-; IDR = A-

Mizuho: VR = bbb+; IDR = A-

www.fitchratings.com

Abenomics: Major Uncertainties…

JGB Yields

Consumption & Corporate

Tax

Government Debt

Ageing Population

Direction of Indices

Inflation and Investment

Balancing the Budget

Sustainable Economic

Growth

Trading Partners

Competitive

Corporate Sector

Asset Quality

JPY

Government Support prospects

www.fitchratings.com

Japan: Trade PartnersReliance on China and Other China-Dependent Countries

0%

20%

40%

60%

80%

100%

Export Import Export Import

China HK Taiwan Korea Asia ANZ NA Europe Others

Source: JTIS

Percentage of Trade Volumes

Dec 2010 Jun 2013

www.fitchratings.com

Risk of JGB Holdings: Large Exposure Manageable

a Japan banks at March 2013, other banks at December 2012. Source: JTIS

Government Bonds/Total Assetsa Duration Control Mitigates Risk

Fitch’s Stress Test ResultsMega Banks’ Average FCC Ratio Under Stress

AFS at Cost: Exposure to Stabilise

Sep 12 (10yr

JGB = 0.765%)

FCC

average

+50bp

(1.265%)

+100bp

(1.765%)

+150bp

(2.265%)

Mega banking groups 9.3% 9.0% 8.6% 8.3%

5

10

15

20

25

Mar 08 Mar 09 Mar 10 Mar 11 Mar 12 Mar 130

10

20

30

40

City banks' current a/c with BOJ (RHS)MUFG (LHS)SMFG (LHS)Mizuho (LHS)

(% total

assets) (JPYtn)

0

1

2

3

4

Mar 09 Mar 10 Mar 11 Mar 12 Mar 13

MUFG SMFG Mizuho(Yr)

0

5

10

15

20

StC

ha

rtere

d (

aa-)

No

rdea(a

a-)

Wells

Farg

o(a

a-)

Sta

te S

tre

et(

a+

)

CA

(a)

ING

(a)

Un

iCre

dit(b

bb+

)

Gro

up

e B

PC

E(a

)

MU

FG

(a)

SG

(a-)

BB

VA

(bb

b+

)

Santa

nde

r(b

bb+

)

SM

FG

(a-)

Miz

uho

(bbb+

)

BoC

(bb

)

(%)

www.fitchratings.com

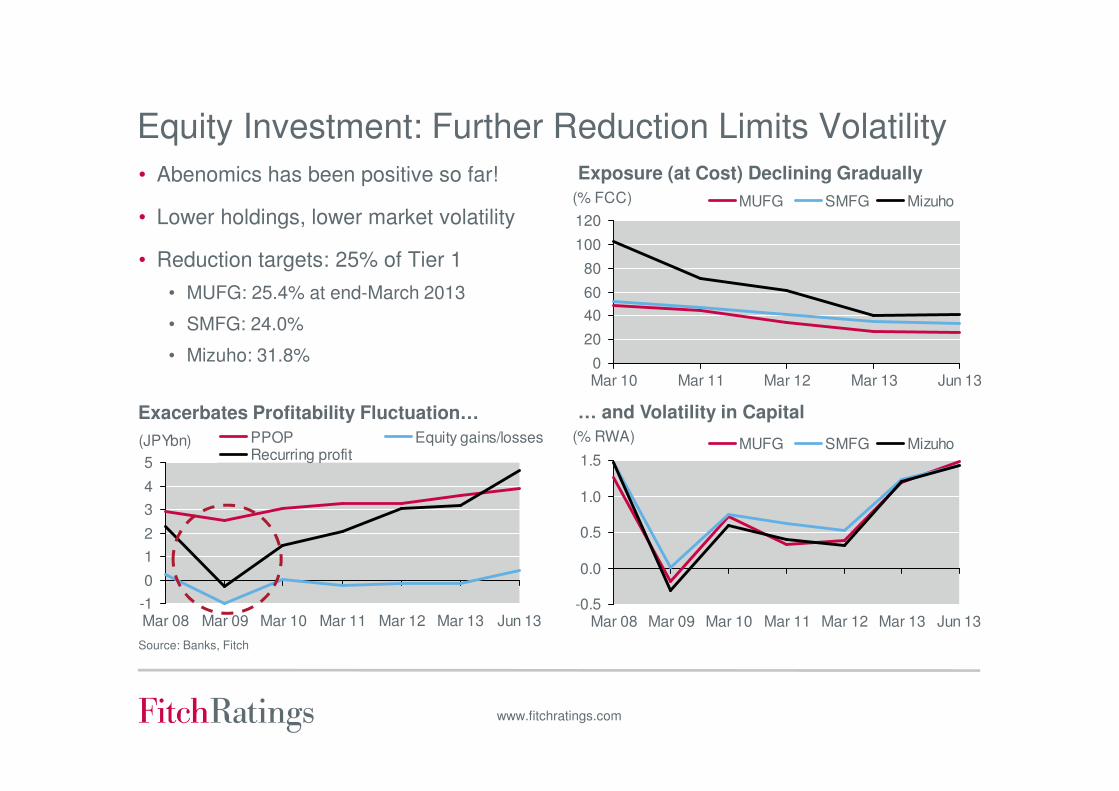

Equity Investment: Further Reduction Limits Volatility

• Abenomics has been positive so far!

• Lower holdings, lower market volatility

• Reduction targets: 25% of Tier 1

• MUFG: 25.4% at end-March 2013

• SMFG: 24.0%

• Mizuho: 31.8%

Source: Banks, Fitch

Exposure (at Cost) Declining Gradually

Exacerbates Profitability Fluctuation… … and Volatility in Capital

0

20

40

60

80

100

120

Mar 10 Mar 11 Mar 12 Mar 13 Jun 13

MUFG SMFG Mizuho(% FCC)

-1

0

1

2

3

4

5

Mar 08 Mar 09 Mar 10 Mar 11 Mar 12 Mar 13 Jun 13

PPOP Equity gains/lossesRecurring profit

(JPYbn)

-0.5

0.0

0.5

1.0

1.5

Mar 08 Mar 09 Mar 10 Mar 11 Mar 12 Mar 13 Jun 13

MUFG SMFG Mizuho(% RWA)

www.fitchratings.com

Domestic Landscape: Little Attraction for Banks

Note: Figures are each group's consolidated figures. Source: Banks, Fitch

Corporate Funds Flow Drives Loans

Risk/Return Reward Evident in NIM? Fee Income to Supplement NIR

Lending has Ticked Upwards in 2013

0.0

0.5

1.0

1.5

FYE08 FYE09 FYE10 FYE11 FYE12 FYE13

MUFG SMFG Mizuho(%)

0.7

0.8

0.9

1.0

1.1

FYE08 FYE09 FYE10 FYE11 FYE12 FYE13

MUFG SMFG Mizuho(FYE08=1)

0.8

0.9

1.0

1.1

MUFG SMFG Mizuho

FYE08 FYE09 FYE10

FYE11 FYE12 FYE13(FYE08=1)

-40

0

40

80

120

FYE03 FYE05 FYE07 FYE09 FYE11 FYE13

Change in capital Bond issuanceLT debt ST debtInternal capital generation DepreciationNet flow(JPYtn)

www.fitchratings.com

Non-APAC Bank Deleveraging = Opportunities

• Deleveraging confined

mostly to EU banks

• Pronounced in most markets,

but already tapering

• US claims growth flat to

modest

• Gaining share where foreign

claims are falling

• Growing Japanese share of

foreign claims

• Complement organic growth

with stakes in higher-growth

markets in APAC…

• …but more patient in EU

Source: BIS, Fitch

0

5

10

15

20

25

30

0

5000

10000

15000

20000

99 01 03 05 07 09 11 Q113

Foreign claim (LHS)

Developed APAC* (RHS)

Japan (RHS)

Europe (RHS)

US (RHS)(USbn)

*Australia, Korea and Taiwan

60

70

80

҂

(%)

0

10

20

30

40

50

60

0

1000

2000

3000

99 01 03 05 07 09 11 Q113

Foreign claim (LHS)

US (RHS)

Europe (RHS)

Japan (RHS)

Australia, Korea and Taiwan (RHS)(USbn)

*Australia, NZ, Korea, HK, Macau, Singapore, Taipei

(%)

0

10

20

30

40

50

60

0

300

600

900

1200

1500

1800

99 01 03 05 07 09 11 Q113

Foreign claim (LHS)

US (RHS)

Europe (RHS)

Developed APAC (RHS)**

Japan (RHS)(USbn)

*Excl. Korea & Taiwan (DMs); **Austraila, Korea & Taiwan

(%)

Share of Foreign Claims: Developed APAC*

Share of Foreign Claims: Developed Europe

Share of Foreign Claims: Emerging APAC*

Share of Foreign Claims: US

*Australia, Korea and Taiwan

0

20

40

60

80

0

2,000

4,000

6,000

8,000

Foreign claim (LHS)

Japan (RHS)

Europe (RHS)

(USbn) (%)

99 01 03 05 07 09 11 Q113

www.fitchratings.com

0

5

10

15

20

25

FYE10 FYE11 FYE12MUFG

FYE13 FYE10 FYE11 FYE12SMFGª

FYE13 FYE10 FYE11 FYE12Mizuho

FYE13

Others E. Europe W. Europe Latin America N. America Asia (ex Japan)(% total loans)

Mega Banks: Offshore Expansion

APAC: A Loan Growth Engine

Overseas Loans: Fee Income GrowthOverseas Loans: Enhancing NIM

0.0

0.5

1.0

1.5

FYE08 FYE09 FYE10 FYE11 FYE12 FYE13

MUFG (Jp) MUFG (Ovs.)SMFG (Jp) SMFG (Ovs.)Mizuho (Jp) Mizuho (Ovs.)

(%)

0.0

0.5

1.0

1.5

2.0

FYE08 FYE09 FYE10 FYE11 FYE12 FYE13

MUFG SMFG Mizuho(FYE08=1)

Note: Figures are operating banks non-consolidatedNote: Figures are each group's consolidated figuresª Sumitomo Mitsui Banking Corporation (SMBC) non-consolidated. Source: Banks, Fitch

www.fitchratings.com

0

1

2

3

4

MUFG Mizuho SMFG Global peer

ave.

5 yr ave. Latestª(%)

-0.5

0.0

0.5

1.0

1.5

BA

C

Barc

lays

BN

PP

Citi

CS

Deuts

che

GS

HS

BC

JP

Morg

an

MS

SG

UB

S

MU

FG

SM

FG

Miz

uho

Ave, LatestROA (%)

0369

1215

BA

C

Barc

lays

BN

PP

Citi

CS

Deuts

che

GS

HS

BC

JP

Morg

an

MS

SG

UB

S

MU

FG

SM

FG

Miz

uho

FCC ratio Fully-loaded B3 CET1(%)

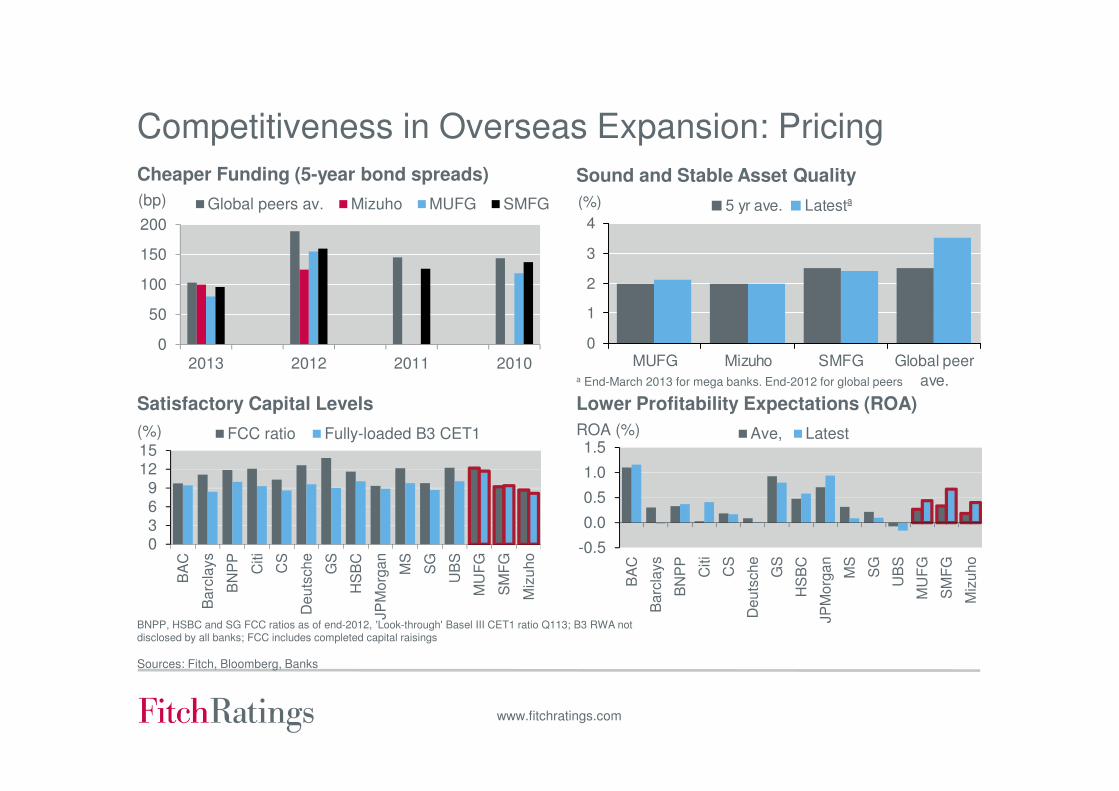

Competitiveness in Overseas Expansion: Pricing

Cheaper Funding (5-year bond spreads)

BNPP, HSBC and SG FCC ratios as of end-2012, 'Look-through' Basel III CET1 ratio Q113; B3 RWA not disclosed by all banks; FCC includes completed capital raisings

Sources: Fitch, Bloomberg, Banks

Sound and Stable Asset Quality

Satisfactory Capital Levels Lower Profitability Expectations (ROA)

0

50

100

150

200

2013 2012 2011 2010

Global peers av. Mizuho MUFG SMFG(bp)

a End-March 2013 for mega banks. End-2012 for global peers

www.fitchratings.com

Offshore Expansion: Non-Organic Growth

Date Name Country Stake acquired (%)

MUFG Jun 2008 Dah Sing Financial Holdings Limited Hong Kong 15.0

Oct 2008 Morgan stanley US 21.8

Oct 2008 Aberdeen Asset Management UK 18.8

Nov 2008 UnionBanCal Corporation US 100.0

Apr 2010 Tamalpais Bank US 100.0

Apr 2010 Frontier Bank US 100.0

Nov 2010 The Royal Bank of Scotland UK n.a.

Apr 2011 SWS MU Fund Management Co.,Ltd. China 33.3

Dec 2012 Vietnam Joint Stock Commercial Bank for Industry and Trade (VietinBank) Vietnam 20.0

Apr 2013 PB Capital Corporation (sub. of Deutsche Bank; U.S. commercial property loans) US n.a.

Jul 2013 Bank of Ayudhya Thailand max 75%

SMFG Jul 2008 Barclays PLC UK 1.4

Dec 2008 KB Financial Group Korea 1.1

Jan 2010 The Bank of East Asia Ltd. Hong Kong 9.5

Jun 2010 Kotak Mahindra Bank Ltd India 4.5

Jan 2012 Moelis & Company US n.a.

Jan 2012 The Royal Bank of Scotland (aircraft leasing assets) UK n.a.

Mar 2012 PT Indonesia Infrastructure Finance Indonesia 14.9

Apr 2012 China Post & Capital Fund Management Co.,Ltd China 24.0

May 2013 BTPN Indonesia 24.26 (max 40%)

Mizuho Jan 2008 Merrill Lynch & Co., Inc ( converted to a stake in Bank of America) US n.a.

Aug 2008 Evercore Partners Inc US 14.7

Nov 2010 BlackRock, Inc. US n.a.

Aug 2011 PT Imora Motor/PT Balimor Finance Indonesia 51.0

Sep 2011 Vietcombank Vietnam 15.0

Jun 2012 West LB Brasil Brazil 100.0

www.fitchratings.com

Japanese Banks: Challenges of Expansion

• Credit and operating risks

• Limited track record in target markets

• Limited funding ability (i.e. wholesale versus retail)

• FX

• Control and governance

• Management resources

• More aggressive expansion increases burden on management

• Shareholder expectations – compromise prudence in return for growth

• Increasing complexity

• Compliance/reporting costs (regulatory frameworks differ across countries)

• Cultural differences

• Basel 3

• Full deductions for large minority stakes

• What if impairments coincide with future target minimum capital thresholds?

www.fitchratings.com

Disclaimer

Fitch Ratings’ credit ratings rely on factual information received from issuers and other sources.

Fitch Ratings cannot ensure that all such information will be accurate and complete. Further, ratings

are inherently forward-looking, embody assumptions and predictions that by their nature cannot be

verified as facts, and can be affected by future events or conditions that were not anticipated at the

time a rating was issued or affirmed.

The information in this presentation is provided “as is” without any representation or warranty.

A Fitch Ratings credit rating is an opinion as to the creditworthiness of a security and does not

address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned.

A Fitch Ratings report is not a substitute for information provided to investors by the issuer and its

agents in connection with a sale of securities.

Ratings may be changed or withdrawn at any time for any reason in the sole discretion of

Fitch Ratings. The agency does not provide investment advice of any sort. Ratings are not

a recommendation to buy, sell, or hold any security.

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE

LIMITATIONS AND DISCLAIMERS AND THE TERMS OF USE OF SUCH RATINGS AT WWW.FITCHRATINGS.COM.

New York One State Street Plaza New York, NY 10004

London 30 North Colonnade Canary WharfLondon E14 5GN