Embed Size (px)

Citation preview

SPAIN

January - December 2017

31 January 2018

22

DisclaimerBanco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of

1995. Forward-looking statements may be identified by words such as “expect”, “project”, “anticipate”, “should”, “intend”, “probability”, “risk”, “VaR”, “RORAC”, “RoRWA”, “TNAV”, “target”, “goal”, “objective”,

“estimate”, “future” and similar expressions. These forward-looking statements are found in various places throughout this presentation and include, without limitation, statements concerning our future business

development and economic performance and our shareholder remuneration policy. While these forward-looking statements represent our judgment and future expectations concerning the development of our

business, a number of risks, uncertainties and other important factors could cause actual developments and results to differ materially from our expectations. These factors include, but are not limited to: (1)

general market, macro-economic, industry, governmental and regulatory trends; (2) movements in local and international securities markets, currency exchange rates and interest rates; (3) competitive

pressures; (4) technological developments; and (5) changes in the financial position or credit worthiness of our customers, obligors and counterparties. Numerous factors, including those reflected in the Annual

Report on Form 20-F filed with the Securities and Exchange Commission of the United States of America (the “SEC”) –under “Key Information-Risk Factors”- and in the Documento de Registro de Acciones

filed with the Spanish Securities Market Commission (the “CNMV”) –under “Factores de Riesgo”- could affect the future results of Santander and could result in other results deviating materially from those

anticipated in the forward-looking statements. Other unknown or unpredictable factors could cause actual results to differ materially from those in the forward-looking statements.

Forward-looking statements speak only as of the date of this presentation and are based on the knowledge, information available and views taken on such date; such knowledge, information and views may

change at any time. Santander does not undertake any obligation to update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

The information contained in this presentation is subject to, and must be read in conjunction with, all other publicly available information, including, where relevant any fuller disclosure document published by

Santander. Any person at any time acquiring securities must do so only on the basis of such person's own judgment as to the merits or the suitability of the securities for its purpose and only on such information

as is contained in such public information having taken all such professional or other advice as it considers necessary or appropriate in the circumstances and not in reliance on the information contained in the

presentation. No investment activity should be undertaken on the basis of the information contained in this presentation. In making this presentation available, Santander gives no advice and makes no

recommendation to buy, sell or otherwise deal in shares in Santander or in any other securities or investments whatsoever.

Neither this presentation nor any of the information contained therein constitutes an offer to sell or the solicitation of an offer to buy any securities. No offering of securities shall be made in the United States

except pursuant to registration under the U.S. Securities Act of 1933, as amended, or an exemption therefrom. Nothing contained in this presentation is intended to constitute an invitation or inducement to

engage in investment activity for the purposes of the prohibition on financial promotion in the U.K. Financial Services and Markets Act 2000.

Note: Statements as to historical performance or financial accretion are not intended to mean that future performance, share price or future earnings (including earnings per share) for any period will necessarily

match or exceed those of any prior year. Nothing in this presentation should be construed as a profit forecast.

The businesses included in each of our geographic segments and the accounting principles under which their results are presented here may differ from the included businesses and local applicable accounting

principles of our public subsidiaries in such geographies. Accordingly, the results of operations and trends shown for our geographic segments may differ materially from those of such subsidiaries.

In addition to the financial information prepared under International Financial Reporting Standards (“IFRS”), this presentation includes certain alternative performance measures as defined in the Guidelines on

Alternative Performance Measures issued by the European Securities and Markets Authority on 5 October 2015 (ESMA/2015/1415es) as well as Non-IFRS measures. The APMs and Non-IFRS Measures are

performance measures that have been calculated using the financial information from the Santander Group but that are not defined or detailed in the applicable financial information framework and therefore

have neither been audited nor are capable of being completely audited. These APMs and Non-IFRS Measures are been used to allow for a better understanding of the financial performance of the Santander

Group but should be considered only as additional information and in no case as a replacement of the financial information prepared under IFRS. Moreover, the way the Santander Group defines and calculates

these APMs and Non-IFRS Measures may differ to the way these are calculated by other companies that use similar measures, and therefore they may not be comparable. Please refer to the quarterly financial

Report for further details of the APMs and Non-IFRS Measures used, including its definition or a reconciliation between any applicable management indicators and the financial data presented in the

consolidated financial statements prepared under IFR, see Section 26 of the Documento de Registro de Acciones for Banco Santander filed with the CNMV on July 4, 2017 (available on the Web page of the

CNMV -www.cnmv.es- and at Banco Santander -www.santander.com) and Item 3A of the Annual Report on Form 20-F for the year ended December 31, 2016, filed with the U.S. Securities and Exchange

Commission on March 31, 2017 (the “Form 20-F”). For a discussion of the accounting principles used in translation of foreign currency-denominated assets and liabilities to euros, see note 2(a) to our

consolidated financial statements on Form 20-F and to our consolidated financial statements available on the CNMV’s website (www.cnmv.es) and on Banco Santander’s website (www.santander.com).

Content

Macroeconomic environment

and financial system

Strategy and business

Results

Appendix

Note: All figures excluding Popular

44

Macroeconomic environment

3.4 3.3 3.1 2.7 2.4

2015 2016 2017 (e) 2018 (e) 2019 (e)

Annual GDP Growth (%, real)

Unemployment rate (%)Inflation (annual change, %)

Interest rate (official rate, %)

0.05 0.00 0.00 0.00

0.50

2015 2016 2017 2018 (e) 2019 (e)

-0.5-0.2

2.01.7 1.7

2015 2016 2017 2018 (e) 2019 (e)

22.119.6

17.215.2 13.9

2015 2016 2017 2018 (e) 2019 (e)

The expansionary cycle in the Spanish economy is expected to continue in the coming years, with

interest rates rises not anticipated before 2019…

Source: Santander Research Department

55

Macroeconomic environment

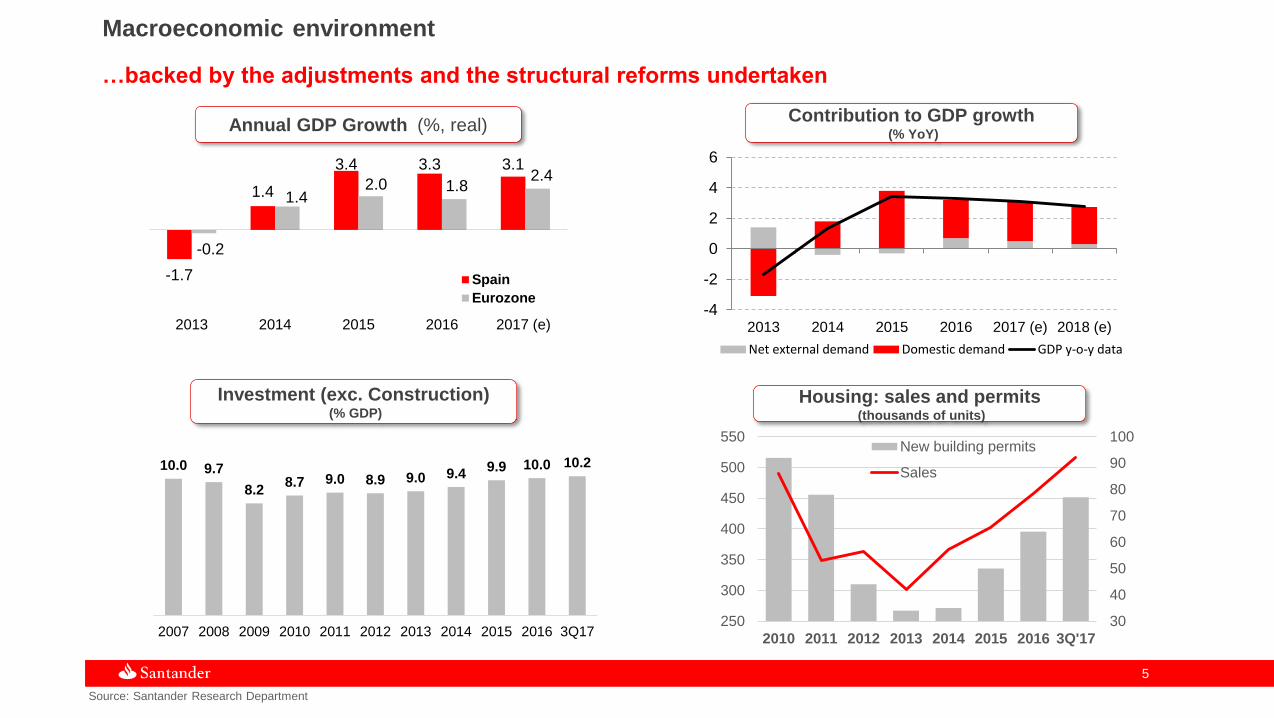

…backed by the adjustments and the structural reforms undertaken

Source: Santander Research Department

Annual GDP Growth (%, real)

-1.7

1.4

3.4 3.3 3.1

-0.2

1.42.0 1.8

2.4

2013 2014 2015 2016 2017 (e)

Spain

Eurozone

Contribution to GDP growth(% YoY)

-4

-2

0

2

4

6

2013 2014 2015 2016 2017 (e) 2018 (e)

Net external demand Domestic demand GDP y-o-y data

Investment (exc. Construction)(% GDP)

10.0 9.7

8.28.7 9.0 8.9 9.0 9.4

9.9 10.0 10.2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 3Q17

Housing: sales and permits(thousands of units)

30

40

50

60

70

80

90

100

250

300

350

400

450

500

550

2010 2011 2012 2013 2014 2015 2016 3Q'17

New building permits

Sales

66

Source: ECB and Bank of Spain. Other Monetary Financial Institutions.

Total banking system volumes

Loans to customers Savings

Loans to Households & Non Financial entities are decreasing at a slower pace than 2016

In savings, the flow from deposits to mutual funds continues

958 989 999

414 380 318

77 54 7088 94 80

1,537 1,517 1,467

Dec'15 Dec'16 Nov'17

Mutual

Funds 220 235 261

Public sector

in Spain

Non-monetary financial

institutions EMU

Other non-resident

sectors in Spain

Households & non-financial

entities in Spain

EUR billion EUR billionYTD

-1.1%

-1.3%

YTD

+10.7%

-3.3%

+1.0%

1,232 1,196 1,181

5561 64

90 88 79

78 65 70

1,4551,410

1,394

Dec'15 Dec'16 Nov'17

Content

Macroeconomic environment

and financial system

Strategy and business

Results

Appendix

88

Our Franchise

The financial group includes retail networks, global businesses and specialised entities

(1) Million euros; (2) Underlying ROTE; (3) Other non-resident sector in Spain as of Nov 2017 (lastest available) excluding Popular. Including Popular: Market share Loans 18.3% and Deposits 18.9%.(4) Millions.

KEY DATA 2017 Var. YoY2017 STRATEGIC PRIORITIES

Predictable, sustainable and profitable growth

Bank of choice for SMEs and corporates

Improve efficiency and customer experience

Best bank to work for

Gross loans1 148,585

Customer funds1 251,196

Attributable profit1 1,180

ROTE2 10.11% +122 bp

Efficiency ratio 57.2% -154 bp

Loans’ market share3 12.9 +20 bp

Deposits’ market share3 14.1 +136 bp

Loyal customers4 1.9

Digital customers4 3.2

Branches 2,843

Employees 22,916

+42%

+15%

-2%

-0%

-2%

+12%

+46%

99

Digital eco-system renewalCredit Cards

Commercial strategy and business transformation

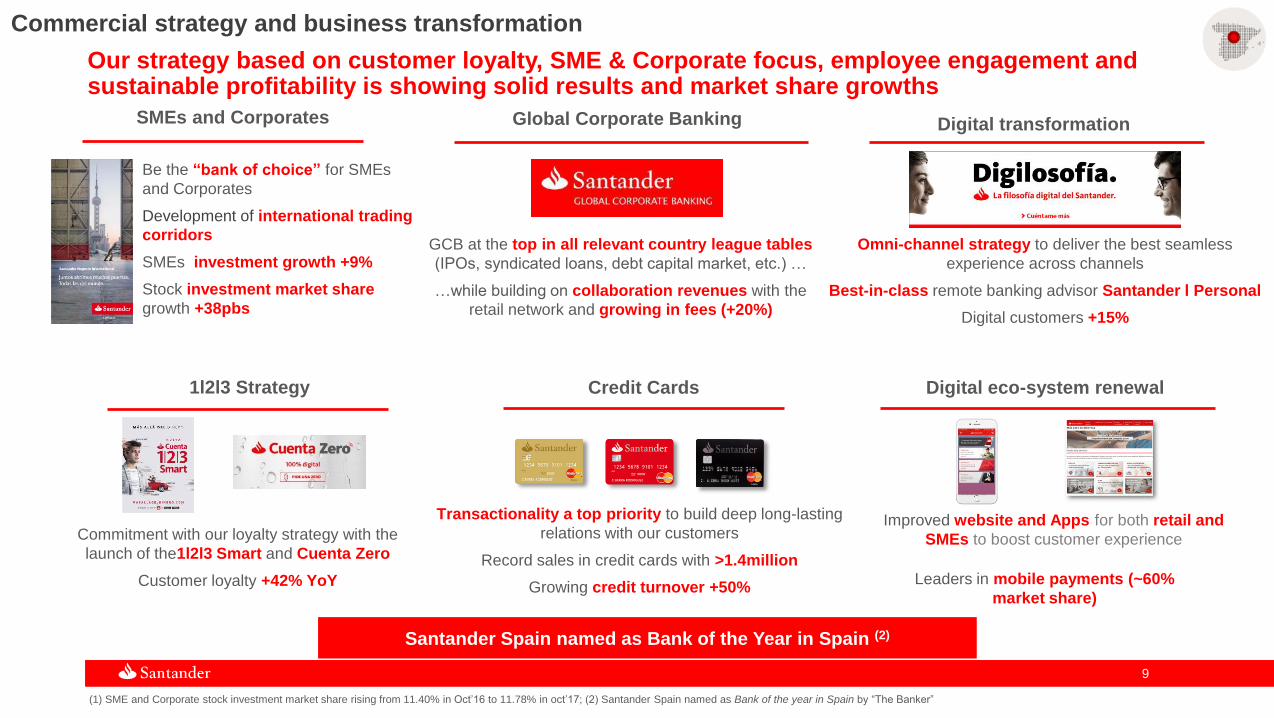

Our strategy based on customer loyalty, SME & Corporate focus, employee engagement and sustainable profitability is showing solid results and market share growths

1l2l3 Strategy

Global Corporate BankingSMEs and Corporates

Commitment with our loyalty strategy with the

launch of the1l2l3 Smart and Cuenta Zero

Customer loyalty +42% YoY

Improved website and Apps for both retail and

SMEs to boost customer experience

Be the “bank of choice” for SMEs

and Corporates

Development of international trading

corridors

SMEs investment growth +9%

Stock investment market share

growth +38pbs

GCB at the top in all relevant country league tables

(IPOs, syndicated loans, debt capital market, etc.) …

…while building on collaboration revenues with the

retail network and growing in fees (+20%)

Digital transformation

Omni-channel strategy to deliver the best seamless

experience across channels

Best-in-class remote banking advisor Santander l Personal

Digital customers +15%

Santander Spain named as Bank of the Year in Spain (2)

Transactionality a top priority to build deep long-lasting

relations with our customers

Record sales in credit cards with >1.4million

Growing credit turnover +50%Leaders in mobile payments (~60%

market share)

(1) SME and Corporate stock investment market share rising from 11.40% in Oct’16 to 11.78% in oct’17; (2) Santander Spain named as Bank of the year in Spain by “The Banker”

1010

322 341

1,013

Customers

+6%

+54%

Loyal individuals (k)

Loyal companies (k)

Digital customers (k)

Customer centric approach: loyalty and digital transformation are key levers to improve results

and satisfaction.

1,559

Dec’16 Dec`17

Dec’16 Dec’17

2,736 3,158

Dec’16 Dec’17

+15%

• Our commercial strategy is improving customer loyalty and increasing our transactionality

(mobile payments, cards usage…) leading to increases in commercial activity (+3,5 pp in new

mortgage production1)

• Corporate strategy: being the “Bank of choice” for SMEs and Corporates

• Growing in high value-added products: capturing the potential of our international footprint

(+16% in International business production) and growing in collaboration revenues 24%

• Focused on digital transformation, from internal processes to a customer omni-channel

experience, leveraging in our digital philosophy Digilosofía

• Leaders in mobile payments(>60% market share) and best-in-class remote banking advisor

(1) New production mortgage market share rising from 8.0% in Nov’16 to 11.5% in Nov’17

1111

(1) Excluding repos

Total loans

Total gross loans (€Bn1)

151 151 152 149 149

Dec 16 Mar 17 Jun 17 Sep 17 Dec 17

Growth in new lending activity is not reflected in gross loans stock due to drop in Institutions and GCB

Dec 17 Dec 16 Sep 17

Institutions 12 -10.4 -3.5

Individual customers 54 +0.3 +0.1of which:

- Housing mortgages 46 -0.4 -0.2

Companies 52 +1.2 +1.6

Corporate 31 -5.4 -2.3

Gross loans (w/o repos) 149 -1.6 -0.20

Repos 9 +37.8 +1.3

Provisions (4) -18.4 -3.50

Net loans 154 +0.5 -0.0

% var. /

1212

Total customer funds

Total customer funds (€Bn)

Focus on growing through demand deposits and mutual funds

175 177 185 185 193

49 5254 55

5812 12

12 12 11 236 241 251 252 263

Dec 16 Mar 17 Jun 17 Sep 17 Dec 17

Demand +

Time deposit

Repos & other

Mutual funds

Pension funds

% var. /

Dec 17 Dec 16 Sep 17

Demand deposits 154 +19.0 +5.0Time deposits 39 -15.8 +1.5

Deposits w/o Repos 193 +9.9 +4.2

Mutual funds 58 +18.4 +5.7

Customer funds 251 +11.7 +4.6

Pension funds 11 +2.0 +1.5Repos 1 -34.2 -42.2

Total customer funds 263 +11.1 +4.2

Content

Macroeconomic environment

and financial system

Strategy and business

Results

Appendix

1414

Net interest income. Yield and costs

YoY NII evolution affected by mortgage repricing in a competitive and low interest rates environment

QoQ impacted by higher average volumes in customer deposits. Lower contribution from ALCO and GCB

Cost of deposits (%)

Yield on loans (%)Net Interest Income (€MM)

0.47 0.46 0.46 0.46 0.48

4Q'16 1Q'17 2Q 3Q 4Q

747 747 749 726 686

4Q'16 1Q'17 2Q 3Q 4Q

2.10 2.04 2.04 1.96 1.96

(1) Net interest income annualised / Total assets average period (2) Quarter average.

NIM1

(%)

0.93 0.95 0.92 0.86 0.79

Official interest rate2

(%)

0.00 0.00 0.00 0.00 0.00

1515

Net fee income

Positive evolution of fee income YoY (+16%), backed by a strong rise in fees related to means of

payment, mutual funds and GCB activity

In the quarter, 10% increase mainly due to transactional services

Net fee income (€MM)

451 459

537509

562

4Q'16 1Q'17 2Q 3Q 4Q

2017 2016 YoY QoQ

Fees from services 935 893 +4.7 +8.7

Mutual and pension

funds 476 455 +4.6 -0.8

Insurance 212 229 -7.6 +16.5

Other 445 204 +118.6 +23.3

Total fee income 2,067 1,781 +16.1 +10.3

% var

1616

EUR million

2017 2016 YoY QoQ

Net interest income 2,909 3,077 -5.5 -5.5

Net fees 2,067 1,781 +16.1 +10.3

Subtotal 4,976 4,858 +2.4 +1.0

Other 718 750 -4.3 -39.8

Total 5,694 5,608 +1.5 -4.7

% var

Gross income

Good performance in fee income offset the lower NII

Positive impact QoQ from dividends received in GCB activity and negative effect for the

DGF charge (€153 MM)

Gross income (€MM)

1,324

1,539

1,3511,435

1,368

4Q'16 1Q'17 2Q 3Q 4Q

(1).- Other includes Gains (losses) on financial transactions and Other Operating income

1

1717

(1) Calculation of efficiency ratio includes amortisations

Operating expenses

Lower costs YoY reflected the efficiency plan announced in 2016

QoQ increased due to costs related to Openbank, Elavon integration and IT depreciations

Operating expenses (€MM)

802 798 806 815 841

4Q'16 1Q'17 2Q 3Q 4Q

EUR million

2017 2016 YoY QoQ

General expenses 3,080 3,156 -2.4 +2.7

- Personnel 1,597 1,632 -2.1 -0.7

- Other 1,482 1,524 -2.7 +6.4

Amortisations 180 140 +28.1 +11.3

Total 3,259 3,297 -1.1 +3.2

Efficiency ratio (%) 57.2 58.8

Branches 2,843 2,911

Employees 22,916 23,017

% var

1

1818

LLPs and Cost of credit (€MM; %)

85

163137

104 110

4Q'16 1Q'17 2Q 3Q 4Q

Cost of credit1

Loan-Loss provisions

Net operating income after loan-loss provisions (LLPs)

Sharp fall in LLPs and further improvement in NPLs and cost of credit YoY

0.37 0.33 0.33 0.31 0.33

EUR million

2017 2016 YoY QoQ

Net operating income 2,434 2,311 +5.3 -15.0

Loan-loss provisions 513 585 -12.3 +5.8

Net operat. income

after provisions 1,921 1,726 +11.3 -19.2

Coverage ratio (%) 45.9 48.3

NPL ratio (%) 4.72 5.41

% var

(1) Cost of credit: Provisions to cover losses due to impairment of loans in the last 12 months / average customer loans and advances of the last 12 months

1919

Attributable profit

Profit backed by fee income (more than offsetting pressure on NII), cost control and LLPs

Attributable profit (€MM)

237

362

241

311265

4Q'16 1Q'17 2Q 3Q 4Q

EUR million

2017 2016 YoY QoQ

Underlying PBT 1,714 1,459 +17.5 -14.3

Tax on profit 518 416 +24.4 -12.0

Consolidated profit 1,197 1,043 +14.7 -15.4

Minority interests 17 21 -18.2 -57.4

Underlying att. profit 1,180 1,022 +15.4 -14.8

Non-recurring1 — (216) — —

Attributable profit 1,180 806 +46.4 -14.8

Effective tax rate (%) 30.2% 28.5%

% var

(1).- In 2Q’16 capital gains from the disposal of the stake in VISA Europe, and restructuring costs

2020

Final remarks

The expansionary cycle in the Spanish economy is expected to continue in the coming years.

GDP growth is backed by the adjustments and the structural reforms undertaken.

Economic environment and financial system

Santander:

Strategy and activity

Santander:

Results

Become the best retail and commercial bank in Spain by improving our value proposition and

transforming the way we do business.

Continue growing our 1l2l3 strategy to improve customer loyalty and to gain market share. Developed the

new Digital philosophy to enhance digital capabilities and boost efficiency and profitability.

New lending increased in main retail products and segments, especially in mortgages.

Demand deposits and mutual funds continued to grow.

Positive evolution in net fees YoY offset the pressure on margins (NII + Net Fees: +2.4%) and lower

results in Gains (losses) on financial transactions.

Cost to income improvement underscoring the positive trend in costs.

Decrease in provisions backed by credit quality improvement.

Content

Macroeconomic environment

and financial system

Strategy and business

Results

Appendix

Note: the following slides provide data on the Spain unit, which includes the retail network of Santander, Global Corporate Banking,

and the ALCO portfolio in Spain.

Not included: Santander Consumer Finance unit in Spain nor Spain's Real Estate activity, as described in Santander Group's quarterly

Financial Report (see Description of Segments in Information by principal segments chapter). All figures excluding Popular

2222

Balance sheet

EUR million Change

Dec 17 Dec 16 Amount %

Customer loans 153,632 152,850 782 0.5

Cash, central banks and credit institutions 89,585 54,207 35,378 65.3

Debt securities 61,836 58,084 3,752 6.5

o/w: available for sale 42,780 38,727 4,054 10.5

Other financial assets 35,391 37,741 (2,350) (6.2)

Other assets 10,354 9,473 881 9.3

Total assets 350,798 312,354 38,444 12.3

Customer deposits 193,639 176,779 16,860 9.5

Central banks and credit institutions 79,146 52,071 27,075 52.0

Other financial liabilities 41,168 46,951 (5,784) (12.3)

Other liabilities 7,883 4,186 3,697 88.3

Total liabilities 338,549 300,850 37,699 12.5

Total equity 12,249 11,504 744 6.5

Other managed and marketed customer funds 77,221 66,649 10,572 15.9

Mutual funds 58,438 49,357 9,080 18.4

Pension funds 10,563 10,359 203 2.0

Managed portfolios 8,221 6,932 1,288 18.6

2323

Income Statement

EUR million Change

2017 2016 Amount %

Net interest income 2,909 3,077 (169) (5.5)

Net fees 2,067 1,781 287 16.1

Gains (losses) on financial transactions 429 595 (167) (28.0)

Other operating income 289 155 135 87.0

Gross income 5,694 5,608 86 1.5

Operating expenses (3,259) (3,297) 37 (1.1)

General administrative expenses (3,080) (3,156) 77 (2.4)

Personnel (1,597) (1,632) 35 (2.1)

Other general administrative expenses (1,482) (1,524) 42 (2.7)

Depreciation and amortisation (180) (140) (39) 28.1

Net operating income 2,434 2,311 123 5.3

Net loan-loss provisions (513) (585) 72 (12.3)

Other income (207) (267) 60 (22.6)

Underlying profit before taxes 1,714 1,459 255 17.5

Tax on profit (518) (416) (102) 24.4

Underlying profit from continuing operations 1,197 1,043 153 14.7

Net profit from discontinued operations — — — —

Underlying consolidated profit 1,197 1,043 153 14.7

Minority interests 17 21 (4) (18.2)

Underlying attributable profit to the Group 1,180 1,022 157 15.4

Net capital gains and provisions — (216) 216 (100.0)

Attributable profit to the Group 1,180 806 374 46.4

*

*Including capital gains from the sale of VISA Europe and restructuring costs

2424

*Including capital gains from the sale of VISA Europe and restructuring costs

EUR million

1Q 16 2Q 16 3Q 16 4Q 16 1Q 17 2Q 17 3Q 17 4Q 17

Net interest income 819 783 728 747 747 749 726 686

Net fees 424 449 456 451 459 537 509 562

Gains (losses) on financial transactions 224 65 149 157 230 (42) 119 121

Other operating income 75 46 64 (30) 103 106 81 (0)

Gross income 1,543 1,343 1,398 1,324 1,539 1,351 1,435 1,368

Operating expenses (837) (834) (824) (802) (798) (806) (815) (841)

General administrative expenses (801) (799) (791) (766) (752) (765) (771) (792)

Personnel (415) (410) (401) (408) (399) (399) (401) (398)

Other general administrative expenses (386) (389) (390) (358) (352) (365) (370) (394)

Depreciation and amortisation (36) (35) (33) (36) (46) (41) (44) (49)

Net operating income 706 509 574 522 741 545 621 528

Net loan-loss provisions (231) (129) (140) (85) (163) (137) (104) (110)

Other income (37) (82) (51) (97) (64) (64) (55) (23)

Underlying profit before taxes 438 298 382 340 514 344 461 395

Tax on profit (126) (85) (108) (97) (146) (98) (145) (128)

Underlying profit from continuing operations 312 213 274 243 367 246 316 267

Net profit from discontinued operations — — — — — — — —

Underlying consolidated profit 312 213 274 243 367 246 316 267

Minority interests 5 5 5 6 6 5 5 2

Underlying attributable profit to the Group 307 208 270 237 362 241 311 265

Net capital gains and provisions* — (216) — — — — — —

Attributable profit to the Group 307 (8) 270 237 362 241 311 265

Quarterly Income Statement

Thank you

Our purpose is to help people and

businesses prosper.

Our culture is based on the belief that

everything we do should be