Embed Size (px)

Citation preview

Belpex clearing & settlementJanuary 2008

Albert VreemanBusiness Development Manager

Background

Recognition:Recognition:– Belpex introduces new market segments: continuous day-

ahead and intra-day– Efficient solution required.– Continuous day-ahead market introduces new type of risk,

requiring “margining” to be applied.– Traditional “close-out” mechanism not supported: “close-out

issue”– Continuous intra-day market requires changes to the invoicing

cycle (scope).– Modification of ARP contract removes “delivery risk” Belpex is

exposed to.

Close-out issue

Restricted to buying Participants not meeting requirementsRestricted to buying Participants not meeting requirementsTypical closeTypical close--out mechanism assumes CCP to take title to out mechanism assumes CCP to take title to delivery obligations:delivery obligations:– CCP to “own” the electricity– CCP to offset defaulter’s physical position in the market place i.e. find

a “replacement buyer”– CCP to incur damages as a result of market prices having moved away

from original contract price– CCP to recover damages (in whole or in part) from margins deposited

by defaulter.Issues:Issues:– In respect of the Belpex market, APX does not take title to deliveries; it

only receives financial obligations, whereas delivery obligations reside with Participants and Belpex.

– When taking title to delivery obligations, APX would require a supplier license under Belgian law, for which APX (or a party similar to it) does not qualify.

Close-out mechanism in PA CSS

Each Participant mandates APX to:Each Participant mandates APX to:– offset its physical position in the market place, if it were to default.– to recover damages (in whole or in part) from margins and any other

collateral deposited by it, if it were to default.APX:APX:– Warrants to selling Participants, that they will receive the original

contract price (APX takes losses in case of only partial recovery of damages = consistent with prevailing clearing capital structure)

Title to the contract remains with the original buyerTitle to the contract remains with the original buyerCloseClose--out on behalf of defaulting buyerout on behalf of defaulting buyerCloseClose--out for risk and account of defaulting buyerout for risk and account of defaulting buyerSeller guaranteed to receive original contract price, APX to Seller guaranteed to receive original contract price, APX to compensate for losses if collateral was insufficient compensate for losses if collateral was insufficient

ARP contract amendment

Removes Removes BelpexBelpex’’ss exposure to exposure to ““delivery riskdelivery risk”” in respect in respect of selling Participantsof selling Participants– ARP Perimeter Fee mechanism no longer required– Reduces Variation Collateral requirement for net selling

Participants

Changes to PA CSS

Belpex Day Ahead Market renamed to Belpex Spot MarketBelpex Day Ahead Market renamed to Belpex Spot Market– Three market segments: DAM, CoDAM and CIM.– Definitions updated accordingly.

Initial and Variation Margining introducedInitial and Variation Margining introduced– Applies to CoDAM Instruments.

Inclusion of a system whereby:Inclusion of a system whereby:– APX is mandated by Participant CSS to close-out positions in

case it is a buyer and defaults.– APX warrants that sellers receive original contract price.

Modification of the Variation Collateral requirementModification of the Variation Collateral requirement– Recognizing removal of Belpex’s exposure to “delivery risk”.– Maintaining net sellers to contribute to Collective Fund, but

removing the Individual Variation Collateral.Removal of the ARP Perimeter Fee mechanismRemoval of the ARP Perimeter Fee mechanism– Recognizing removal of Belpex’s exposure to “delivery risk”.

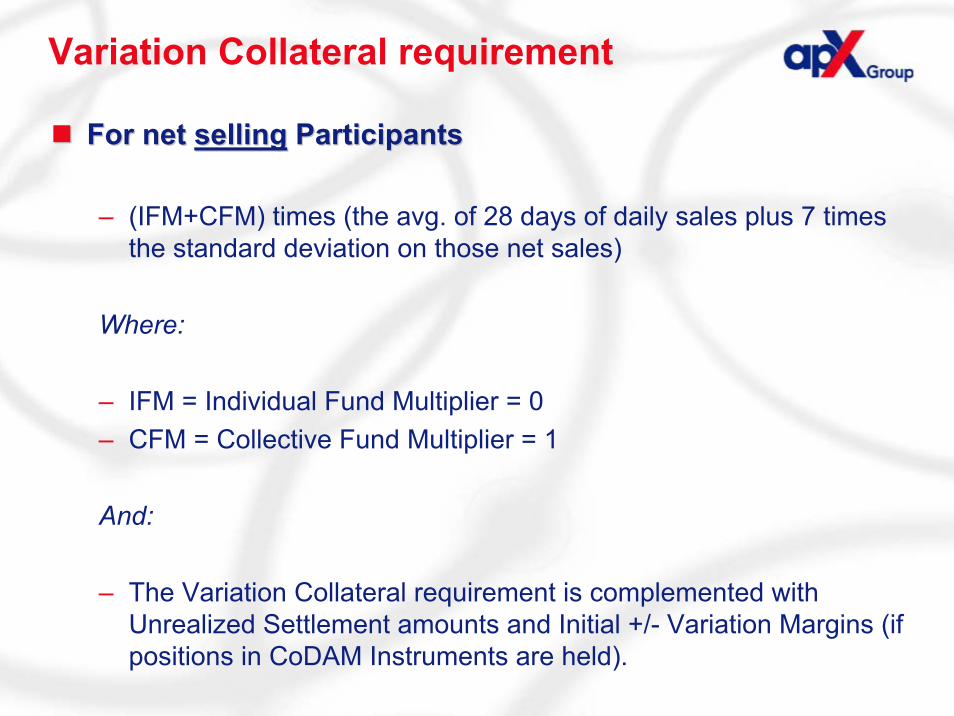

Variation Collateral requirement

For net For net sellingselling ParticipantsParticipants

– (IFM+CFM) times (the avg. of 28 days of daily sales plus 7 timesthe standard deviation on those net sales)

Where:

– IFM = Individual Fund Multiplier = 0– CFM = Collective Fund Multiplier = 1

And:

– The Variation Collateral requirement is complemented with Unrealized Settlement amounts and Initial +/- Variation Margins (if positions in CoDAM Instruments are held).

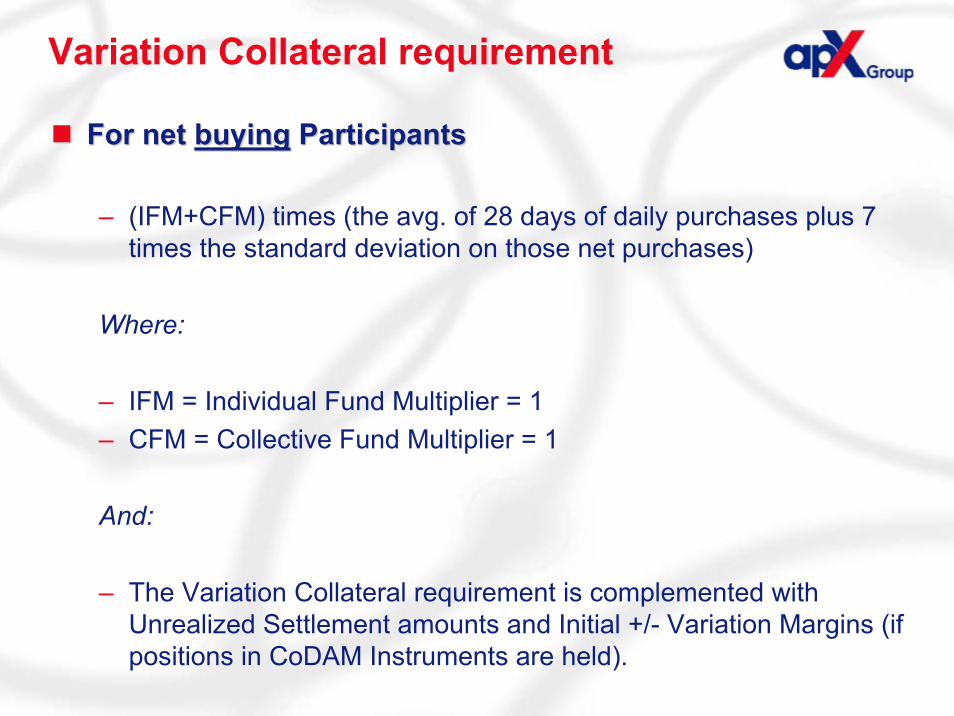

Variation Collateral requirement

For net For net buyingbuying ParticipantsParticipants

– (IFM+CFM) times (the avg. of 28 days of daily purchases plus 7 times the standard deviation on those net purchases)

Where:

– IFM = Individual Fund Multiplier = 1– CFM = Collective Fund Multiplier = 1

And:

– The Variation Collateral requirement is complemented with Unrealized Settlement amounts and Initial +/- Variation Margins (if positions in CoDAM Instruments are held).

Questions?Questions?

A VITAL LINK IN ENERGY TRADING

SettlementBrussels

January 2008

Introduction

Settlement process overviewSettlement process overviewChanges to the settlement processChanges to the settlement process

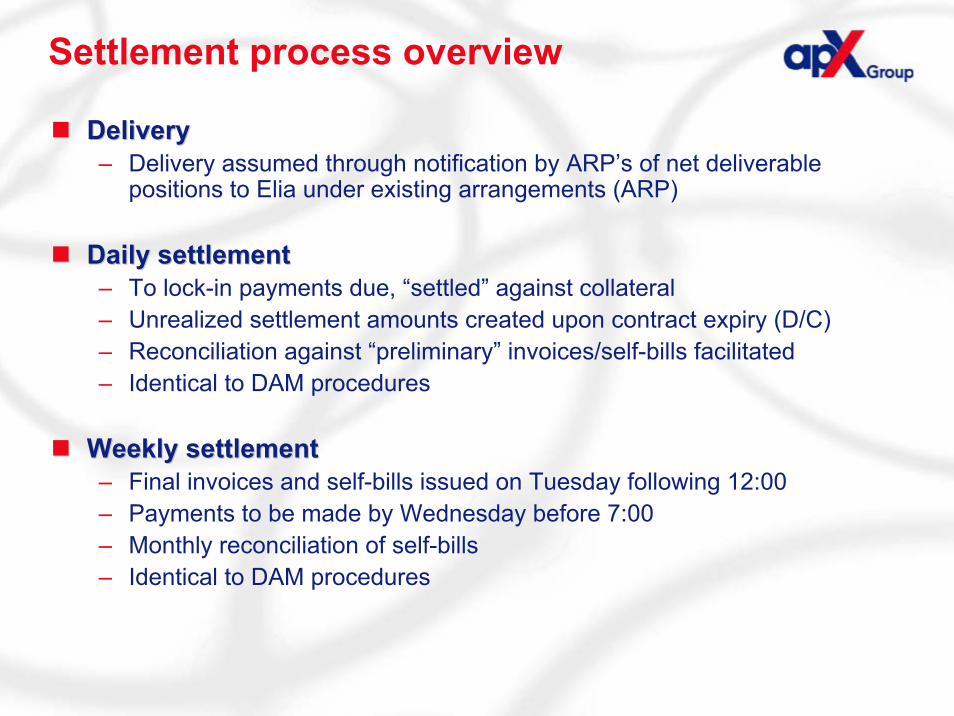

Settlement process overview

DeliveryDelivery– Delivery assumed through notification by ARP’s of net deliverable

positions to Elia under existing arrangements (ARP)

Daily settlementDaily settlement– To lock-in payments due, “settled” against collateral– Unrealized settlement amounts created upon contract expiry (D/C)– Reconciliation against “preliminary” invoices/self-bills facilitated– Identical to DAM procedures

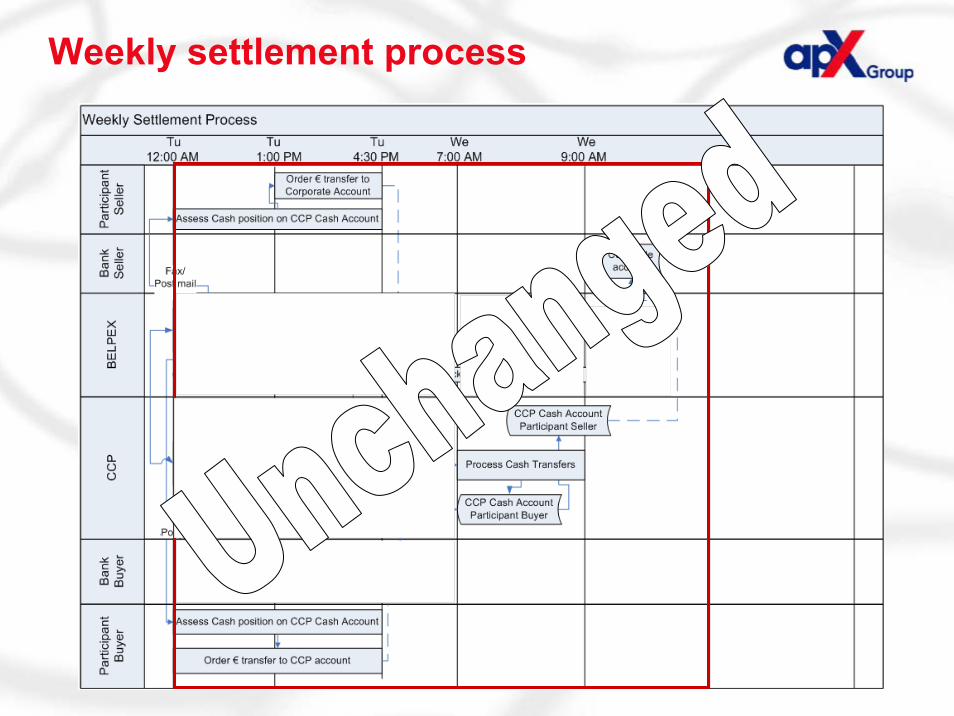

Weekly settlementWeekly settlement– Final invoices and self-bills issued on Tuesday following 12:00– Payments to be made by Wednesday before 7:00– Monthly reconciliation of self-bills– Identical to DAM procedures

Daily settlement process

Weekly settlement process

Weekly settlement process

Monthly reconciliation process

Changes to settlement process

DayDay--Ahead Spot Market (DAM)Ahead Spot Market (DAM)– Change of invoicing/self-bill scope from Wed-Tue deliveries to Tue-Mon

deliveries– Invoice/self-bill date will be Monday, available on Tuesday consistent

with today’s timings– No further changes (operational timings remain the same).

Continuous IntraContinuous Intra--Day Market (CIM)Day Market (CIM)– New, but not different from DAM.– Last Instrument on invoice/self-bill relates to delivery Monday H24

Continuous DayContinuous Day--Ahead Market (Ahead Market (CoDAMCoDAM))– New, but not different from DAM.

Single invoice/selfSingle invoice/self--bill for all market segmentsbill for all market segments– 6 lines each, separating energy and fees per market segment

Collateral and MarginingBrussels

January 2008

Collateralization

DayDay--Ahead Spot MarketAhead Spot Market– No changes, except for those related to ARP contract amendment.

Continuous IntraContinuous Intra--Day MarketDay Market– Contracts attract Unrealized Settlement amounts (D/C)– Orders require full Collateral coverage prior to entering– Open Orders reduce Participant’s remainder Collateral (Accrued Orders)– Unrealized Settlements disappear following receipt of payment as part of

weekly settlement.

Continuous DayContinuous Day--Ahead MarketAhead Market– Contracts attract Margins when Instruments are still open for trading.– Margins replaced by Unrealized Settlement amounts following Instrument

expiry.– Unrealized Settlements disappear following receipt of payment as part of

weekly settlement.

Margining

Initial MarginInitial Margin– Assumes the value at-risk when closing-out of a defaulting Participant’s

position– Based on net buy position (BP) or net sell position (SP) in €– Initial Margin = ( BP * longX ) + ( SP * shortX ).

Variation marginVariation margin– Accrued profit or loss (P/L) on Contracts in Instrument that have not yet

expired.– Contracts valued against last (reference) price at least once per day.– Difference between last price and transacted price.– P/L collateralized, not settled.– Sum of P’s and L’s = Variation Margin (net debit or credit)

Margin requirementMargin requirement– Initial Margin +/- Variation Margin (if any).

Transaction cycle

Margin parameters

Subject to frequent evaluation of adequacySubject to frequent evaluation of adequacy– No reliable historic prices available today– Over time, markets may proof not to behave symmetric, hence…– … potentially different parameters for buy and sell positions

Can be changed by giving noticeCan be changed by giving noticeInitial margin parameters linked to Liquidity ClassInitial margin parameters linked to Liquidity Class– Level to which positions are offset (netted) before calculating the Initial

Margin.– Limited set of Instruments reduces offset opportunities, which will

increase when more Instruments are introduced.Initial margin parameters will be:Initial margin parameters will be:– Applied to net buy positions– Base: 35% (offset between Base Day and Base WkEnd)– Peak: 57%– Off-peak: 30%

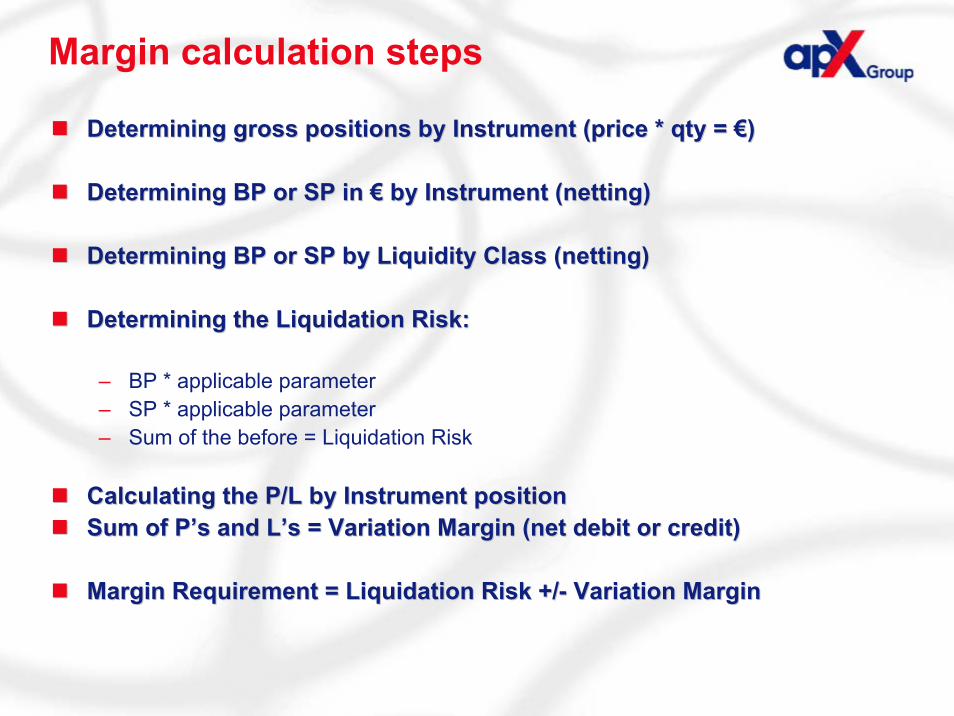

Margin calculation steps

Determining gross positions by Instrument (price * qty = Determining gross positions by Instrument (price * qty = €€))

Determining BP or SP in Determining BP or SP in €€ by Instrument (netting)by Instrument (netting)

Determining BP or SP by Liquidity Class (netting)Determining BP or SP by Liquidity Class (netting)

Determining the Liquidation Risk:Determining the Liquidation Risk:

– BP * applicable parameter– SP * applicable parameter– Sum of the before = Liquidation Risk

Calculating the P/L by Instrument positionCalculating the P/L by Instrument positionSum of PSum of P’’s and Ls and L’’s = Variation Margin (net debit or credit)s = Variation Margin (net debit or credit)

Margin Requirement = Liquidation Risk +/Margin Requirement = Liquidation Risk +/-- Variation MarginVariation Margin

Questions?Questions?

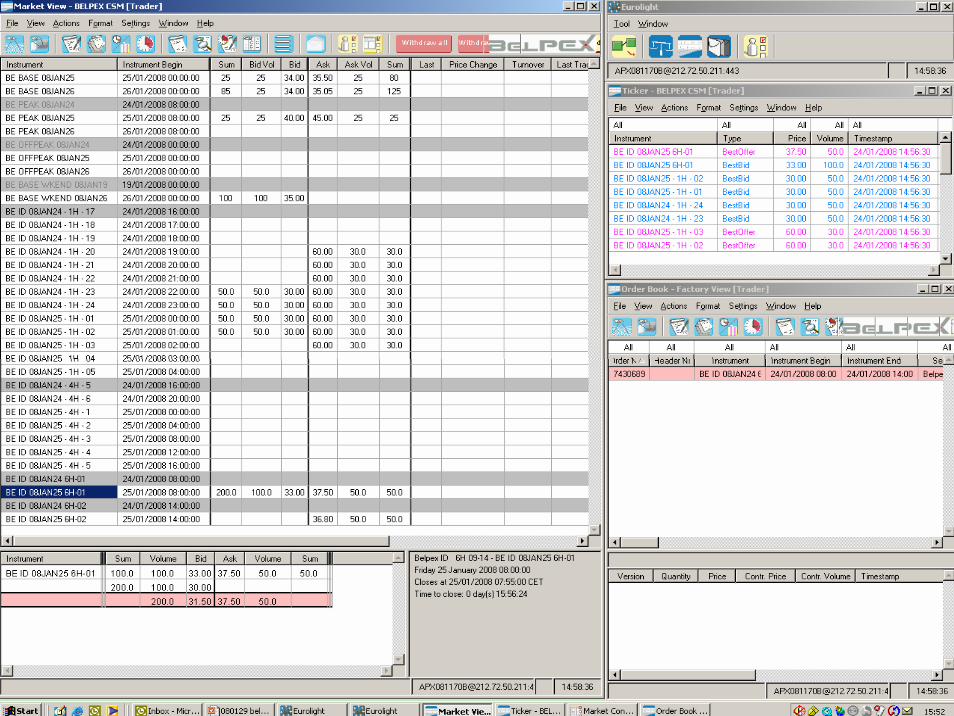

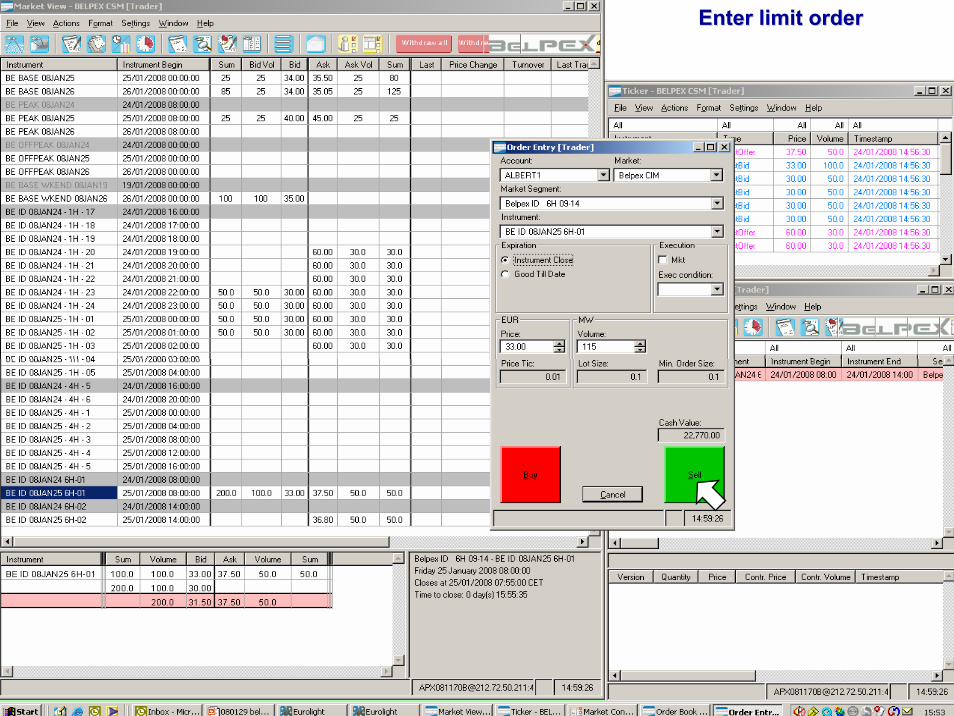

Belpex CSM in EuroLightJanuary 2008

Albert VreemanBusiness Development Manager

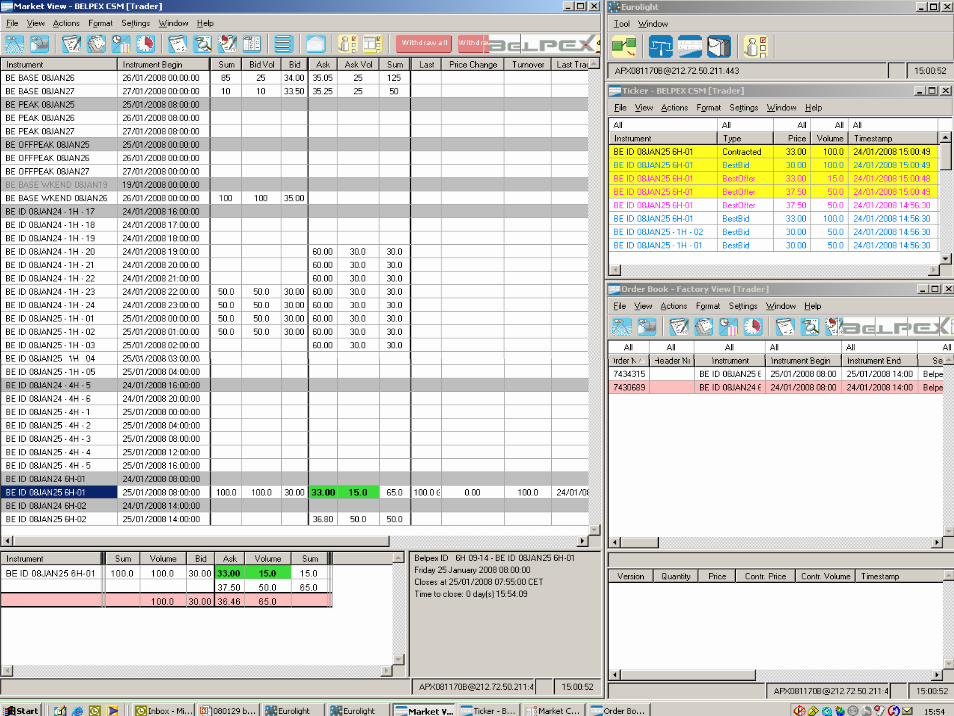

Enter limit orderEnter limit order

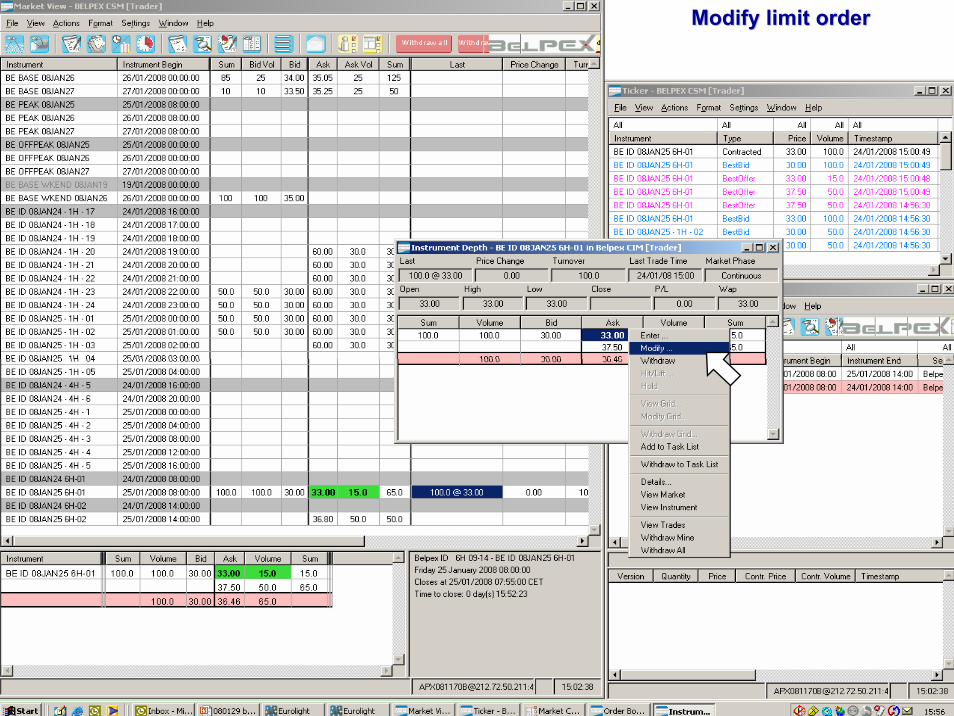

Modify limit orderModify limit order

Modify limit orderModify limit order

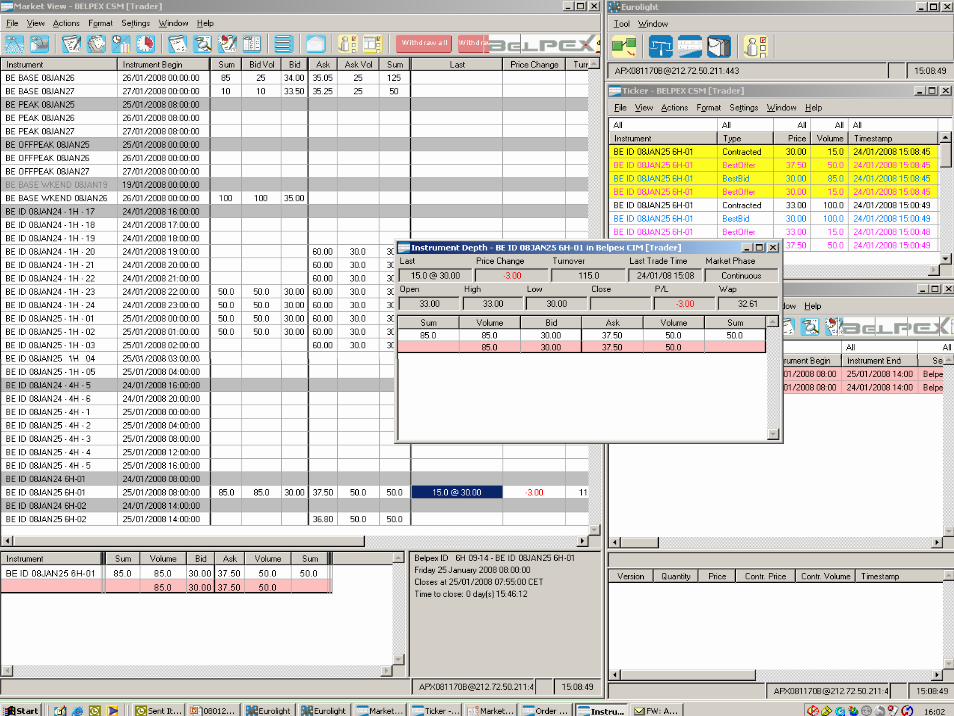

View detailed Order status View detailed Order status historyhistory

Mass entry of Orders: Task ListMass entry of Orders: Task List

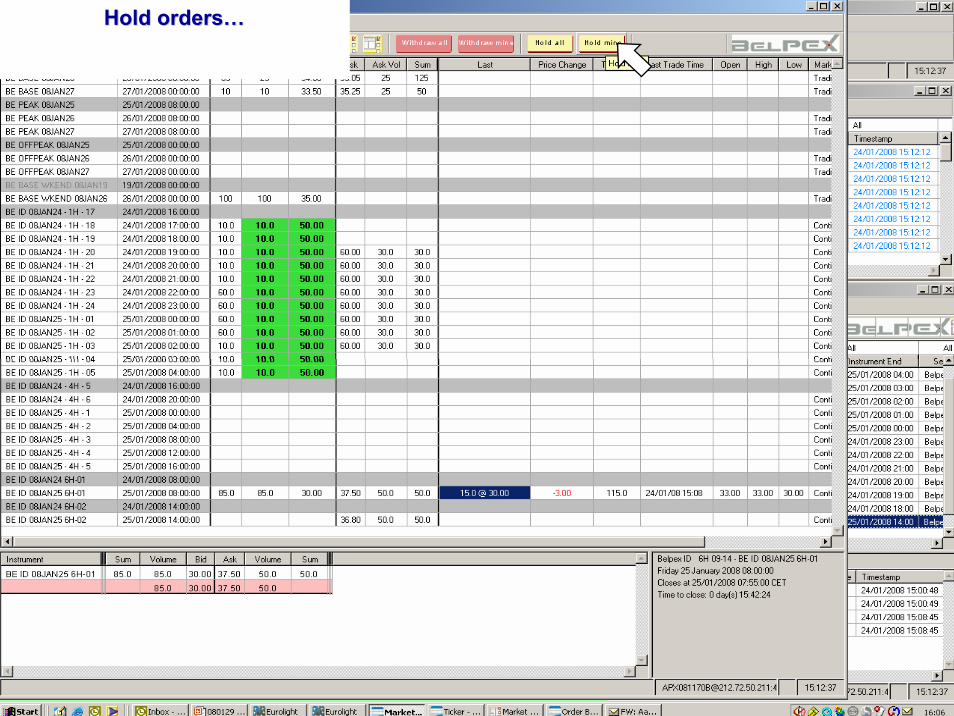

Hold ordersHold orders……

…… have a cup of coffeehave a cup of coffee……

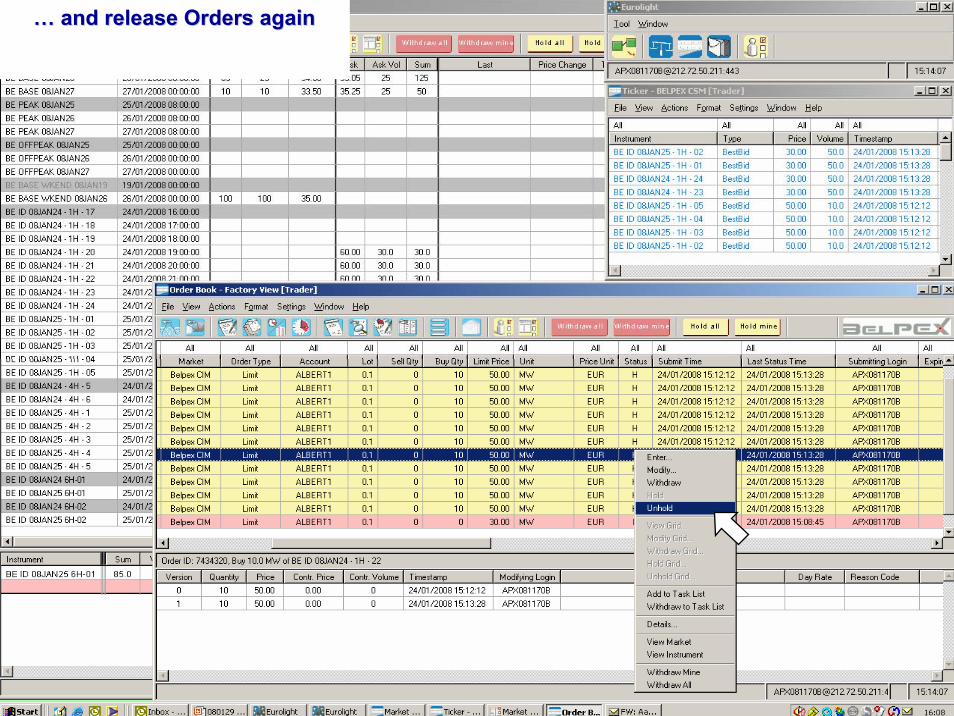

…… and release Orders againand release Orders again

View Contracts concludedView Contracts concluded

Identify cancelled (and Identify cancelled (and offsetting) Contractsoffsetting) Contracts

AA

AABBBB