Embed Size (px)

Citation preview

ITAÚ UNIBANCO S.A. MANAGEMENT REPORT To our Stockholders: We present the Management Report and financial statements of ITAÚ UNIBANCO S.A. and its subsidiaries (ITAÚ UNIBANCO CONSOLIDATED) for the periods from January 1 to June 30, 2010 and 2009, in accordance with the regulations established by the Brazilian Corporate Law, the National Monetary Council (CMN), the Central Bank of Brazil (BACEN) and the Superintendency of Private Insurance (SUSEP). NET INCOME AND STOCKHOLDERS' EQUITY ITAÚ UNIBANCO CONSOLIDATED net income totaled R$ 3,662 million for the period and net income per share of capital stock was R$ 0.89. Consolidated stockholders' equity totaled R$ 37,063 million and book value per share reached R$ 9.05. ASSETS AND FUNDS RAISED Assets totaled R$ 618,948 million and were substantially made up of R$ 280,110 million of Interbank Investments, Securities and Derivative Financial Instruments, and R$ 216,092 million of Loan, Lease, Other Credit Operations and Foreign Exchange Portfolio. Raised and Managed Funds represented R$ 534,697 million. CIRCULAR LETTER No. 3,068/01 OF BACEN ITAÚ UNIBANCO CONSOLIDATED hereby represents to have the financial capacity and the intention to hold to maturity the securities classified under the line “held-to-maturity securities” in the balance sheet, in the amount of R$ 2,953 million, corresponding to only 2.8% of the total securities and derivative financial instruments held. ACKNOWLEDGEMENTS We thank our shareholders and clients for their indispensable support and trust, and our employees for their determination and commitment, which have been essential to reaching differentiated results. São Paulo, August 30, 2010. Executive Board

ITAÚ UNIBANCO S.A.

Chief Executive Officer Directors (Continued)ROBERTO EGYDIO SETUBAL GILBERTO TRAZZI CANTERAS

HENRIQUE RUTHER (*)Vice-Presidents JACKSON RICARDO GOMES

ALEXANDRE DE BARROS JASON PETER CRAUFORD ALFREDO EGYDIO SETUBAL JEAN MARTIN SIGRIST JÚNIORGERALDO JOSÉ CARBONE JOÃO ANTONIO DANTAS BEZERRA LEITEJOSÉ CASTRO ARAÚJO RUDGE JOÃO LUIZ DE MEDEIROSMÁRCIO DE ANDRADE SCHETTINI JORGE LUIZ VIEGAS RAMALHO MARCO AMBROGIO CRESPI BONOMI LAVÍNIA MORAES DE ALMEIDA NOGUEIRA JUNQUEIRA MARCOS DE BARROS LISBOA LEILA CRISTIANE BARBOZA BRAGA DE MELORUY VILLELA MORAES ABREU LINDA AGARINAKAMURARICARDO VILLELA MARINO LUÍS ANTONIO RODRIGUESSÉRGIO RIBEIRO DA COSTA WERLANG LUÍS EDUARDO GROSS SIQUEIRA CUNHA

LUIS TADEU MANTOVANI SASSI Executive Directors LUIZ ANTONIO FERNANDES CALDAS MORONE

CAIO IBRAHIM DAVID (*) LUIZ ANTONIO NOGUEIRA DE FRANÇACELSO SCARAMUZZA LUIZ EDUARDO LOUREIRO VELOSO CLAUDIA POLITANSKI LUIZ FELIPE PINHEIRO DE ANDRADEDEMOSTHENES MADUREIRA DE PINHO NETO LUIZ FERNANDO OLIVEIRA BARRICHELOFERNANDO MARSELLA CHACON RUIZ LUIZ MARCELO ALVES DE MORAESIVO LUIZ DE SÁ FREIRE VIEITAS JUNIOR MANOEL ANTONIO GRANADOJOÃO JACÓ HAZARABEDIAN MARCELO BOOCKJOSÉ ROBERTO HAYM MARCELO LUIS ORTICELLI LUÍS OTAVIO MATIAS MARCO ANTONIO ANTUNESOSVALDO DO NASCIMENTO MARCO ANTONIO SUDANORICARDO BALDIN MARCOS ANTÔNIO VAZ DE MAGALHÃES SANDRA NUNES DA CUNHA BOTEGUIM MARCOS AUGUSTO CAETANO DA SILVA FILHO

MARCOS BRAGA DAINESIDirectors MARCOS SILVA MASSUKADO

ADRIANO BRITO DA COSTA LIMA MARCOS VANDERLEI BELINI FERREIRA ALMIR VIGNOTO MARIO LUIZ AMABILE (*)ANDRÉ SAPOZNIK MAURÍCIO FERREIRA DE SOUZA ANDRÉA MATTEUCCI PINOTTI CORDEIRO MAURO MORELLIANTONIO CARLOS AZZI JÚNIOR NATALÍSIO DE ALMEIDA JÚNIORANTONIO CARLOS RICHECKI RIBEIRO OLIVIO MORI JÚNIOR ANTONIO SIVALDI ROBERTI FILHO OSMAR MARCHINIARNALDO PEREIRA PINTO OSVALDO JOSÉ DAL FABBROAURÉLIO JOSÉ DA SILVA PORTELLA PAULO EIKIEVICIUS CORCHAKICARLOS AUGUSTO DE OLIVEIRA PAULO MEIRELLES DE OLIVEIRA SANTOSCARLOS EDUARDO DE CASTRO PEDRO PAULO DE ALMEIDA CARNEIRO CUNHA CARLOS EDUARDO DE SOUZA LARA PLÍNIO CARDOSO DA COSTA PATRÃO CARLOS EDUARDO MACCARIELLO (*) RENATA HELENA DE OLIVEIRA TUBINICARLOS EDUARDO MONICO RENÊ MARCELO GONÇALVES CARLOS HENRIQUE DONEGÁ AIDAR RICARDO LIMA SOARESCARLOS HENRIQUE ZANVETTOR RICARDO ORLANDOCECÍLIA MARIA ARELLANO MISZPUTEN RICARDO RIBEIRO MANDACARU GUERRACESAR PADOVAN RICARDO TERENZI NEUENSCHWANDERCÍCERO MARCUS DE ARAÚJO ROBERTO LAMY CLÁUDIO CESAR SANCHES ROBERTO MASSARU NISHIKAWA CLAUDIO JOSÉ COUTINHO ARROMATTE ROGERIO CARVALHO BRAGACOSMO FALCO ROGÉRIO PAULO CALDERÓN PERES CRISTIANE MAGALHÃES TEIXEIRA PORTELLA ROMILDO GONÇALVES VALENTEDANIEL LUIZ GLEIZER (*) ROONEY SILVAEDUARDO ALMEIDA PRADO SERGIO GUILLINET FAJERMAN (*)EDUARDO HIROYUKI MIYAKI (*) SERGIO SOUZA FERNANDES JÚNIOR ERNESTO ANTUNES DE CARVALHO VILMAR LIMA CARREIRO (*)FERNANDO DELLA TORRE CHAGASFERNANDO JOSÉ COSTA TELES

(*) Elected at the ASM of April 30, 2010 and the ESM of May 28, 2010 and sworn in 08/02/2010.

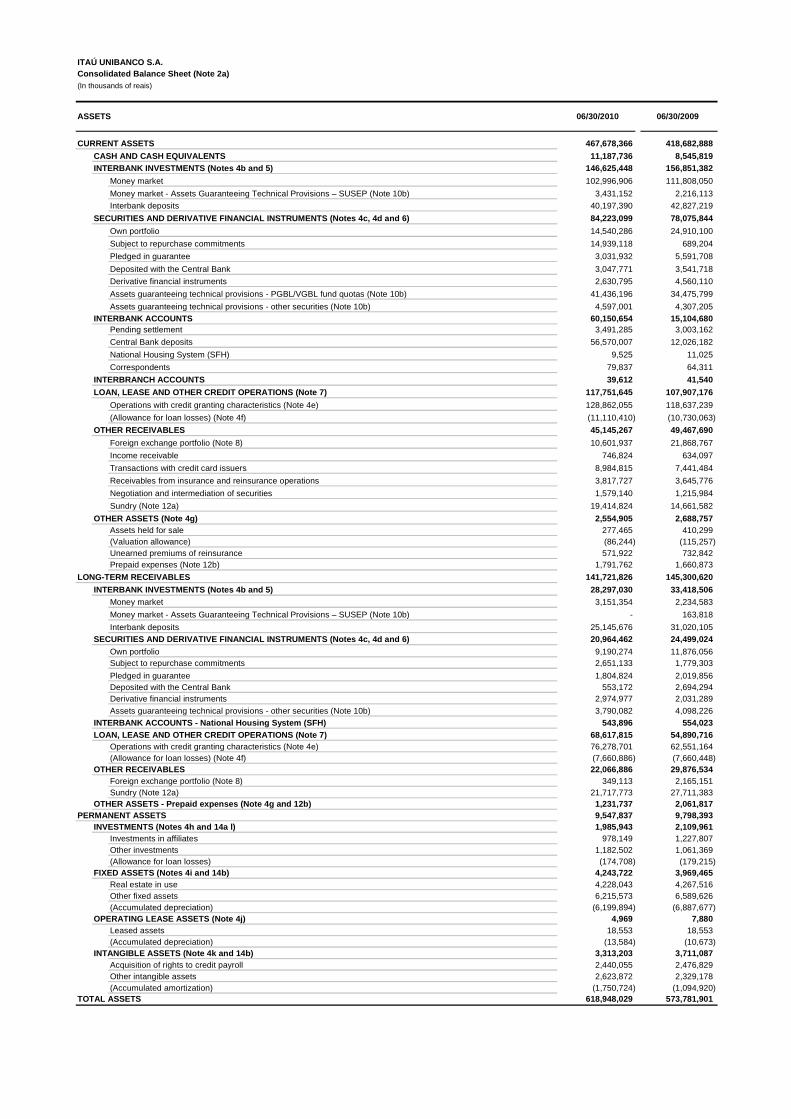

467,678,366 418,682,888

11,187,736 8,545,819 146,625,448 156,851,382

Money market 102,996,906 111,808,050

Money market - Assets Guaranteeing Technical Provisions – SUSEP (Note 10b) 3,431,152 2,216,113

Interbank deposits 40,197,390 42,827,219

84,223,099 78,075,844

Own portfolio 14,540,286 24,910,100

Subject to repurchase commitments 14,939,118 689,204

Pledged in guarantee 3,031,932 5,591,708

Deposited with the Central Bank 3,047,771 3,541,718

Derivative financial instruments 2,630,795 4,560,110

Assets guaranteeing technical provisions - PGBL/VGBL fund quotas (Note 10b) 41,436,196 34,475,799

Assets guaranteeing technical provisions - other securities (Note 10b) 4,597,001 4,307,205 60,150,654 15,104,680

Pending settlement 3,491,285 3,003,162

Central Bank deposits 56,570,007 12,026,182

National Housing System (SFH) 9,525 11,025

Correspondents 79,837 64,311

39,612 41,540

117,751,645 107,907,176

Operations with credit granting characteristics (Note 4e) 128,862,055 118,637,239

(Allowance for loan losses) (Note 4f) (11,110,410) (10,730,063)

45,145,267 49,467,690

Foreign exchange portfolio (Note 8) 10,601,937 21,868,767

Income receivable 746,824 634,097

Transactions with credit card issuers 8,984,815 7,441,484

Receivables from insurance and reinsurance operations 3,817,727 3,645,776

Negotiation and intermediation of securities 1,579,140 1,215,984

Sundry (Note 12a) 19,414,824 14,661,582

2,554,905 2,688,757 Assets held for sale 277,465 410,299 (Valuation allowance) (86,244) (115,257) Unearned premiums of reinsurance 571,922 732,842 Prepaid expenses (Note 12b) 1,791,762 1,660,873

141,721,826 145,300,620

28,297,030 33,418,506 Money market 3,151,354 2,234,583

Money market - Assets Guaranteeing Technical Provisions – SUSEP (Note 10b) - 163,818

Interbank deposits 25,145,676 31,020,105 20,964,462 24,499,024

Own portfolio 9,190,274 11,876,056 Subject to repurchase commitments 2,651,133 1,779,303

Pledged in guarantee 1,804,824 2,019,856 Deposited with the Central Bank 553,172 2,694,294 Derivative financial instruments 2,974,977 2,031,289

Assets guaranteeing technical provisions - other securities (Note 10b) 3,790,082 4,098,226 543,896 554,023

68,617,815 54,890,716 Operations with credit granting characteristics (Note 4e) 76,278,701 62,551,164 (Allowance for loan losses) (Note 4f) (7,660,886) (7,660,448)

22,066,886 29,876,534 Foreign exchange portfolio (Note 8) 349,113 2,165,151 Sundry (Note 12a) 21,717,773 27,711,383

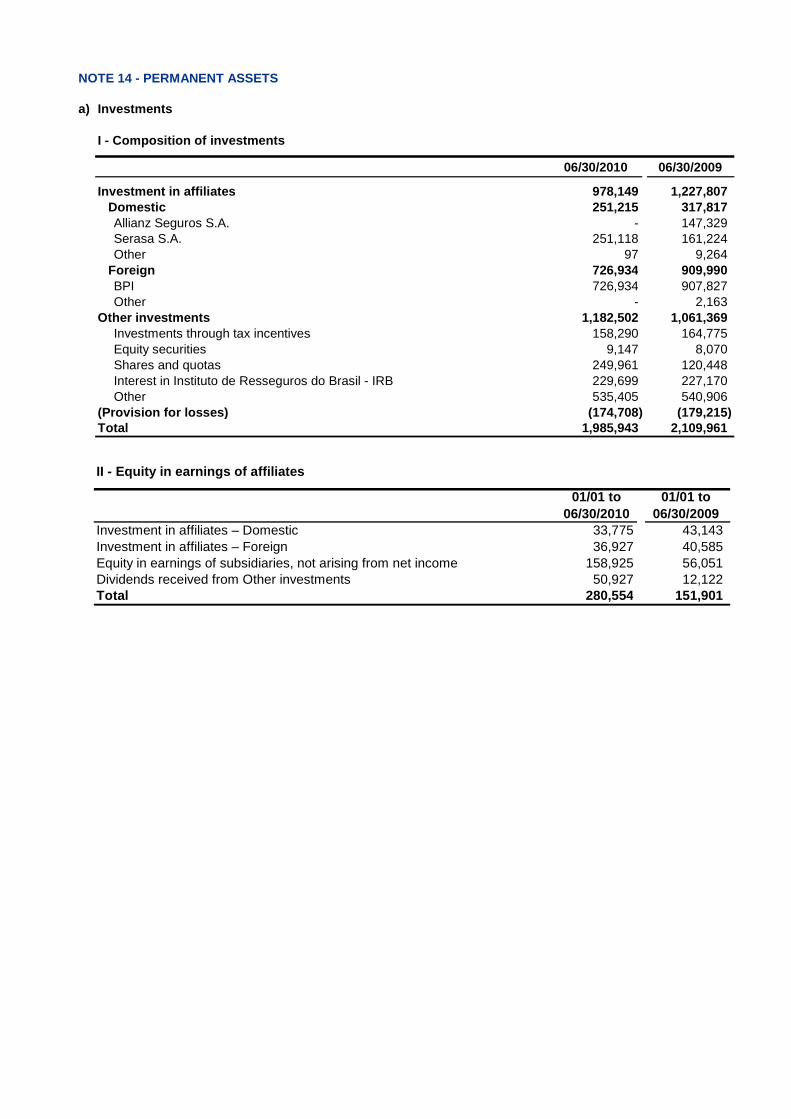

1,231,737 2,061,817 9,547,837 9,798,393 1,985,943 2,109,961

Investments in affiliates 978,149 1,227,807 Other investments 1,182,502 1,061,369 (Allowance for loan losses) (174,708) (179,215)

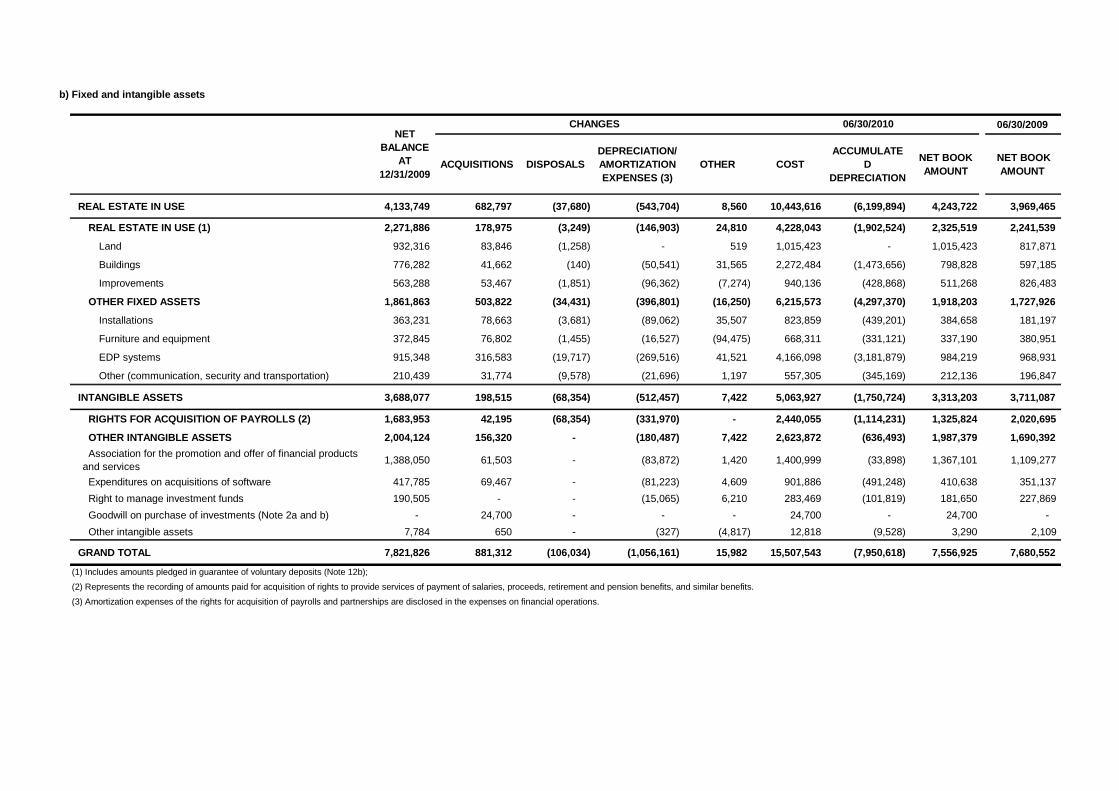

4,243,722 3,969,465 Real estate in use 4,228,043 4,267,516 Other fixed assets 6,215,573 6,589,626 (Accumulated depreciation) (6,199,894) (6,887,677)

4,969 7,880 Leased assets 18,553 18,553 (Accumulated depreciation) (13,584) (10,673)

INTANGIBLE ASSETS (Note 4k and 14b) 3,313,203 3,711,087 Acquisition of rights to credit payroll 2,440,055 2,476,829 Other intangible assets 2,623,872 2,329,178 (Accumulated amortization) (1,750,724) (1,094,920)

618,948,029 573,781,901

06/30/2010 06/30/2009

CASH AND CASH EQUIVALENTS

CURRENT ASSETS

ASSETS

INTERBANK INVESTMENTS (Notes 4b and 5)

INTERBRANCH ACCOUNTS

OTHER RECEIVABLES

ITAÚ UNIBANCO S.A.Consolidated Balance Sheet (Note 2a)(In thousands of reais)

LOAN, LEASE AND OTHER CREDIT OPERATIONS (Note 7)

SECURITIES AND DERIVATIVE FINANCIAL INSTRUMENTS (No tes 4c, 4d and 6)

LONG-TERM RECEIVABLES

INTERBANK INVESTMENTS (Notes 4b and 5)

SECURITIES AND DERIVATIVE FINANCIAL INSTRUMENTS (No tes 4c, 4d and 6)

INTERBANK ACCOUNTS - National Housing System (SFH)

OTHER ASSETS (Note 4g)

INTERBANK ACCOUNTS

TOTAL ASSETS

LOAN, LEASE AND OTHER CREDIT OPERATIONS (Note 7)

OTHER RECEIVABLES

OTHER ASSETS - Prepaid expenses (Note 4g and 12b)

INVESTMENTS (Notes 4h and 14a l)

FIXED ASSETS (Notes 4i and 14b)

PERMANENT ASSETS

OPERATING LEASE ASSETS (Note 4j)

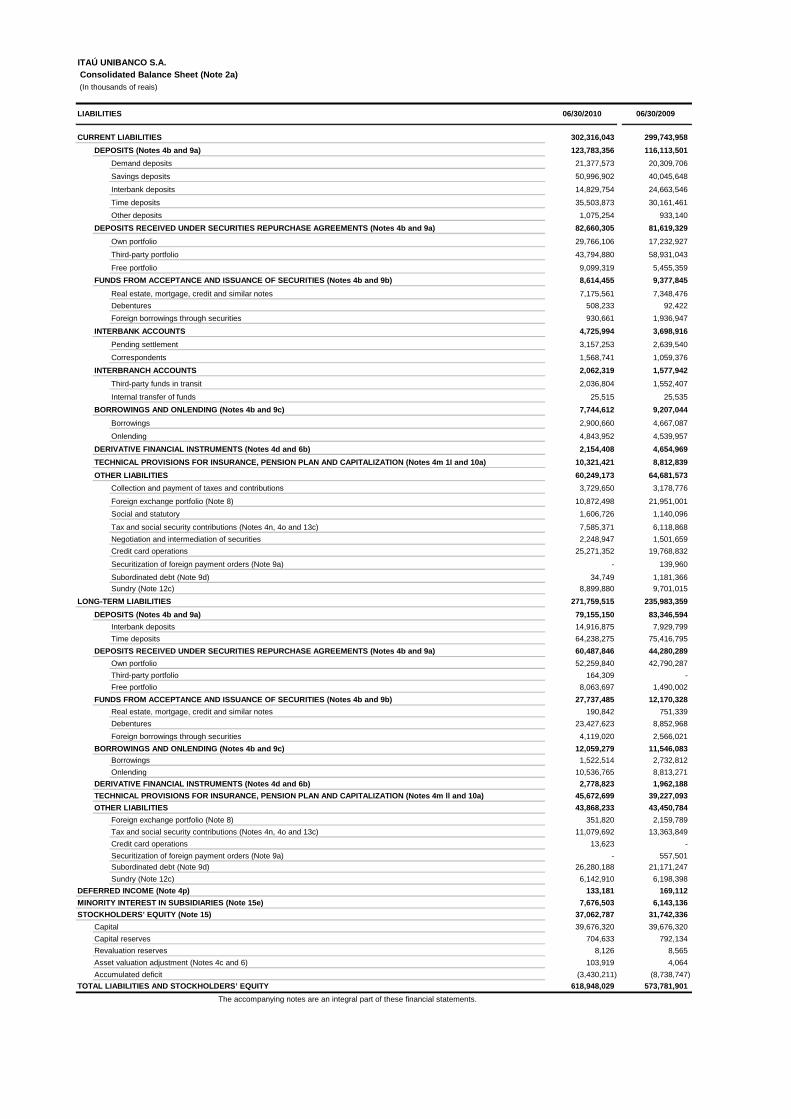

302,316,043 299,743,958

123,783,356 116,113,501

Demand deposits 21,377,573 20,309,706

Savings deposits 50,996,902 40,045,648

Interbank deposits 14,829,754 24,663,546

Time deposits 35,503,873 30,161,461

Other deposits 1,075,254 933,140

82,660,305 81,619,329

Own portfolio 29,766,106 17,232,927

Third-party portfolio 43,794,880 58,931,043

Free portfolio 9,099,319 5,455,359

8,614,455 9,377,845

Real estate, mortgage, credit and similar notes 7,175,561 7,348,476

Debentures 508,233 92,422

Foreign borrowings through securities 930,661 1,936,947

4,725,994 3,698,916

Pending settlement 3,157,253 2,639,540

Correspondents 1,568,741 1,059,376

2,062,319 1,577,942

Third-party funds in transit 2,036,804 1,552,407

Internal transfer of funds 25,515 25,535

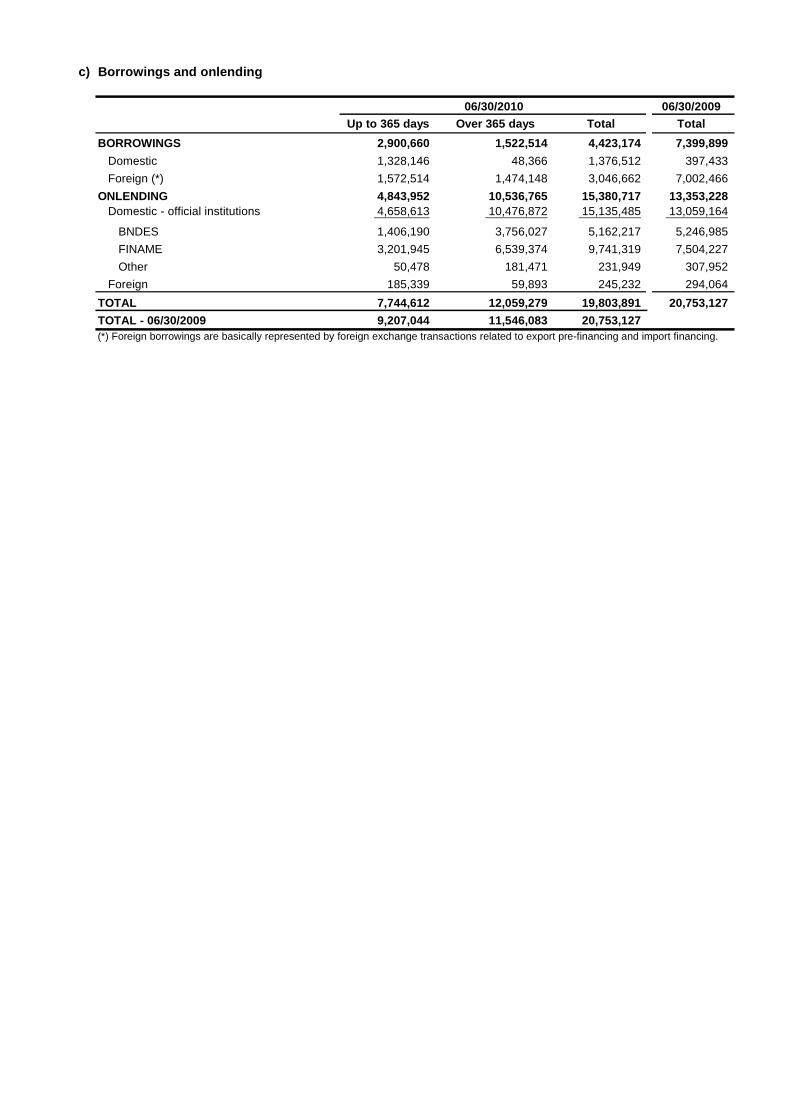

7,744,612 9,207,044

Borrowings 2,900,660 4,667,087

Onlending 4,843,952 4,539,957

2,154,408 4,654,969

10,321,421 8,812,839

60,249,173 64,681,573

Collection and payment of taxes and contributions 3,729,650 3,178,776

Foreign exchange portfolio (Note 8) 10,872,498 21,951,001

Social and statutory 1,606,726 1,140,096

Tax and social security contributions (Notes 4n, 4o and 13c) 7,585,371 6,118,868

Negotiation and intermediation of securities 2,248,947 1,501,659

Credit card operations 25,271,352 19,768,832

Securitization of foreign payment orders (Note 9a) - 139,960

Subordinated debt (Note 9d) 34,749 1,181,366

Sundry (Note 12c) 8,899,880 9,701,015

271,759,515 235,983,359

79,155,150 83,346,594

Interbank deposits 14,916,875 7,929,799

Time deposits 64,238,275 75,416,795

60,487,846 44,280,289

Own portfolio 52,259,840 42,790,287

Third-party portfolio 164,309 -

Free portfolio 8,063,697 1,490,002

27,737,485 12,170,328

Real estate, mortgage, credit and similar notes 190,842 751,339

Debentures 23,427,623 8,852,968

Foreign borrowings through securities 4,119,020 2,566,021

12,059,279 11,546,083 Borrowings 1,522,514 2,732,812

Onlending 10,536,765 8,813,271

2,778,823 1,962,188

45,672,699 39,227,093

43,868,233 43,450,784

Foreign exchange portfolio (Note 8) 351,820 2,159,789

Tax and social security contributions (Notes 4n, 4o and 13c) 11,079,692 13,363,849

Credit card operations 13,623 -

Securitization of foreign payment orders (Note 9a) - 557,501 Subordinated debt (Note 9d) 26,280,188 21,171,247

Sundry (Note 12c) 6,142,910 6,198,398

133,181 169,112

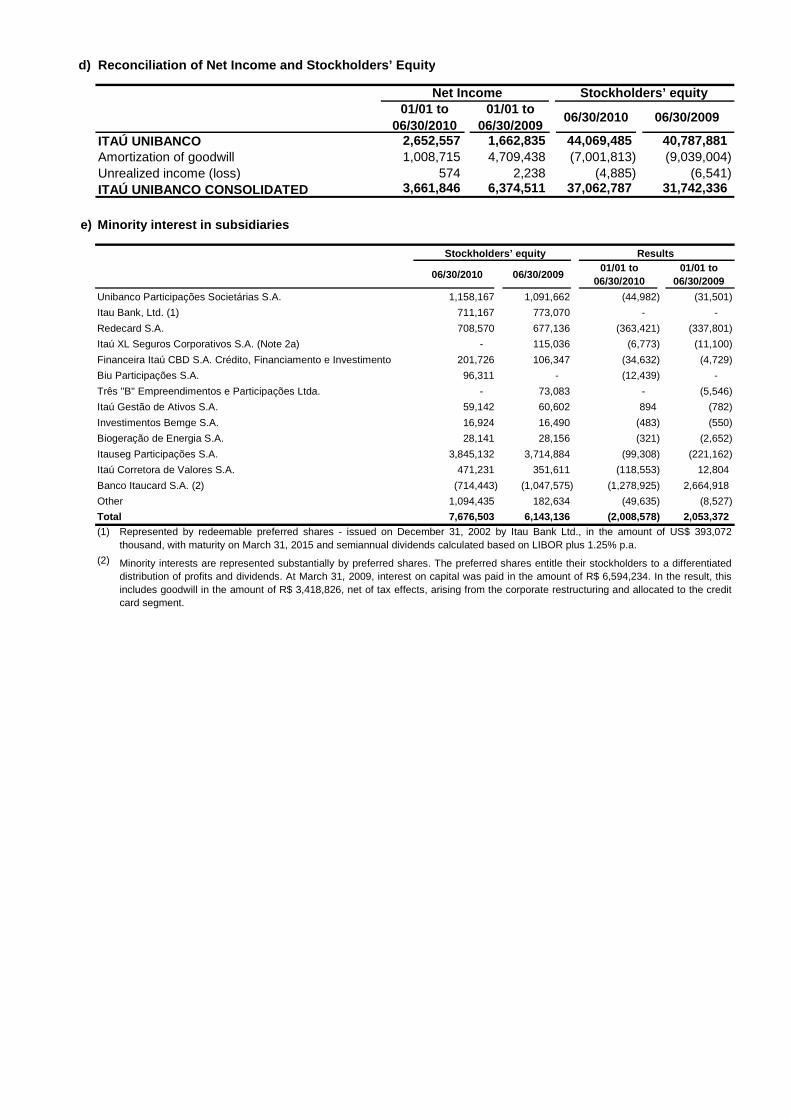

7,676,503 6,143,136

37,062,787 31,742,336

39,676,320 39,676,320

704,633 792,134

8,126 8,565

103,919 4,064

(3,430,211) (8,738,747)

618,948,029 573,781,901

06/30/2009

The accompanying notes are an integral part of these financial statements.

DEPOSITS (Notes 4b and 9a)

DEPOSITS RECEIVED UNDER SECURITIES REPURCHASE AGREEMENTS (Notes 4b and 9a)

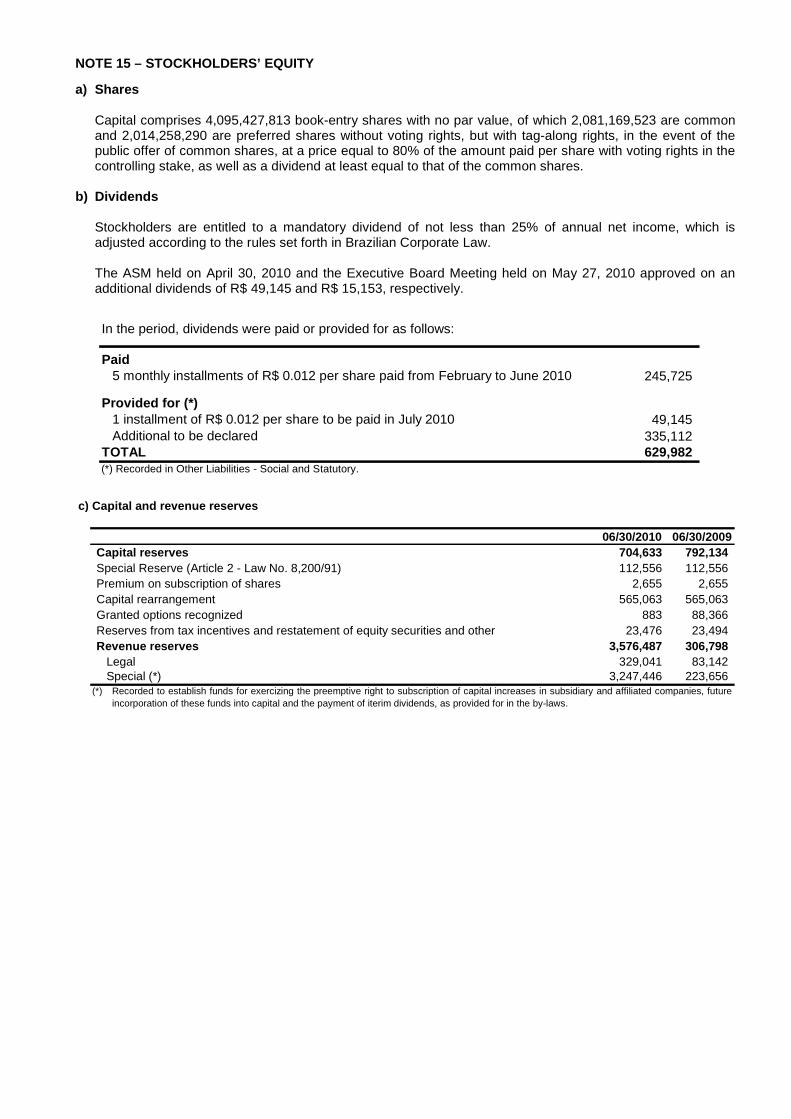

Capital reserves

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY

TECHNICAL PROVISIONS FOR INSURANCE, PENSION PLAN AN D CAPITALIZATION (Notes 4m ll and 10a)

DEFERRED INCOME (Note 4p)

MINORITY INTEREST IN SUBSIDIARIES (Note 15e)

Capital

Asset valuation adjustment (Notes 4c and 6)

DEPOSITS (Notes 4b and 9a)

LONG-TERM LIABILITIES

TECHNICAL PROVISIONS FOR INSURANCE, PENSION PLAN AN D CAPITALIZATION (Notes 4m 1I and 10a)

OTHER LIABILITIES

DERIVATIVE FINANCIAL INSTRUMENTS (Notes 4d and 6b)

DEPOSITS RECEIVED UNDER SECURITIES REPURCHASE AGREEMENTS (Notes 4b and 9a)

FUNDS FROM ACCEPTANCE AND ISSUANCE OF SECURITIES (N otes 4b and 9b)

INTERBANK ACCOUNTS

STOCKHOLDERS’ EQUITY (Note 15)

06/30/2010LIABILITIES

ITAÚ UNIBANCO S.A. Consolidated Balance Sheet (Note 2a) (In thousands of reais)

CURRENT LIABILITIES

INTERBRANCH ACCOUNTS

BORROWINGS AND ONLENDING (Notes 4b and 9c)

Accumulated deficit

FUNDS FROM ACCEPTANCE AND ISSUANCE OF SECURITIES (N otes 4b and 9b)

BORROWINGS AND ONLENDING (Notes 4b and 9c)

DERIVATIVE FINANCIAL INSTRUMENTS (Notes 4d and 6b)

OTHER LIABILITIES

Revaluation reserves

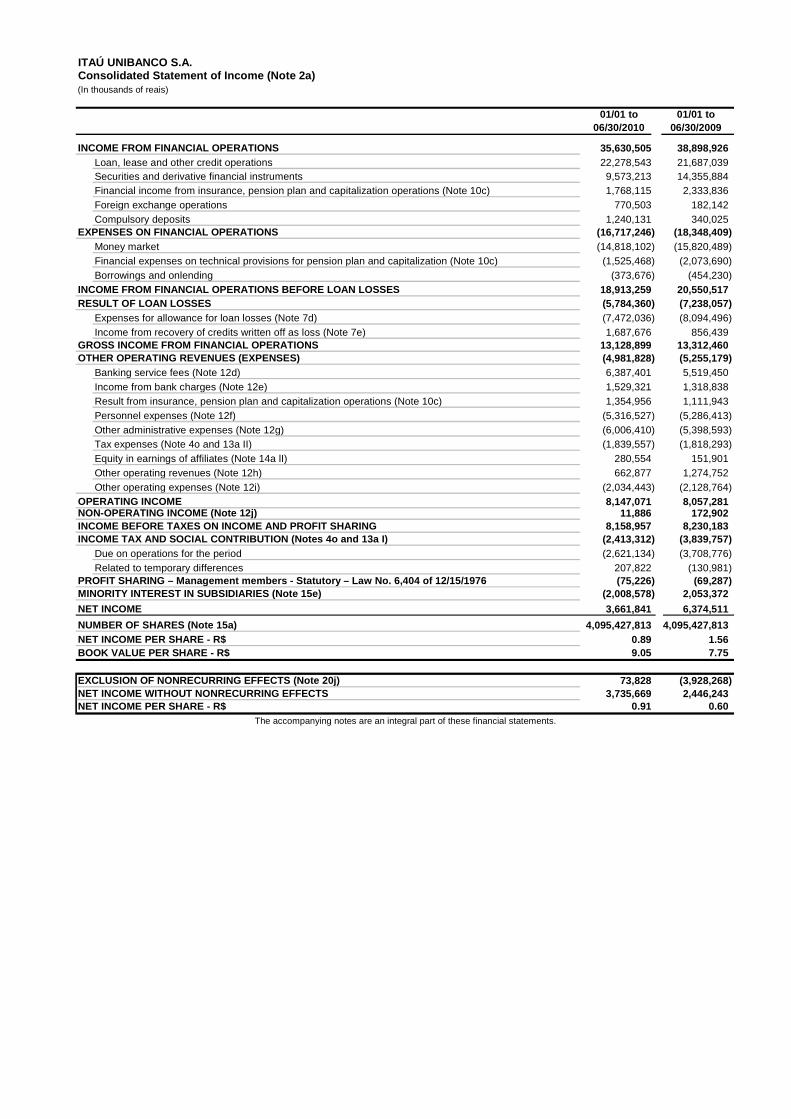

35,630,505 38,898,926 22,278,543 21,687,039 9,573,213 14,355,884 1,768,115 2,333,836

770,503 182,142 1,240,131 340,025

(16,717,246) (18,348,409) (14,818,102) (15,820,489)

(1,525,468) (2,073,690) (373,676) (454,230)

18,913,259 20,550,517 (5,784,360) (7,238,057) (7,472,036) (8,094,496) 1,687,676 856,439

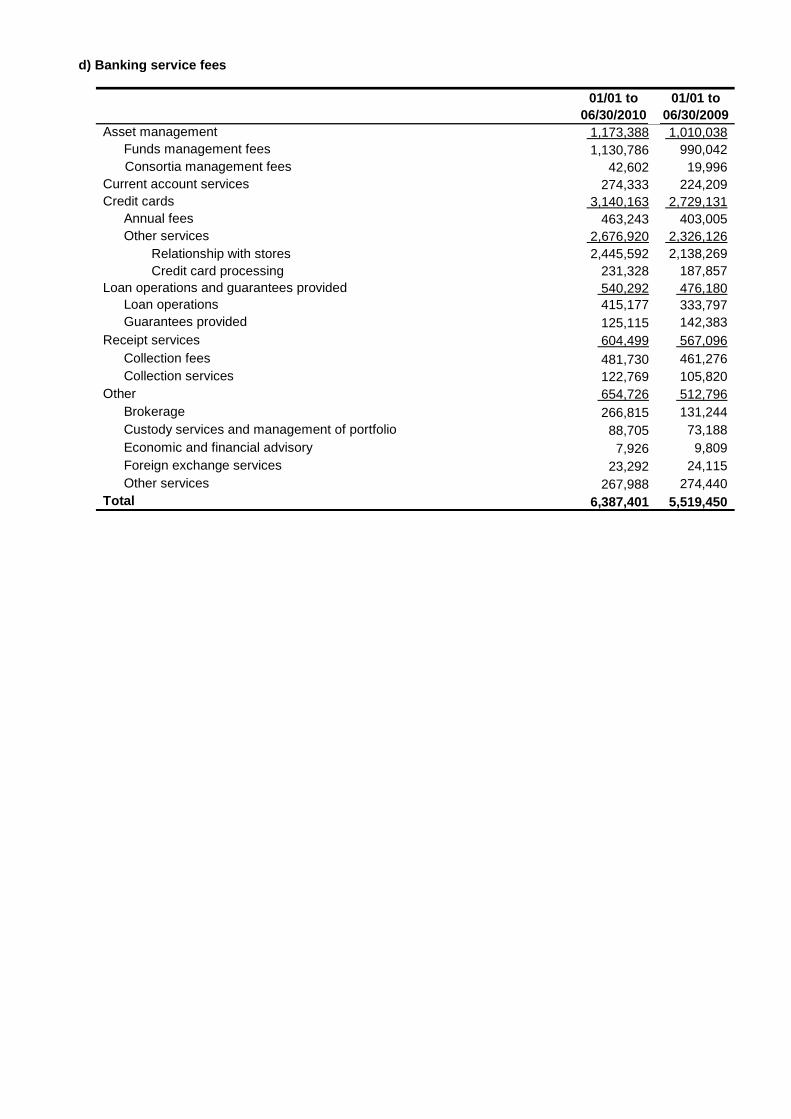

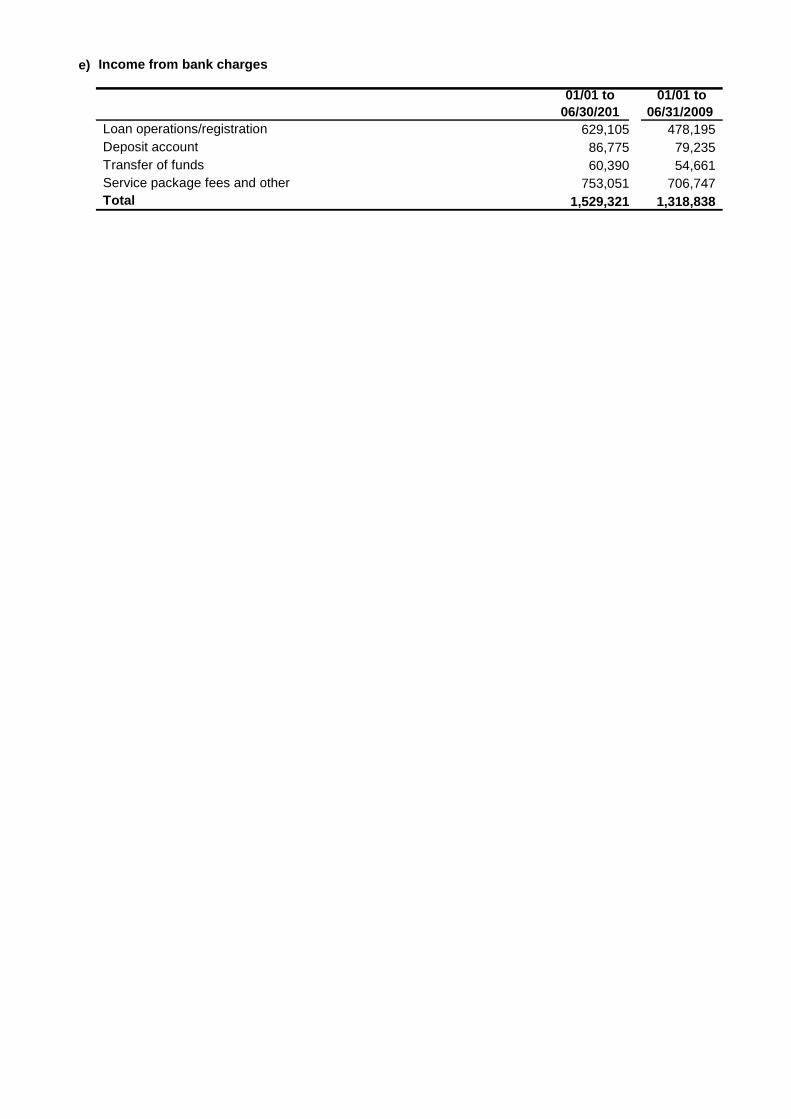

13,128,899 13,312,460 (4,981,828) (5,255,179) 6,387,401 5,519,450 1,529,321 1,318,838 1,354,956 1,111,943

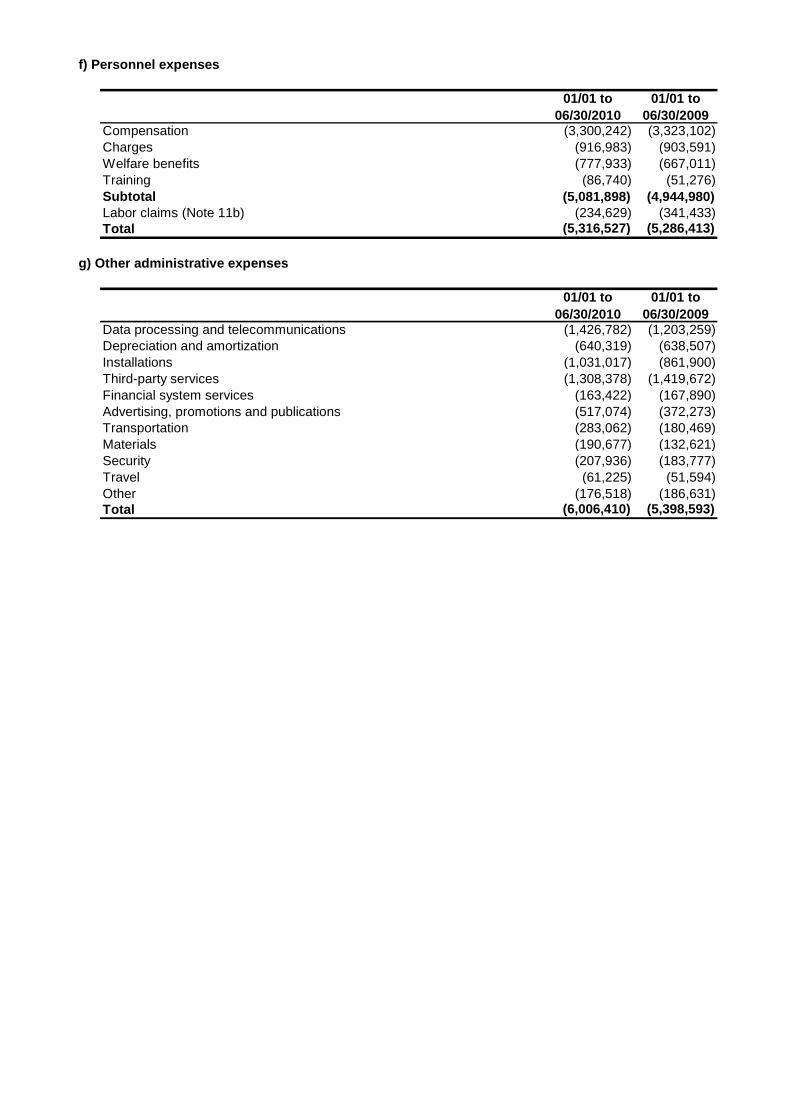

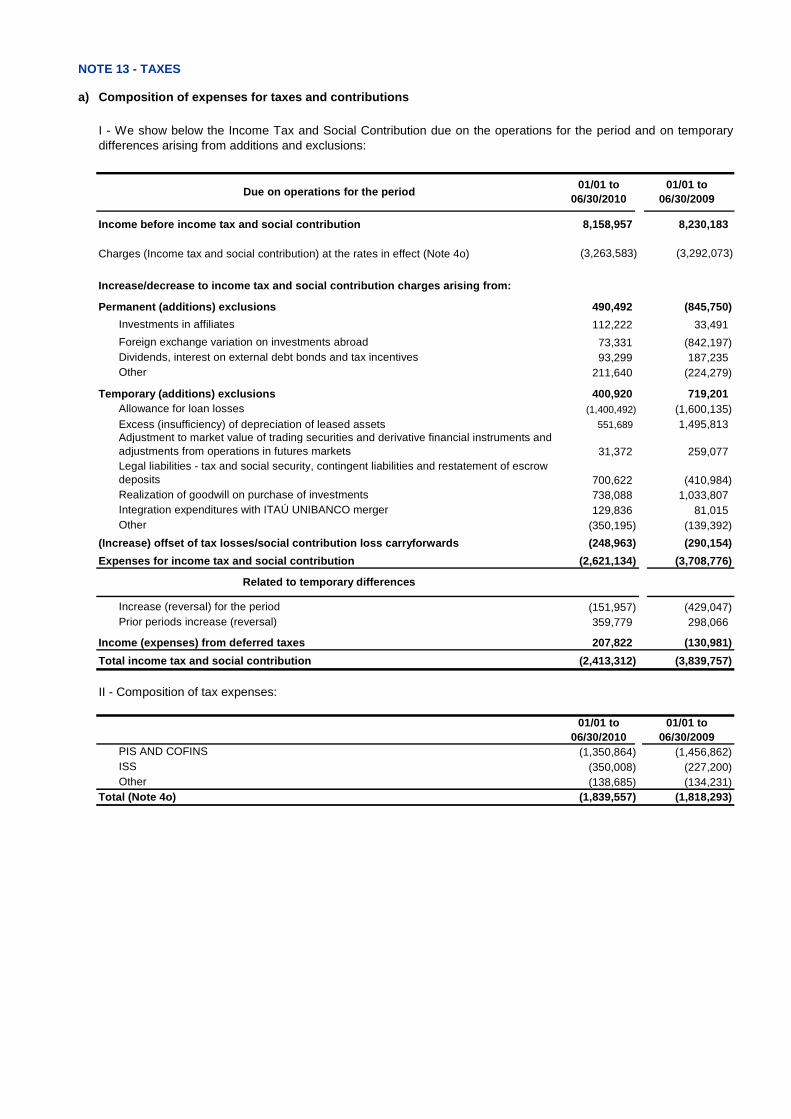

(5,316,527) (5,286,413) (6,006,410) (5,398,593) (1,839,557) (1,818,293)

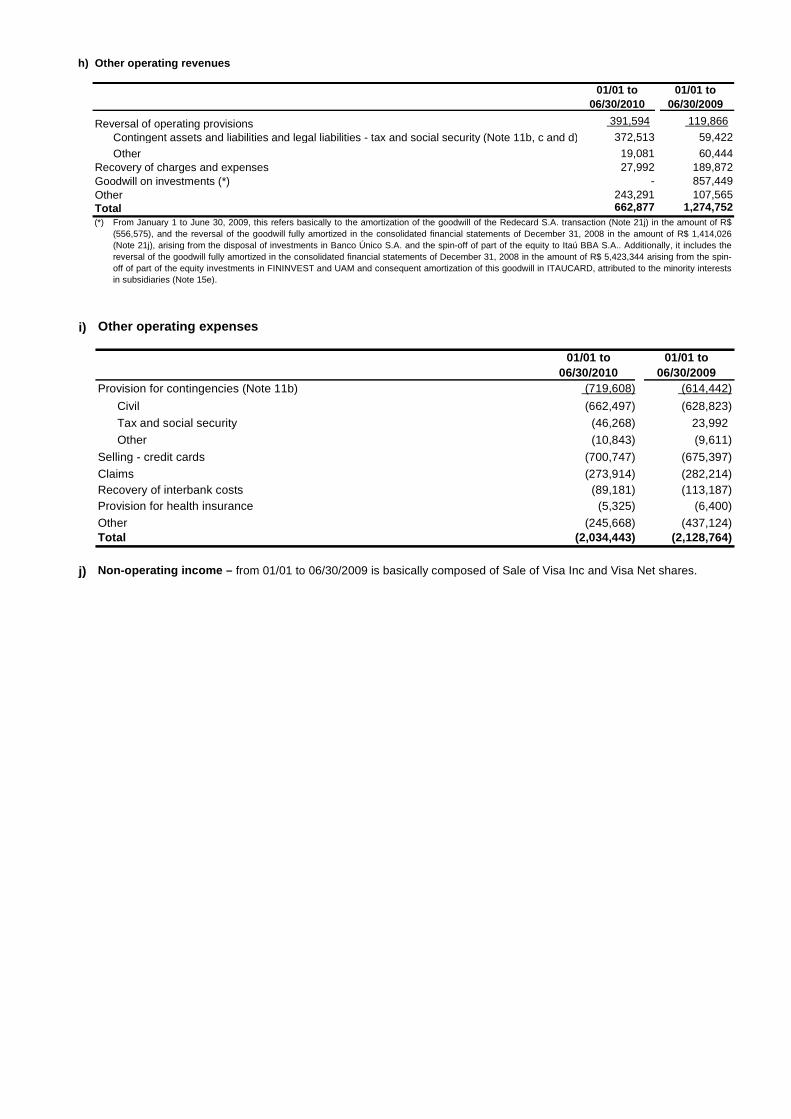

280,554 151,901 662,877 1,274,752

(2,034,443) (2,128,764) 8,147,071 8,057,281

11,886 172,902 8,158,957 8,230,183

(2,413,312) (3,839,757) (2,621,134) (3,708,776)

207,822 (130,981) (75,226) (69,287)

(2,008,578) 2,053,372

3,661,841 6,374,511

4,095,427,813 4,095,427,8130.89 1.56 9.05 7.75

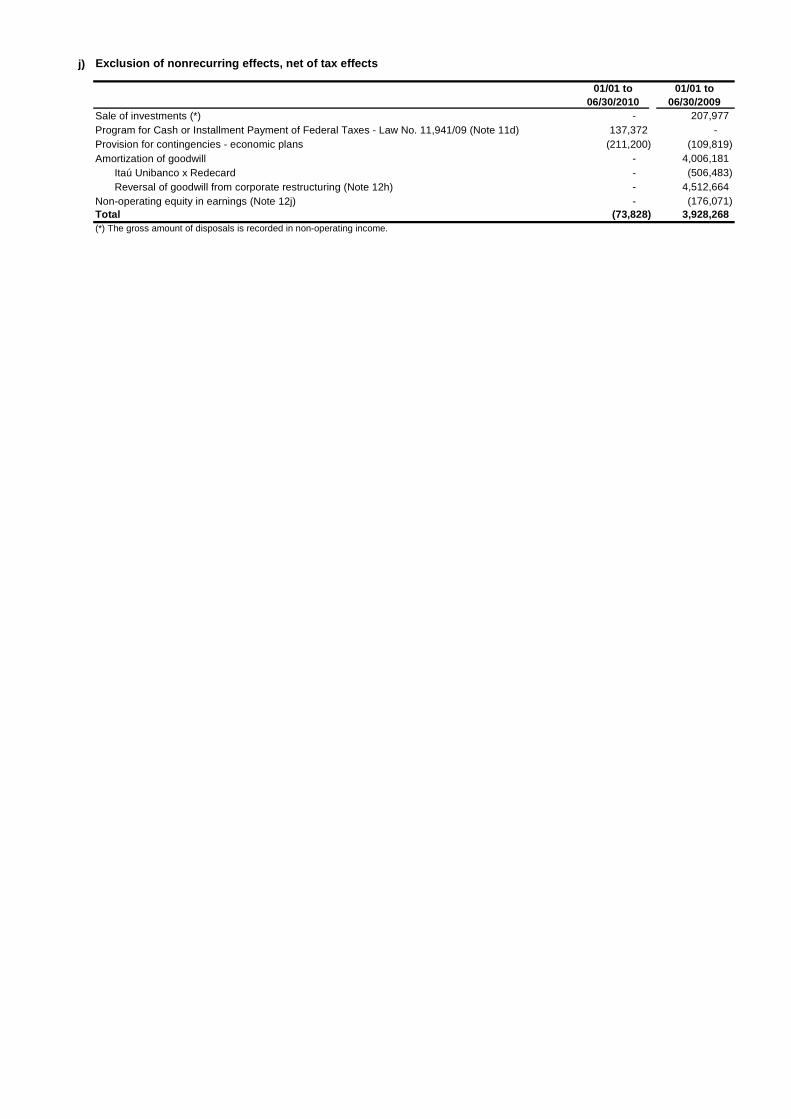

73,828 (3,928,268) 3,735,669 2,446,243

0.91 0.60 NET INCOME PER SHARE - R$

BOOK VALUE PER SHARE - R$

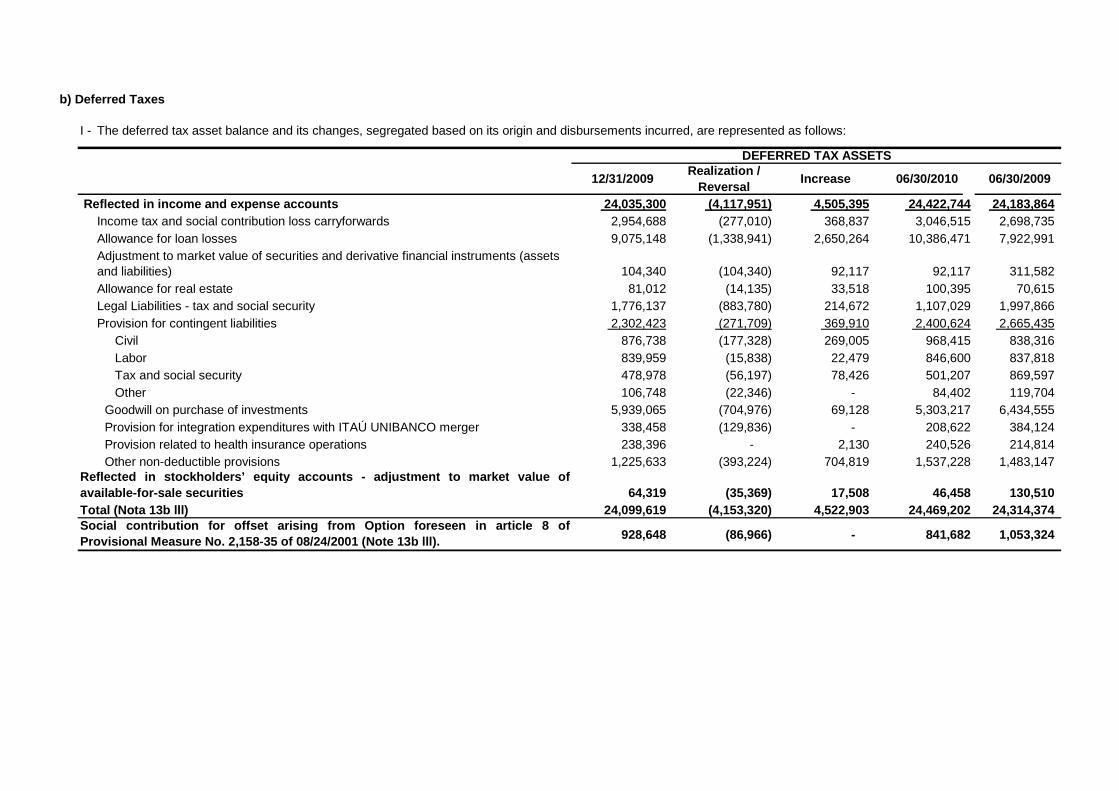

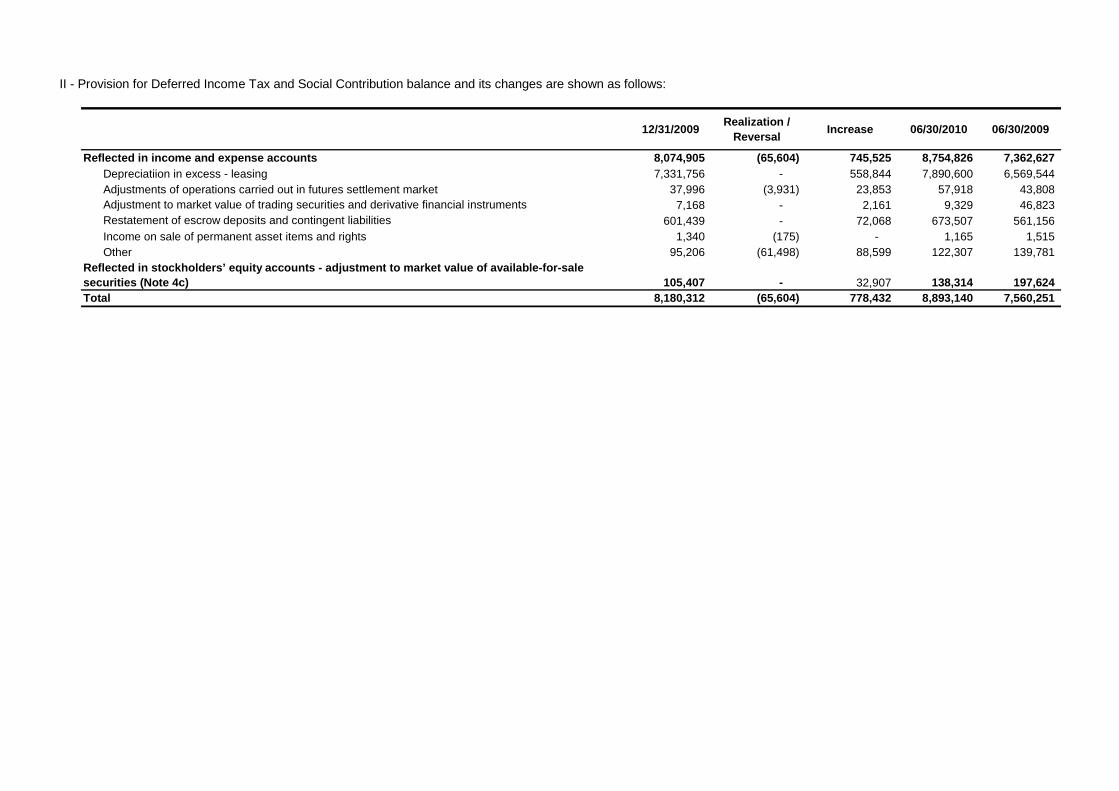

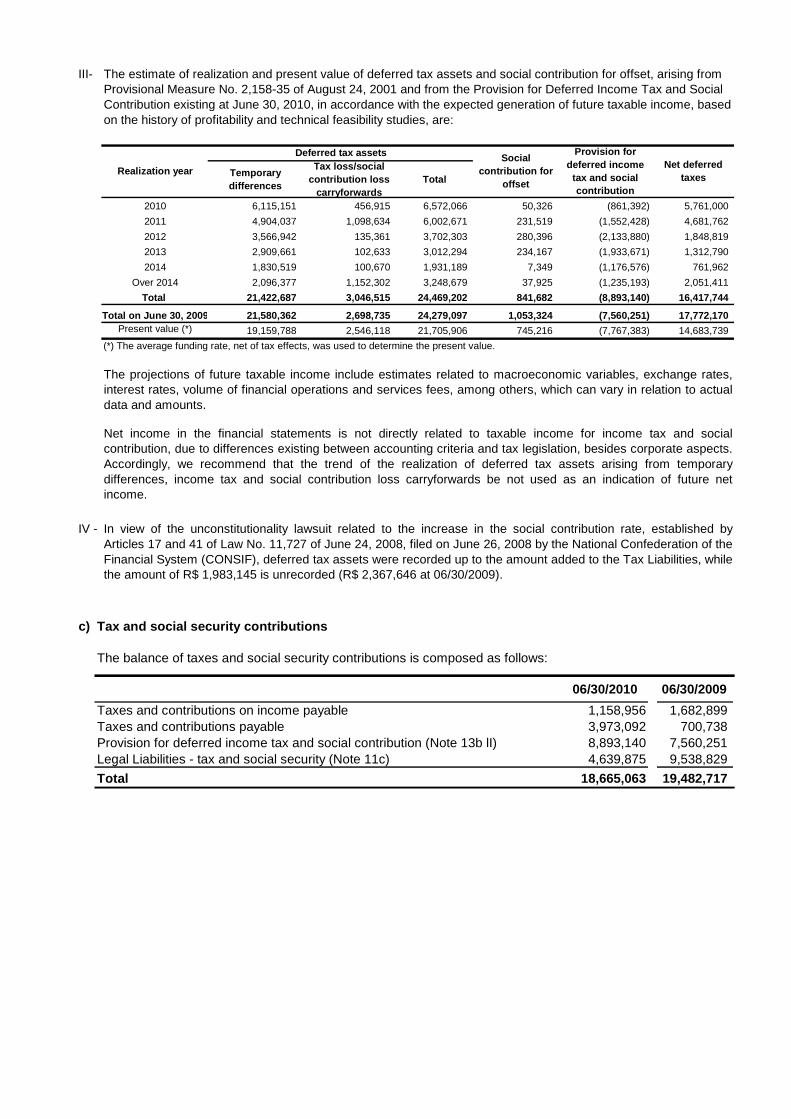

INCOME TAX AND SOCIAL CONTRIBUTION (Notes 4o and 13 a I)Due on operations for the period

NET INCOME

NUMBER OF SHARES (Note 15a)

MINORITY INTEREST IN SUBSIDIARIES (Note 15e)

Related to temporary differences

INCOME BEFORE TAXES ON INCOME AND PROFIT SHARING

NET INCOME PER SHARE - R$

Other operating revenues (Note 12h)Other operating expenses (Note 12i)

OPERATING INCOMENON-OPERATING INCOME (Note 12j)

Money market

01/01 to 06/30/2009

INCOME FROM FINANCIAL OPERATIONS BEFORE LOAN LOSSESRESULT OF LOAN LOSSES

Loan, lease and other credit operationsINCOME FROM FINANCIAL OPERATIONS

01/01 to 06/30/2010

Securities and derivative financial instrumentsFinancial income from insurance, pension plan and capitalization operations (Note 10c)

OTHER OPERATING REVENUES (EXPENSES)Banking service fees (Note 12d)

Result from insurance, pension plan and capitalization operations (Note 10c)

ITAÚ UNIBANCO S.A.Consolidated Statement of Income (Note 2a)(In thousands of reais)

Foreign exchange operationsCompulsory deposits

EXPENSES ON FINANCIAL OPERATIONS

Financial expenses on technical provisions for pension plan and capitalization (Note 10c)Borrowings and onlending

Income from recovery of credits written off as loss (Note 7e)GROSS INCOME FROM FINANCIAL OPERATIONS

Expenses for allowance for loan losses (Note 7d)

Income from bank charges (Note 12e)

The accompanying notes are an integral part of these financial statements.

EXCLUSION OF NONRECURRING EFFECTS (Note 20j)NET INCOME WITHOUT NONRECURRING EFFECTS

Other administrative expenses (Note 12g)Tax expenses (Note 4o and 13a II)Equity in earnings of affiliates (Note 14a lI)

Personnel expenses (Note 12f)

PROFIT SHARING – Management members - Statutory – L aw No. 6,404 of 12/15/1976

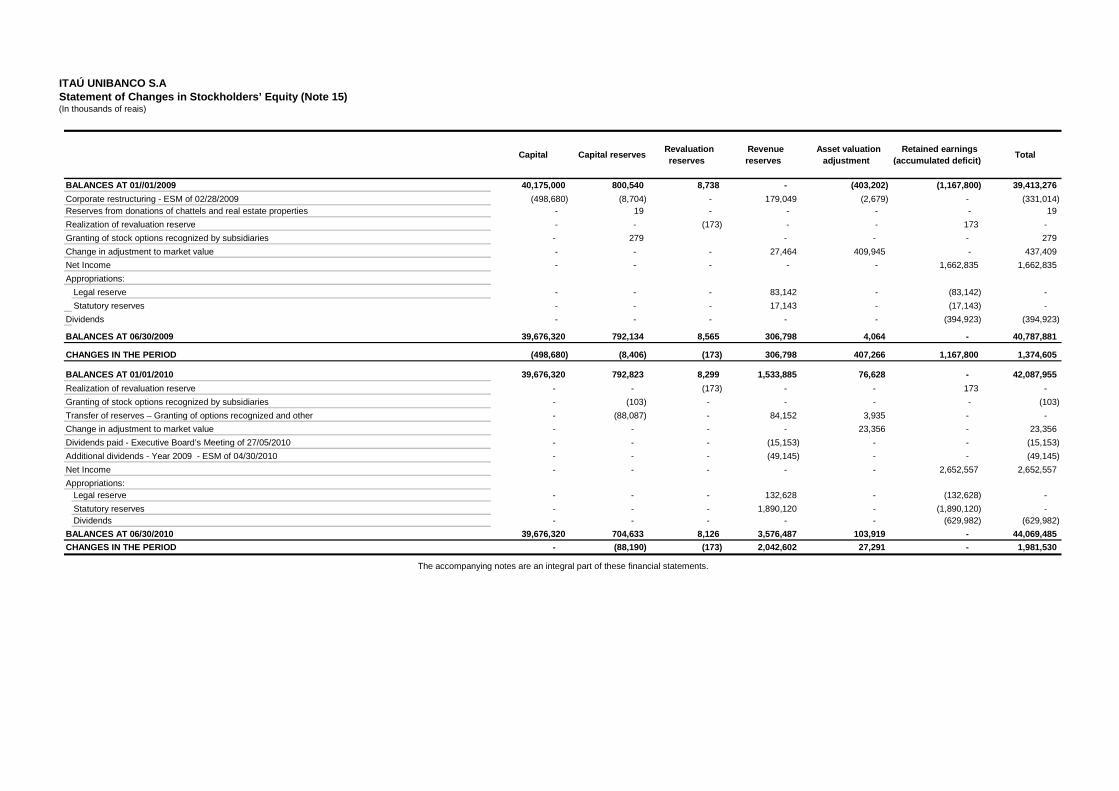

Capital Capital reserves Revaluation

reserves Revenue reserves

Asset valuation adjustment

Retained earnings (accumulated deficit)

Total

40,175,000 800,540 8,738 - (403,202) (1,167,800) 39,413,276

(498,680) (8,704) - 179,049 (2,679) - (331,014) - 19 - - - - 19

- - (173) - - 173 -

Granting of stock options recognized by subsidiaries - 279 - - - 279

- - - 27,464 409,945 - 437,409

- - - - - 1,662,835 1,662,835

Legal reserve - - - 83,142 - (83,142) -

Statutory reserves - - - 17,143 - (17,143) -

Dividends - - - - - (394,923) (394,923)

39,676,320 792,134 8,565 306,798 4,064 - 40,787,881

(498,680) (8,406) (173) 306,798 407,266 1,167,800 1,374,605

39,676,320 792,823 8,299 1,533,885 76,628 - 42,087,955

- - (173) - - 173 -

- (103) - - - - (103)

- (88,087) - 84,152 3,935 - -

- - - - 23,356 - 23,356

- - - (15,153) - - (15,153)

- - - (49,145) - - (49,145)

- - - - - 2,652,557 2,652,557

Legal reserve - - - 132,628 - (132,628) -

Statutory reserves - - - 1,890,120 - (1,890,120) - Dividends - - - - - (629,982) (629,982)

39,676,320 704,633 8,126 3,576,487 103,919 - 44,069,485

- (88,190) (173) 2,042,602 27,291 - 1,981,530

The accompanying notes are an integral part of these financial statements.

Net Income

Appropriations:

BALANCES AT 06/30/2010

CHANGES IN THE PERIOD

Transfer of reserves – Granting of options recognized and other

Change in adjustment to market value

Dividends paid - Executive Board’s Meeting of 27/05/2010

Additional dividends - Year 2009 - ESM of 04/30/2010

Realization of revaluation reserve

Granting of stock options recognized by subsidiaries

BALANCES AT 01/01/2010

Realization of revaluation reserve

BALANCES AT 01//01/2009

Corporate restructuring - ESM of 02/28/2009 Reserves from donations of chattels and real estate properties

Change in adjustment to market value

Net Income

CHANGES IN THE PERIOD

BALANCES AT 06/30/2009

Appropriations:

ITAÚ UNIBANCO S.A

(In thousands of reais)Statement of Changes in Stockholders’ Equity (Note 15)

01/01 to 06/30/2010

01/01 to 06/30/2009

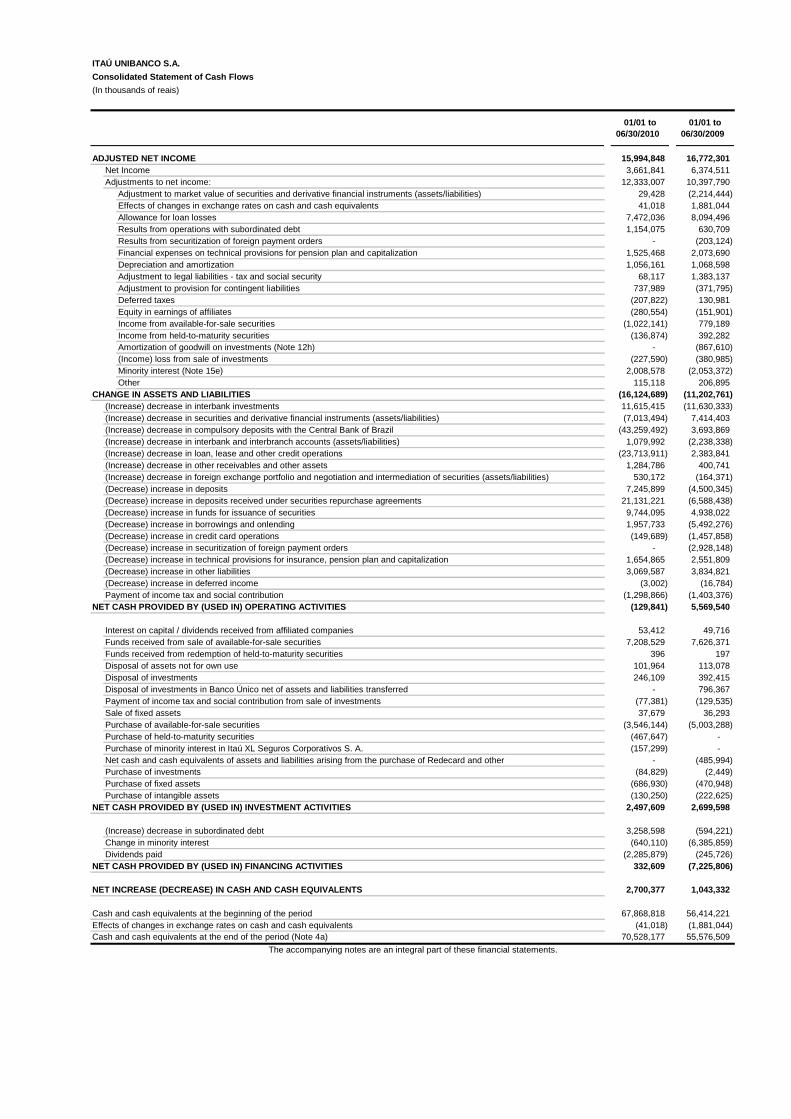

15,994,848 16,772,301 3,661,841 6,374,511

12,333,007 10,397,790Adjustment to market value of securities and derivative financial instruments (assets/liabilities) 29,428 (2,214,444)Effects of changes in exchange rates on cash and cash equivalents 41,018 1,881,044Allowance for loan losses 7,472,036 8,094,496Results from operations with subordinated debt 1,154,075 630,709Results from securitization of foreign payment orders - (203,124)Financial expenses on technical provisions for pension plan and capitalization 1,525,468 2,073,690Depreciation and amortization 1,056,161 1,068,598Adjustment to legal liabilities - tax and social security 68,117 1,383,137Adjustment to provision for contingent liabilities 737,989 (371,795)Deferred taxes (207,822) 130,981Equity in earnings of affiliates (280,554) (151,901)Income from available-for-sale securities (1,022,141) 779,189Income from held-to-maturity securities (136,874) 392,282Amortization of goodwill on investments (Note 12h) - (867,610)(Income) loss from sale of investments (227,590) (380,985)Minority interest (Note 15e) 2,008,578 (2,053,372)Other 115,118 206,895

(16,124,689) (11,202,761) 11,615,415 (11,630,333) (7,013,494) 7,414,403

(43,259,492) 3,693,869 1,079,992 (2,238,338)

(23,713,911) 2,383,841 1,284,786 400,741

530,172 (164,371) 7,245,899 (4,500,345)

21,131,221 (6,588,438) 9,744,095 4,938,022 1,957,733 (5,492,276) (149,689) (1,457,858)

- (2,928,148)(Decrease) increase in technical provisions for insurance, pension plan and capitalization 1,654,865 2,551,809

3,069,587 3,834,821(Decrease) increase in deferred income (3,002) (16,784)

(1,298,866) (1,403,376) (129,841) 5,569,540

Interest on capital / dividends received from affiliated companies 53,412 49,716Funds received from sale of available-for-sale securities 7,208,529 7,626,371Funds received from redemption of held-to-maturity securities 396 197Disposal of assets not for own use 101,964 113,078Disposal of investments 246,109 392,415Disposal of investments in Banco Único net of assets and liabilities transferred - 796,367

(77,381) (129,535)Sale of fixed assets 37,679 36,293Purchase of available-for-sale securities (3,546,144) (5,003,288)Purchase of held-to-maturity securities (467,647) -Purchase of minority interest in Itaú XL Seguros Corporativos S. A. (157,299) -Net cash and cash equivalents of assets and liabilities arising from the purchase of Redecard and other - (485,994)Purchase of investments (84,829) (2,449)Purchase of fixed assets (686,930) (470,948)Purchase of intangible assets (130,250) (222,625)

2,497,609 2,699,598

(Increase) decrease in subordinated debt 3,258,598 (594,221)Change in minority interest (640,110) (6,385,859)Dividends paid (2,285,879) (245,726)

NET CASH PROVIDED BY (USED IN) FINANCING ACTIVITIES 332,609 (7,225,806)

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENT S 2,700,377 1,043,332

67,868,818 56,414,221Effects of changes in exchange rates on cash and cash equivalents (41,018) (1,881,044)

70,528,177 55,576,509

Payment of income tax and social contribution

Payment of income tax and social contribution from sale of investments

NET CASH PROVIDED BY (USED IN) INVESTMENT ACTIVITIE S

Cash and cash equivalents at the beginning of the period

NET CASH PROVIDED BY (USED IN) OPERATING ACTIVITIES

(Increase) decrease in interbank investments

ADJUSTED NET INCOME

Adjustments to net income:

(Decrease) increase in other liabilities

(Increase) decrease in other receivables and other assets

(Decrease) increase in securitization of foreign payment orders

(Decrease) increase in deposits received under securities repurchase agreements(Decrease) increase in funds for issuance of securities(Decrease) increase in borrowings and onlending(Decrease) increase in credit card operations

ITAÚ UNIBANCO S.A.

Consolidated Statement of Cash Flows

(In thousands of reais)

The accompanying notes are an integral part of these financial statements.

Cash and cash equivalents at the end of the period (Note 4a)

Net Income

(Increase) decrease in securities and derivative financial instruments (assets/liabilities)

(Increase) decrease in foreign exchange portfolio and negotiation and intermediation of securities (assets/liabilities)(Decrease) increase in deposits

(Increase) decrease in compulsory deposits with the Central Bank of Brazil(Increase) decrease in interbank and interbranch accounts (assets/liabilities)(Increase) decrease in loan, lease and other credit operations

CHANGE IN ASSETS AND LIABILITIES

ITAÚ UNIBANCO S.A.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FROM JANUARY 1 TO JUNE 30, 2010 AND 2009

(In thousands of Reais)

NOTE 1 - OPERATIONS

Itaú Unibanco S.A. (ITAU UNIBANCO) is a publicly-held company which, together with its subsidiary and affiliated companies, operates in Brazil and abroad, with all types of banking activities, through its commercial, investment, consumer credit, real estate loan, finance and investment credit, and lease portfolios, including foreign exchange operations, and other complementing activities, with emphasis on Insurance, Private Pension Plans, Capitalization, Securities Brokerage and Administration of Credit Cards, Consortia, Investment Funds and Managed Portfolios.

NOTE 2 – PRESENTATION OF THE FINANCIAL STATEMENTS a) Presentation of the Financial Statements

The financial statements of ITAÚ UNIBANCO and its subsidiaries (ITAÚ UNIBANCO CONSOLIDATED) have been prepared in accordance with accounting principles established by the Brazilian Corporate Law, including the amendments produced by Laws No. 11,638, of December 28, 2007, and No. 11,941 of May 27, 2009, in conformity, when applicable, with the instructions issued by the Central Bank of Brazil (BACEN), the National Monetary Council (CMN), the Superintendency of Private Insurance (SUSEP) and the National Council of Private Insurance (CNSP), which include the use of estimates necessary to calculate accounting provisions. On May 12, 2010 SUSEP approved the contract signed on November 12, 2009 related to the acquisition by ITAÚ UNIBANCO HOLDING of a minority interest in the subsidiary company Itaú XL Seguros Corporativos S.A. for the amount of R$ 157,299, giving rise to a goodwill of R$ 24,700.

In order to enable the proper analysis of net income, the heading “Net income without nonrecurring effects” is presented below the Consolidated Statement of Income, and this effect is highlighted in a heading called “Exclusion of nonrecurring effects” (Note 20j). As set forth in the sole paragraph of article 7 of BACEN Circular No. 3,068, of November 8, 2001, securities classified as trading securities (Note 4c) are presented in the Balance Sheet under Current Assets regardless of their maturity dates. Lease Operations are presented, at present value, in the Balance Sheet, and the related income and expenses, which represent the financial result of these operations, are presented, grouped together, under loan, lease and other credit operations in the Statement of Income. Advances on exchange contracts are reclassified from Other Liabilities – Foreign Exchange Portfolio. The foreign exchange result is presented on an adjusted basis, with the reclassification of expenses and income, in order to represent exclusively the impact of variations and differences of rates on the balance sheet accounts denominated in foreign currencies.

b) Convergence into international accounting standa rds

The CMN Resolution No. 3,786, of September 24, 2009, and BACEN Circular No. 3,472, of October 23, 2009, established that from December 31, 2010 the financial institutions shall prepare and annually report their consolidated financial statements adopting the international financial reporting standards according to the pronouncements issued by the International Accounting Standard Board (IASB), translated into the Portuguese language by a Brazilian company registered with the International Accounting Standards Committee Foundation (IASC Foundation). The accounting pronouncements issued by the Accounting Pronouncements Committee (CPC) and the respective international standards of IASB that will be adopted in the consolidated financial statements until the end of 2010 and may impact the stockholders’ equity and/or results are as follows:

• CPC 2 (IAS 21) – Effects on changes in foreign exchange rates and conversion of financial statements: Effect on results from January 1 to June 30, 2010 (without effects on stockholders’ equity) for allocation of foreign exchange variation in the stockholders’ equity related to controlled companies with functional currency other than Real, basically represented by the Itaú Europa, Chile, Argentina, Uruguay and Paraguay units (Note 18).

• CPC 11 (IFRS 4) – Insurance contracts: Management does not expect significant effects; • CPC 15 (IFRS 3) – Business combinations: in the period from January 1 to June 30, 2010 there was not

any transaction that could exert significant effects; • CPC 24 (IAS 10) – Subsequent events: Dividends and interest on capital declared after the accounting

period to which the financial statements refer, if these are above the minimum mandatory dividend, they shall be reversed with effects on stockholders’ equity (Note 15b);

• CPC 32 (IAS 12) – Taxes on Income: Recognition of a credit in the stockholders’ equity of the opening

balance sheet of an amount of deferred tax assets not recorded according to Note 13b IV;

• CPC 33 (IAS 19) – Employee benefits: recognition of a credit in the stockholders’ equity of opening balance sheet of the surplus of benefit plans according to Note 17c; and

• CPC 38 (IAS 39) – Financial Instruments: Recognition and Measurement – Loss on recoverable amount

for not receiving financial assets: Review of the procedures adopted for setting up the Allowance for Loan Losses. Management does not expect an amount above that recorded in the allowance.

The other pronouncements shall basically impact the disclosure of information. c) Consolidation

As set forth in paragraph 1, article 2, of BACEN Circular No. 2,804, of February 11, 1998, the financial statements of ITAÚ UNIBANCO CONSOLIDATED comprise the consolidation of its foreign branches and subsidiaries. Intercompany transactions and balances and results have been eliminated on consolidation. The investments held by consolidated companies in Exclusive Investment Funds are consolidated. The investments in these fund portfolios are classified by type of transaction and were distributed by type of security, in the same categories in which these securities had been originally allocated. The effects of the Foreign Exchange Variation on investments abroad are classified in the heading Securities and Derivative Financial Instruments in the Statement of Income, including the comparative figures. The difference in Net Income and Stockholders’ Equity between ITAÚ UNIBANCO and ITAÚ UNIBANCO CONSOLIDATED (Note 15d) results from the elimination of unrealized profits arising from transactions between the parent company and consolidated companies, and from the adoption of different criteria for the amortization of goodwill originated on purchase of investments, net of the respective deferred tax assets: In ITAÚ UNIBANCO, the goodwill recorded in subsidiaries, mainly originated from the ITAÚ UNIBANCO merger, is being amortized based on the expected future profitability and appraisal reports or upon realization of the investment, according to the rules and guidance from CMN and BACEN. In ITAÚ UNIBANCO CONSOLIDATED, this goodwill was fully amortized in the periods when these investments were made, in order to: a) permit better comparability with previous periods’ consolidated financial statements; and b) permit measuring Net Income and Stockholders’ Equity based on conservative criteria. From January 1, 2010, the goodwill originated from the purchase of investments is no longer fully amortized in the consolidated financial statements, for purposes of comparability of the current accounting practices with the international financial reporting standards.

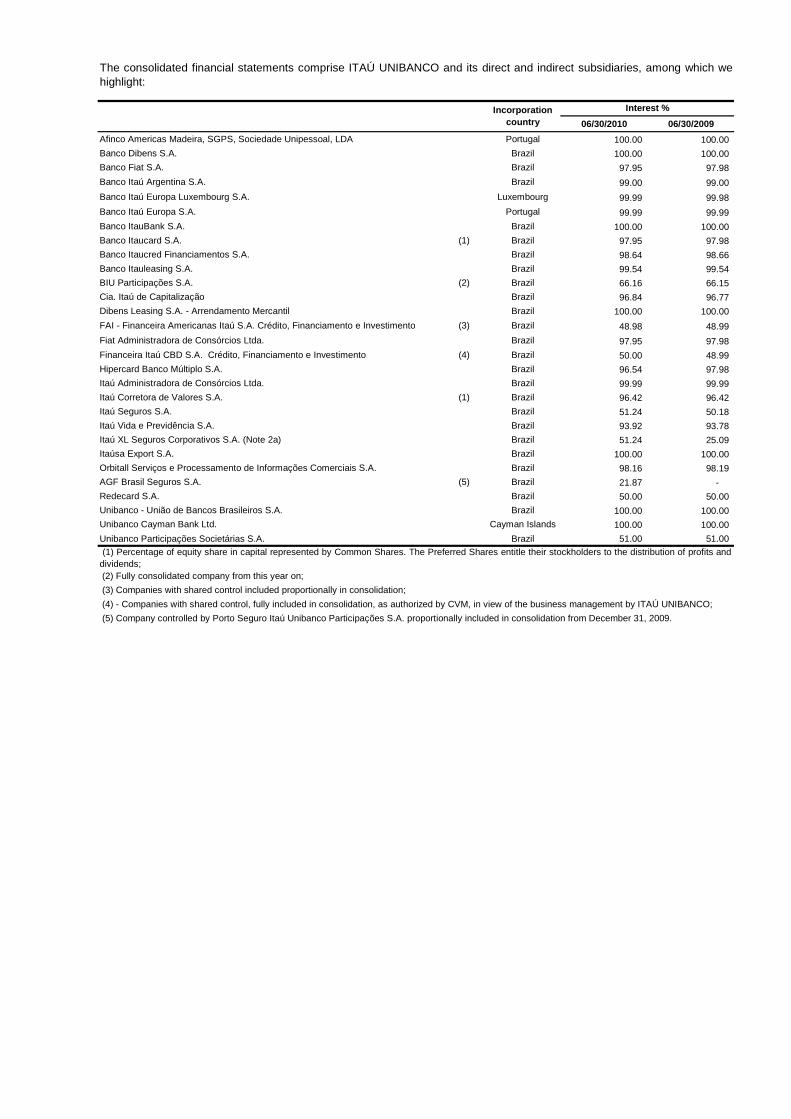

06/30/2010 06/30/2009

Afinco Americas Madeira, SGPS, Sociedade Unipessoal, LDA Portugal 100.00 100.00

Banco Dibens S.A. Brazil 100.00 100.00

Banco Fiat S.A. Brazil 97.95 97.98

Banco Itaú Argentina S.A. Brazil 99.00 99.00

Banco Itaú Europa Luxembourg S.A. Luxembourg 99.99 99.98

Banco Itaú Europa S.A. Portugal 99.99 99.99

Banco ItauBank S.A. Brazil 100.00 100.00

Banco Itaucard S.A. (1) Brazil 97.95 97.98

Banco Itaucred Financiamentos S.A. Brazil 98.64 98.66

Banco Itauleasing S.A. Brazil 99.54 99.54

BIU Participações S.A. (2) Brazil 66.16 66.15

Cia. Itaú de Capitalização Brazil 96.84 96.77

Dibens Leasing S.A. - Arrendamento Mercantil Brazil 100.00 100.00

FAI - Financeira Americanas Itaú S.A. Crédito, Financiamento e Investimento (3) Brazil 48.98 48.99

Fiat Administradora de Consórcios Ltda. Brazil 97.95 97.98

Financeira Itaú CBD S.A. Crédito, Financiamento e Investimento (4) Brazil 50.00 48.99

Hipercard Banco Múltiplo S.A. Brazil 96.54 97.98

Itaú Administradora de Consórcios Ltda. Brazil 99.99 99.99

Itaú Corretora de Valores S.A. (1) Brazil 96.42 96.42

Itaú Seguros S.A. Brazil 51.24 50.18

Itaú Vida e Previdência S.A. Brazil 93.92 93.78

Itaú XL Seguros Corporativos S.A. (Note 2a) Brazil 51.24 25.09

Itaúsa Export S.A. Brazil 100.00 100.00

Orbitall Serviços e Processamento de Informações Comerciais S.A. Brazil 98.16 98.19

AGF Brasil Seguros S.A. (5) Brazil 21.87 -

Redecard S.A. Brazil 50.00 50.00

Unibanco - União de Bancos Brasileiros S.A. Brazil 100.00 100.00

Unibanco Cayman Bank Ltd. Cayman Islands 100.00 100.00

Unibanco Participações Societárias S.A. Brazil 51.00 51.00

(5) Company controlled by Porto Seguro Itaú Unibanco Participações S.A. proportionally included in consolidation from December 31, 2009.

(4) - Companies with shared control, fully included in consolidation, as authorized by CVM, in view of the business management by ITAÚ UNIBANCO;

(3) Companies with shared control included proportionally in consolidation;

The consolidated financial statements comprise ITAÚ UNIBANCO and its direct and indirect subsidiaries, among which wehighlight:

(2) Fully consolidated company from this year on;

Interest %

(1) Percentage of equity share in capital represented by Common Shares. The Preferred Shares entitle their stockholders to the distribution of profits anddividends;

Incorporation country

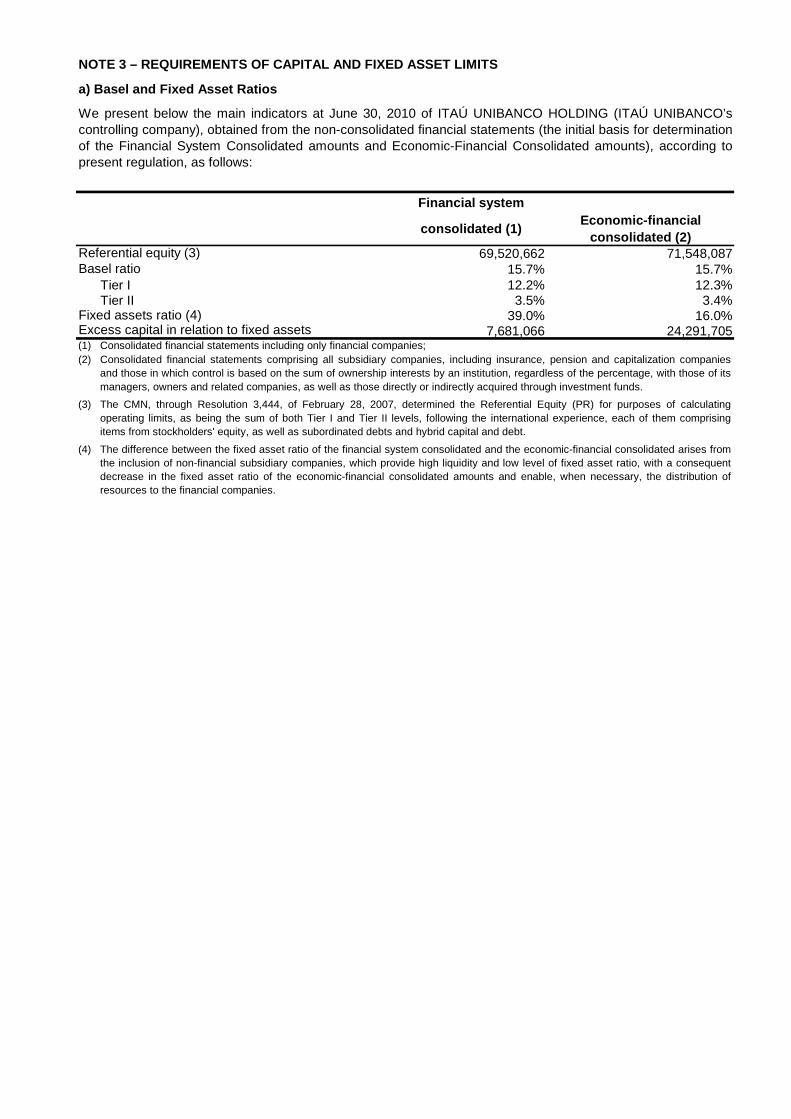

Financial system

consolidated (1)Economic-financial

consolidated (2)69,520,662 71,548,087

15.7% 15.7%Tier I 12.2% 12.3%Tier II 3.5% 3.4%

39.0% 16.0%7,681,066 24,291,705

(1)(2)

(3)

(4)

NOTE 3 – REQUIREMENTS OF CAPITAL AND FIXED ASSET LI MITS

a) Basel and Fixed Asset Ratios

The CMN, through Resolution 3,444, of February 28, 2007, determined the Referential Equity (PR) for purposes of calculatingoperating limits, as being the sum of both Tier I and Tier II levels, following the international experience, each of them comprisingitems from stockholders' equity, as well as subordinated debts and hybrid capital and debt.

Referential equity (3)Basel ratio

We present below the main indicators at June 30, 2010 of ITAÚ UNIBANCO HOLDING (ITAÚ UNIBANCO’scontrolling company), obtained from the non-consolidated financial statements (the initial basis for determinationof the Financial System Consolidated amounts and Economic-Financial Consolidated amounts), according topresent regulation, as follows:

The difference between the fixed asset ratio of the financial system consolidated and the economic-financial consolidated arises fromthe inclusion of non-financial subsidiary companies, which provide high liquidity and low level of fixed asset ratio, with a consequentdecrease in the fixed asset ratio of the economic-financial consolidated amounts and enable, when necessary, the distribution ofresources to the financial companies.

Fixed assets ratio (4)Excess capital in relation to fixed assets

Consolidated financial statements including only financial companies;Consolidated financial statements comprising all subsidiary companies, including insurance, pension and capitalization companiesand those in which control is based on the sum of ownership interests by an institution, regardless of the percentage, with those of itsmanagers, owners and related companies, as well as those directly or indirectly acquired through investment funds.

NOTE 4 – SUMMARY OF THE MAIN ACCOUNTING PRACTICES a) Cash and Cash Equivalents – For purposes of Consolidated Statement of Cash Flows, it includes cash and

current accounts in banks (considered in the heading cash and cash equivalents), interbank deposits and securities purchased under agreements to resell - Funded position that have original maturities of up to 90 days or less.

b) Interbank investments, remunerated restricted cr edits – Brazilian Central Bank, remunerated

deposits, deposits received under securities repurc hase agreements, funds from acceptance and issuance of securities, borrowings and onlendings a nd other receivables and payables - Transactions subject to monetary correction and foreign exchange variation and operations with fixed charges are recorded at present value, net of the transaction costs incurred, calculated “pro rata die” based on the effective rate of transactions, according to CVM Resolution No. 556 of November 12, 2008.

c) Securities - Recorded at cost of acquisition restated by the index and/or effective interest rate and

presented in the Balance Sheet, according to BACEN Circular No. 3,068, of November 8, 2001. Securities are classified into the following categories:

• Trading securities – acquired to be actively and frequently traded, and adjusted to market value, with a

contra-entry to the results for the period; • Available-for-sale securities – securities that can be negotiated but are not acquired to be actively and

frequently traded. They are adjusted to their market value with a contra-entry to an account disclosed in stockholders’ equity;

• Held-to-maturity securities – securities, except for non-redeemable shares, for which the bank has the

financial condition and intends or is required to hold them in the portfolio up to their maturity, are recorded at cost of acquisition, or market value, whenever these are transferred from another category. The securities are adjusted up to their maturity date, not being adjusted to market value.

Gains and losses on available-for-sale securities, when realized, are recognized at the trading date in the statement of income, with a contra-entry to a specific stockholders’ equity account. Decreases in the market value of available-for-sale and held-to-maturity securities below their related costs, resulting from non-temporary reasons, are recorded in results as realized losses.

d) Derivative financial instruments - These are classified on the date of their acquisition, according to management's intention of using them either as a hedge or not, according to BACEN Circular No. 3,082, of January 30, 2002. Transactions involving financial instruments, carried out upon the client's request, for their own account, or which do not comply with hedging criteria (mainly derivatives used to manage the overall risk exposure) are stated at market value, including realized and unrealized gains and losses, which are recorded directly in the statement of income.

The derivatives used for protection against risk exposure or to modify the characteristics of financial assets and liabilities, which have changes in market value are highly associated with those of the items being protected at the beginning and throughout the duration of the contract, and which are found effective to reduce the risk-related to the exposure being protected, are classified as a hedge, in accordance with their nature:

• - Market Value Hedge – Financial assets and liabilities, as well as their related financial instruments, are

accounted for at their market value plus realized and unrealized gains and losses, which are recorded directly in the statement of income;

• - Cash Flow Hedge - The effective amount of the hedge of assets and liabilities, as well as their related

financial instruments, are accounted for at their market value plus realized and unrealized gains and losses, net of tax effects, when applicable, and recorded in a specific account in stockholders’ equity. The ineffective portion of hedge is recorded directly in the statement of income.

e) Loan, lease and other credit operations (Operati ons with credit granting characteristics) - these transactions are recorded at present value and calculated “pro rata die” based on the variation of the contracted index, and are recorded on the accrual basis until the 60th day overdue in financial companies. After the 60th day, income is recognized upon the effective receipt of installments. Credit card operations include receivables arising from purchases made by cardholders. The funds related to these amounts are included in Other Liabilities – Credit Card Operations.

f) Allowance for loan losses - the balance of the allowance for loan losses was recorded based on the credit

risk analysis at an amount considered sufficient to cover loan losses according to the rules determined by CMN Resolution No. 2,682 of December 21, 1999, among which are:

• Provisions are recorded from the date loans are granted, based on the client’s risk rating and on the

periodic quality evaluation of clients and industries, and not only in the event of default; • Based exclusively on delinquency, write-offs of credit operations against loss may be carried out 360

days after the due date of the credit or 540 days for operations that mature after a period of 36 months. Additionally, in this period, other factors related to analysis of the quality of the client/loan may generate write-offs before these periods.

g) Other assets - these assets are mainly comprised by assets held for sale relating to real estates available

for sale, own real estate not in use or received as payment in kind, which are adjusted to market value through the set-up of a provision, according to current regulations; reinsurance unearned premiums (Note 4m I); and prepaid expenses, corresponding to disbursements, the benefit of which will occur in future periods.

h) Investments - In subsidiary and affiliated companies, investments are accounted for under the equity

method. The consolidated financial statements of foreign branches and subsidiaries are adapted to comply with Brazilian accounting practices and converted into Reais. Other investments are recorded at cost, and adjusted to market value by setting up a provision in accordance with current standards.

i) Fixed assets - These assets are stated at cost of acquisition or construction, less accumulated depreciation,

restated up to December 31, 2007, when applicable. For insurance, pension plan and capitalization operations, property and equipment are adjusted to market value supported by appraisal reports. They correspond to rights related to tangible assets intended for maintenance of the company’s operations or exercised for such purposes, including assets arising from transactions that transfer to the company their benefits, risks and controls. The items acquired through Lease contracts are recorded according to CVM Resolution No. 554, of November 12, 2008, as contra-entry to Lease obligations. Depreciation is calculated using the straight-line method, based on monetarily corrected cost, at the following annual rates:

Real estate in use 4 % to 8 % Leasehold improvements From 10% Installations, furniture, equipment and security, transportation and communication systems 10 % to 25 % EDP systems 20 % to 50 %

j) Operating leases – leased assets are stated at cost of acquisition less accumulated depreciation. The

depreciation of leased assets is recognized under the straight-line method, based on their usual useful lives, taking into account that the useful life shall be decreased by 30% should it meet the conditions provided for by the Ordinance No. 113 of February 26, 1988 issued by the Ministry of Finance. Receivables are recorded in lease receivable at the contractual amount, with contra-entry to unearned income accounts. The recognition in income will occur on the due date of the installments.

k) Intangible assets – correspond to rights acquired whose subjects are intangible assets intended for

maintenance in the company or exercised for such purpose, according to CMN Resolution No. 3,642, of November 26, 2008. They are composed of rights acquired to credit payrolls and partnership agreements, amortized over the agreement terms, and software and customer portfolios, amortized over a term varying from five to ten years.

l) Reduction to the recoverable value of assets – a loss is recognized when there are clear evidences that assets are stated at a non-recoverable value. From 2008, this procedure started to be adopted annually at the end of each year.

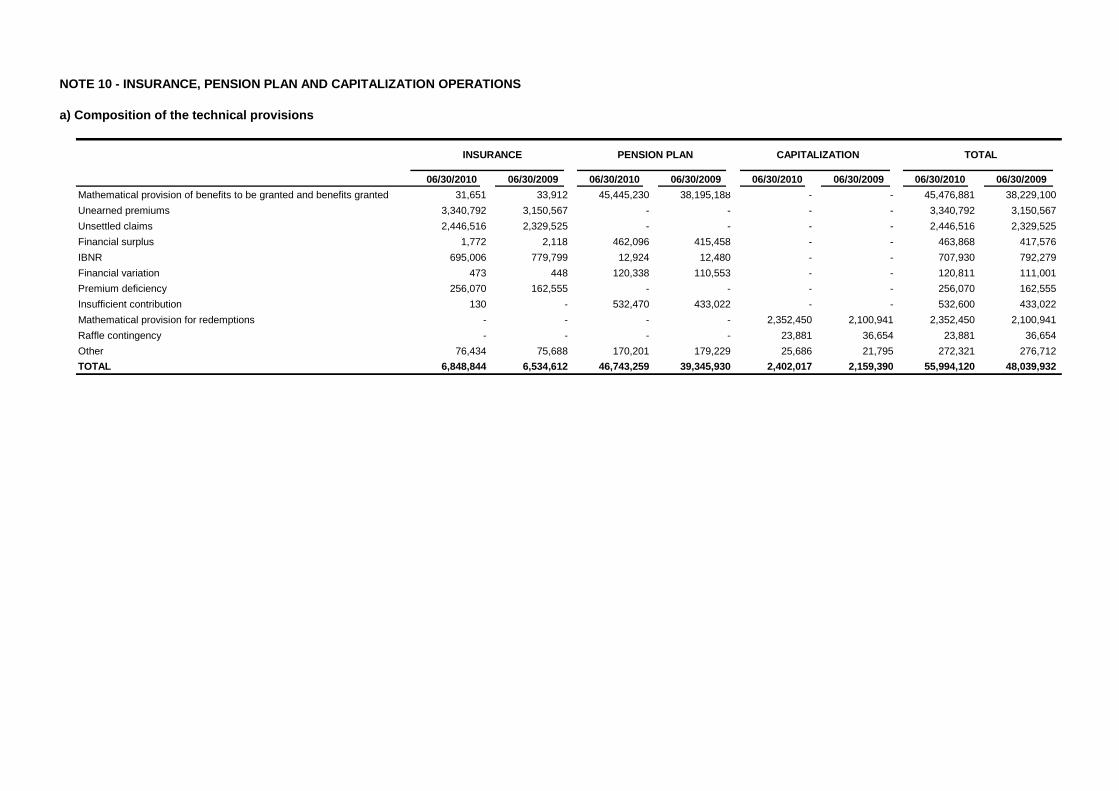

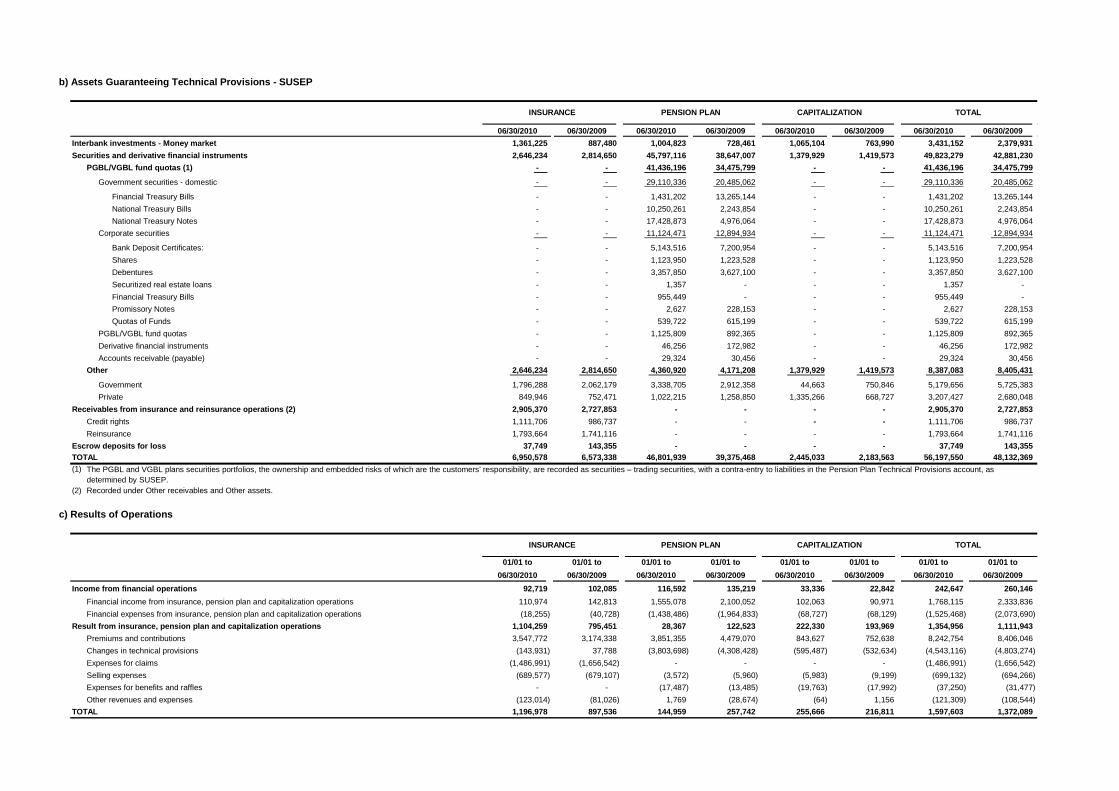

m) Insurance, pension plan and capitalization opera tions – Insurance premiums, acceptance coinsurance

and selling expenses are accounted for in accordance with the insurance effectiveness term, through the recognition and reversal of the provision for unearned premiums and deferred selling expenses. Interest arising from fractioning of insurance premiums is accounted for as incurred. Revenues from social security contributions, gross revenue from capitalization certificates and respective technical provisions are recognized upon receipt.

I - Credit from operations and other assets related to insurance and reinsurance operations:

• Insurance premiums receivable – Refer to installments of insurance premiums receivable, current and past due, in accordance with insurance policies issued.

• Reinsurance recoverable amounts – Refer to claims paid to the insured party pending recovery from

Reinsurer, installments of unsettled claims and incurred but not reported claims – Reinsurance (IBNR), classified in assets in accordance with the criteria established by CNSP Resolution No. 162, of December 26, 2006, as amended by CNSP Resolution No. 195, of December 16, 2008, and SUSEP Circular No. 379, of December 19, 2008.

• Reinsurance unearned premiums – recognized to determine the portion of reinsurance unearned

premiums, calculated “pro rata die”, and for risks not issued computed based on estimates, based on the actuarial technical study and in compliance with the criteria established by CNSP Resolution No. 162, of December 26, 2006, as amended by CNSP Resolution No. 195, of December 16, 2008, and SUSEP Circular No. 379, of December 19, 2008.

II - Technical provisions of insurance, pension pla n and capitalization – provisions are set up according

to the technical notes approved by SUSEP and criteria established by CNSP Resolution No. 162 of December 26, 2006 and the amendments introduced by CNSP Resolution No. 181 of December 19, 2007, and CNSP Resolution No. 195 of December 16, 2008.

II.I - Insurance:

• Provision for unearned premiums – recognized to determine unearned premiums related to the

risk coverage period, calculated pro rata die, and for risks not yet issued, calculated based on estimates, according to an actuarial technical study;

• Provision for premium deficiency – recognized according to the Technical Actuarial Note in case

of insufficient Provision for unearned premiums;

• Provision for unsettled claims – recognized based on claims of loss in an amount sufficient to cover future commitments, awaiting judicial decision, which amounts are determined by court-appointed experts and legal advisors that make assessments based on the insured amounts and technical regulations, taking into consideration the likelihood of unfavorable outcome to the insurance company;

• Provision for claims incurred but not reported (IBNR) – recognized for the estimated amount of

claims occurred for risks assumed in the portfolio but not reported.

II.II - Pension Plan and Individual life with livin g benefits – correspond to liabilities assumed such as retirement plans, disability, pension and annuity.

• Mathematical provisions for benefits to be granted and benefits granted – correspond to

commitments assumed with participants, but for which benefits are not yet due, and to those receiving the benefits, respectively;

• Provision for insufficient contribution – recognized in case of insufficient mathematical provisions;

• Provision for events occurred but not reported (IBNR) – recognized at the estimated amount of events occurred but not reported;

• Provision for financial surplus – recognized by the difference between the contributions adjusted

daily by the Investment Portfolio and the funds guaranteeing them, according to the plan’s regulation;

• Provision for financial variation – recognized according to the methodoloy provided for in the

Technical Actuarial Note in order to guarantee that the financial assets are sufficient to cover mathematical provisions.

II.III- Capitalization:

• Mathematical provision for redemptions – represents capitalization certificates received to be

redeemed;

• Provision for raffle contingencies – recognized according to the methodology provided for in the Technical Actuarial Note to cover the Provision for raffles in the event of insufficient funds.

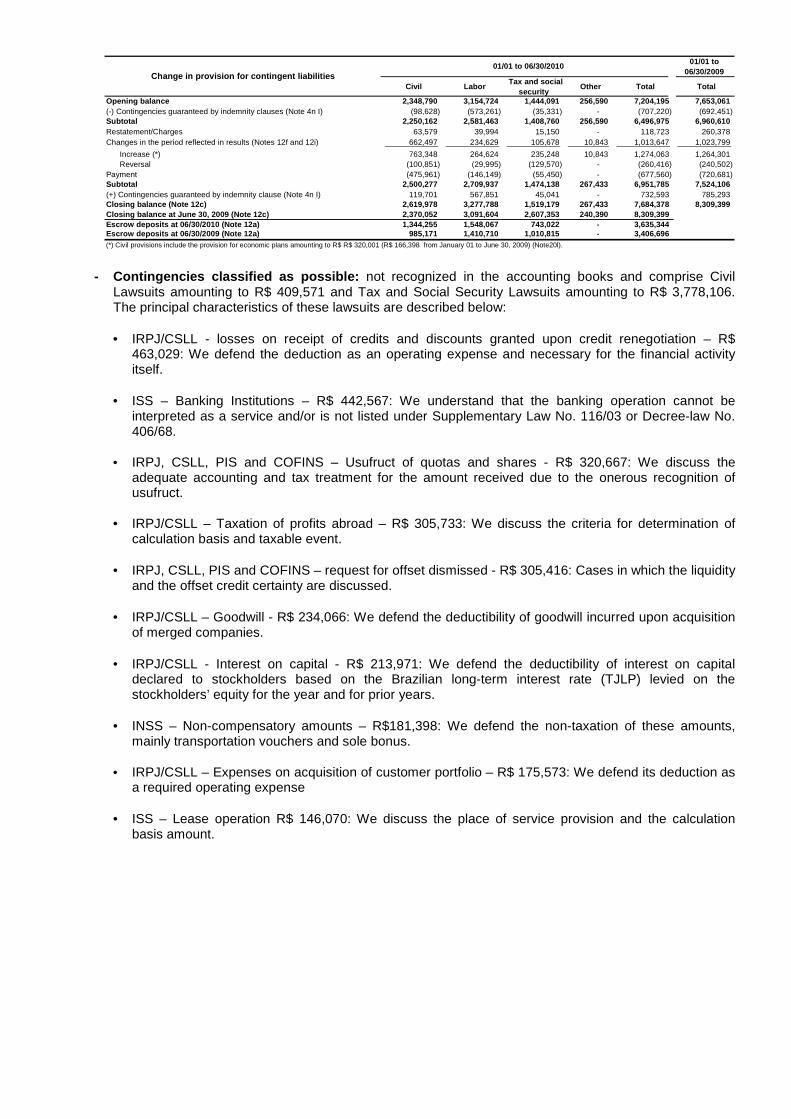

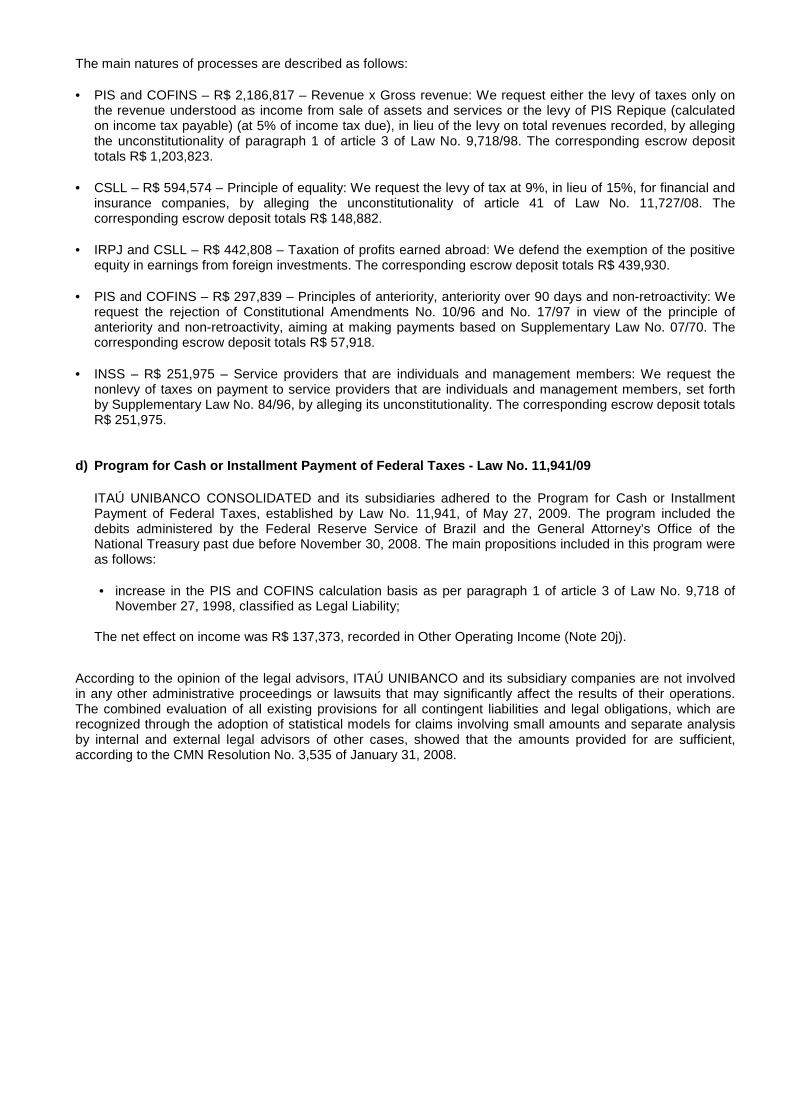

n) Contingent assets and liabilities and legal liab ilities – Tax and social security: assessed, recognized

and disclosed according to the provisions set forth in CMN Resolution No. 3,535 of January 31, 2008.

I - Contingent assets and liabilities

Refer to potential rights and obligations arising from past events, the occurrence of which is dependent upon future events. • Contingent assets: not recognized, except upon evidence ensuring a high reliability level of realization,

usually represented by claims awarded a final and unappealable judgment and confirmation of the recoverability of the claim through receipt of amounts or offset against another liability.

• Contingent liabilities: basically arise from administrative proceedings and lawsuits, inherent in the

normal course of business, filed by third parties, former employees and governmental bodies, in connection with civil, labor, tax and social security lawsuits and other risks. These contingencies are calculated based on conservative practices, being usually recorded based on the opinion of legal advisors and considering the probability that financial resources shall be required for settling the obligation, the amount of which may be estimated with sufficient certainty. Contingencies are classified either as probable, for which provisions are recognized; possible, which are disclosed but not recognized; or remote, for which recognition or disclosure are not required. Any contingent amounts are measured through the use of models and criteria which allow their adequate measurement, in spite of the uncertainty of their term and amounts.

Escrow deposits are restated in accordance with the current legislation.

Contingencies guaranteed by indemnity clauses in privatization processes and with liquidity are only recognized upon judicial notification with simultaneous recognition of receivables, without any effect on results.

II - Legal liabilities – tax and social security

Represented by amounts payable related to tax liabilities, the legality or constitutionality of which are subject to administrative or judicial defense, recognized at the full amount under discussion.

Liabilities and related escrow deposits are adjusted in accordance with the current legislation.

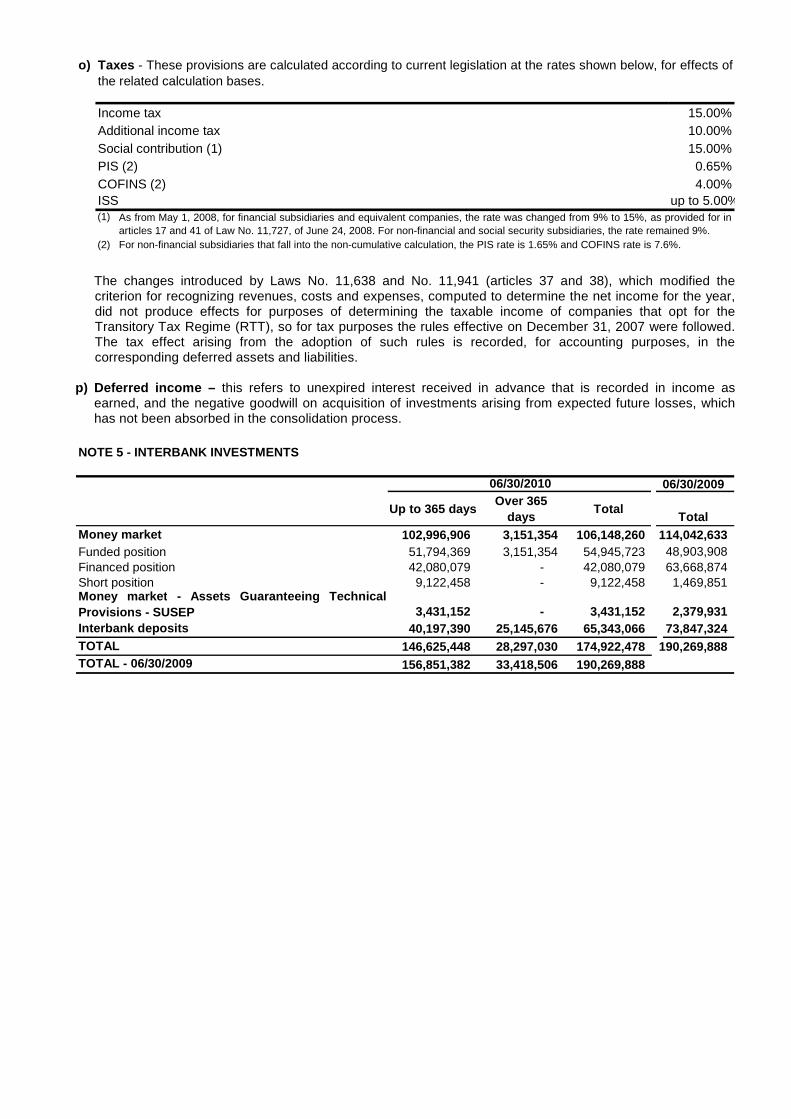

o)

15.00%10.00%15.00%

0.65%4.00%

up to 5.00% (1)

(2)

ISS

Income tax

As from May 1, 2008, for financial subsidiaries and equivalent companies, the rate was changed from 9% to 15%, as provided for inarticles 17 and 41 of Law No. 11,727, of June 24, 2008. For non-financial and social security subsidiaries, the rate remained 9%.For non-financial subsidiaries that fall into the non-cumulative calculation, the PIS rate is 1.65% and COFINS rate is 7.6%.

COFINS (2)

Taxes - These provisions are calculated according to current legislation at the rates shown below, for effects ofthe related calculation bases.

Additional income taxSocial contribution (1)PIS (2)

The changes introduced by Laws No. 11,638 and No. 11,941 (articles 37 and 38), which modified the criterion for recognizing revenues, costs and expenses, computed to determine the net income for the year, did not produce effects for purposes of determining the taxable income of companies that opt for the Transitory Tax Regime (RTT), so for tax purposes the rules effective on December 31, 2007 were followed. The tax effect arising from the adoption of such rules is recorded, for accounting purposes, in the corresponding deferred assets and liabilities.

p) Deferred income – this refers to unexpired interest received in advance that is recorded in income as

earned, and the negative goodwill on acquisition of investments arising from expected future losses, which has not been absorbed in the consolidation process.

06/30/2009

Up to 365 daysOver 365

daysTotal

Total102,996,906 3,151,354 106,148,260 114,042,633

Funded position 51,794,369 3,151,354 54,945,723 48,903,908 Financed position 42,080,079 - 42,080,079 63,668,874 Short position 9,122,458 - 9,122,458 1,469,851

3,431,152 - 3,431,152 2,379,931 40,197,390 25,145,676 65,343,066 73,847,324

146,625,448 28,297,030 174,922,478 190,269,888 156,851,382 33,418,506 190,269,888 TOTAL - 06/30/2009

Money market - Assets Guaranteeing TechnicalProvisions - SUSEPInterbank depositsTOTAL

NOTE 5 - INTERBANK INVESTMENTS

06/30/2010

Money market

06/30/2009

ResultsStockholders'

equity39,934,030 49,865 287,259 40,271,154 38.2 1,121,032 1,709,145 1,233,443 5,783,508 5,572,208 24,851,818 43,332,283 17,297,713 659 (1,933) 17,296,439 16.4 259,428 1,382,220 359,254 3,053,645 1,779,449 10,462,443 16,321,393

National Treasury Bills 4,567,437 (5,450) (116) 4,561,871 4.3 479,085 - 52,461 1,482,933 1,674,504 872,888 13,903,036 14,042,850 37,357 97,251 14,177,458 13.5 104,639 296,809 25,498 1,227,126 1,938,021 10,585,365 9,722,473

658,616 15,675 (24,234) 650,057 0.6 277,122 16,282 5,543 19,246 23,466 308,398 321,861 3,367,414 1,624 216,291 3,585,329 3.4 758 13,834 790,687 558 156,768 2,622,724 3,061,615

- - - - - - - - - - - 1,905 3,500,959 42,388 18,941 3,562,288 3.4 263,130 135,237 1,428,777 1,279,623 54,303 401,218 3,663,462

- - - - - - - - - - - 256,460 - - - - - - - - - - - 100,782

220,511 3,377 - 223,888 0.2 25,042 56,151 62,945 34,164 - 45,586 302,145 Central Bank 70,427 1,891 - 72,318 0.1 - 39,465 3 29,865 - 2,985 173,003 National Treasury 150,084 1,486 - 151,570 0.1 25,042 16,686 62,942 4,299 - 42,601 129,142

62 1 - 63 - - - 1 - - 62 - 788,674 - (433) 788,241 0.7 168,104 - 179,220 440,917 - - 864,576 447,330 - (6,799) 440,531 0.4 - - - 440,531 - - 374,347

1,300,553 - 25,781 1,326,334 1.3 - - 1,071,445 254,889 - - 952,658 18,206 1 - 18,207 - - 18,093 108 - - 6 76

368,362 - (1) 368,361 0.4 66,268 45,322 58,195 108,368 35,896 54,312 295,340 351,270 38,968 386 390,624 0.4 1,801 15,485 56,853 - 17,902 298,583 498,741

1,403 18 - 1,421 - 34 1 3 754 - 629 4,232 4,588 23 7 4,618 - 1,881 185 7 - 505 2,040 14,105

14,060,193 91,988 159,970 14,312,151 13.6 2,929,457 176,319 439,949 858,844 1,707,808 8,199,774 14,511,925 3,086,304 7,171 69,704 3,163,179 3.0 28,178 21,401 72,500 117,727 522,930 2,400,443 1,453,581 2,909,244 - 535 2,909,779 2.8 425,870 120,733 115,770 451,235 629,869 1,166,302 2,143,244 1,860,970 60,118 (4,523) 1,916,565 1.8 1,916,565 - - - - - 1,533,588 1,347,833 174 543 1,348,550 1.3 791 7,161 174,209 129,019 378,175 659,195 3,181,777

- - - - - - - - - - - 139,462 502,672 24,515 14,371 541,558 0.5 537,746 - - - - 3,812 2,012,651

Fixed income 291,224 109 6,601 297,934 0.3 294,122 - - - - 3,812 1,661,507 Credit rights 24,985 - - 24,985 - 24,985 - - - - - 89,547 Other 186,463 24,406 7,770 218,639 0.2 218,639 - - - - - 261,597

4,241,815 10 79,367 4,321,192 4.1 16,156 24,685 41,202 124,285 154,782 3,960,082 3,912,282 111,355 - (27) 111,328 0.1 4,151 2,339 36,268 36,578 22,052 9,940 135,340

41,436,196 - - 41,436,196 39.4 41,436,196 - - - - - 34,475,799 98,931,378 184,241 466,170 99,581,789 94.7 45,749,815 2,020,701 3,102,169 7,921,975 7,334,319 33,452,810 95,983,469 73,301,816 184,241 - 73,486,057 69.9 44,551,155 1,917,998 1,028,361 3,190,899 5,088,184 17,709,460 64,217,465 22,676,779 - 466,170 23,142,949 22.0 1,194,216 101,131 2,055,360 4,596,998 2,013,794 13,181,450 28,872,993

2,952,783 - - 2,952,783 2.8 4,444 1,572 18,448 134,078 232,341 2,561,900 2,893,011 5,508,293 97,479 - 5,605,772 5.3 598,248 801,597 569,066 661,884 1,042,446 1,932,531 6,591,399

104,439,671 281,720 466,170 105,187,561 100.0 46,348,063 2,822,298 3,671,235 8,583,859 8,376,765 35,385,341 102,574,868 44.1% 2.7% 3.5% 8.2% 8.0% 33.6%

(139,915) (96,084)

(140,610) 14,358

103,919 (4,764,078) (141,146) (28,007) (4,933,231) 100.0 (352,544) (271,490) (485,158) (1,045,216) (933,692) (1,845,131) (6,617,157)

101,447,999 572,548 554,321 102,574,868 100.0 42,735,952 2,257,313 6,422,764 11,306,472 10,114,160 29,738,207 (110,854) (390,244)

(67,021) 17,862

4,064 (5,912,974) (704,183) - (6,617,157) 100.0 (2,370,666) (642,221) (625,729) (1,016,353) (570,606) (1,391,582)

SUBTOTAL - SECURITIES

DERIVATIVE FINANCIAL INSTRUMENTS

Other

Available-for-sale securities Held-to-maturity securities (3) (4)

Trading securities

GOVERNMENT SECURITIES - ABROAD

CORPORATE SECURITIES

Securitized real estate loans

PGBL/VGBL fund quotas (2)

Austria

Deferred taxesAdjustments of securities reclassified in prior years to held-to-maturity securities

(3) Unrecorded positive adjustment to market value in the amount of R$ 530,287 (R$ 322,838 at 06/30/2009).

(4) Management sets forth guidelines to classify securities. The classification of the current portfolio of securities, as well as the securities purchased in the period, is periodically and systematically evaluated based on such guidelines. As set forth in Article 5 of BACEN Circular No. 3,068, of November 8, 2008, the revaluation regarding the classification of securitiescan only be made upon preparation of trial balances for six-month periods. In addition, the transfer from “held-to-maturity” to the other categories can only occur in view of an isolated, unusual, nonrecurring and unexpected reason, which has occurred after the classification date. No reclassifications or changes to the existing guidelines have been made in the period.

ADJUSTMENT TO MARKET VALUE - SECURITIES – STOCKHOLD ERS’ EQUITYDERIVATIVE FINANCIAL INSTRUMENTS (LIABILITIES) - 06 /30/2009(1) Includes the amount of R$ 13,552,861 (R$ 17,958,272 at 06/30/2009) of securities pledged in guarantee, of which: Assets Guaranteeing Technical Provisions R$ 5,179,655 (R$ 5,725,383 at 06/30/2009), securities linked to BACEN R$ 3,600,943 (R$ 6,236,012 at 06/30/2009) and securities deposited with the Clearing House for the Custody and FinancialSettlement of Securities R$ 4,772,264 (R$ 5,996,878 at 06/30/2009).

(2) The PGBL and VGBL plans securities portfolios, the ownership and embedded risks of which are the customers’ responsibility, are recorded as securities, as determined by SUSEP, with a contra-entry to liabilities in the Pension Plan Technical Provisions account.

TOTAL SECURITIES AND DERIVATIVE FINANCIAL INSTRUMEN TS (ASSETS)

Adjustment of subsidiaries and affiliatesAdjustment to market of accounting hedge

TOTAL SECURITIES AND DERIVATIVE FINANCIAL INSTRUMEN TS (ASSETS) - 06/30/2009

DERIVATIVE FINANCIAL INSTRUMENTS (LIABILITIES)

Adjustment to market of accounting hedgeDeferred taxes

Adjustment of subsidiaries and affiliates

ADJUSTMENT TO MARKET VALUE - SECURITIES – STOCKHOLD ERS’ EQUITYAdjustments of securities reclassified in prior years to held-to-maturity securities

See below the composition by Securities and Derivatives type, maturity and portfolio already adjusted to their respective market values.

06/30/2010

Argentina

Brazilian External Debt BondsOther

National Treasury/Securitization

GOVERNMENT SECURITIES - DOMESTIC (1)Financial Treasury Bills

National Treasury Notes

NOTE 6 - SECURITIES AND DERIVATIVE FINANCIAL INSTRU MENTS (ASSETS AND LIABILITIES)

a) Summary per maturity

Cost

Provision for adjustment to market value with impact on: Over 720 daysMarket value 31 - 90 366 - 720% 91 - 1800 - 30 181 - 365

Quotas of Funds

Chile

Portugal

United States

Korea

Russia

Shares

Market value

Debentures Promissory Notes

Mexico

Eurobonds and other Bank Deposit Certificates

Other

DenmarkSpain

Paraguay

h) Derivative financial instruments

The globalization of the markets in recent years has resulted in a high level of sophistication in the financial products used. As a result of this process, there has been an increasing demand for derivative financial instruments to manage market risks, mainly arising from fluctuations in interest and exchange rates, commodities and other asset prices. Accordingly, ITAU UNIBANCO CONSOLIDATED and its subsidiaries operate in the derivative markets for meeting the growing needs of their clients, as well as carrying out their risk management policy. Such policy is based on the use of derivative instruments to minimize the risks resulting from commercial and financial operations. The derivative financial instruments’ business with clients is carried out after the approval of credit limits. The process of limit approval takes into consideration potential stress scenarios. Knowing the client, the sector in which it operates and its risk appetite profile, in addition to providing information on the risks involved in the transaction and the negotiated conditions, ensures transparency in the relationship between the parties and the supply of a product that better meet the needs of the client in view of its operating characteristics. The derivative transactions carried out by ITAÚ UNIBANCO CONSOLIDATED and its subsidiaries with clients are neutralized in order to eliminate market risks. Most derivative contracts traded by the institution with clients in Brazil are swap, forward, option and futures contracts, which are registered at the BM&FBovespa or at the CETIP S.A. - OTC Clearing House (CETIP). Overseas transactions are carried out with futures, forwards, options and swaps with registration mainly in the Chicago, New York and London Exchanges. It should be emphasized that there are over-the-counter operations, but their risks are low as compared to the institutions’ total. Noteworthy is also the fact that there are no structured operations based on subprime assets and all operations are based on risk factors traded at stock exchanges. The main risk factors of the derivatives, assumed at June 30, 2010, were related to the foreign exchange rate, interest rate, commodities, U.S. dollar coupon, Reference Rate coupon, Libor and variable income. The management of these and other market risk factors is supported by sophisticated statistical and deterministic models. Based on this management model, the institution, with the use of transactions involving derivatives, has been able to optimize the risk-return ratios, even under highly volatile situations. Most derivatives included in the institution’s portfolio are traded at stock exchanges. The prices disclosed by stock exchanges are used for these derivatives, except in cases in which the low representativeness of price due to illiquidity of a specific contract is identified. Derivatives typically precified like this are futures contracts. Likewise, there are other instruments whose quotations (fair prices) are directly disclosed by independent institutions and which are precified based on this direct information. A great part of the Brazilian government securities, highly-liquid international (public and private) securities and shares fit into this situation. For derivatives whose prices are not directly disclosed by stock exchanges, fair prices are obtained by pricing models which use market information, deducted based on prices disclosed for higher liquidity assets. Interest and market volatility curves which provide entry data for the models are extracted from those prices. Over-the-counter derivatives, forward contracts and securities without much liquidity are in this situation. The total value of margins pledged in guarantee was R$ 6,229,900 (R$ 15,189,239 at June 30, 2009) and was basically composed of government securities.

Balance sheet account receivable / (received) payable

/ (paid)

Adjustment to market value (in

results / stockholders’

equity)06/30/2010 06/30/2009 06/30/2010 06/30/2010 06/30/2010 06/30/2009

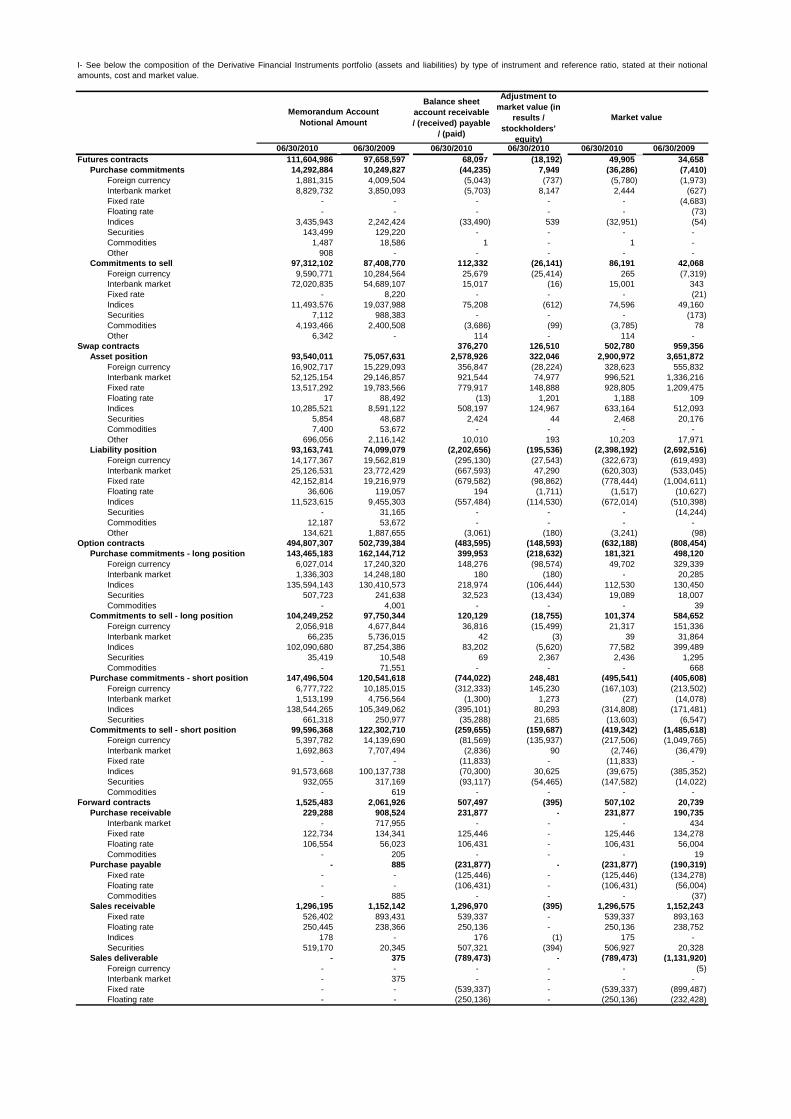

111,604,986 97,658,597 68,097 (18,192) 49,905 34,658 14,292,884 10,249,827 (44,235) 7,949 (36,286) (7,410)

Foreign currency 1,881,315 4,009,504 (5,043) (737) (5,780) (1,973) Interbank market 8,829,732 3,850,093 (5,703) 8,147 2,444 (627) Fixed rate - - - - - (4,683) Floating rate - - - - - (73) Indices 3,435,943 2,242,424 (33,490) 539 (32,951) (54) Securities 143,499 129,220 - - - - Commodities 1,487 18,586 1 - 1 - Other 908 - - - - -

97,312,102 87,408,770 112,332 (26,141) 86,191 42,068 Foreign currency 9,590,771 10,284,564 25,679 (25,414) 265 (7,319) Interbank market 72,020,835 54,689,107 15,017 (16) 15,001 343 Fixed rate - 8,220 - - - (21) Indices 11,493,576 19,037,988 75,208 (612) 74,596 49,160 Securities 7,112 988,383 - - - (173) Commodities 4,193,466 2,400,508 (3,686) (99) (3,785) 78 Other 6,342 - 114 - 114 -

376,270 126,510 502,780 959,356 93,540,011 75,057,631 2,578,926 322,046 2,900,972 3,651,872

Foreign currency 16,902,717 15,229,093 356,847 (28,224) 328,623 555,832 Interbank market 52,125,154 29,146,857 921,544 74,977 996,521 1,336,216 Fixed rate 13,517,292 19,783,566 779,917 148,888 928,805 1,209,475 Floating rate 17 88,492 (13) 1,201 1,188 109 Indices 10,285,521 8,591,122 508,197 124,967 633,164 512,093 Securities 5,854 48,687 2,424 44 2,468 20,176 Commodities 7,400 53,672 - - - - Other 696,056 2,116,142 10,010 193 10,203 17,971

93,163,741 74,099,079 (2,202,656) (195,536) (2,398,192) (2,692,516) Foreign currency 14,177,367 19,562,819 (295,130) (27,543) (322,673) (619,493) Interbank market 25,126,531 23,772,429 (667,593) 47,290 (620,303) (533,045) Fixed rate 42,152,814 19,216,979 (679,582) (98,862) (778,444) (1,004,611) Floating rate 36,606 119,057 194 (1,711) (1,517) (10,627) Indices 11,523,615 9,455,303 (557,484) (114,530) (672,014) (510,398) Securities - 31,165 - - - (14,244) Commodities 12,187 53,672 - - - - Other 134,621 1,887,655 (3,061) (180) (3,241) (98)

494,807,307 502,739,384 (483,595) (148,593) (632,188) (808,454) 143,465,183 162,144,712 399,953 (218,632) 181,321 498,120

Foreign currency 6,027,014 17,240,320 148,276 (98,574) 49,702 329,339 Interbank market 1,336,303 14,248,180 180 (180) - 20,285 Indices 135,594,143 130,410,573 218,974 (106,444) 112,530 130,450 Securities 507,723 241,638 32,523 (13,434) 19,089 18,007 Commodities - 4,001 - - - 39

104,249,252 97,750,344 120,129 (18,755) 101,374 584,652 Foreign currency 2,056,918 4,677,844 36,816 (15,499) 21,317 151,336 Interbank market 66,235 5,736,015 42 (3) 39 31,864 Indices 102,090,680 87,254,386 83,202 (5,620) 77,582 399,489 Securities 35,419 10,548 69 2,367 2,436 1,295 Commodities - 71,551 - - - 668

147,496,504 120,541,618 (744,022) 248,481 (495,541) (405,608) Foreign currency 6,777,722 10,185,015 (312,333) 145,230 (167,103) (213,502) Interbank market 1,513,199 4,756,564 (1,300) 1,273 (27) (14,078) Indices 138,544,265 105,349,062 (395,101) 80,293 (314,808) (171,481) Securities 661,318 250,977 (35,288) 21,685 (13,603) (6,547)

99,596,368 122,302,710 (259,655) (159,687) (419,342) (1,485,618) Foreign currency 5,397,782 14,139,690 (81,569) (135,937) (217,506) (1,049,765) Interbank market 1,692,863 7,707,494 (2,836) 90 (2,746) (36,479) Fixed rate - - (11,833) - (11,833) - Indices 91,573,668 100,137,738 (70,300) 30,625 (39,675) (385,352) Securities 932,055 317,169 (93,117) (54,465) (147,582) (14,022) Commodities - 619 - - - -

1,525,483 2,061,926 507,497 (395) 507,102 20,739 229,288 908,524 231,877 - 231,877 190,735

Interbank market - 717,955 - - - 434 Fixed rate 122,734 134,341 125,446 - 125,446 134,278 Floating rate 106,554 56,023 106,431 - 106,431 56,004 Commodities - 205 - - - 19

- 885 (231,877) - (231,877) (190,319) Fixed rate - - (125,446) - (125,446) (134,278) Floating rate - - (106,431) - (106,431) (56,004) Commodities - 885 - - - (37)

1,296,195 1,152,142 1,296,970 (395) 1,296,575 1,152,243 Fixed rate 526,402 893,431 539,337 - 539,337 893,163 Floating rate 250,445 238,366 250,136 - 250,136 238,752 Indices 178 - 176 (1) 175 - Securities 519,170 20,345 507,321 (394) 506,927 20,328

- 375 (789,473) - (789,473) (1,131,920) Foreign currency - - - - - (5) Interbank market - 375 - - - - Fixed rate - - (539,337) - (539,337) (899,487) Floating rate - - (250,136) - (250,136) (232,428)

Purchase payable

Sales receivable

Purchase commitments - short position

Commitments to sell - short position

Forward contractsPurchase receivable

Swap contractsAsset position

Purchase commitments - long position

Commitments to sell - long position

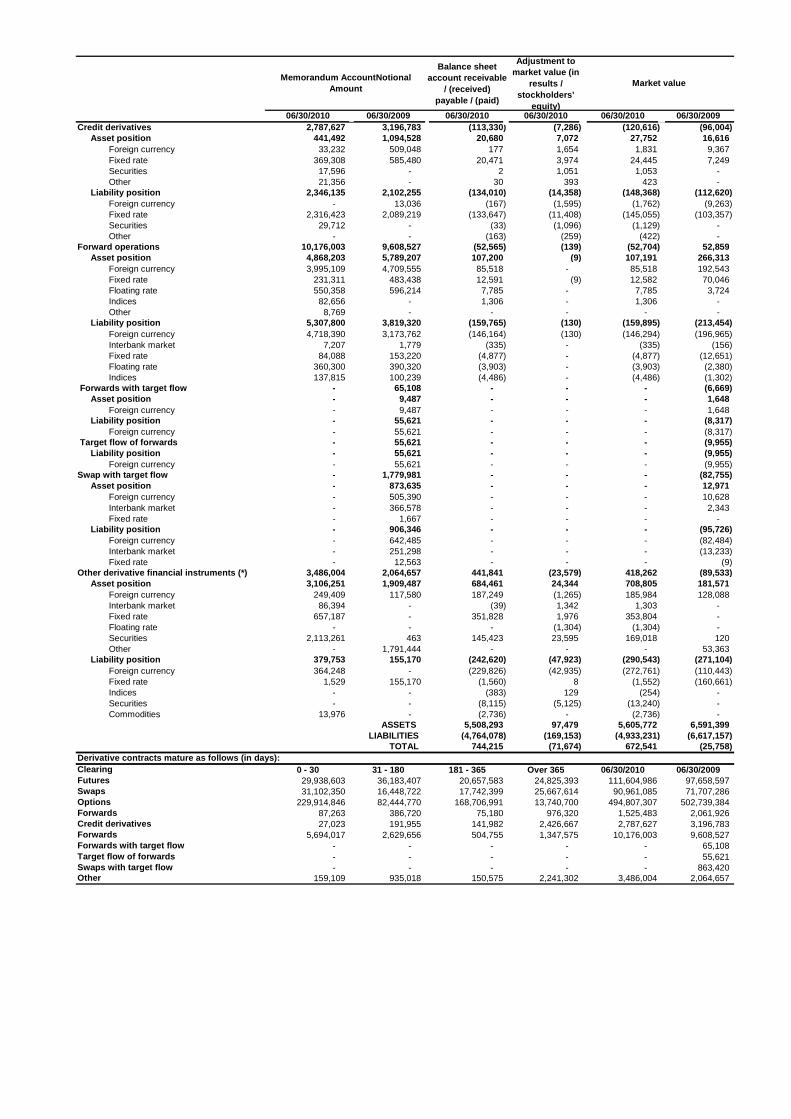

I- See below the composition of the Derivative Financial Instruments portfolio (assets and liabilities) by type of instrument and reference ratio, stated at their notionalamounts, cost and market value.

Liability position

Option contracts

Sales deliverable

Memorandum Account Notional Amount

Market value

Futures contractsPurchase commitments

Commitments to sell

Balance sheet account receivable

/ (received) payable / (paid)

Adjustment to market value (in

results / stockholders’

equity)06/30/2010 06/30/2009 06/30/2010 06/30/2010 06/30/2010 06/30/2009

2,787,627 3,196,783 (113,330) (7,286) (120,616) (96,004) 441,492 1,094,528 20,680 7,072 27,752 16,616

Foreign currency 33,232 509,048 177 1,654 1,831 9,367 Fixed rate 369,308 585,480 20,471 3,974 24,445 7,249 Securities 17,596 - 2 1,051 1,053 - Other 21,356 - 30 393 423 -

2,346,135 2,102,255 (134,010) (14,358) (148,368) (112,620) Foreign currency - 13,036 (167) (1,595) (1,762) (9,263) Fixed rate 2,316,423 2,089,219 (133,647) (11,408) (145,055) (103,357) Securities 29,712 - (33) (1,096) (1,129) - Other - - (163) (259) (422) -

10,176,003 9,608,527 (52,565) (139) (52,704) 52,859 4,868,203 5,789,207 107,200 (9) 107,191 266,313

Foreign currency 3,995,109 4,709,555 85,518 - 85,518 192,543 Fixed rate 231,311 483,438 12,591 (9) 12,582 70,046 Floating rate 550,358 596,214 7,785 - 7,785 3,724 Indices 82,656 - 1,306 - 1,306 - Other 8,769 - - - - -

5,307,800 3,819,320 (159,765) (130) (159,895) (213,454) Foreign currency 4,718,390 3,173,762 (146,164) (130) (146,294) (196,965) Interbank market 7,207 1,779 (335) - (335) (156) Fixed rate 84,088 153,220 (4,877) - (4,877) (12,651) Floating rate 360,300 390,320 (3,903) - (3,903) (2,380) Indices 137,815 100,239 (4,486) - (4,486) (1,302)

- 65,108 - - - (6,669) - 9,487 - - - 1,648

Foreign currency - 9,487 - - - 1,648 - 55,621 - - - (8,317)

Foreign currency - 55,621 - - - (8,317) - 55,621 - - - (9,955) - 55,621 - - - (9,955)

Foreign currency - 55,621 - - - (9,955) - 1,779,981 - - - (82,755) - 873,635 - - - 12,971

Foreign currency - 505,390 - - - 10,628 Interbank market - 366,578 - - - 2,343 Fixed rate - 1,667 - - - -

- 906,346 - - - (95,726) Foreign currency - 642,485 - - - (82,484) Interbank market - 251,298 - - - (13,233) Fixed rate - 12,563 - - - (9)

3,486,004 2,064,657 441,841 (23,579) 418,262 (89,533) 3,106,251 1,909,487 684,461 24,344 708,805 181,571

Foreign currency 249,409 117,580 187,249 (1,265) 185,984 128,088 Interbank market 86,394 - (39) 1,342 1,303 - Fixed rate 657,187 - 351,828 1,976 353,804 - Floating rate - - - (1,304) (1,304) - Securities 2,113,261 463 145,423 23,595 169,018 120 Other - 1,791,444 - - - 53,363

379,753 155,170 (242,620) (47,923) (290,543) (271,104) Foreign currency 364,248 - (229,826) (42,935) (272,761) (110,443) Fixed rate 1,529 155,170 (1,560) 8 (1,552) (160,661) Indices - - (383) 129 (254) - Securities - - (8,115) (5,125) (13,240) - Commodities 13,976 - (2,736) - (2,736) -

ASSETS 5,508,293 97,479 5,605,772 6,591,399 LIABILITIES (4,764,078) (169,153) (4,933,231) (6,617,157)

TOTAL 744,215 (71,674) 672,541 (25,758)

0 - 30 31 - 180 181 - 365 Over 365 06/30/2010 06/30/200929,938,603 36,183,407 20,657,583 24,825,393 111,604,986 97,658,597 31,102,350 16,448,722 17,742,399 25,667,614 90,961,085 71,707,286

229,914,846 82,444,770 168,706,991 13,740,700 494,807,307 502,739,384 87,263 386,720 75,180 976,320 1,525,483 2,061,926 27,023 191,955 141,982 2,426,667 2,787,627 3,196,783

5,694,017 2,629,656 504,755 1,347,575 10,176,003 9,608,527 - - - - - 65,108 - - - - - 55,621 - - - - - 863,420

159,109 935,018 150,575 2,241,302 3,486,004 2,064,657

Memorandum AccountNotional Amount

Market value

Liability position

Credit derivativesAsset position

Liability position

Forward operationsAsset position

Liability position

Forwards with target flowAsset position

Target flow of forwardsLiability position

Liability position

Other derivative financial instruments (*)

Swap with target flowAsset position

Asset position

Liability position

Derivative contracts mature as follows (in days):ClearingFuturesSwapsOptions

Target flow of forwardsSwaps with target flowOther

ForwardsCredit derivativesForwardsForwards with target flow

II -

a)

b)

Accounting hedge

The swap operations contracted in a negotiation associated with the funding and/or investment in theamount of R$ 302,414 (R$ 720,766 at 06/30/2009) are recorded at amounts restated in accordancewith variations occurred in respective ratios (“curve”) and are not valued at their market value, aspermitted by BACEN Circular No. 3,150/02.

The gains or losses related to the accounting hedge of cash flows that we expect to recognize in results in the following 12 months amount to R$ 168,980 (R$ 1,184 at 06/30/2009).

The purpose of the hedge relationship of ITAU UNIBANCO CONSOLIDATED is to protect the cashflow of payment of debt interest (CDB / Redeemable preferred shares) related to its variable interestrate risk (CDI / LIBOR), making the cash flow constant (fixed rate) and independent from thevariations of DI Cetip Over and LIBOR.

To protect the future cash flows of debt against exposure to variable interest rate (CDI), at June 30,2010 ITAÚ UNIBANCO CONSOLIDATED negotiated DI Futures agreements at BM&FBOVESPA withmaturity between 2010 and 2017 in the amount of R$ R$ 22,445,674 (R$ 13,021,089 at 06/30/2009).To protect the future cash flows of debt against exposure to variable interest rate (LIBOR), at June 30,2010 ITAÚ UNIBANCO CONSOLIDATED negotiated swap contracts with maturity in 2015 in theamount of R$ 708,119. These derivative financial instruments gave rise to adjustment to market valuenet of tax effects recorded in stockholders’ equity of (R$ 53,183) (R$ (213,822) at 06/30/2009), ofwhich (R$ 37,681) (R$ (213,822) at 06/30/2009) refers to CDB and R$ (15,502) refers to RedeemablePreferred shares. The hedged items total R$ 23,153,794 (R$ 12,557,126 at 06/30/2009), of which R$22,445,674 are CDB with maturities between 2010 and 2017 and R$ 708,119 are swaps ofredeemable preferred shares with maturity in 2015.

The effectiveness computed for hedge portfolio was in conformity with the provisions of BACENCircular No. 3,082 of January 30, 2002.

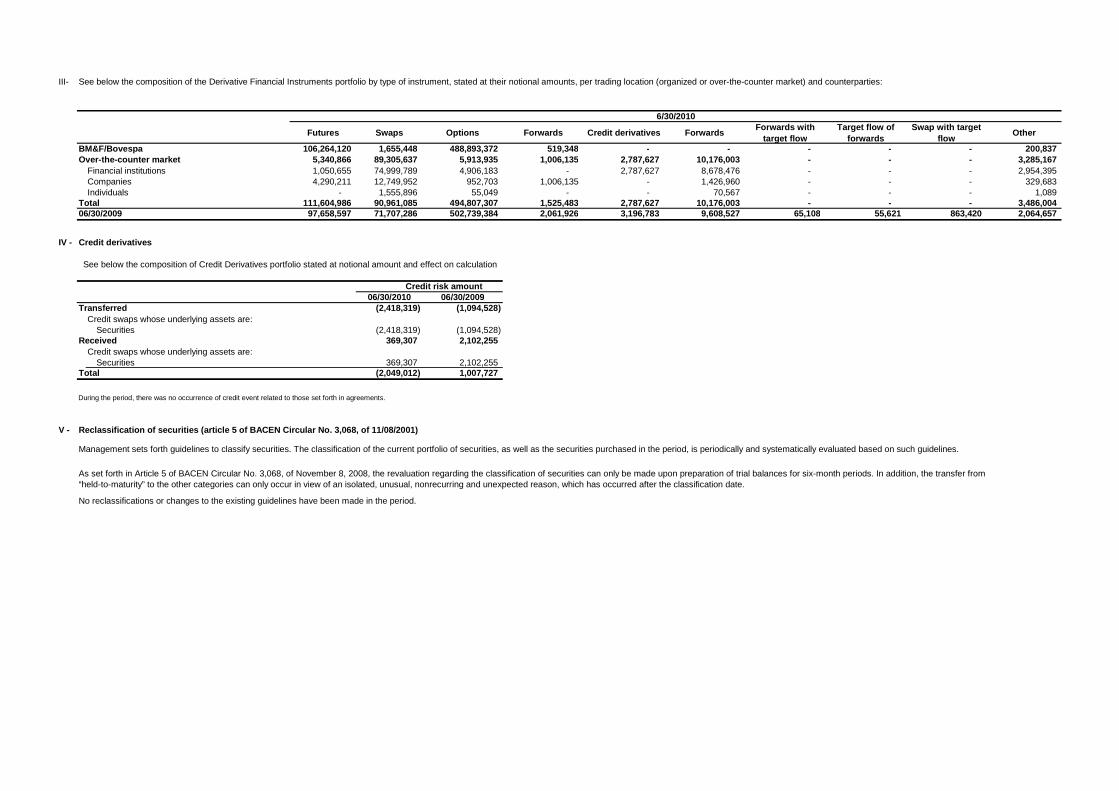

III-

Futures Swaps Options Forwards Credit derivatives Forwar ds Forwards with

target flowTarget flow of

forwardsSwap with target

flowOther

106,264,120 1,655,448 488,893,372 519,348 - - - - - 200,837 5,340,866 89,305,637 5,913,935 1,006,135 2,787,627 10,176,003 - - - 3,285,167 1,050,655 74,999,789 4,906,183 - 2,787,627 8,678,476 - - - 2,954,395 4,290,211 12,749,952 952,703 1,006,135 - 1,426,960 - - - 329,683

- 1,555,896 55,049 - - 70,567 - - - 1,089 111,604,986 90,961,085 494,807,307 1,525,483 2,787,627 10,176,003 - - - 3,486,004 97,658,597 71,707,286 502,739,384 2,061,926 3,196,783 9,608,527 65,108 55,621 863,420 2,064,657

IV -

06/30/2010 06/30/2009(2,418,319) (1,094,528)

(2,418,319) (1,094,528) 369,307 2,102,255

369,307 2,102,255 Total (2,049,012) 1,007,727

V -

See below the composition of the Derivative Financial Instruments portfolio by type of instrument, stated at their notional amounts, per trading location (organized or over-the-counter market) and counterparties:

Companies

Reclassification of securities (article 5 of BACEN Circular No. 3,068, of 11/08/2001)

06/30/2009

Credit derivatives

IndividualsTotal

As set forth in Article 5 of BACEN Circular No. 3,068, of November 8, 2008, the revaluation regarding the classification of securities can only be made upon preparation of trial balances for six-month periods. In addition, the transfer from“held-to-maturity” to the other categories can only occur in view of an isolated, unusual, nonrecurring and unexpected reason, which has occurred after the classification date.

Management sets forth guidelines to classify securities. The classification of the current portfolio of securities, as well as the securities purchased in the period, is periodically and systematically evaluated based on such guidelines.

No reclassifications or changes to the existing guidelines have been made in the period.

Credit risk amount

Credit swaps whose underlying assets are:Securities

6/30/2010

During the period, there was no occurrence of credit event related to those set forth in agreements.

Credit swaps whose underlying assets are:Received

Securities

BM&F/BovespaOver-the-counter market

Financial institutions

Transferred

See below the composition of Credit Derivatives portfolio stated at notional amount and effect on calculation

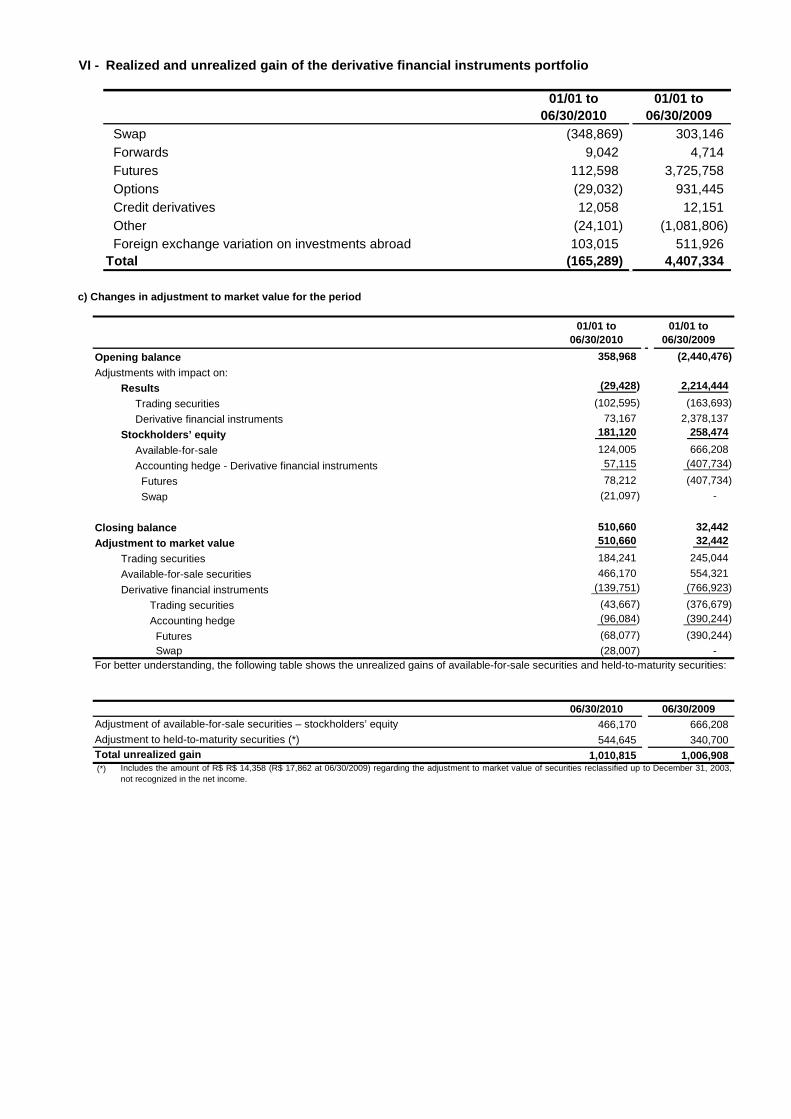

VI -

01/01 to 06/30/2010

01/01 to 06/30/2009

Swap (348,869) 303,146 Forwards 9,042 4,714 Futures 112,598 3,725,758 Options (29,032) 931,445 Credit derivatives 12,058 12,151 Other (24,101) (1,081,806) Foreign exchange variation on investments abroad 103,015 511,926 Total (165,289) 4,407,334

Realized and unrealized gain of the derivative fina ncial instruments portfolio

01/01 to 06/30/2010

01/01 to 06/30/2009

358,968 (2,440,476)

(29,428) 2,214,444

(102,595) (163,693)

73,167 2,378,137 181,120 258,474

Available-for-sale 124,005 666,208

Accounting hedge - Derivative financial instruments 57,115 (407,734)

Futures 78,212 (407,734)

Swap (21,097) -

510,660 32,442 510,660 32,442

184,241 245,044

466,170 554,321 (139,751) (766,923)

Trading securities (43,667) (376,679)

Accounting hedge (96,084) (390,244)

Futures (68,077) (390,244)

Swap (28,007) -

06/30/2010 06/30/2009466,170 666,208

544,645 340,700

1,010,815 1,006,908 (*)

c) Changes in adjustment to market value for the pe riod

Stockholders’ equityDerivative financial instruments

Closing balance

Opening balanceAdjustments with impact on:

ResultsTrading securities

Available-for-sale securities

Trading securities

Adjustment to market value

Derivative financial instruments