Embed Size (px)

Citation preview

Analysis

Special Situa ons Research delivers comprehensive, independent research on high-profile economic proposalsincluding M&A and proxy contests, and on the implica ons for shareholders of evolving trends in corporategovernance and shareholder rights.

© 2016. All Rights Reserved. Ins tu onal Shareholder Services Inc. | www.issgovernance.com

August 1, 2016

ISS Special Situations Research

Executive Summary

On May 30, 2016, less than 16 months a erthe company’s IPO, controlling shareholderDalian Wanda launched an offer to buy the14.4% of H shares outstanding in DalianWanda Commercial Proper es.

While the transac on is structured as atender offer, holders of H shares must firstapprove the delis ng of the company at anAug. 15 shareholder mee ng for the tenderoffer to be declared uncondi onal. .

One month a er the deal was announced,however, Dutch pension fund APG (5.0% of Hshares) laid out its concerns about the offer,causing the spread to widen substan ally.Under Hong Kong rules, if more than 10% ofH shares vote against the delis ng—anecessary condi on to the tender— it maynot proceed, raising real risk of non-comple on.

Process and Key Terms:The deal process is rela vely simple given thecompany’s status as a controlled company.The company was approached by itscontrolling shareholder, and the board set upan independent commi ee to evaluate theoffer. The commi ee retained its ownfinancial advisor to evaluate the transac on.

The offer of HK$ 52.80 per share was officiallyannounced on May 30, 2016 and lateraccepted by the DWCP’s commi ee ofindependent directors. The tender offer iscondi onal on approval of the delis ng.

Strategic rationaleThe company does not provide a strategicra onale to support the Dalian Wanda Grouptakeover offer, but the bidder encouragesshareholders to accept the offer based on:

The certain and immediate premium forthe illiquid H shares of approximately36.1% over the closing price on 30 March

ContentsExecu ve Summary 1Trading Comps & Historical Performance 5Shareholder Base 7Background 8Strategic Ra onale 9Valua on 11Conclusion and Vote Recommenda on 14

Chris CernichPhone: +1 [email protected]

Chart Focus

Source: Thomson One. In HK$

Contacts

Dalian Wanda Commercial Properties (HKG:3699):proposed acquisition by Dalian Wanda Group

Nelson SeraciPhone: +34 688 629 [email protected]

Vote Recommendation: Vote FOR the delisting of H shares

Record Date Aug. 15, 2016Mee ng Date Aug. 15, 2016

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 2

August 1, 2016ISS Special Situations Research

2016, immediately prior to the deal’sannouncement, and approximately 10.0% overthe IPO price;

The ability to avoiding holding unlisted shares, asthe H shares will be delisted should the tenderoffer be declared uncondi onal; and

The fact that a third party is unlikely to pay aconsiderable premium for the H Shares, giventhe controlling stake of the Dalian Wanda Group.

The poten al offer was announced barely 16 monthsa er the company’s IPO, and it seems reasonable toques on whether the offer somehow contradicts thera onale for the IPO or market condi ons havechanged so much as to jus fy a sale.

In December 2014 the company had already warnedover the sustainability of real estate market growthin China, sta ng that "the PRC property market isaffected by the recent slowdown in China’s economicgrowth. There have been increasing concerns overthe sustainability of the real estate market growth inChina" (IPO prospectus).

In its 2015 Annual Report, the company stated that"China is s ll facing downward pressure with the rateof industry growth slowing down, local governmentshave implemented a series of policies rela ng to thereal estate industry in 2015, covering a cut in interestrates and a reduc on of the reserves that certainbanks must hold, a reduc on of down payment forhousing accumula on fund loan (which is a specialhousing loan offering to those eligible persons whohave made contribu on to the housing providentfund in the PRC), tax incen ve and li of homebuying restric ons. These helped the real estateindustry to gradually recover from depression.”

The wording from the company reports does notseem to reflect a heightened level of concern frommanagement vs. the me of the IPO, though thesitua on in China indeed deteriorated in theinterim period between the two reports. The totalinvestment in real estate development grew by1.0% in 2015, as compared to a growth rate ofapproximately 19.8% in 2013 and 10.5% in 2014.

On Jan. 10, 2016, the company announced it wasexpec ng contracted sales to decrease by 39% in2016. During the first five months of 2016 thecompany’s contracted sales declined by 12.0% orHK$ 4.9 bn, though this was par ally compensatedby an increase in HK1.7 bn in rental and hotelincome, which is more recurring in nature. ChinaResources Land, probably the closest listed peer,achieved a 49% increase in contracted sales overthe same period.

Credit ra ng agencies have put the company onnega ve watch (Moody's) or downgraded it (S&P):

"However, the company's ra ng outlookremains nega ve, reflec ng our concerns thatits credit metrics will weaken in the next 12-18months and will pressure its Baa2 ra ng," saysKaven Tsang, a Moody's Vice President andSenior Analyst. ..The nega ve outlook alsoreflects our concern that DWCP's liquidityposi on will weaken as its scales backcontracted sales" (Moody's, Feb. 18, 2016).

"The downgrade reflects our view that WandaCommercial's aggressive expansion appe te togrow its investment property por olio couldresult in higher financial leverage over the next24 months than we had previously

an cipated," said Standard & Poor's creditanalyst Ma hew Kong. “The company's cashflows are also likely to weaken because thesignificant reduc on in contracted sales willoffset the robust growth in rental income." (TheStandard, Feb. 3, 2016).

The decrease in contracted sales seems intended tosome extent, as the company pushed throughinventory during the booming years and has nowdecelerated sales in a weaker market (and cutacquisi ons of new land). The company startedtalking about a change to an “asset light” strategyshortly a er the IPO, heading in the direc on ofmaking ownership and opera on of proper es(shopping centers and hotels) its main business, withproperty development (apartments and offices inshopping mall complexes) a secondary one.

Analysts are divided on the risks of this strategy,though if there is a consensus that seems to be thatit will be a bumpy road managing the transi on inbusiness model with a slowdown in the market andfinancial leverage. Some analysts were concernedthat the sharp cut of contracted sales target to thedifficult physical property market in lower- er ci eswhere Wanda has majority presence, not a managedstrategic transi on to an asset light model.

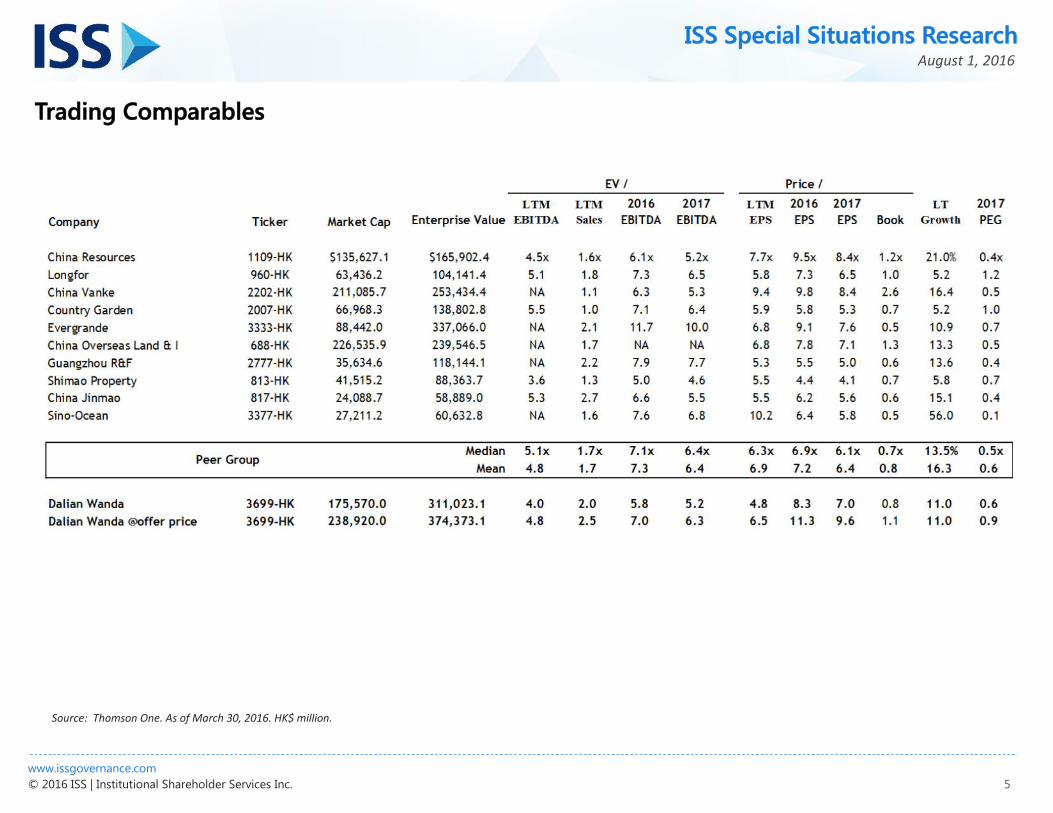

ValuationWe used the 11 peers selected by the independentdirector commi ee's financial advisor in our analysis.We note, however, that most peers are largelyresiden al property developers, as opposed todevelopers and operators of shopping malls. ChinaResources Land is probably the closest peer in termsof business model and exposure.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 3

August 1, 2016ISS Special Situations Research

Premium vs. market price:

The offer represents a premium of approximately40.6% over the unaffected closing price on March 30,2016, as adjusted by the 2015 HK$1.25 dividend (ex-dividend date May 27, 2016). The short termpremium might look substan al considering this is aminority squeeze-out for shareholders holding only14% of the shares outstanding, though it is barely apremium to the price six months before theannouncement given the downtrend in the stock.The offer is also a premium of 15.9% to the IPO priceadjusted by dividends of HK$ 45.55. From the IPO todate peers have increased by approximately 23%,and China Resources Land by 9%. Compared to theevolu on of the la er since IPO, the nominal 15.9%premium of the offer would actually represent asingle digit premium.

Valua on vs. Comparables:

Since its lis ng in Dec. 2014, the company's stocktraded in lockstep with the median of peers andChina Resources Land un l late 2015, when adivergence became apparent. By the me of theannouncement of a poten al offer on March 30,2016, the company had underperformed ChinaResources Land by 8 percentage points since the IPO.This might to be related to the decline in contractedsales, which had grown by 10% during 1H15 butdeclined by 1.6% in 2H15 (the company disclosesmonthly figures, allowing the market to followclosely its performance). Moreover, any weakness inopera onal performance is magnified at thecompany because its financial leverage is muchhigher than that of China Resources Land.

Valua on ra os echo this story, with the companytrading at an average Price/Book ra o 8% lower than

that of China Resources Land during the first yearof trading, and the discount widening over me to19% at the deal’s announcement. If one values thecompany at the average discount of the first yearof trading, its fair Price/Book mul ple would be1.07x. The offer price implies a Price/Book ra o of1.13x, or an approximately 6% premium to thisnormalized ra o.

Analyst Target prices:

The gap between share prices and analyst targetprices also kept widening un l early 2016. At the

me of the poten al offer announcement onMarch 30, 2016, the company was trading at a40.6% discount to the unaffected target price, vs.33.3% for China Resources Land. The offer price ofHK$ 52.80 is a 21.6% discount to the unaffectedtarget price.

Comparison to similar deals:

The one-day premium of 40.6% compares well withthe 32.4% median premium of similar successfuldeals reported in the fairness opinion. Over longerlook-back periods that advantage dissipates: the180-day premium to the average of daily prices of16.0% looks low vs. the 52.2% median of similarsuccessful deals.

According to the fairness opinion, the transac onimplies a 10.8% discount to the company's adjustedNAV (i.e. using the appraiser's valua on for thecompany's real estate), lower than all reporteddeals as well as the 32.4% average discount toAdjusted NAV. We note that the other dealsinvolved developers of residen al property mostly,which tend to trade at higher discounts.

Conclusion and Vote Recommendation:The company is going though its first cyclicaldownturn as a listed en ty, a period that of concernabout “opportunis c ming” transac ons led by acontrolling shareholder.

The first ques on shareholders face is why theyshould accept such a premium in this part of thecycle. While analysts are divided on the risks, there isa consensus that it will be a bumpy road managingthe transi on in business model with a slowdown inthe market and financial leverage.

The second ques on is whether shareholders arebeing properly compensated for the loss of poten alupside. There seem to be valid reasons behind theshare price underperformance that preceded theannouncement of the takeover: a decline incontracted sales coupled with higher leverage duringa sluggish period for the Chinese economy.

If these concerns were misplaced, and one wouldvalue the company based on the stock evolu on andhistoric discount to Price/Book ra o of ChinaResources Land, then the deal would imply a singledigit premium, low even for minority squeeze-outstandards. The other end of the spectrum is arguingthat the 40% one-day premium is reflec ve ofintrinsic value, which seems an exaggera on whenthe deal premium s ll implies a 10% discount toNAV. A mid-point, which seems a realis cassump on given the industry and strategicbackground, would imply a reasonable premium in acash deal for minori es holding 14.4% of sharesoutstanding.

Based on these factors, we recommend shareholdersvote FOR the transac on.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 4

August 1, 2016ISS Special Situations Research

Transaction Summary

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 5

August 1, 2016ISS Special Situations Research

Trading Comparables

Source: Thomson One. As of March 30, 2016. HK$ million.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 6

August 1, 2016ISS Special Situations Research

Historical Financial Performance

Source: Thomson One. HK$ million.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 7

August 1, 2016ISS Special Situations Research

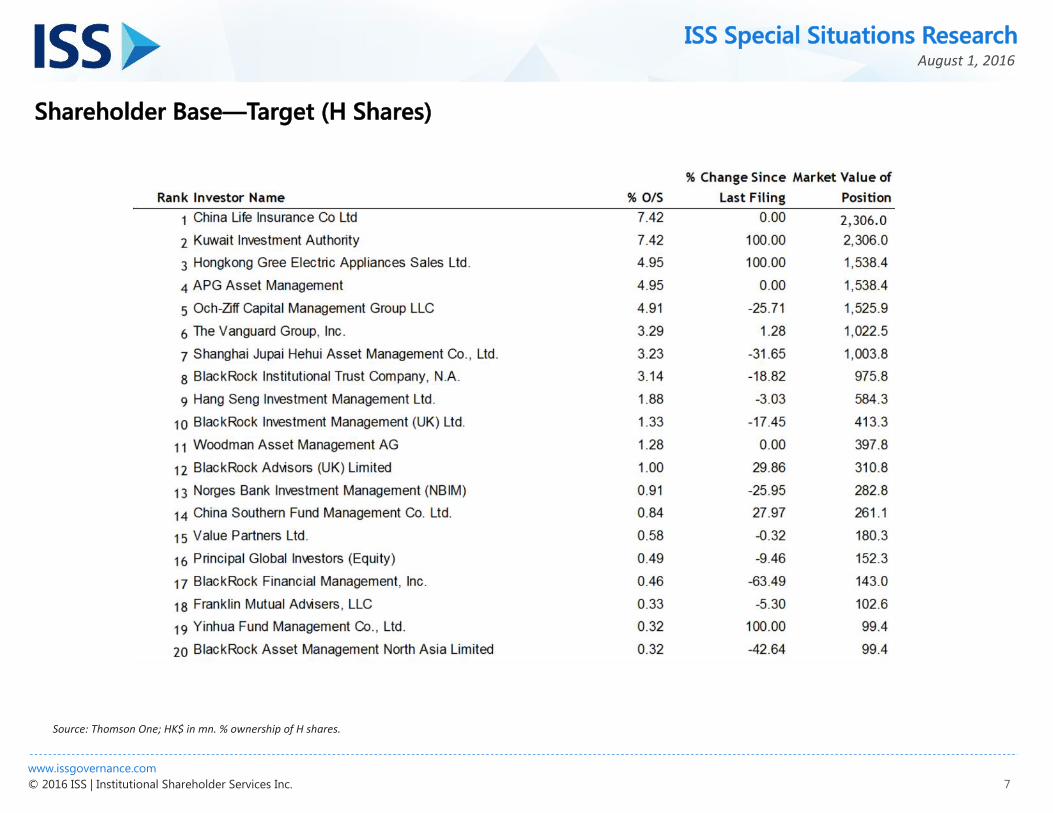

Shareholder Base—Target (H Shares)

Source: Thomson One; HK$ in mn. % ownership of H shares.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 8

August 1, 2016ISS Special Situations Research

Background

Dalian Wanda Commercial Proper es Co. Ltd (DWCP) is one of China’s largestcommercial and residen al property developers. The company’s ac vi es includedevelopment and sales of retail, office and residen al buildings; investment andopera on of large shopping centers; development and opera on of 5-star orsuper 5-star hotels; and property management.

The company is controlled by Wang Jianlin (54%), through its Dalian Wanda groupand other en es. The company had its IPO in December 2014, and in March2016 its controlling shareholder announced it was planning an offer for holders ofH shares (14.4% of total shares outstanding). The offer of HK$ 52.80 per sharewas officially announced on May 30, 2016 and later accepted by the DWCP’scommi ee of independent directors. While the transac on is structured as atender offer, holders of H shares must vote on the delis ng of the company at anAug. 15 shareholder mee ng in order for the tender offer to be declareduncondi onal.

Dutch pension fund APG (5.0% of H shares) has stated the offer raises concerns,causing the spread to widen substan ally upon APG’s announcement on June 29,2016. Currently the shares trade at a 10% discount to the offer price. The dealrequires approval by 75% of votes of H shareholders, and no more than 10% ofthe H shares outstanding vo ng against it.

Key Events

March 30, 2016 Dalian Wanda Group considering offer for DWCP

May 30, 2016 Dalian Wanda Group announces offer for DWCP

June 29, 2016 News of shareholder opposi on

Aug. 15, 2016 EGM

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 9

August 1, 2016ISS Special Situations Research

Strategic RationaleThe company does not provide a strategic ra onale to support the Dalian WandaGroup takeover offer, but the bidder encourages shareholders to accept the offerbased on:

Premium valua on, as the offer represents a premium of approximately36.1% over the closing price of HK$38.80 per H Share on 30 March 2016,being the closing price on the date of announcement (which announcementwas made a er trading hours that day), and a premium of approximately10.0% over the IPO price;

Certain and immediate premium for illiquid H Shares;

Avoiding holding unlisted shares, as the H shares will be delisted should thetender offer be declared uncondi onal; and

A third party is unlikely to be willing to pay a considerable premium for the HShares, given the controlling shareholding of the Dalian Wanda Group.

The poten al offer was announced barely 16 months a er the company’s IPO,and it seems reasonable to ques on whether the offer somehow contradicts thera onale for the IPO or market condi ons have changed so much as to jus fy asale.

In December 2014 the company had already warned over the sustainability of realestate market growth in China, sta ng that "the PRC property market is affectedby the recent slowdown in China’s economic growth. There have been increasingconcerns over the sustainability of the real estate market growth in China" (IPOprospectus).

In its 2015 Annual Report, the company stated that "China is s ll facingdownward pressure with the rate of industry growth slowing down, localgovernments have implemented a series of policies rela ng to the real estateindustry in 2015, covering a cut in interest rates and a reduc on of the reservesthat certain banks must hold, a reduc on of down payment for housingaccumula on fund loan (which is a special housing loan offering to those eligiblepersons who have made contribu on to the housing provident fund in the PRC),tax incen ve and li of home buying restric ons. These helped the real estate

industry to gradually recover from depression" (2015 Annual report).

The wording from the company reports does not seem to reflect a heightenedlevel of concern from management vs. the me of the IPO, though the situa onin China indeed deteriorated in the interim period between the two reports.The total investment in real estate development grew by 1.0% in 2015, ascompared to a growth rate of approximately 19.8% in 2013 and 10.5% in 2014.On Jan. 10, 2016, the company announced it was expec ng contracted sales todecrease by 39% in 2016. During the first five months of 2016 the company’scontracted sales declined by 12.0% or HK$ 4.9 bn, though this was par allycompensated by an increase in HK1.7 bn in rental and hotel income, which ismore recurring in nature. China Resources Land, probably the closest listedpeer, achieved a 49% increase in contracted sales over the same period.

Credit ra ng agencies have put the company on nega ve watch (Moody's) ordowngraded it (S&P):

"However, the company's ra ng outlook remains nega ve, reflec ng ourconcerns that its credit metrics will weaken in the next 12-18 months andwill pressure its Baa2 ra ng," says Kaven Tsang, a Moody's Vice Presidentand Senior Analyst. ..The nega ve outlook also reflects our concern thatDWCP's liquidity posi on will weaken as its scales back contractedsales" (Moody's, Feb. 18, 2016).

"The downgrade reflects our view that Wanda Commercial's aggressiveexpansion appe te to grow its investment property por olio could result inhigher financial leverage over the next 24 months than we had previouslyan cipated," said Standard & Poor's credit analyst Ma hew Kong. “Thecompany's cash flows are also likely to weaken because the significantreduc on in contracted sales will offset the robust growth in rentalincome." (The Standard, Feb. 3, 2016).

The decrease in contracted sales seems intended to some extent, as thecompany pushed through inventory during the booming years and has nowdecelerated sales in a weaker market (and cut acquisi ons of new land). Thecompany started talking about a change to an “asset light” strategy shortlya er the IPO, heading in the direc on of making ownership and opera on ofproper es (shopping centers and hotels) its main business, with property

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 10

August 1, 2016ISS Special Situations Research

development (apartments and offices in shopping mall complexes) a secondaryone.

Analysts are divided on the risks of this strategy, though if there is a consensusthat seems to be that it will be a bumpy road managing the transi on in businessmodel with a slowdown in the market and financial leverage. Some analysts wereconcerned that the sharp cut of contracted sales target to the difficult physicalproperty market in lower- er ci es where Wanda has majority presence, not amanaged strategic transi on to an asset light model.

Deal Process, Terms, and Governance

Deal Process:

The deal process is rela vely simple given the company’s status as a controlledcompany. The company was approached by its controlling shareholder, and theboard set up an independent commi ee to evaluate the offer. The commi eein turn appointed its own financial advisor to evaluate the transac on.

Terms

The offer of HK$ 52.80 per share was officially announced on May 30, 2016 andlater accepted by the DWCP’s commi ee of independent directors. While thetransac on is structured as a tender offer, minori es should vote on thedelis ng of the company assuming the tender offer is successful. The tenderoffer is condi onal on approval of the delis ng.

The deal requires approval by 75% of votes of H shareholders, and no morethan 10% of the H shares outstanding vo ng against it.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 11

August 1, 2016ISS Special Situations Research

Valuation Analysis

The following analysis is not intended to defini vely determine the per-sharevalue. Valua on is as much art as science and is highly dependent on the

underlying assump ons over which reasonable people can disagree. As such, ouranalysis is meant merely to indicate a poten al range of value that in our opinion,

and based on public informa on, appears to be reasonable.

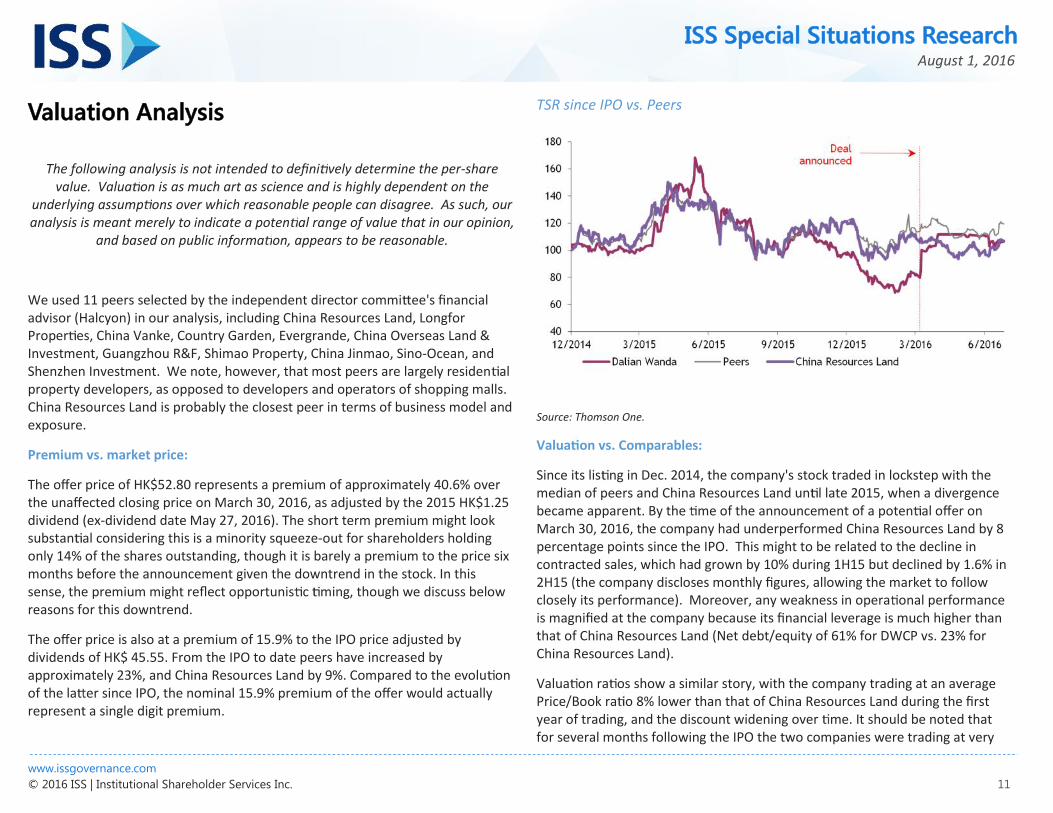

We used 11 peers selected by the independent director commi ee's financialadvisor (Halcyon) in our analysis, including China Resources Land, LongforProper es, China Vanke, Country Garden, Evergrande, China Overseas Land &Investment, Guangzhou R&F, Shimao Property, China Jinmao, Sino-Ocean, andShenzhen Investment. We note, however, that most peers are largely residen alproperty developers, as opposed to developers and operators of shopping malls.China Resources Land is probably the closest peer in terms of business model andexposure.

Premium vs. market price:

The offer price of HK$52.80 represents a premium of approximately 40.6% overthe unaffected closing price on March 30, 2016, as adjusted by the 2015 HK$1.25dividend (ex-dividend date May 27, 2016). The short term premium might looksubstan al considering this is a minority squeeze-out for shareholders holdingonly 14% of the shares outstanding, though it is barely a premium to the price sixmonths before the announcement given the downtrend in the stock. In thissense, the premium might reflect opportunis c ming, though we discuss belowreasons for this downtrend.

The offer price is also at a premium of 15.9% to the IPO price adjusted bydividends of HK$ 45.55. From the IPO to date peers have increased byapproximately 23%, and China Resources Land by 9%. Compared to the evolu onof the la er since IPO, the nominal 15.9% premium of the offer would actuallyrepresent a single digit premium.

TSR since IPO vs. Peers

Source: Thomson One.

Valua on vs. Comparables:

Since its lis ng in Dec. 2014, the company's stock traded in lockstep with themedian of peers and China Resources Land un l late 2015, when a divergencebecame apparent. By the me of the announcement of a poten al offer onMarch 30, 2016, the company had underperformed China Resources Land by 8percentage points since the IPO. This might to be related to the decline incontracted sales, which had grown by 10% during 1H15 but declined by 1.6% in2H15 (the company discloses monthly figures, allowing the market to followclosely its performance). Moreover, any weakness in opera onal performanceis magnified at the company because its financial leverage is much higher thanthat of China Resources Land (Net debt/equity of 61% for DWCP vs. 23% forChina Resources Land).

Valua on ra os show a similar story, with the company trading at an averagePrice/Book ra o 8% lower than that of China Resources Land during the firstyear of trading, and the discount widening over me. It should be noted thatfor several months following the IPO the two companies were trading at very

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 12

August 1, 2016ISS Special Situations Research

similar valua ons, despite China Resources Land being controlled by thegovernment, something for which analysts tend to assign a premium in China.When the poten al transac on was announced, that discount had widened to19%. If one values the company at the average discount of the first year oftrading, its fair Price/Book mul ple would be 1.07x. The offer price implies aPrice/Book ra o of 1.13x, or an approximately 6% premium to this normalizedra o.

Price to Book Ra o vs. Peers

Source: Thomson One.

Analyst Target prices:

The valua on divergence vs. peers since late 2015 is also evident when comparingthe company's stock price with the consensus target price. The gap betweentarget prices and stock price kept on widening un l early 2016.

At the me of the poten al offer announcement on March 30, 2016, the companywas trading at a 40.6% discount to the unaffected target price, vs. 33.3% for ChinaResources Land. The offer price of HK$ 52.80 is a 21.6% discount to theunaffected target price.

Stock price vs. Consensus Target Price (CNY)

Source: Thomson One.

Comparison to similar deals:

The one-day premium of 40.6% compares well with similar deals that weresuccessful as reported in the fairness opinion (median of 32.4%). Over longerlook-back periods that advantage dissipates: the 180-day premium to theaverage of daily prices of 16.0% looks low vs. the 52.2% for the median ofsimilar successful deals.

According to the fairness opinion, the transac on implies a 10.8% discount tothe company's adjusted NAV (i.e. using the appraiser's valua on for thecompany's real estate), lower than the average discount to Adjusted NAV of32.4% for similar deals, and actually the lowest of all deals in the sample. Wenote that the other deals involved developers of residen al property mostly,which tend to trade at higher discounts.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 13

August 1, 2016ISS Special Situations Research

Conclusion:

At first glance, the offer appears opportunis c given the weakness in thecompany’s share price since late 2015. But there seems to be credible reasons forat least part of that weakness: a decline in contracted sales coupled with higherleverage during a sluggish period for the Chinese economy. If these concernswere misplaced, and one would value the company based on the stock evolu onand historic discount to Price/Book ra o of China Resources Land, then the dealwould imply a single digit premium, low even for minority squeeze-out standards.The other end of the spectrum is arguing that the 40% one-day premium isreflec ve of intrinsic value, given the decline in fundamentals.

www.issgovernance.com© 2016 ISS | Institutional Shareholder Services Inc. 14

August 1, 2016ISS Special Situations Research

Conclusion and Vote RecommendationThe company is going though its first cyclical downturn as a listed en ty, a periodthat is o en associated with the “opportunis c ming” label for deals. For Asiandeals led by a controlling shareholder, in par cular, this triggers a heightenedlevel of concern for many investors.

The first ques on shareholders face is why they should accept such a premium inthis part of the cycle. While analysts are divided on the risks, there is a consensusthat it will be a bumpy road managing the transi on in business model with aslowdown in the market and financial leverage.

The second ques on is whether shareholders are being properly compensated forgiving up the poten al upside. There seems to be valid reasons behind the shareprice underperformance that preceded the announcement of the takeover: adecline in contracted sales coupled with higher leverage during a sluggish periodfor the Chinese economy.

If these concerns were misplaced, and one would value the company based onthe stock evolu on and historic discount to Price/Book ra o of China ResourcesLand, then the deal would imply a single digit premium, low even for minoritysqueeze-out standards. The other end of the spectrum is arguing that the 40%one-day premium is reflec ve of intrinsic value, which seems an exaggera onwhen the deal premium s ll implies a 10% discount to NAV. A mid-point, whichseems a realis c assump on given the industry and strategic background, wouldimply a reasonable premium in a cash deal for minori es holding 14.4% of sharesoutstanding.

Based on these factors, we recommend shareholders vote FOR the transac on.

The Global Leader in Corporate GovernanceIns tu onal Shareholder Services Inc. (ISS) is the leading provider of corporate governance solu ons for asset owners, investment managers, and asset serviceproviders. ISS’ solu ons include objec ve governance research and recommenda ons, end-to-end proxy vo ng and distribu on solu ons, turnkey securi esclass-ac on claims management, and reliable global governance data and modeling tools.

More than 1,600 clients turn to ISS to apply their corporate governance views, iden fy governance risk, and manage their complete proxy vo ng needs on aglobal basis. ISS is a global company with more than 900 professionals located across 17 offices in 12 countries.

For more informa on, please visit: www.issgovernance.com

The issuer that is the subject of this analysis may have purchased self-assessment tools and publica ons from ISS Corporate Solu ons, Inc. (formerly known as ISS Corporate Services, Inc. andreferred to as "ICS"), a wholly-owned subsidiary of ISS, or ICS may have provided advisory or analy cal services to the issuer in connec on with the proxies described in this report. These tools andservices may have u lized preliminary peer groups generated by ISS’ ins tu onal research group. No employee of ICS played a role in the prepara on of this report. If you are an ISS ins tu onalclient, you may inquire about any issuer's use of products and services from ICS by emailing [email protected].

This proxy analysis and vote recommenda on has not been submi ed to, nor received approval from, the United States Securi es and Exchange Commission or any other regulatory body. WhileISS exercised due care in compiling this analysis, it makes no warranty, express or implied, regarding the accuracy, completeness or usefulness of this informa on and assumes no liability withrespect to the consequences of relying on this informa on for investment or other purposes. In par cular, the research and vo ng recommenda ons provided are not intended to cons tute anoffer, solicita on or advice to buy or sell securi es nor are they intended to solicit votes or proxies.

ISS is an independent company owned by en es affiliated with Vestar Capital Partners (“Vestar”). ISS and Vestar have established policies and procedures to restrict the involvement of Vestarand any of Vestar’s employees in the content of ISS' analyses. Neither Vestar nor their employees are informed of the contents of any of ISS' analyses or recommenda ons prior to theirpublica on or dissemina on.

The issuer that is the subject of this proxy analysis may be a client of ISS or ICS, or the parent of, or affiliated with, a client of ISS or ICS.

One or more of the proponents of a shareholder proposal at an upcoming mee ng may be a client of ISS or ICS, or the parent of, or affiliated with, a client of ISS or ICS. None of the sponsors ofany shareholder proposal(s) played a role in preparing this report.

ISS may in some circumstances afford issuers, whether or not they are clients of ICS, the right to review dra research analyses so that factual inaccuracies may be corrected before the report andrecommenda ons are finalized. Control of research analyses and vo ng recommenda ons remains, at all mes, with ISS.

ISS makes its proxy vo ng policy forma on process and summary proxy vo ng policies readily available to issuers, investors and others on its public website:h p://www.issgovernance.com/policy.

- - -

Copyright © 2016 Ins tu onal Shareholder Services Inc. All Rights Reserved. This proxy analysis and the informa on herein may not be reproduced or redisseminated in whole or in part withoutprior wri en permission from ISS.