Embed Size (px)

DESCRIPTION

Islamic Finance in the UK

Citation preview

Copyright © 2011 Tuffin Ferraby Taylor 1 All rights reserved

Copyright © 2011 Tuffin Ferraby Taylor 2

All rights reserved

Contents: Foreword p.3 Introduction p.4 Islamic finance basics p.8 Focus on important terms p.11 State of the current market p.16 Conclusion p.18 Preface This piece is meant to be an introductory guide, which does not make assumptions about the reader’s familiarity with Islamic principles and claims no religious authority. Instead, this piece focuses on the work others have done in the field of contemporary Islamic finance, and attempts to summarise the current trends of a system which is still in the initial stages of development and prone to changes and obstacles in the short term. Furthermore, many of the Arabic terms used in this piece, such as Shari’a, can be written in many different ways (such as Shari’ah, Sharia, Shyriah, etc.). The spellings chosen for this piece were those that were most commonly used and/or easiest to read and pronounce for non-Arabic readers. Similarly, conventions vary for capitalisation and italicisation. This piece uses conventions common in other pieces on Islamic finance, and italicises most terms to help the reader learn unfamiliar words.

Copyright © 2011 Tuffin Ferraby Taylor 3 All rights reserved

This guide to Islamic finance will appeal to those UK businesses seeking to gain a better understanding of the issues involved and to indicate some of the underlying principles of Shari’a law which influence them.

The Shard and the Chelsea Barracks redevelopment are two recent examples of developments that illustrate the growing significance of Islamic-based finance. We believe that the principles of Islamic finance will become an increasingly important consideration when providing Technical Due Diligence and Project Monitoring advice.

This is clearly a major growth area and London is emerging as a global centre for Islamic finance.

To help understand this approach to finance, we have developed this original piece of research designed to provide an informed introduction to the subject.

Alan Pemberton Managing Partner Tuffin Ferraby Taylor LLP

Fore

word

Copyright © 2011 Tuffin Ferraby Taylor 4

All rights reserved

Background A large portion of the world’s population is currently unable or unwilling to participate in conventional financial systems because of religious constraints. The creation of an Islamic financial system is an attempt to be more inclusive of many of these individuals while also establishing ethical investment structures. These systems are based on concerns for equity and justice, responsibility towards weaker parts of society, and other moral obligations and principles.i As such, they are part of the large and recent growth in environmentally conscious and socially responsible property investment. The basis for the ethical grounding of these new Islamic financial structures lies in overarching guiding principles, as determined by Shari’a law, which is built on interpretations of Islam by prominent scholars to help guide the daily lives of practicing Muslims. In the context of real estate, these principles are primarily concerned with avoiding riba (financial interest), gharar (uncertainty), and forbidden (haram) activities. The implications of these three principles will be discussed in greater detail later in this paper. Recent History

During the early development of modern Islamic finance during the 1980s, many institutions in Islamic countries made changes that were only skin deep, leading to widespread scepticism that Islamic finance was simply a renaming of western finance.ii For individuals who are unaware of recent changes in Islamic finance, this scepticism may remain. Transparency and clarity are therefore essential in the establishment of any Islamic finance system today.

More recently, Islamic finance systems have shown noticeable resilience and stability during the financial crises, with some observers arguing they have withstood the pressures of the financial downturn better than conventional financial systems, a fact that has not gone unnoticed by regulators and investors.iii This stability has even proven attractive to non-Muslims, who have also invested in many Shari’a-compliant financial systems, particularly in Malaysia.iv While Asian countries like Malaysia and Indonesia tend to gravitate towards a more regulated solution to the drive for Islamic finance transparency and standardisation, those in the Middle East prefer to respond to market demand.v In fact, the Islamic finance industry is rapidly transforming from niche to mainstream, with worldwide banking assets estimated at US$750 bn in 2007, with a growth rate of 15 to 20 percent per annum.vi By 2010, the Islamic financial industry reached $1 trillion, and is continuing to grow.vii Islam is the fastest growing religion in the world viii, and within the next decade, the Islamic finance industry is likely to capture half the savings of the 1.6 billion practicing Muslims ix, at which point Standard & Poor’s estimate the global market for Islamic finance could reach $4 trillion in total (Currently, however, only around 15% of Muslims are interested in Islamic finance x). The driving force behind the vast majority of this growth comes from the under-30 segment of the Islamic world in response to a resurgence of interest in their cultural and religious identity.xi

Intr

oduc

tion

Copyright © 2011 Tuffin Ferraby Taylor 5 All rights reserved

In East Asia, the population, and potential market for Shari’a compliant finance, is 28.7m in Malaysia (60,4% Muslim) and 245.6m in Indonesia (86.1% Muslim).xii In the Gulf Cooperation Council countries, the figures are as follows: 26.1m in Saudi Arabia (100% Muslim), 5.1m in the United Arab Emirates (96% Muslim), 3m in Oman (95% Muslim), 2.6m in Kuwait (85% Muslim), 1.2m in Bahrain (81.2% Muslim), and 850k in Qatar (77.5% Muslim).xiii

In addition, while only 2.7% of the UK’s population is Muslim, there are still over twice as many Muslims in Britain as there are people of any denomination in Qatar.

Because Islamic investors seek stable, periodic income streams which are equivalent to interest incomes on conventional bonds or loans, they find real estate an attractive investment. Its relatively fixed and periodic cash flow through its rental stream provides exactly what Islamic investors are looking for, and structurally there is little difference between a non-geared conventional real estate fund and one which is Shari’a compliant.xiv As an asset class, real estate is attractive to any investor because of its value for diversification and risk reduction, as returns have relatively low correlations with other asset classes. Real estate helps hedge inflation as well, since rental streams can increase with inflation. Furthermore, unlike other types of investment, the investor has direct control over some aspects of

performance (through property improvements and renovation). xv Tenancy and contractual agreements often require amendment to comply with Shari’a principles, but the changes are far less complicated than those required to adapt other asset classes.xvi Additionally, for Shari’a compliant real estate investments in Europe, the total returns have been similar to the marketplace as a whole, ranging from 10 to 18 percent between 2001 and 2006.xvii

In the UK

The Gulf States and Malaysia are currently the main centres for Islamic finance, but the

There are now over 2 million

Muslims permanently

residing in the UK 17

Copyright © 2011 Tuffin Ferraby Taylor 6

All rights reserved

UK is perceived as very progressive.xviii Exact figures are hard to come by, but RICS xix found that Middle Eastern investment in European real estate totalled around £827 mn in 2001, of which around 91% ended up in the UK, a 225% increase over the previous year. Furthermore, RICS estimated in 2006 that 11% of total foreign investment in UK commercial property came from the Middle East, a significant rise from around 4% in 2004. In London itself, the numbers are much higher. In 1998, for example, over 20% of commercial property investment came from the Muslim world.xx The UK remains the favoured destination for Shari’a compliant funds in Europe, especially in London, which has a key competitive edge due to a broad range of available skills coupled with conscious regulatory and tax regime changes.xxi In addition, London is closer to the time zones of Middle-Eastern states than New York or Los Angeles, and benefits from New York’s perceived indifference to Islamic finance.xxii In addition, Birmingham is itself striving to become the Islamic finance centre of Europe. Islamic finance in the United States should not be discounted, however. It has remained off the radar since 9/11, but there is evidence that the US has larger Islamic finance market than the UK.xxiii In 2006, Gordon Brown stated that he wanted to see London become the global centre for Islamic finance xxiv, a sentiment that has been echoed repeatedly by prominent business and government leaders. According to the Bureau of National Affairs, London is already the strongest Islamic financial centre outside of the Muslim World.xxv

In commercial real estate, the effect has been noticeable. Not only has Islamic finance funded landmarks like the Shard, it is also expected to facilitate the construction of 10,000 homes in London - worth an estimated £5bn in investment from overseas buyers looking for high-end residential developments. This has been aided even further by the recent political upheaval in Egypt, Tunisia, and Libya, which will likely lead to investment from cash-rich buyers seeking a stable and stable location to lock up their wealth.xxvi Furthermore, UK banks are fighting to reduce property debt, which may be as high as £224bn. Half of the loans are set to mature by 2013, with £45.9bn of debt due to mature in 2011 alone. In 2010, lenders took possession of and sold property worth £500m, while ‘writing off’ a further £500m.xxvii Key property lenders, like RBS and Lloyds TSB will have to find new homes for their debt to reduce their exposure, and sovereign wealth and overseas funds are well placed to acquire this property and debt. Many of these potential investors could come from predominantly Islamic countries, so long as Shari’a compliant investment criteria are catered for adequately. UK Policy

The UK government’s approach has been primarily reactive so far, only enacting legislation when specific problems arise in the development of Islamic finance.xxviii However, HMRC have been very receptive to ensuring the tax treatment of Islamic finance is no more onerous than conventional finance.xxix Keeping that in mind, the Bureau of National Affairs states that taxation policy still needs

Copyright © 2011 Tuffin Ferraby Taylor 7 All rights reserved

attention to ensure the future growth of the sector.xxx One of the regulatory hurdles overcome already is the elimination of double stamp duty on Islamic mortgages, which occurred both upon purchase of the property by the bank and on the transfer of the property to the customer at the end of the mortgage. This was fixed by government legislation in 2003 to ensure a single stamp duty occurred instead.xxxi

The government also brought Ijara contracts within the FSA’s regulatory framework under the Finance Act 2007 as Home Purchase Plans (HPPs) to level the playing field and provide equal protection for customers in relation to conventional household mortgages.xxxii 2007 also saw commitments to legislative changes that would facilitate Shari’a-compliant insurance (takaful) in the UK.xxxiii Furthermore, the previous UK government looked into a rolling programme of up to £2 bn of sovereign sukuk issuance. Although they announced in 2009 that such an issuance would not provide value for money in the prevailing economic climate, they stated that they would continue to keep the situation under review. It remains to be seen what impact the current coalition government will have on Islamic financial regulation and incentives. If sovereign sukuk issuance is revived, investment potential looks good. There are strong signs that as the global marketplace recovers, investors are happy to buy more exotic instruments, like Islamic bonds.xxxiv

Copyright © 2011 Tuffin Ferraby Taylor 8 All rights reserved

Isla

mic

Fin

ance

Bas

ics Introduction

In discussing Islamic finance, it is important to start by noting that in many cases, Islamic finance may appear to be almost identical to conventional finance to the casual observer.xxxv This is essential to understanding Islamic finance as a whole, as in most cases Islamic finance has the same goals as conventional finance in regards to solving financial puzzles. Islamic finance, however, uses a different approach to solving the same puzzle, with similar end results. The principals of Shari’a law that affect Islamic finance are derived from the Quran, Islam’s Holy Book, and the Sunnah, the Sayings and Acts of the Prophet Mohammed. In regards to real estate, these principles are primarily concerned with avoiding 3 items: riba, gharar, and forbidden (haram) activities. The concepts can be sophisticated, but are summarised below. Riba

Riba is the Arabic term for financial interest. The banning of interest under Shari’a law means that traditional mortgage structures, for example, are forbidden, as they require the payment of interest over the length of a contract. For most Islamic investors, this has proven to be the main barrier to investment, and has therefore been the main focus of legal and financial changes to make Islamic finance possible in the UK (along with the taxation implications of these changes). Thankfully, most of the financial needs conventionally met by interest-bearing contracts can be met by alternative Islamic financing methods, though there are a few complications to keep in mind. An important consequence of the condemnation of riba is that charging

increased rates for deferred payments, such as for late rental payments in a lease, is also forbidden under some interpretations of Shari’a law. Instead, rates can be set higher, with reduced charges for earlier payments. This reverse tactic has received almost unanimous acceptance in recent years, although some of its financial applications remain controversial.xxxvi Instead of interest on late payments, it is also acceptable for the financial institution to ask the client to make a payment to charity as penalty.xxxvii It is important to note, however, that some Shari’a compliant financial services do charge late fees to cover additional administrative costs.xxxviii While this should be considered as an option, it could appear to clients as disingenuous. While interest was originally prohibited based on divine authority, Muslim scholars have also recently contested the theory behind interest. They have rebutted arguments that interest is a reward for savings, a product of capital, or provides for differences between the value of present and future goods.xxxix Instead, they argue that prohibiting interest results in shared risks for borrower and lender, and ties rewards to the performance of the business venture itself. This means that returns are more equitable during positive and negative economic circumstances, and are only earned when a business venture adds value to society.

It is important to note that many Muslims have chosen to disregard the ban on interest in order to participate in the global banking system.xl It is also important to remember that Shari’a-compliant investments are guided by personal ethics, though exceptions are sometimes made when Shari’a-compliant services are unable to meet the needs of a

Copyright © 2011 Tuffin Ferraby Taylor 9 All rights reserved

client. In essence, these investments are often driven by moral commitments, and attempts to incorporate these methods should aim to address these needs. These are not made to fulfil UK legal requirements, but personal and religious standards. Any conflicts will be solved legally under UK laws, not Shari’a law. Gharar

The term gharar is used to denote uncertainty, which is prohibited in Shari’a-compliant financial contracts, as ambiguous contracts are considered a form of deception. It is therefore essential that any potential investment contract tackles transparency from the outset. This also means that the sale of an item that may or may not exist, such as the future harvest of an oyster diver, is also forbidden. This is because the buyer cannot know what sort of harvest he will receive. However, if the diver is paid based on a fixed number of hours of work, the contract is permitted. In this case, the object being sold is well defined, and therefore allowed. It’s easy to see that in most cases, gharar can be eliminated from contracts by ensuring ambiguities are non-existent.xli When applied to real estate investment, one can see that conventional insurance would be forbidden, as the insured may never collect any money from the insurance company (in addition to the fact that many insurance companies invest significant portions of their funds in interest-bearing bonds or accounts).xlii To meet this need, Islamic insurance funds called takaful can be employed (see the next section for more information on these funds).

One more example which may be important to consider is that contemporary forwards, futures, and options are not permitted, as they are considered non-concluded and therefore invalid.xliii For example, agreeing to sell a property for a fixed amount in a month’s time is forbidden, as is selling a property on an unpredictable future condition, such as on the condition that the investor’s funds increase by 20% in the next quarter. Contracts must be in regard to immediate deals only, and only deal in assured outcomes. While there is some uncertainty contained in rent reviews, they are usually considered to be compliant - though there are usually caps on rent changes built into contracts. Forbidden activities

As stated previously, the prohibition of riba ensures that all business ventures add value to society. It follows then that ventures which are considered to destroy value according to Islamic beliefs are also forbidden. These ventures include investments in defence/armaments, gambling, alcohol, tobacco, pork products, pornography, and cinemas (though cinema’s are likely to be considered compliant in the UK, they will not

“Spending by buyers from the Middle East is one of the main factors which has protected sales of new-build housing in London compared to other

parts of the country” Simon Brown, Northland Capital 18

Copyright © 2011 Tuffin Ferraby Taylor 10 All rights reserved

be in regions like Saudi Arabia). Real estate investments involving buildings with tenants involved in any of these businesses could be a problem and, so again, transparency is key.

For large real estate investments, it is likely that a small proportion will not comply with Shari’a Law – such as a supermarket which also sells alcohol. This may seem like a deal breaker, but in many instances exceptions are made for the sake of pragmatism. Some Shari’a boards allow up to 5% of an investment to be non-compliant, for example. In addition, this non-compliance can be offset by donations to charity in a process called ‘portfolio purification’.xliv

Copyright © 2011 Tuffin Ferraby Taylor 11 All rights reserved

Focu

s on

Impo

rtan

t Te

rms Financing methods and structures

A number of alternative financing methods have arisen which are permitted and fully compatible with the principles of Shari’a law. However, all such structures have to be certified by the Shari’a Board, a panel of expert scholars with the expertise to interpret Islamic law. In addition, every financial transaction must be scrutinised by the Shari’a Board to ensure full compliance. The key financing methods currently used are listed below. Note: the Arabic names for contracts are often used in the industry to reinforce credibility. xlv Sukuk

Similar to a conventional bond, but asset backed. The asset is leased to a client to yield a return on investment, and the asset itself has proportionate beneficial ownership. Sukuks are popular in the UK, but they currently encounter difficulties when applying tax rules that normally apply to debts.xlvi The tax costs to potential investors are equivalent to conventional financing, however. In fact, despite a general slowdown in sukuk issuance as a result of the credit crisis and general uncertainties regarding the Shari’a-compliance of existing structures, the London Stock Exchange saw £2.8bn raised from six sukuk issues. This is part of the £9bn raised since the first London-listed sukuk was launched in 2006.xlvii It should also be noted that Japan has also begun to enter the sukuk market, along with more traditional suppliers of Islamic finance.xlviii

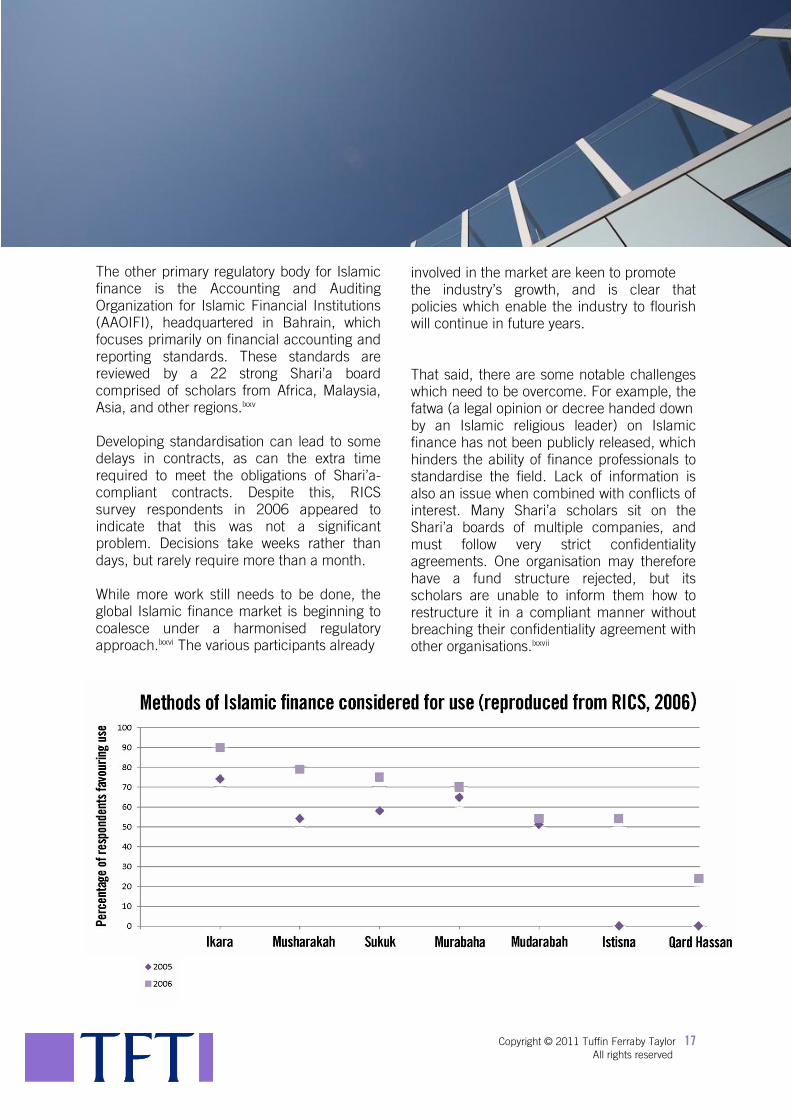

Ijara

A Shari’a compliant lease agreement. Instead of a traditional interest-based loan, Ijara allows the financial institution to earn profits by charging rentals on a leased asset. This concept can be extended to a lease-purchase agreement in the form of Ijara-wa-iqtinah, which is binding to the lessor only, while the lessee may either purchase the property at the end of the lease for a pre-determined price, or return it to the lessor. Ijara is the most popular financial structure for property investment, and its popularity is only growing. Of those surveyed by RICS in 2006, 90% said it was their preferred financial structure, up from 74% in 2005. An important point to note here is that the obligation to conduct major maintenance and insure the leased asset lies with the lessor.xlix This eliminates any uncertainty arising from tenants’ dilapidations obligations contained in conventional (or fully, repairing and insuring) leases. Murabahah Purchase by a financial institution with resale to the client with a predetermined premium, such as 110% of the original price (this premium must be determined as a percentage, and not as a lump sum). The capital user pays this higher price in instalments, effectively obtaining credit without paying interest. An important note must be made here that when the contract is signed, the financial institution must already own the property or item in question.l This means that the capital provider must bear the full risk that the client may back out of the contract prior to signing. As stated earlier, prohibitions on riba mean that late instalment payments cannot result in

Copyright © 2011 Tuffin Ferraby Taylor 12 All rights reserved

added interest payments. Instead, the contract can only give discounts on early payments. Additionally, the mark-up included in the contract cannot be altered during the life of the contract. Therefore the contract cannot be linked with inflation or indices. It should also be noted that Islamic mark-up contracts have a distinctive advantage for asset control in the case of client defaulting. Most conventional debt contracts result in bankruptcy proceedings during which the client retains asset control. In Islamic mark-up contracts, however, the financial institution retains control of the asset until the client makes the final payments.li

In 2010, Shari’a scholars rejected Murabahah as not being compliant in spirit. They are unlikely to disappear soon however, with few alternatives available.lii Mudarabah

An investment partnership similar to conventional limited partnerships, in which the investor provides capital to another party. Profits are shared on a pre-agreed ratio, but loss of investment is born solely by the investor, while the other party loses its share of anticipated income, and receives no compensation for their efforts.

Copyright © 2011 Tuffin Ferraby Taylor 13 All rights reserved

Musharakah

While the Mudarabah is analogous to a conventional arrangement between a fund manager and its investors, the Musharakah is akin to a joint venture partnership, being a partnership with both profit and loss sharing.liii Profits are shared according to an agreed ratio, while losses are proportional to the capital or investment or each partner. All partners have the right to exercise executive powers in the project if they wish, in a similar manner to a conventional partnership structure and the holding of voting stock in a limited company. This financing arrangement is often regarded as the purest form of Islamic financing.liv A sub-category exists in the form of Musharaka mutanaqisah (a diminishing partnership). In contrast to a leasing model such as Ijara, where the ownership of the property remains with the lessor for the entire lease period, in a diminishing partnership the financing agency and the customer share ownership.lv In this model, the customer’s payments contain both a rental payment for the portion of the property owned by the financing agency, and a buy-out payment for part of the overall ownership. Over time, the customer’s ownership share increases until they own the entire asset and the contract is completed. In the early part of the contract, a large portion of the payment is rent, and a small part is a buy-out payment. Towards the end, rental payments are small and the buy-out payments are larger. Istisna’a This contract is useful for the production of goods, including any process of manufacturing, assembling, construction, or packaging. It involves a party producing specific goods and services according to mutually-agreed specifications at a set price

for a fixed date of delivery. This contract exists primarily to circumvent issues caused by the forbidden sale of undefined future items or services, as discussed earlier under gharar. This contract requires many

Copyright © 2011 Tuffin Ferraby Taylor 14 All rights reserved

conditions to be met, and should be established with the help of an Islamic legal expert.lvi

Qard Hassan

Qard Hassan is an interest-free loan given either for short-term funding requirements or charity, as the borrower is only required to pay back the initial loan amount. These loans are not popular, and are rarely used.lvii Takaful

Traditional insurance companies are prohibited under Shari’a Law due to issues of riba and gharar, as noted earlier. The Islamic alternative is the creation of cooperative or mutual insurance company, which is owned entirely by its policyholders. Participating members pool funds to be used in the event of legitimate insurance claims. As already noted, conventional insurance is sometimes permitted when takaful insurance schemes are unable to provide appropriate coverage. Islamic Fund Management

There tend to be two filters on companies included in Islamic investment funds (such as the Dow Jones Islamic Index). The first filter excludes all companies whose primary practices involve forbidden products (such as tobacco or alcohol), and is fairly straight-forward.lviii The second filter rules out companies which carry interest-bearing debt, receive interest or other ‘impure’ income, or trade in debts at prices other than their face value. In addition, the Dow Jones Islamic Index excludes companies:

1. With a debt to total asset ratio of 33% or more

2. With non-compliant activities which

comprise more than 5% of revenue 3. With accounts receivable to total

assets ratio of 45% or more lix Islamic Real Estate Investment Trusts (I-REITs)

Malaysia’s Securities Commission released guidelines for Islamic REITs in 2005. Subsequently, these REITs have proven popular. The first two - Alaqar and BSDreit -focused on two property sectors, hospitals and oil palm plantations, with a combined assets in 2007 of around £200m.lx

Copyright © 2011 Tuffin Ferraby Taylor 15 All rights reserved

As with normal REITs, capital appreciation and the income from the real estate or companies are used to provide returns to investors.lxi They differ from normal REITs, however, in that they are lower risk and have portfolio diversification benefits.lxii The FMA also found that I-REITs are more stable in the long run (but not the short run), and that they seem to outperform non-restricted REITs.lxiii They also seem to provide a potential hedge against inflation, and appeal to pension funds and retirees, among others.lxiv To make these REITs Shari’a-compliant, the Malaysian Securities Commission lxv identified a few important guidelines: When a portion of rental is from non-

permissible activities, these rentals cannot exceed 20% of the I-REIT’s total turnover.

The I-REIT cannot own properties where all the tenants operate non-permissible activities.

For new tenants, the I-REIT cannot accept tenants whose activities are fully non-permissible.

If tenants operate mixed activities, only 20% of the floor area can be used for non-permissible activities. If the activities do not involve the usage of space, the Shari’a board will make a decision.

All forms of investment, deposit, and financing must be Shari’a-compliant.

The property insurance must be based on takaful schemes, unless such schemes are unable to provide coverage, in which case conventional insurance will be permitted.

In addition all properties and tenants I-REITS must be screened and approved by a Shari’a Board.lxvi Since 2001, at least 22 I-REITs have been created worldwide, raising over $3b in capital for investment.lxvii RICS stated in 2006 that once REITs made it to the UK, it was highly likely that Shari’a compliant REITs will be among the first established.lxviii While around 20 corporate groups have adopted UK REIT status since 2006, none have been Shari’a compliant.lxix There are challenges to implementing Islamic REITs in the UK (such as ensuring that while listed on a recognised stock exchange, non-Islamic investors are unable to change investments in a way which breached Shari’a-compliant rules), but none of these challenges are insurmountable.lxx

Copyright © 2011 Tuffin Ferraby Taylor 16 All rights reserved

Stat

e of

the

Curr

ent M

arke

t Providers of Islamic finance

According to the Banker lxxi, there were 20 conventional and three Islamic banks offering Islamic services in the UK in 2008. Islamic banks are noticeably different, in that their ‘depositors’ are shareholders and earn dividends when the bank profits or lose savings if the bank posts a loss.lxxii As of 2007, the total value of Shari’a compliant commercial property in the UK exceeds £329m, with ABC Islamic Asset Management as the leading market player in the UK. Other institutions which provide Islamic financial services include, but are not limited to, the following:

ABN AMRO ANZ Grindlays and Flemings American Express Bank of America Barclays BNP Paribas Citibank Commerzbank Deutsche Bank Goldman Sachs HSBC Kleinwort Benson Merrill Lynch Pictet & Cie Royal Bank of Canada Standard Chartered UBS

In addition, a survey by Tuffin Ferraby Taylor identified the following as major providers:

Abu Dhabi Islamic Bank Al Rajhi Bank Dubai Islamic Bank Islamic Bank of Britain Islamic Development Bank

Kuwait Finance House Royal Bank of Scotland Qatar Islamic Bank

Worldwide, the largest real estate fund has $1.6 b in assets and is run by HSBC Amanah. With around 600 properties, the fund is too large for Shari’a scholars to analyse each property individually. They therefore use a backbone document, which Shari’a Boards add approved modules to as needed.lxxiii Investors in Islamic Finance

The major investors of Islamic financial services are often the same as the major providers (see previous section). They also include various investment companies and fund managers, as well as individuals. As mentioned previously, the under-30 segment of the Islamic world is the leading group driving Islamic investment. It is important to note that Shari’a compliant commercial property and leasing funds are currently closed ended, with only a few wealthy institutions and individuals subscribing. They are also usually less liquid than conventional investments, with funds locked in for periods of 3 to 5 years and only limited options for redemptions. International standardisation and regulation

Based in Kuala Lumpur, the Islamic Financial Services Board (IFSB) is a multilateral body supported by the industry to construct guidelines for governance and regulation of Islamic Finance, as well as identify means of addressing Basel II issues. Its members include the International Finance Corporation, central banks from many Asian countries, and the UK Financial Services Authority (FSA).lxxiv

Copyright © 2011 Tuffin Ferraby Taylor 17 All rights reserved

The other primary regulatory body for Islamic finance is the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), headquartered in Bahrain, which focuses primarily on financial accounting and reporting standards. These standards are reviewed by a 22 strong Shari’a board comprised of scholars from Africa, Malaysia, Asia, and other regions.lxxv Developing standardisation can lead to some delays in contracts, as can the extra time required to meet the obligations of Shari’a-compliant contracts. Despite this, RICS survey respondents in 2006 appeared to indicate that this was not a significant problem. Decisions take weeks rather than days, but rarely require more than a month. While more work still needs to be done, the global Islamic finance market is beginning to coalesce under a harmonised regulatory approach.lxxvi The various participants already

involved in the market are keen to promote the industry’s growth, and is clear that policies which enable the industry to flourish will continue in future years. That said, there are some notable challenges which need to be overcome. For example, the fatwa (a legal opinion or decree handed down by an Islamic religious leader) on Islamic finance has not been publicly released, which hinders the ability of finance professionals to standardise the field. Lack of information is also an issue when combined with conflicts of interest. Many Shari’a scholars sit on the Shari’a boards of multiple companies, and must follow very strict confidentiality agreements. One organisation may therefore have a fund structure rejected, but its scholars are unable to inform them how to restructure it in a compliant manner without breaching their confidentiality agreement with other organisations.lxxvii

Copyright © 2011 Tuffin Ferraby Taylor 18 All rights reserved

Conc

lusi

on

Moving forward with commercial real estate London is already a magnet for global Islamic investment. Currently, however, much of that investment focuses on asset classes other than real estate, and property consultants are not actively involved in Shari’a-compliant property selection and renovation. This has the potential to change in the near future, especially with high-profile Shari’a compliant projects like the Shard already taking place. The £100bn or more in property debt set to mature by 2013 will also have a strong influence on future trends. Key property lenders, like RBS and Lloyds TSB will have to find new homes for their debt to reduce their exposure. Sovereign wealth and funds from predominantly Islamic countries are well placed to acquire this property and debt, so long as Shari’a compliant investment criteria are catered for adequately. This should not be difficult, as contractual amendments for Shari’a compliant real estate are somewhat flexible, and much simpler than the changes required for other asset classes. The principles of Shari’a law have implications for the contractual framework between landlords and tenants and in particular the clauses that detail payments and restrictive uses. Where Shari’a compliant funds acquire property or property debt the principles could also have implications for due diligence and specifically an analysis of existing leases. Conventional leases contain inherently uncertain provisions especially in relation to tenants’ repairing, redecorating and reinstating obligations; there is no contractual certainty over future financial liabilities. Generally, the parties have no contractual right to change the terms of a lease.

Islamic real estate finance can support the corporate social responsibility and sustainability obligations of many organisations by providing a robust ethical framework which can sit alongside those already established for environmental criteria. Socially responsibly investments as a whole are gaining momentum, and Islamic financial services have a significant role to play in their future development. This is especially true with younger investors, and it is no surprise that the recent surge in Islamic finance is being driven by investors under the age of 30. Overall, much of this growth is likely to be seen in London, which already has a very strong lead on the rest of Europe and the United States. In the UK, this growth is already being followed by other major cities like Birmingham, where Islamic finance is set to continue to grow. By adapting conventional finance methods to Shari’a principles, market leaders stand to make impressive returns in an otherwise slowly recovering market, and have increased access to international markets in East Asia and the Middle East. With over 1.6bn practicing Muslims worldwide, the potential for the UK property market cannot be overstated.

Copyright © 2011 Tuffin Ferraby Taylor 19 All rights reserved

Full References: ABC International Bank (2011) Sharia compliant refinance, at http://www.alburaq.co.uk/faqs.asp, accessed Jan 11, 2011 Abraham, R., Long, S., and Henderson, S. (2008) Real estate finance in Dubai, International Finance Law Review, 27, p. 60-62 Aston Business School (2011) Islamic Finance for Corporate UK Conference, June 16, 2011 Ainley, M., Mashayekhi, A., Hicks, R., Rahman, A. and Ravalia, A. (2007) Islamic finance in the UK: Regulations and Challenges, Financial Services Authority Central Intelligence Agency (2011) CIA World Factbook, available at http://www.cia.gov/library/publications/the-world-factbook El-Gamal, M.A. (2000) A basic guide to contemporary Islamic Banking and Finance, Rice University, Texas FMA (date unknown) The relative performance of debt-restricted Real Estate Investment Trusts (REITs): Does Faith Matter?, Paper #8701633 from FMA.org Hammond, E. (2011) Investors transform UK horizon, Financial Times, Special Report:Islamic Finance, May 12, 2011 Hwa, T.K. and Noor, A.R. (2007) Islamic REITs: a Syariah-compliant investment option, 12th Asian Real Estate Society Annual Conference, Macau, China Jessop, N., and Bell, S. (2009) Islamic finance: A key to London’s future prosperity?,Tax Planning International: Gulf States: Special Supplement, p. 9-13 Bureau of National Affairs Khan Iqbal (2001) Issues and relevance of Islamic finance in Britain, HSBC Amanah Finance, UK KPMG (2010) India Shariah Finance Summit 2010, New Delhi McMillan, M. (2011) Islamic Finance and the European Corporate: Misfit or Strategic Fit?, Presented at the Islamic Finance for Corporate UK Conference at Aston Business School, June 16, 2011 Miller (2007) UK welcomes the sukuk, International Finance Law Review, 26, p. 24-25 Newell, G. and Osmadi, A. (2010) Assessing the importance of factors influencing the future development of REITs in Malaysia, Pacific Rim Property Research Journal, 16, 3, p. 358-374 Oakley, D. (2011) Sukuk: Market shows resilience, Financial Times, Special Report:Islamic Finance, May 12, 2011

O’Neal, N.C. (2010) The development of Islamic finance in America: The future of Islamic Real Estate Investment Trusts, Real Property, Trust and Estate Law Journal, 44, p. 279-297 Osmadi, A.B. (2007) REITs: A new property dimension to Islamic finance, 13th Pacific-Rim Real Esatate Society Conference, Freemantle, Western Australia Rammal, H.G. (date unkown) Financing through musharaka: Principles and application, obtainable at http://www.islamicmortgages.co.uk/index.php?id=260 Royal Institution of Chartered Surveyors (2006) Current trends in Shariah property investment Royal Institution of Chartered Surveyors (2005) Sharia property investment: Developing and international strategy Simmons & Simmons (2010) Islamic Finance Timewell, S. (2008) UK on the verge of sukuk issuance, The Banker, April, p. 114-115 Thomas, D. (2011) Banks in race to shed commercial property debt, Financial Times, May 19, 2011 Ullah, H. and Tuppen, E. (2011) Islamic REIT... it’s just a matter of time, Global Islamic Finance, March 2011, p. 29-30 Vuong, H. (2009) In-Focus: Shariah compliant real estate investment, in PRUPIM’s International Real Estate Perspective, May 2009 Vuong, H. (2010) A principled approach, Investments and Pensions Europe, Feature: Sharia-Compliant Investment, March/April 2010, p. 55 Walmsley, G. (2010) Another year of growth and development for the London Stock Exchange markets for Islamic finance, London Stock Exchange Woychuck, I. (2011) Real Estate Investments: Advantages and Disadvantages, Investopedia, obtainable at http://www.investopedia.com/university/real_estate/real_estate4.asp

Copyright © 2011 Tuffin Ferraby Taylor 20 All rights reserved

Photos: The front cover was obtained from Flickr under creative commons licenses allowing for re-use with attribution, including for commercial purposes. Below is the web address of the work featured in this report:

http://www.flickr.com/photos/zoonabar/3138814931/ All other images are the copyright of Tuffin Ferraby Taylor. Citations (short form):

i KPMG (2010) ii El-Gamal (2000) iii KPMG (2010); BNA (2009) iv KPMG (2010); Zaher and Hassan (2001) v Vuong (2010) vi KPMG (2010); RICS (2006); Miller (2007) vii Aston Business School (2011) viii Zaher and Hassan (2001) ix KPMG (2010); Zaher and Hassan (2001) x Aston Business School (2011) xi KPMG (2010) xii CIA (2011) xiii CIA (2011) xiv Vuong (2010) xv Woychuk (2011) xvi Vuong (2009) xvii RICS (2006) xviii Jessop & Bell (2009) xix RICS (2005) xx Khan (2001) xxi Miller (2007); Walmsley (2010); RICS (2006); RICS (2005) xxii Jessop & Bell (2009) xxiii McMillan (2011) xxiv RICS (2006) xxv Jessop & Bell (2009) xxvi Hammond (2011) xxvii Thomas (2011) xxviii Jessop & Bell (2009) xxix Walmsley (2010) xxx Jessop & Bell (2009) xxxi Ainley, Mashayekhi, Hicks, Rahman, & Ravalia(2007) xxxii Ainley, Mashayekhi, Hicks, Rahman, & Ravalia (2007) xxxiii Miller (2007) xxxiv Oakley (2011) xxxv El-Gamal (2000) xxxvi El-Gamal (2000) xxxvii Rammal (date unknown) xxxviii ABC International Bank (2011) xxxix Zaher and Hassan (2001) xl O’Neal (2010) xli El-Gamal (2000) xlii El-Gamal (2000) xliii El-Gamal (2000) xliv RICS (2006); Vuong (2010) xlv El-Gamal (2000) xlvi See BNA (2009) for further details

xlvii Walmsley (2010) xlviii Miller (2007) xlix Abraham, Long, and Henderson (2008) l El-Gamal (2000) li Zaher and Hassan (2001) lii McMillan (2011) liii Vuong (2010) liv El-Gamal (2000) lv El-Gamal (2000) lvi El-Gamal (2000) lvii RICS (2006) lviii El-Gamal (2000) lix El-Gamal (2000) lx Hwa & Noor (2007) lxi O’Neal (2010) lxii Newell & Osmadi (2010) lxiii FMA (date unknown) lxiv FMA (date unknown) lxv Hwa & Noor (2007) lxvi Osmadi (2007) lxvii O’Neal (2010) lxviii RICS (2006) lxix Ullah & Tuppen (2011) lxx Ullah & Tuppen (2011) lxxi Timewell (2008) lxxii Zaher and Hassan (2001) lxxiii McMillan (2011) lxxiv Miller (2007) lxxv Miller (2007) lxxvi Miller (2007) lxxvii McMillan (2011)

Contact: David Mann, Partner [email protected] Mat Lown, Partner [email protected] Pemberton [email protected] www.tftconsultants.com