Embed Size (px)

Citation preview

Excellence in Integrated Reporting 2021

Is the most transformative perspective the one you don’t have?

B | Excellence in Integrated Reporting 2021

Purpose of the 2021 EY Excellence in Integrated Reporting survey The purpose of the survey is to encourage and benchmark standards of excellence in the quality of integrated reporting to investors and other stakeholders in South Africa’s listed company sector.

Over the years it became clear that financial statements on their own did not tell the whole story of a company’s performance. Companies therefore started reporting on their environmental impacts, employee-related issues and corporate social responsibility issues in a separate report often referred to as a sustainability report, which accompanies the financial information distributed to shareholders.

Since 2010, all companies listed on the Johannesburg Stock Exchange (JSE) have been required to produce an integrated report in line with King III. This requirement has been carried forward to King IV, effective for financial years commencing on or after 1 April 2017. In addition, the JSE requires application and disclosure of King IV in any report lodged with them after 1 October 2017.

EY has been commissioning the Excellence in Integrated Reporting survey for the last ten years in order to encourage excellence in the quality of integrated reporting to investors and other stakeholders by South Africa’s top companies.

Contact For more information on this survey, contact Larissa Clark, IFRS Desk Leader, EY Africa at [email protected].

Disclaimer The survey findings and rankings of the integrated reports have been independently prepared by the three adjudicators with affiliations to the University of Cape Town (UCT), comprising Professors Alexandra Watson (Emeritus Professor), Goolam Modack (College of Accounting) and Mark Graham (Graduate School of Business). Accordingly, the survey findings and ranking of the integrated reports are the views of the adjudicators.

The other material has been prepared for general information purposes only and is not intended to be relied on as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

Virtual workshop The Excellence in Integrated Reporting workshop will be held as a virtual event this year, due to the social distancing regulations in place. During the workshop we will:

• Provide an overview of the 2021 EY Excellence in Integrated Reporting survey results;

• Discuss positive and negative trends in integrated reporting;

• Highlight examples of leading practice, to assist companies to prepare their next integrated report;

• Reflect on how companies should deal with the on-going socio-economic effects of COVID-19 and the recent unrest in SA in their integrated reports; and

• Consider the requirements of the revised International <IR> Framework, published in 2021.

Date: Wednesday 29 September 2021 at 3pm with a replay on Tuesday 5 October at 10am.

Please contact [email protected]

For more information please visit: ey.com/en_za Follow us on Twitter: @EY_Africa

C | Excellence in Integrated Reporting 2021

Ajen Sita

Chief Executive Officer, EY Africa

Bothwell Mazarura

Chief Financial Officer, Kumba Iron Ore Ltd

Leigh Roberts

Chief Executive Officer, Integrated

Reporting Committee of South Africa

Mark Graham

Associate Professor, Graduate School of Business,

University of Cape Town

Alfred Visagie

Head Investor Relations, Nedbank Group Ltd

Stephen Ntsoane

Assurance Leader, EY Africa

Larissa Clark

IFRS Desk Leader, EY Africa

Excellence in Integrated Reporting 2020

D | Excellence in Integrated Reporting 2021

Leon Kok

Chief Financial Officer, Redefine Properties Ltd

Leila Fourie

Chief Executive Officer, JSE Ltd

Nicola Kleyn

Dean of Executive Education at the

Rotterdam School of Management; Member

of EYQ, EY’s Global think-tank

Gautam Jaggi

EYQ Global Insights Director, EY Global Markets

2020 Winners

Contents

02 Introduction

03 Leading with purpose – Reset for growth

04 Reimagining a purpose-led growth strategy

06 Integrated reporting – time to refocus?

08 Towards international sustainability standards

10 10 Years of integrated reporting in South Africa

12 2021 Rankings

14 Top 10 companies

17 Overall impressions at a glance

19 2021 Adjudicators’ observations and overall performance

23 The mark plan at a glance

24 The mark plan and adjudication process

26 About the adjudicators

27 How can EY help?

1 | Excellence in Integrated Reporting 2021

Contents

2020 will always be remembered as the year that brought us the COVID-19 pandemic. Office based employees were turned into Zoom and MS Teams experts overnight as gatherings were halted, international supply chains were disrupted, and international travel was restricted. As the COVID-19 pandemic spread to all corners of the world, our companies, industries and wider economy were severely impacted. It was challenging for most companies to deal with the immediate impact of the pandemic and remain resilient during this time.

2021 will be remembered as the year of the vaccine. As more vaccines become available and vaccination rates in South Africa start to increase, we are optimistic that restrictions will soon be lifted. In some parts of the world, people are slowly returning to their offices, restrictions on travel are being lifted and sporting events are allowing spectators.

2021 also brought South Africans other unique challenges as we saw widespread civil unrest and looting during July. The reactions to these events were as varied as the reasons therefor. At the same time, it was a powerful reminder of the importance of building an inclusive economy and society. Ajen Sita, our Africa CEO, considers the importance of entities having a clearly defined purpose and focussing on long-term value creation (see page 3).

Adversity, such as what South African companies have had to deal with over the past 2 years, creates an opportunity to revisit and reimagine our business strategies. As economies start to open up again and business can operate in a manner similar to that of the pre-pandemic era, it is important to recognise that a growth strategy cannot be based on the same assumptions and principles as before. It will not be a return to business as it once was. Businesses should use this

opportunity to revisit their strategies, to create sustainable and long-term value. We explore the five critical ingredients in formulating a purpose-led, long-term value strategy (page 4).

This has not only been a year of unprecedented economic uncertainty due to the pandemic and the recent South African civil unrest; we have also seen unprecedented developments on the reporting front. In April 2021, the Trustees of the IFRS Foundation, the oversight body of the International Accounting Standards Board (IASB), published a proposal to amend the IFRS Foundation Constitution to accommodate the formation and operation of an International Sustainability Standards Board (ISSB). This will pave the way for a global suite of sustainability standards under the banner of the IASB. We have included an interview with James Luke, IFRS Desk, EY Africa and member of the IASB Foundation’s Advisory Council, on these important developments and what they mean for South African reporters. We have also asked Alex Watson, Professor Emeritus, University of Cape Town, to share her perspective on the purpose of South African integrated reports and whether our integrated reports are still fit for purpose.

This is the tenth year that we have commissioned the Excellence in Integrated Reporting survey and awards. As we reflect on this important milestone, we have included some comments on the journey so far and the trends that we have seen (see page 10). We believe that in times of unprecedented economic uncertainty it is more important than ever to encourage companies to report in a transparent and balanced way. EY is committed to continue the quest for excellence in integrated reporting. We hope that companies will be both inspired and encouraged by those who have set the bar high to improve the quality of their integrated reports.

We are joined on this critical journey by the University of Cape Town’s College of Accounting, as we track and evaluate the efforts by the Top 100 JSE listed companies to explain the value that they create over the short, medium and long-term. This survey is made possible by the continued involvement and dedicated efforts of Professors Alex Watson, Mark Graham and Goolam Modack, the panel of independent adjudicators from the College of Accounting at the University of Cape Town.

It is our great pleasure to congratulate Redefine Properties for achieving first place in our 2021 awards. As you will read further on in this report, the judges felt Redefine’s report is attractive, well laid out and easy to read. The strategic overview, the integrated stakeholder engagement and the use of capitals to explain the group’s value creation story are examples of excellent disclosures that demonstrate integrated thinking within the group. The section of the governance report that shows how the board considers material matters to ensure the achievement of the group’s strategic objectives and desired governance outcomes can be considered best practice.

We also congratulate Nedbank Group and Kumba Iron Ore on achieving second and third place respectively. Our congratulations are extended to all the entities included in the Top 10 for their outstanding reports. We commend the entities that achieved the rankings of “Excellent” and “Good” for their efforts and the examples they have set.

For more details on how the companies were selected, the mark plan and the adjudicators, please refer to page 23.

Introduction

2 | Excellence in Integrated Reporting 2021

Embracing uncertainty

3 | Excellence in Integrated Reporting 2021

As the business environment around the world evolved during the pandemic, so have CEO priorities and the need for leaders to initiate a strategic reset. To put their businesses back on a growth trajectory, entities need to re-evaluate their purpose. There is an ongoing shift from the view that the primary purpose of companies is to enhance and protect value for shareholders, to the view that corporations should understand and address the needs of their broader stakeholders and in doing so create long-term sustainable value.

The shift to a focus on long-term value is an important one. It is a focus away from short-term profit-making to long-term value creation. But more than that it is a focus on creating value for customers, employees, and society as a whole and not simply maximising shareholder’s value. It recognises that there is a disconnect between the traditional net asset value of an entity and the value that an entity creates which includes the non-financial metrics, such as customer relationships, intellectual capital, and competitive advantages. There is no doubt that progress has been made but there is more work to do. Looking at our own 2021 Excellence in Integrated Reporting survey showed us that 48 of the 100 companies reviewed have made a serious attempt at producing an integrated report that focusses on long-term value. The other 52 have not.

So, if we are to reset our strategy, what do companies need to consider? Companies that thrive, do so because their leaders understand that investing in a broader set of stakeholder considerations will have a considerable impact on their ability to attract capital; their ability to attract top talent as well as drive the sustainability of their businesses. This is a long-term value approach to building a growth strategy. The challenge is to move beyond the short-term financial reporting bias towards drivers of long-term value.

Long term value starts with a clear sense of purpose. The formulation of an entity’s purpose is an aspirational or unique reason for existing. Where the purpose of an entity is clearly defined, it will meaningfully inform business decisions and commitments. Purpose helps everyone who deals with the company to understand what the organisation actually stands for and against, who they are, their values as

well as their positioning. An increasingly informed group of consumers, customers and stakeholders know the type of organisations they want to associate with and those are purpose-led businesses who reflect strong hopes, ambitions, and aspirations.

Adversity has created opportunity. Companies need to use this opportunity to evaluate, re-set and implement their strategies in double quick time. We look forward to working with the business community and other stakeholders to create long-term value.

Leading with purpose – Reset for growth

Purpose helps everyone who deals with the company to understand what the organisation actually stands for and against, who they are, their values as well as their positioning.

“Ajen SitaChief Executive Officer, EY Africa

Reimagining a purpose-led growth strategy

Reimagining a purpose-led growth strategy

Source: EY – The CEO imperative – Rebound to more sustainable growth

4 | Excellence in Integrated Reporting 2021

It has been more than a year since the COVID-19 pandemic began. South Africa and many parts of the world are still feeling the impact of the various waves and the unprecedented economic lockdown. The recent civil unrest in Kwa-Zulu Natal and Gauteng has brought further social and economic hardship to many communities. The consequences of these events will be felt for many years to come.

At the same time, as vaccines become more freely available and vaccination rates increase, we are starting to contemplate life beyond COVID-19. In some parts of the world, economies and businesses are opening up, people are slowly returning to their offices and businesses as restrictions on gatherings and international travel are being lifted.

Even in those countries and industries where economies are beginning to rebound, the pandemic has resulted in an incredibly changed business environment. This is an opportunity to revisit and reimagine business strategies. But a growth strategy in the post-pandemic era cannot be built on the same assumptions and principles that drove results in the pre-pandemic era. It will not be a return to business as it once was. Businesses should use this opportunity to revisit their strategies, to create sustainable and long-term value.

In order to create this long-term value, it is important that an entity has a clear and shared understanding of its purpose. This is the reason a business exists – the ‘why’. Its growth strategy should formulate how the entity’s purpose will be achieved. There are five key elements that will need to be considered in formulating a purpose-led growth strategy.

Sustainability – Sustainability is one of the defining challenges of our lifetime. It is also the innovation opportunity of a generation. Entities are increasingly embracing the business case for sustainability. Becoming a purpose-driven business may require difficult trade-offs as long-term investments are prioritised over short-term profit making.

Businesses that have refocussed their purpose have experienced some important payoffs. Purpose-driven businesses have employees who are more engaged, committed and motivated. Research has shown that businesses that both define and act with purpose outperform their peers by 5-7%. This also provides businesses with an opportunity to differentiate their products, as customers are four times more likely to buy from businesses with a strong purpose.

Trust – In the post-pandemic era, trust will be a licence to operate. At a time that trust in governments and institutions is at an all-time low, the importance of building trust in an increasingly virtual and connected world will be critical to create long-term value. People want to trust the organisations they buy from, work for and invest in.

Technology – The pandemic has given businesses that were well-positioned to work remotely and function independently of a physical space, a competitive advantage. It has also highlighted the fact that we are capable of being far more flexible and able to work remotely much more extensively than what we thought possible. The pandemic has catapulted us into the ‘digital first’ era overnight. But the technology revolution is only just beginning.

Many studies show that the desire for technological acceleration is one of the most significant drivers of transformation. If businesses are to successfully harness technology at speed, they need to upskill and reskill their employees. Organisations will also need to create a culture of agility and a transformative mindset to be able to successfully adopt digital transformation.

Trade – Geopolitical tensions and the uncertainty that they create are forcing businesses to re-evaluate their operating models. As trade flows and patterns are changing, businesses will need to adapt their strategies to deal with ever changing and unpredictable complexities. The optimisation of supply chains will be critical, not only to ensure resilience in times of instability, but also from an ethical point of view due to pressures from stakeholders. As economies around the world re-open at different rates, businesses with flexible trade strategies will be best placed to take advantage of the opportunities to grow.

People – Any purpose-led long-term value strategy will only be successful where people are put front and centre of everything. Businesses need the right talent to conceptualise and execute a purpose-led strategy – a scarce resource. The most advanced innovations, or cutting-edge technologies, can fail if they lose sight of human values. Leading businesses are already reimagining how their people work and where they work, establishing a new hybrid approach to working. This will not only manage the transition to the post-pandemic era, but also enable these businesses to allow increasingly flexible working arrangements for their employees in the future.

In order to create this long-term value, it is important that an entity has a clear and shared understanding of its purpose.Stephen Ntsoane

“

Stephen NtsoaneAssurance Leader, EY Africa

Larissa ClarkIFRS Desk Leader, EY Africa

5 | Excellence in Integrated Reporting 2021

A purpose-led strategy is the path to long-term value in the post-COVID environment. This is a strategy built on sustainability, trust, technology, trade and putting people at the centre of every decision an entity makes. Now is the time to re-evaluate your purpose and strategy and take advantage of the opportunity to reimagine these to create long-term value.

Reimagining a purpose-led growth strategy

Integrated reporting – time to refocus?

1 Read more about the results of the survey from page 19 to 22.2 In April 2021, the Trustees of the IFRS Foundation, the oversight body of the International Accounting Standards Board (IASB), published a proposal to amend the IFRS Foundation

Constitution to accommodate the formation and operation of an International Sustainability Standards Board (ISSB). You can read more about their proposals on page 8.

Integrated reporting – time to refocus?

6 | Excellence in Integrated Reporting 2021

Ten years after the introduction of integrated reporting in South Africa, are our integrated reports serving their purpose and continuing to lead, or at least follow, global best practice in integrated reporting? This is a difficult question to answer at this point when the purpose of corporate reporting is being reconsidered, globally. As we mark ten years of integrated reporting in South Africa, it is a good time to reflect on what the purpose of integrated reporting in South Africa is and whether we need to refocus our efforts.

South African companies rushed into integrated reporting in 2010, whilst the adoption in the rest of the world has been slower, possibly allowing preparers to benefit from the learnings of early adopters and developments in reporting requirements. In South Africa the purpose and consistency of application of the International <IR> Framework has varied between reporting entities – 30 of the 100 reports included in this survey state that their integrated report is aimed at a variety of stakeholders, whereas 25 of the reports state that their report is primarily aimed at the providers of capital1. Recent global developments have provided more clarity on the purpose of different types of reports, and in particular, the distinction between reports that focus on enterprise value as opposed to those that focus on the enterprise’s impact on sustainable development. Both issues are topical, and relevant, but they are different. A report that tries to combine both, without focusing on the distinction, runs the risk of not successfully serving its purpose and, unfortunately, is not uncommon in South Africa.

The building block approach to corporate reporting, advocated by the International Federation of Accountants (IFAC), is useful to consider when assessing whether a report is achieving its purpose. The starting block is the financial statements which include amounts that are already represented

as monetary amounts, generally prepared in terms of the well documented and widely applied International Financial Reporting Standards (IFRS) and their purpose is well understood. Financial statements may include climate related issues to the extent that they create risks that for example impact discount rates used for impairment calculations, provision for carbon taxes etc. Reporting is then expanded to include those sustainability matters that have the potential to create or diminish enterprise value in the future and that investors may factor into investor and shareholder voting decisions – the enterprise value approach. Reporting can then be expanded even further to include the economic, environmental, and social impacts that are not captured by enterprise value. That gives rise to sustainability reporting, which is multi-stakeholder focused and relevant for assessing sustainable development impacts.

‘Enterprise value reporting’ is the focus of the newly formed (June 2021) Value Reporting Foundation, which has been formed by combining the International Integrated Reporting Council (IIRC) and the American Sustainability Accounting Standards Board (SASB). Their emphasis is on enterprise value reporting and how it is created, preserved, or eroded over time. Integrated reporting is a form of enterprise value reporting, as is evident from the focus of the integrated report on ‘information available to providers of financial capital to enable a more efficient and productive allocation of capital’. Similarly, the focus of the new International Sustainability Standards Board will also be on enterprise value2.

Alex WatsonIndependent non-executive director; Professor Emeritus, University of Cape Town

Applying this distinction to reporting on the current Covid pandemic, the most relevant aspect in an integrated report is to report on how an organisation has demonstrated its resilience and adaptability to unanticipated challenges as that is relevant to future enterprise value creation potential. In contrast, a sustainability report will include disclosures on how an entity has supported its various stakeholders in Covid times, i.e. the outward impact of your current activities.Alex Watson

“

Sustainability reporting is the practice of disclosing the most significant economic, environmental, and social impacts, and therefore the contribution by the entity to sustainability development goals. The Global Reporting Initiative (GRI) Standards are the most widely used standards for sustainability reporting. Individual reporting metrics from the GRI standards may be appropriate for use in reporting on issues that are relevant to enterprise value that are not covered by IFRS.

A challenge, that may be greater in South Africa than elsewhere, is applying, and demonstrating its application, of the double materiality concept, promoted by the European Commission and the GRI. This approach is key to demonstrating the completeness of the reports and to ensure that published reports achieve their purpose. First, the reporting entity needs to consult a broad group of stakeholders to identify all matters which are material to its most significant impacts on the economy, environment, and people. The second level of materiality is then to identify the subset of those issues that are material to enterprise value creation.

A sustainability report will include all material impacts, with only those that are material to enterprise value creation being included in an integrated report. Globally, most companies first prepare a sustainability report and may progress from there to integrated or enterprise value reporting, making it easier to apply the double materiality approach. The requirement for listed South African companies to prepare integrated reports, while many had never prepared a sustainability report, has raised the risk of preparing an integrated report that does not include all material impacts and are not supported by the necessary detailed data collation and verification processes that would have been developed to prepare sustainability reports.

The other aspect to consider is whether the reports take the appropriate point of view, or direction, of reporting. A sustainability report is outward looking as it reports on the company’s impact on the world, whereas an integrated report should report on the extent to which its external environment has an impact on its ability to create value in the future and is therefore more inward looking and future focused.

Applying this distinction to reporting on the current Covid pandemic, the most relevant aspect in an integrated report is to report on how an organisation has demonstrated its resilience and adaptability to unanticipated challenges as that is relevant to future enterprise value creation potential. In contrast, a sustainability report will include disclosures on how an entity has supported its various stakeholders in Covid times, i.e. the outward impact of your current activities.

If ever there is a time to focus on the direction and content of external reports, it is now. Challenges in the operating context caused by the Covid pandemic, climate and other challenges, increased financial capital provider needs for relevant and reliable sustainability information, together with unprecedented progress in clarifying and harmonizing reporting requirements are all reasons to reconsider whether current external reporting practices are fit for purpose. In the post-pandemic era, entities are encouraged to reflect on the purpose of their integrated reports and whether they are achieving its intended purpose.

Integrated reporting – time to refocus?

7 | Excellence in Integrated Reporting 2021

Towards international sustainability standards

Towards international sustainability standards

8 | Excellence in Integrated Reporting 2021

One of the consequences of the COVID-19 pandemic is the increasing focus that non-financial information is receiving. Investors are seeing non-financial information as a core element in investment decisions and there is an increased recognition that financial reporting alone does not provide investors and other stakeholders with a full picture of the value of the company. The expectation gap between the information needs of investors and the non-financial information provided seems to have widened. There is a growing appetite for a formal framework for measuring and communicating intangible value, in particular environmental, societal and governance risks.

In April 2021, the Trustees of the IFRS Foundation (the Trustees), the oversight body of the International Accounting Standards Board (IASB), published a proposal to amend the IFRS Foundation Constitution to accommodate the formation and operation of an International Sustainability Standards Board (ISSB). This will pave the way for a global suite of sustainability standards under the banner of the IASB.

We have asked James Luke, IFRS Desk, EY Africa and member of the IFRS Foundation’s Advisory Council about these important developments and what they mean for South African reporters.

What is the proposed name for the new sustainability standards that will be issued by the ISSB?Based on the documentation released by the Trustees, the proposed name for the standards issued by the ISSB is ‘IFRS sustainability standards’. The Trustees have proposed that the standards and IFRIC interpretations issued by the IASB

be referred to as ‘IFRS Accounting Standards’. It would seem therefore that the concept of ‘IFRS standards’ will be made up of both ‘IFRS Accounting Standards’ and ‘IFRS Sustainability Standards’. I would encourage companies to follow the developments and understand the final constitutional changes of the IFRS foundation and the new standards when the ISSB is created.

The Trustees have announced their views on the strategic direction of the new sustainability standards board. What are they currently proposing?There have been four fundamental choices that the Trustees have made relating to both the scope and approach for the new sustainability standards board, namely:

• To establish the audience to whom the sustainability information would be targeted. The current proposals aim to focus on the information needs of investors, lenders and creditors with an emphasis on enterprise value, therefore taking a capital market approach rather than a multi-stakeholder approach. While this may disappoint some stakeholders, the narrower scope makes this project more manageable and is consistent with the concepts underlying current IFRS standards.

• To meet the information needs of investors on all environmental, social and governance matters. This is a broad mandate and climate-related matters are being regarded as a priority as there has been clear signalling from both regulators and the investor community that climate risk is pervasive and of importance.

• To build on the work of existing frameworks. The Trustees have identified that the new board would build upon the work of the Task Force on Climate-related Financial Disclosures (TCFD), as well as work by the alliance of leading standard-setters in sustainability reporting focused on enterprise value.

• To make use of a buildings block approach. This approach would allow the ISSB to provide a global baseline of standards for sustainability reporting and at the same time enhance comparability and consistency of sustainability reporting. In addition, this will allow for flexibility in coordinating with other frameworks and local regulations, accommodating a wider range of reporting requirements.

What are the requirements that Trustees consider essential for the success of a sustainability standards board?The IFRS foundation is an independent standard-setting body. Therefore, the Trustees have considered the following requirements to make this proposed board a success:

• A sufficient level of global support from public authorities, global regulators and market stakeholders in key markets;

• Collaboration with regional initiatives to achieve global consistency and reduce complexity in sustainability reporting;

• Adequate governance structures for the board;

• Appropriate level of technical expertise for Trustees, members and staff;

1 IFRS Practice Statement Exposure Draft ED/2021/6 Management Commentary

James LukeIFRS Desk, EY Africa

Towards international sustainability standards

9 | Excellence in Integrated Reporting 2021

• Capacity to obtain financial support and to achieve the required level of separate funding;

• Development of a structure and culture that seeks to build effective synergies with financial reporting; and

• Ensuring the current mission and resources of the Foundation are not compromised.

Will the composition and governance structure of the ISSB be similar to the existing requirements of the IASB?I do think that this will be monitored by the Trustees. The concept of sustainability is far wider than that of financial reporting and you may find that the skills required on the board may change from time to time. This could be addressed by a rotation of board members or if need be by a change of the size of the board.

Recently, the IASB issued an IFRS Practice Statement Exposure Draft on Management Commentary1. How will the issuance of this revised practice statement impact the development of the sustainability standards? The practise statement exposure draft proposes a separate appendix detailing the requirements and guidance about intangible resources and relationships, as well as ESG matters. The board sees the management commentary as an appropriate location for reporting on ESG matters and envisages the revised practice statement being applied in conjunction with the sustainability reporting requirements and guidance.

That being said, it is very clear from discussions held by the Trustees and the Advisory Council that there will be a link between both boards. Generally, many issues will affect both boards and they would need to work together on solving these issues and setting standards. We may find that as the boards progress with their work, the management commentary may become the vehicle that is best suited for sustainability disclosures that will be published by reporting entities. While this exposure draft is being driven by the IASB, we may find subsequent exposure drafts being issued by both boards.

It is clear that there are currently a large number of developments in the non-financial reporting space. What does all this mean for South African reporters?Although South African companies have prepared sustainability reports for many years, these reports have largely focussed on sustainable development matters. In recent years much more attention has been given to governance related matters, as a result of the spate of governance failures we have seen in public and private companies. An area that South African companies will need to focus much more on in the future is climate-related matters and how their operations are impacting the environment. This is in line with the international demand from both regulators and investors for increased climate related disclosures from companies.

We have entered a transitional phase in terms of reporting where investors and regulators are demanding more non-financial information from companies. These decisions will include an assessment of the needs of their stakeholders. In

this assessment entities would probably consider whether the information they are providing meets these stakeholder needs, whether it would require expanding their processes and systems that record and analyse their non-financial metrics, and whether these disclosures explain how the non-financial information supports and enhances the value that the company creates.

Overall, I think that South African companies do have an edge over other jurisdictions and internationally South Africa has been considered one of the leading countries with respect to integrated reporting. However, I do see the playing field starting to change and our companies may have to be agile in their reconsiderations when it comes to their reporting. There is no reason why South African companies cannot set the benchmark in terms of the proposed sustainable reporting.

In 2012 the Top 10 were not ranked.

Nedbank Group Ltd

Nedbank Group Ltd

Nedbank Group Ltd

Kumba Iron Ore Ltd

Kumba Iron Ore Ltd

Liberty Holdings Ltd

Royal Bafokeng

Platinum Ltd

Gold Fields Ltd

10 Years of integrated reporting in South Africa

10 Years of integrated reporting in South Africa

20 20 20 20 20 20 20 2020 19 18 17 16 15 14 13

Kumba Iron Ore Ltd and Redefine Properties Ltd have been in the Top 3 for 5 consecutive years, whilst Nedbank Group Ltd has been in the Top 3 for 4 consecutive years.

Truworths International Ltd has been in the Top 10 for all 10 years of Excellence in Integrated Reporting, whilst Sasol Ltd has been in the Top 10 for 9 years.

Kumba Iron Ore Ltd, Nedbank Group Ltd, Standard Bank Group Ltd and Vodacom Group Ltd have been in the Top 10 for 8 years whilst Redefine Properties Ltd has been in the Top 10 for 7 years.

Liberty Holdings Ltd and Absa Group Ltd (previously called Barclays Africa Group Ltd) have both been in the Top 10 for 6 years.

Past winners

10 | Excellence in Integrated Reporting 2021

10 Years of integrated reporting in South Africa

10 Years of integrated reporting in South Africa

The journey so far Positive trends over the years Progress still to be made after 10 years

• Insufficient explanation of the value the business wishes to create for itself and others.

• No clear identification as to whether the integrated report focus on factors that are relevant to capital providers and enterprise value or a broader audience.

• Not enough emphasis on strategy and value creation.

• Not clear what is needed to achieve strategic objectives.

• Poor evidence of integrated thinking.

• Trade-offs between capitals not given enough prominence.

• Not enough explanation of how the business will use its various capitals (or resources) to create value.

• Balance not achieved – challenges, constraints, disappointments, and negative outcomes.

• Lack of explanation of how governance structures /processes will create/preserve value.

• No description of the process that is followed to ensure the integrity of the information.

• “Integrated reporting is a journey” has become the great <IR> cliché!

• Early reports were often a sustainability report combined with the annual financial statements and some management commentary.

• Diversity in structure and innovation in communication seen over the years.

• Ongoing struggle to strike a balance between the traditional annual report and a more forward-looking report that emphasises strategy and value creation.

• 50% of JSE listed (top 100) companies are still NOT (really) getting it right.

• Gap widening between reports ranked as ‘Excellent’ and those ranked as ‘Average’ and ‘Progress to be made’.

• South Africa’s top reports are comparable with the best in the world.

• Significant improvements in the quality of (the better) integrated reports.

• Improved connectivity of information, particularly for those with a clearly articulated purpose.

• Better use of infographics, navigation tools and cross references.

• Improved articulation of business models and operating context.

• Better differentiation of outputs and outcomes and more robust data.

• Innovation in layout and structure.

• Greater conciseness.

• Greater use of websites for detailed remuneration, sustainability, and compliance information.

• Increased usage of the UN’s Sustainable Development Goals.

By Mark Graham, Associate Professor, Graduate School of Business, University of Cape Town

11 | Excellence in Integrated Reporting 2021

12 | Excellence in Integrated Reporting 2021

2021 Rankings

2021 RankingsTop 10 rankings

with Honours with Honours with HonoursRedefine

Properties Ltd

Nedbank Group Ltd

Kumba Iron Ore

Ltd

Anglo American Platinum Ltd

Absa Group Ltd Oceana Group Ltd

Standard Bank Group Ltd

Vodacom Group Ltd

Netcare LtdTruworths

International Ltd

“Honours” is awarded to those high quality integrated reports, which the adjudicators believe have come closest to complying with the requirements of the <IR> Framework.

13 | Excellence in Integrated Reporting 2021

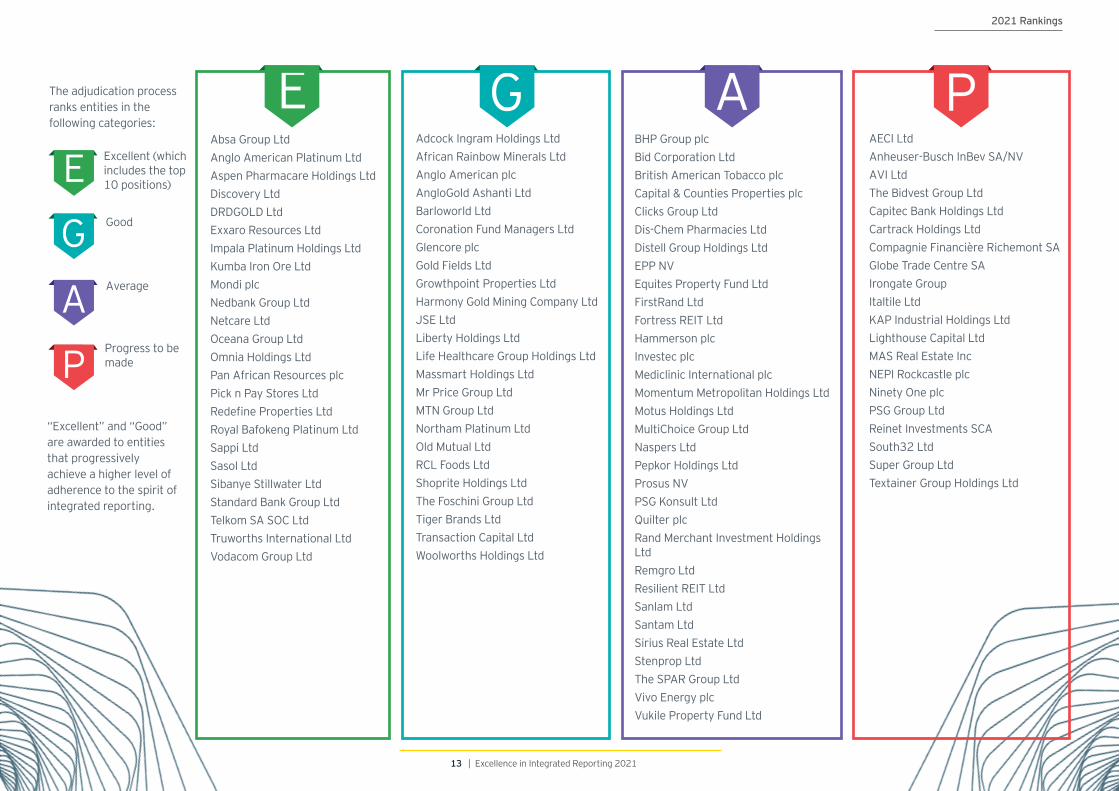

Adcock Ingram Holdings LtdAfrican Rainbow Minerals LtdAnglo American plcAngloGold Ashanti LtdBarloworld LtdCoronation Fund Managers LtdGlencore plcGold Fields LtdGrowthpoint Properties LtdHarmony Gold Mining Company LtdJSE LtdLiberty Holdings LtdLife Healthcare Group Holdings LtdMassmart Holdings LtdMr Price Group LtdMTN Group LtdNortham Platinum LtdOld Mutual LtdRCL Foods LtdShoprite Holdings LtdThe Foschini Group LtdTiger Brands LtdTransaction Capital LtdWoolworths Holdings Ltd

Absa Group LtdAnglo American Platinum LtdAspen Pharmacare Holdings LtdDiscovery LtdDRDGOLD LtdExxaro Resources LtdImpala Platinum Holdings LtdKumba Iron Ore LtdMondi plcNedbank Group LtdNetcare LtdOceana Group LtdOmnia Holdings LtdPan African Resources plcPick n Pay Stores LtdRedefine Properties LtdRoyal Bafokeng Platinum LtdSappi LtdSasol LtdSibanye Stillwater LtdStandard Bank Group LtdTelkom SA SOC LtdTruworths International LtdVodacom Group Ltd

BHP Group plcBid Corporation LtdBritish American Tobacco plcCapital & Counties Properties plcClicks Group LtdDis-Chem Pharmacies LtdDistell Group Holdings LtdEPP NVEquites Property Fund LtdFirstRand LtdFortress REIT LtdHammerson plcInvestec plcMediclinic International plcMomentum Metropolitan Holdings LtdMotus Holdings LtdMultiChoice Group LtdNaspers LtdPepkor Holdings LtdProsus NVPSG Konsult LtdQuilter plcRand Merchant Investment Holdings LtdRemgro LtdResilient REIT LtdSanlam LtdSantam LtdSirius Real Estate LtdStenprop LtdThe SPAR Group LtdVivo Energy plcVukile Property Fund Ltd

AECI LtdAnheuser-Busch InBev SA/NVAVI LtdThe Bidvest Group LtdCapitec Bank Holdings LtdCartrack Holdings LtdCompagnie Financière Richemont SAGlobe Trade Centre SAIrongate GroupItaltile LtdKAP Industrial Holdings LtdLighthouse Capital LtdMAS Real Estate IncNEPI Rockcastle plcNinety One plcPSG Group LtdReinet Investments SCASouth32 LtdSuper Group LtdTextainer Group Holdings Ltd

Good* Average* Progress to be made*Excellent*

The adjudication process ranks entities in the following categories:

Excellent (which includes the top 10 positions)

Good

Average

Progress to be made

“Excellent” and “Good” are awarded to entities that progressively achieve a higher level of adherence to the spirit of integrated reporting.

2021 Rankings

Redefine’s report is attractive, well laid out and easy to read. The strategic overview, the integrated stakeholder engagement and the use of capitals to explain the group’s value creation story are examples of excellent disclosures that demonstrate integrated thinking within the group. The section of the governance report that shows how the board considers material matters to ensure the achievement of the group’s strategic objectives and desired governance outcomes can be considered best practice. The detailed reporting on trade-offs provides useful insight into the tough choices facing the group and the thinking that lies behind their decision making. The report incorporates the Sustainable Development Goals (SDGs) in a meaningful manner and explains how the group arrived at the specific SDGs that are relevant to the group. We particularly liked the explanation of the materiality determination process and the graphic that was used to illustrate how the group’s material matters were crystallised. The explanation of performance against the various strategic objectives is comprehensive and balanced. Furthermore, there is a useful explanation of why each performance measure is important and each measure is clearly linked to other elements within the report.

Nedbank’s report has a clear emphasis on value creation and strategy. It commences with a section that outlines the group’s approach to integrated thinking, the integrated reporting process and the way in which the report is structured. The report itself is structured in a sensible way that makes it easy to follow the value creation narrative. The focus of the report is on the ability of the organisation to create value for its stakeholders, with an appropriate suite of supporting documents to provide additional compliance and other information. We particularly liked the governance section of the report and the way in which it focusses on value creation and preservation together with clear cross references to where more information can be found on any issue. The discussion on strategic trade-offs and the impact on capitals, outcomes and KPI’s is an excellent example of showing how strategic decisions are made in an integrated way. The report handles the impact of the COVID-19 pandemic in a thoughtful manner, particularly in the context of framing risk, scenario planning and the outlook for the future.

Redefine Properties Ltd Nedbank Group Ltd

14 | Excellence in Integrated Reporting 2021

By Mark Graham, Associate Professor, Graduate School of Business, University of Cape Town

Top 10 companies

Top 10 companies

Kumba’s report has an excellent strategic focus with the appropriate amount of strategic detail being provided. The report makes use of iconography to guide the reader through the report, whilst the report itself presents a wealth of information in a balanced, transparent, and interconnected manner. The narrative is crisp and concise with good use being made of appendices to present more detailed information that may be of interest to readers. We particularly liked the section that outlines the group’s ability to create value over time and the way in which this is clearly framed within the context of its capitals and inputs together with the challenges that exist in securing the necessary inputs. The explanation of the group’s strategy is clear and attention is given to explicitly outlining the short, medium and long-term strategies. The identification of material issues and their implications for value creation, together with the group’s strategic response provides useful insight into the group’s operating context. The group’s opportunities are clearly presented and the way in which they are linked to the capitals is an indication of integrated thinking within the group.

Kumba Iron Ore Ltd

Vodacom’s report is easy to navigate and makes excellent use of icons to link sections and guide the reader. The report is crisp, concise, attractive and easy to read. It has a strong focus on both strategy and value creation. We particularly liked the one-page introduction to the group’s strategy that shows the linkage between strategic objectives, historic performance and medium-term goals, this provides a good introduction to the more comprehensive detail that follows. The disclosures, within the explanation of the group’s business model, of the investments made in various resources and relationships to sustain value are useful. The sections that outline how the group is responding to its external operating environment and to stakeholder ‘hot topics’ are excellent. The report clearly shows how the group’s ability to deliver value depends on the contribution and activities of a range of stakeholders. In addition to comprehensive disclosure of material stakeholder issues, an internal assessment of the quality of the relationship with each stakeholder group is also provided. The governance disclosures are enhanced by detailing the Board’s key focus areas and showing how these are linked to the group’s risk and strategy.

Vodacom Group Ltd

Amplats’ report commences with a useful explanation of its approach to reporting and the principles that are applied in drafting its integrated annual report. We particularly liked the explanation of how the reporting boundary is determined by working outwards from the core legal entity to consider risks, opportunities and outcomes associated with entities or stakeholders that have a significant effect on the group’s ability to create value. The sections that outline the group’s strategy, business model and the markets within which it operates are particularly helpful in setting out the context for the group’s value creation story. Furthermore, the roadmap that shows how the group plans to deliver on its strategy within short, medium and long-term time horizons is useful. The group’s risks are clearly presented, appropriately integrated with strategy and illustrated with a heat map that shows the likelihood and consequence of each risk. The reporting is balanced and the explanation of the group’s trade-offs and the way in which they are managed is excellent. Informative infographics show the economic contribution that the group makes in both South Africa and Zimbabwe.

Anglo American Platinum Ltd

Netcare’s report contains a wealth of useful information and its sensible structure makes the report easy to navigate. The section dealing with the COVID-19 pandemic is detailed, helpful and appropriate, given the sector in which the group operates. We particularly liked the strong focus on creating measurable value for each class of stakeholder. Material matters are linked to stakeholder concerns and strategic pillars and clearly separated into immediate and ongoing priorities. The way in which strategy progress against each of the strategic pillars is reported and linked to remuneration is excellent. Good use is made of icons to distinguish between positive, negative or neutral outcomes in both the current year and in the future. The linkage to the operating environment, the group’s response, and related risks with extensive cross referencing to where more detail can be found gives a clear insight into the agility and resilience of the organisation. The detail provided on each of the group’s capitals, especially relationship capital, is comprehensive and clearly explains how sustainable value will be created.

Netcare Ltd

15 | Excellence in Integrated Reporting 2021

Top 10 companies

Truworth’s report has a clear strategic focus with an emphasis on value creation both for itself and for other stakeholders, together with relevant information on how the value that is created is measured. We particularly liked the emphasis on providing information that is specific to the group rather than mere generic or boilerplate disclosures. Furthermore, the report is easy to navigate, avoids the use of jargon and is written using language that is clear and concise. Given the nature of the business, the separate identification of how the impacts of COVID-19 were managed is helpful. We particularly liked the detailed and integrated disclosure of each material issue that incorporates performance against objectives and targets, challenges encountered, future objectives and plans, risks and opportunities as well as achieved and target key performance measures. The section that discloses how the group manages its various stakeholder relationships is excellent. The governance section includes a useful and innovative table that unpacks board deliberations by separating key issues and routine matters by those that have been noted, considered, approved, authorised or resolved.

Truworths International Ltd

Absa’s report commences with a detailed explanation of the materiality determination process. The report focusses on value creation and contains an appropriate mix of forward-looking information and performance disclosures. A wealth of useful, well contextualised and clearly explained data is provided within the report and we particularly liked the extensive use of cross referencing which makes the report easy to navigate. The detail provided in respect of the group’s stakeholders’ needs and expectations, that include both a strategic response to these needs and expectations and performance measures for each stakeholder group, is excellent. The business model is comprehensive and the market drivers that are influencing the business model are clearly explained. The explanation of the group’s strategy is excellent and includes useful linkages to material matters, the capitals, key risks and mitigation actions as well as performance against each strategic objective. The report includes a detailed explanation of the strategic trade-offs facing the group and how these have been managed. Furthermore, the clear identification of how the COVID-19 pandemic is impacting the group’s strategy is helpful.

Absa Group Ltd

Oceana’s report includes a clear focus on the factors that are relevant to its future value creation. The report achieves a high level of connectivity between material issues, strategic objectives, principal risks and the external environment context. We particularly liked the explanation of how various external issues are impacting on the group’s business model. The explanation of how the group manages trade-offs to deliver long-term value is excellent and sufficiently detailed to get a good sense of the effect of each trade-off on the various capitals employed. The material risks are clearly presented within the report by using both inherent and residual risk heat maps to show the principal risks that will affect the group’s ability to create value. The group’s approach to the development of its strategy is detailed and the actual strategies to achieve the various strategic objectives are comprehensively explained. The governance section is well laid out and achieves the objective of explaining how the various governance focus areas support the group’s strategy and contribute towards the group’s governance outcomes.

Oceana Group Ltd

Standard Bank’s report starts with an informative explanation of the group’s approach to integrated thinking. The report is well laid out, with a structure that is easy to follow and navigate. We particularly liked the way in which the report is focused on the group’s value creation story and delivering on the group’s strategy with a suitable distinction between short, medium, and long-term strategies. The group’s five strategic value drivers provide a golden thread to the narrative and help to integrate the business model, constraints, key trade-offs, key priorities, oversight and strategic outcomes. The section that outlines the group’s approach to resource allocation, with its focus on balancing value outcomes, is excellent. The disclosures of financial outcomes and the way in which the financial statements are annotated clarifies the strategic progress that has been made in achieving client focus, employee engagement and risk and conduct. There are extensive and useful disclosures of the group’s impacts in those areas where it believes that it can best achieve the group’s purpose while still making a positive impact on society.

Standard Bank Group Ltd

16 | Excellence in Integrated Reporting 2021

Top 10 companies

17 | Excellence in Integrated Reporting 2021

The quality of “Excellent” and “Good” integrated reports continues to improve

24 Companies ranked as “Excellent”, compared to 22 and 23 in 2020 and 2019 respectively

“Excellent” integrated reports have a coherent value creation narrative

Overall impressions at a glance

3 Integrated reports awarded an “Honours” consistent with 2020

Surveys

Little improvement in those integrated reports ranked as “Average” or “Progress to be made”

24 Companies ranked as “Good” compared to 29 in 2020 and 28 in 2019

Overall impressions at a glance

2019

2020

Excellent

Good

Average and Progress to be made

29

49

49

22

28

23

20212424

52

Positive trends

Negativetrends

Insufficient linkage between key performance indicators and the explanation of how the business is being managed

Unclear distinction between short-, medium- and long-term strategies

Lack of focus on how current activities have impacted the future availability of inputs

Generic explanations of the various trade-offs between the capitals

Insufficient explanation of the value the business wishes to create for itself and others

Useful disclosure on the effects of the COVID-19 pandemic

Remuneration disclosure being linked to strategic progress and/ or other outcomes

Better integration of financial information with the value creation narrative

Increased usage of the UN Sustainable Development Goals

Governance disclosures integrated within the narrative on value creation

18 | Excellence in Integrated Reporting 2021

Overall impressions at a glance

• Top 100 Johannesburg Stock Exchange (JSE) Limited listed companies selected based on their market capitalisation as at 31 December 2020.

• Integrated report or annual report for year-ended on or before 31 December 2020.

• Largest in survey: Prosus NV with a market capitalisation of R2.6 trillion.

• Smallest in survey: Vukile Property Fund Ltd with a market capitalisation of R7.6 billion.

• The 100 companies in the survey account for 97% of the market capitalisation of the JSE at 31 December 2020.

Changes to the top 100

• Eleven companies that appeared in the 2020 survey are no longer regarded as being eligible as a result of falling out of the Top 100 due to relative changes in market capitalisation or other corporate activity.

• New / returning in 2021 survey:

• Cartrack Holdings Ltd

• DRDGOLD Ltd

• Irongate Group

• Lighthouse Capital Ltd

• Ninety One plc

• Oceana Group Ltd

• Omnia Holdings Ltd

• Pan African Resources plc

• Prosus NV

• Stenprop Ltd

• Textainer Group Holdings Ltd

Companies included in the survey

• The quality of “Excellent” and “Good” reports continues to improve.

• Excellent reports have a clear strategic focus, an emphasis on value creation and a high level of connectivity between the various elements presented and consequently have a coherent value creation narrative.

• Very little improvement in those reports ranked as “Average” and “Progress to be made”.

• Some reports have early adopted the new 2021 <IR> Framework.

• Many reports deal with COVID-19 pandemic issues in an integrated and sensible way.

• More reports now including an endorsement signed by all directors.

• More companies are using a broad suite of reports to communicate compliance and sustainability information that previously would have been included in the integrated report.

• Better use of interactive tools to help navigate within the report and to provide a link to additional information.

• Improved linkage of relevant UN Sustainable Development Goals (SDGs) to strategy and outcomes.

• Increased reporting on climate change and inclusion of Task-Force on Climate-related Financial Disclosures.

• More reports now including extracts of financial statements within their financial review and using annotations to explain items within these financial statements.

• General improvement in the disclosure of opportunities.

• Increased reference being made to separate sustainability reports.

• Continued improvements in the use of graphs/tables/infographics and icons to achieve conciseness, integration, and more effective communication.

2021 Adjudicators’ observations and overall performanceBy Mark Graham, Associate Professor, Graduate School of Business, University of Cape Town

2021 Adjudicators’ observations and overall performance

Key observations

19 | Excellence in Integrated Reporting 2021

Trends in the rankings

Excellent

Good

Average and progress to be made

27282931

2827232322

24

24

52

2930

35

27

3332

242829

444236

423941

534949

0

10

20

30

40

50

60

Areas for improvement• Include an explicit statement on the purpose of

the integrated report and the intended audience.

• Include the date of the year-end and the date of approval of the integrated report.

• Need for a better explanation of the materiality determination process.

• Explain the value that the business wishes to create for itself and others early-on in the report.

• Clearly articulate how the continued availability, quality and affordability of significant capitals contribute to the organisation’s ability to achieve its strategic objectives in the future and thereby create value.

• Disclosure of only those inputs that have a material bearing on the ability to create value in the short, medium and long term.

• Include an indication of the date at which the various inputs are measured.

• Include details of any constraints that may exist with respect to the availability of inputs.

• Increase emphasis on value erosion, including negative outcomes and other challenges.

• Provide clear KPI’s or other metrics that will be used to evaluate success and link to the strategy, purpose and/or value creation goals.

• Need for increased disclosure on why specific measures are used and how they have been calculated.

• Better reporting of achievements against previous predictions or targets and why medium and long-term targets have changed in the current year.

• A more coherent narrative around climate change linked to value creation, preservation or erosion.

• Greater clarity on why various SDGs have been selected and how they are relevant to value creation, preservation or erosion.

• What is needed to achieve strategic objectives.

• Make a clearer distinction between short, medium and long-term strategies and disclose the length of each time frame.

• Include information on key board deliberations and link this to strategy and value creation and preservation.

• Make clearer links between the various content elements of the report, particularly where the material issues are identified.

• Ensure that the use of icons, figures, graphs, photographs or pictures do not become excessive and a distraction for the reader.

• Exclude regulatory and compliance detail that is not relevant to the value creation story.

• Provide disclosure of the measures taken to ensure the integrity of the integrated report and the data presented.

2014 2013 20122021 2019 20162020 20172018 2015

2021 Adjudicators’ observations and overall performance

2014 2013 20122021 2019 20162020 20172018 2015

2014 2013 20122021 2019 20162020 20172018 2015

20 | Excellence in Integrated Reporting 2021

143

1755

Honours awards• An “Honours” is given

to those high quality integrated reports that are believed to have come closest to complying with all the requirements of the <IR> Framework.

• 3 integrated reports were awarded an “Honours” award in the current year.

companies are not making a serious attempt to produce an integrated report that complies with the International Integrated Reporting Council’s <IR> Framework.

1 International Accounting Standard 34 – Interim financial reporting (IAS 34)

of the 100 integrated reports state that their integrated reports are aimed at a variety of stakeholders.

pages is the shortest integrated report.

pages is the average length of financial statements within the reports and the average length of the financial statements within reports that are titled an integrated report is 22 pages.

Length of integrated reports

of these endorsements were signed by the directors.

of these 20 companies have their primary listings on stock exchanges other than the JSE.

Title of the report

48

30

163

38

28

37

313

30

20

62

52

25

19

72

of the 100 integrated / annual reports reviewed this year were ranked as “Good” or “Excellent”.

of the 100 companies in the survey do not produce an integrated report.

of the 100 companies in the survey include a specific acknowledgement that the report is endorsed by the directors.

of the 100 integrated reports clearly state that their integrated reports are primarily aimed at providers of capital.

pages is the average length of reports in this year’s survey.

pages is the average length of the reports that are titled an integrated report.

pages is the longest integrated report.

Endorsement by the directors

Audience of integrated reports

Rankings

Style of financial statements

companies in the survey included full financial statements in their report.

companies in the survey include IAS 341 financial statements within their report.

companies included their financial statements at the end of the report.

companies include extracts of their financial statements within their financial review.

2021 Adjudicators’ observations and overall performance

21 | Excellence in Integrated Reporting 2021

Industries included in the survey

• Almost 90% of mining companies are included in the “Excellent” and “Good” categories. This is followed by 52% of consumer products and retail companies and 47% of the financial services companies being included in the “Excellent” and “Good” categories.

• For the third consecutive year, over 20% of the companies included in the 2021 survey operate in the consumer products and retail sector, making this the largest group of companies in a single sector featured in the survey.

• Most of the new companies featured in the survey this year were from the real estate and development, industrial products and mining sector.

• The total number of companies within the financial services and insurance sectors remained consistent with last year.

Cons

umer

pro

duct

s &

reta

il

Real

est

ate

deve

lopm

ent

Indu

stria

l pro

duct

s

Insu

ranc

e

*Oth

er

0%

5%

10%

15%

20%

25%

Industries

201920202021 2018 2017

Fina

ncia

l ser

vice

s

Min

ing

2021 rating per Industry

Insurance

Industrial goods & services

Mining

Financial services

Real estate development

Consumer product & retail

Other

0% 20% 40% 60% 80% 100%

Excellent Good Average Progress to be made

*Industries included in other: technology, media and telecommunications, healthcare, logistics, travel and leisure.

2021 Adjudicators’ observations and overall performance

22 | Excellence in Integrated Reporting 2021

23 | Excellence in Integrated Reporting 2021

The mark plan at a glance

The Content ElementsThe Companies The Guiding Principles

The guiding principles underpin the preparation of an integrated report, informing the content and how information is presented:

1. Strategic focus and future orientation

2. Connectivity of information

3. Stakeholder relationships

4. Materiality

5. Conciseness

6. Reliability and completeness

7. Consistency and comparability

Companies included in the 2021 EY Excellence and Integrated Reporting Awards:

• Top 100 JSE-listed companies

• Based on their market capitalisation as at 31 December 2020

• Pure holding companies are excluded

• Dual listed entities are included

• Integrated report for the year-ended on or before 31 December 2020

Overview of the mark plan

The mark plan is based on the <IR> Framework’s* seven Guiding Principles and the eight Content Elements. In addition, consideration is given to the Framework’s Fundamental Concepts.

The Fundamental Concepts

The fundamental concepts underpin and reinforce the requirements of the Framework:

1. Various capitals that the organisation uses and affects

2. How value is created

*International Integrated Reporting Council’s <IR> Framework, issued in December 2013.

The mark plan at a glance

An integrated report includes the content elements that are fundamentally linked to each other and are not mutually exclusive:

1. Organisational overview and external environment

2. Governance

3. Business model

4. Risks and opportunities

5. Strategy and resource allocation

6. Performance

7. Outlook

8. Basis of presentation

Further details of the mark plan and the adjudication process can be found on next page.

24 | Excellence in Integrated Reporting 2021

The mark plan and adjudication processThe mark plan and adjudication process

How are companies chosen for inclusion in the Excellence in Integrated Reporting Awards?These are the top 100 companies listed on the JSE, selected based on their market capitalisation on the last trading day of the calendar year. This is usually the 31st December.

All companies are regarded as being eligible to be included in the survey, other than pure holding companies, if any. The final top 100 includes the full range of listed companies on the JSE, from resources to industrials, retailers and financial institutions and includes several companies with dual listings. In the case of those companies which operate through a dual listing structure, only the combined group is included in the survey.

How is the mark plan developed?The mark plan is developed by the three adjudicators with affiliations to the University of Cape Town (UCT) in conjunction with EY’s Professional Practice Group. The UCT team comprises of Professors Alexandra Watson (Emeritus Professor), Goolam Modack (College of Accounting) and Mark Graham (Graduate School of Business). All the adjudicators have been involved for many years in EY’s Excellence in Corporate Reporting survey and since 2011 in EY’s Excellence in Integrated Reporting survey.

What is included in the mark plan?The mark plan is quite simple and is based on the guiding principles and content elements that appeared in the The International <IR> Framework (the Framework) that was issued by the International Integrated Reporting Council (IIRC) in December 2013. A mark out of ten is awarded for each of the seven guiding principles (i.e. strategic focus and future orientation, connectivity of information, stakeholder relationships, materiality, conciseness, reliability and

completeness and lastly consistency and comparability). Similarly, a mark out of ten is awarded for each of the eight content elements (i.e. organisational overview and external environment, governance, business model, risks and opportunities, strategy and resource allocation, performance, outlook and finally basis of presentation and preparation). Marks are also awarded for the extent to which the integrated report incorporates the Framework’s fundamental concepts, dealing with how value is created with reference to the six ‘capitals’ where relevant.

What do the adjudicators expect to see with respect to the six capitals?The adjudicators believe that an explanation of how a business creates value with respect to the six capitals is a particularly suitable way for most companies to present much of the content that needs to be presented within its integrated report. Furthermore, an explanation of how value is created within an organisation can sensibly be structured around how value is embodied in the capitals that it uses. Doing this should also give the report a more logical flow.

So whilst the adjudicators do not expect companies to explicitly structure their report around the six capitals, or indeed use this specific terminology, they would certainly look for disclosures relating to the stock and flow of the capitals (i.e. financial, manufactured, etc.) and the extent to which trade-offs between different capitals may influence the organisation’s strategy.

Which document is adjudicated?The document that is labeled as being the integrated report is reviewed and adjudicated. For those dual listed companies that do not produce an integrated report, the adjudicators evaluate the information contained in their annual report. This

is generally not detrimental to those companies as many of the integrated reporting principles are included in their reports, nonetheless. For those companies that operate through a dual listing structure the combined report is reviewed. In all cases the on-line pdf or hard copy of the report is reviewed.

Are separate sustainability reports or other reports reviewed?No, the adjudicators only look at the document that is labelled as being the integrated report or the annual report in the case where companies have not produced an integrated report.

Who actually adjudicates the integrated reports? Each of the integrated reports of the top 100 companies is separately adjudicated by each of the three adjudicators from the University of Cape Town using the pre-agreed mark plan.

Is this simply a box ticking exercise?No, absolutely not. Much more emphasis is placed on the quality of information presented - the relevance, understandability, accessibility and connectedness of that information; whether users of the integrated reports would have a reasonable sense of the issues that are core to the operations of each of the companies and whether companies have dealt with the issues that users would have expected. This implies that much more credit is given for crisply presented information that highlights relevant facts compared to the same information needing to be extracted from less relevant information.

Furthermore, once the marking process is complete, the scores for the seven guiding principles, the eight content elements and for adherence to the fundamental concepts and individual members’ recommended rankings are collated, resulting in a final ranking being awarded. The final ranking is therefore

25 | Excellence in Integrated Reporting 2021

The mark plan and adjudication process

based on a combination of the average of these scores, overall perceptions and extensive discussions surrounding the final rankings for each company. This ranking process is particularly important as the scoring process is subjective and scores may differ, based on the adjudicators’ impressions at the time.

Do the adjudicators attempt to achieve consensus on the scores?No, not really. It’s really the ranking that matters. Where an adjudicator’s ranking differs widely from the others, this is reviewed to ensure that information has not been overlooked. Often, scores may vary widely. While the adjudicators generally agree on what is good disclosure, perception of the relative importance of items may differ. Despite this, there is a high degree of consensus among the adjudicating members’ overall perceptions and recommended rankings.

Is there an overriding objective to the ranking?Yes, absolutely. The overriding objective in ranking the integrated report is the extent to which it complies with the spirit of integrated reporting as defined by the Framework as being “a concise communication about how an organisation’s strategy, governance, performance and prospects, in the context of its external environment, lead to the creation of value over the short, medium and long term”.

The adjudication process results in each of the 100 companies being ranked as “Excellent”, “Good”, “Average” or “Progress to be made”. A further evaluation then results in a ranking of the ten best integrated reports from amongst those that are ranked as “Excellent”.

How do the adjudicators identify and rank the “Top 10”?There are three specific areas which are believed to be crucial to excellence in integrated reporting. These are, the extent to which the report has a clear strategic focus, an emphasis on value creation and a high level of connectivity between the various elements presented. These three areas are then used to identify the “Top 10” integrated reports from all amongst those ranked as “Excellent” and to assign them a ranking within the “Top 10”.

Other than the “Top 10”, are there any other awards?Since 2016 an “Honours” award is given to those high-quality integrated reports which are believed to have come closest to complying with all the requirements of the <IR> Framework.

Mark GrahamMark Graham is an Associate Professor at the University of Cape Town’s (UCT) Graduate School of Business. He is a former Head of the College of Accounting at UCT. He teaches on the MBA and various Executive programs at UCT’s Graduate School of Business. He also runs a popular MBA elective on integrated thinking and reporting. He consults to the accounting profession and regularly presents courses on various aspects of accounting. Mark is the current chair of the adjudicating panel for the annual EY Excellence in Integrated Reporting awards. He has also previously been a member of the adjudication panel of the prior EY reporting awards since they were introduced in 1997.

Alexandra WatsonUntil March 2018, Alex was the Richard Sonnenberg Professor of Accounting in the College of Accounting at the University of Cape Town. She is a past member of the South African Integrated Reporting Committee Working Group, former vice chairman of the Global Reporting Initiative, current chairman of the Financial Reporting Investigations Panel and former Chairman of the Accounting Practices Committee, the technical accounting committee of SAICA. Alex is an independent director of companies and the WWF-SA. Alex has been a member of the adjudicating panel of the EY Excellence in Integrated Reporting awards, and prior EY reporting awards since they were introduced in 1997.

Goolam ModackGoolam is an Associate Professor in the Faculty of Commerce at the University of Cape Town. He is a former Head of the College of Accounting at UCT. He teaches financial reporting at an undergraduate and postgraduate level and has co-authored a number of financial reporting textbooks. Goolam has been a member of the adjudicating panel of the EY Excellence in Integrated Reporting awards, and prior EY reporting awards since 2005. Goolam has past experience as a member of the Malaysian Integrated Reporting adjudicating panel in 2017 and was an independent director of subsidiaries of a financial services group. He also consults to the accounting profession.

About the adjudicatorsAbout the adjudicators

Associate Professor Mark Graham

Graduate School of Business, UCT

Professor Emeritus, UCT

Associate Professor Goolam Modack

College of Accounting, UCT

Independent non-executive director Alex Watson

26 | Excellence in Integrated Reporting 2021

How can EY help?Integrated report benchmarking Contact person