Embed Size (px)

Citation preview

Investor Presentation – January 3, 2019

DisclaimerFORWARD-LOOKING STATEMENTS This presentation contains forward-looking statements and forward-looking information regarding Essential Energy Services Ltd. (the “Corporation” or

“Essential”) within the meaning of applicable securities laws. In particular, this presentation contains forward-looking statements including expectations

regarding 2018 and 2019 capital spending and 2019 in-service timing; expectations regarding Essential’s businesses/service lines, areas of growth,opportunities, activity, pricing, cost structure, outlook, upside, market share, competition, competitive advantages, services offered and the demand forthose services; the advantages of low debt; expectation that low debt provides Essential with greater control over its future and provides growth potential;expectations regarding deep coil supply and the ability for ECWS to grow its deep coil and pumping capacity if market demand dictates; and expectationswith regard to Essential’s advantages. By their nature, forward-looking statements and information involve known and unknown risks and uncertainties thatmay cause actual results to differ materially from those anticipated. Many of these factors and risks are described under the heading “Risk Factors” in theCorporation’s Annual Information Form for the year ended December 31, 2017 and the Corporation’s other filings on record with the securities regulatoryauthorities, which may be accessed through the SEDAR website (www.sedar.com). Although the Corporation believes the expectations and assumptions onwhich such forward-looking statements and information are based are reasonable, the Corporation can not provide assurance these expectations will proveto be correct. Accordingly, readers should not place undue reliance on the forward-looking statements and are cautioned that the foregoing factors are notexhaustive. The forward-looking statements and information contained in this presentation are made as of the date hereof and the Corporation undertakesno obligation to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events orotherwise, unless so required by applicable securities laws. This presentation contains an EV/2019 EBITDAS measure based on analyst consensus estimatesfor EBITDAS as of a particular point in time. The Corporation includes this measure for reference only and not for the purpose of endorsement. Theestimates underlying the EBITDAS estimate reflect the views of the analysts and may not reflect the views of management of the Corporation as at thepoint in time when the applicable estimate was given or as of the date of this presentation.

NON-IFRS MEASURESThroughout this presentation, certain terms used are not measures recognized by International Financial Reporting Standards (“IFRS”) and do not havestandardized meanings prescribed by IFRS including:

• EBITDAS – earnings before finance costs, income taxes, depreciation, amortization, transaction costs, losses or gains on disposal of equipment, write-down of assets, impairment loss, foreign exchange gains or losses and share-based compensation, which includes both equity-settled and cash-settled transactions. Calculated for continuing operations.

• Working capital – current assets less current liabilities.

These measures may not be consistent with the calculation of other companies.

® MSFS is a registered trademark of Essential Energy Services Ltd.

2

Essential Energy Services

3

We deliver oil and gas services for E&P customers as they complete, work-over and abandon wells

What: our equipment and crews are hired by E&P companies to get production out of the ground in an efficient and cost-effective manner

Where: primarily western Canada; with tool operations in the U.S.

Commodity exposure: oil, liquids-rich gas, natural gas - we service them all

ECWS

Coil Tubing Rigs

Fluid Pumpers

Nitrogen Pumpers

Tryton Tools

MSFS® Tools

Conventional Tools

Rentals

• Working capital well in excess of debt; debt to EBITDAS 1.2x (at Sept 30/18)

The Essential Advantage

4

• Skilled workforce

• 440 employees (at Nov 30/18)

• One of the largest deep coil tubing fleets in Canada (“ECWS”)

• An innovative tool business (“Tryton”)

Essential People

Industry Leading Equipment/Services

Low Debt

• Long-term customer relationships; diversity

• Equipment and crews for deeper, longer horizontal wells

Customers and Targeted Work

• Lean organization – cost efficient operations (70% variable)

• Cost structure adapts quickly to industry changes

Variable Cost Structure

Corporate Snapshot

5

(1) Jan 3/19 market capitalization and Sept 30/18 debt.(2) Jan 3/19 market capitalization, Sept 30/18 debt and Jan 3/19 analyst consensus.(3) Jan 3/19 share price and Sept 30/18 book value of shareholders’ equity less intangible assets.

Jan 3/19

Trading Price

52 Week Range

$0.315

$0.24 - $0.82

Market Capitalization $45 million

Long-term Debt (Sept 30/18) $24 million

Enterprise Value(1) $69 million

Working Capital (Sept 30/18) $64 million

Valuation Metrics:

EV/2019 EBITDAS(2) 2.7x

Price/Book(3) 0.3x

Very low valuation: working capital value is similar to enterprise value (i.e. there is no value in the share price for fixed assets or value for the tool business aside from inventory and accounts receivable)

6

Current Industry Challenges

WCSB Oil and Gas Industry

• Additional pipeline export capacity is needed – including pipelines to new markets

• The industry has been under siege from environmental and other interest groups

• Lack of political leadership and foresight ….a made in Canada problem

Implications

• Significant price differential to U.S. oil and natural gas prices

• Many institutional investors have become disinterested in the industry

• Lack of access to equity markets for E&P and oilfield service companies

• Share price implication in 2018 – significant share price decrease for many E&P and oilfield service companies

7

Why Canadian Oil and Gas?

• Production of Canadian oil and gas is subject to stringent environmental, safety and labour standards

• Failure to allow development of export pipelines costs the Canadian economy – estimated at more than $80 million per day(1)

(1) Alberta Government, Nov 19/18.

Consolidated Overview

9

Where We Operate

Canada: The key basins including the Montney, Duvernay, Bakken, Cardium and Viking

U.S.: The Permian, Eagle Fordand Anadarko basins

10

Segment Overview

• One of the largest deep coil tubing fleets in Canada – completions work

• Gen III and IV coil rigs for complex, long-reach horizontal wells

• Gen II coil rigs – steady work

• Fluid and nitrogen pumpers

• Canadian operations

• Employees: 300

• Fixed assets (NBV) Sept 30/18: $113 MM

• Working capital Sept 30/18: $27 MM

• Multi-stage frac system (MSFS®) tools –completions work

• Conventional downhole tools –production and abandonment work

• Rentals – including specialty drill pipe and BOP’s

• Canadian and U.S. operations

• Employees: 115

• Fixed assets (NBV) Sept 30/18: $23 MM

• Working capital Sept 30/18: $42 MM

ECWS Tryton

Tryton – Sept 30/18 Millions

Downhole Tools –Inventory Value

$29

Rentals Asset Value $17

ECWS – Dec 31/18 Equipment Count

Coil Tubing Rigs 29

Fluid Pumpers 19

Nitrogen Pumpers 8

11

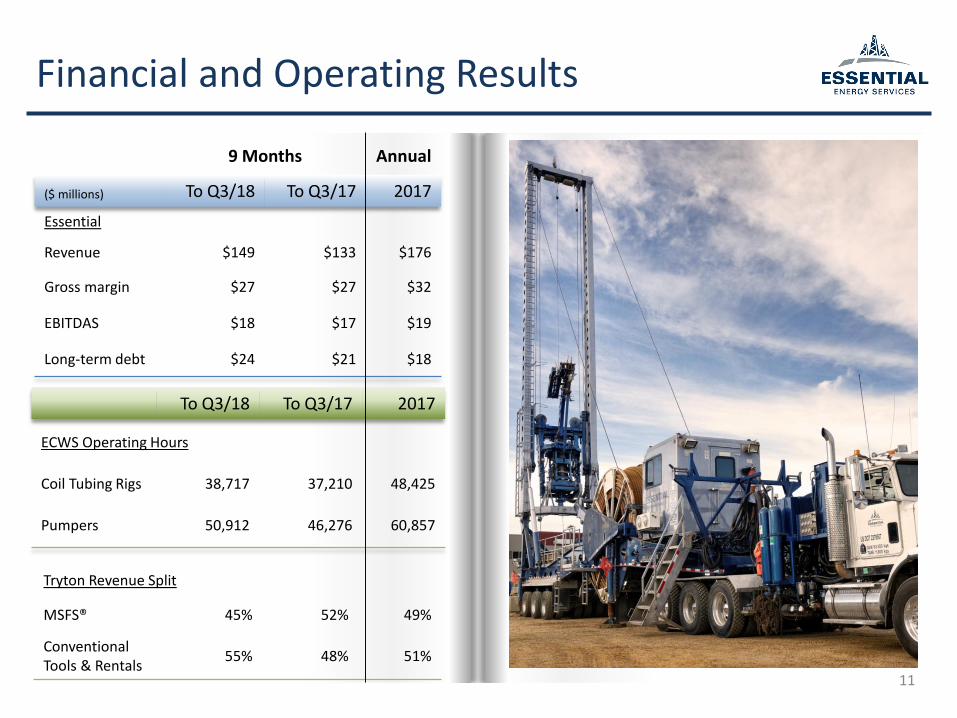

Financial and Operating Results

9 Months Annual

($ millions) To Q3/18 To Q3/17 2017

Essential

Revenue $149 $133 $176

Gross margin $27 $27 $32

EBITDAS $18 $17 $19

Long-term debt $24 $21 $18

Tryton Revenue Split

MSFS® 45% 52% 49%

ConventionalTools & Rentals

55% 48% 51%

To Q3/18 To Q3/17 2017

ECWS Operating Hours

Coil Tubing Rigs 38,717 37,210 48,425

Pumpers 50,912 46,276 60,857

TRYTON$15 MMECWS

$14 MM

12

Where Gross Margin is Generated

TRYTON$68 MMECWS

$81 MM

YTD Q3/18 Revenue: $149MM YTD Q3/18 Gross Margin: $27 MM(1)

(1) Chart excludes centralized overhead costs.

Gross Margin as a % of Revenue YTD Q3/18 YTD Q3/17

ECWS 17% 19%

Tryton 23% 25%

13

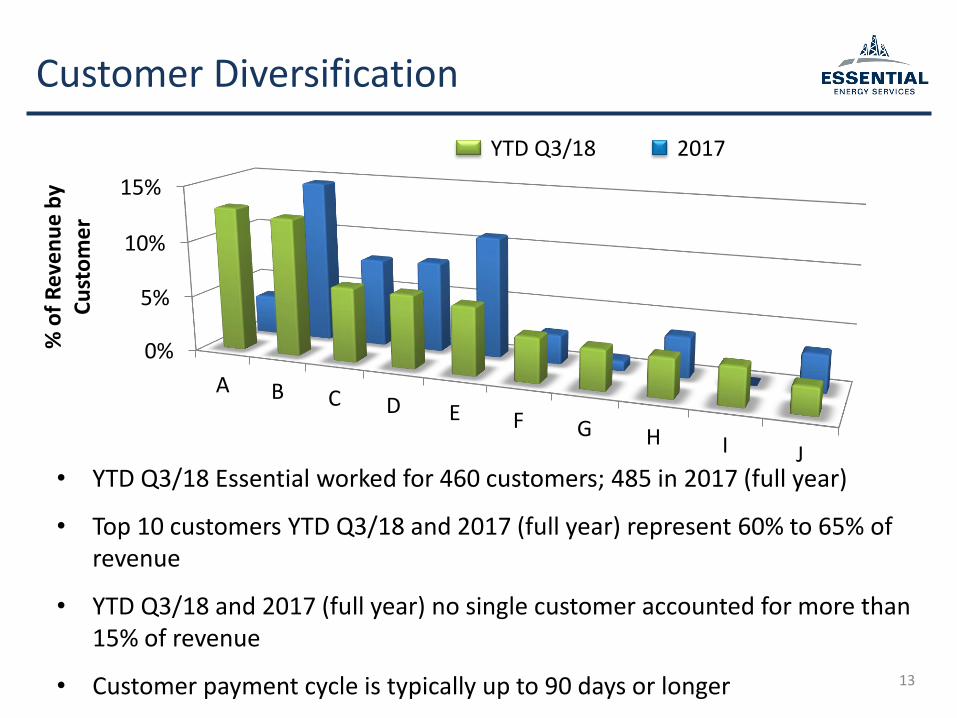

Customer Diversification

0%

5%

10%

15%

A B C D E F G H I J

% o

f R

eve

nu

e b

y C

ust

om

er

YTD Q3/18 2017

• YTD Q3/18 Essential worked for 460 customers; 485 in 2017 (full year)

• Top 10 customers YTD Q3/18 and 2017 (full year) represent 60% to 65% of revenue

• YTD Q3/18 and 2017 (full year) no single customer accounted for more than 15% of revenue

• Customer payment cycle is typically up to 90 days or longer

Essential’s Top 10 Customers

14

• Top 10 represents 60 – 65% of our revenue (YTD Q3/18 and 2017 full year)

• Proud to include names like:

• Customers are looking for:

o The right technology for the task

o Crew competency and continuity

o Stable pricing

o Efficiencies (e.g. wiperless milling)

o Strong safety record (e.g. low TRIF)

Tourmaline Murphy Oil

Shell NuVista Energy

ARC Resources Yangarra Resources

Kelt Exploration Crescent Point Energy

Velvet Energy Husky Energy

The Businesses:ECWS and Tryton

16

ECWS – Coil Tubing Rigs

Conventional Coil Tubing Rig – Rig 2049 Retrofit – Leading Edge

Milling Frac Seats/Bridge Plugs

39%

Fracturing with Coil(1)29%

Cleanout 15%

Stage Tool/Debris Sub Milling 11%

Other(2) 6%

ECWS Job Types

17

YTD Q3/18

(1) Third party fracturing equipment working in conjunction with an Essential coil tubing rig. This includes fracturing through coil or annular coil fracturing with a sliding sleeve system.

(2) Other includes logging and camera work, fishing, cementing and other work.

18

ECWS - Coil Tubing Fleet

At Dec 31/18

Total Fleet

ActiveFleet

Reach/Depth

(m at 2 ⅜”)Target Market

Gen I 2 2 2,700 Cleanouts

Gen II 14 4 4,500 Bakken, Cardium, Montney, Viking

Gen III 8 8 6,500 Montney, Duvernay

Gen IV(1) 5 2 7,200(2) Montney, Duvernay

Total 29 16

(1) Gen IV Total includes a reel trailer that is being retrofit in Q1/19 after which it will be able to work with a Gen II rig and achieve the same depth capacity as a Gen IV rig; it is not counted as Active in this chart and is expected to be Active mid-Q1/19

(2) 7,200 m if coil is transported on the rig; 9,400 m if coil is transported separately

Fleet menu to meet a variety of customer requirements

• Rigs will be activated as demand dictates through the CVIP process (Commercial Vehicle Inspection Program) and by adding crews

• The number of active rigs that are crewed and working varies with demand

• Masted and conventional rigs; greatest demand for the Gen III rigs

• ECWS has fluid pumpers and nitrogen pumpers to support the active fleet

Coil Tubing Demand

19

• Currently the most active plays in the WCSB include the Duvernay and the Montney

• Many of these wells are deeper, horizontal, often high pressure and complex

• Gen III and Gen IV rigs are best-suited for these regions

• Require skilled, experienced crews with a focus on safety

Record Depths:

ECWS: coil completion 7,100 m with a Gen IV rig (2 ⅜” coil)

Industry (WCSB): deepest well drilled 7,848 m

Coil tubing sector (WCSB): deepest coil completion is under 7,500 m

Growing proportion of wells are using deep coil tubing rigs

ECWS Gen IV Retrofit Program

20

• First retrofit in-service early Oct/18 – very well received by customers

• Suitable for Montney and Duvernay deep wells

• Features include:

o Light: 22 tonnes lighter than the original Gen IV design allowing ease of movement between work sites and on customer pads

o Safety and efficiency: efficient to rig-up and move; “quick change” reel system for on-location reel swaps in two hours or less

o Industry-leading reach: with 2 ⅜” coil tubing 7,200 m if coil is transported on the rig; 9,400 m if coil is transported separately

o Industry-leading injector capability: 130K and 160K injector capacity; higher capacity ensures no slippage or inefficiencies on the deepest horizontal wells

As industry demand for deep coil grows, ECWS will be ready

21

Tryton – Downhole Tools and Rentals

MSFS®: Composite Bridge Plug

MSFS®: Ball & Seat Balls

MSFS®: Ball & Seat “cut-away”

22

Tryton – Services Offered

MSFS® Tools

• Completions-focused

• Tools that allow producers to isolate and fracture intervals of horizontal sections of a well separately and continuously

• Primarily provided in Canada

Conventional Tools

• Completion, production and abandonment operations

• Includes conventional packers, tubing anchors, bridge plugs, cement retainers and related accessories

• Canada, U.S. and international

Tryton Rentals

• Drilling focused

• Offers a broad range of oilfield equipment including specialty drill pipe, blowout preventers, specialty equipment for steam-assisted gravity drainage wells

• Canadian operations

23

Tryton – Tool Diversity for Growth

MSFS® Tools – Growing the Number of Choices• Ball & Seat

o Continues to be the most common method

• V-Sleeveo Unlimited number of stages; coil actuatedo Q1/18: completed a 53-stage job in a single tool run in the Cardium

• Composite Bridge Plugo Unlimited number of stages; quick to mill-out

• Hybrid MSFS® – Ball & Seat plus Composite Bridge Plugo Ball & Seat at the “toe” and Composite Bridge Plugs toward the “heel”o Unlimited number of stageso Q1/18: completed two 90-stage MSFS® jobs in the Montney – including the

deepest well drilled to-date in western Canada at 7,848 m

24

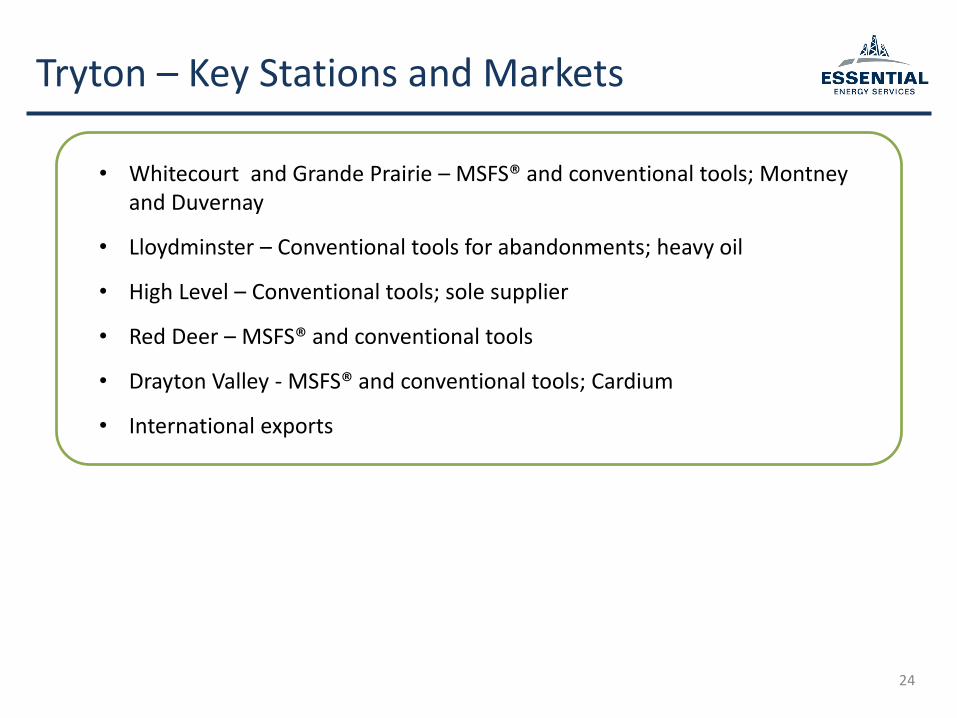

Tryton – Key Stations and Markets

• Whitecourt and Grande Prairie – MSFS® and conventional tools; Montney and Duvernay

• Lloydminster – Conventional tools for abandonments; heavy oil

• High Level – Conventional tools; sole supplier

• Red Deer – MSFS® and conventional tools

• Drayton Valley - MSFS® and conventional tools; Cardium

• International exports

Essential:Low Debt and Capital Spending

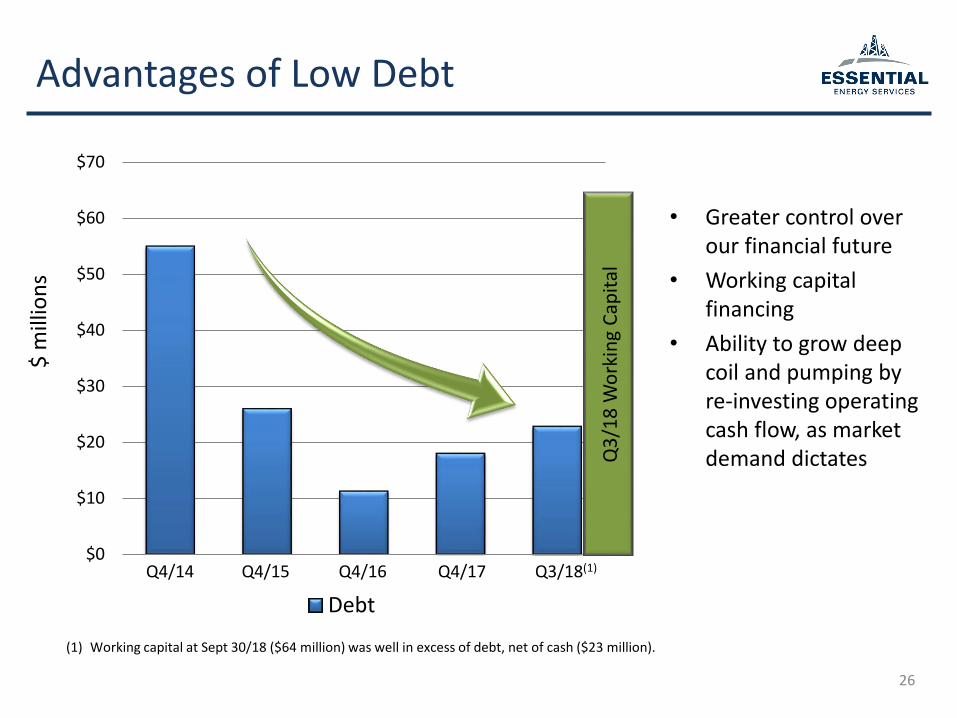

26

Advantages of Low Debt

$0

$10

$20

$30

$40

$50

$60

$70

$ m

illio

ns

Debt

Q4/14 Q4/16Q4/15 Q3/18(1)Q4/17

• Greater control over our financial future

• Working capital financing

• Ability to grow deep coil and pumping by re-investing operating cash flow, as market demand dictates

(1) Working capital at Sept 30/18 ($64 million) was well in excess of debt, net of cash ($23 million).

Q3

/18

Wo

rkin

g C

apit

al

27

Capital Spending Overview

Annual 2018 2017 2016

($ millions) Forecast Actual Actual

Growth $7 $11 $8

Maintenance 9 9 3

Total $16 $20 $11

Focus of 2018 Growth Spending:• Gen IV coil tubing rig retrofit• Two quintuplex fluid pumpers• One N2 pumper• A set of high pressure (15K) BOP’s

2019 Capital Spending Budget will be announced in Jan/19 – expected to be modest due to industry conditions

Looking Forward:Strategic Considerations

Canada - Deep Coil Market Considerations

29

• Industry fleet: the number of “relevant” deep/large diameter coil tubing rigs is small relative to the number of drilling rigs and services rigs

• Pricing has been flat to down (and still below 2014), which discourages investment in new rigs

• Pad work and “steady work” allows pricing and cost efficiencies

Canada - Coil and Pumping Competition

30

• Fraccers in Canada (Trican, Calfrac, STEP) often, but not always, supply their own coil in the current slow market

• International fraccers (Haliburton, BJ-Baker and Schlumberger) typically do not have coil in Canada

• Coil companies (public and private) are struggling – as we are – to make a proper return in Canada given weak pricing

• Some competitor equipment has left Canada – this may result in future “tightness” in deep coil supply if industry spending increases

31

Essential – Upside

ECWS:

• First Gen IV retrofit proves design and engineering

• Four additional Gen IV retrofits can be added – as market demand dictates

• Time and cost of a retrofit is significantly lower than a new build

• Reel trailer retrofit (expected Q1/19) will operate with a Gen II to “deepen” its capacity

• Opportunity to add new quintuplex fluid pumpers and nitrogen pumpers to pair with deep coil rigs – as market demand dictates

• Potential upside from LNG

Tryton:

• Expand market share with innovative/incremental MSFS® tools; customers can choose the tool best suited for wellbore characteristics and preference

• Potential upside from LNG

• Undervalued by many metrics (EV/EBITDAS, Price to Book)

• Debt to EBITDAS: 1.2x at Sept 30/18

• New MSFS® tools provide customers a choice

• Low capital intensity

• Strong customer relationships

• Suitable for complex, long-reach horizontal wells

• Fleet capacity can be increased and “deepened” as market demand dictates

Why Invest in Essential?

32

Innovative Tool Business

Low Debt

Valuation

Industry Leading Coil Tubing Fleet

Appendix

Essential on site near Grande Prairie

Coil Tubing Fleet

34

Gen I Gen II Gen III Gen IV

Number of rigs at Dec 31/18: (Total: 29)

2 14 8 5(1)

1 1/2” coil diameter 8,150 m - - -

1 3/4” coil diameter 5,580 m - - -

2” coil diameter 4,500 m 5,500 m 8,400 m -

2 3/8” coil diameter 2,700 m 4,500 m 6,500 m 7,200 m(2)

2 5/8” coil diameter - 3,500 m 5,200 m 6,700 m

2 7/8” coil diameter - 2,700 m 4,300 m 5,300 m

Injector capacity60,000 lbs,

80,000 lbs100,000 lbs 130,000 lbs

130,000 lbs,

160,000 lbs

(1) Gen IV count includes a reel trailer that is being retrofit in Q1/19 after which it will be able to work with a Gen II rig and achieve the same depth capacity as a Gen IV rig

(2) 7,200 m if the coil is transported on the rig; 9,400 m if the coil is transported separately – using 2 3/8” coil tubing

Deep Coil: Completions & Work-Overs

35

• The number of long-reach horizontal wells increases the demand for Essential’s coil tubing rigs

• In the well completion phase, coil tubing rigs are used for:

Pre-Fracturing

Confirmation runs

Placement of tools to isolate a portion of the well

during facturing

Fracturing

Frac-thru coil

Annular fracturing

Convey and actuate sliding sleeve tools

“Plug-and-perf” operations

Post-Fracturing

Confirmation runs

Cleanouts

Mill-out/drill-out ball and seat systems

• In the post completion phase, coil tubing rigs are used for work-overs and abandonments

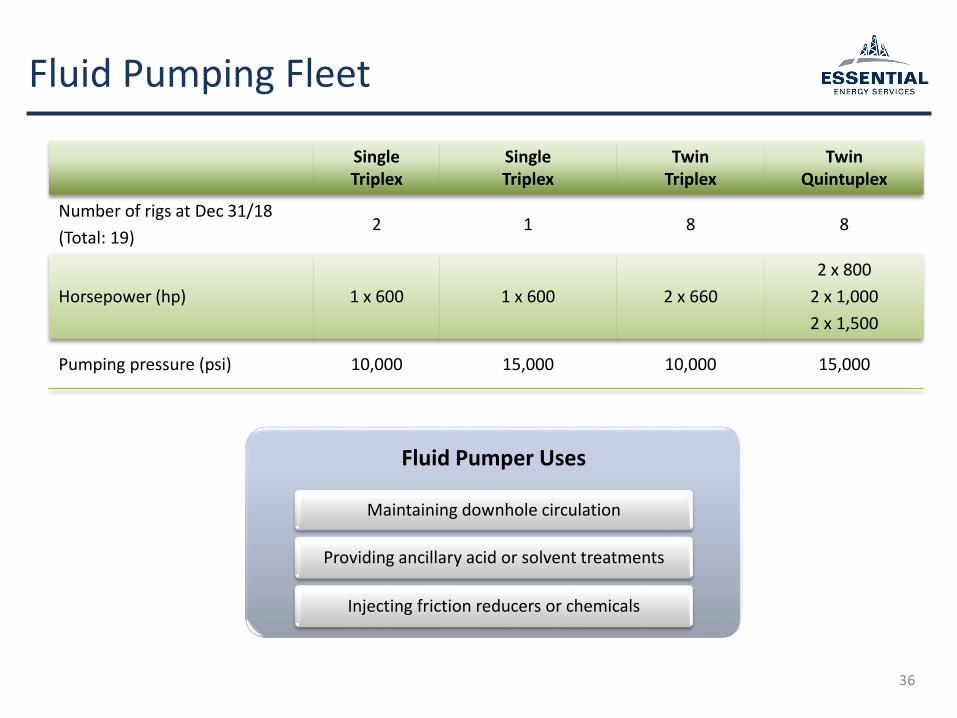

Fluid Pumping Fleet

36

SingleTriplex

SingleTriplex

TwinTriplex

TwinQuintuplex

Number of rigs at Dec 31/18

(Total: 19)2 1 8 8

Horsepower (hp) 1 x 600 1 x 600 2 x 660

2 x 800

2 x 1,000

2 x 1,500

Pumping pressure (psi) 10,000 15,000 10,000 15,000

Fluid Pumper Uses

Maintaining downhole circulation

Providing ancillary acid or solvent treatments

Injecting friction reducers or chemicals

Garnet AmundsonPresident, Chief Executive Officer & Director

Karen PerasaloInvestor Relations

1100, 250 – 2nd Street SWCalgary, Alberta T2P 0C1(403) 513-7272 [email protected]

www.essentialenergy.ca

TSX:ESN