Embed Size (px)

DESCRIPTION

Citation preview

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5 1

SEMPERIT GROUP

INVESTOR PRESENTATION

FY 2013

27 March 2014

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Key Highlights

Operational Development

Financial Performance

Outlook

Agenda

2 Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Excellent financial year 2013

3

Growth and high profitability in a difficult economic environment

Revenue up +9.4% to EUR 906.3m in 2013 (2012: EUR 828.6m)

Record levels for EBITDA (EUR 132.5m) and EBIT (EUR 87.8m)

Proposed dividend: EUR 0.90 basic dividend/share (2012: EUR 0.80)

+ one-time EUR 0.30 anniversary bonus/share

Best year in the history of Semperit

Latexx Partners successfully integrated within one year

Sales and marketing activities stepped up in all segments worldwide

Successful introduction of new products

Winning strategic customers and expansion of market shares

Active strategic raw material management and rigorous cost discipline take effect

Success through implementation of strategic growth projects

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

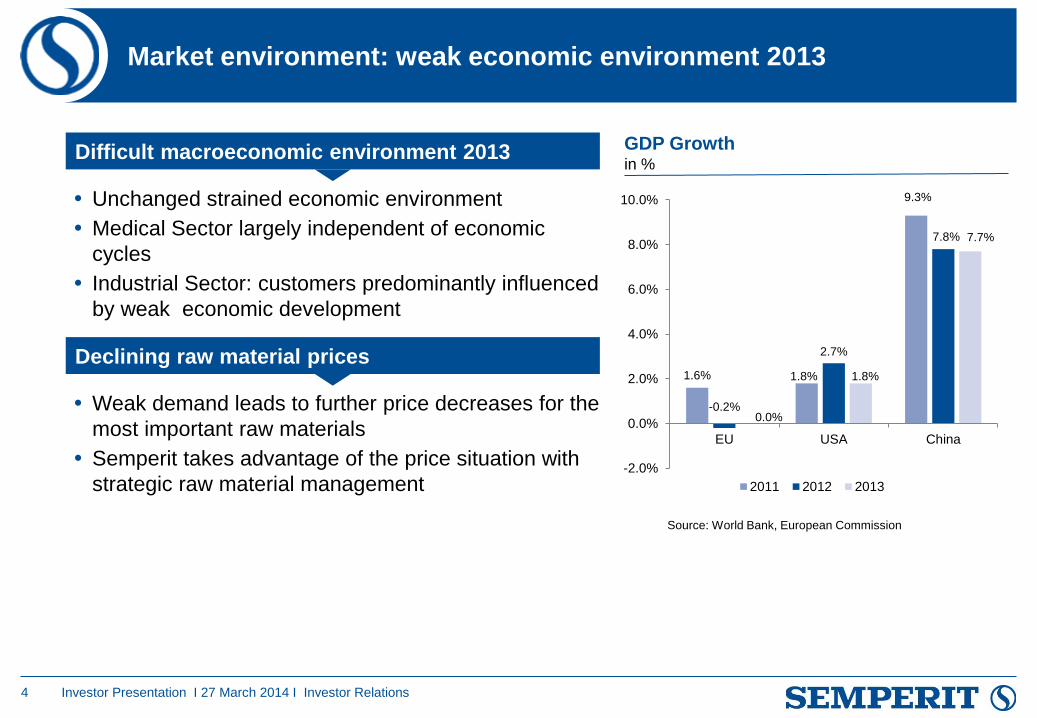

Market environment: weak economic environment 2013

4

Unchanged strained economic environment

Medical Sector largely independent of economic

cycles

Industrial Sector: customers predominantly influenced

by weak economic development

Difficult macroeconomic environment 2013

Weak demand leads to further price decreases for the

most important raw materials

Semperit takes advantage of the price situation with

strategic raw material management

Declining raw material prices

Investor Presentation I 27 March 2014 I Investor Relations

GDP Growth in %

1.6% 1.8%

9.3%

-0.2%

2.7%

7.8%

0.0%

1.8%

7.7%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

EU USA China

2011 2012 2013

Source: World Bank, European Commission

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Key Highlights

Operational Development

Financial Performance

Outlook

Agenda

5 Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Population increase to

9.6 billion people by 2050 (2013: 7.2 billion).1)

Growing prosperity in emerging markets.

Improved hygiene standards in the

emerging markets.

Increasing life expectancy and shift in age

pyramid in industrialised nations.

Medical Sector:

Megatrends as long-term growth drivers

6

Growth market healthcare

1) UNO

Consumption of examination gloves

per capita and year in units

150 - 160

60 - 70

25 - 30 10 - 20

USA Europe Latin America Asia

Source: Semperit

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Sempermed 2013:

Global Growth

7

Successful integration of Latexx Partners enables growth

Sempermed headquarters in Singapore has proven successful

Sempermed grows faster than the market

Capacity utilisation of production facilities above 80%

Examination gloves with strong demand in Europe and the USA

Strong development of application areas industrial and

consumer goods

Business Development

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Industrial Sector

Megatrends as long-term growth drivers

8

Urbanisation, energy consumption & expansion of infrastructure drive growth

Energy and raw material

requirements

Semperflex Semperform Sempertrans

Infrastructure and industrialisation Urbanisation and mobility

2

3

4

5

6

2000 2005 2010 2015 2020 2025

Coal Oil Gas

Regional demand for construction

machinery (in USD bn)

Global construction markets until

2025 (in USD bn)

Global demand for primary energy

sources (in bn tonnes)

8.8

15.0

5

10

15

20

2012 2025

Source: www.statista.com Source: Wood Mackenzie, IEA (International Energy Agency) Source: Global Construction 2025

+70%

34.7

25.8 20.8

4.5 4.6

43.9 39.4

24.5

8.0 6.1

China NorthAmerica

Europe India Latin America

2011

2015

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Semperflex 2013:

Market share gains in Europe and Asia

9

Growth despite weak economy

Increased internationalisation and sales campaign successful

Optimal use of market consolidation to win new customers

Hydraulic hoses: strong business in Europe and recovery in

the USA

Industrial hoses: expansion of the leading market position in

Europe and first strategic steps in the USA and Asia

Business Development

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Sempertrans 2013:

New strategy and the right products prove successful

10

Very good development confirms sustainable turnaround

Internationalisation with increased sales activities in South

America, Asia and Africa continued

Major contracts for a new energy-saving conveyor belt with

German energy company RWE and in Poland

Very good capacity utilisation and start of capacity expansion

in Bełchatów/Poland

Business Development

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Semperform 2013:

Filling attractive growth niches

11

Double-digit volume growth in relevant market niches

Sales and marketing activities strengthened further

Expansion of market shares in building profiles, industrial

moulded parts and handrails

Production capacities fully utilised

Business Development

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Key Highlights

Operational Development

Financial Performance

Outlook

Agenda

12 Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

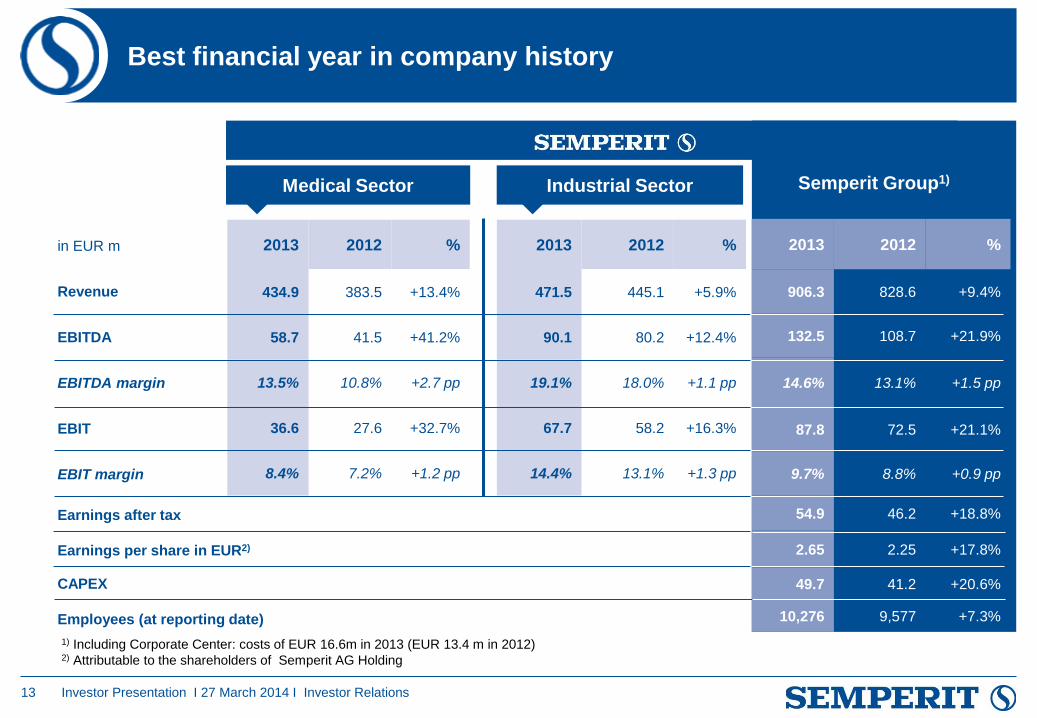

Best financial year in company history

13

2013 2012 %

434.9 383.5 +13.4%

58.7 41.5 +41.2%

13.5% 10.8% +2.7 pp

36.6 27.6 +32.7%

8.4% 7.2% +1.2 pp

in EUR m

Revenue

EBITDA

EBITDA margin

EBIT

EBIT margin

Earnings after tax

Earnings per share in EUR2)

CAPEX

Employees (at reporting date)

Medical Sector Industrial Sector

2013 2012 %

471.5 445.1 +5.9%

90.1 80.2 +12.4%

19.1% 18.0% +1.1 pp

67.7 58.2 +16.3%

14.4% 13.1% +1.3 pp

2013 2012 %

906.3 828.6 +9.4%

132.5 108.7 +21.9%

14.6% 13.1% +1.5 pp

87.8 72.5 +21.1%

9.7% 8.8% +0.9 pp

54.9 46.2 +18.8%

2.65 2.25 +17.8%

49.7 41.2 +20.6%

10,276 9,577 +7.3%

Semperit Group1)

1) Including Corporate Center: costs of EUR 16.6m in 2013 (EUR 13.4 m in 2012) 2) Attributable to the shareholders of Semperit AG Holding

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

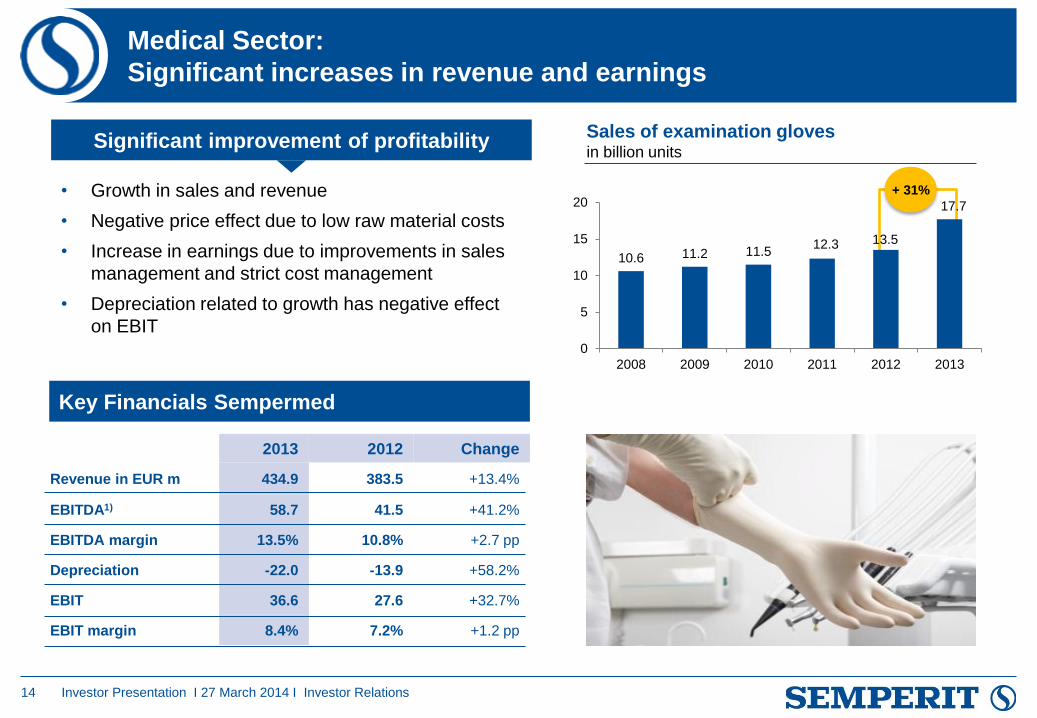

Medical Sector:

Significant increases in revenue and earnings

14

2013 2012 Change

Revenue in EUR m 434.9 383.5 +13.4%

EBITDA1) 58.7 41.5 +41.2%

EBITDA margin 13.5% 10.8% +2.7 pp

Depreciation -22.0 -13.9 +58.2%

EBIT 36.6 27.6 +32.7%

EBIT margin 8.4% 7.2% +1.2 pp

Significant improvement of profitability

• Growth in sales and revenue

• Negative price effect due to low raw material costs

• Increase in earnings due to improvements in sales

management and strict cost management

• Depreciation related to growth has negative effect

on EBIT

Key Financials Sempermed

Investor Presentation I 27 March 2014 I Investor Relations

Sales of examination gloves in billion units

+ 31%

10.6 11.2 11.5 12.3 13.5

17.7

0

5

10

15

20

2008 2009 2010 2011 2012 2013

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

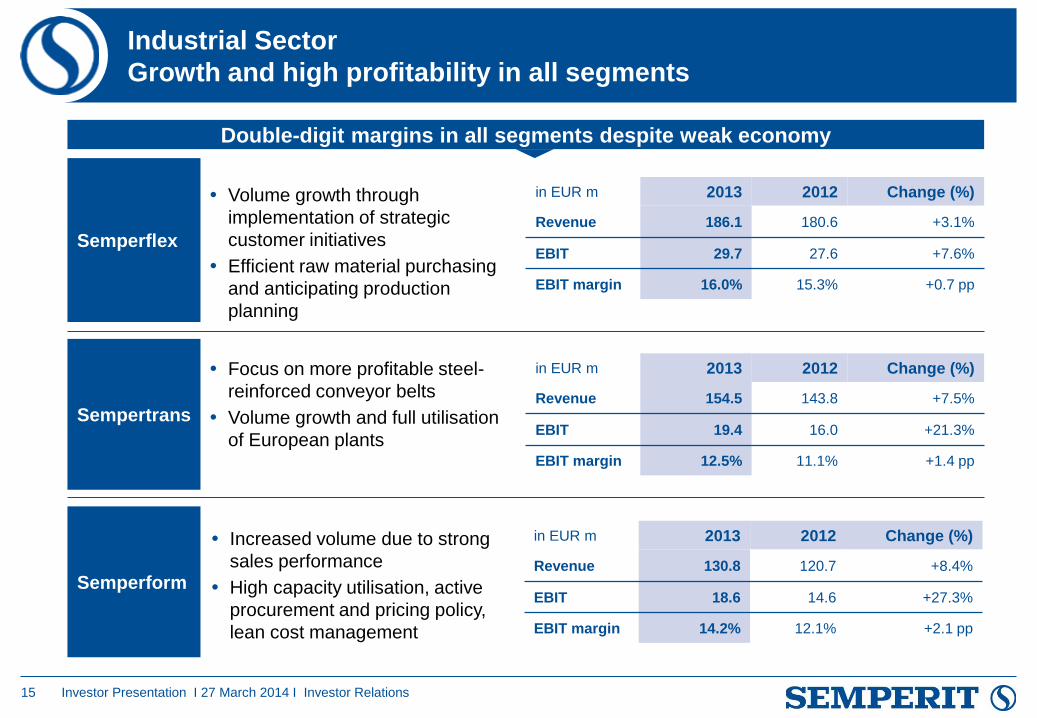

Industrial Sector

Growth and high profitability in all segments

15

Semperflex

Sempertrans

Semperform

Volume growth through

implementation of strategic

customer initiatives

Efficient raw material purchasing

and anticipating production

planning

Focus on more profitable steel-

reinforced conveyor belts

Volume growth and full utilisation

of European plants

Increased volume due to strong

sales performance

High capacity utilisation, active

procurement and pricing policy,

lean cost management

in EUR m 2013 2012 Change (%)

Revenue 186.1 180.6 +3.1%

EBIT 29.7 27.6 +7.6%

EBIT margin 16.0% 15.3% +0.7 pp

Double-digit margins in all segments despite weak economy

in EUR m 2013 2012 Change (%)

Revenue 154.5 143.8 +7.5%

EBIT 19.4 16.0 +21.3%

EBIT margin 12.5% 11.1% +1.4 pp

in EUR m 2013 2012 Change (%)

Revenue 130.8 120.7 +8.4%

EBIT 18.6 14.6 +27.3%

EBIT margin 14.2% 12.1% +2.1 pp

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Excellent cash position and high internal financing capability

16

Cash flow in EUR m

Cash flow from operating activities up 29% to

EUR 137.2m

Cash flow from investing activities at EUR -47.8m after

EUR -151.6m in 2012

(Acquisition of Latexx Partners in 2012)

Cash flow from financing activities amounting to

EUR -32.4m (2012: EUR 80.7m) was characterised by:

Issue of Corporate Schuldschein loan

Repayment of credit lines

Dividend payments

Increase in shareholding in Latexx Partners from

85% to 98%

Cash and cash equivalents rise by 37% to EUR 182.6m

(2012: EUR 133.3m).

Highlights 2013

Investor Presentation I 27 March 2014 I Investor Relations

133.3

-7.7

182.6

Currency effects

Other Items -10.7

Latexx Partners -19.5

CAPEX

Dividend -16.5

Repayment of credits -108,4

Corp. Schuldschein loan +124,6

-49,6

Working capital +21.0

Cash flow from results +116,2

Cash and cash

equivalents 1.1.2013

Cash and cash

equivalents 31.12.2013

+116.2

-108.4

+124.6

-49.6

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

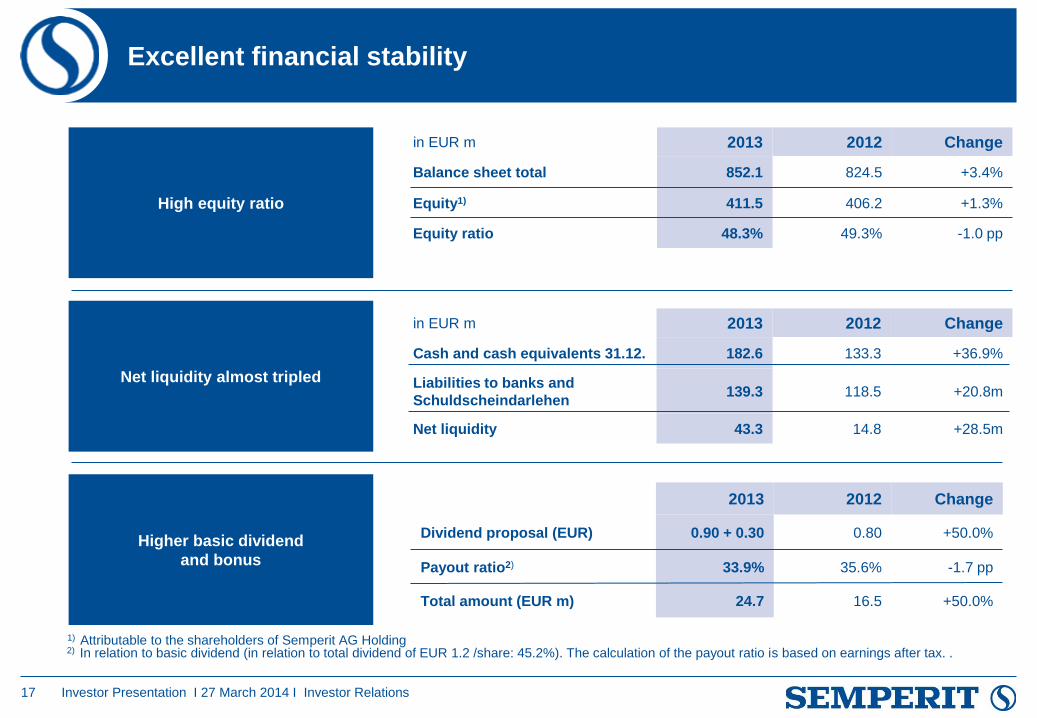

Excellent financial stability

17

in EUR m 2013 2012 Change

Balance sheet total 852.1 824.5 +3.4%

Equity1) 411.5 406.2 +1.3%

Equity ratio 48.3% 49.3% -1.0 pp

in EUR m 2013 2012 Change

Cash and cash equivalents 31.12. 182.6 133.3 +36.9%

Liabilities to banks and

Schuldscheindarlehen 139.3 118.5 +20.8m

Net liquidity 43.3 14.8 +28.5m

2013 2012 Change

Dividend proposal (EUR) 0.90 + 0.30 0.80 +50.0%

Payout ratio2) 33.9% 35.6% -1.7 pp

Total amount (EUR m) 24.7 16.5 +50.0%

High equity ratio

Net liquidity almost tripled

Higher basic dividend

and bonus

1) Attributable to the shareholders of Semperit AG Holding 2) In relation to basic dividend (in relation to total dividend of EUR 1.2 /share: 45.2%). The calculation of the payout ratio is based on earnings after tax. .

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

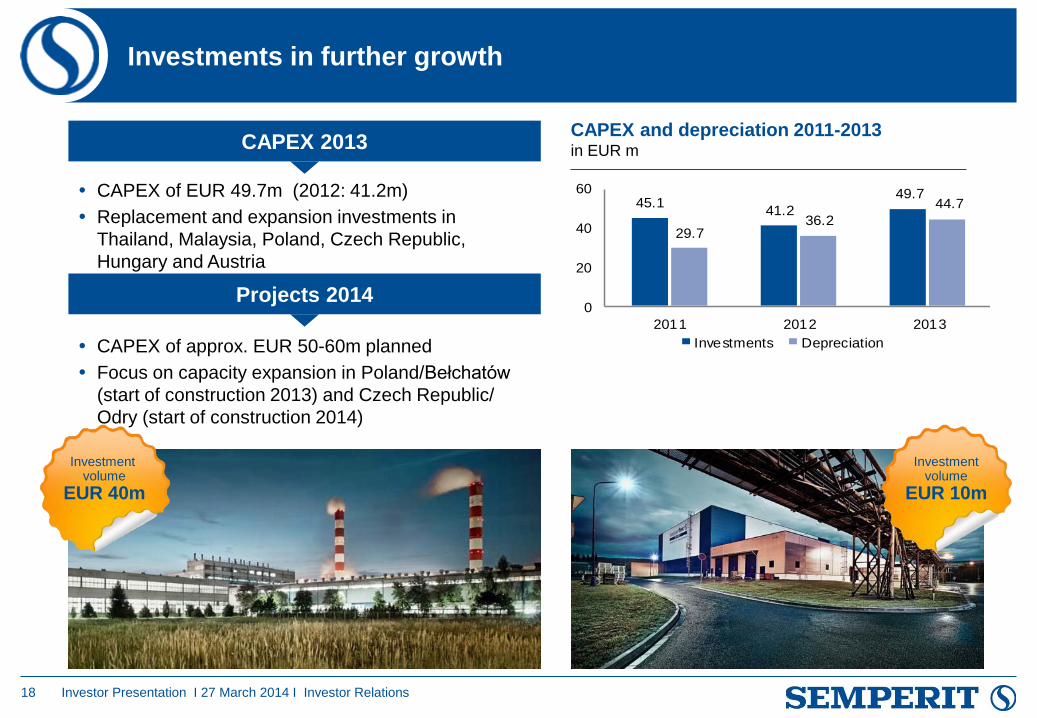

Investments in further growth

18

CAPEX 2013

Projects 2014

CAPEX of approx. EUR 50-60m planned

Focus on capacity expansion in Poland/Bełchatów

(start of construction 2013) and Czech Republic/

Odry (start of construction 2014)

CAPEX of EUR 49.7m (2012: 41.2m)

Replacement and expansion investments in

Thailand, Malaysia, Poland, Czech Republic,

Hungary and Austria

Investment volume

EUR 40m

Investment volume

EUR 10m

Investor Presentation I 27 March 2014 I Investor Relations

CAPEX and depreciation 2011-2013 in EUR m

45.141.2

49.7

29.736.2

44.7

0

20

40

60

2011 2012 2013

Investments Depreciation

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Performance of the Semperit share

19

Semperit share vs. ATX 2013 in EUR m

Key figures Semperit share

26

28

30

32

34

36

38

40

Jan Feb March April May June July Aug Sep Oct Nov Dec 2013

ATX

+6.1%

Semperit

+14.8%

Key figures 2013 2012

Share price at 31.12. in EUR 36.00 31.36

Lowest price in EUR 26.86 26.65

Highest price in EUR 38.22 33.90

Market capitalisation at 31.12. in EUR m 740.6 645.2

Price/earnings ratio 13.6 13.9

Earnings per share in EUR 2.65 2.25

Dividend per share in EUR 0.90 0.80

Dividend payout ratio basic dividend 33.9% 35.6%

Anniversary bonus in EUR 0.30 –

Dividend payout ratio

incl. anniversary bonus 45.2% 35.6%

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Key Highlights

Operational Development

Financial Performance

Outlook

Agenda

20 Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Outlook 2014:

Focus on capacity expansion and organic growth

21

Satisfactory development of the Semperit Group expected

Unchanged growth targets

Continuation of today’s good order situation

Currently high capacity utilisation – expansions will be available as of

the first half of 2015

Satisfactory development of revenue and earnings expected

CAPEX of roughly EUR 50-60 million with a focus on capacity expansion in

Poland and the Czech Republic

No significant growth impulses expected on the economy side

Raw material prices at historic low – no further decline to be expected

Double-digit average revenue growth 2010-2015 (CAGR)

EBITDA margin of 12 - 15%

EBIT margin of 8 - 11%

Largely unchanged market environment

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5 22

SEMPERIT GROUP

INVESTOR PRESENTATION

FY 2013

27 March 2014

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Contact and Financial Calendar

23 Investor Presentation I 27 March 2014 I Investor Relations

Investor Relations

+43 1 79777 - 210

www.semperitgroup.com/en/ir

Modecenterstrasse 22

1031 Vienna, Austria

Financial calendar 2014 of Semperit

29 April 2014 Annual general meeting, Vienna

6 May 2014 Ex-dividend day

8 May 2014 Dividend payment day

20 May 2014 Report on Q1 2014

19 August 2014 Report on H1 2014

18 November 2014 Report on Q1-3 2014

Disclaimer

The information provided in this presentation does not constitute an offer for the sale of securities nor an

invitation to submit an offer to purchase shares of Semperit AG Holding, but exclusively serves information

purposes.

The forecasts, plans and forward-looking statements contained in this report are based on the knowledge

and information available and the assessments made at the time that this report was prepared. As is true of

all forward-looking statements, these statements are subject to risk and uncertainties. As a result, the

actual events may deviate significantly from these expectations. No liability whatsoever is assumed for the

accuracy of projections or for the achievement of planned targets or for any other forward-looking

statements.

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Key Highlights

Operational Development

Financial Performance

Outlook

Agenda

24

Appendix

Investor Presentation I 27 March 2014 I Investor Relations

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Income Statement

25

Underproportional increase in material costs

due to active raw material management and

lower raw material prices

Increase in personnel expenses due to higher

number of employees (esp. Latexx Partners)

Higher other operating expenses due to higher

maintenance costs, outgoing freight and

strategic projects

Higher depreciation due to growth (new

capacities in Surat Thani, Latexx Partners)

Tax rate rises from 16.7% to 18.7%

Higher basic dividend (EUR 0.90/share) + one-

time anniversary bonus (EUR 0.30/share) result

in a payout ratio of 45.2%

in EUR m 2013 2012 Change

Revenue 906.3 828.6 +9.4%

Changes in inventories 9.4 --1.9 -

Own work capitalised 1.0 1.6 -39.3%

Other operating income 24.4 32.8 -25.6%

Material costs -510.7 -501.0 +1.9%

Personnel expenses -152.8 -127.4 +19.9%

Other operating expenses -145.8 -124.1 +17.4%

EBITDA 132.5 108.7 +21.9%

Depreciation and amortisation -44.7 -36.2 +23.6%

EBIT 87.8 72.5 +21.1%

Financial result -16.9 -14.0 +20.1%

EBT 70.9 58.5 +21.3%

Income taxes -16.0 -12.2 +30.9%

Earnings after tax 54.9 46.2 +18.8%

EPS (EUR) 2.65 2.25 +17.8%

DPS (EUR) 1.20 0.80 +50.0%

Key figures income statement 2013 vs. 2012 Highlights 2013

255

255

255

0

77

148

215

38

19

113

120

125

185

191

194

227

230

232

136

154

199

208

213

233

0

0

0

118

175

55

255

223

79

255

154

5

Solid balance sheet structure

26

in EUR m 2013 2012 Change

Assets 372.7 391.1 -4.7%

Inventories 148.4 142.5 +4.2%

Trade receivables

111.2 120.2 -7.4%

Other assets incl.

deferred taxes 219.7 170.8 +28.7%

Total assets 852.1 824.5 +3.4%

in EUR m 2013 2012 Change

Equity 414.2 428.0 -3.2%

Liabilities from redeemable non-

controlling interests 102.4 110.1 -7.0%

Provisions incl. social capital 73.7 64.8 +13.6%

Corporate Schuldschein loan 125.8 0.0 -

Liabilities incl. deferred taxes 136.1 221.6 -38.6%

Equity & Liabilities 852.1 824.5 +3.4%

Highlights 2013 Balance sheet indicators 2013 vs. 2012

Balance sheet total increases primarily due to

higher cash and cash equivalents

(EUR 182.6m)

Property, plant and equipment declines by 4.2%

to EUR 256.6m due to depreciation and

currency effects

Trade working capital declines from

EUR 212.1m to EUR 186.6m

Equity EUR 411.5m (excl. non-controlling

interests)

Liabilities increased by EUR 41.5m to

EUR 438m, especially due to the Corporate

Schuldschein loans.

Investor Presentation I 27 March 2014 I Investor Relations

![Investor Presentation Q4 FY 2016 [Company Update]](https://img.dokumen.tips/doc/110x75/577c7fb51a28abe054a5bb0b/investor-presentation-q4-fy-2016-company-update.jpg)