Embed Size (px)

Citation preview

Investor PresentationApril-June 2021

Forward looking statements and non-IFRS measures

This document may contain forward-looking statements that may or may not prove accurate. For example, statements regarding expected revenue growth

and trading profit margins, market trends and our product pipeline are forward-looking statements. Phrases such as "aim", "plan", "intend", "anticipate",

"well-placed", "believe", "estimate", "expect", "target", "consider" and similar expressions are generally intended to identify forward-looking statements.

Forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause actual results to differ materially

from what is expressed or implied by the statements. For Smith+Nephew, these factors include: risks related to the impact of COVID, such as the depth and

longevity of its impact, government actions and other restrictive measures taken in response, material delays and cancellations of elective procedures,

reduced procedure capacity at medical facilities, restricted access for sales representatives to medical facilities, or our ability to execute business continuity

plans as a result of COVID; economic and financial conditions in the markets we serve, especially those affecting health care providers, payers and

customers (including, without limitation, as a result of COVID); price levels for established and innovative medical devices; developments in medical

technology; regulatory approvals, reimbursement decisions or other government actions; product defects or recalls or other problems with quality

management systems or failure to comply with related regulations; litigation relating to patent or other claims; legal compliance risks and related

investigative, remedial or enforcement actions; disruption to our supply chain or operations or those of our suppliers (including, without limitation, as a

result of COVID); competition for qualified personnel; strategic actions, including acquisitions and dispositions, our success in performing due diligence,

valuing and integrating acquired businesses; disruption that may result from transactions or other changes we make in our business plans or organisation to

adapt to market developments; relationships with healthcare professionals; reliance on information technology and cybersecurity; and numerous other

matters that affect us or our markets, including those of a political, economic, business, competitive or reputational nature. Please refer to the documents

that Smith+Nephew has filed with the U.S. Securities and Exchange Commission under the U.S. Securities Exchange Act of 1934, as amended, including

Smith+Nephew's most recent annual report on Form 20-F, for a discussion of certain of these factors. Any forward-looking statement is based on information

available to Smith+Nephew as of the date of the statement. All written or oral forward-looking statements attributable to Smith+Nephew are qualified by

this caution. Smith+Nephew does not undertake any obligation to update or revise any forward-looking statement to reflect any change in circumstances or

in Smith+Nephew's expectations. The terms ‘Group’ and ‘Smith+Nephew’ are used for convenience to refer to Smith & Nephew plc and its consolidated

subsidiaries, unless the context requires otherwise.

Certain items included in ‘trading results’, such as trading profit, trading profit margin, tax rate on trading results, trading cash flow, trading profit to cash

conversion ratio, EPSA, leverage ratio, and underlying growth are non-IFRS financial measures. The non-IFRS financial measures in this announcement are

explained and reconciled to the most directly comparable financial measure prepared in accordance with IFRS in our Fourth Quarter and Full Year 2020

Results announcement dated 18 February 2021, and our First Quarter 2021 trading report dated 29 April 2021.2

3

1856Thomas James Smith

opened a chemist shop in Hull,UK and develops a new method

for refining cod liver oil

1986Key acquisitions of Richards Medical Company

in Memphis, specialists in orthopaedic products

and DYONICS, an arthroscopy specialists

based in Andover

1995Acquired

Acufex Microsurgical Inc,

making us a market leader in

arthroscopic surgicaldevices

1999

We were listed on the New York Stock

Exchange and in 2001 became a constituent

member of the UK FTSE-100 index

2001

OXINIUM◊, a new material that

improves performance and increases

the service life of total joint

replacement systems, first introduced

2011

PICO◊, the first pocket-sized, single-use

system, revolutionizes the negative

pressure wound therapymarket

2013

JOURNEY◊II BCS sets a new standard inknee

implant performance,designed

to empower patients to return

to an activelifestyle

We exist to restore people’sbodies and their self-belief by using technologies to take the limits off living.

We call this purpose “LifeUnlimited”

2014

Acquired ArthrocareCorp.

to expand our sports

medicine portfolio

2020

We are proud of what we do

and value our 17,500 employees

who make thispossible

1953

We developed a special low-temperatureplaster

for the Everest climbers on the 1953 expedition.

It enabled them to send back their camera films, sealed

and airtight!. This same research led to the development

of importantindustrial products

1937We were listed on the

London stock exchange1928

We produced an

experimental bandage

ElastoplastTM

1896Horatio Nelson Smith

entered into apartnership

with his uncleforming

TJ Smith & Nephew

1914Days after the outbreak of WW1,

we received an order to provide

surgical and field dressing

supplies to French

army within 5months

During WW1, staff grew

from 50 to 1,200

From50

To1200

Over 100

17,500+

◊Trademark of Smith & Nephew, ©2020 Smith & Nephew

1856Smith+Nephew

established

Todayand growing

Our history

2019

Expanding in technologies of the

future, investing inOrthopaedics,

Biologics and Digital Surgery.

4

100Smith+Nephew is a portfolio medical technology business that has been trading for over 160 years, and operates in more than 100 countries

A constituent of the UK’s FTSE 100, with ADRstraded on the New York Stock Exchange

FTSE 100

Annual sales in 2020 were $4.6 billion

$4.6bn

S+N has a progressive dividend policy, and has paid a dividend every year since 1937

Shares

We have around 18,000 employees globally

~18,000

A portfolio medical technology business

5

Other Recon

Advanced Wound Care

Advanced WoundBioactives

Arthroscopic Enabling Technologies

Sports MedicineJoint Repair Trauma

Hips

Knees

Advanced Wound Devices

ALLEVYN◊ LIFEAdvanced Foam Wound Dressings

Collagenase SANTYL◊ Ointment Enzymatic debrider

CORI◊

Surgical System

COBLATION◊

Wand

REGENETEN◊

Bioinductive Implant

PICO◊

Negative Pressure Wound Therapy

JOURNEY◊ II BCSBi-Cruciate

StabilisedKnee System

$4.6bnRevenues

(2020)

OR3O◊

Dual Mobility

EVOS◊ SMALLPlating System

ENT

Leading positions in attractive markets

Zimmer

Biomet33%

Stryker

22%

DePuy

Synthes19%

Smith+

Nephew11%

Others

15%

Arthrex

33%

Smith+

Nephew26%

DePuy

Mitek13%

Stryker

11%

Others

17%3M

19%

Smith+

Nephew14%

Molnlycke

9%Convatec

7%

Others

51%

Data used in 2020 estimates generated by Smith+Nephew is based on publicly available sources and internal analysis and represents an indication of market shares1 A division of Johnson & Johnson.

$12.6bn market+2% 2017-19 average growth

-15% 2020 growth

$4.6bn market+5% 2017-19 average growth

-12% 2020 growth

$9.1bn market+5% 2017-19 average growth

-3% 2020 growth

#4 position #2 position #2 position

Hip & Knee Implants Sports Medicine Advanced Wound Management

6

1

1

Our performance

7* Underlying growth percentage after adjusting for the effect of currency translation, acquisitions and disposals.

** 2020 net debt includes lease liabilities.

$4,560m -12.1%*

64.6¢

Revenue

Adjusted earnings per share (EPSA)

Trading cash conversion

Net debt

$683m 15.0% margin

37.5¢

Trading profit

Dividend per share

1020 10481123 1169

683

2016 2017 2018 2019 2020

82.694.5

100.9 102.2

64.6

2016 2017 2018 2019 2020

30.835.0 36.0 37.5 37.5

2016 2017 2018 2019 2020

15501281

1104

1600

1926

2016 2017 2018 2019 2020

75%

90% 85% 83%

101%

2016 2017 2018 2019 2020

101%

$1,926m**

46694765

4904

5138

4560

2016 2017 2018 2019 2020

First Quarter 2021

8

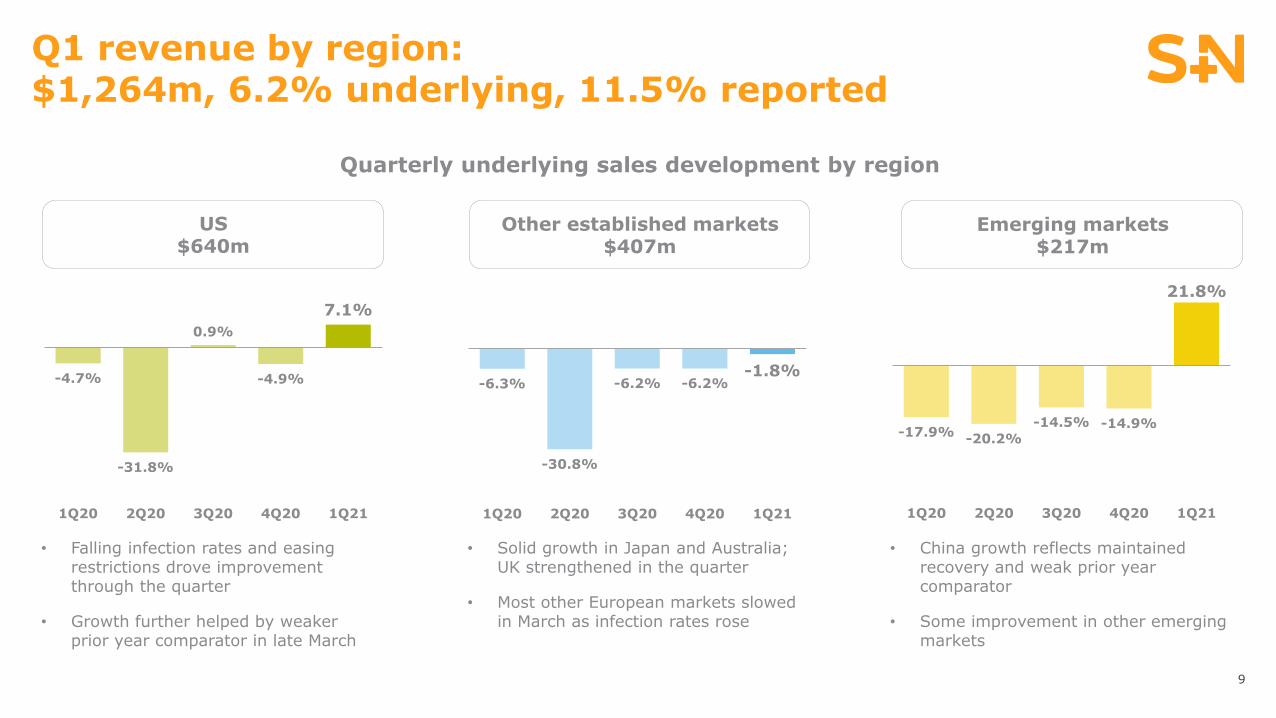

Q1 revenue by region: $1,264m, 6.2% underlying, 11.5% reported

9

US$640m

Other established markets$407m

Emerging markets$217m

• Falling infection rates and easing restrictions drove improvement through the quarter

• Growth further helped by weaker prior year comparator in late March

• Solid growth in Japan and Australia; UK strengthened in the quarter

• Most other European markets slowed in March as infection rates rose

• China growth reflects maintained recovery and weak prior year comparator

• Some improvement in other emerging markets

-4.7%

-31.8%

0.9%

-4.9%

7.1%

1Q20 2Q20 3Q20 4Q20 1Q21

-6.3%

-30.8%

-6.2% -6.2%-1.8%

1Q20 2Q20 3Q20 4Q20 1Q21

-17.9%-20.2%

-14.5% -14.9%

21.8%

1Q20 2Q20 3Q20 4Q20 1Q21

Quarterly underlying sales development by region

Q1 revenue: $1,264m, 6.2% underlying, 11.5% reported

10

Product franchise growth

Global

US

Other Established Markets

Emerging Markets

Revenue split

Geographical growth

US$640m

Other Established Markets

$407m

Emerging Markets$217m

21.8%

-1.8%

7.1%

6.2%

-3.2%

26.7%

4.5%

9.3%

-4.6%

11.7%

12.0%

10.4%

12.0%

17.7%

9.1%

-10.3%

1.6%

Arthroscopic Enabling Technologies

Orthopaedics

Hips

Knees

Advanced Wound Management

Advanced Wound Care

Advanced Wound Bioactives

Advanced Wound Devices

ENT

Sports Medicine & ENT

Trauma & Extremities

Other Recon

Sports Medicine Joint Repair

11

• Targeting underlying revenue growth of 10-13%

− Hips to continue to outperform Knees

− Sports Medicine & ENT to rebound strongly

− AWM momentum to continue

• Trading margin range of 18-19%

− COVID impact on gross margin; partial offset from efficiency programmes

− Dilution relative to 2019 from investment in R&D (c.100bps), initial dilution from completed M&A (c.150bps)

− FX headwind relative to 2019 (c.100bps)

• Tax rate on trading results in the range of 18-19%

• Targets assume improvement in conditions through the year,

with surgery volumes largely unconstrained by COVID in H2

2021 outlook

Priorities for 2021

12

Priorities for 2021 – Strategy and COVID

13

Return to top-line growth and recapture momentum

Drive further operational improvement

Continue to respond effectively to COVID

Priority for 2021: Return to top-line growth and recapture momentum

Clear strategy for growth

• New commercial model

• New commercial leadership

• Portfolio enhanced through M&A

Investment in innovation

• Step up in R&D investment

New Leadership Team

Maximising portfolio potential

• Driving higher return from portfolio and growing recent launches

• Continuing to drive commercial excellence across franchises

Delivering value of the acquired assets

• Driving synergistic growth in Trauma & Extremities, Joint Repair, ENT and Bioactives

• Adding further value-creating opportunities focused on high-growth segments

Launching expanded pipeline of innovation

• High cadence of product launches across the franchises

• Further increase in R&D investment

Foundations from 2018/9 Driving sustainable revenue growth

14

1

2

3

Growth strategy in action – Wound franchise example

15

Bioactives underlying growth by quarter (normalised)

Strategy

• Increased focus on key account management

• “Win big” with IDNs and national tenders

Process

• Rollout of new end-to-end launch excellence process

People

• Improved engagement and turnover with focus on talent development, mentoring and diversity • Co-selling of acquired Osiris products

successfully rolled out

• Preparing for new forms and geographical expansions

-20%

-10%

0%

10%

20%

Q1

2019

Q2

2019

Q3

2019

Q4

2019

Q1

2020

Q2

2020

Q3

2020

Q4

2020

Q1

2021

*

* Normalised for 2020/21 year-end shipment timing effects

Maximising portfolio potential1 Delivering value of the acquired assets2

Progress on key R&D projects

16

Orthopaedics

Sports Medicine & ENT

Advanced Wound Management

Recently launched growth drivers

Key 2021 projects*

OR3O◊ Dual mobility Porous Knee systemHip & Knee implants SYNC Modular Trays New Hip & Knee instruments Streamlined instrument set for THA and TKA

CORI◊ TKARI.HIP Navigation on CORI

Tissue balancing for robotic-assisted TKA

Robotics & digital surgery

CORI TensionerHip 7 Navigation on Kick

EVOS Large Frag/Periprosthetic Broadening EVOS trauma plate portfolioTrauma & Extremities Digital Taylor Spatial Frame

Capsular repair launches in Hip

Advanced Healing launches in Shoulder

INTELLIO◊ Connected Tower

FASTFIX◊ FLEX

DOUBLEFLO◊

Next generation meniscal repair

Arthroscopic tower fluid management

Sports Medicine Joint Repair

Arthroscopic Enabling Technologies

ENT

REGENETEN◊ Expansion Product and region expansion

TULA◊

HALO◊ WEREWOLF◊ ENT Wand

PICO PROTECT

Lyopreserved biotissue

Next generation single-use NPWT

Advanced Wound Bioactives

Advanced Wound Devices

GRAFIX◊, PL XC & PL CORE

STRAVIX◊, PL & MESHED

Lyopreserved biotissue

LEAF◊ 2.0

PICO◊ Region and Indication Expansion

Clinical Decision Support

Blue indicates products from recent acquisitions

Next generation Patient monitoring system

ARIA Home PT Remote physical therapy module

Porous offering for Knee portfolio

Navigation assisted Hip procedures

Increased efficiency in External fixation

*All innovation launches coming after completing relevant regulatory review, clearance and approval processes

Advanced Wound Care

✔

✔

✔

✔

✔ Denotes first regulatory clearance received

Launching expanded pipeline of innovation3

Demonstrated launch excellenceGrowth inflections from new products in recent years

17

3.9%

-5.4%

-28.9%

9.8%

4.4%

11.5%

Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021

OR3O launch Q4 2019

6%

8%

14.0%

Q1 2017 Q3 2017 Q1 2018 Q3 2018 Q1 2019 Q3 2019

-2%

-4%

-1.1%-2.1%

0.8%

5.1%

Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019

FLOW 90 launch Q2 2019

LENS 4K launch Q3 2019

REGENETEN acquired end 2017

US Hips growth vs peers Sports Medicine Joint Repair

quarterly growth

AET quarterly growth

PICO 7 sNPWT

PICO annual sales

2011 2013 2015 2017 2019

REGENETENBioinductive Implant

OR3O Dual Mobility

LENS 4KSurgical Imaging System

FLOW 90 Wand

Drive further operational improvementOperations transformation and process efficiencies

18

• Five year operations efficiency plan, with work started in late 2019

• Targeting c.$200m of annualised cost savings

• Restructuring costs of c.$350m in total, by end of 2023

Process efficiencies

• Simplify end-to-end processes

• Improve commercial execution and product launches

• Invest in IT and Digital solutions

Operations transformation

• Continuing manufacturing network optimisation

• Outsourcing of warehousing and distribution

• Process transformation, with Lean deployment and greater automation

Continue to respond effectively to COVID

19

• Flexible and updated working environments

• COVID secure sites with deployment of social distancing technology

• Control discretionary costs while COVID outbreak continues

• Support customers in person and remotely

• Transform medical education, with new online platform in 2021

Customers Employees Cost control

Appendices

20

Technical guidance for 2021

21

April 2021

Foreign exchange and acquisitions

Translational FX impact on revenue growth(1) 2.9%

Acquisition impact on revenue growth 1.9%

Non-trading items

Restructuring costs $140-150m

Acquisition and integration costs $35-45m

European Medical Device Regulation (MDR) compliance costs c. $60m

Other

Amortisation of acquisition intangibles $170-180m

Income from associates c. $10m

Net interest(2) $75-80m

Other finance costs c. $15m

Tax rate on trading result 18-19%

(1) Based on the foreign exchange rates prevailing on 23rd April 2021(2) Includes interest associated with IFRS 16 Leases

Franchise revenue analysis

2020 2021

Q1Growth

%

Q2Growth

%

Q3Growth

%

Q4Growth

%

Full YearGrowth

%

Q1Growth

%

Q1Revenue

$m

Orthopaedics (8.3) (34.0) (2.8) (10.2) (14.0) 1.6 540

Knee Implants (10.6) (46.9) (9.5) (16.2) (21.0) (10.3) 212

Hip Implants (8.6) (26.9) 7.1 (0.5) (7.4) 9.1 154

Other Reconstruction 19.4 (51.5) (3.1) (45.6) (26.1) 17.7 25

Trauma & Extremities (7.1) (11.1) (1.4) (1.3) (5.1) 12.0 149

Sports Medicine & ENT (9.5) (33.3) (4.5) (5.2) (13.0) 10.4 373

Sports Medicine Joint Repair (7.1) (32.0) (2.7) (0.3) (10.2) 12.0 198

Arthroscopic Enabling Technologies

(11.2) (32.1) (1.6) (5.0) (12.4) 11.7 146

ENT (15.2) (44.0) (24.8) (33.1) (29.7) (4.6) 29

Advanced Wound Management (4.0) (17.6) (6.1) (4.4) (8.1) 9.3 351

Advanced Wound Care (6.7) (14.6) (6.9) (2.1) (7.5) 4.5 175

Advanced Wound Bioactives (8.6) (18.7) (4.5) (9.9) (10.5) 26.7 116

Advanced Wound Devices 13.0 (23.7) (6.9) 0.2 (4.8) (3.2) 60

Total (7.6) (29.3) (4.2) (7.1) (12.1) 6.2 1,264

22All revenue growth rates are on an underlying basis and without adjustment for number of selling days.

Regional revenue analysis

23

2020 2021

Q1Growth

%

Q2Growth

%

Q3Growth

%

Q4Growth

%

Full YearGrowth

%

Q1Growth

%

Q1Revenue

$m

US (4.7) (31.8) 0.9 (4.9) (10.1) 7.1 640

Other Established Markets(1) (6.3) (30.8) (6.2) (6.2) (12.3) (1.8) 407

Established Markets (5.4) (31.4) (1.8) (5.4) (11.0) 3.4 1,047

Emerging Markets (17.9) (20.2) (14.5) (14.9) (16.8) 21.8 217

Total (7.6) (29.3) (4.2) (7.1) (12.1) 6.2 1,264

(1) Other Established Markets’ are Australia, Canada, Europe, Japan and New Zealand. All revenue growth rates are on an underlying basis and without adjustment for number of selling days

Q1 consolidated revenue analysis

24

Q12021

Q12020

Reportedgrowth

Underlying Growth

Acquisitions/disposals

Currency impact

Consolidated revenue by franchise $m $m % % % %

Orthopaedics 540 497 8.7 1.6 4.3 2.8

Knee Implants 212 230 (7.9) (10.3) - 2.4

Hip Implants 154 137 12.6 9.1 - 3.5

Other Reconstruction 25 21 21.0 17.7 - 3.3

Trauma & Extremities 149 109 36.3 12.0 21.7 2.6

Sports Medicine & ENT 373 328 13.7 10.4 - 3.3

Sports Medicine Joint Repair 198 172 15.2 12.0 - 3.2

Arthroscopic Enabling Technologies 146 126 15.5 11.7 - 3.8

ENT 29 30 (2.2) (4.6) - 2.4

Advanced Wound Management 351 309 13.6 9.3 - 4.3

Advanced Wound Care 175 158 10.5 4.5 - 6.0

Advanced Wound Bioactives 116 91 27.2 26.7 - 0.5

Advanced Wound Devices 60 60 1.3 (3.2) - 4.5

Total 1,264 1,134 11.5 6.2 1.9 3.4

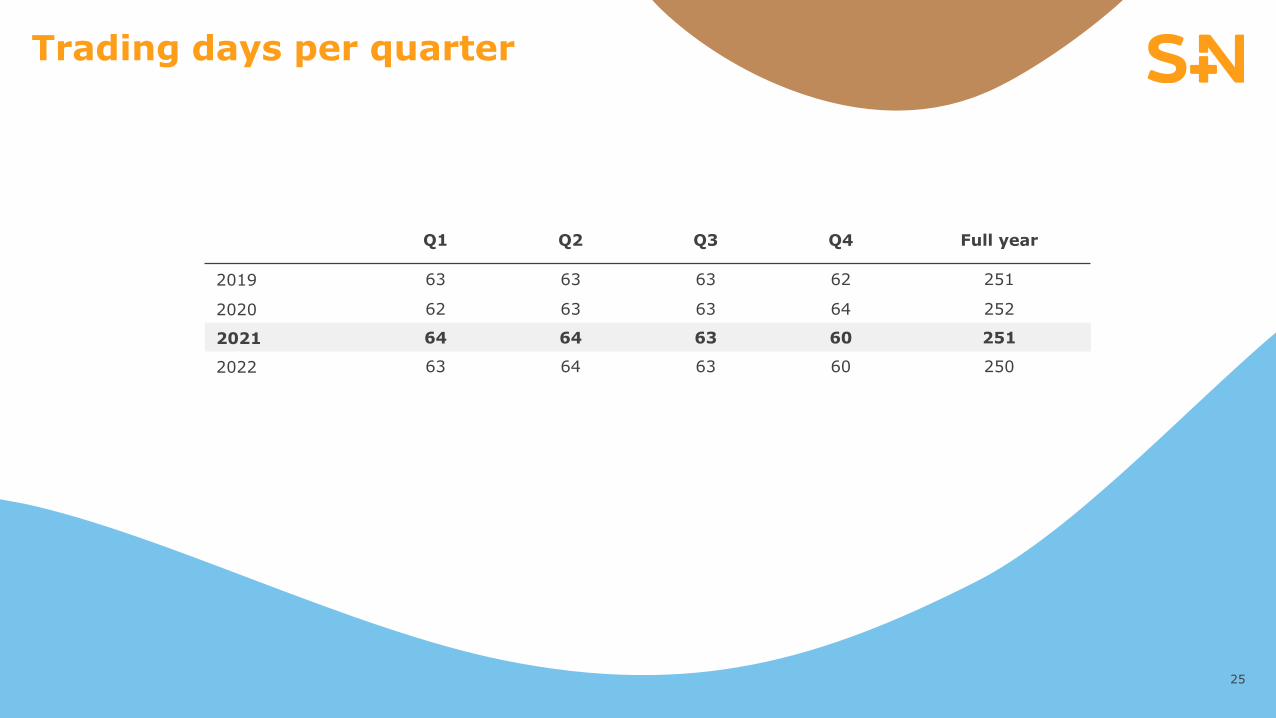

Trading days per quarter

25

Q1 Q2 Q3 Q4 Full year

2019 63 63 63 62 251

2020 62 63 63 64 252

2021 64 64 63 60 251

2022 63 64 63 60 250

Our sustainability strategy and 2020 highlights

8,000 hours of employee volunteering in the

communities in which we live and work.

Target: between 2020 and 2030, contribute 1 million

volunteer hours.

$4.7 million product donations to underserved

communities.

Target: between 2020 and 2030, donate $125 million in

products.

Eight Global Employee Inclusion Groups were

established. Our senior leaders and managers

were trained on inclusion.

Target: empower and promote the inclusion of all.

26

All sites in Memphis (US) began sourcing

renewable electricity, which consumes over 40%

of the Group’s electricity.

Target: achieve an 80% absolute reduction in total life

cycle greenhouse gas emissions by 2050, beginning by

implementing 100% renewable electricity plans at our

facilities in Memphis (US) and Malaysia, and at all of our

strategic manufacturing facilities by 2050.

1,853 tonnes: We sent 7% less waste to landfill

during 2020 compared to the previous year.

Target: achieve zero waste to landfill at our facilities in

Memphis (US) and Malaysia by 2050, and at all of our

strategic manufacturing facilities by 2030.

Started to develop our packaging reduction

roadmap, as well as our packaging sustainability

strategy.

Target: by 2025, incorporate at least 30% post-

consumer recycled content into all non-sterile packaging

materials, as well as incorporating packing materials

from sustainable sources for new packaging parts.

We have started risk mapping our supply chain.

Target: to complete the assessment of all suppliers by

2025, including subsequent tier levels, to assumer

compliance with our sustainability requirements.

Initiated sustainability reviews within New

Product Development.

Target: by 2022, include sustainability review in New

Product Development phase reviews for all new

products and product acquisitions.

PeopleCreating a lasting positive impact on our

communities

PlanetA medical technology business with a

positive impact

ProductsInnovating sustainably