Embed Size (px)

Citation preview

Wockhardt Limited

Investor MeetAugust 2012

Safe Harbor Statement

• Except for historical information contained herein, statements in this communication, which includewords or phrases such as “will”, “aim”, “will likely result”, “would”, “believe”, “may”, “expect”, “willcontinue”, “anticipate”, “estimate”, “intend”, “plan”, “contemplate”, “seek to”, “future”, “objective”,“goal”, “likely”, “project”, “should”, “potential”, “will pursue” and similar expressions or variations ofsuch expressions may constitute “forward looking statements”. These forward looking statementsinvolve a number of risks, uncertainties and other factors that could cause actual results to differmaterially from those suggested by the forward looking statements. These risks and uncertaintiesinclude, but are not limited to our ability to successfully implement our strategy, our growth andexpansion plans, obtain regulatory approvals, our provisioning policies, technological changes,investment and business income, cash flow projections, our exposure to market risks as well as otherrisks. Wockhardt Limited does not undertake any obligation to update forward looking statements toreflect events or circumstances after the date thereof.

Investor Meet Aug 2012 2

Business Highlights

Dr. Murtaza KhorakiwalaManaging Director – Wockhardt Limited

August 2012

Key Questions

1. Do we have a Sustainable Business Model2. Q1 Results & Peer Positioning3. Will we deliver Consistent Profits

Investor Meet Aug 2012 26

Sustainable Business Model

Investor Meet Aug 2012 27

WOCKHARDT

Research

GlobalisationOperational Excellence

Sustainable Business Model

Investor Meet Aug 2012 28

WOCKHARDT

Research

GlobalisationOperational Excellence

Research

Generics

• Blockbuster• Niche• Complex Technology

Biosimilars• Insulins• MABs

New Chemical Entity

• Anti Infectives

Investor Meet Aug 2012 29

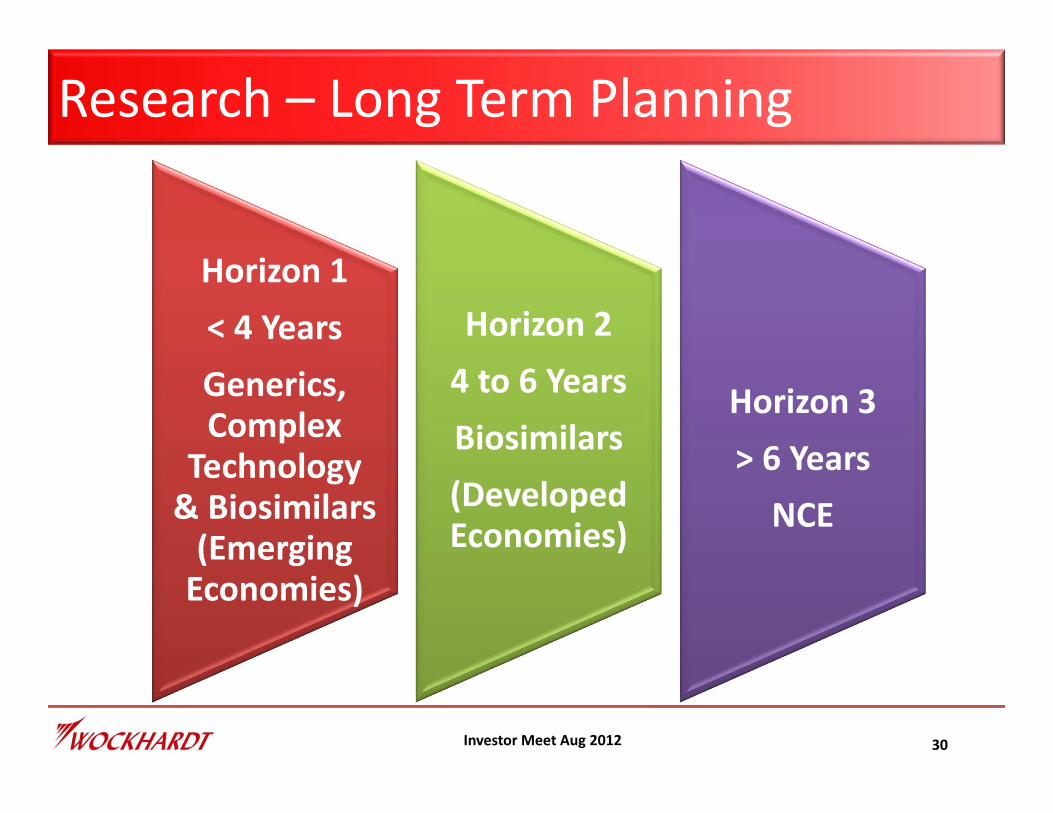

Research – Long Term Planning

Investor Meet Aug 2012 30

Horizon 1< 4 YearsGenerics, Complex

Technology & Biosimilars(Emerging Economies)

Horizon 24 to 6 YearsBiosimilars(Developed Economies)

Horizon 3> 6 YearsNCE

Complex Products Focused Research

458Products sold in USA & Europe manufactured in India, USA, UK & Ireland

164Global Patents granted globally. 1585 patents filed

578Scientists developing innovative and technologically advanced medicines

33US ANDAs pending approval

Investor Meet Aug 2012 31

3 R&D Centers Worldwide

Won Patent Awards 3 Years in a row

Recent Product Launches

Investor Meet Aug 2012 32

US6 – FY12PantoprazoleDonepezilVenlafaxineFluticasoneLevofloxacinClarithromycin

6 – FY12PantoprazoleDonepezilVenlafaxineFluticasoneLevofloxacinClarithromycin

4 – FY13 (till date)LEC

ValacyclovirLansoprazole OTCFexofenadine OTC

4 – FY13 (till date)LEC

ValacyclovirLansoprazole OTCFexofenadine OTC

UK7 – FY12Alendronic Acid

Mycophenolate MofetilRemifentanil Powder Inj

OxycodoneAdenosine Soln Inj

DonepezilClarithromycin

7 – FY12Alendronic Acid

Mycophenolate MofetilRemifentanil Powder Inj

OxycodoneAdenosine Soln Inj

DonepezilClarithromycin

3 – FY13 (till date)AtorvastatinLosartanRopinarole

3 – FY13 (till date)AtorvastatinLosartanRopinarole

OthersFY12

13 – Ireland24 – India

FY1213 – Ireland24 – India

FY13 (till date)4 ‐ Ireland6 ‐ India

FY13 (till date)4 ‐ Ireland6 ‐ India

Product Approvals Since 1 April ‘12

Investor Meet Aug 2012 33

US

6 – Till DateLansoprazole OTC

Clopidogrel BisulphateAlfuzosin

EntacaponeFelodipine

Ziprasidone (TA)

UK

2 – Till DateAtorvastatinLevetiracetam

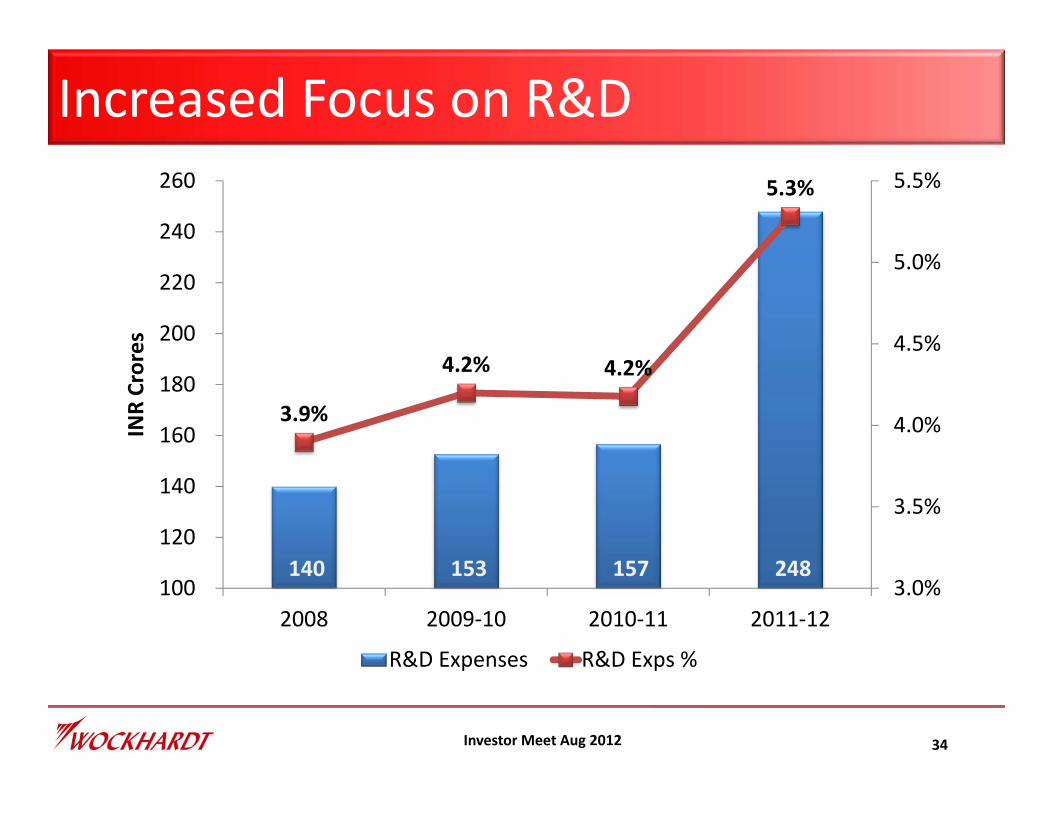

Increased Focus on R&D

Investor Meet Aug 2012 34

140 153 157 248

3.9%

4.2% 4.2%

5.3%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

100

120

140

160

180

200

220

240

260

2008 2009‐10 2010‐11 2011‐12

INR Crores

R&D Expenses R&D Exps %

Sustainable Business Model

Investor Meet Aug 2012 35

WOCKHARDT

Research

GlobalisationOperational Excellence

Global Operations

Investor Meet Aug 2012 36

RoW operationsWockhardt Direct operations

USA

UK, Ireland,France, Switz.

India

Mexico

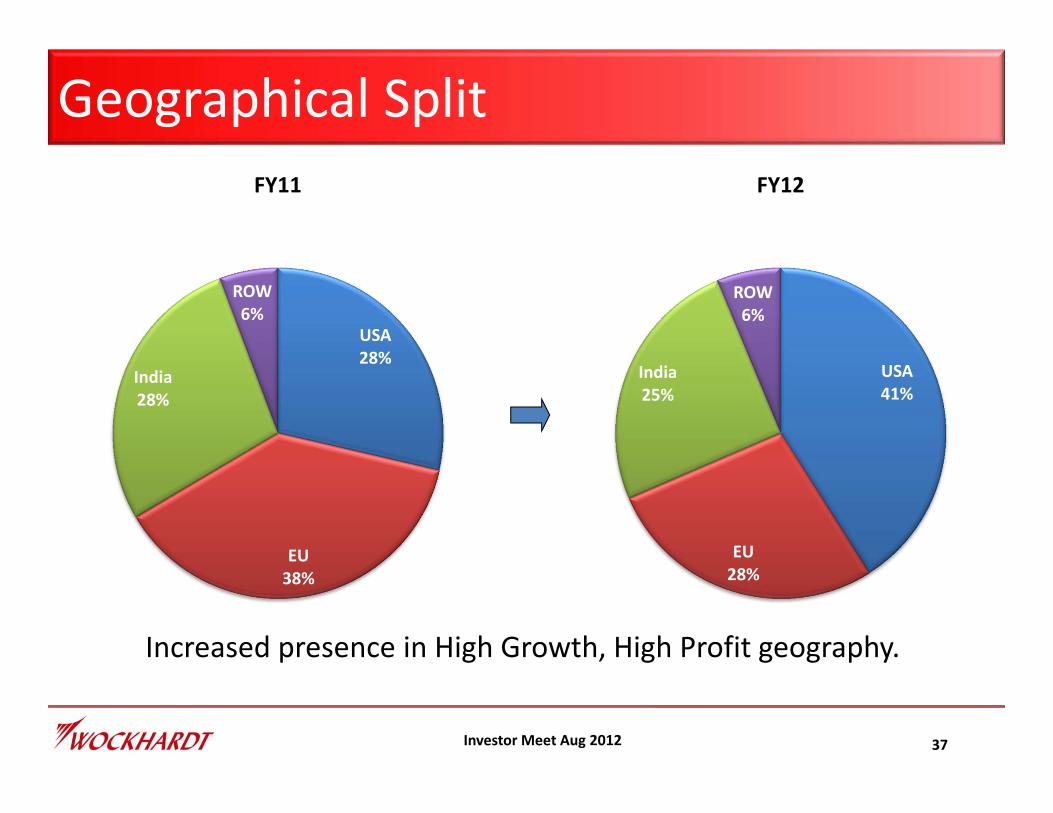

Geographical Split

37Investor Meet Aug 2012

USA28%

EU38%

India28%

ROW6%

FY11

USA41%

EU28%

India25%

ROW6%

FY12

Increased presence in High Growth, High Profit geography.

US Business: Profitable Growth

Investor Meet Aug 2012 38

• Growth of 78% YOY

• 6 New Products launched in

FY12

• 6 Approvals received in FY13 &

4 launched

• Improved Market Share

position in key products

• Surge in the Injectable

business

• Launch of AG version of

Stalevo® - LEC

$144m

$211m

$375m

$ values at convenience translation rate of Rs.50.83

EU Operations: Strong UK OperationsUK Operations

• Strong UK operations growth by

13% against a depressed market

growth

• UK business rank No. 3 in

overall Generic space and No. 2

in UK hospital business

• 7 new products launched in

FY12 and 3 in Q1 FY13

including Atorvastatin

Investor Meet Aug 2012 39

669

758

600

640

680

720

760

800

FY11 FY12

Rs.cr.

UK

£ 82m

£ 92m

£ values at convenience translation rate of Rs.81.44

EU Operations: Ireland & France

Investor Meet Aug 2012 40

Ireland Operations

• Continues to be No. 1 branded generic

company in Ireland with 30% market share

• Launched 13 products in FY 12 and 4 in

YTD FY13 including Atorvastatin

France Operations

• De-growth of 52% due to

genericization of its key drug

• Restructured the operations

– Reduced operating costs by ~70%

– Reduced employees from 497 to 63

472

229

0

100

200

300

400

500

FY11 FY12

Rs.cr.

France

194 183

0

50

100

150

200

250

FY11 FY12

Rs.cr.

Ireland

€ 28.6m € 27.0m

€ 70m

€ 34m

€ values at convenience translation rate of Rs.67.90

India & RoW Operations• Indian Branded Business grew

at 16% in FY12 compared to

15% market Growth.

• 7 Brands among top 300

Industry brands

• Strong pan India field force of

over 3000 employees

• 3rd rank in Indian Pain

management market.

• RoW operations grew by 36% in

FY12

Investor Meet Aug 2012 41

Sustainable Business Model

Investor Meet Aug 2012 42

WOCKHARDT

Research

GlobalisationOperational Excellence

Fit & Trim Operations

Gross Margins at 64% in FY12 vs. 63% in FY08

Operating Expenses at32% in FY12 vs.40% in FY08

Investor Meet Aug 2012 43

EBITDA Margins at 31% in FY12 vs. 18% in FY10

Manufacturing Cost (‐29%)

Investor Meet Aug 2012 44

100117

136

164

8470 71

‐

100

200

2008 2009‐10 2010‐11 2011‐12

Base

Relative No. of Units Relative Cost per unit

People Productivity (+27%)

632 588 542 589

17.6%16.2%

14.5%

12.8%

6%

9%

12%

15%

18%

400

450

500

550

600

650

2008 2009‐10 2010‐11 2011‐12

INR Crore

Employee Cost Employee Cost as % of Sales

Investor Meet Aug 2012 45

Working Capital (Improved by 26%)

1160 916 882 1106

32.3%

25.2%23.5% 24.0%

15%

18%

21%

24%

27%

30%

33%

36%

400

500

600

700

800

900

1000

1100

1200

2008 2009‐10 2010‐11 2011‐12

INR Crore

Working Capital Working Capital as % of Sales

Investor Meet Aug 2012 46

* Working Capital measured as on the last Working Day of the respective Year

Q1 Results

Sales – Growth of 35% over Q1FY12

1,053 1,111 1,209 1,241 1,426600

750

900

1,050

1,200

1,350

1,500

Jun‐11 Sep‐11 Dec‐11 Mar‐12 Jun‐12

Sales

Investor Meet Aug 2012 48

Growth of 35% over Q1FY12

5th Consecutive Quarter of Sequential Growth

EBITDA – Growth of 61% over Q1FY12

312 323 376 429 502

29.5% 29.1%

31.1%

34.6% 35.2%

20%

22%

24%

26%

28%

30%

32%

34%

36%

200

300

400

500

600

Jun‐11 Sep‐11 Dec‐11 Mar‐12 Jun‐12

EBITDA & EBITDA Margins

EBITDA EBITDA Margin

Investor Meet Aug 2012 49

Growth of 61% over Q1FY12

10th Consecutive Quarter of Sequential Growth

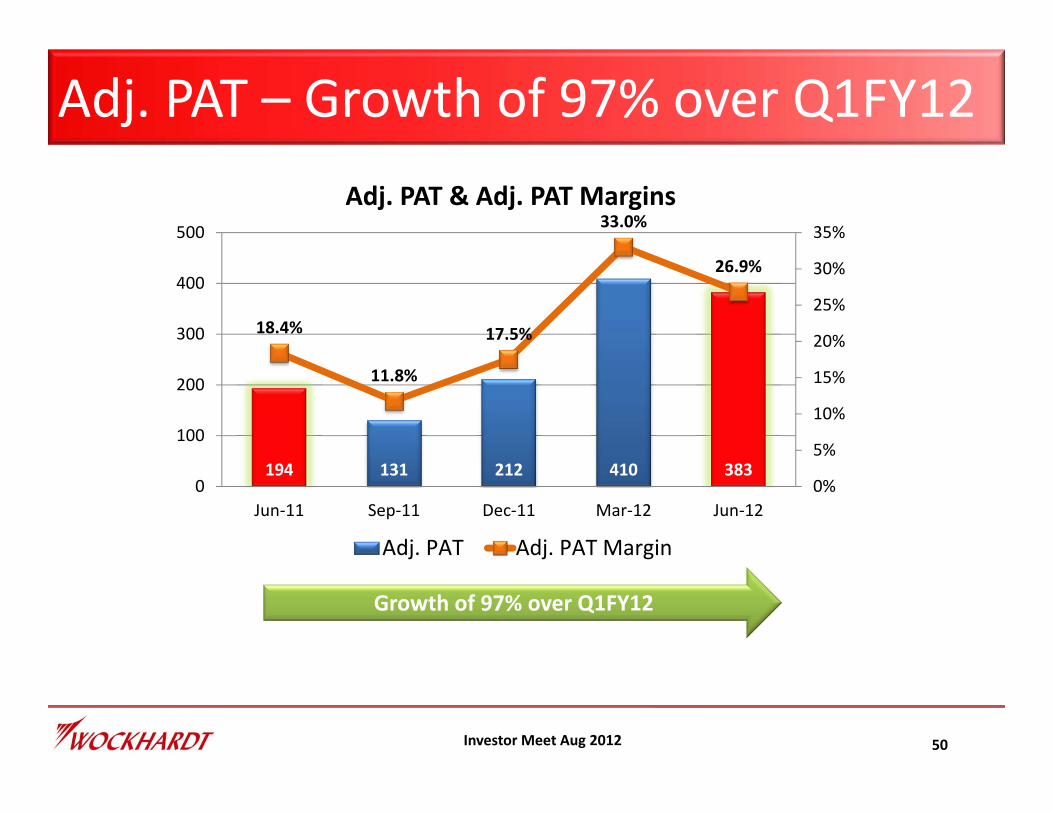

Adj. PAT – Growth of 97% over Q1FY12

194 131 212 410 383

18.4%

11.8%

17.5%

33.0%

26.9%

0%

5%

10%

15%

20%

25%

30%

35%

0

100

200

300

400

500

Jun‐11 Sep‐11 Dec‐11 Mar‐12 Jun‐12

Adj. PAT & Adj. PAT Margins

Adj. PAT Adj. PAT Margin

Investor Meet Aug 2012 50

Growth of 97% over Q1FY12

Peer Positioning

Peer Positioning – Q1FY13

Investor Meet Aug 2012 52

SALES – No. 6

2,683 2,541

2,254

2,012

1,594

1,426

1,041

‐

500

1,000

1,500

2,000

2,500

3,000

Sun Pharma Dr Reddys Lupin Cipla Cadila Healthcare Wockhardt Glenmark

563

502 499

458

345

165

100

150

200

250

300

350

400

450

500

550

600

Sun Pharma Cipla Wockhardt Dr Reddys Lupin Cadila Healthcare Glenmark

Peer Positioning – Q1FY13

Investor Meet Aug 2012 53

EBITDA3rd Highest in Industry

1242 Top 3

Peer Positioning – Q1FY13

Investor Meet Aug 2012 54

EBITDA Margins2nd Highest in Industry

35.2%

28.0%

21.7%20.3% 19.7%

15.9%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Sun Pharma Wockhardt Cipla Cadila Healthcare Lupin Dr Reddys Glenmark

Top 346.3%

401 378

336

280

195

78

‐

50

100

150

200

250

300

350

400

450

500

Sun Pharma Cipla Wockhardt Dr Reddys Lupin Cadila Healthcare Glenmark

Peer Positioning – Q1FY13

Investor Meet Aug 2012 55

PAT3rd Highest in Industry

796 Top 3

Peer Positioning – Q1FY13

Investor Meet Aug 2012 56

PAT Margins2nd Highest in Industry

30%

27%

20%

13%12% 12%

8%

5%

10%

15%

20%

25%

30%

Sun Pharma Wockhardt Cipla Dr Reddys Lupin Cadila Healthcare Glenmark

Top 3

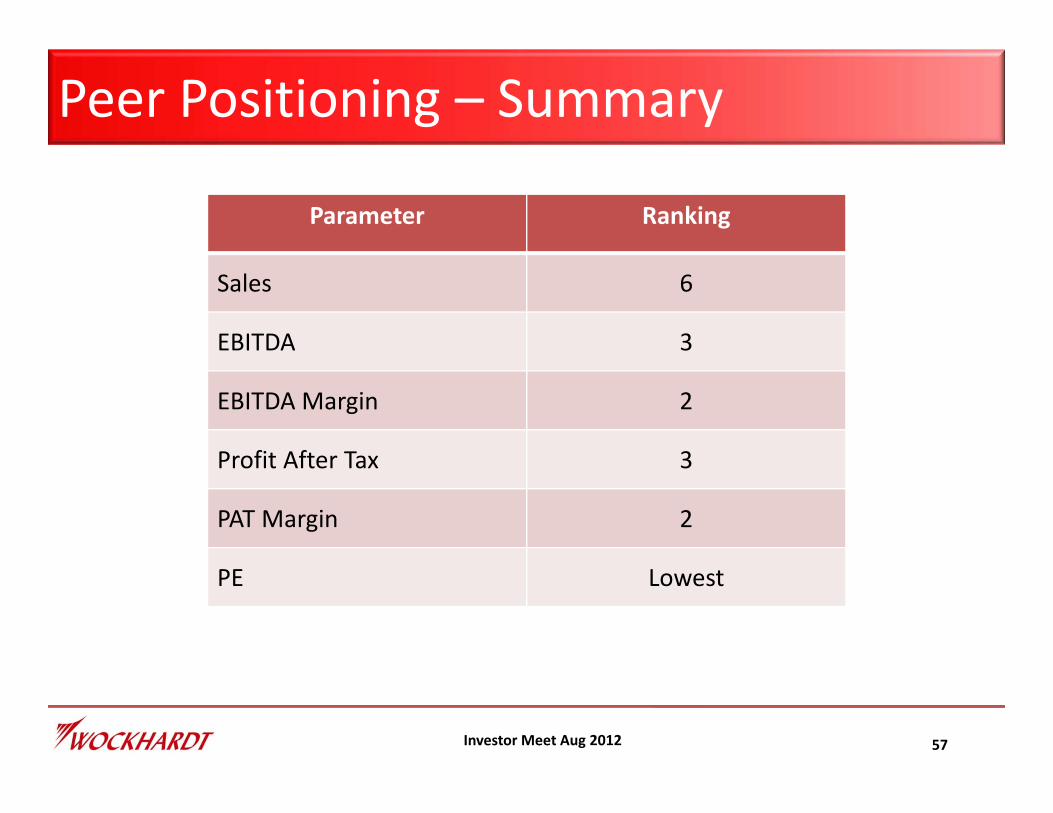

Peer Positioning – Summary

Investor Meet Aug 2012 57

Parameter Ranking

Sales 6

EBITDA 3

EBITDA Margin 2

Profit After Tax 3

PAT Margin 2

PE Lowest

Peer Positioning

Investor Meet Aug 2012 58

Courtesy : Mint

Consistent Profitable Growth

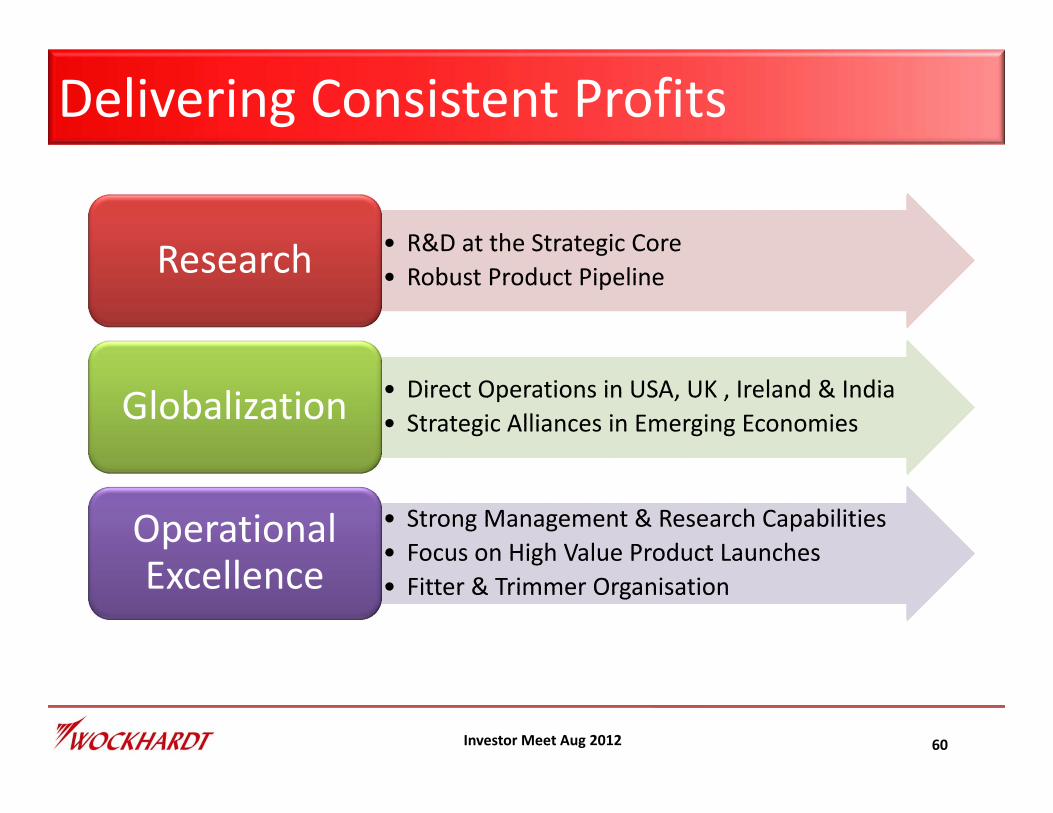

Delivering Consistent Profits

Investor Meet Aug 2012 60

• R&D at the Strategic Core• Robust Product Pipeline• R&D at the Strategic Core• Robust Product PipelineResearch

• Direct Operations in USA, UK , Ireland & India• Strategic Alliances in Emerging Economies• Direct Operations in USA, UK , Ireland & India• Strategic Alliances in Emerging EconomiesGlobalization

• Strong Management & Research Capabilities• Focus on High Value Product Launches• Fitter & Trimmer Organisation

• Strong Management & Research Capabilities• Focus on High Value Product Launches• Fitter & Trimmer Organisation

Operational Excellence

Summary

Summary: A Sustainable Business Model

Focused strategy on driving growth in key markets: US, UK and India

Investor Meet Aug 2012 62

Summary: A Sustainable Business Model

Focus on core operations

Investor Meet Aug 2012 63

Summary: A Sustainable Business Model

Sustained Profitability Growth

Investor Meet Aug 2012 64

Summary: A Sustainable Business Model

Robust Research & Development Program

Investor Meet Aug 2012 65

Summary: A Sustainable Business Model

Strong Manufacturing Capabilities

Investor Meet Aug 2012 66

Summary: A Sustainable Business Model

Highly Competent Leadership at the helm

Investor Meet Aug 2012 67

Summary: A Sustainable Business Model

Wockhardt Associate Ownership Mindset

Investor Meet Aug 2012 68

Investor Meet Aug 2012 69

“A man is but the product of his thoughts. What he thinks, he becomes”

Mahatma Gandhi

![Investor Meet [Company Update]](https://img.dokumen.tips/doc/110x75/577c7a6b1a28abe054951eb5/investor-meet-company-update.jpg)

![Investor Meet Presentation [Company Update]](https://img.dokumen.tips/doc/110x75/577cb48b1a28aba7118c80c9/investor-meet-presentation-company-update.jpg)