Embed Size (px)

Citation preview

1

Investor Day

THURSDAY, JUNE 9, 2016

JOHN MACDONALD PRESIDENT & CEO

Forward-Looking Statements

3

This presentation contains forward-looking information within the meaning of applicable Canadian securities laws (“forward-looking statements”). Statements other than statements of historical fact

contained in this presentation may be forward-looking statements, including, without limitation, management’s expectations, intentions and beliefs concerning anticipated future events, results,

circumstances, economic performance or expectations with respect to Enercare Inc. (“Enercare”), including Enercare’s business operations, business strategy and financial condition. Forward-looking

statements may include words such as “anticipates”, “believes”, “budgets”, “could”, “estimates”, “expects”, “goal”, “intends”, “may”, “outlook”, “plans”, “strive”, “target” and “will”, although not all forward-

looking statements contains these words.

Some of the specific forward-looking statements in this presentation include, but are not limited to, statements with respect to the following:

• Enercare’s strategic priorities, including future product rollouts, geographic expansion and customer initiatives and the impact on Enercare’s business of the implementation of those strategic

initiatives;

• accretion or other financial enhancements anticipated to arise as a result of the acquisition of SEHAC Holdings Corporation (“Service Experts”) (the “Service Experts Acquisition”) and the impact on

Enercare’s business of the Acquisition;

• Enercare’s growth initiatives in Home Services and Sub-Metering;

• Enercare’s estimated 2016 Canadian income taxes, prospective U.S. tax efficiencies and initiatives and the estimated tax savings from those efficiencies and initiatives; and

• Enercare’s 2016 target capital expenditures, target range of IRR from those expenditures and sources of capital.

These forward-looking statements may reflect the internal projections, expectations, future growth, results of operations, performance, business prospects and opportunities of Enercare and are based on

information currently available to Enercare and/or assumptions that Enercare believes are reasonable. Actual results and developments may differ materially from results and developments discussed in

the forward-looking statements, as they are subject to a number of risks and uncertainties. In developing these forward-looking statements, certain material assumptions were made. These forward-looking

statements are also subject to certain risks. These factors include, but are not limited to:

• actual future market conditions being different than anticipated by management; and

• the failure to realize the anticipated benefits of the Acquisition, strategic initiatives and tax efficiencies.

Material factors or assumptions that were applied to drawing a conclusion or making an estimate set out in forward-looking statements regarding Enercare’s strategic priorities, growth initiatives and the

Acquisition include:

• the view of management regarding current and anticipated market conditions;

• industry trends remaining unchanged;

• the financial and operating attributes of Enercare and Service Experts as at the date hereof and the anticipated future performance of Enercare and Service Experts;

• assumptions regarding foreign exchange rates, income tax rates and commodity prices;

• the extent to which the Service Experts Acquisition is accretive, which may be impacted by the realization and timing of synergies and the operating performance of Enercare and Service Experts;

• assumptions regarding the volume and mix of business activities remaining consistent with current trends;

• assumptions regarding non-recurring transaction costs estimated to be incurred by Enercare in connection with the Service Experts acquisition; assumptions regarding future selling, general and

administration costs estimated to be incurred by Enercare, including in connection with the running of Service Experts; and

• the number of common shares outstanding and remaining constant.

Material factors or assumptions that were applied to drawing a conclusion or making an estimate set out in forward-looking statements regarding income taxes in 2016 and U.S. efficiencies are found on

the slides titled “Understanding our 2016 Canadian Income Taxes” and “Pursuing Prospective U.S. Tax Efficiencies”.

Material factors or assumptions that were applied to drawing a conclusion or making an estimate set out in forward-looking statements regarding capital expenditures in 2016, target IRR ranges and

sources of capital are found on the slide titled “Self-Funding Our Significant Growth in 2016”.

Readers are cautioned that this list of material factors or assumptions is not exhaustive. Although forward-looking statements contained in this presentation are based upon what management believes are

reasonable assumptions, there can be no assurance that actual results will be consistent with these forward-looking statements. Accordingly, readers should not place undue reliance on such forward-

looking statements and assumptions as management cannot provide assurance that actual results or developments will be realized or, even if substantially realized, that they will have the expected

consequences to, or effects on, Enercare. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current

expectations, including the matters discussed in Enercare’s most recently filed Management’s Discussion and Analysis and in its current Annual Information Form. These forward-looking statements are

subject to change as a result of new information, future events or other circumstances in which case they will only be updated by Enercare where required by law. These forward looking statements speak

as of the date of this presentation.

VISION To be the premier provider of essential

home and commercial services and energy

solutions in North America

5

Evolution of Enercare 1950s - 1999

1999 - 2002

2002 - 2011

2011 - 2015

2015 -

HOME SERVICES

• WATER HEATER

• FINANCIAL

INTEREST

• WATER HEATER SERVICE

• CUSTOMER RELATIONSHIPS

• PROTECTION PLAN & HVAC SALES

2016

2014

6

OHCS: Transformational and Accretive

(1) See “Non-IFRS Financial and Performance Measures” found in Enercare’s MD&A dated May 12, 2016.

(2) Normalized Distributable Cash and Normalized Distributable Cash per common share exclude transaction costs and synergies, and have been normalized by

$19 million in 2015 to account for timing differences in taxes paid related to the acquisition of Direct Energy’s Ontario Home and Small Commercial Services

business (“OHCS”). Gives effect to the 2014 bought deal offering, excluding the over-allotment option.

INTEGRATED

• New brand platform

• New products

• New geographies

TRANSFORMED

• IT

• Culture

• Employees

ACHIEVED • Enhanced service

• Strong organic growth

• Acquisitions

31%

2015 Normalized

Distributable Cash per

common share(1)(2)

7

Service

Experts

Service Experts: A Scalable North American Platform

(1) See “Non-IFRS Financial and Performance Measures” found in Enercare’s MD&A dated May 12, 2016.

(2) Normalized Pro Forma Distributable Cash per common share exclude transaction costs and synergies and have been normalized by $19 million in 2015 and 2016 to

account for timing differences in taxes paid related to the acquisition of Direct Energy’s Ontario Home and Small Commercial Services business (“OHCS”). Gives effect

to the 2016 bought deal offering, excluding the over-allotment option.

2016 Normalized Pro

Forma Distributable Cash per common

share(1)(2)

25%

Enercare Customer Locations Service Experts Locations EENA Commercial National Accounts

8

Evolution of Sub-metering

2008 2010 2012 2013 2014 2015 2016

Acquisition

of

Stratacon

Inc.

Acquisition

of Enbridge

Electric

Connections

Launched

Water

Metering

Product

Acquisition of

Triacta Power

Technologies

Inc.

Launched

Thermal

Metering

Product

Launched

Gas

Metering

Product

Enercare Connections is the largest

private sub-metering company in Canada

9

Listening to Our Investors and Analysts

Based on our preliminary analysis, we believe

we can achieve cost synergies of approximately

5 to 8 cents per share by the end of 2017

Growth Strategy &

Drivers of

Growth

Visibility Aspirational Goals &

Guidance

Synergies Service Experts

Acquisition

10

Enercare S&P/TSX Total Return Index S&P/TSX Small Cap Total Return Index

332

74

112

5-Year Total Return

235

91 115

3-Year Total Return

116

87 92

1-Year Total Return

179

85 101

2-Year Total Return

Return on $100 Investment Over Respective Time Periods

$100

Enercare’s 5-year return is in the top 10% of the

S&P TSX Composite Index

Top TSX Performer

11

$0.65 $0.66 $0.67 $0.68 $0.70 $0.73 $0.84 $0.92

Enercare’s Annualized Dividend per Common Share

+2% +2%

+2%

+2%

+4%

+16%

+42% since 2011

Paid out more than $250(1) million in dividends to our

shareholders since 2011

Returning Significant Capital to Shareholders

+10%

(1) Dividends paid from January 2011 until May 31, 2016.

12

Today’s Agenda

14:00 Welcome & Introductory Remarks John Macdonald, President and CEO

14:15 Sub-metering John Piercy, SVP & General Manager

Kevin Neild, Director Revenue Assurance & Customer Operations

14:45 Home Services Jenine Krause, Chief Operating Officer

15:15 Brand Marketing Lorne Solway, Chief Marketing Officer

15:30 BREAK

15:45 Service Experts Scott Boxer, Chief Executive Officer

16:30 Financial Overview Evelyn Sutherland, Chief Financial Officer

13

14 14

THURSDAY, JUNE 9, 2016

KEVIN NEILD Director Revenue Assurance

& Customer Operations

16

Sub-metering: Gaining Momentum

1. Rising electricity prices drive awareness & demand for sub-metering

2. A growing number of regulatory regimes mandate or support utility sub-metering, which drives significant change in consumption behaviour

3. Compelling business case for property managers & owners – enhancing value of real estate assets

Utility sub-metering is the implementation of a system that

allows a landlord, property developer, firm, condominium association,

homeowners association, or other multi-occupant property to bill

occupants for individual measured utility usage

17

Sub-metering Demand Driven by Rising Electricity Prices

7.5 7.9

8.8 9.1

10.1

11

12.1

6.5 6.8

7.5 7.8

8.6

9.4

10.3

2010 2011 2012 2013 2014 2015 2016

Higher Tier Lower Tier

~8.3 % CAGR tiered

price increase

During the same period CPI had a CAGR of 1.5%, and

Ontario Rent increases had a CAGR of 2.4%

Historical Tiered Rates per Kwh (cents)

18

1.1 TWh/year in electricity savings by full

deployment* or the equivalent of 94,848

homes’ electricity use for 1 year(3)

158 MW – Summer Peak Demand Reduction

by full deployment* or the equivalent to 1,500

average cars(4)

Significant Conservation Benefit & Change in Behaviour(1)

Tenants who pay for their

own electricity consume

40% less on average

What is the conservation potential if Ontario were to introduce sub-

metering for all multi-residential/bulk metered residential properties?

(1) Evaluation of the impact of Sub-metering on Multi-residential Electricity Consumption and the Potential Economic and Environmental

Impact on Ontario prepared by Navigant Consulting Ltd. For Enercare dated January 8, 2016

(2) Based on five year rollout, as per Navigant Report in 2016.

(3) According to the US Environmental Protection Agency’s Greenhouse Gas Equivalencies Calculator

(4) 1 HP = 0.746 kW, so 158 MW is equal to approximately 210,000 HP. An average car (Toyota Corolla for example) has an estimated

engine power of 140 HP and 158 MW gas equivalent power to 1,500 Toyota Corollas.

This is 5 times the net annual savings

of the province’s entire 2014 Consumer

Initiatives Portfolio for conservation(2)

19

Enercare

Individual

Meter

Readings

Bulk

Utility

Line

Sub-metering provides a compelling value proposition

for our clients: cost reductions and energy

conservation benefits

Compelling Business Case - Retrofit

20

Long-Tail Business with Long Duration Contracts Chart Is For Illustrative Purposes Only. Based On An Assumed ‘Typical’ Building*

$(150,000)

$(100,000)

$(50,000)

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

YR1 YR2 YR3 YR4 YR5 YR6 YR7 YR8 YR9 YR10 YR11 YR12 YR13 YR14 YR15 YR16 YR17 YR18

$ C

DN

ECI’s Capital Investment in Meter Hardware & Installation

Net

Revenue

Average length of sub-metering

contract is 18 years

* New Construction 120 units, Net Revenue fee of $20/unit, Capital Cost $800/unit. 18-year average contract life

5.7-Year

Payback

Cash flow Capital

Retest and reseal the meters

Annual Cash flow

21

Integrated Product & Services Offering

Electrical 84.0%

Water 11.7%

Thermal 4.1%

Gas 0.2%

Contracted Units by Service Type – Q1 2016

Solution Includes: financing, hardware, installations, billing

services, customer care & regulatory upkeep

Ontario 94.8%

Alberta 5.0%

Saskachewan 0.2%

Geographies Served Q1 2016

22

Integrated Net Revenues Add to EBITDA Growth

Multi-commodity invoices provide

higher EBITDA / invoice

$19

$17

$14

$12

Electricity Thermal Gas Water

Retrofit New Construction

*Weighted Average, Net Revenue billed/service in May 2016.

Net Revenues*

23

Attractive Market Size and Existing Base (as of Q1 2016)

46% 213,422 54%

New Construction Units Total Number of

Contracted Units

Retrofit Units

Estimated unmetered

units remaining in Ontario**

Estimated units

constructed in Ontario*

*CMHC Housing Market Outlook Ontario Edition, Q2 2016: ~40,000 additional units to be added per year in both 2016 and 2017

** Based on Enercare’s building database using known buildings with estimated number of units (as at Q1 2016)

Sub-metering Services Business Model

24

93

132

156 166

185

205

213

77

94

115

136

151 155 159

50 57

71 82

96 103

107

2010 2011 2012 2013 2014 2015 Q1 2016

Contracted Installed Billing

Unit Continuity (In thousands) 17% CAGR

15% CAGR

16% CAGR

Strong embedded revenues in contracted

units pipeline: 2 to 1 versus billing units

Achieving Scale in Sub-metering

25

A+

Accredited Business

eBilling

34% penetration

OESP

Working Committee

Record Performance in 2015

15% Sub-metering

Revenue

89% Sub-metering

EBITDA

Strong Business Results & Operational Excellence

JOHN PIERCY SVP & General Manager

Sub-metering

27

Contracted

services

growth

Billable

unit

conversion

New

products

New

markets

Economies

of scale

Growth Drivers

Setting Ourselves Apart From the Competition

28

Integrated Design,

Installation & Operations

High Quality Standards

On-time Installations

Regulatory Experts

In-House

Exceptional Customer

Care

Multi-commodity Offerings

Investment Grade Public

Company

Industry Leadership

29

Offering a “Whole Building” Solution

ELECTRIC

THERMAL

GAS WATER

4 Services

4 Admin Fees

1 Bill

30

• Geoexchange

• Geographic Expansion

• Retrofit

• New Construction

• Multi Commodities

Growth Drivers

Drive penetration in existing segments . . . Enter new growth markets

Common infrastructure, including sales,

installations, billing, customer care and servicing

Residential

• Commercial Installations

• Meter Data Management

Triacta Meter Sales

• Canada

• United States

Commercial

31

Sales 20%

Technical 39% Billing

17%

Care 24%

Sub-Metering Employees (excluding Triacta)

Strong Customer Oriented & Technical Organization

Organized to capitalize on

growth opportunities

(100,000)

(75,000)

(50,000)

(25,000)

-

25,000

50,000

75,000

100,000

0

20

40

60

80

100

120

140

160

2013 2014 2015

FTEs Adjusted EBITDA per FTE

Adjusted EBITDA per FTE

$56,238

$86,348

$112,420

32

Strategic Acquisition of Triacta

• Enercare was Triacta’s largest customer

• Triacta has the most advanced

multi-residential sub-metering technology

• Acquisition reduced Enercare’s capital

cost and secured our supply chain

• Allows us to invest in technology that

give us new technical features

• Provides entry point into other geographies

• Creates opportunities for product expansion

33

Leading The Pack

Direct

internet

connectivity

Multi-protocol

out of the box

10-year

seal

period

Software

configurable

Regulatory

approvals for

billing

Direct

factory

support

Triacta’s Competitive Advantages

34

Currently OEM for global

electrical hardware suppliers

Installed in 11 countries & 30 states

and provinces in North America

Growth opportunity in U.S.

as regulations drive demand

New generation meters to be

developed in 2016

Technology Leadership & Growing Market Potential

Triacta PowerHawk Metering System

Home Services THURSDAY, JUNE 9, 2016

37

JENINE KRAUSE Chief Operating Officer

Home Service

Our Platform

39

Employees

Home Services Franchisees

~800 ~450

Service Coverage

Footprint Locations

92% of Ontario 6 Offices

Channels

Franchisees Dealers Contractors

7 36 45

40

Flexible Multi-Channel Operating Model

Maximizes Geographic Coverage

• Operating primarily in GTA,

Southwestern Ontario,

Niagara and Ottawa

• Residential and

commercial customers;

retrofit and new build

• Certified technicians

• Strong sales expertise

• Strong focus on safety

• Operating in GTA, and

Ottawa under long-term

contracts

• Fully branded Enercare

• Residential customers

• Receive royalty on sales

• Access to sales and

technical training and

support

• Must meet Enercare

service, quality and safety

standards

• Established local service

providers in smaller

markets

• Co-branded with Enercare

• Residential customers

• Sales incentives, install

and service fees

• Marketing support provided

• Access to sales and

technical training and

support

• Must meet Enercare

service, quality and safety

standards

Corporate Franchisee Dealers

41

Successfully Completed Integration of OHCS* Acquisition

IT Integration

Customer Operations

Employee

Service

Delivery

New

Products

Enhanced

Service

Offerings

Strong Organic

Growth

Transformed

Achieved Growth

Integrated

Launched several new

products

Rolled-out new service

metrics

Logistics roll out

Employee engagement

Re-established

relationship with the union

Repatriated call centres to

Canada

IT integration

Accelerated rentals

Attrition improvement

Dealer growth

* OHCS refers to the acquisition of Direct Energy’s Ontario Home and Small Commercial Services business.

42

Winning & Growing: Where We Are Today

Strong financial results

Exceptional customer

service

Winning in a competitive

market

Growing products &

services across Ontario

43

Protecting our Business

2002- Present

1M customers billed by Enbridge,

mitigates credit risk as we are entitled

to receive payment in 21 days for

99.51% of cases

2009-Present

Customer education programs

2010-Present

The Buyout Contract: 68% of net book

value is protected by a buyout contract

January 1, 2014

Enhancements to the

Open Bill Access Program

April 1, 2015

Bill 55-The Stronger Protection

for Ontario Consumers Act

44

Rental Units Provide Base for Cross Selling

1.1 Million

Rental Units

Two-thirds of HVAC

units are from protection plan

relationships

543,000

Protection Plans

Other

Products

Opportunity to cross-sell

other products including

plumbing and duct cleaning

4,391

HVAC Units

Installed

Cross-selling

is a key driver of

Enercare’s future

growth

80% of protection plan

customers are cross sold

from the water heater

relationship

Large water heater and

HVAC rental unit base

provides significant

platform for cross-selling

Cross-selling to increase lifetime

value of a customer

45

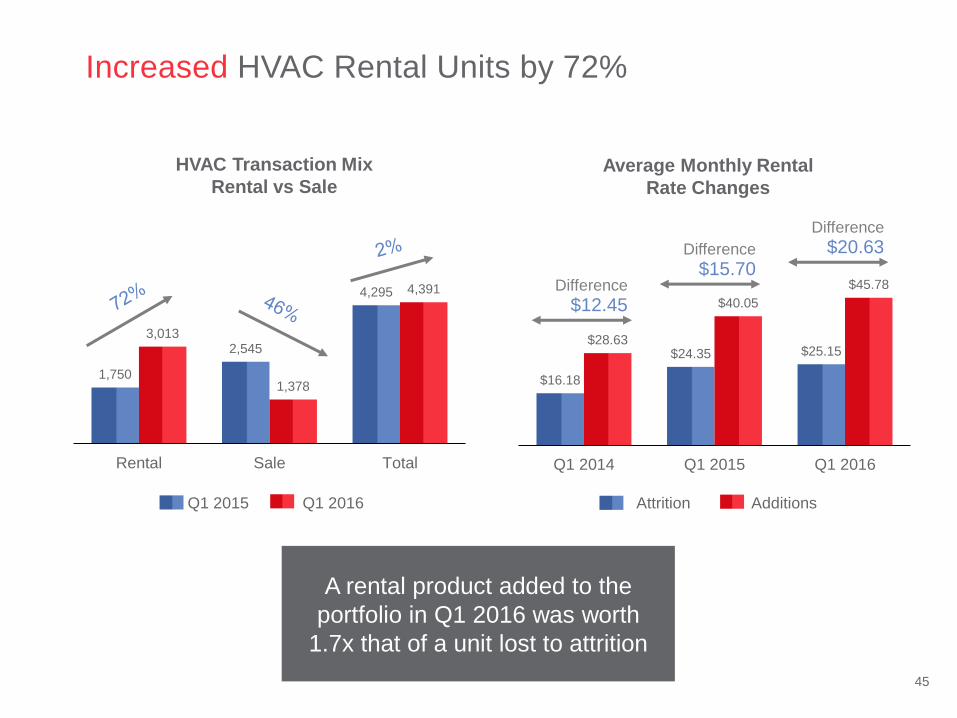

Increased HVAC Rental Units by 72%

1,750

2,545

4,295

3,013

1,378

4,391

Rental Sale Total

HVAC Transaction Mix

Rental vs Sale

Q1 2016 Q1 2015

$16.18

$24.35 $25.15 $28.63

$40.05

$45.78

Q1 2014 Q1 2015 Q1 2016

Average Monthly Rental

Rate Changes

Additions Attrition

Difference

$12.45

Difference

$15.70

Difference

$20.63

A rental product added to the

portfolio in Q1 2016 was worth

1.7x that of a unit lost to attrition

46

6% 7% 3% 4%

44% 33%

44%

46%

3%

3% 7%

2007 2015

Rental Portfolio Revenue

Increasing Rental Units Margin and Value

Other

Tankless

CV

HVAC

Electric

Product

Gross

Margin $

(excluding other

products

category)

Home Services

revenue is gradually

shifting to higher

margin products

Highest Margin

Lowest Margin

PV

47

The long-term EBITDA

impact of an HVAC rental unit

is ~2.5x that of the short-term

EBITDA on an outright sale

11%

25%

53%

69%

89%

75%

47%

31%

2013 2014 2015 Q1 2016

Split Between HVAC Rentals & Sales

Rentals Sales

Rationale for renting vs. owning

• Peace of mind

• No upfront costs

• Predictable monthly payments

• Preventative maintenance every 1-2 years

• Repairs, parts and labour included

• Priority service

HVAC Evolution: Rental vs. Out Right Sale

48

Long-Term Benefits of Growing HVAC Rental Base

2015 2016 2017 2018 2019 2020 2021 2022 2023

Illustrative Example Only*

of CAGR of HVAC Revenue Assuming 10,000 new units per annum at $80 per month

*This is an illustrative example only and not a forecast.

HVAC rental unit strategy is expected

to provide significant compounded annual growth

over the long-term

($Millions) 2015 2016 2017 2018 2019 2020 2021 2022 2023 Total

Revenue 10 20 30 40 50 60 70 80 90 450

Capital Outlay 50 50 50 50 50 50 50 50 50 450

49

High Return Products

Water Heaters

2015 Capital IRR

$64M* 16% - 21%

HVAC

2015 Capital IRR

$33M* 13% - 20%

*Water heater capex includes new customers and exchange while HVAC capex includes only new customers

50

Revenue per Contract

Focusing on Higher Margin Protection Plans

Q1 2016 Protection Plan Unit Continuity

14,000

Additions

16,000

Attrition

543,000

Contracts

Upselling to HVAC and higher value

products is a key element

of our protection plan strategy

2,000

HVAC Sales

& Rentals

Jan to April

2015

Jan to April

2016

51

Delivering Excellent Customer Service:

A Cornerstone of Customer Loyalty

Delivering Excellent Service

• Focusing on the metrics that matter

• Requesting immediate customer feedback

• Investing in technology for technicians and agents

• Measuring every front line customer facing employee

2014 2015 Q1 2016

Source: Enercare Net Promoter Score Database, April 2016

Improvements in Net Promoter Scores

52

Best Advice

• Understand what

the customers

needs

• Recommend the

right solution for

the customer

• Provide advice on

how the customer

can save money by

maximizing

efficiency

• Safe Installation

aligned with safety

standards

• Ongoing product

maintenance

• Recommend

additional products

as needed

Excellent Service Delivery

Best Technicians

Products Service, Quality & Breadth

Customer

Requirements

Energy

Efficiency Safety

Additional

Products

Best advice is the key to get more of our

products in our customers homes

53

Customer Acquisition Through Channel Investment

Sales expansion to new channels will extend our

reach of products and services in the marketplace

18% Alternate channels will

continue to grow

• Inbound

• Field Cross-sell

• Outbound

• Online & Digital

82% Traditional channels generate

the majority of sales

• Inbound

• Field

• Builder

Traditional Channels Alternate Channels

54

What’s Next

3+ Years

Geographic & Product Growth

Expand customer base

through dealer strategy

Continue growth across Canada,

launch new products that complement

existing services

Whole Home

Grow Rental Continuity

Become trusted service advisor,

deliver multi-product value offering

and increase our share of the household

Innovation

Mobile application launch Lead in connected home; leverage strengths in

service delivery to build customer value

2017 2016

55

• Support our

existing

business

• Build on our

strengths in

heating, cooling

and plumbing

• Continue to

build value in

the whole

home offer

Excellent Service Delivery

Best Technicians

Products Service, Quality & Breadth

Untapped Opportunity: Dealer Expansion & Product Growth

Footprint Expansion

New Product Introduction

56

Pursuing Whole Home

Connected Home Hub

(coming soon)

Furnace or Boiler

Water Heater

Plumbing Air

Quality

Duct

Cleaning

Air

Conditioning

Electrical

(coming soon)

Water Treatment

57

Innovation: Connected Home

Marketing THURSDAY, JUNE 9, 2016

LORNE SOLWAY Chief Marketing Officer

61

Brand Video

62

BRAND PROMISE

BRAND POSITIONING

BRAND STRATEGY

BRAND VISION

Building Our Brand Platform

IS NOW

66

Rebranding Objectives

67

Extensive Rebranding

68

<1% Nov 2014

20% Nov 2015

Dramatically Increased Consumer Awareness

Source: Vision Critical Brand Tracking Study (Wave 2), November 2015

69

43

31 35

28 29

18

Enercare’s Customer Ratings Are Higher

Than Its Key Competitors

Positive Brand Perception

HVAC Water Heaters

Enercare Brand A Brand B Enercare Brand A Brand B

Source: Vision Critical Brand Tracking Study (Wave 2), Nov 2015 70

71

2014 2015 Q1 2016

Rising Net Promoter Scores

Source: Enercare NPS Database, Apr 2016

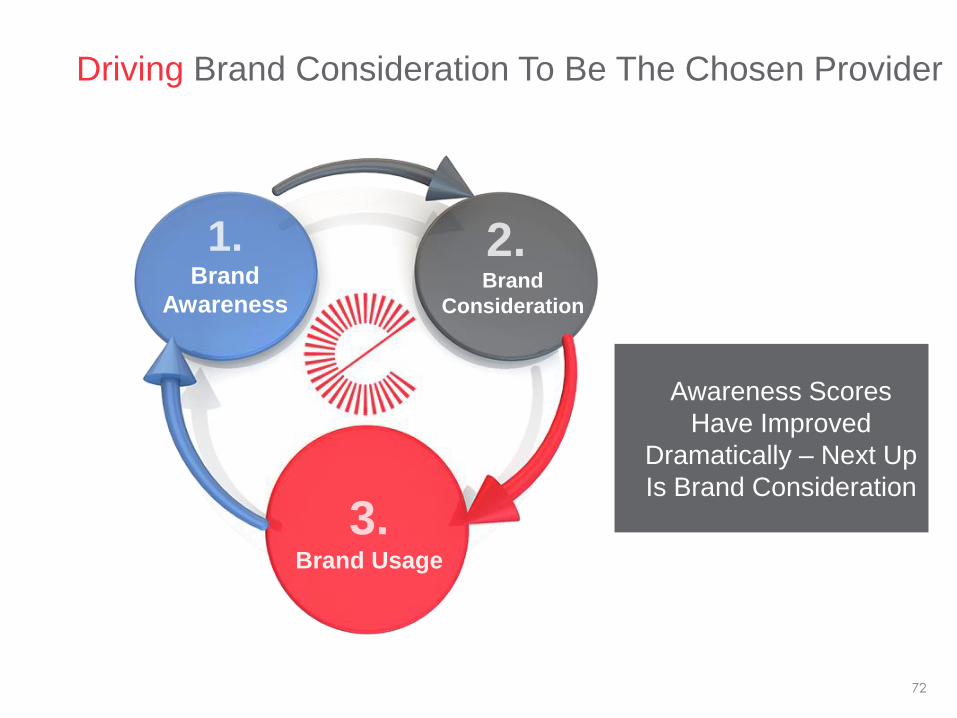

Awareness Scores

Have Improved

Dramatically – Next Up

Is Brand Consideration

2. Brand

Consideration

1. Brand

Awareness

3. Brand Usage

Driving Brand Consideration To Be The Chosen Provider

72

Knowing What Our Customers Want

Easy To Do

Business With

1 Get appointment quickly

2 Fix problem on first visit

3 24/7 Service

4 Emergency after-hours

calls

5 Resolve issue

A Company

I Can Trust

Care About

Its Customers

1 Safe & proper equipment install

2 Reputable professional service

3 Honest in all dealings

4 Stand behind product/services

5 Fair prices

1 Not left without HVAC service

2 Explains work being done

3 Extends equipment life vs sell

4 Offers helpful advice

5 Respects my home

Easy, Trust & Care

underpin our efforts to increase NPS and drive sales

73

Should we outline each of these boxes

74

Creative

Platform

Evolution

New

Cause

Platform

Deeper

Segmentation

&

CRM

Digital

Enablement

Strengthen Our Brand, Build Awareness & Drive Sales

Humanizing our Brand

75

76

Launching our Fresh Start Program

77

Do It For Me Stability Seekers Energy Efficiency

Relevant offers, content and communications drive

higher response rates and return on investment

The Future: Deeper Segmentation & CRM

78

Leading an Industry Transformation

79

Customer Mobile App – Fast & Easy Appointment Scheduling

Driving Sales & Lowering Costs Through Technology

80

Additional Enhancements To Further Drive Sales

82

Service Experts

THURSDAY, JUNE 9, 2016

SCOTT J. BOXER Chief Executive Officer

Service Experts LLC

84

79%

15%

4% 2%

Residential Service,Maintenance & Replacement

Commercial Service,Maintenance & Replacement

ResidentialNew Construction

CommercialNew Construction

SERVICE

REPLACEMENT

2015 Revenue Mix

Leading Provider of HVAC Services

In 2015, Service Experts had more than 645,000 customer

appointments and over 215,000 maintenance plans, serving

over 2,000 homes and businesses each day

85

Residential Service & Replacement Commercial Service & Replacement

81% US $291

11% US $40

7% US $23

1% US $5

SERVICE

79% US $342

15% US $67

4% US $16

2% US $7

Growth Strategy is Paying Off

Strong revenue growth

underlie Service Experts’ attractive free cash flow

2015 Revenue Mix(1)

(US$ millions)

(1) Revenue mix percentages have been normalized to exclude discontinued operations.

Residential New Construction Commercial New Construction

2012 Revenue Mix(1)

(US$ millions)

Total Revenue = US$359 million Total Revenue = US$432 million

7% CAGR

Constant Currency

SERVICE

REPLACEMENT REPLACEMENT

86

Complimentary & Scalable North American Platform

90 locations across US and Canada

29 states and 3 Canadian provinces

41 centers in top 100 MSAs (US)

Locations in 4 of the top Canadian cities

2,800 employees (94% in field)

Enercare Customer Locations

Service Experts Locations

EENA Commercial National Accounts

87

Focused Evolution of Service Experts

2016 2013 2004-5 2000 1996

Lennox Combines

Service Experts and Lennox Retail

(100+125 = 225)

American Capital Acquires

Service Experts from Lennox

(96)

A roll-up of HVAC contractors with strong local

brands across the U.S. and Canada

Enercare Acquires

Service Experts

(90)

Refocus to Service

and Replacement

(125)

Roll-up of U.S.

Contractors

(IPO’d with 12)

88

2010 2011 2012 2013 2014 2015

Revenue (US$ millions)

Dramatic 3-Year Turnaround

Adjusted EBITDA

(US$ millions)

$40

-$40 2010 2011 2012 2013 2014 2015

$500

$300

89

Loss of Accountability Restored Accountability at All Levels

What Happened: 2010-2012

Accumulation of Poor Decisions

• Created a top heavy structure

– field area centralization

– eliminated local P&Ls

– eliminated local GMs

• Corporate driven strategies vs. field

• Eliminated local brands

• Disruption of sales incentive plan

– variable to fixed/variable commission

– talent defection

What Did We Do: 2013 to Present

Made Significant & Permanent Changes

• A flattened structure

– eliminated 80+ field area managers

– restored local P&Ls

– brought back local GMs

• Field support philosophy

• Restored local legacy names (50+ years)

• Restored 100% commissioned sales

• Industry-leading supply agreements

• Strong executive management team

Making The Turnaround Happen

New executive management team brought in

to steer major turnaround

90 [ 90 ]

Steadily Increasing Customer Satisfaction Ratings

Structural

Reorganization

Branding Shift

Customer Satisfaction Ratings (based on ~50K surveys per year)

Service Experts’ customer satisfaction

ratings are at record high levels

2013 New executive

management team

91

Recessionary

Period

HVAC Industry Overview*

• U.S. Market ~ US$82 billion with 3.4% growth 2015-2020 / replacement growth > 6%

• Positive macro factors: confidence, unemployment, housing activity and green regulations

• Possible deraillers: political uncertainty, inflation and weather

105

110

115

120

125

130

135

140

2000 2002 2004 2006 2008 2011 2013 2015

Release of

pent-up

demand

Catch-up on Deferred Replacement

(Pent-up Demand)

Replacement Cycle from Mid-2000

Housing Boom

~9.2 million

homes added

from 2003 to 2007

Growing Housing Stock . . . With Benefit of Significant Pent-Up Demand

3%

4%

5%

6%

7%

8%

9%

10%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

% Installed Base Replaced Avg % Replaced

Favourable Outlook for Large & Growing U.S. Market

* Source: Public filings, Company websites, management estimates

IBISWorld Industry Report 23822a Heating & Air-Conditioning Contractors in the U.S. – November 2015

In m

illio

ns

92 Source: Public filings, Company websites, management estimates

IBISWorld Industry Report 23822a Heating & Air-Conditioning Contractors in the U.S. – November 2015

Fragmented and Competitive Landscape

U.S. Canada Regional & Local

Various Regional &

Local Operations

Company-

Owned

Company-

Owned Franchise Franchise

Company-

Owned Company-owned

Revenue:

~$400M

Revenue:

~$700M

Revenue:

~$200M Revenue: n/a

Revenue:

~$500M Revenue: up to $100M

90 locations 70 locations 187 locations 211 locations 19 locations 100,000+ locations

Co-branding National/

Co-branding

Mixed

Branding

Mixed

Branding

National

Branding Local branding

Minimal non-

HVAC services

offered

Plumbing Plumbing

Electric

Plumbing

Electric

Re-model

Home

Protection

Various other non-HVAC

services offered

Service Experts’

Main

Competition

93

Long-Term Business Model Built on Trust

Equipment

Sales

Ancillary

Sales/

Services

Demand

Service

Inspection

& Tune-up

Services

SERVICE

PLANS

50%

50% 50%

50%

75% 75%

94

Expanding through acquisition and

investment

Acquire

strategic

actionable

assets

Expand

service

offerings

Let’s Talk Growth

Search engine optimization (SEO)

Increase average ticket of customer base

Increase outbound marketing effort

Expand National Accounts sales strategy

Executing our core business model to

drive organic growth

95

Driving Engagement Through Effective SEO Marketing

Website Redesign: Primary Goals

Improve user experience

Responsive design

Automated, local website

Robust SEO strategy: traffic to site

Drive online reviews

Key Metric 2015 Change

%

Total Center Visits +104%

Organic Center Visits (SEO) +35%

Center Online Appointments +124%

Non-Center Appointments (.com/.ca) +37%

Online Chat - NEW n/a

Calls from Websites +62%

Google search:

75% of key words on page one

96

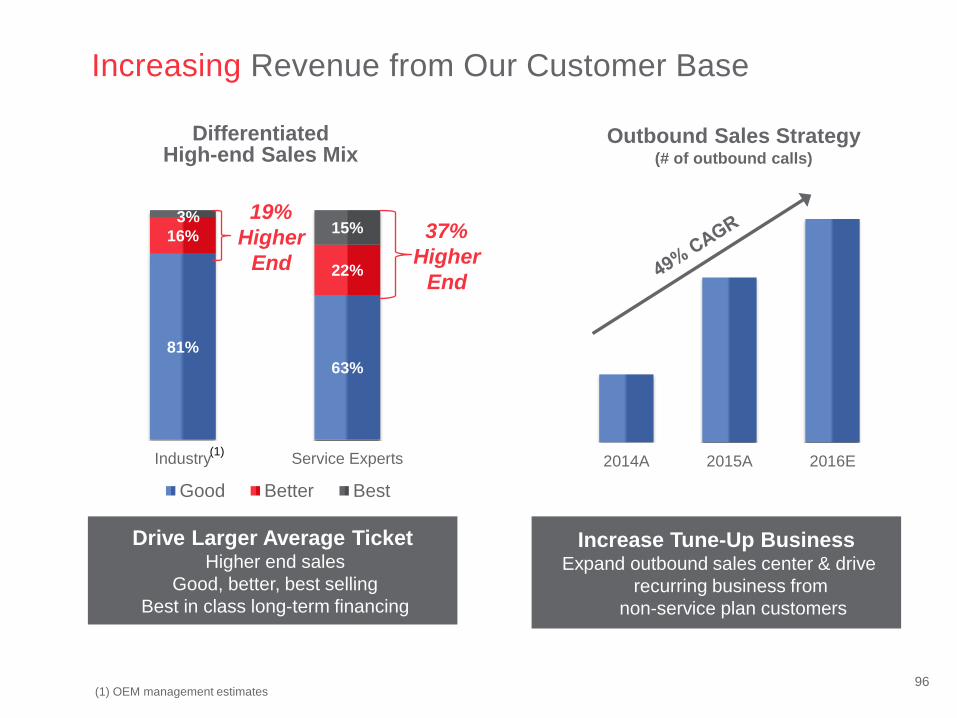

2014A 2015A 2016E

81%

63%

16%

22%

3% 15%

Industry Service Experts

Good Better Best

37%

Higher

End

19%

Higher

End

Increasing Revenue from Our Customer Base

(1) OEM management estimates

(1)

Differentiated High-end Sales Mix

Drive Larger Average Ticket Higher end sales

Good, better, best selling

Best in class long-term financing

Increase Tune-Up Business Expand outbound sales center & drive

recurring business from

non-service plan customers

Outbound Sales Strategy (# of outbound calls)

97

Double-Digit Revenue Growth in National Accounts

Overview

Acquired Engineering Excellence

National Accounts in 2014

Support retail commercial sites in all

50 States, Puerto Rico and Canada

through 750 contractors/self-perform (with

our own technicians)

Growth Initiatives

Penetrate existing accounts:

Top 9 accounts over 17,000 opportunities

Service new accounts

Convert to self-perform

– 5 States to 12

– more attractive to customers

Planned change out of rooftop units

Customer A ~ 60 500

Customer B ~ 200 1,500

Customer C ~ 250 1,400

Customer D ~ 300 500

Customer E ~ 200 2,000

Customer F ~ 150 3,000

Customer G ~ 50 300

Customer H ~ 150 600

Customer I ~ 50 9,000

Total ~ 1,400 ~ 19,000

Client # of Locations

Under Contract

Total Locations

(Approximate)

98

Typical Profile of Acquisition Current Pipeline

Many M&A Opportunities in Highly Fragmented Industry

Highly Fragmented Industry

with Actionable Opportunities

1. Tuck-ins (1 – 2013, 5 – 2014, 3 – 2015)

2. New geographies (1 – 2015)

3. National Accounts Services (1 – 2014)

All HVAC/Plumbing (Service/Replacement)

25-45 Years 10+ Years in Business

All Strong Brand/Reputations

US$10-$40 Million > US$5 Million Revenue

Up to 17K Agreements Strong Service Agreement Base

99

Expanding Our Service Offering

Provides labor

coverage to

complement

manufacturer

parts coverage

Cross-sell

plumbing to

existing customer

base

Training

technicians &

sales consultants

to be holistic

house expert

Large,

underserved

segment in U.S.

Creating options

ULTIMATE LABOR

PROTECTION

PLAN

PLUMBING

HOME

PERFORMANCE

CONTRACTING

RENTAL

MODEL

Significant opportunity to leverage

existing customer base

100

• UBER-like Customer Interactions

• On Time – Right Tech – Right Parts

• Mobile Workforce Optimization

• Eliminate Non-Value Add Functions

– Visibility of Parts Availability

– Automate Back Office Functions

• Enhance Business Intelligence

– Customer + Equipment + History

Focused on Advancing Technology

to Drive Future Sales & Lower Costs

Operational

Efficiency

Transforming

Customer Experience

101

1.1 Million Rentals

545,000 Repair &

Maintenance

Plans

19,000 HVAC Units

Installed

Related

Products &

Services Plumbing

Duct Cleaning

Indoor Air Quality

Energy Audits

700,000 Customer

Appointments

Untapped Value and Organic Growth Potential(1)

(1) Operating statistics for year ended December 31, 2015

215,000+

Maintenance

Plans

645,000

Customer

Appointments

Related

Products &

Services Plumbing

Duct Cleaning

Indoor Air Quality

Energy Audits

33,000 HVAC Units

Installed

Future Rentals

Roll-out schedule for HVAC rental units

Canada – 2016

United States – 2017

103

Financial Overview

THURSDAY, JUNE 9, 2016

EVELYN SUTHERLAND CFO

105

158 165 162 169 183

235

272

2010 2011 2012 2013 2014 2015 PF2015

207 255 276 299

363

564

1,119

2010 2011 2012 2013 2014 2015 PF2015

Total Revenue C$ millions

Acquisition Adjusted EBITDA(1)

C$ millions

Outstanding Growth

(1) See “Non-IFRS Financial and Performance Measures” in Enercare’s MD&A dated May 12, 2016.

(2) Refer to Enercare’s prospectus dated March 22, 2016 for detailed calculations.

(2) (2)

106

188 187 186 189

242

426

2010 2011 2012 2013 2014 2015

Major Catalysts for Future Growth

1 HVAC rentals

2 Improved customer retention

3 New products

4 New geographies

5 Tuck-in acquisitions

First full year with OHCS*

Growth and Evolution of Home Services

Home Services

Revenue C$ millions

* OHCS refers to the acquisition of Direct Energy’s Ontario Home and Small Commercial Services business..

107

$104 $107

Q1 2015 Q1 2016

Home Services Revenue (C$ millions)

~$9.2

+2%

+11%

$9.2 deferral

of revenue in

Q1 2016 due

to HVAC

rental

initiative

Successfully Growing Long-Term Recurring Revenues

The long-term EBITDA* impact of an

HVAC rental unit is ~2.5x that of the

short-term gain on an outright sale

* See “Non-IFRS Financial and Performance Measures” in Enercare’s MD&A dated May 12, 2016.

11%

25%

53%

69%

89%

75%

47%

31%

2013 2014 2015 Q1 2016

Split Between HVAC Rentals & Sales

Rentals Sales

108

Major Catalysts for Future Growth

1 Contracted unit growth

2 Billable unit conversion

3 Operating leverage

4 New products and services

6

15 18 19

22

31

2010 2011 2012 2013 2014 2015

Building Out Sub-metering

Sub-metering

Net Revenue* C$ millions

*Net revenue is a Non-IFRS measure and is calculated using revenue less commodity flow through charges.

109

Understanding Our 2016 Canadian Income Taxes

Deferral of partnership

income

OHCS(1) partial

tax year

Standard current taxes

Original estimate for 2016 Canadian

incomes taxes: C$46-C$53M(2)

(1) OHCS refers to the acquisition of Direct Energy’s Ontario Home and Small Commercial Services business.

(2) Tax guidance is expected to be updated in conjunction with our Q2 2016 earnings release in August 2016, to reflect the acquisition of Service Experts.

110

Pursuing Prospective U.S. Tax Efficiencies

C$26M-$33M

of Annual

Deductions

338 Election(1)

• Allows for full tax basis on US purchase price

• Estimated value of US$65 million on a net present value basis

• Creates approximately C$24-$28 million of tax shield in the US for 15 years

Transfer Pricing(2)

• Providing for the reimbursement of expenses incurred in Canada and charged to the US (tax rate of 26.5% vs. 39.6%)

• Estimated annual cross charge will be between C$2–$5 million

(1) Estimates are subject to change pending the finalization of the purchase price allocation. The estimate is based on a purchase price of C$388 million for Service Experts’ US operations

and a purchase price allocation of an intangible and goodwill value of C$389 million, which for US tax purposes are 100% deductible, straight-line over 15 years. The exchange rate used

was $0.778.

(2) Based on an estimate of corporate expenses incurred to mange and benefit the US operations of Service Experts.

111

Capex Target Range for 2016 IRR Achieved in 2015

HVAC rentals $30M - $40M 13%-20%(3)

Sub-metering growth $10M – $20M 10%-16%(4)

In-house financing $1M - $5M –

Water heater additions $25M – $30M 16%-18%(3)

Water heater

exchanges

$30M – $40M 18%-21%(3)

Corporate $3M – $6M –

Building $12M – $16M –

Total Range $111M – $157M(2) 10%-21%

Cash from Ops

85%

Debt 15%

Sources of Capital

Self-Funding Our Significant Growth in 2016(1)

Uses of Capital – C$ (excluding Service Experts)

(1) Excludes acquisitions.

(2) The target range of capital spend for Home Service is largely based on the number and type of equipment originated (assumed to be approximately 25,000 water heater and water treatment rental

additions, 50,000 water heater exchanges and 10,000 HVAC rental additions) and the mix between rental, sales and financing arrangements similar to actual results experienced in the last 6

months of operations. The target range for capital spend in Sub-metering is based on the number and type of metering equipment installed during the year assumed to be approximately 17,000

units. Corporate capital includes IT software and hardware, furniture and fixtures and other capital projects. The building relates to a new head office to be purchased in Q2 of 2016.

(3) Based on 2015 actual average revenue and cost of goods sold per unit and sales, general and administration (“SG&A”) expenses which were allocated based on the number of incidents or number

of active units, depending on the nature of the expense, over a useful life of 16 years, with revenue price increases of 2.5% per year and expense inflation assumed at 2.25% per year and with a

tax rate of 26.5%.

(4) Based on 2015 actual contracted sales and their respective net revenue per suite, capital cost per suite and based on actual average SG&A costs per billable service for 2015, over an initial meter

seal period of 10 years, a contract length of 18 years, an expense inflation rate of 2.25% per year, price increase inflation of 2.5% per year and with a tax rate of 26.5%.

112

Actual

December 31, 2015

Strong Balance Sheet

BBB+ S&P (DBRS: BBB High)

3.5% Weighted Average

Interest Rate

3.1% Weighted Average

Interest Rate

3.2x Leverage Profile

3.7x Leverage Profile

9.0x(3)

Interest Coverage

8.7x(3)

Interest Coverage

BBB S&P

(DBRS: BBB High/negative)

3.1% Weighted Average

Interest Rate

3.5x(2)(3)

Leverage Profile

8.7x(4)

Interest Coverage

Original Pro Forma

December 31, 2015

(1) Revised Pro Forma balance sheet metrics reflect the cash raised from the over-allotment from the equity issuance, the excess cash as a result of the stronger than expected US/CAD

exchange rate and the reduction in the line of credit from this excess cash.

(2) Calculated using Debt divided by Acquisition Adjusted EBITDA (for a definition, please refer to the Non-IFRS Financial and Performance Measures section in Enercare’s Q1 2016 MD&A

dated May 12, 2016). Pro Forma Acquisition Adjusted EBITDA excludes transaction costs and synergies. Please refer to Enercare’s prospectus dated March 22, 2016 for a definition and

reconciliation of Pro Forma Acquisition Adjusted EBITDA.

(3) Debt excludes pension, other post-employment benefit (OPEB) liabilities and capital lease obligations.

(4) Calculated using Acquisition Adjusted EBITDA (for a definition of this Non-IFRS measure, please refer to the Non-IFRS Financial and Performance Measures section in Enercare’s Q1 2016

MD&A dated May 12, 2016) and excludes the balances associated with OPEB and capital lease obligations.

BBB S&P

(DBRS: BBB High/negative)

Revised Pro Forma

December 31, 2015(1)

113

Creating Value for Shareholders

Investing in growth

Increasing our

distributable cash

Returning capital through dividends and buying back our shares

115

Investor Day

THURSDAY, JUNE 9, 2016