Embed Size (px)

Citation preview

1

Morgans Research

January 2018

2

Investment Strategy : Prelude

Market forces are on the move heading into 2018. Global growth is improving (Europe the standout), helping US bond rates to three and a half year highs. This can be taken as positive or negative for equities depending on whether you’re more optimistic about equities friendly growth, or more worried about equities unfriendly inflation (higher rates).

Either way, capital markets are likely to be challenged in a rising rate environment, with the rise and fall of Bitcoin indicative of how rapidly risk capital can rise and fall back to earth. Note that external/ geo-political risks also still bubble in the background.

Investors can’t afford to take their eye off the ball in 2018. Our Investment Strategy remains cautious overall, but plenty of compelling investment ideas are still on offer amongst the noise.

3

Agenda

� Strategy snapshot

� Economic outlook

� Asset allocation

� International diversification

� Best equities ideas

Data Sources: IRESS, Morgans, Factset, Morningstar unless otherwise noted.

44

We’re cautiously optimistic about equities given the pickup in global economic growth, offset by

the fact that Australian shares appear to be pricing this in well before it translates into higher earnings.

Strategy snapshot

5

“Goldilocks Trade” extends equities into year 9 of their bull run

JPMorgan Global Composite PMI (Growth) US 10-Year bond rates bounce to 3.5 year highs

50

51

52

53

54

55

56

Jun-14 Jun-15 Jun-16 Jun-17

Index

Steady economic growth at low inflation has been “just right”, meaning that Central Banks haven’t needed to move market friendly monetary settings in dramatic fashion. However higher that expected inflation, leading to higher rates, is a material risk to markets in 2018.

6

Several competing forces suggest investors should be on guard

With markets at elevated valuations, investors also appear to be complacent to ongoing external risks and a wide range of possible economic outcome.

Market friendly

� Accommodative monetarypolicy

� US and European recoveries entrenched

� Improving potential for fiscal

spend to replace monetary policy

� Higher commodity prices

� US Tax reform

Unfriendly

� Global credit tightening cycle begins

� High asset prices / Speculative bubbles

� North Korean brinkmanship

� Political instability in Washington

� Increased trade protectionism

Unknowns

� Potentially disorderly capital market re-balancing

� Emerging market debt

� UK’s exit from the EU

� Inflationary threats

� Other geo-politics

7

US Equities are supported by good profit growth

Record US share prices look expensive, but are supported by material (12%) growth in corporate earnings, which are also now accelerating.

S&P 500 – Share prices (dark blue) versus Earnings (light blue)

8

However high valuations and low volatility also look disconnected from prevailing risks

S&P500 market volatility is at 24 year lows

Market bulls make the point that low volatility is a by-product of economic conditions ideal for markets to keep edging higher.

Bears point to a lack of worry as a sign of complacency to economic risks.

These are uncharted waters.

9

Aussie Equities are trying to pre-empt elusive profit growth

Earnings growth for Aussie Industrials is tepid (6-7% ex-Resources) versus the long term average (10-11%).

ASX200 Industrials – Share prices (dark blue) versus Earnings (light blue)

10

Leading to fully priced valuations

ASX200 Industrials 12-month forward PE multiple

Valuations imply that either forecast company profits are too conservative, domestic interest rates are heading lower, or that shares are too expensive.

11

The outlook is mixed for Aussie large cap stalwarts

The top 12 stocks account for half of the Australian market and therefore distort aggregate metrics. Investors need to become familiar with smaller, and less familiar names / opportunities.

12

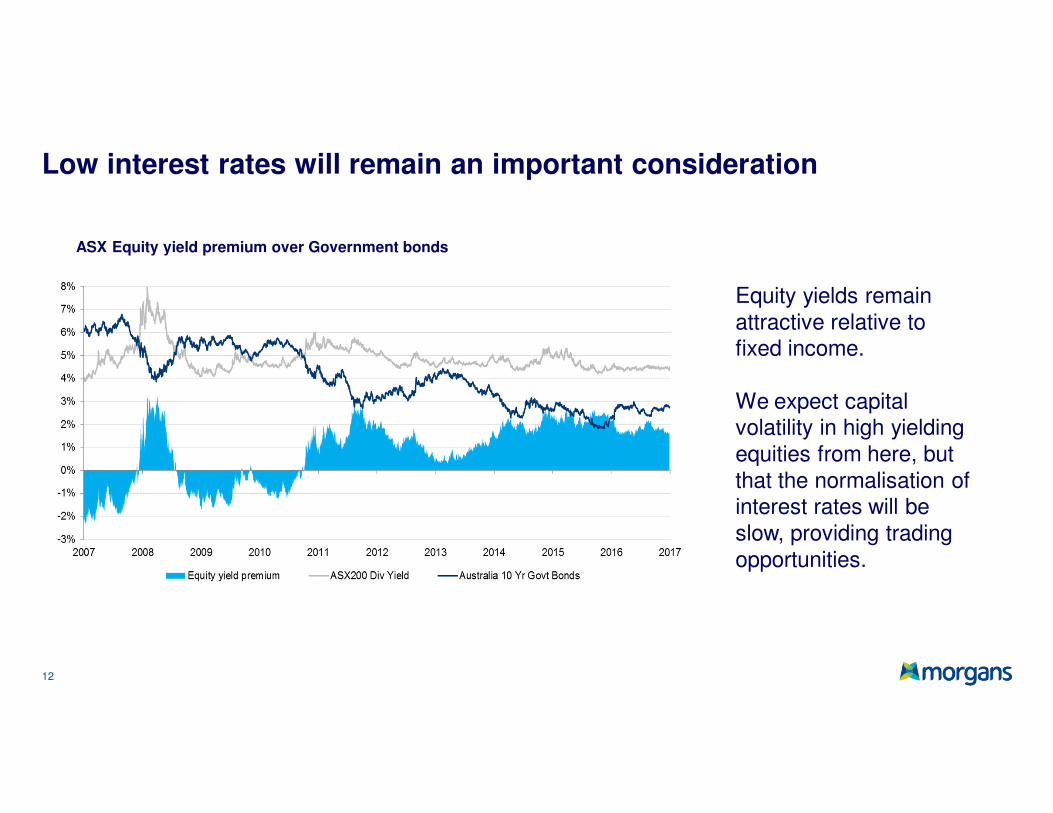

Low interest rates will remain an important consideration

ASX Equity yield premium over Government bonds

Equity yields remain attractive relative to fixed income.

We expect capital volatility in high yielding equities from here, but that the normalisation of interest rates will be slow, providing trading opportunities.

13

2018 Outlook

• Markets remain in a sweet spot with global growth becoming entrenched and an

absence of inflation. Rising interest rates are typically kryptonite for bull markets, hence

we’re watching inflation closely. We think that disorderly capital market rebalancing can be

avoided if Central Bank rate normalization is gradual through 2018.

• High yielders are likely to underperform in a rising rates environment. Hence we

recommend allocating less exposure to defensives and more exposure to cyclicals.

• Europe and Asia are leading (we forecast the Euro to outperform), the US is steady and

Australia is lagging in terms of investment exposure appeal. Synchronised growth and a

weaker US dollar provide strong tailwinds for commodities.

• Markets look vulnerable while valuations look stretched and while geo-politcical risks are in

play. We prefer to deploy capital at cheaper valuations during market volatility.

14

Tactical recommendations

• Moderate expectations : Given the reality

of extended valuations and below-average

growth, investors need to caution against

expectations of above-higher returns.

• Avoid complacency : Resist assuming

higher risk in pursuit of diminishing returns.

This includes large cap stalwarts.

• Be opportunistic : Retain cash to protect

capital and capture opportunities and

remember to crystallize profit when

appropriate.

� Diversify internationally : Seek relatively

compelling offshore dynamics in Europe,

Asia and the US, while domestic conditions

remain slow.

� Follow conviction : Solid returns are still

achievable in companies proving they can

still thrive in this environment.

1515

Economic outlook

The global economy in 2018 is on track to deliver its best growth performance since with GFC, with

the outlook for Europe and the Euro standouts.

16

The global economy : Europe the standout

Eurozone PMI and GDP

We don’t expect Brexit contagion to spread. Arguably Europe has more to lose than the UK if it turns a political issue into an Economic one.

� The Euro Area economy is growing almost as fast as it was in the period of great prosperity before the GFC (2006)

� Growth should accelerate to 2.5% in 2018, with inflation of only 1.2%, ideal conditions for European investors.

� Very high unemployment at 9% leaves plenty of capacity grow versus the US at full employment.

� This supports strong appreciation of the Euro over both the USD and AUD.

17

� Growth in corporate profits of 6-7% (Industrials only) reflects sluggish economic growth.

� We’re optimistic that Australian growth will rise sharply to 3.0% in 2018, ahead of market expectations.

� However an oversupply of labour means that wages growth and core inflation remain low.

� We expect RBA cash rates to remain stable, while economic growth and inflation remain tepid.

Australia : Slow recovery from a growth recession

Australian Economic forecasts – end of 2018

18

� Our modelling suggests that both US and Australian shares are trading in line with short term fundamentals, but that those fundamentals are improving.

� Higher US earnings will feed into stronger growth in the Australian economy.

� We prefer to use likely market volatility as an accumulation opportunity in high quality and high conviction stocks.

Stock markets : Trading ahead of fundamentals

Stock market performance

1919

Asset allocation

Strategic Asset Allocation (SAA) is the process of allocating funds between asset classes to

balance investors’ return objectives and risk tolerance. It is one of the most important, but one of the most overlooked aspects of wealth management.

20

The Economic Cycle : Recovery is supportive for Equities

Economic conditions remain in equity friendly recovery mode as financial settings remain accommodative, although market forces are shifting.

With synchronised global growth now picking up, upside risk to inflation (and interest rates) is likely to challenge income-oriented asset classes (property and income assets) especially while valuations are elevated.

We expect the steady normalisation in interest rates to support a gradual transition in outperformance from defensive and high yield assets, to cyclical and growth assets.

The Economic cycle

We are Here

21

Strategic Asset Allocation : A systematic approach

Critical to our SAA approach is clearly

defining the risk profile and objectives of

individual investors.

We use recommended long term

Benchmark allocations per asset class

around which we apply shorter term

Tactical Tilts.

The current stage of the economic cycle is

supportive of reducing allocations in

defensive assets in favour of increasing

exposure to assets which capture the

early stages of economic growth. This

incorporates a higher weighting to equities

and lower allocations to Income Assets.

Recommended Asset Allocations inclusive of Tactical Tilts

2222

International investing

Investing offshore not only provides access to superior returns, but also allows investors to

capture global trends, mitigate regional risk, and leverage currency movement.

23

Diversification – Risk mitigation

Most Australian SMSF’s have almost no exposure to International shares. A significant ‘home bias’ exposes investors to sub-optimal diversification and risk mitigation due to a high concentration into Australia-centric drivers.

Average Australian SMSF Asset Allocation

ASX200 Index shows Australia’s poor Sector

diversification

MSCI World Index offers access to relatively diverse/compelling

themes

Australian shares

Cash & Deposits

Commercial Property

Unlisted Shares

Managed Investments

Listed Trusts

Res. Property

Foreign Shares 1%

Other Assets

Financials52%

Materials13%

Consumer Staples7%

Industrials7%

Health Care7%

Energy5%

Telco2%

Consumer Discretionary

3%

Utilities3%

IT1%

Financials19%

Materials5%

Consumer Staples11%

Industrials11%

Health Care13%

Energy7%

Telco3%

Consumer Discretionary

12%

Utilities4%

Information Technology

14%

24

Preferred International funds : LICs and ETFs

Thematic exposures

� European recovery

� Aging demographics

� Technology

� Emerging markets and Asia

Diversification

• Sector and geographic

2525

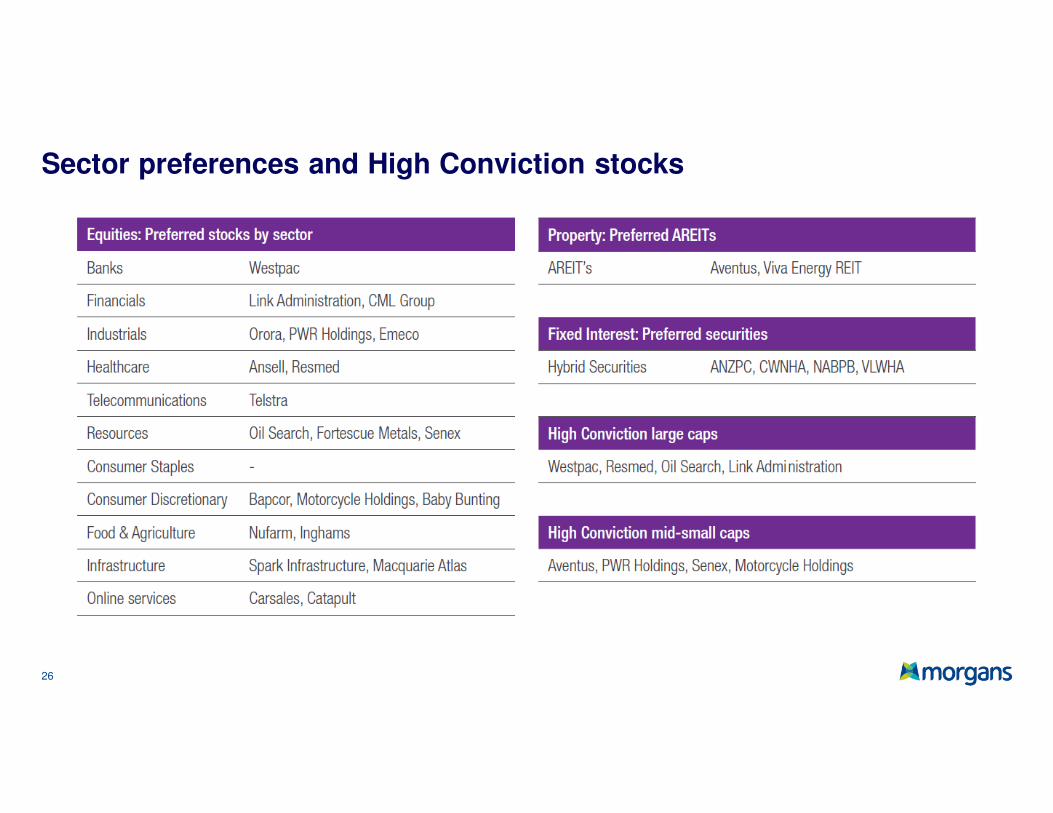

Best equities ideas

High Conviction stocks we think offer the highest

risk-adjusted 12-month returns supported by a high

level of analyst confidence.

Our Equity Model Portfolios are managed by

the Morgans Investment Committee for use as

guides for various investing styles/ risk profiles.

26

Sector preferences and High Conviction stocks

27

Equity Model Portfolios

28

Equity Model Portfolio performance

Relative performance Portfolio Performance since Nov 2011 (start $250k)

The relative appeal of income versus growth strategies has fluctuated with confidence in the outlook for economic reflation (growth).

2929

Appendices

30

Morgans – Built around personalised service

33 Year history

Australia's leading full service financial advisory group

100% Staff owned

90% of all Australians live within 100km of a Morgans office

+300,000 clients, +500 authorised representatives operating from 60 offices

$60 billion of funds under advice.

+$20 billion raised via 700 transactions for Australian companies over 25 years

Award-winning research team, covering + 250 companies across all industry

Top-ranked small and mid cap corporate finance house

31

Morgans research team

32

Undertaking significant corporate contact

33

Generating value for clients

34

We try to use fear and misunderstanding to our clients’ advantage

35

This presentation is provided for general information purposes only and is not intended as an offer to enter into any transaction. This information contained in it is not necessarily complete and its accuracy can not be guaranteed. We have prepared this presentation without consideration of the investment objectives, financial situation or particular needs of any individual investor.

Before a client makes an investment decision, a client should, with or without Morgans' assistance, consider whether any advice contained in the presentation is appropriate in light of their particular investment needs, objectives and financial circumstances. It is unreasonable to rely on any recommendation without first having spoken to your adviser for a personal recommendation.

The information contained in this presentation has been taken from sources believed to be reliable. Morgans Financial Limited does not represent that the information is accurate or complete and it should not be relied on as such. Any opinions expressed reflect Morgans' judgment at this date and are subject to change. Morgans and/or its affiliated companies may make markets in the securities discussed. Further Morgans and/or its affiliated companies and/or their employees from time to time may hold shares, options, rights and/or warrants on any issue included in this presentation and may, as principal or agent, sell such securities.

The Directors of Morgans advise that they and persons associated with them may have an interest in the above securities and that they may earn brokerage, commissions, fees and other benefits and advantages, whether pecuniary or not and whether direct or indirect, in connection with the making of a recommendation or a dealing by a client in these securities, and which may reasonably be expected to be capable of having an influence in the making of any recommendation, and that some or all of our representatives may be remunerated wholly or partly by way of commission.

The presentation is proprietary to Morgans Financial Limited and may not be disclosed to any third party or used for any other purpose without the prior written consent of Morgans.

Morgans Financial Limited (ABN 49 010 669 726 AFSL 235410)A Participant of ASX Group

Principal Office: Level 29, Riverside Centre, 123 Eagle Street, Brisbane QLD 4000

This document has been prepared by Morgans Financial Limited in accordance with its Australian Financial Services Licence (AFSL no. 235410). The views expressed herein are solely the views of Morgans Financial Limited.

General disclaimer

36 Presentation Title

![[] Going For Gold Upper-Intermediate SB.pdf](https://img.dokumen.tips/doc/110x75/563dba01550346aa9aa1dc57/wwwfisierulmeuro-going-for-gold-upper-intermediate-sbpdf.jpg)