Embed Size (px)

Citation preview

Important disclosures and certifications are contained from page 8 of this report. www.danskeresearch.com

Investment Research — General Market Conditions

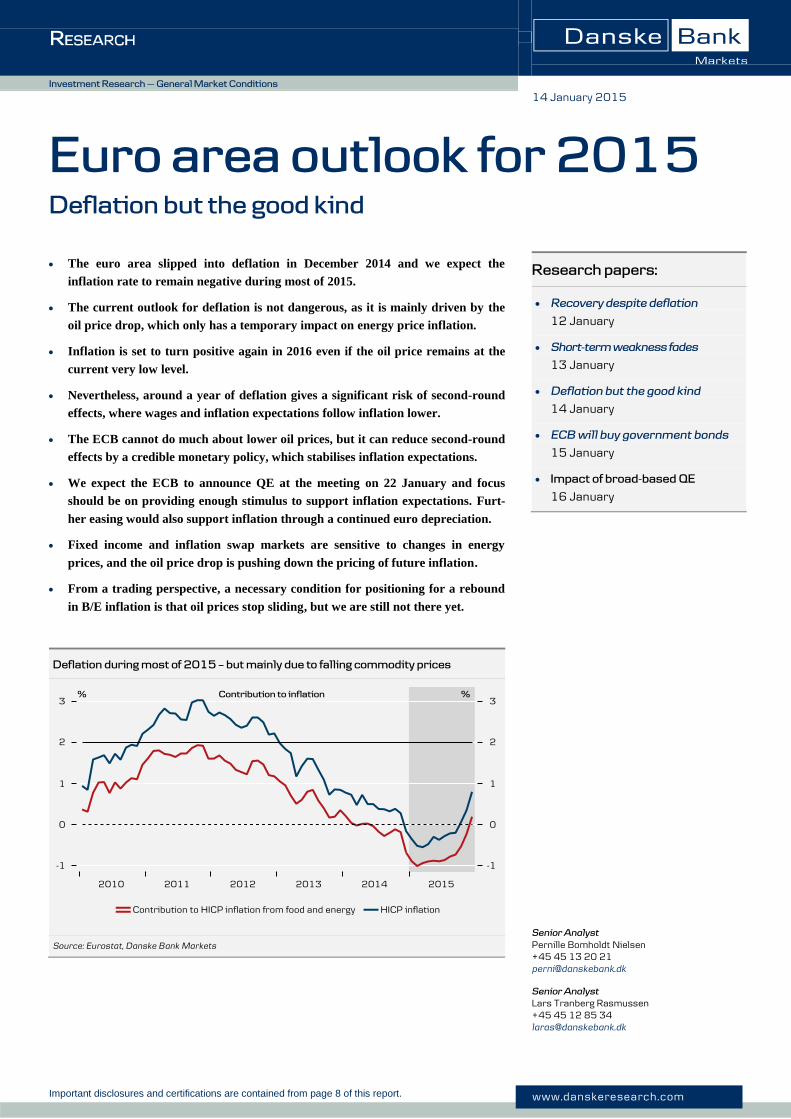

The euro area slipped into deflation in December 2014 and we expect the

inflation rate to remain negative during most of 2015.

The current outlook for deflation is not dangerous, as it is mainly driven by the

oil price drop, which only has a temporary impact on energy price inflation.

Inflation is set to turn positive again in 2016 even if the oil price remains at the

current very low level.

Nevertheless, around a year of deflation gives a significant risk of second-round

effects, where wages and inflation expectations follow inflation lower.

The ECB cannot do much about lower oil prices, but it can reduce second-round

effects by a credible monetary policy, which stabilises inflation expectations.

We expect the ECB to announce QE at the meeting on 22 January and focus

should be on providing enough stimulus to support inflation expectations. Furt-

her easing would also support inflation through a continued euro depreciation.

Fixed income and inflation swap markets are sensitive to changes in energy

prices, and the oil price drop is pushing down the pricing of future inflation.

From a trading perspective, a necessary condition for positioning for a rebound

in B/E inflation is that oil prices stop sliding, but we are still not there yet.

Deflation during most of 2015 – but mainly due to falling commodity prices

Source: Eurostat, Danske Bank Markets

14 January 2015

Senior Analyst Pernille Bomholdt Nielsen +45 45 13 20 21 [email protected]

Senior Analyst Lars Tranberg Rasmussen +45 45 12 85 34 [email protected]

Research papers:

Recovery despite deflation

12 January

Short-term weakness fades

13 January

Deflation but the good kind

14 January

ECB will buy government bonds

15 January

Impact of broad-based QE

16 January

Euro area outlook for 2015

Deflation but the good kind

2 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

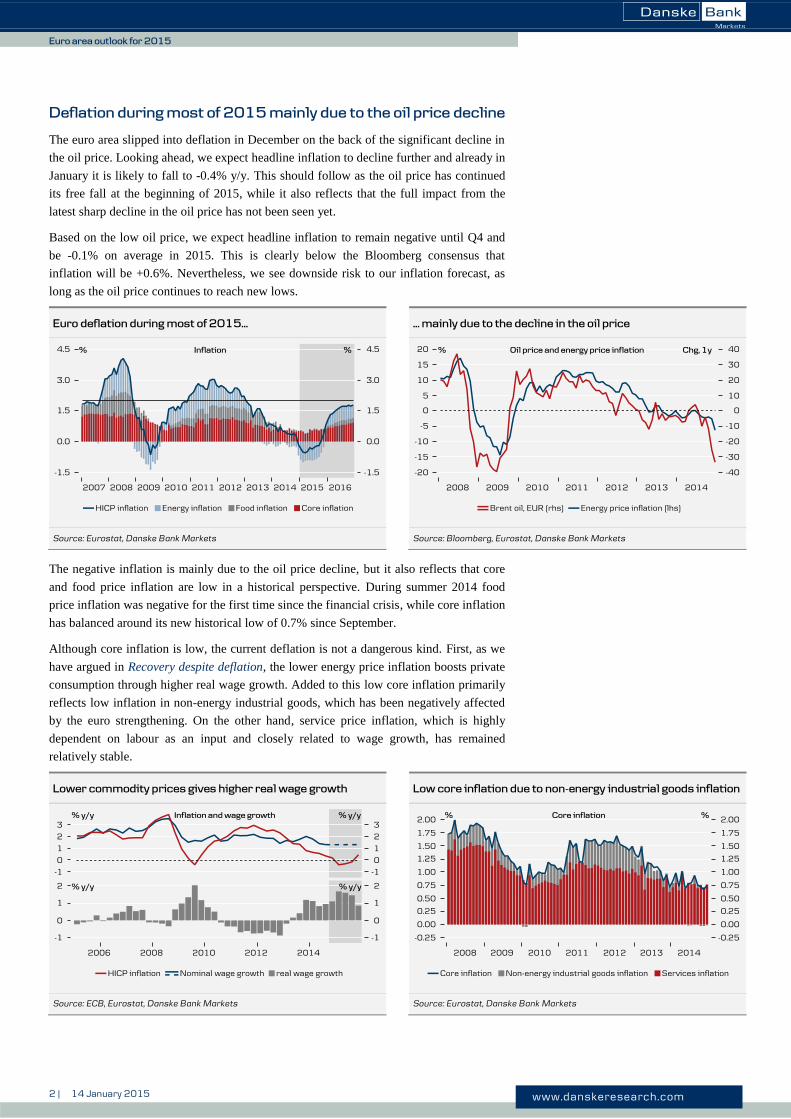

Deflation during most of 2015 mainly due to the oil price decline

The euro area slipped into deflation in December on the back of the significant decline in

the oil price. Looking ahead, we expect headline inflation to decline further and already in

January it is likely to fall to -0.4% y/y. This should follow as the oil price has continued

its free fall at the beginning of 2015, while it also reflects that the full impact from the

latest sharp decline in the oil price has not been seen yet.

Based on the low oil price, we expect headline inflation to remain negative until Q4 and

be -0.1% on average in 2015. This is clearly below the Bloomberg consensus that

inflation will be +0.6%. Nevertheless, we see downside risk to our inflation forecast, as

long as the oil price continues to reach new lows.

Euro deflation during most of 2015... ... mainly due to the decline in the oil price

Source: Eurostat, Danske Bank Markets Source: Bloomberg, Eurostat, Danske Bank Markets

The negative inflation is mainly due to the oil price decline, but it also reflects that core

and food price inflation are low in a historical perspective. During summer 2014 food

price inflation was negative for the first time since the financial crisis, while core inflation

has balanced around its new historical low of 0.7% since September.

Although core inflation is low, the current deflation is not a dangerous kind. First, as we

have argued in Recovery despite deflation, the lower energy price inflation boosts private

consumption through higher real wage growth. Added to this low core inflation primarily

reflects low inflation in non-energy industrial goods, which has been negatively affected

by the euro strengthening. On the other hand, service price inflation, which is highly

dependent on labour as an input and closely related to wage growth, has remained

relatively stable.

Lower commodity prices gives higher real wage growth Low core inflation due to non-energy industrial goods inflation

Source: ECB, Eurostat, Danske Bank Markets Source: Eurostat, Danske Bank Markets

3 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

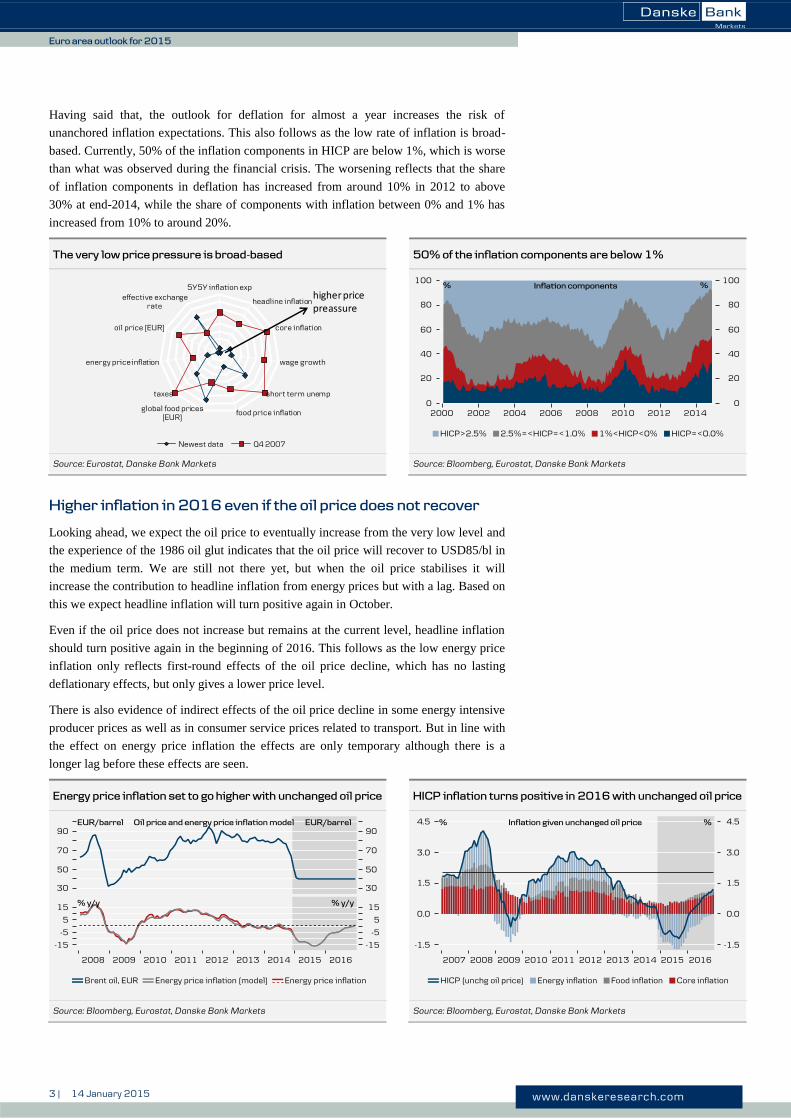

Having said that, the outlook for deflation for almost a year increases the risk of

unanchored inflation expectations. This also follows as the low rate of inflation is broad-

based. Currently, 50% of the inflation components in HICP are below 1%, which is worse

than what was observed during the financial crisis. The worsening reflects that the share

of inflation components in deflation has increased from around 10% in 2012 to above

30% at end-2014, while the share of components with inflation between 0% and 1% has

increased from 10% to around 20%.

The very low price pressure is broad-based 50% of the inflation components are below 1%

Source: Eurostat, Danske Bank Markets Source: Bloomberg, Eurostat, Danske Bank Markets

Higher inflation in 2016 even if the oil price does not recover

Looking ahead, we expect the oil price to eventually increase from the very low level and

the experience of the 1986 oil glut indicates that the oil price will recover to USD85/bl in

the medium term. We are still not there yet, but when the oil price stabilises it will

increase the contribution to headline inflation from energy prices but with a lag. Based on

this we expect headline inflation will turn positive again in October.

Even if the oil price does not increase but remains at the current level, headline inflation

should turn positive again in the beginning of 2016. This follows as the low energy price

inflation only reflects first-round effects of the oil price decline, which has no lasting

deflationary effects, but only gives a lower price level.

There is also evidence of indirect effects of the oil price decline in some energy intensive

producer prices as well as in consumer service prices related to transport. But in line with

the effect on energy price inflation the effects are only temporary although there is a

longer lag before these effects are seen.

Energy price inflation set to go higher with unchanged oil price HICP inflation turns positive in 2016 with unchanged oil price

Source: Bloomberg, Eurostat, Danske Bank Markets Source: Bloomberg, Eurostat, Danske Bank Markets

5Y5Y inflation exp

headline inflation

core inflation

wage growth

short term unemp

food price inflationglobal food prices [EUR]

taxes

energy price inflation

oil price [EUR]

effective exchange rate

Newest data Q4 2007

higher pricepreassure

4 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

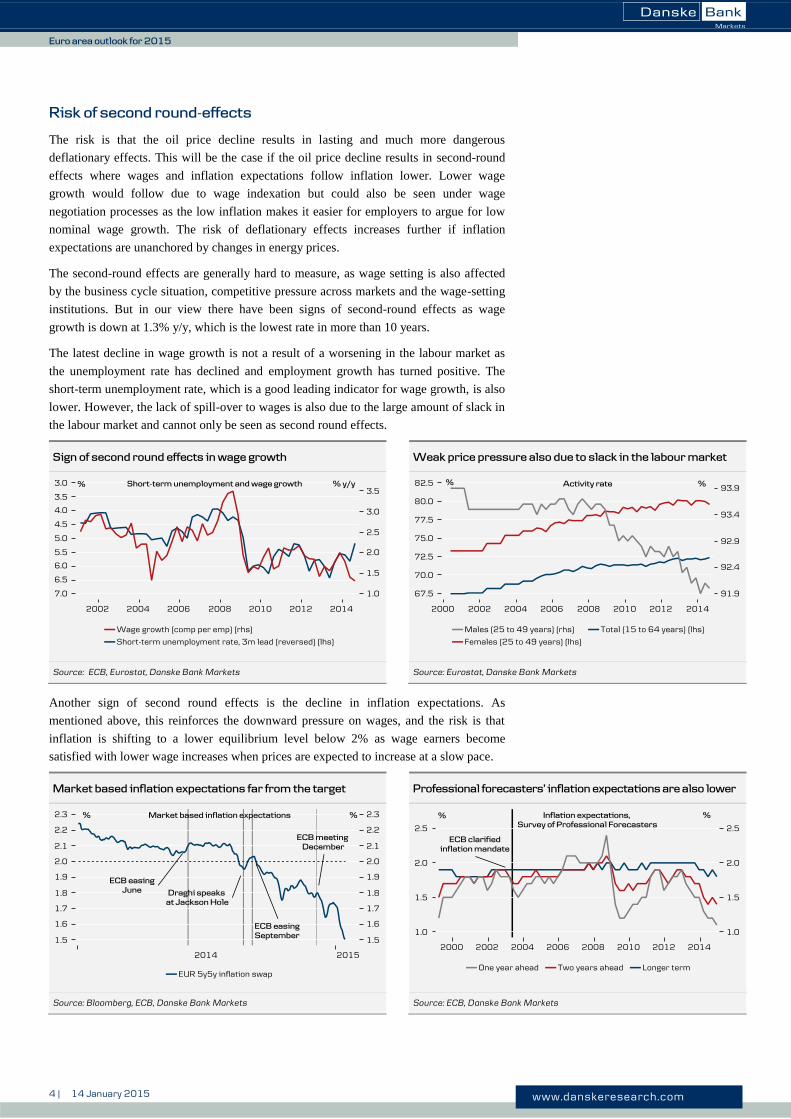

Risk of second round-effects

The risk is that the oil price decline results in lasting and much more dangerous

deflationary effects. This will be the case if the oil price decline results in second-round

effects where wages and inflation expectations follow inflation lower. Lower wage

growth would follow due to wage indexation but could also be seen under wage

negotiation processes as the low inflation makes it easier for employers to argue for low

nominal wage growth. The risk of deflationary effects increases further if inflation

expectations are unanchored by changes in energy prices.

The second-round effects are generally hard to measure, as wage setting is also affected

by the business cycle situation, competitive pressure across markets and the wage-setting

institutions. But in our view there have been signs of second-round effects as wage

growth is down at 1.3% y/y, which is the lowest rate in more than 10 years.

The latest decline in wage growth is not a result of a worsening in the labour market as

the unemployment rate has declined and employment growth has turned positive. The

short-term unemployment rate, which is a good leading indicator for wage growth, is also

lower. However, the lack of spill-over to wages is also due to the large amount of slack in

the labour market and cannot only be seen as second round effects.

Sign of second round effects in wage growth Weak price pressure also due to slack in the labour market

Source: ECB, Eurostat, Danske Bank Markets Source: Eurostat, Danske Bank Markets

Another sign of second round effects is the decline in inflation expectations. As

mentioned above, this reinforces the downward pressure on wages, and the risk is that

inflation is shifting to a lower equilibrium level below 2% as wage earners become

satisfied with lower wage increases when prices are expected to increase at a slow pace.

Market based inflation expectations far from the target Professional forecasters’ inflation expectations are also lower

Source: Bloomberg, ECB, Danske Bank Markets Source: ECB, Danske Bank Markets

5 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

The ECB cannot do much about falling oil prices and the low energy price inflation, but it

can reduce second-round effects by a credible monetary policy strategy, which stabilises

inflation expectations. In light of this we expect the ECB to announce government bond

purchases at the meeting on 22 January. Focus for the ECB should be on providing

enough stimulus to a) convince wage earners that they should expect 2% inflation and b)

generate enough demand to get unemployment down and dampen the downside pressure

on wage increases.

Weaker euro puts upwards pressure on inflation

Further monetary easing from the ECB should at the same time support inflation through

a weakening of the effective euro. This follows as the currency depreciation boosts import

prices, which in turn puts upward pressure on domestic prices. Based on our expectation

that the ECB will announce QE in January the effective euro should weaken further

during H1 and the aggregate weakening of around 10% should support inflation by

around 0.3pp in 2015 and 0.7pp in 2016.

The main impact of the euro weakening should be seen in non-energy industrial goods

inflation. However, it printed negative in Q4 14 and we are still waiting for the first

evidence that the impact of the past euro strengthening is waning. The risk is that the

impact on inflation will be smaller than usually as companies are absorbing the impact of

the currency depreciation due to weak demand and/or low inflation expectations.

Looking ahead, we expect private consumption to continue to increase, implying

companies will be more confident that lack of demand is not a concern. Based on this we

expect the pass-through to consumer prices of the cost of the currency depreciation to be

seen in H1. Added to this further easing from the ECB will strengthen the spill-over if the

monetary easing results in higher inflation expectations.

Euro depreciation puts upward pressure on inflation 10% euro weakening should increase inflation by 0.3pp in 15

Source: Bloomberg, Danske Bank Markets Source: OECD, Danske Bank Markets

The conclusions above imply we expect core inflation to slowly increase during our

forecast horizon. This should also follow as the stronger recovery will continue to give a

lower unemployment rate which supports wage pressure. However, the large amount of

slack in the labour market should imply that the impact on wage growth will be modest.

In light of this we expect a decline in core inflation to 0.5% y/y in March.

6 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

Second-round effects also reflected in structural changes

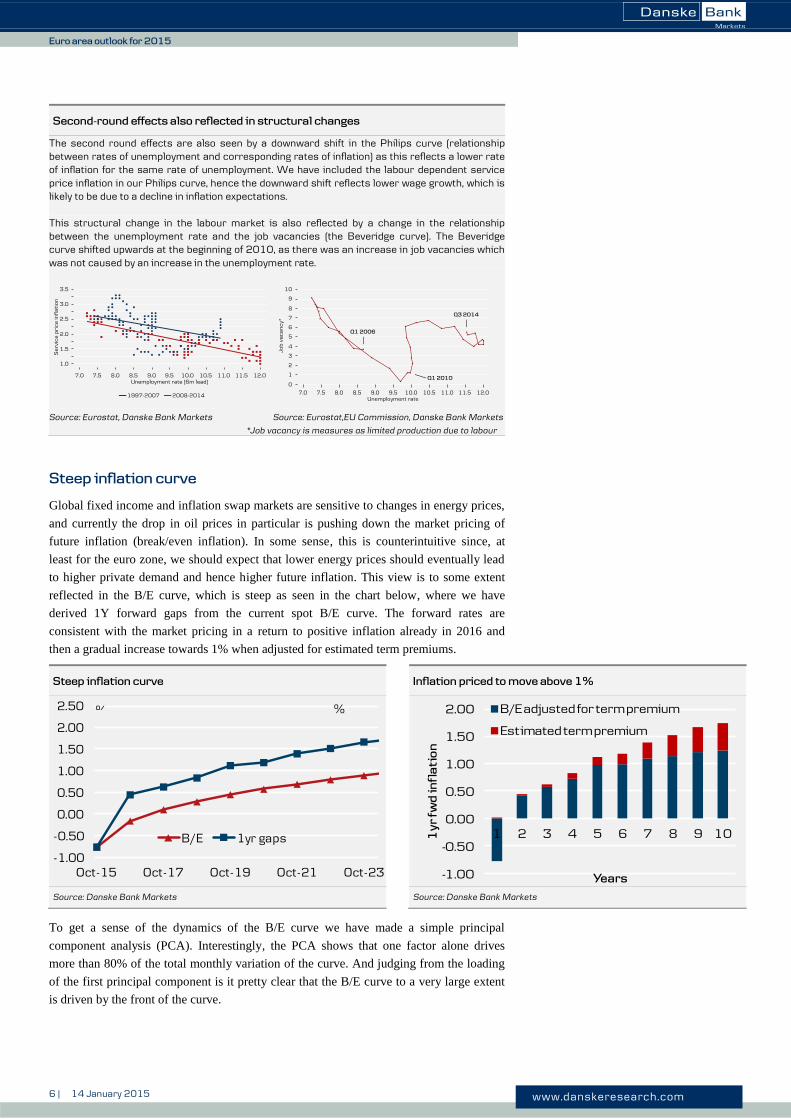

The second round effects are also seen by a downward shift in the Philips curve (relationship between rates of unemployment and corresponding rates of inflation) as this reflects a lower rate of inflation for the same rate of unemployment. We have included the labour dependent service price inflation in our Philips curve, hence the downward shift reflects lower wage growth, which is likely to be due to a decline in inflation expectations. This structural change in the labour market is also reflected by a change in the relationship between the unemployment rate and the job vacancies (the Beveridge curve). The Beveridge curve shifted upwards at the beginning of 2010, as there was an increase in job vacancies which was not caused by an increase in the unemployment rate.

Source: Eurostat, Danske Bank Markets Source: Eurostat,EU Commission, Danske Bank Markets

*Job vacancy is measures as limited production due to labour

Steep inflation curve

Global fixed income and inflation swap markets are sensitive to changes in energy prices,

and currently the drop in oil prices in particular is pushing down the market pricing of

future inflation (break/even inflation). In some sense, this is counterintuitive since, at

least for the euro zone, we should expect that lower energy prices should eventually lead

to higher private demand and hence higher future inflation. This view is to some extent

reflected in the B/E curve, which is steep as seen in the chart below, where we have

derived 1Y forward gaps from the current spot B/E curve. The forward rates are

consistent with the market pricing in a return to positive inflation already in 2016 and

then a gradual increase towards 1% when adjusted for estimated term premiums.

Steep inflation curve Inflation priced to move above 1%

Source: Danske Bank Markets Source: Danske Bank Markets

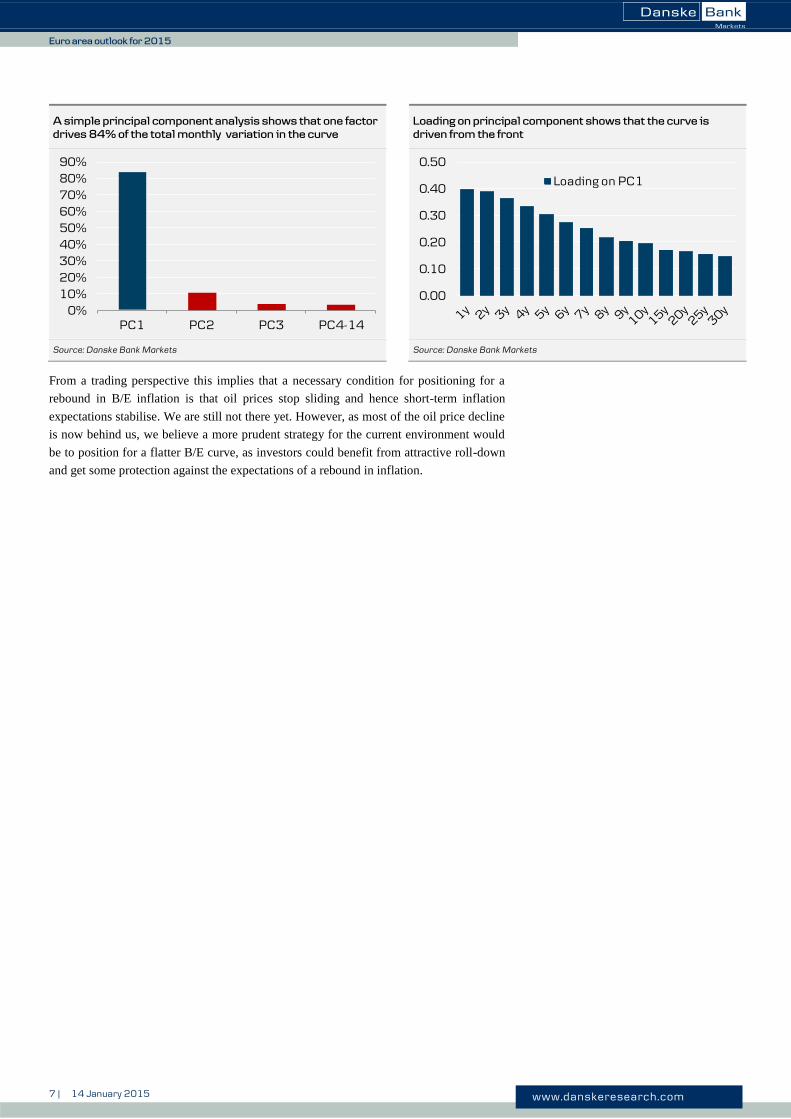

To get a sense of the dynamics of the B/E curve we have made a simple principal

component analysis (PCA). Interestingly, the PCA shows that one factor alone drives

more than 80% of the total monthly variation of the curve. And judging from the loading

of the first principal component is it pretty clear that the B/E curve to a very large extent

is driven by the front of the curve.

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

Oct-15 Oct-17 Oct-19 Oct-21 Oct-23

B/E 1yr gaps

% %

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

1 2 3 4 5 6 7 8 9 101y

r f

wd

in

fla

tio

n

Years

B/E adjusted for term premium

Estimated term premium

7 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

A simple principal component analysis shows that one factor

drives 84% of the total monthly variation in the curve

Loading on principal component shows that the curve is

driven from the front

Source: Danske Bank Markets Source: Danske Bank Markets

From a trading perspective this implies that a necessary condition for positioning for a

rebound in B/E inflation is that oil prices stop sliding and hence short-term inflation

expectations stabilise. We are still not there yet. However, as most of the oil price decline

is now behind us, we believe a more prudent strategy for the current environment would

be to position for a flatter B/E curve, as investors could benefit from attractive roll-down

and get some protection against the expectations of a rebound in inflation.

0%10%20%30%40%50%60%70%80%90%

PC1 PC2 PC3 PC4-14

0.00

0.10

0.20

0.30

0.40

0.50

Loading on PC1

8 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

Disclosure This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske

Bank’). The authors of the research report are Pernille Bomholdt Nielsen, Senior Analyst, and Lars Tranberg

Rasmussen, Senior Analyst

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’

rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-

quality research based on research objectivity and independence. These procedures are documented in Danske

Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any

request that might impair the objectivity and independence of research shall be referred to Research Management

and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do

not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate

finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology

as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors upon request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including as sensitivity analysis

of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be

considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments

(i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or

options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial

Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not

untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates

and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation

any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not

9 | 14 January 2015 www.danskeresearch.com

Eu

ro a

rea o

utlo

ok fo

r 20

15

Euro area outlook for 2015

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior

written consent.

Disclaimer related to distribution in the United States This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer

and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S.

Securities and Exchange Commission. The research report is intended for distribution in the United States solely

to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this

research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence

of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are

not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements

of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial

Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-

U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be

registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and

auditing standards of the U.S. Securities and Exchange Commission.