Embed Size (px)

Citation preview

1

INVESTMENT OPPORTUNITIES IN MALAYSIA

Programm

Informationsveranstaltung, Dezentrale Energieversorgung in

Malaysia

Zarina SaadDirector

MIDA Munich13 September 2016

About MIDA

Malaysia: Investment Outlook

Renewable Energy Outlook

Investment Strategies

Incentives

2

Incentives

Who Are We?

3

First point of contact for investors who intend to set up projects in the manufacturing

and services sectors in Malaysia

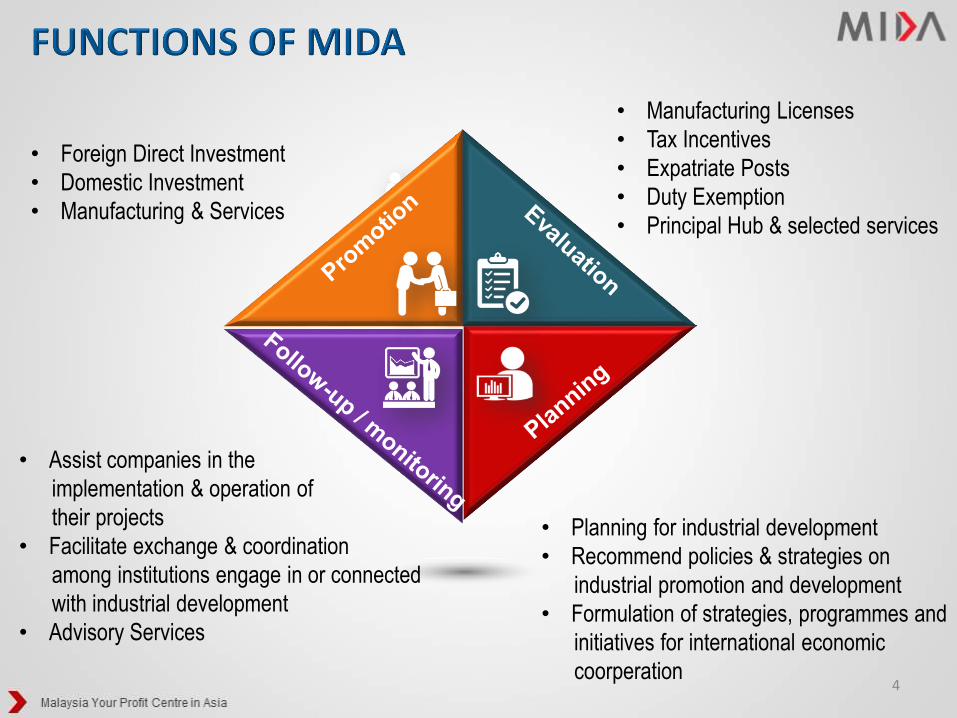

Malaysian Industrial Development Authority - Established in 1967 under Act of Parliament, 1965

The principal Malaysian Governmentagency responsible for the promotion ofinvestments and coordination ofindustrial development and selectedservices sectors in the country

4

Follow-up /

Monitoring

• Foreign Direct Investment

• Domestic Investment

• Manufacturing & Services

• Manufacturing Licenses

• Tax Incentives

• Expatriate Posts

• Duty Exemption

• Principal Hub & selected services

• Assist companies in the

implementation & operation of

their projects

• Facilitate exchange & coordination

among institutions engage in or connected

with industrial development

• Advisory Services

• Planning for industrial development

• Recommend policies & strategies on

industrial promotion and development

• Formulation of strategies, programmes and

initiatives for international economic

coorperation

Tokyo

Osaka

Seoul

Taipei

ShanghaiGuangzhou

MalaysiaSingapore

Sydney

Mumbai

Dubai

Stockholm

Frankfurt

Munich

Milan

Paris

London

Boston

New York

ChicagoSan Jose

Los Angeles Houston

23 Overseas Centres

Beijing

5

MIDA Munich

MIDA Munich Area of Coverage

Austria

Bavaria

Baden Württemberg

Germany

Poland

Czech Republic

Slovakia

Slovenia

Estonia

Latvia

Bulgaria

Romania

Lithuania

Headquarter

KL Sentral, Kuala Lumpur

Johor Bahru

Melaka

Seremban

Selangor

Ipoh

Penang

Alor Setar

Kota Bharu

Kuala

Terengganu

KuantanKota Kinabalu

Kuching

7

Malaysia : Economy and Investment Outlook

9

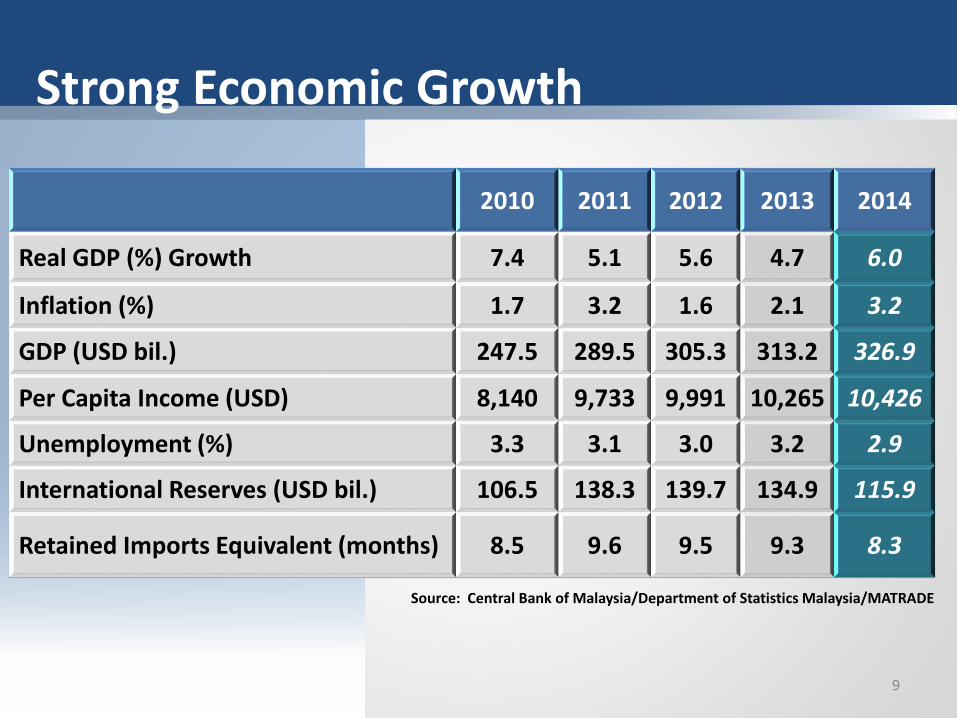

Strong Economic Growth

2010 2011 2012 2013 2014

Real GDP (%) Growth 7.4 5.1 5.6 4.7 6.0

Inflation (%) 1.7 3.2 1.6 2.1 3.2

GDP (USD bil.) 247.5 289.5 305.3 313.2 326.9

Per Capita Income (USD) 8,140 9,733 9,991 10,265 10,426

Unemployment (%) 3.3 3.1 3.0 3.2 2.9

International Reserves (USD bil.) 106.5 138.3 139.7 134.9 115.9

Retained Imports Equivalent (months) 8.5 9.6 9.5 9.3 8.3

Source: Central Bank of Malaysia/Department of Statistics Malaysia/MATRADE

0

10

20

30

40

50

60

70

2012 2013 2014

10

9.816.7

US

Bill

ion

Approved Investment in the Economy

18.1

Foreign Direct Investment (FDI) constitutes 25-30% of the total investments approved.

46.6

60.8

65.5

36.8

44.1

47.4

Foreign Domestic

11Source: MIDA 11

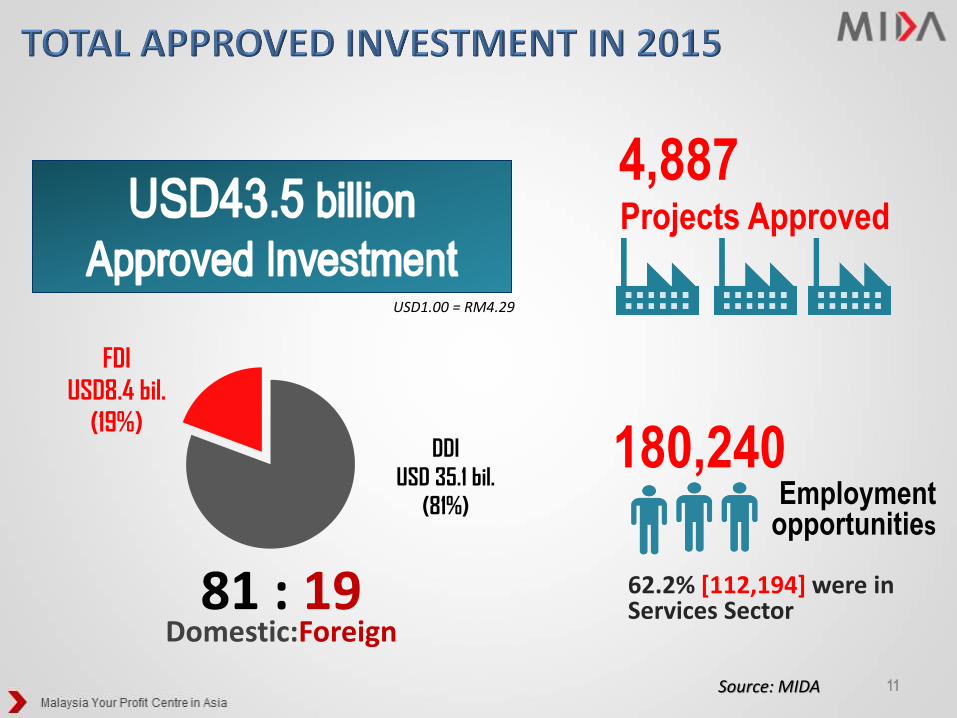

4,887Projects Approved

USD1.00 = RM4.29

180,240Employment

opportunities

62.2% [112,194] were in Services Sector81 : 19

Domestic:Foreign

FDI

USD8.4 bil.

(19%)DDI

USD 35.1 bil.

(81%)

-

0,2

0,4

0,6

0,8

1,0

1,2

12

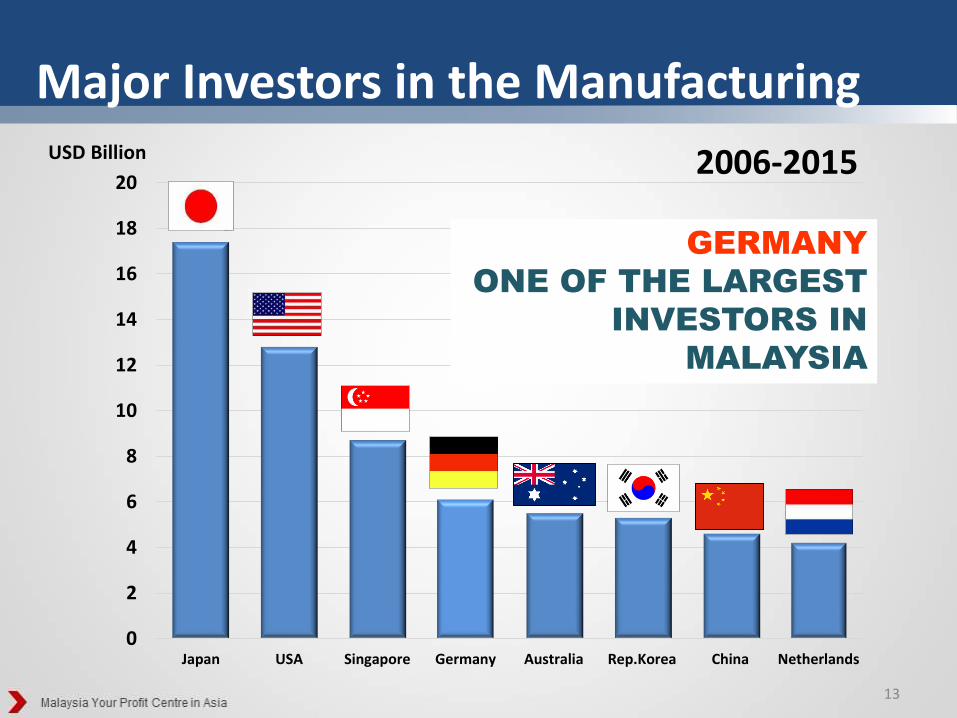

USD Billion

0.7

1.00.9

0.4

0.3 0.3 0.3 0.30.2 0.1

0

2

4

6

8

10

12

14

16

18

20

Japan USA Singapore Germany Australia Rep.Korea China Netherlands

13

Major Investors in the Manufacturing

2006-2015USD Billion

GERMANY

ONE OF THE LARGEST

INVESTORS IN

MALAYSIA

14

Major Investors From EU in the Manufacturing

2006-2015

0

1

2

3

4

5

6

7

Germany Netherlands UK Spain France Italy Norway

USD Billion

GERMANY

THE LARGEST

INVESTOR FROM EU

Electrical & Electronics, Basic Metal Products, Chemical Products , Petroleum Products (Inc.

Petrochemicals) and Non Metallic Mineral industries contribute the lion’s share of approved

foreign investments for the period 2007-2014

Investment by Industries

Electrical & Electronics

Basic Metal Products

Chemical Products

Petroleum Products

Non Metallic Mineral Products

Food Manufacturing

Machinery & Equipment

Transport Equipment

Fabricated Metal Products

Others

USD26.7 bil.

USD14.1 bil.USD9.7 bil.

USD5.6 bil.

USD4.1 bil.

Total Foreign Investment Approved : USD77.6 Billion

16

MNCs in Malaysia

17

German Companies in Malaysia

18

Manufacturing operations in Malaysia

Major German Companies

19

Major German Companies

Manufacturing operations in Malaysia

MALAYSIA HAS LIBERAL POLICIES

20

Freedom to Repatriate Capital, Interest, Dividends and Profits – No Restrictions

Manufacturing & selected services sectors can be wholly foreign-owned

OWNERSHIP

CAPITAL

EXPATRIATE POSTS

Liberal policy, based on merit of each case

World’s Perspective

global offshoring destination(A.T. Kearney Global Services Location Index™ 2016)

protecting investors(World Bank Doing Business 2015 Report)

IMD world talent rankings(IMD's World Competitiveness Yearbook 2015)

most competitive economy in overall performance (IMD's World Competitiveness Yearbook 2015)

in ease of doing business (World Bank Doing Business 2015 Report)

most competitive nation in the world (WEF's Global Competitiveness Report 2015-2016)

22

most attractive investment destination(Baseline Profitability Index (BPI) 2015)

Liberal Investment Policies

Harmonious Industrial RelationsQuality of Life

Good Track Record

STRATEGIC LOCATION

Banking System

23

Well Developed Infrastructure/

Connectivity

Pro-businessGovernment

Political and Economic Stability

Young, Trainable and Educated Labour Force

RENEWABLE ENERGY (RE) OUTLOOK

25

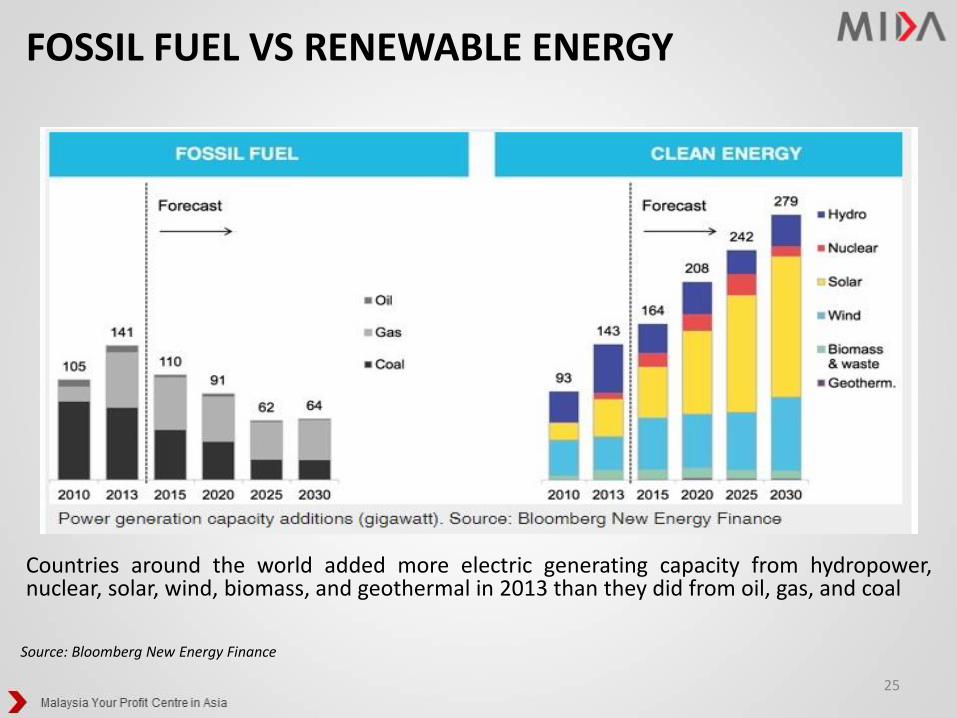

Source: Bloomberg New Energy Finance

Countries around the world added more electric generating capacity from hydropower,nuclear, solar, wind, biomass, and geothermal in 2013 than they did from oil, gas, and coal

FOSSIL FUEL VS RENEWABLE ENERGY

COMPARISON ON RE POLICIES IN ASEAN (AS OF 2015)

Source: ACE, 2015

27

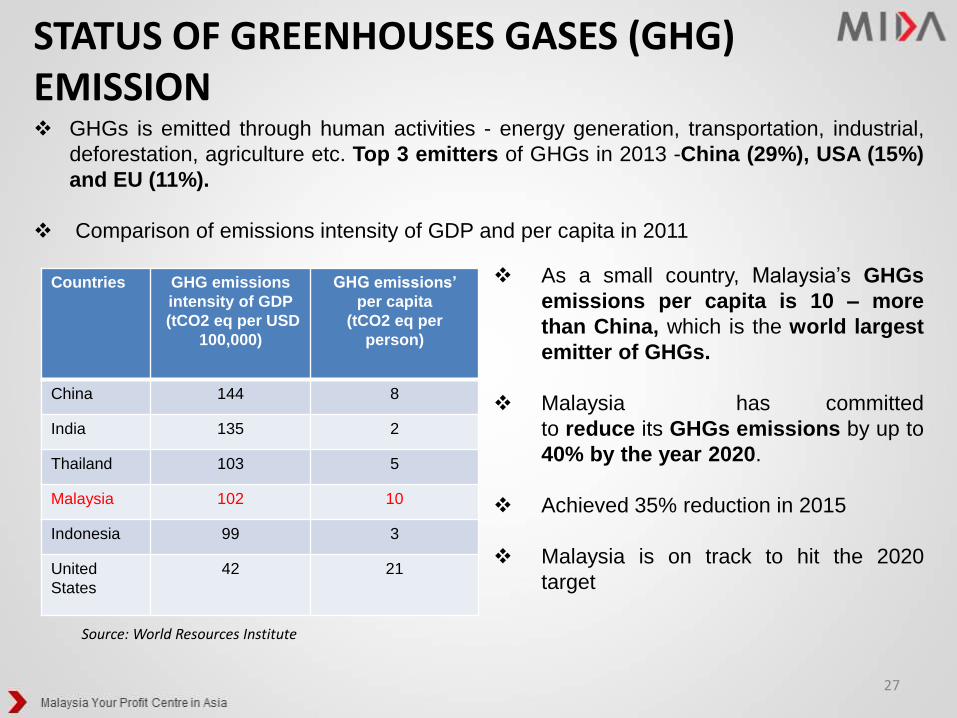

STATUS OF GREENHOUSES GASES (GHG) EMISSION GHGs is emitted through human activities - energy generation, transportation, industrial,

deforestation, agriculture etc. Top 3 emitters of GHGs in 2013 -China (29%), USA (15%)

and EU (11%).

Comparison of emissions intensity of GDP and per capita in 2011

As a small country, Malaysia’s GHGs

emissions per capita is 10 – more

than China, which is the world largest

emitter of GHGs.

Malaysia has committed

to reduce its GHGs emissions by up to

40% by the year 2020.

Achieved 35% reduction in 2015

Malaysia is on track to hit the 2020

target

Countries GHG emissions

intensity of GDP

(tCO2 eq per USD

100,000)

GHG emissions’

per capita

(tCO2 eq per

person)

China 144 8

India 135 2

Thailand 103 5

Malaysia 102 10

Indonesia 99 3

United

States

42 21

Source: World Resources Institute

28

MALAYSIA’S INITIATIVES TO GO GREEN

SAVE Programme, MEPS

Components

of a

Green

Economy

Five-Fuel Diversification Policy,

NREPAPRenewable Energy

Energy Efficient

Building

Transport

3R Programme

Tax Incentives,

GTFS, FiT

Retrofitting of Govt. buildings, GBI

rating tool

Biodiesel B5, NAP2014, Electric Mobility

Waste Management

INVESTMENT STRATEGIES

Quality Investment (FDI & DDI)

Strong Linkages with Domestic

Industries

Completing the

ecosystem

Capital Intensive

High Value Added

Utilization of natural

resourcesGreen &

Clean Technology

Skills Intensive

High Income Jobs

Iconic/ Pioneer Project

High Technology &

Knowledge Intensive

QUALITY INVESTMENT

30

ECOSYSTEM APPROACH

Promote the entire value chain of industry clusters

31

Strengthen & complete the ecosystem

R&D,

Design

Solar Wafer/

Cells

Solar

Modules

System

Integrator

Polysilicon

/ Ingot

Metal

Silicon

APPROVED & IN VARIOUS STAGES OF IMPLEMENTATION

Imex SemiconImex Semicon

Cosmos

Petroleum &

Mining

EXAMPLE: SOLAR INDUSTRY ECOSYSTEM

ST

RA

TE

GIC

LE

VE

L

RENEWABLE ENERGY ECOSYSTEM

POLICIES

PR

OJ

EC

T L

EV

EL

SU

PP

OR

TIN

G

EN

VIR

ON

ME

NT

RE STAKEHOLDERSAUTHORITIES /

AGENCIES

PROJECT IMPLEMENTATION

SOLAR

BROADER ENABLING

ENVIRONMENT

(infrastructure, industry

network, talent)

SERVICE PROVIDERS

Eg.

- Ditrolic

- Gading Kencana

- Solar Plus

FINANCIERS

Eg.

- GTFS (MGTC)

- Commercial Banks

MANUFACTURERS (Machinery and Equipment)- Domestics:

RE Solar – PV Modules e.g. First Solar, MSR, EndauPV Industries,Panasonic Energy

- Inverter– Mounting, cables, conduits, structures– Transformer

RE Biomass / Biogas – Gas engines e.g. MTU Services, Sime DarbyIndustrial, UMW Synergistic Generation

– Boilers e.g. BoilerMech, Borsig BoilerSystem, Enco Boiler, Mackenzie Industries

RE Mini Hydro - Powerhouse to house the electromechanicalequipment and all its auxiliary equipment includingcontrol room, Transformer

- Various international

BIOMASS BIOGAS SMALL HYDRO

RESOURCES

- Sunlight irradiance

- Rivers

- Palm oil plantation /

millers.

DEVELOPERS

Eg.

- Cypark Resources

- Felda

- BioXcell

RESEARCH ANDDEVELOPMENT

(study on Geothermaland Wind maps)

INCENTIVES

MAJOR INCENTIVES

35

MAJOR INCENTVES

TAX INCENTIVES

FEED-IN TARIFF

SCHEME

GREEN TECHNOLOGY

FUNDING SCHEME

Pioneer Status

Income tax exemption ranging from 70% & 100% for a period

of 5 & 10 years

Investment Tax Allowance

60% & 100% on qualifying capital expenditure for 5 years

Reinvestment Allowance

60% on qualifying capital expenditure for 15 consecutive years

Import Duty Exemption

For raw materials/components and machinery and equipment

Incentives

MAJOR INCENTIVES

36

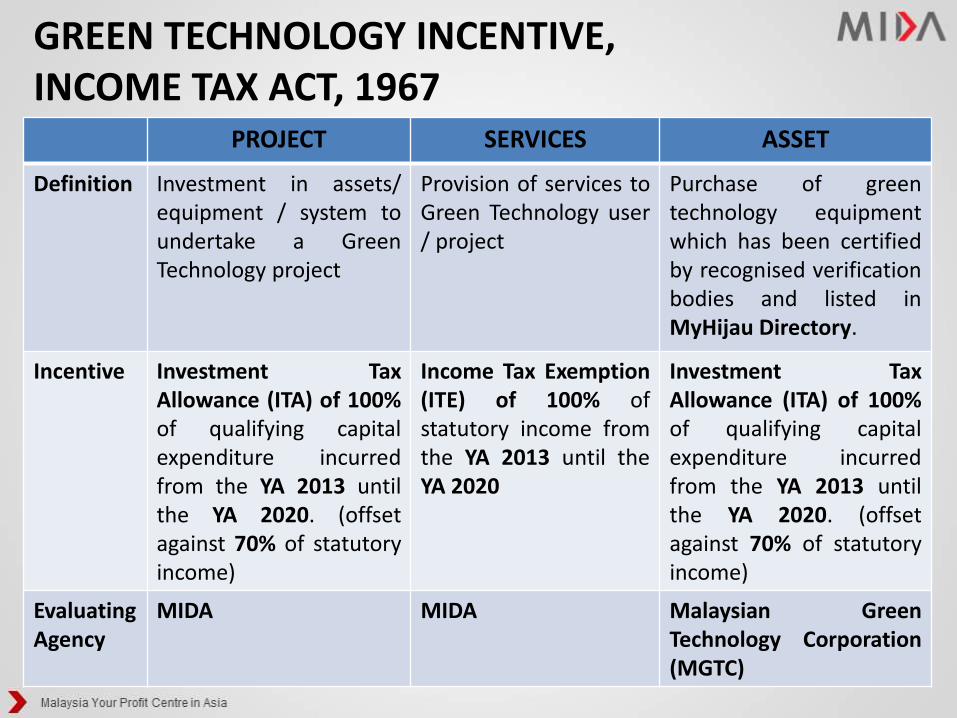

GREEN TECHNOLOGY INCENTIVE, INCOME TAX ACT, 1967

PROJECT SERVICES ASSET

Definition Investment in assets/equipment / system toundertake a GreenTechnology project

Provision of services toGreen Technology user/ project

Purchase of greentechnology equipmentwhich has been certifiedby recognised verificationbodies and listed inMyHijau Directory.

Incentive Investment TaxAllowance (ITA) of 100%of qualifying capitalexpenditure incurredfrom the YA 2013 untilthe YA 2020. (offsetagainst 70% of statutoryincome)

Income Tax Exemption(ITE) of 100% ofstatutory income fromthe YA 2013 until theYA 2020

Investment TaxAllowance (ITA) of 100%of qualifying capitalexpenditure incurredfrom the YA 2013 untilthe YA 2020. (offsetagainst 70% of statutoryincome)

Evaluating Agency

MIDA MIDA Malaysian GreenTechnology Corporation(MGTC)

PROMOTED INDUSTRIES

Energy

• Renewable Energy

• Energy Efficiency

Building

• Green Building

• Green Data Centre

Integrated Waste Management

• Waste recycling

• Waste recovery

• Waste treatment

Supporting Services

• Certification & verification bodies

• Green Township

• Electric Vehicle Services

RENEWABLE ENERGY (RE)

Commercial & industrial business entities which undertake generation

of energy using RE sources:

*Solar

Biomass

Biogas

Mini-Hydro

Geothermal

Feasibility study, system design &

advisory & consultancy, testing &

commissioning

Project Services

* Exception : Solar project under FiT Scheme

Free Trade Agreements

Market Access offered by Malaysia

14 Free Trade

AgreementsMARKET

3.0 Billion Population

42

Malaysia’s Involvement in FTAs

Regional ASEAN Free Trade Area (AFTA)

ASEAN-China FTA

ASEAN-India FTA [Trade in Goods]

ASEAN-Republic of Korea FTA

ASEAN-Japan Comprehensive

Economic Partnership (AJCEP)

[Trade in Goods]

ASEAN-Australia-New Zealand FTA

Trans-Pacific Partnership (TPP)Bilateral Malaysia-Turkey FTA

Malaysia-India Comprehensive

Economic Cooperation Agreement

(MICECA)

Malaysia-Japan Economic

Partnership Agreement (MJEPA)

Malaysia-New Zealand FTA

(MNZFTA)

Malaysia-Australia FTA (MAFTA)

Malaysia-Chile FTA (MCFTA)

Malaysia-Pakistan Comprehensive

Economic Partnership Agreement

(MPCEPA)

Bilateral Malaysia-EU

Regional Regional Cooperation

Economic Partnership

(RCEP) [Japan, China,

Korea, Australia, New

Zealand and India]

Bilateral Malaysia-Bangladesh

Malaysia-Gulf

Cooperation Council

(GCC)

Malaysia-European Free

Trade Association

(EFTA)

Concluded Under Negotiations

Under Initiation

Malaysia’s Concluded FTA – AFTA

• Potential market of 600 million in ASEAN

• Already zero tariffs for 99% of products

• ASEAN Economic Community and Single Market by 2015

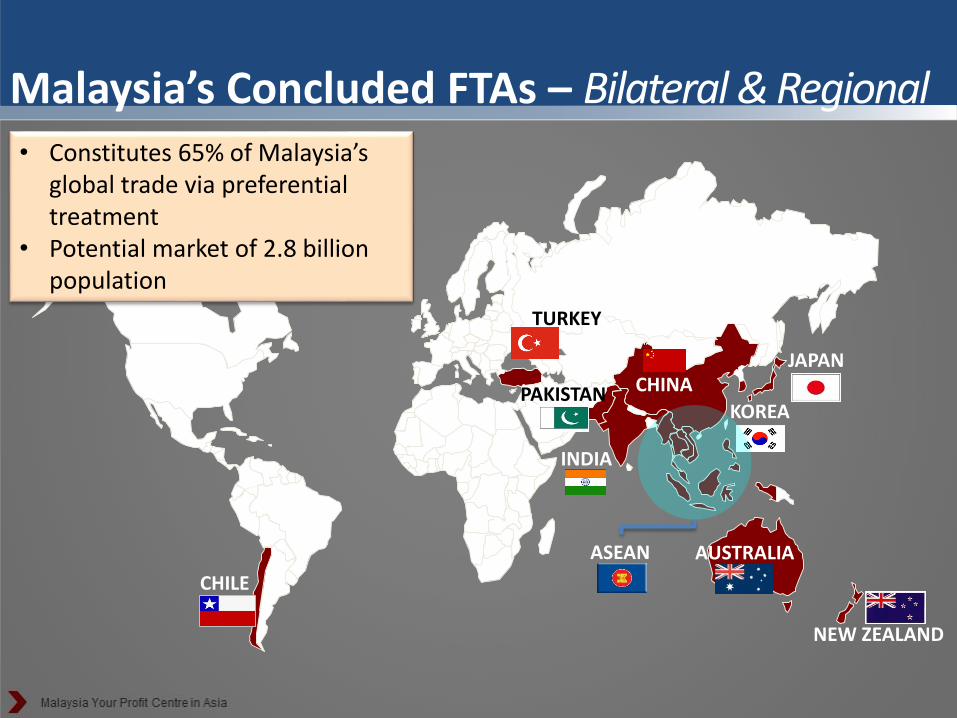

Malaysia’s Concluded FTAs – Bilateral & Regional

INDIA

PAKISTAN CHINA

ASEAN

KOREA

JAPAN

AUSTRALIA

NEW ZEALAND

CHILE

• Constitutes 65% of Malaysia’s global trade via preferential treatment

• Potential market of 2.8 billion population

TURKEY

Population 625 million

- Youth 60%

GDP USD2,398 billion

GDP Growth 5.1%

GDP per capita USD3,837

Total Trade USD2,511 billion

- Intra-ASEAN USD608 billion

- Ratio to GDP 104.7%

Total FDI USD122.4 billion

- Intra-ASEAN USD21.8 billion

Tourist Arrivals 89.3 million

- Intra-ASEAN 39.9 million

ASEAN – AT A GLANCE

- www. mida.gov.my - INVEST IN MALAYSIA > YOUR PROFIT CENTRE IN ASIA

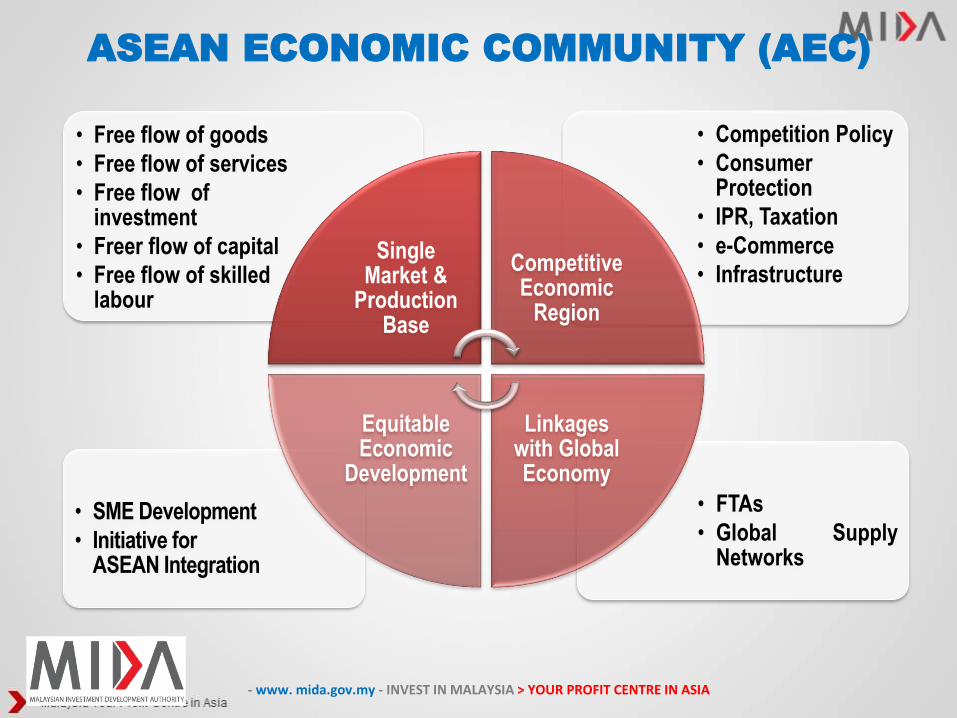

• FTAs

• Global SupplyNetworks

• SME Development

• Initiative for ASEAN Integration

• Competition Policy

• Consumer Protection

• IPR, Taxation

• e-Commerce

• Infrastructure

• Free flow of goods

• Free flow of services

• Free flow of investment

• Freer flow of capital

• Free flow of skilled labour

Single Market &

Production Base

Competitive Economic

Region

Linkages with Global Economy

Equitable Economic

Development

ASEAN ECONOMIC COMMUNITY (AEC)

- www. mida.gov.my - INVEST IN MALAYSIA > YOUR PROFIT CENTRE IN ASIA

3rd largest market in the world

Population in million

JAPAN

128

EU

502

INDIA

1,195

CHINA

1,340

USA

310

ASEAN

625

7th largest economy in the world

GDP 2013 in US$ trillion

Brazil

ASEAN

United Kingdom

France

Germany

Japan

China

United States 16.8

9.2

4.9

3.7

2.8

2.7

2.4

2.2

Fast growing economy

Real GDP Growth 2013 (%)

7.7

5.2

5.0

Japan

United States

India

ASEAN

China 7.7

5.2

5.0

2.2

1.6 Source: ASEANStat, IMF, WB

- www. mida.gov.my - INVEST IN MALAYSIA > YOUR PROFIT CENTRE IN ASIA

ASEAN: GROWING THROUGH ECONOMIC

INTEGRATION

Thank you

For more information

Visit: www.mida.gov.my

Zarina SaadDirectorMalaysian Investment Development Authority6th Floor, BürkleinhausBürkleinstraße 1080538 MunichGermanyTel: +49 89 203 0043 0Fax: +49 89 203 0043 15E-mail: [email protected]