Embed Size (px)

Citation preview

1

SANTA BARBARA COUNTY

EMPLOYEES' RETIREMENT SYSTEM

INVESTMENT GOALS,

POLICIES, AND PROCEDURES

December 8, 2009

2

TABLE OF CONTENTS Page SECTION 1 3 Purpose 4 Policies and Procedures 4 SECTION 2 6 Plan Asset Allocation and Rebalancing Guidelines 7 Plan Asset Allocation Characteristics 9 Performance Objectives 11 Table 1 - Five Year Performance Objectives 12 Table 2 - Objectives for Individual Portfolio Components 13 Proxy Voting Guidelines 14 Manager Monitoring Procedures and Probationary Criteria 21 SECTION 3 26 Manager Guidelines 27 Plan Asset Allocation Managers 28 Investment Management Guidelines and Objectives 29 SECTION 4 50 Glossary of Investment Terms 51 Indices 51 Statistical Terms 52 Other Key Terms 53

3

SECTION 1

4

Purpose This document will provide the framework for the investment management of the Santa Barbara County Employees' Retirement System (System). Specifically, it will address:

the general goals of the investment program the policies and procedures for the management of the System's assets specific investment guidelines (asset allocation) performance objectives

The philosophy incorporated herein is to allow for sufficient flexibility in the management process to capture investment opportunities as they occur, yet set forth reasonable parameters to ensure prudence and care in the execution of the investment program.

General Investment Goals The general investment goals are broad in nature to encompass the purpose of the retirement program and its investments. They articulate the philosophy by which the System will manage the assets of the retirement plan within the applicable regulatory constraints. 1. The overall goal of the System's retirement program is to provide timely and sufficient benefits to

its participants and their beneficiaries, as required under the plan, through a carefully planned and executed investment program.

2. The System seeks to produce a return on investment that is based on levels of liquidity and

investment risk that are prudent and reasonable, given prevailing capital market conditions. While the System recognizes the importance of the preservation of capital, it also adheres to the theory of capital market pricing which maintains that varying degrees of investment risk should be rewarded with compensating returns. Consequently, prudent risk-taking is justifiable.

3. The System’s investment program shall at all times comply with existing and future applicable

state and federal regulations including but not limited to the California Constitution as amended by Proposition 21.

Policies and Procedures Webster's Dictionary defines "policy" as a "plan or principle" and "procedure" as the "method" by which a task is accomplished. Together, the policies and procedures for the investment program guide its implementation and outline the specific responsibilities of the Board of Retirement ("the Board") for Santa Barbara County. Therefore, it is the policy of the Board that: 1. The investment of the assets of the System shall be based on a financial plan that will consider:

the financial condition of the retirement plan the expected long-term capital market outlook

5

the Board’s risk tolerance future growth of active and retired participants inflation and the rate of salary increase cash flow.

The financial plan measures the potential impact on pension costs of alternative investment policies in terms of risk and return based on various levels of asset diversification and the current and projected liability structure of the retirement plan.

2. Based on the financial plan, it will be the responsibility of the Board to determine the specific

allocation of the investments among the various asset classes considered prudent given the retirement plan's liability structure. The long-term allocation guidelines shall be expressed in terms of ranges for each asset class to provide sufficient flexibility to take advantage of shorter-term market opportunities as they may occur. The asset allocation, which is the System's investment structure, shall be sufficiently diversified to maintain risk at a reasonable level as determined by the Board without imprudently sacrificing return. The Board shall determine performance benchmarks against which the asset allocation plan shall be reviewed to ensure that the asset mix remains appropriate to meet the long-term goals of the retirement program. The System will review annually its current financial plan.

3. In accordance with the asset allocation guidelines the Board will select external investment

managers with demonstrated experience and expertise whose investment styles collectively will implement the planned asset allocation. The Board will set guidelines for these managers and regularly review their investment performance against stated objectives.

4. It is the responsibility of the Board to administer the investments of the System at the lowest

possible cost, being careful to avoid sacrificing quality. These costs include but are not limited to management and custodial fees, consulting fees, transaction costs and other administrative costs chargeable to the System.

The procedures to be undertaken for the investment management of the System's assets are: 1. The Board of Retirement is empowered with ultimate decision-making authority with regard to the

development and execution of the System's investment program. Only the Board in its sole discretion can delegate any portion of that decision-making authority.

2. A formal review of the System's investment structure will be conducted annually by the Board. 3. The investments of the System shall be reviewed no less than quarterly and more often as needed

to ensure that policy guidelines continue to be appropriate and are met. Performance objectives shall be determined by the Board for the total fund, each asset class and each investment manager, and the Board shall monitor investment returns on both an absolute and comparative basis. The source of information for these reviews shall come from staff, outside consultants, and investment managers.

6

SECTION 2

7

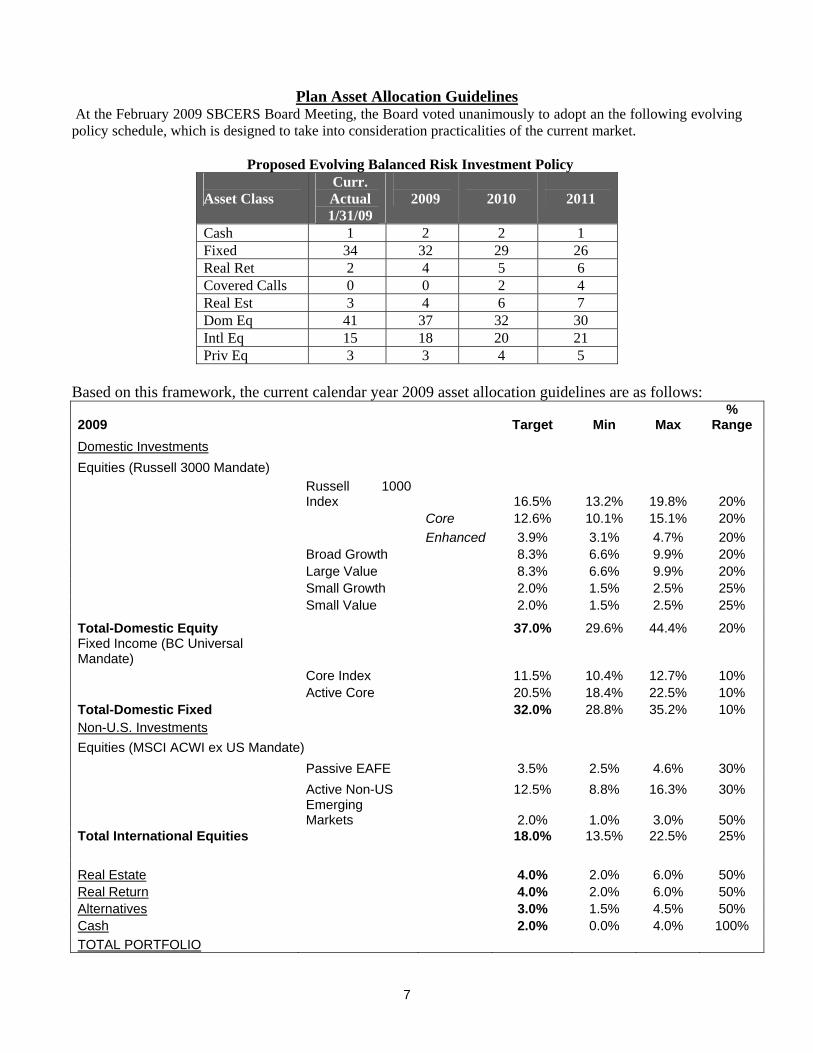

Plan Asset Allocation Guidelines At the February 2009 SBCERS Board Meeting, the Board voted unanimously to adopt an the following evolving policy schedule, which is designed to take into consideration practicalities of the current market.

Proposed Evolving Balanced Risk Investment Policy Asset Class

Curr. Actual 1/31/09

2009

2010

2011

Cash 1 2 2 1 Fixed 34 32 29 26 Real Ret 2 4 5 6 Covered Calls 0 0 2 4 Real Est 3 4 6 7 Dom Eq 41 37 32 30 Intl Eq 15 18 20 21 Priv Eq 3 3 4 5

Based on this framework, the current calendar year 2009 asset allocation guidelines are as follows:

2009 Target Min Max %

Range Domestic Investments Equities (Russell 3000 Mandate)

Russell 1000 Index 16.5% 13.2% 19.8% 20%

Core 12.6% 10.1% 15.1% 20% Enhanced 3.9% 3.1% 4.7% 20% Broad Growth 8.3% 6.6% 9.9% 20% Large Value 8.3% 6.6% 9.9% 20% Small Growth 2.0% 1.5% 2.5% 25% Small Value 2.0% 1.5% 2.5% 25%

Total-Domestic Equity 37.0% 29.6% 44.4% 20% Fixed Income (BC Universal Mandate) Core Index 11.5% 10.4% 12.7% 10% Active Core 20.5% 18.4% 22.5% 10% Total-Domestic Fixed 32.0% 28.8% 35.2% 10% Non-U.S. Investments Equities (MSCI ACWI ex US Mandate) Passive EAFE 3.5% 2.5% 4.6% 30% Active Non-US 12.5% 8.8% 16.3% 30%

Emerging Markets 2.0% 1.0% 3.0% 50%

Total International Equities 18.0% 13.5% 22.5% 25% Real Estate 4.0% 2.0% 6.0% 50% Real Return 4.0% 2.0% 6.0% 50% Alternatives 3.0% 1.5% 4.5% 50% Cash 2.0% 0.0% 4.0% 100% TOTAL PORTFOLIO

8

Portfolio Rebalancing Policy As markets move over time, the actual asset mix of the Fund’s portfolio may diverge from the target allocations established by the Board through the asset allocation process. If fund assets are allowed to deviate too far from the target allocations, there is a risk that the portfolio will fail to meet the management objectives set by the Board. On the other hand, the Board is aware that continual rebalancing of the portfolio to the asset allocation targets may result in significant transaction costs. Cognizant of these risks, the Board will rebalance the Fund portfolio in accord with the following guidelines and procedures: A. With respect to each major asset class group, asset class and subasset class for which the Board

has set a target allocation, the Board, in consultation with its staff and its investment consultant, will establish rebalancing minimum and maximum range limitations.

B. The Board and staff will monitor the portfolio’s asset allocation relative to target allocations and

ranges on a monthly basis. If the actual allocations fall within the defined ranges, no rebalancing will be required. If actual allocations for a major asset class group, an asset class or sub asset class fall outside the predetermined range, staff will develop and execute a strategy for rebalancing back to the target allocation, including the time frame for accomplishing the proposed rebalancing. Generally, rebalancing shall not occur more frequently than every three months. Each economic cycle is unique. In the event of extreme volatility, or severe downward or upward changes in market conditions, the Chief Executive Officer (CEO) shall have the delegated authority to rebalance, or hold off on rebalancing, as deemed appropriate. Such determinations shall be based on all aspects of the rebalancing issue, including all rebalancing costs. In the event that the CEO rebalances or avoids rebalancing in such extreme downward or upward market situations, the CEO shall notify the Board Chair after the rebalancing has or has not occurred and shall report to the Retirement Board at the next meeting. The CEO shall address any such conditions on a case by case basis.

C. In executing any required rebalancing, staff should prioritize implementation procedures as

follows:

1. Investing net contributions into asset classes that are below their range limitations;

2. Drawing cash flowing out of the portfolio (for benefit payments and expenses) from asset classes that are above their range limitations (using interest payments, rental revenues and dividends); and

3. Selling overweighted assets and/or buying underweighted assets.

9

Plan Asset Allocation Characteristics Equities Core - designed to track the return of the Russell 1000 Index, an index biased toward large capitalization stocks, within approximately .5% per year. The large stock core portfolio is a low-risk, broadly diversified portfolio with a market-like yield and P/E ratio. Enhanced - designed to provide small incremental returns over the Russell 1000 Index in a very risk-controlled manner. Broad Growth – designed to invest in companies that comprise the broad US equity market. Portfolio is characterized by higher risk, lower yield stocks with P/E ratios higher than the general equity market. The growth stock portfolio will display above market performance in rising markets and equal to or over market performance in down markets. Large Value - designed to outperform the market in down and flat markets, while approximating market performance in up markets. Value portfolios provide participation in companies that are undervalued relative to the market and are usually characterized by high yields and low P/E ratios. Small Growth - designed to invest in companies that reside within the smaller company segment of the US equity market. Portfolio is characterized by higher risk, lower yield stocks with P/E ratios higher than the general equity market. The small growth stock portfolio will typically display above market performance in rising markets and lower-than-market performance in down markets. Small Value - designed to invest in companies that reside within the smaller company segment of the US equity market. Expected to outperform the market in down and flat markets, while approximating market performance in up markets. Small value portfolios provide participation in smaller companies that are undervalued relative to the market and are usually characterized by high yields and low P/E ratios. Fixed Income Core Index - designed to track the return of the Barclays Universal Index. Assets are invested and reinvested with the objective of achieving a total return approximating the return of the Barclays Universal Index. Active Core – designed to produce a total return that exceeds the Barclays Universal Index. Key focus is on adjusting the maturities, sectors, quality, and coupons of a portfolio of bonds to exploit market opportunities. Average maturity 5 to 10 years. International Passive EAFE - designed to track the total return of the Morgan Stanley Europe, Australasia and Far East (EAFE) Index. This index consists of stocks in the world's major equity markets outside of North and South America. Typically it includes large capitalization companies in each market representing

10

approximately "70%" of each market. The portfolio is a broadly diversified portfolio with risk and fundamental characteristics similar to that of the EAFE benchmark. The index strategy followed provides low-cost exposure to the benchmark. International Active Equities - focus on equity securities of non-U.S. companies traded on foreign security exchanges and denominated in foreign currencies. International equities provide increased company investment opportunities as well as excellent diversification due to the counter cyclical nature of business and economic trends between the U. S. and other countries. Emerging Markets – focus on equity securities of non-U.S. companies traded on foreign security exchanges, denominated in foreign currencies, located in markets of developing economies such as Argentina, Chile, Jordan, Malaysia, Mexico, Philippines, and Thailand. Emerging markets equities increase the size of and exposure to the investable universe of foreign securities beyond those located in developed markets. Real Estate/Real Return Real Estate – focus on providing immediate protection against unexpected inflation, dampening overall portfolio volatility and providing excellent diversification from traditional capital market exposure. Provides equity participation in commercial, industrial, or residential properties and other related opportunities. Participation in this segment of the asset class might include (i) investments in funds that invest directly in real estate properties and/or (ii) investments in publicly traded Real Estate Investment Trusts (REITs) and/or Real Estate Operating Companies (REOCs). Because these latter investments trade in the public markets, they may prove to be more volatile than private real estate. Private real estate returns tend to be more stable because property values change only when they are appraised. Real Return – focus on providing investment returns that consistently exceed inflation, provide principal protection and diversify the portfolio from traditional capital market volatility exposure. Participation in this segment of the asset class might include (i) investment strategies that emphasize inflation-protected securities, (ii) asset allocation strategies that utilize a wide spectrum of asset classes including many real asset classes (e.g., commodities, natural resources, etc.), and/or (iii) other absolute return-oriented strategies. The primary purpose of the Real Return segment is to diversify and augment the Real Estate component by delivering potentially stable, inflation-protected returns. Alternative Alternative Investments - The Board may review from time to time non-traditional portfolio investments such as venture capital, options, futures, and other new investment vehicles as they become available and meet fiduciary requirements.

11

Performance Objectives

The System's performance objectives can be divided into two components: objectives for the overall fund and objectives for the individual portfolio components. Both levels of objectives will be incorporated in quarterly reviews of the System's performance. The performance objectives for the overall fund are fourfold: 1. Objective relative to asset allocation targets 2. Objective relative to financial plan assumptions 3. Objective relative to inflation 4. Objective relative to actuarial rate of interest The first objective results in a comparative index that reflects the System's unique asset allocation policy (see Table 1). Exceeding this objective indicates that the active management of the various portfolio components has added value over a passively managed fund with a similar asset mix. The second objective relates actual asset class performance to financial plan assumptions to review the ongoing asset allocation. The inflation objective requires that the investment performance provide an adequate real return over the expected rate of inflation, the primary driver of benefits and, therefore, pension costs. Lastly, the System should earn a return over the assumed actuarial interest rate of 8.16% per year. Individual portfolio components also have performance objectives reflecting the unique investment style of each category. The investment style and performance benchmarks for the five objectives stated above are shown in Table 2.

12

Table 1

Five-Year Performance Objectives at February 2009

Overall Fund Objectives

1. Relative to asset allocation targets (2009 Policy), index weighted by: 2% 90-day treasury bills 37% Russell 3000 Index 32% Barclays Universal Index 18% MSCI All Country World ex U.S. (ACWI ex-US) Index 3% Russell 3000 (lagged) 4% Real Return 4% NCREIF Real Estate Index (lagged) 100%

2. Relative to Financial Plan Assumptions: Asset Category Expected Real Rate of Return % Domestic Equity 10.00% Domestic Fixed Income 5.25% International Equity 10.00% Emerging Markets 10.00% Real Estate 4.50% Real Return 7.25% Alternatives 12.50% Cash 4.00%

3. Relative to assumed actuarial rate of interest:

Nominal Return above 8.16%

13

Table 2

Objectives for Individual Portfolio Components Domestic Investments Equities Russell 3000 Index Passive Core Return equal to Russell 1000 Index Core Russell 1000 Index annually Broad Growth 1.5% in excess of Russell 3000 Growth over market cycle Large Value 1.0% in excess of Russell 1000 Value over market cycle Small Growth 1.5% in excess of Russell 2000 Growth over market cycle Small Value 1.5% in excess of Russell 2000 Value over market cycle Fixed Income Investments Core 1.0% in excess of Barclays Aggregate Index Core Plus 1.0% in excess of Barclays Universal Index International Investments Equities MSCI ACWI ex U.S. Index Passive EAFE Return equal to MSCI-EAFE Active Non-US 1.0% in excess of MSCI-EAFE over 3-5 yr. rolling period Emerging Markets 2.5% per annum in excess of MSCI-Emerging Markets Free over 3-5 yr. rolling

period Real Estate Real Estate 1.0% per annum in excess of the NCREIF Real Estate Index Real Return Hedge Funds T-bills + 3.0% TIPS Barclays TIPS Index Alternatives Private Equity Russell 3000 + 3.0% (over period no less than 5 years)

14

Proxy Voting Policy The following criteria deal with matters considered of a financial nature only. In most cases they are general policy guidelines to voting shares held at annual and special corporation shareholder meetings. They are not designed to substitute for analysis and judgment which should be exercised as circumstances dictate. The guidelines should not be regarded as mandatory, if local factors and prudence suggest otherwise. Exceptions may be made based on the legal requirements of the countries, local conventions or states in which the company is registered. It is recognized that, in foreign markets, there may be practical difficulties in obtaining notices of company meetings and that the timeliness and disclosure requirements which prevail in the U.S. are often not evident. In those circumstances where adequate and timely disclosure of information necessary to reach an informed and meaningful decision is not possible, the responsible party may abstain. It is also recognized that the decision to abstain by the party responsible for voting the proxy may be due to practical difficulties, to other financial criteria which outweigh the benefits to be gained by voting or to practical difficulties and circumstances beyond its control. Notwithstanding any limitations, it is expected that there will be no abstentions on issues that may affect the economic value of the shareholdings. It is expected that in all cases, the parties will make a good faith effort to get the necessary materials, but it is recognized that, in foreign markets, the means for obtaining planned company meeting notices, dates and agendas, may not be readily available. Nevertheless, a true and accurate record shall be kept of how proxies have been voted or otherwise managed. It is understood that it is the intent of the Board to exercise its voting authority, either directly or through other parties, to whom it has delegated responsibility for voting proxies, according to their judgment of its best financial interest, whenever and wherever possible, and that, while logistics or other factors may sometimes interfere with this intent and principle, it is the ultimate goal of the Board to work with the indicated parties to remove the barriers to voting all shares over time. With respect to the delegation of proxy voting responsibility, the Board may authorize investment managers to vote shares in accord with this policy. The Board may also utilize the services of a proxy voting agent to assist it in the voting of shares. In the latter regard, SBCERS staff shall work with any such agent to ensure votes are cast in a manner consistent with this policy. To the extent that these guidelines do not address a particular issue, the Board delegates to the Plan Manager, the authority to direct the agent on such issues, guided by the general principles of this policy, which is directed toward maximizing shareholder value for the benefit of SBCERS’s ultimate beneficiaries.

A. Auditors

1. When there is reason to believe the company’s auditors have become complacent in the performance of their auditing duties, a vote against that auditors’ continuance may be cast.

B. Board of Directors

1. Generally, information and circumstances permitting, votes are to be cast in favor of annual election of all directors. Exceptions may be made as circumstances dictate or when pertinent information is unavailable. Once all shareholders have decided through the voting process that the board should be staggered, nominees should be elected based on their qualifications and merits, though SBCERS’s interest may argue for actions proposing the repeal of staggered terms.

15

2. Generally, votes are to be cast in favor of simple majority approval, of shares outstanding, as appropriate for merger proposals. Proposals seeking higher percentages may be approved only if approval is in the financial interest of SBCERS. Exceptions may be made when pertinent information is unavailable. For example, a proposal which sought to reduce the supermajority requirement from 80% to 66 2/3% would generally receive a favorable vote; whereas, a proposal to increase the vote required from a simple majority to a higher percentage would generally not receive a favorable vote.

3. It is concluded that corporate board members’ primary responsibilities should be to direct the companies in the interest of all the shareholders. Any proposed director qualifications should relate to a prospective director’s capacity to function on behalf of all the shareholders; to the extent that such qualifications are disclosed, votes are to be cast on this basis.

4. Generally, votes are to be cast against blanket requests for limitations of liability and

indemnification protection of directors and officers. Generally, such requests allow the protected individual to escape liability even if he or she is found by the courts to have been grossly negligent in the performance of his or her duties as a director and/or officer of the corporation. It is concluded that it is not in the best interest of shareholders to grant such protection on an across-the-board basis, Exceptions may be made as circumstances and legal requirements dictate.

a) Legal requirements and circumstances permitting, positive votes may be cast for

management sponsored proposals requesting increased indemnification of directors and officers due to damage caused by violations of the duty of care, so long as the director/officer satisfied a “good faith” standard. Broader protection may be supported, provided there is a reasonable basis for support.

b) Legal requirements and circumstances permitting, positive votes may be cast for

increased indemnification proposals where a director/officer defense is unsuccessful, unless there is a final legal/court determination that the director/officer acted in bad faith and not for a purpose that he or she could reasonably believe was in the best interest of the company. Broader protection may be supported, provided there is a reasonable basis for such support.

c) Legal requirements and circumstances permitting, votes may be cast against

company proposals that request the elimination or limitation of directors’ liability for acts evolving from negligence, or other violations of the duty of care that go beyond reasonable standards, except in markets where local conventions suggest otherwise.

5. Votes on the payment of fees to inside (or corporate) directors will be cast in consideration of

the average fee per director relative to other companies in the same industry or country. Votes are generally to be cast against proposals granting retirement benefits to outside directors, except in markets where local conventions suggest otherwise. Proposals that seek to pay outside directors’ fees in stock instead of cash will receive a positive vote. In the

16

absence of adequate or definitive information, SBCERS will cast its vote based on the surrounding circumstances and the judgment of the responsible party.

6. Generally, votes should be withheld for the entire slate of proposed directors when

management is proposing a series of defensive measures, which serve to insulate incumbent management and hinder the ability of mergers or takeovers to proceed. In the absence of adequate or definitive information, SBCERS will cast its vote based on the surrounding circumstances and the judgment of the responsible party.

7. Where director candidate(s) are employed by a company having a 20% or greater interest in

the subject company, the director candidate(s) will be considered affiliated outsiders, unless they have worked directly for the company in the past, in which case they are classified as insiders. Support shall not routinely be withheld for boards composed solely of such directors, unless relative corporate performance is markedly bad.

8. Generally, shareholder proposals requesting the board of directors to establish a nominating

committee for the selection of director candidates are to receive a favorable vote. SBCERS believes that all important review committees such as nominating, audit or compensation should be staffed by a majority of independent directors. Proposals and/or actions which seek to have such a structure established may be initiated or supported by SBCERS. In the absence of adequate or definitive information, SBCERS will cast its vote based on the surrounding circumstances and the judgment of the responsible party.

9. Proposals which seek to limit the tenure of directors should receive a negative vote.

Proposals which require directors to own a minimum amount of company stock in order to qualify as a director or to remain on the board should receive a negative vote. In the absence of adequate or definitive information, SBCERS will cast its vote based on the surrounding circumstances and the judgment of the responsible party.

C. Executive Compensation

1. Stock options and incentive compensation plans must have the overriding purpose of motivating corporate personnel. To ensure that such plans are cost and performance effective, attention should be paid to corporate performance. Exceptions may be made when pertinent information is unavailable or when legal requirements do not permit execution of this principle.

2. Votes are generally to be cast against executive incentive stock option plans if the minimum

potential dilution of all company plans, including the proposal, is more than 15% of the total outstanding voting power. This figure includes shares proposed for a new plan or amendment plus shares reserved under all existing plans, plus all shares under option but not yet exercised. Typically, no greater than 1 percent dilution per year for the life of the plan should be experienced by shareholders. Exceptions may be made when pertinent information is unavailable or when legal requirements do not permit execution of this principle.

17

3. Votes are generally to be cast against executive incentive stock option plans which would sell shares to executives at any discount to market value at the time of grant, unless a lower value may be legally offered.

4. Votes are generally to be cast against Restricted Stock Option Plans, outright stock grants or

other arrangements to such as pyramiding, stock appreciation rights and cashless exercise. Votes are generally to be cast against proposals which would allow the board to replace or reprice underwater options without shareholder approval. Exceptions may be made when pertinent information is unavailable or when legal requirements do not permit execution of this principle.

5. Executives are defined as the five most highly compensated executive officers of a company

and its subsidiaries, and such other senior-level executive and management employees who are designated to receive executive incentive compensation, apart from that which is given to general employees. Exceptions may be made when pertinent information is unavailable or when legal requirements do not permit execution of this principle.

6. It is the responsibility of the companies to clearly, understandably, and adequately explain

the plans and their effects with examples where necessary in order to fully define intent. However, where time permits, inquiry may be made about corporate proposals which are not clear. If the information available and/or obtained is not considered clear or adequate, votes cast will be based on the surrounding circumstances and the judgment of the responsible parties.

7. Generally, any attempt to create an unusually favorable compensation structure in advance of

sale of a company should be opposed; however, such proposals will be considered on a case-by-case basis.

E. Employee Compensation

1. Generally, employee stock purchase plans, savings and investment plans, or thrift plans are to receive a positive vote, so long as exercise or purchase price is not less than 85% of fair market value on the date of grant or purchase, and no loans are made for the purpose of settling payment for shares or any tax liability arising from exercise or purchase of such shares. Shares issued and reserved with respect to such plans shall only be done when necessary and for the specific uses of the plans. However, such proposals will be considered on a case-by-case basis.

Generally, ESOP’s which are funded by the debt of the corporation and/or which represent

large percentages of the outstanding shares or cause substantial dilution to ownership and voting power are to be given a careful review. In the absence of any extraordinary or beneficial (to SBCERS) circumstances, these plans should not be approved. Shareholder proposals which seek to have a vote on all such plans should receive a positive vote.

18

F. Mergers, Acquisitions, Takeovers

1. SBCERS wants all offers evaluated on its behalf, which are presented for any company in which it invests. To the extent that adequate information is available and legal requirements, and investment practices permit, defensive tactics should be opposed. Each proposal should be reviewed on its own merit, as nothing written here should be constructed as a substitute for the judgment of the responsible party. These defensive tactics may be, but are not limited to:

a) Golden parachutes. b) Poison-pill preferred. c) Lock-up options. d) Supermajority voting provision, with the exceptions noted above in Section B (2). e) Fair price or minimum price provisions. f) Unequal voting rights based on length of ownership of stock. g) Requiring that shareholders only be allowed to act at meetings rather than by

written consent. h) Requiring that all offers be approved by the company’s management and/or board

of directors before offers are submitted to shareholders.

i) Requiring that only the board of directors be allowed to increase its size, or that a

supermajority of all outstanding shares is necessary to create a larger board of directors, and allowing the board of directors to fill vacancies on the board of directors in between meetings, without shareholder approval.

j) Requiring that all directors may only be removed for cause, usually on the basis

of a supermajority vote, and that directors be allowed to fill vacancies for full terms rather than the remainder of unexpired terms.

k) Providing for a set of designated “alternate” directors to be appointed to any mid-

term vacancy. l) Requiring that the power to call a special meeting of the shareholders be vested in

the board of directors and/or the chairman exclusively, or providing that such a meeting can only be called after a demand by a supermajority of stockholders, or increasing the number of shareholders necessary to constitute a quorum at an annual or special meeting.

m) Adopting supermajority voting provisions for transactions between the target

company and an “interested shareholder.”

19

n) Requiring that the percentage vote requirement be based on all outstanding shares

entitled to vote and not on votes actually cast. o) Enacting redemption provisions where if any person owns a certain percentage of

stock pursuant to a hostile tender offer, which is opposed by the management and/or board of directors, the other shareholders have the right to have their shares redeemed by the company at a specified price.

p) Requiring the board and/or senior management to consider social, economic and

“other factors” when evaluating a bid for the company, rather than basing its decision solely on the price being offered.

q) Granting a director who is the chairman or chief executive officer a second or tie-

breaking vote. r) Reincorporating in other states solely for the purpose of seeking protection

against tender offers and takeovers. s) Issuance of new common and preferred shares and placing the issues in so called

“friendly” hands, sympathetic to management.

t) Assuming large amounts of debt which will impair the capital position of the

corporation, in order to repurchase the corporation’s stock and avoid a tender offer.

2. Each proposal will be evaluated on its merits, but if it is determined that the sole aim of the

proposal is to entrench management, and wrest authority and control from shareholders, a vote is to be cast against such proposals. However, this guideline is no substitute for the judgment of the responsible party.

3. SBCERS also opposes so-called “Omnibus Resolutions”, where management offers one item

which is beneficial to shareholders, such as anti-greenmail, and attaches a “rider” or other items such as the ones described above, which are not in the best interest of shareholders. In this situation, a vote will be cast against the entire proposal. A letter (where appropriate) to management may be written by the designated party indicating displeasure with this “lumping” and requesting that the issues be separated.

4. Generally, votes are to be cast against proposals which adopt or give the board of directors

discretionary power to adopt measures designed to deter takeover attempts or other attempts to obtain control of the corporation by making such attempts extremely financially unattractive or impossible, unless such action has received the prior approval of the shareholders of that company. However, such actions will be reviewed on a case-by-case basis, and legal requirements and circumstances will dictate SBCERS’s vote on this matter.

5. Reincorporation proposals will be examined on a case-by-case basis.

20

G. Corporate Financing Proposals

1. Authorization of increased shares shall generally be limited to that amount which may be necessary for financing within the next twelve months unless the corporation sets forth other compelling reasons. It is deemed advisable to exercise some control over authorized stock and issuance thereof to allow shareholders input on acquisitions which could change the fundamental characteristics of the company held. Support will generally be given for proposals to increase authorized shares if the proposed increase represents potential dilution of no more than 100% unless a clear need for the excess shares is presented by the company.

2. In general, all shareholder proposals on financial matters are to be given due consideration by

SBCERS and/or its advisers. It is incumbent on the companies to respond adequately to these proposals. An inadequate or casual response may affect the responsible party’s deliberation and weigh in favor of voting for the shareholder proposal.

21

Portfolio Monitoring Procedures and Criteria

Background - Why Investment Manager Monitoring Is Important

The monitoring of SBCERS’ investment managers is critical because it is part of the fiduciary responsibility of the Board on behalf of SBCERS plan participants and beneficiaries. As the fiduciary for SBCERS, the Board is responsible for determining when and whether certain factors may be detrimentally impacting an investment manager’s ability to invest on behalf of SBCERS. In cases where such factors are deemed to have an irreversible detrimental impact, the Board should have a formal mechanism for taking the appropriate action with respect to the investment manager(s) in question. The procedures and criteria below allow such a process to take place (see Section 4 for definitions of key terms used in this section). For example, one key factor might be an investment manager’s investment personnel. What happens if key investment personnel managing a portfolio on behalf of SBCERS leave the firm? Since institutional investing is (in a very strong sense) a service business, changes in personnel could significantly alter an investment manager’s ability to produce favorable long-term investment results. Another example would be deterioration of an investment portfolio’s performance versus a pre-assigned benchmark, or versus other similarly managed portfolios, which might signal a significant change in an investment manager’s style or investment process. If the change in process is, indeed, material, then an institution (such as SBCERS) that utilizes that investment manager might elect to replace that investment manager with another firm that has a process that better matches the institutional user’s original intentions/objectives. Finally, for a variety of reasons, a portfolio’s investment performance simply may not prove satisfactory (i.e., consistent and/or prolonged underperformance versus a pre-assigned benchmark). In such cases, the Board may lose confidence in the respective investment manager’s ability to add value. The monitoring procedures and criteria provide the Board with a systematic process for taking specific action(s) if such circumstances arise. How the Investment Manager Monitoring Procedures Will Work As highlighted above, ongoing monitoring of SBCERS’ investment managers is a necessary component of the Board’s fiduciary role. Specifically, these procedures allow the Board to take action if they are not satisfied with specific aspects of an investment manager’s activities and/or investment performance. In addition, investment monitoring helps an institution achieve consistent long-term investment success. These monitoring procedures are designed to take place in sequence in order to provide an ample amount of information and feedback to the Board before any significant changes are decided upon It is expect that the Board shall delegate all or a portion of these tasks to its investment consultant. The Board may review and modify investment performance criteria (in Schedule 1) or other portions of this document periodically as needed basis. There are two major groups of monitoring activities: Ongoing Monitoring and Periodic Monitoring. Both the investment manager and the Board (and/or its investment consultant) conduct certain

22

monitoring functions. A significant aspect of the Ongoing Monitoring activity is the measurement and assessment of investment performance. This procedure is described below.

Ongoing Monitoring Activities Investment Performance Review of Investment Manager(s) and its(their) Investment Portfolio(s) As part of the ongoing reporting process, the investment manager will report monthly, quarterly, and trailing annualized performance of the respective portfolio(s) to SBCERS and its consultant on an ongoing basis. In addition, the investment manager will provide performance attribution statistics (typically on a quarterly basis) that explain the causes of under- or outperformance. The investment manager will also report any changes in investment-related personnel, organization or investment approach/strategy that may potentially impact the investment results of the portfolio in question.

Independent Evaluation of Investment Performance by SBCERS SBCERS staff (and/or SBCERS’s investment consultant) will evaluate investment performance on an ongoing basis using the investment performance criteria found in Schedule 1. Such evaluations will also be used to verify investment performance information disclosed by the investment managers themselves (see above). If the investment manager(s) do(es) not meet one or more of the criteria in Schedule 1, staff will place the specific investment manager(s) on watch status for investment performance reasons and report this action to the Board at the next Board meeting. As part of the quarterly performance reporting process, investment performance evaluation will indicate (i) whether an investment manager is on watch status; (ii) the reason for watch status, (iii) the approximate date the investment manager and the respective portfolio was placed on watch status, (iv) the length the investment manager has been on watch status, and (v) additional comments. If the investment manager/portfolio was placed on watch status for investment performance reasons, the status report will also include post-watch investment performance to gauge if the investment manager is addressing investment performance issues.

Periodic Monitoring Activities As part of its ongoing fiduciary responsibilities, as well as in assessing the potential of an investment manager to produce future added value, SBCERS and its investment consultant should review several qualitative aspects of an investment manager’s management and practices. Key qualitative factors include, but are not limited to:

Review of investment manager(s) investment guidelines to ensure they are consistent with SBCERS’ mandate for the investment manager(s);

Review of the investment manager(s) investment strategy and style, especially the buy/sell disciplines;

Review of portfolio activity, specifically the turnover rate, number of holdings, and execution costs;

Risk profile relative to the portfolio’s benchmark; Review of organizational structure; Stability of investment manager personnel and organization; Review of investment manager contractual obligations to SBCERS (including

23

management fees).

As discussed in the above two sections, certain investment manager(s) may (i) fail to meet pre-established investment performance criteria and/or (ii) may prove sub-standard across any number of qualitative factors. In such cases, the next step would be for SBCERS (or SBCERS’ investment consultant) to produce a document called a Portfolio Review. This Portfolio Review would explain those factors where the investment manager(s) and/or portfolio(s) are failing to meet specific criteria and provide a basis for putting investment manager(s) on watch status. The Portfolio Review would typically be in the form of a memo to the Board.

Watch Status of an Investment Manager/Portfolio An investment manager/portfolio attains watch status if at least one of two events occurs: (i) the portfolio’s investment performance does not meet the criteria found in Schedule 1, or (ii) after the Portfolio Review is conducted, staff and/or the investment consultant recommends to the Board that an investment manager is a candidate for watch status. Under Item (i), the Board delegates to staff the authority to place a manager on watch status prior to a formal meeting with the Board. For Item (ii), the Board then approves or disapproves the recommendation contained in the Portfolio Review. Regardless of how an investment manager attains watch status, staff will issue a formal notification to the investment manager. This formal notification of watch status will include, but not be limited to, the following items:

Meeting date when the Board approved the recommendation to place the investment manager on watch;

Reason(s) for placing the investment manager on watch status; Conditions for being released from watch status (see below); and Maximum length of watch status.

Watch serves two basic purposes. First, it is a major decision step the Board takes to begin transitioning from one investment manager to an alternative investment manager. Second, it allows the investment manager on watch status time to take any corrective action (or justify its changing condition) before the Board elects to terminate its existing relationship with the investment manager. Typically, once a manager is placed on watch status, it should be able to exhibit improvement within a time frame of up to fifteen months. The Board maintains final discretion in determining the length of the watch status period.

1. A manager is placed on Watch Satus Shall appear before the Board in the month following being placed on Watch Status (or as soon thereafter as deemed practical by the SBCERS’ Board) to inform the Board in person the status of the SBCERS’ account and the managers prospects for the near and longer term, and

2. Any manager placed on Watch Satus shall be reviewed by the Investment Consultant and staff within six months after being placed on Watch.

Release from Watch Status Investment managers that show indications of an improvement, as reviewed by the investment consultant and determined by the Board, in one or more of the factors described earlier may be released

24

from watch status. Examples of improvements warranting a change in status are:

1. Improved investment performance in approximately fifteen months (or less) from the time of being placed on watch status.

2. Investment style characteristics return to, and remain at, levels originally agreed upon. 3. Qualitative factors (such as organizational structure stabilizes, personnel adjustments,

compliance requirements, etc.) are met/satisfied. To release an investment manager from watch status, the Board must formally take action to do so. This action should be supported by documentation (produced by staff and/or investment consultant) similar in format to the Portfolio Review described above. This document would highlight original reasons for the watch status and discussion of how the investment manager has addressed these issues and warrants release from watch status.

Replacement / Termination If an investment manager is not released from watch status within the appropriate period (given as up to fifteen months from the time the manager was placed on watch, with Board discretion to adjust the period), then the investment consultant should recommend that the Board replace and/or the investment manager. The Board then approves or disapproves the recommendation. To terminate and/or replace an investment manager, the Board must formally take action to do so. This action should be supported by documentation (produced by staff and/or investment consultant) similar in format to the Portfolio Review described above. This document would highlight original reasons for the watch status and discussion of continued developments during watch status that led to the termination/replacement recommendation.

25

Schedule 1

Investment Performance Criteria

Two (2) consecutive quarters is defined as six (6) months in a row; does not necessarily correspond to calendar quarter-end dates. See Addendum in Statement of Investment Policy for specific benchmark information.

1 Return discounts from a benchmark return based on 2/3 of the typical tracking error estimates of the specified type of portfolio. 2 Annualized Return is the average annual return of either the portfolio or its benchmark. 3 VRR – Value Relative Ratio – is calculated as: Portfolio Cumulative Return Relative / Benchmark Cumulative Return Relative. 4 Tracking error is a measure of the volatility of the average annual difference between the portfolio’s return and the benchmark’s return.

Asset Class

Short-term (Rolling 12 mth periods)

Medium-term (Rolling 36 mth periods)

Long-term

Active Domestic Equity Invesco (Enhanced Large) First Republic (Broad Growth) AllianceBernstein (Large Value) OFII (Small Growth) DFA (Small Value)

Portfolio Return < Benchmark Return – 3.0%1 in any quarter

Portfolio Annlzd. Return2 < Benchmark Annlzd. Return – 1.5% for 2 consecutive qtrs.

VRR3 < 0.98 For 2 consecutive quarters

Passive Domestic Equity AllianceBernstein (LargeCore)

Tracking Error4 > 0.35% in any quarter

Tracking Error > 0.20% for 2 consecutive qtrs.

Portfolio Annlzd. Return < Benchmark Annlzd. Return –0.10% for 2 consecutive qtrs.

Active International Equity Lord Abbett (Developed Markets) PanAgora (Developed Markets) Boston Company (Emerging Markets)

Portfolio Return < Benchmark Return – 4.5% in any quarter

Portfolio Annlzd. Return < Benchmark Annlzd. Return – 2.5% for 2 consecutive qtrs.

VRR < 0.98 For 2 consecutive qtrs.

Passive International Equity SSgA (Developed Markets)

Tracking Error > 0.70% in any quarter

Tracking Error > 0.40% for 2 consecutive qtrs.

Portfolio Annlzd. Return < Benchmark Annlzd. Return –0.25% for 2 consecutive qtrs.

Active Fixed Income STW (Core Fixed) Reams (Core Fixed) Artio (Core Fixed)

Portfolio Return < Benchmark Return – 1.0% in any quarter

Portfolio Annlzd. Return < Benchmark Annlzd. Return – 0.6% for 2 consecutive qtrs.

VRR < 0.99 for 2 consecutive qtrs.

Fund of Hedge Funds (Real Return)

Arden (Fund of Hedge Funds)

Portfolio Return < Benchmark Return - 3.5% in any quarter

Portfolio Annlzd. Return < Benchmark Annlzd. Return – 2.5% for 2 Consecutive qtrs.

VRR < 1.00 for 2 consecutive Qtrs.

26

SECTION 3

27

Manager Guidelines

Manager guidelines encompass two areas, 1. general guidelines applicable to all managers, and 2. specific guidelines, including performance objectives unique to each manager.

The general guidelines are:

Manager investment philosophy, style, and strategy shall remain consistent and shall not change without the express written approval of the Board of Retirement.

Sector and security selection, portfolio quality and timing of purchases and sales are delegated to the investment manager.

The following transactions are prohibited: purchase of non-negotiable securities, short sales, selling on margin, puts, calls, options, straddles, other than covered options.

Transactions that involve a broker acting as a "Principal", where such broker is also the investment manager who is making the transaction is prohibited, except where specifically approved by the Board.

Transactions shall be executed at the lowest possible cost. The use of derivative instruments (“derivatives”) such as options, futures, and other

hedging instruments for risk control purposes by the System’s investment managers is permissible subject to specified guidelines (see Investment Manager Guidelines).

28

Plan Asset Allocation Managers

To fulfill the asset allocation guidelines, the following investment managers have been selected: Domestic Investments Equities Core Russell 1000 Index AllianceBernstein Enhanced INVESCO Institutional, Inc. Broad Growth First Republic Investment Management Large Value AllianceBernstein Small Growth OFI, Inc. Small Value DFA Fixed Active Core Artio Investment Management Active Core STW Fixed Income Management Active Core Reams Asset Management International Investments Equities Passive EAFE State Street Global Advisors Active EAFE Lord Abbett PanAgora Emerging Markets The Boston Company Real Estate Private Real Estate RREEF

29

Investment Management Guidelines and Objectives For

Alliance Bernstein Institutional Investment Management

Russell 1000 Core Index Fund Definition of Manager Style AllianceBernstein will manage a Russell 1000 Index Fund which will provide equity participation in industry and market capitalization sectors approximately in proportion to their share of the market as represented by the Russell 1000 Index. The goal of the management style is to closely track the performance of the Russell 1000 Index in a portfolio with low turnover. Portfolio Characteristics

Price/earnings ratio and yield similar to the Russell 1000 Index. Diversification, as represented by an R squared of .99 or greater. Risk relative to the market as represented by beta of 1.00. Fully invested at all times, i.e., less than 5% in cash reserves. No more than 5% of the portfolio may be invested in any one issue unless the security

represents more than 5% of the market capitalization of the Russell 1000 Index. No issue shall be held in the portfolio if as a result more than 5% of the outstanding

shares of such company are held in SBCERS’s portfolio. Performance Objectives To invest and reinvest assets in the Account with the performance objective of having the investment results approximate the performance of the Russell 1000 Index within + or - 20 basis points annually. In the context of the Account's objective, it is understood that in managing the Account, the Manager will not be required to utilize customary economic, financial, market analyses or other traditional investment management techniques.

30

Investment Management Guidelines and Objectives For

INVESCO, a Division of AMVESCAP Enhanced Russell Index Fund Definition of Manager Style INVESCO will manage an enhanced equity product that is designed to: (1) outperform the Russell 1000 Index over time and (2) control risk by having a similar overall risk profile as the Russell 1000. Portfolio Characteristics The Enhanced Equity product consists of a fully-invested diversified portfolio of equities, and any temporarily uninvested cash is held in a short-term fixed income portfolio. The Enhanced Equity product uses the INVESCO proprietary Stock Selection Model to generate forecasts of excess return for each stock relative to a universe of approximately 1000 large capitalization, liquid stocks. The return forecasts are combined with risk attributes for each company, provided by BARRA’s Risk Model, in an optimizer in order to create a portfolio with the desired relative return/risk characteristics. Required rebalancing trades are implemented at as low a total transaction cost as possible. In general, the Manager will rebalance the Enhanced Equity product on a monthly basis. However, the Manager will rebalance on an intra-month basis as needed. The targeted number of holdings is 300. The annual targeted turnover is approximately 35%. The maximum over/underweight for each industry, as defined by BARRA, is .50% relative to the Russell 1000 at time of rebalance. Portfolio Guidelines The portfolio shall be comprised of cash equivalents and equity securities of companies doing business in the United States with minimum market capitalizations of $500 million. Equity securities shall be restricted to those issues listed on the New York, American, NASDAQ, or other nationally recognized United States stock exchanges. The portfolio may also contain no more than 5% unleveraged Russell 1000 Index futures for purposes of liquidity and tracking. Use of derivatives for speculation is prohibited. For prudent diversification the portfolio shall be highly diversified. Diversification will be defined in statistical terms relative to the Russell 1000 Index. The diversification objective is R-Squared, a correlation coefficient squared of 0.95 or better and a standard error of one percent per year. These statistical measures estimate the degree to which the portfolio should follow the Russell 1000 Index and the range of variation of results around the benchmark’s expected results. Performance Objectives The performance objective of the portfolio will be to generate returns of 100 basis points in excess of the total returns of the Russell 1000 index annually.

31

Investment Management Guidelines and Objectives For

First Republic Investment Management Broad Growth Definition of Manager Style First Republic Investment Management (FRIM) will manage a portfolio that will add value above a passively managed portfolio using stock selection as the principal tool. Sector rotation and reduction of equity commitment in favor of cash equivalents may be used if such strategies fit in with the manager's assessment of investment values and the market environment for equity investments in general. It is expected these companies will be medium to large firms. The goal of this management style is to equal or outperform the market as measured by the Russell 3000 Growth Index in up markets and to equal or outperform the market in down markets, in keeping with FRIM's traditional capital conservation orientation. Portfolio Characteristics

Price/earnings ratio and yield may vary, but will normally not vary from market P/E and yield of the Russell 3000 Growth Index by more than 20%.

Risk relative to the market as measured by beta, with few exceptions, will not exceed 1.5. Cash position and non-equity exposure may vary at manager's discretion. Initial position in any stock may not exceed 5% of portfolio assets. No issue shall be held in the portfolio if, as a result,

a. more than 10% of the outstanding shares of that company are held by the manager in the total of all its accounts, or,

b. more than 5% if the outstanding shares are held in SBCERS' portfolio. Performance Objectives 1. Equal or exceed Russell 3000 Growth Index in up markets, while equaling or

outperforming the same index in down markets. 2. Outperform Russell 3000 Growth by 1.5% or more over a market cycle, defined as 3 to 5

years. 3. Produce above average returns and remain in the top half of a broad manager universe, over

a market cycle defined as 3 to 5 years.

32

Investment Management Guidelines and Objectives For

Alliance Bernstein Institutional Investment Management

Large Value Definition of Manager Style AllianceBernstein Institutional Investment Management will mange a value oriented portfolio which will invest in U.S. traded stocks of companies which are undervalued relative to the market in terms of assets, normalized earnings, dividend yields and other appropriate evaluation measures. It is expected these companies generally will be larger firms with established operating records. The goal of this management style will to be to outperform the market as represented by Russell 1000 Value index. Investment Objectives On a time-weighted total return basis, investment performance is expected to exceed the Russell 1000 Value Index by 1% over a full business cycle. Investments: Issues will be listed on the New York Stock Exchange, American Stock Exchange, Regional Exchanges or Over-the-Counter markets. ADRs and International Stocks that trade on these U.S. exchanges are also allowed at a maximum of 10% of the portfolio market value in the aggregate. The active value equity style manager shall have as its guidelines an emphasis on equities producing total return through appreciation and dividend income. The manager shall have a history of consistent successful value investing. There will be a maximum of 5% cash or cash equivalents in the portfolio excluding cash held in connection with pending purchases and sales, put and call options, margin purchases, letter stock, direct or private placements, or commodities. Diversification: No more than 5% of the manger's portfolio at cost, and 8% at market value, shall be invested in any one company. No more than 25% of the portfolio at market value shall be invested in any one industry as defined by Standard & Poor’s. Capitalization Only Securities of companies with a minimum market capitalization of $600 million are permissible. Portfolio Characteristics The portfolio’s price to book will generally be lower than that of the Russell 1000 Value, the price to earnings will generally be lower than the Russell 1000 Value and the dividend yield will generally be higher than the Russell 1000 Value.

33

Reporting: Formal quarterly reporting will include an accounting statement showing portfolio income, holdings and transactions; a summary of market and portfolio activity including total return statistics; and a statement of the market outlook and investment strategy. Review Meetings: Review meetings will be held at least annually with the Board. Results as reported by the consultant in relation to objectives; organizational changes during the preceding 12 months; and a review of market and investment strategy will be presented.

34

Investment Management Guidelines and Objectives For

OFI, INC. Small Growth Definition of Manager Style OFII will manage a portfolio that will add value above a passively managed portfolio using stock selection as the principal tool. Sector rotation and reduction of equity commitment in favor of cash equivalents may be used if such strategies fit in with the manager's assessment of investment values and the market environment for equity investments in general. The portfolio is expected to hold stocks of smaller firms. The goal of this management style is to equal or outperform the small cap growth market as measured by the Russell 2000 Growth Index across all phases of a small cap market cycle. Portfolio Characteristics

Price/earnings ratio and yield may vary, but will normally not vary from market P/E and yield of the Russell 2000 Growth Index by more than 20%.

Risk relative to the Russell 2000 Growth Index as measured by beta, with few exceptions, will not exceed 1.5.

Cash position and non-equity exposure may vary at manager's discretion. Initial position in any stock may not exceed 5% of portfolio assets. No issue shall be held in the portfolio if, as a result,

a. more than 10% of the outstanding shares of that company are held by the manager in the total of all its accounts, or,

b. more than 5% if the outstanding shares are held in SBCERS' portfolio. Performance Objectives 1. Outperform the Russell 2000 Growth Index by 1.5% or more over a market cycle, defined

as 3 to 5 years. 2. Produce above average returns and remain in the top half of a small cap growth manager

universe, over a market cycle defined as 3 to 5 years.

35

Investment Management Guideline and Objectives For

Dimensional Fund Advisors (DFA) Small Value Definition of Manager Style DFA will manage a portfolio that will add value above a passively managed portfolio using quantitative screening/modeling and proprietary portfolio trading procedures as the principal tools to add value. It is expected that the portfolio will remain fully invested at all times. The portfolio is expected to hold stocks of smaller firms. The goal of this management style is to equal or outperform the small cap value market as measured by the Russell 2000 Value Index across all phases of a small cap market cycle. Portfolio Characteristics

Price/earnings ratio and yield may vary, but will normally not vary from market P/E and yield of the Russell 2000 Value Index by more than 20%.

Risk relative to the Russell 2000 Value Index as measured by beta, with few exceptions, will not exceed 1.5.

Cash position and non-equity exposure may vary at manager's discretion. Initial position in any stock may not exceed 5% of portfolio assets. No issue shall be held in the portfolio if, as a result,

a. more than 10% of the outstanding shares of that company are held by the manager in the total of all its accounts, or,

b. more than 5% if the outstanding shares are held in SBCERS' portfolio. Performance Objectives 1. Outperform the Russell 2000 Value Index by 1.5% or more over a market cycle, defined

as 3 to 5 years.

2. Produce above average returns and remain in the top half of a small cap value manager universe, over a market cycle defined as 3 to 5 years.

36

Investment Management Guidelines and Objectives For

Artio Investment Management Active Core Definition of Manager Style Artio Investment Management (JBIM) will manage a Core Plus fixed income portfolio with the goal to outperform the Barclays Universal Index using index like risk. Eligible Investments JBIM may invest in U.S. Treasuries and Agencies, U.S. and Yankee corporate bonds, Medium Term Notes, Mortgage pass-through securities (GNMA, FNMA, FHLMC, Savings & Loan, Banks, Whole Mortgages, Commercial Mortgage-Backed, REMICs), Collateralized Mortgage Obligations (CMOs), Asset-Backed Securities, 144A Securities, Preferred Stock, Convertible Securities, High-Yield securities, Municipal bonds, and non-US Dollar bonds. Short-term instruments can include U.S. Treasury and Agency issues, Certificates of Deposit and Bankers Acceptances, Repurchase Agreements, Commercial Paper, short corporate notes and Medium term notes, Asset backed securities, and US. money market funds and Bank STIFs. Portfolio Characteristics 1. The portfolio duration shall be within 33% plus or minus of the benchmark duration.

2. The credit quality of the portfolio should average single A or better. 3. Investments in any single issuer (excluding government and agency issues) may not

exceed 5% of the portfolio’s market value at the time of purchase. 4. A minimum of 70% of portfolio holdings must be rated at least Baa3 by Moody’s or

BBB- by Standard & Poor’s at the time of purchase. 5. In the event of a downgrade of an investment grade security below Baa3 or BBB-, JBIM

must notify SBCERS about the downgrade and inform of its intention to retain or sell. 6. A maximum of 25% of the portfolio may be in non-U.S. Dollar Sovereign Government

holdings at the time of purchase, including positions hedged and unhedged and any securities linked to foreign interest rates.

7. A maximum of 5% of the portfolio may be in non-currency derivatives, defined as

structured notes with a principal indexing or CMOs of the following types: lOs, inverse lOs, PRNs, inverse PRNs, and POs.

37

8. Derivatives used for substitution, risk control, and arbitrage strategies are permitted. Use

of derivatives for speculation is prohibited. For non-exchange traded derivatives, counterparty credit status shall be of the highest caliber with care taken to avoid credit guarantees extended through to parties less creditworthy than the primary counterparty in the transaction. Counterparty exposure is limited to firms with a short-term credit rating of at least A1/P1, single counterparty exposure limited to 5% of the cost value of the aggregate portfolio as well as any specific manager portfolio.

9. At no time will the use of leverage be permitted in fixed income portfolios. Performance Objectives To outperform the Barclays Universal Index with index like risk by at least 100 basis points over a full market cycle defined as 3 to 5 years.

38

Investment Management Guidelines and Objectives For

STW Fixed Income Management Active Core Definition of Manager Style STW Fixed Income Management will manage an intermediate-duration fixed-income portfolio designed to protect and increase the fund's income stream. The portfolio will be invested in undervalued market sectors and within these sectors undervalued bonds. Fully priced bonds will be traded for greater numbers of cheaper bonds. Portfolio Characteristics The goals of the fund and STW's investment style are such that the following characteristics are expected to be representative of the portfolio:

ASSET ALLOCATION - Investments will be limited to fixed-income securities and/or cash equivalents.

MATURITY - The portfolio will be invested in intermediate bonds under most markets conditions. Short term investments will typically be less than 10% of assets, but may constitute up to 40% under conditions that are believed to be extremely adverse for fixed-income investment.

DIVERSIFICATION - The number of issues held will generally be limited when quality spreads are narrow (e.g., fewer than 10). A greater number of issues will generally be held when quality spreads are wide (e.g., 25 or more).

TURNOVER - The portfolio will be aggressively managed. Turnover will vary based on market conditions and may exceed 300% annually when spreads change and/or markets are active and could be less than 50% when spread relationships are narrow and markets are inactive.

TYPES OF INVESTMENTS - The portfolios will be invested in fixed-income securities or cash equivalents including, but not limited to: Certificates of Deposits, Bankers Acceptances, commercial paper, money market funds, US Governments, US Government Agencies, corporates, municipals, mortgage passthroughs, asset-backed securities and other trusts, and sovereign and treaty obligations.

CURRENCY - All investments will be US-Dollar-denominated or fully hedged into US Dollars.

There are no security-level restrictions placed upon the portfolio either in terms of minimum, maximum or weighted average maturity, quality or coupon, so long as its structure is consistent with its restrictions, goals and objectives as stated elsewhere.

QUALITY - All bonds must be rated in the highest four broad categories (i.e., AAA, AA, A, BBB) by at least one recognized rating service except that bonds not receiving a rating may be purchased under the following circumstances:

39

o The issue is guaranteed by the US Government, its instrumentalities and/or quasi-agencies.

o Other similarly ranking debt of the issuer is rated in one of the four broad rating categories by a recognized rating service. STW must believe that, if the issue were submitted to a major rating service, it would receive a rating in one of the highest four rating categories. In this case it would be considered to have received such a rating for the purpose of these investment guidelines.

o Term commercial paper must be rated A-1 or Prime-1 (the highest rating given such investment by Moody's Investors Service and Standard & Poor's) [Bank CD and BA standards are currently under review] or believed, after diligent study, to be deserving of such rating. STW may purchase short-term investment funds approved by the corporate custodian for use in similar funds without applying these tests to each investment in such funds.

o The only bonds that may be purchased which are rated BBB or equivalent are those of regulated public utilities.

DIVERSIFICATION RESTRICTION - No more than 10% of the assets of the fund, at market value, will be purchased in the securities of any one issuer. Exceptions are US Governments, US Government Agencies, and securities which themselves represent interest in a pool of diversified investments.

CHANGES IN STATUS - If a security purchased should cease to meet these guidelines, it may be held or swapped for another security of the same issuer. The Dollar value of the holdings of that issuer may not be increased materially by additional purchases.

PERFORMANCE OBJECTIVES To produce a total return that exceeds that of an unmanaged long bond portfolio by 1% annually, measured over a trailing five-year period. STW utilizes the Barclays Aggregate Index as a proxy for the unmanaged portfolio.

40

Investment Management Guidelines and Objectives For

Reams Asset Management

Active Core Definition of Manager Style Reams Asset Management will manage a Core Plus fixed income portfolio with the goal to outperform the Barclays Universal Index using index like risk. Eligible Investments Reams Asset Management may invest in U.S. Treasuries and Agencies, U.S. and Yankee corporate bonds, Medium Term Notes, Mortgage pass-through securities (GNMA, FNMA, FHLMC, Savings & Loan, Banks, Whole Mortgages, Commercial Mortgage-Backed), Collateralized Mortgage Obligations (CMOs), Asset-Backed Securities, 144A Securities, Preferred Stock, Convertible Securities, High-Yield securities, and non-US Dollar Sovereign Government Bonds. Short-term instruments can include U.S. Treasury and Agency issues, Certificates of Deposit and Bankers Acceptances, Repurchase Agreements, Commercial Paper, short corporate notes and Medium term notes, Asset backed securities, and US. money market funds and Bank STIFs. Portfolio Characteristics 1. The portfolio duration shall be within 33% plus or minus of the benchmark duration.

2. The credit quality of the portfolio should average single A or better. 3. Investments in any single issuer (excluding government and agency issues) may not

exceed 5% of the portfolio’s market value at the time of purchase. 4. A minimum of 85% of portfolio holdings must be rated at least Baa3 by Moody’s or

BBB- by Standard & Poor’s at the time of purchase. 5. In the event of a downgrade of an investment grade security below Baa3 or BBB-, Reams

Asset Management must notify SBCERS about the downgrade and inform of its intention to retain or sell.

6. A maximum of 15% of the portfolio may be in non-U.S. Dollar Sovereign Government

holdings at the time of purchase, including positions hedged and unhedged and any securities linked to foreign interest rates.

7. A maximum of 5% of the portfolio may be in derivatives, defined as structured notes

41

with a principal indexing or CMOs of the following types: lOs, inverse lOs, PRNs, inverse PRNs, and POs.

8. Derivatives used for substitution, risk control, and arbitrage strategies are permitted. Use

of derivatives for speculation is prohibited. For non-exchange traded derivatives, counterparty credit status shall be of the highest caliber with care taken to avoid credit guarantees extended through to parties less creditworthy than the primary counterparty in the transaction. Counterparty exposure is limited to firms with a short-term credit rating of at least A1/P1, single counterparty exposure limited to 5% of the cost value of the aggregate portfolio as well as any specific manager portfolio.

9. At no time will the use of leverage be permitted in fixed income portfolios. Performance Objectives To outperform the Barclays Universal Index with index like risk by at least 100 basis points over a full market cycle defined as 3 to 5 years.

42

Investment Management Guidelines and Objectives For

State Street Bank & Trust Company Passive EAFE Definition of Manager Style State Street will manage a portfolio with an MSCI EAFE Index mandate. This portfolio will fully replicate the benchmark index and will minimize transaction costs Portfolio Characteristics Fully replicate the MSCI EAFE Index, holding 1120 securities in 20 countries. Performance Objectives To provide a rate of return which will match the return of the MSCI EAFE INDEX +/- .5% on an annualized basis.

43

Investment Management Guidelines and Objectives For

Lord Abbett

Objective: The strategy’s investment objective is to seek long-term capital appreciation and to outperform the MSCI EAFE Index over a full market cycle (3 to 5 years) (the objective to outperform the MSCI EAFE Index is a target and as such its achievement can not be guaranteed). To pursue its goal, the Investment Manager invests in a diversified portfolio of primarily equity securities of non-U.S. companies. The portfolio will diversify its investments among a number of different countries throughout the world. Lord Abbett defines U.S. securities as those that trade primarily on U.S. exchanges or markets, including the NASDAQ and are U.S. dollar-denominated, excluding ADRs. For the purposes of the Investment Guidelines, ADRs are treated as non-U.S. securities. U.S. securities are issued by companies that are incorporated in the U.S. or incorporated in off-shore jurisdictions but headquartered in the U.S. Any security that does not fit under the above definition for “U.S.” will be categorized as “non-U.S.”. These definitions will be applied at time of purchase. Parameters: The following parameters will apply. If the Investment Manager believes that varations to these Investment Guidelines are expected to persist for more than two weeks, the Investment Manager is required to discuss the variation with the Client. Compliance with these investment restrictions will be determined at the time of the purchase or sale of the security:

The Investment Manager shall seek to maintain a fully invested portfolio. The Investment Manager may invest up to 10% of the portfolio’s total net assets in cash and cash equivalents. However, if the Investment Manager determines that this allocation is a strategic decision and not a temporary situation, the Client will be notified of this determination within three days after greater than 10% of the portfolio’s net assets are invested in these instruments.

The portfolio shall be diversified to reduce the impact of losses in individual investments.

Exposure shall be to a minimum of 60 stocks quoted in at least 10 countries.