Embed Size (px)

Citation preview

Introducing Ratings Navigator for Banks

www.fitchratings.com | April 2014 2

ContactsEMEA: Gordon Scott Financial Institutions +44 20 3530 1075 [email protected]

Bridget Gandy +44 20 3530 1095 [email protected]

James Longsdon +44 20 3530 1076 [email protected]

James Watson +7 495 956 9901 [email protected]

Erwin van Lumich +34 93 323 8403 [email protected]

David Weinfurter +44 20 3530 1505 [email protected]

North America: Joo-Yung Lee +1 212-908-0560 [email protected]

Chris Wolfe +1 212-908-0771 [email protected]

Nathan Flanders +1 212-908-0827 [email protected]

Asia Pacific: Mark Young +65 6796 7229 [email protected]

Jonathan Cornish +852 2263 9901 [email protected]

Latin America: Franklin Santarelli +1 212-908-0739 [email protected]

Business and Relationship Management: David Wharrier Managing Director +44 203 530 1150 [email protected]

David Turner EMEA +44 203 530 1442 [email protected]

John Bareiss North America +1 312 368 3162 [email protected]

Kathleen Holtzman LATAM +1 212 908 9103 [email protected]

Vivek Goyall APAC +65 6796 7203 [email protected]

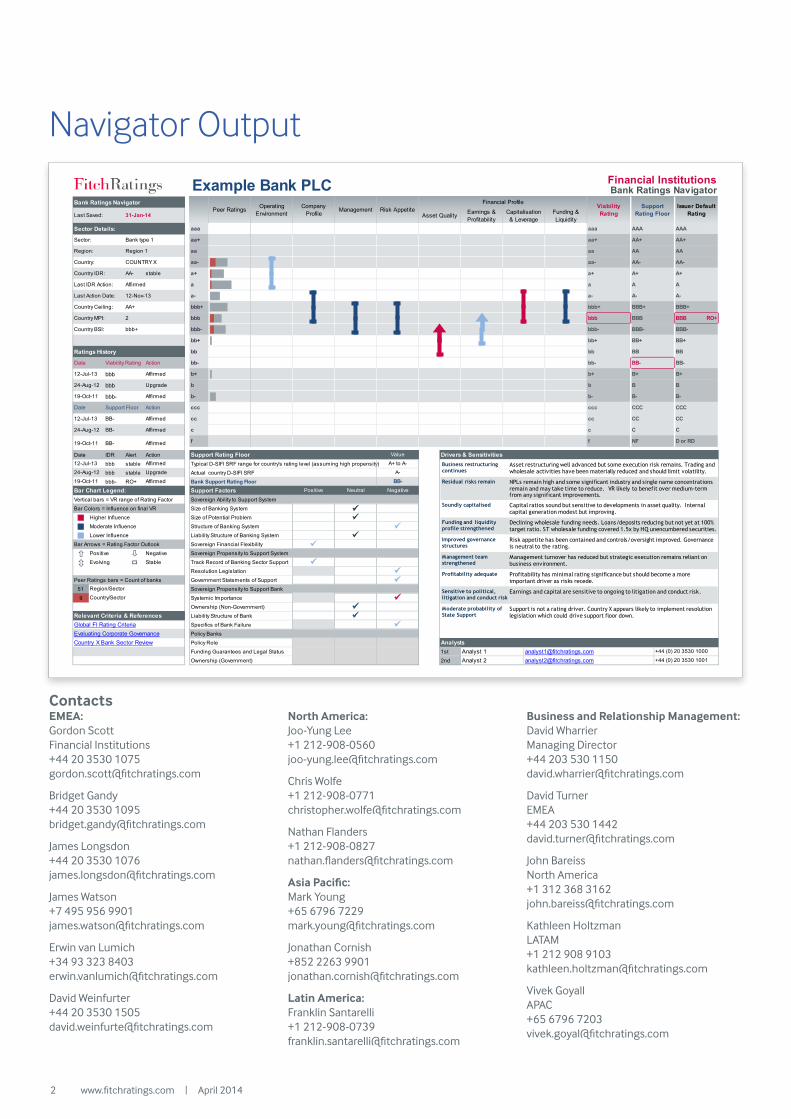

Financial InstitutionsBank Ratings Navigator

Bank Ratings Navigator

Sector Details: aaa aaa AAA AAA RO+

Sector: aa+ aa+ AA+ AA+ RO+

Region: aa aa AA AA RO+

Country: aa- aa- AA- AA- RO+

Country IDR: AA- stable a+ a+ A+ A+ RO+

Last IDR Action: a a A A RO+

Last Action Date: a- a- A- A- RO+

Country Ceiling: AA+ bbb+ bbb+ BBB+ BBB+ RO+

Country MPI: 2 bbb bbb BBB BBB RO+

Country BSI: bbb+ bbb- bbb- BBB- BBB- RO+

bb+ bb+ BB+ BB+ RO+

Ratings History bb bb BB BB RO+

Date Viability Rating Action bb- bb- BB- BB- RO+

bbb b+ b+ B+ B+ RO+

bbb b b B B RO+

bbb- b- b- B- B- RO+

Date Support Floor Action ccc ccc CCC CCC RO+

BB- cc cc CC CC RO+

BB- c c C C RO+

BB- f f NF D or RD RO+

Date IDR Alert Action Support Rating Floor Drivers & Sensitivitiesbbb stable Typical D-SIFI SRF range for country's rating level (assuming high propensity)

bbb stable Actual country D-SIFI SRF

bbb- RO+ Bank Support Rating FloorBar Chart Legend: Support FactorsVertical bars = VR range of Rating Factor Sovereign Ability to Support System

Bar Colors = Influence on final VR Size of Banking System

Higher Influence Size of Potential Problem

Moderate Influence Structure of Banking System

Lower Influence Liability Structure of Banking System

Bar Arrows = Rating Factor Outlook Sovereign Financial Flexibility

Positive Negative Sovereign Propensity to Support System

Evolving Stable Track Record of Banking Sector Support

Resolution Legislation

Peer Ratings bars = Count of banks Government Statements of Support

51 Sovereign Propensity to Support Bank

9 Systemic Importance

Ownership (Non-Government)

Relevant Criteria & References Liability Structure of Bank

Specifics of Bank Failure

Policy Banks

Policy Role AnalystsFunding Guarantees and Legal Status 1st

Ownership (Government) 2nd

Global FI Rating Criteria

Country X Bank Sector ReviewEvaluating Corporate Governance

Peer Ratings Operating Environment

BB-

Company Profile

Management

A-

A+ to A-

Value

Negative

+44 (0) 20 3530 1000

+44 (0) 20 3530 1001

Issuer Default RatingCapitalisation

& Leverage

Risk Appetite

Support Rating FloorEarnings &

ProfitabilityAsset Quality

Financial Profile Viability Rating

Region/Sector

Country/Sector

Upgrade

19-Oct-11 Affirmed

19-Oct-11

24-Aug-12

12-Jul-13

12-Jul-13

24-Aug-12 Upgrade

Affirmed

Last Saved:

19-Oct-11

31-Jan-14

12-Nov-13

Affirmed

Example Bank PLC

Positive Neutral

Funding & Liquidity

Bank type 1

12-Jul-13 Affirmed

24-Aug-12

Affirmed

COUNTRY X

Region 1

Analyst 1Analyst 2

[email protected]@fitchratings.com

Affirmed

Affirmed

Affirmed

Business restructuring continues

Asset restructuring well advanced but some execution risk remains. Trading and wholesale activities have been materially reduced and should limit volatility.

Residual risks remain

Soundly capitalised

NPLs remain high and some significant industry and single name concentrations remain and may take time to reduce. VR likely to benefit over medium-term from any significant improvements.

Capital ratios sound but sensitive to developments in asset quality. Internal capital generation modest but improving.

Funding and liquidity profile strengthened

Improved governance structures

Management team strengthened

Profitability adequate

Sensitive to political, litigation and conduct risk

Moderate probability of State Support

Declining wholesale funding needs. Loans/deposits reducing but not yet at 100% target ratio. ST wholesale funding covered 1.5x by HQ unencumbered securities.

Risk appetite has been contained and controls/oversight improved. Governance is neutral to the rating.

Management turnover has reduced but strategic execution remains reliant on business environment.

Profitability has minimal rating significance but should become a more important driver as risks recede.

Earnings and capital are sensitive to ongoing to litigation and conduct risk.

Support is not a rating driver. Country X appears likely to implement resolution legislation which could drive support floor down.

Navigator Output

3

Related Research• Global Financial Institutions Rating Criteria,

January 2014• Evaluating Corporate Governance Master Criteria,

December 2012• Rating FI Subsidiaries and Holding Companies,

August 2012• Macro Prudential risk Monitor, October 2013• Country-Specific Treatment of Re-covery ratings,

June 2013

Ratings Navigator for Banks

The Ratings Navigator provides clarity and transparency around the key drivers of bank issuer ratings.

The dashboard-style tool aims to replicate the analytical thought process and present a bank’s key rating drivers, strengths and weaknesses in a standardised format. The representation also provides clarity over the combination of different components of Fitch’s unique bank rating methodology (viability rating and support).

An example of the complete output is illustrated in Appendix 1 and 2. The remainder of this document gives guidance for each component of the dashboard.

The Financial Institutions Rating FrameworkThe analytical components of the Ratings Navigator comprise a mix of qualitative and quantitative assessments which combine to form the overall Viability Rating assessment. This is complemented by a qualitative assessment of factors that drive an analysis of support to produce an IDR that will typically reflect the ‘higher of’ approach articulated in the rating criteria. The rating framework is depicted in the rating columns (Viability/Support/IDR) which indicate how each has been assessed and typically the IDR is presented as the higher of the Viability or Support assessment.

For more detailed information on Fitch’s rating framework please refer to the January 2014 Global FI Rating Criteria.

The Ratings Navigator is a visual summary of Fitch’s Global Financial Institutions Rating Criteria. Quantitative data, such as financial and risk metrics, adds context and helps to explain ratings as opposed to determining or implying a rating directly.

This guide should be read in conjunction with Fitch’s Global Financial Institutions Rating Criteria dated 31 January 2014 which provides insight into the key rating factors and why they are important in the context of bank ratings. Where relevant this guide uses illustrative examples to explain context and importance. However such examples should not be viewed as definitive or exhaustive. Note that the Ratings Navigator does not introduce a new methodology or approach to the analysis, it is not a quantitative model. The tool simply complements the analyst thought processes and represents these in a format that aids transparency around the key credit drivers.

www.fitchratings.com | April 2014 4

How should I interpret the factor assessment values?The dashboard does not calculate a rating using the factor assessments; the overall rating will reflect the broad aggregation of the individual factor scores weighted by their relative importance. The absolute positioning of each factor score together with its relative importance provides an indication of the key rating drivers and the potential rating impact of changes to each absolute or relative assessment.

How can I work out what a particular factor assessment means?Factor definitions are provided in Fitch’s rating criteria. These detail the characteristics expected to be displayed under each factor for a given rating level.

What does ‘relative importance’ mean?All factors are deemed to be of importance in determining the rating hence the relative importance indicator is showing which factors are exerting the greatest or least influence on the final rating. In the example, ‘operating environment’, which is often considered to be a constraining factor, is imparting a low importance in the rating. Capital is a rating strength compared with asset quality which is a weak point but both are key rating drivers as shown through their relative importance.

Each rating factor assessment provides three key pieces of information:

• The absolute level assessment - depicted as a 3-notch range across the ‘aaa’ scale.

• The relative importance of the factor in determining the final rating – colour-coded to show ‘higher’ (red), ‘moderate’ (dark blue) and ‘lower’ (light blue) importance.

• An indication of future trend – using arrows to denote ‘positive’, ‘negative’, ‘stable’ (no arrows) or ‘evolving’.

Viability Rating Assessment

All factors are deemed to be of importance in determining the rating...

Viability Rating (VR)(aaa scale) Based on Stand-Alone Strength

Key rating factors:• Operating Environment• Company Profile• Management• Risk Appetite• Financial Profile

StrengthSupport Rating (SR)(1-5 scale)Based on Stronger of Institutional and Sovereign Support

Support Rating Floor (SRF)(AAA scale)Based on Sovereign Support

Key rating factors:• Sovereign’s ability to support• Sovereign’s propensity to

support banking sector• Sovereign’s propensity to

support specific FI

Long-Term Issuer Default Rating (LT IDR)(AAA scale) Based on Higher of VR and Institutional/Sovereign Support

Potential LT IDR level based on institutional (shareholder) support(AAA scale)

Key rating factors:• Parent’s ability to support• Parent’s propensity to support/

subsidiary classification• Legal and regulatory obligations/

constraints

5

Ratings Navigator for Banks

Will the relative importance be the same across all banks in a given country?No. The operating environment factor assessment will be the same for all or most banks operating in the same domestic environment. Its relative importance however will be bank-specific but may be similar across many banks. All other factor assessments will be bank-specific both in terms of the absolute level and the relative importance.

Would I expect to see several higher and lower importance factors?Not necessarily. The importance indicator is issuer-specific and it may well be the case that all or most factors are of broadly equal importance in which case all factors may be indicated as ‘moderate’. It is likely that where higher importance factors are indicated there will be others of lower importance offsetting – but not necessarily on a one-for-one basis.

How are factors that exert an extremely high influence presented?These would still be indicated as ‘higher’ (red) but the extreme element would be apparent from most, if not all, other factors being of lower importance. Examples may be the operating environment in weak emerging markets.

What does the ‘trend’ indicator tell me?The trend indicator provides Fitch’s view on the likely future direction of each individual rating factor, and the net effect should correspond to an overall rating outlook.

Note however that by directional change we mean that the 3-notch range may move in the direction of the arrow. What we are not indicating is that we expect there will be an improvement in a particular metric (eg profitability) that leaves the absolute assessment unchanged ie it is an indicator of a structural change.

So how should the combination of absolute, relative and trend indicators be interpreted?This can be illustrated using the example. The example bank is operating in a strong and stable environment that does not constrain the rating and, as such, its importance to the rating is more limited than other rating factors. As noted above, asset quality is considered the key weakness and, if it improves in line with expectations, will most likely drive an improvement in the viability rating. The ‘earnings & profitability’ assessment is borderline investment grade but expected to show structural improvement. However as it is deemed to be of lower importance in the assessment the positive trend to that factor is unlikely to be a material component of the overall positive outlook and any improvement, when it occurs is likewise unlikely to drive the overall rating upwards. Capital is perceived to be a rating strength and is mitigating weak asset quality. Other factors are considered stable and in line with the overall rating.

What does the ‘Peer Ratings’ data tell me?This graphic shows the existing viability ratings of banks classified as the same type/sector of bank (eg retail or universal commercial bank) in the same country as the rated bank (brown bars) and (silver bars) those of the same bank type in the same geographical region (eg Developed Markets Europe). The legend in the left hand sidebar also provides a count of the number of entities captured under each measure.

Bar Arrows = Rating Factor Outlook

Positive Negative

Evolving Stable

aaa

aa+

aa

aa-

a+

a

a-

bbb+

bbb

bbb-

bb+

bb

Peer Ratings

Peer Ratings bars = Count of banks

51

9

Region/Sector

Country/Sector

www.fitchratings.com | April 2014 6

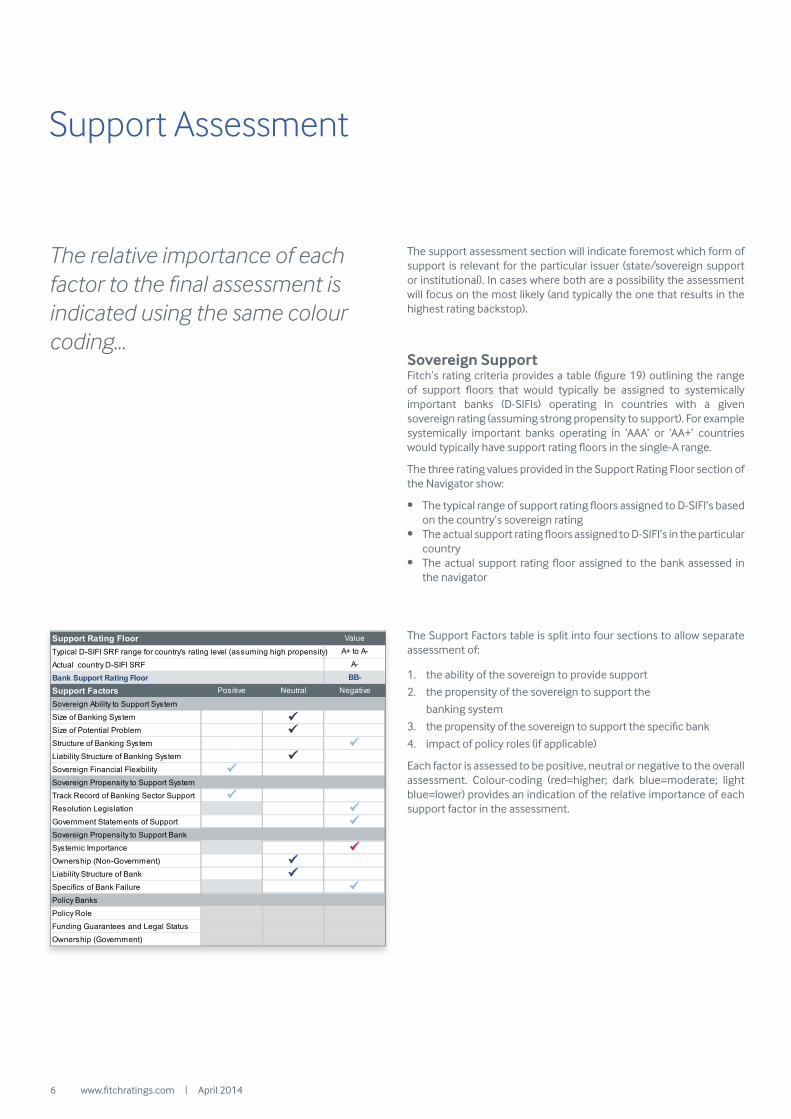

The support assessment section will indicate foremost which form of support is relevant for the particular issuer (state/sovereign support or institutional). In cases where both are a possibility the assessment will focus on the most likely (and typically the one that results in the highest rating backstop).

Sovereign SupportFitch’s rating criteria provides a table (figure 19) outlining the range of support floors that would typically be assigned to systemically important banks (D-SIFIs) operating in countries with a given sovereign rating (assuming strong propensity to support). For example systemically important banks operating in ‘AAA’ or ‘AA+’ countries would typically have support rating floors in the single-A range.

The three rating values provided in the Support Rating Floor section of the Navigator show:

• The typical range of support rating floors assigned to D-SIFI’s based on the country’s sovereign rating

• The actual support rating floors assigned to D-SIFI’s in the particular country

• The actual support rating floor assigned to the bank assessed in the navigator

The Support Factors table is split into four sections to allow separate assessment of:

1. the ability of the sovereign to provide support

2. the propensity of the sovereign to support the

banking system

3. the propensity of the sovereign to support the specific bank

4. impact of policy roles (if applicable)

Each factor is assessed to be positive, neutral or negative to the overall assessment. Colour-coding (red=higher; dark blue=moderate; light blue=lower) provides an indication of the relative importance of each support factor in the assessment.

Support Assessment

The relative importance of each factor to the final assessment is indicated using the same colour coding...

Support Rating FloorTypical D-SIFI SRF range for country's rating level (assuming high propensity)

Actual country D-SIFI SRF

Bank Support Rating FloorSupport FactorsSovereign Ability to Support System

Size of Banking System

Size of Potential Problem

Structure of Banking System

Liability Structure of Banking System

Sovereign Financial Flexibility

Sovereign Propensity to Support System

Track Record of Banking Sector Support

Resolution Legislation

Government Statements of Support

Sovereign Propensity to Support Bank

Systemic Importance

Ownership (Non-Government)

Liability Structure of Bank

Specifics of Bank Failure

Policy Banks

Policy Role

Funding Guarantees and Legal Status

Ownership (Government)

BB-

A-

A+ to A-

Value

Negative

Positive Neutral

7

Ratings Navigator for Banks

Institutional SupportParent IDR

Total Adjustments (notches)

Bank Institutional Support:Support FactorsParent Ability to Support

Relative Size

Propensity to Support: Legal / Regulatory

Legal/Regulatory obligations or barriers

Non-binding support agreements or commitments

Cross default clauses

Propensity to Support: Defining characteristics

Role in group

Potential for disposal

Implication of subsidiary default

Propensity to Support: Typical characteristics

Integration

Jurisdiction

Ownership

Support track record

Subsidiary performance and prospects

Branding

Rationale for separate legal entity

Equalised 1-2 Notches

A+0

A

Value

>2 Notches

How do I interpret the support factors table?Numbers 1 and 2 above deal with systemic factors and these should be what drive the positioning of the actual D-SIFI support rating floor in a given country within (or outside of) the typical range for its country rating. The actual D-SIFI support floor will depend on the aggregate effect of each factor assessment (positive, neutral or negative) together with their relative importance.

Numbers 3 and, if relevant, 4 above (bank specific propensity) will vary bank by bank and addresses how individual banks are perceived within the system and therefore explain any difference between the bank-specific support floor and the country’s D-SIFI support floor. In most cases the greatest differentiating factor will be systemic importance.

Will the systemic factors be the same for all banks in the same country?In most cases they will be the same as (a) there ought to be no difference in the ability of the sovereign to provide support nor (b) its willingness to support the banking system. However, the relative importance assessments of the systemic factors could vary by bank. For example, for a small bank of low systemic importance with a Support rating floor of ‘No floor’, most (if not all) systemic factors are likely to be of low importance to the ‘No floor’ SRF.

What does ‘policy role’ mean?Here we are considering additional factors that often greatly influence a state’s propensity to support ie the extent to which the bank may perform a role of policy institution, the existence of any special legal status and/or direct strategic government ownership.

Institutional Support This assessment follows similar principles in order to determine the degree of notching from the rating of the parent. The baseline is typically the parent’s IDR but in some cases (eg where the parent is itself reliant on external support) we may notch from the parent’s viability rating. Similar to the sovereign support framework, the institutional support assessment considers both ability and propensity factors in determining the appropriate notching. Propensity includes what we have referred to as ‘defining’ and ‘typical’ characteristics; defining characteristics will typically have the greatest influence on the notching decision. The relative importance of each factor to the final assessment is indicated using the same colour coding as in the sovereign support and viability rating assessments.

www.fitchratings.com | April 2014 8

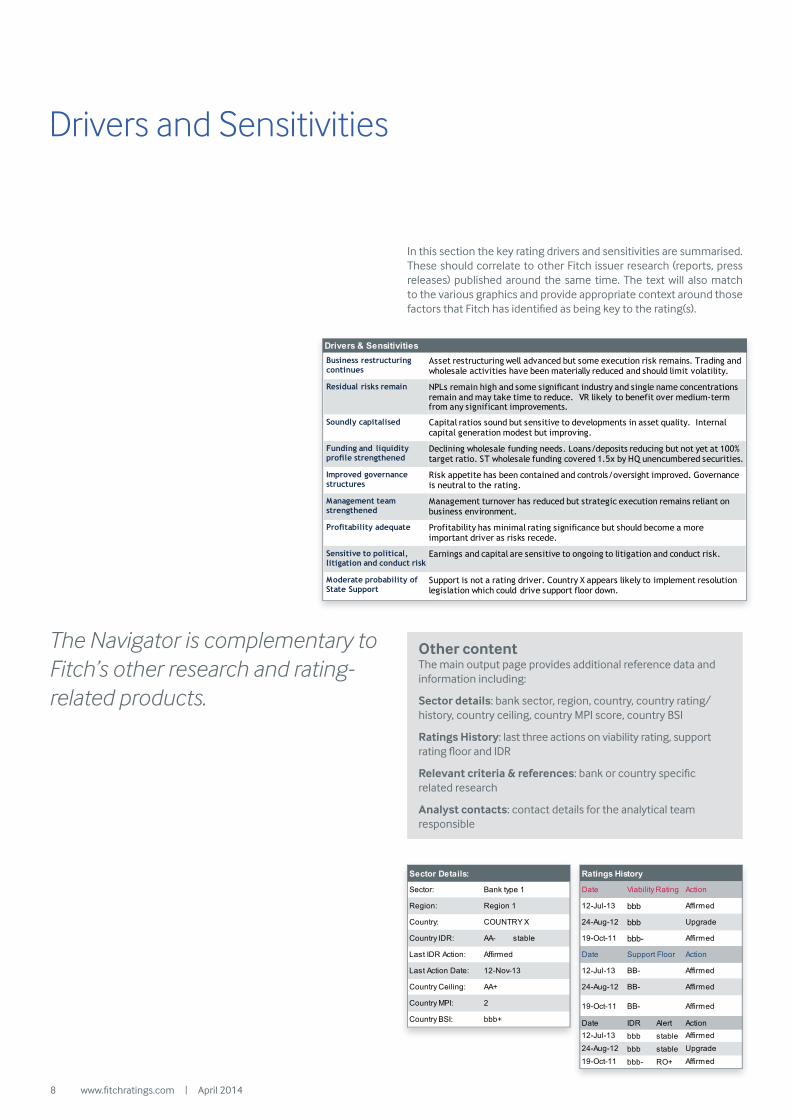

In this section the key rating drivers and sensitivities are summarised. These should correlate to other Fitch issuer research (reports, press releases) published around the same time. The text will also match to the various graphics and provide appropriate context around those factors that Fitch has identified as being key to the rating(s).

Drivers and Sensitivities

Other content The main output page provides additional reference data and information including:

Sector details: bank sector, region, country, country rating/history, country ceiling, country MPI score, country BSI

Ratings History: last three actions on viability rating, support rating floor and IDR

Relevant criteria & references: bank or country specific related research

Analyst contacts: contact details for the analytical team responsible

The Navigator is complementary to Fitch’s other research and rating-related products.

Drivers & SensitivitiesBusiness restructuring continues

Asset restructuring well advanced but some execution risk remains. Trading and wholesale activities have been materially reduced and should limit volatility.

Residual risks remain

Soundly capitalised

NPLs remain high and some significant industry and single name concentrations remain and may take time to reduce. VR likely to benefit over medium-term from any significant improvements.

Capital ratios sound but sensitive to developments in asset quality. Internal capital generation modest but improving.

Funding and liquidity profile strengthened

Improved governance structures

Management team strengthened

Profitability adequate

Sensitive to political, litigation and conduct risk

Moderate probability of State Support

Declining wholesale funding needs. Loans/deposits reducing but not yet at 100% target ratio. ST wholesale funding covered 1.5x by HQ unencumbered securities.

Risk appetite has been contained and controls/oversight improved. Governance is neutral to the rating.

Management turnover has reduced but strategic execution remains reliant on business environment.

Profitability has minimal rating significance but should become a more important driver as risks recede.

Earnings and capital are sensitive to ongoing to litigation and conduct risk.

Support is not a rating driver. Country X appears likely to implement resolution legislation which could drive support floor down.

Sector Details:

Sector:

Region:

Country:

Country IDR: AA- stable

Last IDR Action:

Last Action Date:

Country Ceiling: AA+

Country MPI: 2

Country BSI: bbb+

12-Nov-13

Bank type 1

Affirmed

COUNTRY X

Region 1

Ratings History

Date Viability Rating Action

bbb

bbb

bbb-

Date Support Floor Action

BB-

BB-

BB-

Date IDR Alert Action

bbb stable

bbb stable

bbb- RO+

Upgrade

19-Oct-11 Affirmed

19-Oct-11

24-Aug-12

12-Jul-13

12-Jul-13

24-Aug-12 Upgrade

Affirmed

19-Oct-11

Affirmed

12-Jul-13 Affirmed

24-Aug-12

Affirmed

Affirmed

Affirmed

Sector Details:

Sector:

Region:

Country:

Country IDR: AA- stable

Last IDR Action:

Last Action Date:

Country Ceiling: AA+

Country MPI: 2

Country BSI: bbb+

12-Nov-13

Bank type 1

Affirmed

COUNTRY X

Region 1

Ratings History

Date Viability Rating Action

bbb

bbb

bbb-

Date Support Floor Action

BB-

BB-

BB-

Date IDR Alert Action

bbb stable

bbb stable

bbb- RO+

Upgrade

19-Oct-11 Affirmed

19-Oct-11

24-Aug-12

12-Jul-13

12-Jul-13

24-Aug-12 Upgrade

Affirmed

19-Oct-11

Affirmed

12-Jul-13 Affirmed

24-Aug-12

Affirmed

Affirmed

Affirmed

9

Ratings Navigator for Banks

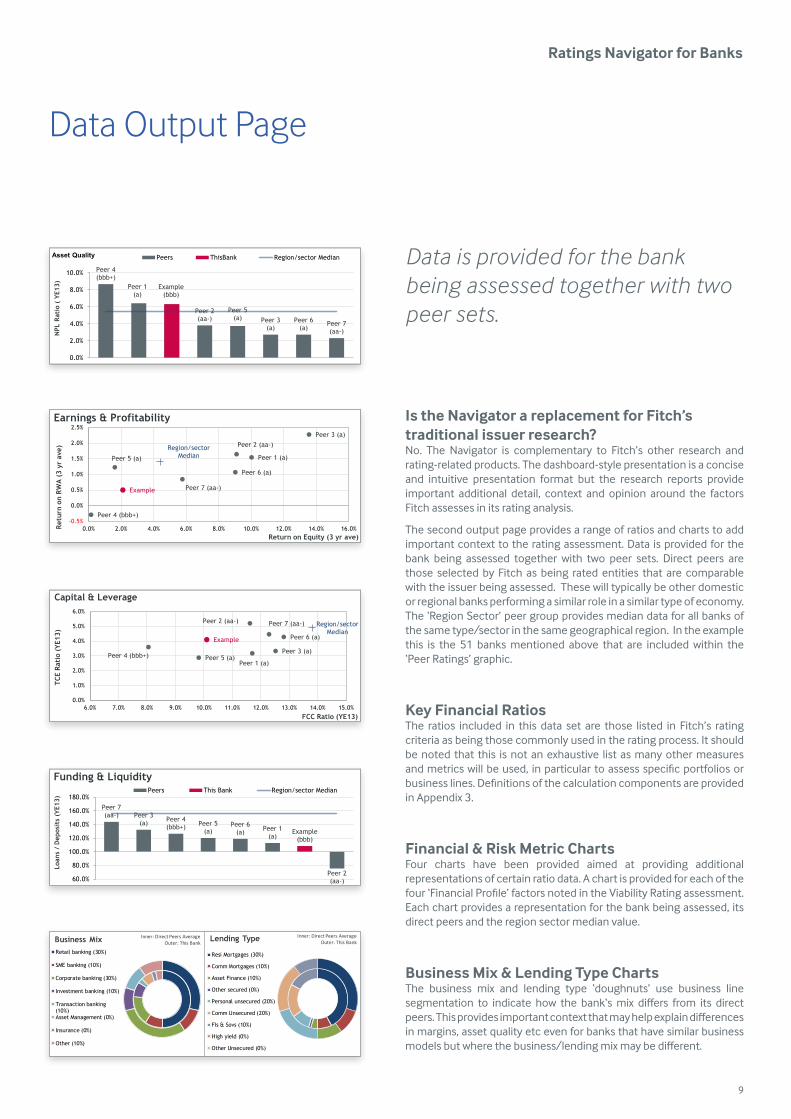

Data Output Page

Is the Navigator a replacement for Fitch’s traditional issuer research?No. The Navigator is complementary to Fitch’s other research and rating-related products. The dashboard-style presentation is a concise and intuitive presentation format but the research reports provide important additional detail, context and opinion around the factors Fitch assesses in its rating analysis.

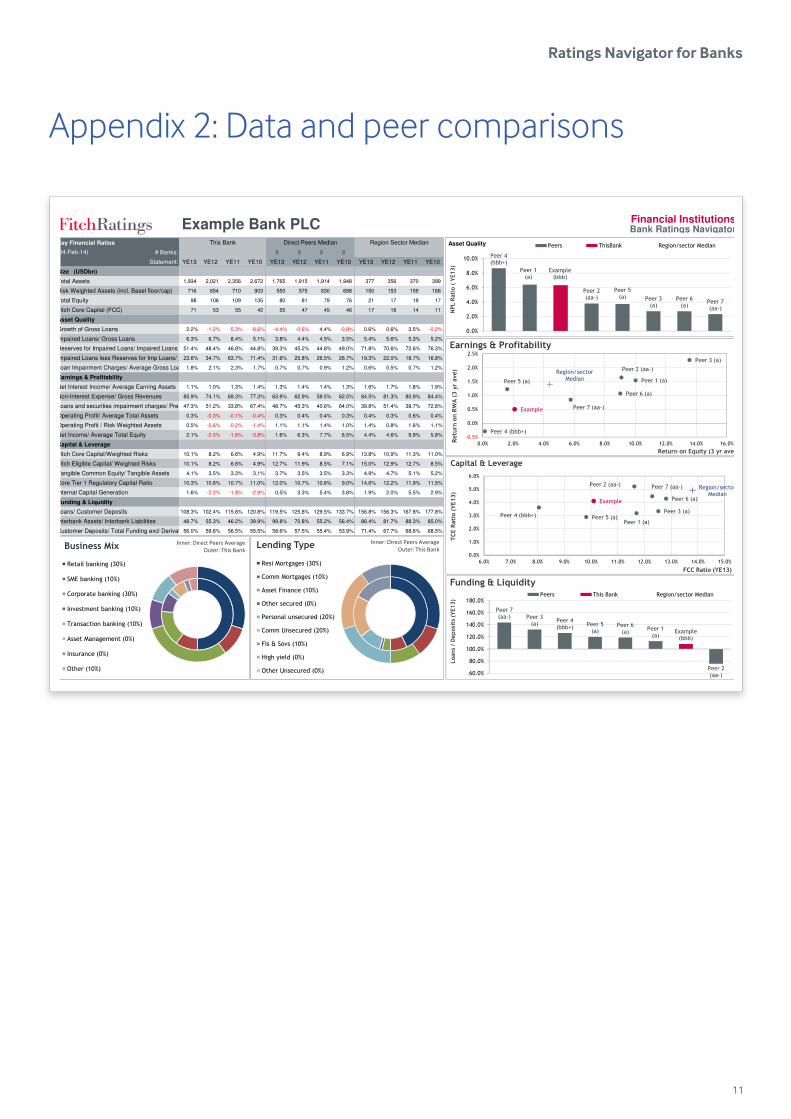

The second output page provides a range of ratios and charts to add important context to the rating assessment. Data is provided for the bank being assessed together with two peer sets. Direct peers are those selected by Fitch as being rated entities that are comparable with the issuer being assessed. These will typically be other domestic or regional banks performing a similar role in a similar type of economy. The ‘Region Sector’ peer group provides median data for all banks of the same type/sector in the same geographical region. In the example this is the 51 banks mentioned above that are included within the ‘Peer Ratings’ graphic.

Key Financial RatiosThe ratios included in this data set are those listed in Fitch’s rating criteria as being those commonly used in the rating process. It should be noted that this is not an exhaustive list as many other measures and metrics will be used, in particular to assess specific portfolios or business lines. Definitions of the calculation components are provided in Appendix 3.

Financial & Risk Metric ChartsFour charts have been provided aimed at providing additional representations of certain ratio data. A chart is provided for each of the four ‘Financial Profile’ factors noted in the Viability Rating assessment. Each chart provides a representation for the bank being assessed, its direct peers and the region sector median value.

Business Mix & Lending Type ChartsThe business mix and lending type ‘doughnuts’ use business line segmentation to indicate how the bank‘s mix differs from its direct peers. This provides important context that may help explain differences in margins, asset quality etc even for banks that have similar business models but where the business/lending mix may be different.

Data is provided for the bank being assessed together with two peer sets.

Peer 4(bbb+)

Peer 1(a)

Example (bbb)

Peer 2(aa-)

Peer 5(a) Peer 3

(a)Peer 6

(a)Peer 7(aa-)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

NPL

Rat

io (

YE1

3)

Peers ThisBank Region/sector MedianAsset Quality

Example

Region/sector Median Peer 1 (a)

Peer 2 (aa-)Peer 3 (a)

Peer 4 (bbb+)

Peer 5 (a)

Peer 6 (a)

Peer 7 (aa-)

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%Retu

rn o

n RW

A (

3 yr

ave

)

Return on Equity (3 yr ave)

Earnings & Profitability

Example

Region/sector Median

Peer 1 (a)

Peer 2 (aa-)

Peer 3 (a)Peer 4 (bbb+) Peer 5 (a)

Peer 6 (a)

Peer 7 (aa-)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

6.0% 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0% 14.0% 15.0%

TCE

Rati

o (Y

E13)

FCC Ratio (YE13)

Capital & Leverage

Peer 7(aa-) Peer 3

(a) Peer 4(bbb+) Peer 5

(a)Peer 6

(a) Peer 1(a)

Example (bbb)

Peer 2(aa-)60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

180.0%

Loan

s /

Dep

osit

s (Y

E13)

Funding & LiquidityPeers This Bank Region/sector Median

Business MixRetail banking (30%)

SME banking (10%)

Corporate banking (30%)

Investment banking (10%)

Transaction banking(10%)Asset Management (0%)

Insurance (0%)

Other (10%)

Inner: Direct Peers AverageOuter: This Bank

Lending Type

Resi Mortgages (30%)

Comm Mortgages (10%)

Asset Finance (10%)

Other secured (0%)

Personal unsecured (20%)

Comm Unsecured (20%)

FIs & Sovs (10%)

High yield (0%)

Other Unsecured (0%)

Inner: Direct Peers AverageOuter: This Bank

www.fitchratings.com | April 2014 10

Financial InstitutionsBank Ratings Navigator

Bank Ratings Navigator

Sector Details: aaa aaa AAA AAA RO+

Sector: aa+ aa+ AA+ AA+ RO+

Region: aa aa AA AA RO+

Country: aa- aa- AA- AA- RO+

Country IDR: AA- stable a+ a+ A+ A+ RO+

Last IDR Action: a a A A RO+

Last Action Date: a- a- A- A- RO+

Country Ceiling: AA+ bbb+ bbb+ BBB+ BBB+ RO+

Country MPI: 2 bbb bbb BBB BBB RO+

Country BSI: bbb+ bbb- bbb- BBB- BBB- RO+

bb+ bb+ BB+ BB+ RO+

Ratings History bb bb BB BB RO+

Date Viability Rating Action bb- bb- BB- BB- RO+

bbb b+ b+ B+ B+ RO+

bbb b b B B RO+

bbb- b- b- B- B- RO+

Date Support Floor Action ccc ccc CCC CCC RO+

BB- cc cc CC CC RO+

BB- c c C C RO+

BB- f f NF D or RD RO+

Date IDR Alert Action Support Rating Floor Drivers & Sensitivitiesbbb stable Typical D-SIFI SRF range for country's rating level (assuming high propensity)

bbb stable Actual country D-SIFI SRF

bbb- RO+ Bank Support Rating FloorBar Chart Legend: Support FactorsVertical bars = VR range of Rating Factor Sovereign Ability to Support System

Bar Colors = Influence on final VR Size of Banking System

Higher Influence Size of Potential Problem

Moderate Influence Structure of Banking System

Lower Influence Liability Structure of Banking System

Bar Arrows = Rating Factor Outlook Sovereign Financial Flexibility

Positive Negative Sovereign Propensity to Support System

Evolving Stable Track Record of Banking Sector Support

Resolution Legislation

Peer Ratings bars = Count of banks Government Statements of Support

51 Sovereign Propensity to Support Bank

9 Systemic Importance

Ownership (Non-Government)

Relevant Criteria & References Liability Structure of Bank

Specifics of Bank Failure

Policy Banks

Policy Role AnalystsFunding Guarantees and Legal Status 1st

Ownership (Government) 2nd

Global FI Rating Criteria

Country X Bank Sector ReviewEvaluating Corporate Governance

Peer Ratings Operating Environment

BB-

Company Profile

Management

A-

A+ to A-

Value

Negative

+44 (0) 20 3530 1000

+44 (0) 20 3530 1001

Issuer Default RatingCapitalisation

& Leverage

Risk Appetite

Support Rating FloorEarnings &

ProfitabilityAsset Quality

Financial Profile Viability Rating

Region/Sector

Country/Sector

Upgrade

19-Oct-11 Affirmed

19-Oct-11

24-Aug-12

12-Jul-13

12-Jul-13

24-Aug-12 Upgrade

Affirmed

Last Saved:

19-Oct-11

31-Jan-14

12-Nov-13

Affirmed

Example Bank PLC

Positive Neutral

Funding & Liquidity

Bank type 1

12-Jul-13 Affirmed

24-Aug-12

Affirmed

COUNTRY X

Region 1

Analyst 1Analyst 2

[email protected]@fitchratings.com

Affirmed

Affirmed

Affirmed

Business restructuring continues

Asset restructuring well advanced but some execution risk remains. Trading and wholesale activities have been materially reduced and should limit volatility.

Residual risks remain

Soundly capitalised

NPLs remain high and some significant industry and single name concentrations remain and may take time to reduce. VR likely to benefit over medium-term from any significant improvements.

Capital ratios sound but sensitive to developments in asset quality. Internal capital generation modest but improving.

Funding and liquidity profile strengthened

Improved governance structures

Management team strengthened

Profitability adequate

Sensitive to political, litigation and conduct risk

Moderate probability of State Support

Declining wholesale funding needs. Loans/deposits reducing but not yet at 100% target ratio. ST wholesale funding covered 1.5x by HQ unencumbered securities.

Risk appetite has been contained and controls/oversight improved. Governance is neutral to the rating.

Management turnover has reduced but strategic execution remains reliant on business environment.

Profitability has minimal rating significance but should become a more important driver as risks recede.

Earnings and capital are sensitive to ongoing to litigation and conduct risk.

Support is not a rating driver. Country X appears likely to implement resolution legislation which could drive support floor down.

Appendix 1: Rating analytics and rationale

11

Ratings Navigator for Banks

Financial InstitutionsBank Ratings Navigator

Key Financial Ratios

# Banks: 8 8 8 8

Statement: YE13 YE12 YE11 YE10 YE13 YE12 YE11 YE10 YE13 YE12 YE11 YE10

Size (USDbn)

Total Assets 1,934 2,021 2,356 2,672 1,765 1,915 1,914 1,948 377 356 370 399

Risk Weighted Assets (incl. Basel floor/cap) 716 654 710 903 550 575 630 698 150 153 159 166

Total Equity 98 106 109 135 80 81 79 76 21 17 19 17

Fitch Core Capital (FCC) 71 53 55 42 55 47 45 46 17 16 14 11

Asset Quality

Growth of Gross Loans 2.2% -1.2% -5.3% -8.6% -4.4% -0.6% 4.4% -0.9% 0.6% 0.6% 3.5% -0.2%

Impaired Loans/ Gross Loans 6.3% 6.7% 8.4% 5.1% 3.8% 4.4% 4.5% 3.5% 5.4% 5.6% 5.3% 5.2%

Reserves for Impaired Loans/ Impaired Loans 51.4% 48.4% 46.8% 44.8% 39.3% 45.2% 44.8% 49.0% 71.8% 70.6% 72.6% 76.3%

Impaired Loans less Reserves for Imp Loans/ Fitch Core Capital23.6% 34.7% 63.7% 71.4% 31.6% 25.8% 26.5% 26.7% 19.3% 22.0% 18.7% 16.8%

Loan Impairment Charges/ Average Gross Loans1.8% 2.1% 2.3% 1.7% 0.7% 0.7% 0.9% 1.2% 0.6% 0.5% 0.7% 1.2%

Earnings & Profitability

Net Interest Income/ Average Earning Assets 1.1% 1.0% 1.3% 1.4% 1.3% 1.4% 1.4% 1.3% 1.6% 1.7% 1.8% 1.9%

Non-Interest Expense/ Gross Revenues 85.9% 74.1% 69.3% 77.3% 63.9% 62.9% 59.5% 62.5% 84.5% 81.3% 80.9% 84.4%

Loans and securities impairment charges/ Pre-impairment Op. Profit47.3% 51.2% 33.8% 67.4% 48.7% 45.3% 40.6% 64.0% 39.8% 51.4% 38.7% 72.8%

Operating Profit/ Average Total Assets 0.3% -0.3% -0.1% -0.4% 0.3% 0.4% 0.4% 0.3% 0.4% 0.3% 0.6% 0.4%

Operating Profit / Risk Weighted Assets 0.5% -0.6% -0.2% -1.4% 1.1% 1.1% 1.4% 1.0% 1.4% 0.8% 1.6% 1.1%

Net Income/ Average Total Equity 2.1% -2.0% -1.6% -3.8% 1.6% 6.3% 7.7% 6.5% 4.4% 4.6% 9.9% 5.8%

Capital & Leverage

Fitch Core Capital/Weighted Risks 10.1% 8.2% 6.6% 4.9% 11.7% 9.4% 8.9% 6.9% 13.8% 10.9% 11.3% 11.0%

Fitch Eligible Capital/ Weighted Risks 10.1% 8.2% 6.6% 4.9% 12.7% 11.9% 8.5% 7.1% 15.0% 12.9% 12.7% 8.5%

Tangible Common Equity/ Tangible Assets 4.1% 3.5% 3.3% 3.1% 3.7% 3.5% 3.5% 3.3% 4.9% 4.7% 5.1% 5.2%

Core Tier 1 Regulatory Capital Ratio 10.3% 10.6% 10.7% 11.0% 12.0% 10.7% 10.6% 9.0% 14.6% 12.2% 11.9% 11.5%

Internal Capital Generation 1.6% -2.2% -1.8% -2.9% 0.5% 3.3% 5.4% 3.8% 1.9% 2.0% 5.5% 2.9%

Funding & Liquidity

Loans/ Customer Deposits 108.3% 102.4% 115.6% 120.8% 119.5% 125.8% 129.5% 133.7% 156.8% 156.3% 167.8% 177.8%

Interbank Assets/ Interbank Liabilities 48.7% 55.3% 46.2% 39.9% 99.8% 70.8% 55.2% 56.4% 86.4% 81.7% 88.3% 85.0%

Customer Deposits/ Total Funding excl Derivatives56.0% 59.6% 56.5% 55.5% 58.6% 57.5% 55.4% 53.9% 71.4% 67.7% 68.6% 68.5%

(04-Feb-14)

Example Bank PLCDirect Peers MedianThis Bank Region Sector Median

Inner: Direct Peers AverageOuter: This Bank

Inner: Direct Peers AverageOuter: This Bank

Asset Quality

Appendix 2: Data and peer comparisons

www.fitchratings.com | April 2014 12

Appendix 3: Ratio reconciliation

Navigator Ratio Name FDR Line FDR Ratio Name Formula Description (components and FDR line references)

Size

Total Assets 235000 11. Total Assets

15. Total Earning Assets +1. Cash and Due From Banks +3. Foreclosed Real Estate +4. Fixed Assets +5. Goodwill +6. Other Intangibles +8. Deferred Tax Assets +9. Discontinued Operations +10. Other Assets +7. Current Tax Assets

Risk Weighted Assets (incl. Basel floor/cap)

2170000Risk Weighted Assets including floor/cap per Basel II

Risk Weighted Assets including floor/cap per Basel II

Total Equity 284000 6. Total Equity

1. Common Equity +2. Non-controlling Interest +3. Securities Revaluation Reserves +4. Foreign Exchange Revaluation Reserves +5. Fixed Asset Revaluations and Other Accumulated OCI

Fitch Core Capital (FCC) 965500 9. Fitch Core Capital

(1. Total Equity as reported (including non-controlling interests) +2. Fair value effect incl in own debt/borrowings at fv on the B/S- CC only) -(3. Non-loss-absorbing non-controlling interests +4. Goodwill +5. Other intangibles +6. Deferred tax assets deduction +7. Net asset value of insurance subsidiaries +8. First loss tranches of off-balance sheet securitizations)

Asset Quality

Growth of Gross Loans 919500 2. Growth of Gross Loans

((8. Gross Loans -Reverse repurchase agreements included in loans) -( 8. Gross Loans Year End(s) Ago) - (Reverse repurchase agreements included in loans Year End(s) Ago)) /(( (8. Gross Loans Year End(s) Ago) - (Reverse repurchase agreements included in loans Year End(s) Ago))

Impaired Loans/ Gross Loans 920000 3. Impaired Loans/ Total Gross Loans(9. Memo: Impaired Loans included above) /(8. Gross Loans -Reverse repurchase agreements included in loans)

Reserves for Impaired Loans/ Impaired Loans

9210005. Reserves for Impaired Loans/ Impaired Loans

(6. Less: Reserves for Impaired Loans/ NPLs) /(9. Memo: Impaired Loans included above)

Impaired Loans less Reserves for Imp Loans/ Fitch Core Capital

9212506. Impaired Loans less Reserves for Imp Loans/ Fitch Core Capital

(9. Memo: Impaired Loans included above - 6. Less: Reserves for Impaired Loans/ NPLs) / 9. Fitch Core Capital

Loan Impairment Charges/ Average Gross Loans

9220008. Loan Impairment Charges/ Average Gross Loans

(21. Loan Impairment Charge) /(Average Loans -Average Reverse repurchase agreements included in loans)

Earnings & ProfitabilityNet Interest Income/ Average Earning Assets

9050005. Net Interest Income/ Average Earning Assets

(8. Net Interest Income) /(Average Earning Assets)

Non-Interest Expense/ Gross Revenues

9070002. Non-Interest Expense/ Gross Revenues

(18. Total Non-Interest Expenses) /((15. Total Non-Interest Operating Income +8. Net Interest Income))

Loans and securities impairment charges/ Pre-impairment Op. Profit

9085006. Loans and securities impairment charges/ Pre-impairment Op. Profit

(21. Loan Impairment Charge +22. Securities and Other Credit Impairment Charges) /(20. Pre-Impairment Operating Profit)

Operating Profit/ Average Total Assets

9095008. Operating Profit/ Average Total Assets

(23. Operating Profit) /(Average Assets)

Operating Profit / Risk Weighted Assets

91040011. Operating Profit / Risk Weighted Assets

(23. Operating Profit) /(Risk Weighted Assets including floor/cap per Basel II)

Net Income/ Average Total Equity 911000 1. Net Income/ Average Total Equity (Net Income/ Average Total Equity)

Capital & Leverage

Fitch Core Capital/Weighted Risks 914000 1. Fitch Core Capital/Weighted Risks(9. Fitch Core Capital) /(Risk Weighted Assets including floor/cap per Basel II)

Fitch Eligible Capital/ Weighted Risks

9142002. Fitch Eligible Capital/ Weighted Risks

(9. Memo: Fitch Eligible Capital) /(10. Fitch Adjusted Weighted Risks)

Tangible Common Equity/ Tangible Assets

9145003. Tangible Common Equity/ Tangible Assets

(6. Total Equity -5. Goodwill -6. Other Intangibles -Deferred Tax Assets to be Deducted from Core Capital) /(11. Total Assets -5. Goodwill -6. Other Intangibles -Deferred Tax Assets to be Deducted from Core Capital)

Core Tier 1 Regulatory Capital Ratio

915700 6. Core Tier 1 Regulatory Capital Ratio Core Tier 1 Regulatory Capital Ratio

Internal Capital Generation 918000 11. Internal Capital Generation

(32. Net Income -40. Memo: Common Dividends Relating to the Period -41. Memo: Preferred Dividends Related to the Period) /(6. Total Equity)

Funding & Liquidity

Loans/ Customer Deposits 924500 1. Loans/ Customer Deposits

(8. Gross Loans -Reverse repurchase agreements included in loans) /(4. Total Customer Deposits -Repurchase agreements included in customer deposits)

Interbank Assets/ Interbank Liabilities

9250002. Interbank Assets/ Interbank Liabilities

(1. Loans and Advances to Banks -Reverse repurchase agreements included in loans and advances to banks) /(5. Deposits from Banks -Repurchase agreements included in deposits from banks)

Customer Deposits/ Total Funding excl Derivatives

9255003. Customer Deposits/ Total Funding excl Derivatives

(4. Total Customer Deposits) /(15. Total Funding -13. Derivatives)

13

Ratings Navigator for Banks

Disclaimer

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTP://FITCHRATINGS.COM/UNDERSTANDINGCREDITRATINGS. IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY'S FREE WEB SITE AT WWW.FITCHRATINGS.COM. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. FITCH'S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, AFFILIATE FIREWALL, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT SECTION OF THIS SITE. FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO THE RATED ENTITY OR ITS RELATED THIRD PARTIES. DETAILS OF THIS SERVICE FOR RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE. Copyright © 2014 by Fitch, Inc., Fitch Ratings Ltd. and its subsidiaries. 33 Whitehall Street, New York, NY 10004. Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Fitch Australia Pty Ltd holds an Australian financial services licence (AFS licence no. 337123) which authorises it to provide credit ratings to wholesale clients only. Credit ratings information published by Fitch is not intended to be used by persons who are retail clients within the meaning of the Corporations Act 2001. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. In issuing and maintaining its ratings, Fitch relies on factual information it receives from issuers and underwriters and from other sources Fitch believes to be credible. Fitch conducts a reasonable investigation of the factual information relied upon by it in accordance with its ratings methodology, and obtains reasonable verification of that information from independent sources, to the extent such sources are available for a given security or in a given jurisdiction. The manner of Fitch's factual investigation and the scope of the third-party verification it obtains will vary depending on the nature of the rated security and its issuer, the requirements and practices in the jurisdiction in which the rated security is offered and sold and/or the issuer is located, the availability and nature of relevant public information, access to the management of the issuer and its advisers, the availability of pre-existing third-party verifications such as audit reports, agreed-upon procedures letters, appraisals, actuarial reports, engineering reports, legal opinions and other reports provided by third parties, the availability of independent and competent third-party verification sources with respect to the particular security or in the particular jurisdiction of the issuer, and a variety of other factors. Users of Fitch's ratings should understand that neither an enhanced factual investigation nor any third-party verification can ensure that all of the information Fitch relies on in connection with a rating will be accurate and complete. Ultimately, the issuer and its advisers are responsible for the accuracy of the information they provide to Fitch and to the market in offering documents and other reports. In issuing its ratings Fitch must rely on the work of experts, including independent auditors with respect to financial statements and attorneys with respect to legal and tax matters. Further, ratings are inherently forward-looking and embody assumptions and predictions about future events that by their nature cannot be verified as facts. As a result, despite any verification of current facts, ratings can be affected by future events or conditions that were not anticipated at the time a rating was issued or affirmed. The information in this report is provided "as is" without any representation or warranty of any kind. A Fitch rating is an opinion as to the creditworthiness of a security. This opinion is based on established criteria and methodologies that Fitch is continuously evaluating and updating. Therefore, ratings are the collective work product of Fitch and no individual, or group of individuals, is solely responsible for a rating. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. Fitch is not engaged in the offer or sale of any security. All Fitch reports have shared authorship. Individuals identified in a Fitch report were involved in, but are not solely responsible for, the opinions stated therein. The individuals are named for contact purposes only. A report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed or withdrawn at anytime for any reason in the sole discretion of Fitch. Fitch does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. Fitch receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from US$1,000 to US$750,000 (or the applicable currency equivalent) per issue. In certain cases, Fitch will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor, for a single annual fee. Such fees are expected to vary from US$10,000 to US$1,500,000 (or the applicable currency equivalent). The assignment, publication, or dissemination of a rating by Fitch shall not constitute a consent by Fitch to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of the United Kingdom, or the securities laws of any particular jurisdiction. Due to the relative efficiency of electronic publishing and distribution. 140028

New York33 Whitehall Street, New York, NY 10004 +1 212 908 0500 +1 800 75 FITCH

London30 North Colonnade Canary Wharf London E14 5GN +44 20 3530 1000

Fitch GroupFitch Ratings www.fitchratings.com

Fitch Solutions www.fitchsolutions.com