Embed Size (px)

Citation preview

www.ceep.cas.cn

BingYue Liu

Department of Statistics and FinanceUniversity of Science and Technology of China

June 18-21, Singapore

Interval Tests for Structural Breaks in the Dependence:

Empirical Evidence of Oil and Gold Markets

40th IAEE International Conference

www.ceep.cas.cn

Interval Tests for Structural Breaks

Introduction

Crude Oil

•Important commodity

•Large trading volume

•Low price

Gold•Important precious metal

•Hedge heaven

Co-movement•Positive

•Dynamic

Guidance•Investment portfolio

•Risk management

2

www.ceep.cas.cn

Literature

Baffes (2007), Hammoudeh and Yuan (2008), Soytas et al.

(2009), Sari et al. (2010), Narayan et al. (2010), Zhang and Wei

(2010), Reboredo (2013)•Method

Static relationship

Linear relationship

•Conclusion

Short-term or long-term relationship

Causal relationship

But•Market volatility

•Market mechanism change under extreme market shock

Structural (Large) change in dependence

3

Interval Tests for Structural Breaks

www.ceep.cas.cn

Contribution

Apply TVCopula to analyze dependence of oil & gold•Nonlinear

•Dynamic

•Small change in dependence

Change point test to analyze dependence of oil & gold•Large change in dependence

•But

Extreme shocks last not long

Hardly capture the dependent features in extreme risk period

Propose change interval test•Capture the dependent features in an extreme period

•Test the effect of extreme shocks on the co-movement across markets

•Empirical evidence of crude oil and gold markets

4

Interval Tests for Structural Breaks

www.ceep.cas.cn 5

Interval Tests for Structural Breaks

0 t1 t2 t3 t4 t5 T

Dependent

Rela

tionship

Comparision between Change Point and Change Interval

www.ceep.cas.cn 6

Interval Tests for Structural Breaks

www.ceep.cas.cn 7

Interval Tests for Structural Breaks

, , 1

1

ˆ arg max log | ;i

T

i i t i t t i

t

f x

F , 1, 2i , and then 1, 2, 1

1

ˆ ˆ ˆarg max log , | ;T

t t t t

t

c u u

F

1 2ˆ ˆ ˆ ˆ, ,IFM

1

0 0ˆ 0,IFMT N G

www.ceep.cas.cn

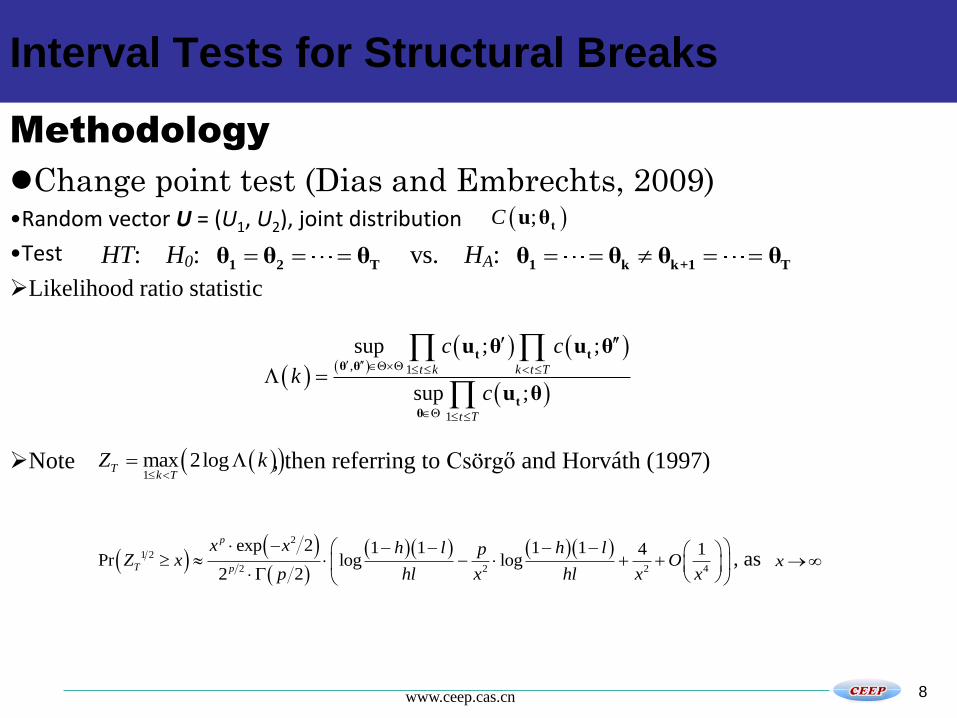

Methodology

Change point test (Dias and Embrechts, 2009)•Random vector U = (U1, U2), joint distribution

•Test

Likelihood ratio statistic

Note , then referring to Csörgő and Horváth (1997)

8

Interval Tests for Structural Breaks

;Ct

u θ

HT: H0: 1 2 Tθ θ θ vs. HA:

1 k k+1 Tθ θ θ θ

, 1

1

sup ; ;

sup ;

t k k t T

t T

c c

kc

t tθ θ

tθ

u θ u θ

u θ

1max 2logT

k TZ k

2

1 2

2 2 2 4

exp 2 1 1 1 1 4 1Pr log log

2 2

p

T p

x x h l h lpZ x O

p hl x hl x x

, as x

www.ceep.cas.cn

Methodology

Change interval test•Define parameter space

•Construct hypothesis test

9

Interval Tests for Structural Breaks

1 1 2 21 1, , : , ,

1 T 1 k k k k Tθ θ θ θ θ θ θ θQ ,

11

0 , , : 1 T 1 2 Tθ θ θ θ θQ ,

1 1

12

0 1, , : , 1 T 1 k k Tθ θ θ θ θ θQ ,

2 2

13

0 1, , : , 1 T 1 k k Tθ θ θ θ θ θQ .

HT11: H0: 11

0, , 1 Tθ θ Q vs. HA: 11

0, , 1 Tθ θ Q Q ,

HT12: H0: 12

0, , 1 Tθ θ Q vs. HA: 12

0, , 1 Tθ θ Q Q ,

HT13: H0: 13

0, , 1 Tθ θ Q vs. HA: 13

0, , 1 Tθ θ Q Q .

Null hypothesis

HT11: No change point

HT12: No change point or

only one change point in k1

HT13: No change point or

only one change point in k2

www.ceep.cas.cn 10

Interval Tests for Structural Breaks

www.ceep.cas.cn

Empirical Analysis

11

Interval Tests for Structural Breaks

Estimates for marginal distribution models

Oil

Model: t tr a , t t ta , 2 2 2

1 1 1t t t tI a , 0,1t t

1.07e-04 0.008* a 0.012** 0.961*** 0.050*** 8.465***

Gold

Model: t tr a , t t ta , 2 2 2

1 1t t ta , 0,1t t

0.049** 0.013*** 0.038*** 0.954*** 5.247***

Note: a *, **, *** denote the significant levels of 10%, 5% and 1%, respectively.

Oil & Gold: volatility clustering

Oil: volatility asymmetry

Oil & Gold: innovation symmetric fat-tailed distribution

www.ceep.cas.cn

Empirical Analysis

12

Interval Tests for Structural Breaks

Change point test over the whole sample period

Period n T 1 2

Tz 1 2 1 2

T TP Z z H0 (0.95) Time of Change

Normal

1/4/2006–4/29/2016 1 2546 5.542 4.40e-06 R. a 10/9/2013

1/4/2006–10/9/2013 1 1913 1.851 1 -- --

10/10/2013–4/29/2016 1 633 2.765 0.165 -- --

t

1/4/2006–4/29/2016 2 2546 5.720 1.16e-05 R. 10/9/2013

1/4/2006–10/9/2013 2 1913 2.758 0.608 -- --

10/10/2013–4/29/2016 2 633 2.739 0.516 -- --

Clayton

1/4/2006–4/29/2016 1 2546 4.749 2.22e-04 R. 11/7/2013

1/4/2006–11/7/2013 1 1934 2.347 0.484 -- --

11/8/2013–4/29/2016 1 612 2.183 0.525 -- --

Note: a R. denotes the null hypothesis is rejected at the 5% level.

Change point test can only check out one change point over the whole sample period.

www.ceep.cas.cn

Empirical Analysis

13

Interval Tests for Structural Breaks

Change interval test for financial crisis over the whole sample period

Copula n

Initial Period: 7/1/2008–6/30/2009

Period of Change Change Interval Test Statistics

1k 2k HT11 HT12 HT13

Normal 1 9/10/2008 4/23/2009 13.677** a 6.828** 13.140**

t 2 9/9/2008 4/23/2009 14.440** 6.046* 13.012**

Clayton 1 9/9/2008 6/11/2009 9.570** 6.872** 9.567**

All Copula -- 9/9/2008 4/23/2009 -- -- --

Note: a *, ** denote the significant levels of 5% and 1%, respectively.

Change interval period: 9/9/2008-4/23/2009

www.ceep.cas.cn

Empirical Analysis

14

Interval Tests for Structural Breaks

Change point test for pre-crisis period

Period n T 1 2

Tz 1 2 1 2

T TP Z z H0 (0.95) Time of Change

Pre-crisis Period: 1/4/2006–9/9/2008

Normal

1/4/2006–9/9/2008 1 666 2.637 0.223 -- --

t

1/4/2006–9/9/2008 2 666 2.602 0.660 -- --

Clayton

1/4/2006–9/9/2008 1 666 2.275 0.457 -- --

Note: a R. denotes the null hypothesis is rejected at the 5% level.

No change point in the pre-crisis period.

www.ceep.cas.cn 15

Change point test for post-crisis period

Period n T 1 2

Tz 1 2 1 2

T TP Z z H0 (0.95) Time of Change

Post-crisis Period: 4/24/2009–4/29/2016

Normal

4/24/2009–4/29/2016 1 1728 7.030 4.56e-10 R. a 4/27/2010

4/24/2009–4/27/2010 1 248 2.371 0.311 -- --

4/28/2010–4/29/2016 1 1480 4.007 0.004 R. 10/9/2013

4/28/2010–10/9/2013 1 847 3.434 0.028 R. 9/19/2011

10/10/2013–4/29/2016 1 633 2.765 0.165 -- --

4/28/2010–9/19/2011 1 343 2.542 0.238 -- --

9/20/2011–10/9/2013 1 504 2.344 0.382 -- --

t

4/24/2009–4/29/2016 2 1728 6.739 2.67e-08 R. 4/27/2010

4/24/2009–4/27/2010 2 248 2.328 0.793 -- --

4/28/2010–4/29/2016 2 1480 4.488 0.003 R. 10/9/2013

4/28/2010–10/9/2013 2 847 3.455 0.103 -- --

10/10/2013–4/29/2016 2 633 2.739 0.516 -- --

Clayton

4/24/2009–4/29/2016 1 1728 5.707 1.68e-06 R. 5/5/2010

4/24/2009–5/5/2010 1 253 1.671 0.854 -- --

5/6/2010–4/29/2016 1 1475 3.869 0.007 R. 11/7/2013

5/6/2010–11/7/2013 1 863 2.205 0.539 -- --

11/8/2013–4/29/2016 1 612 2.183 0.525 -- --

Note: a R. denotes the null hypothesis is rejected at the 5% level.

www.ceep.cas.cn 16

Interval Tests for Structural Breaks

Test for the structural change between pre-crisis and post-crisis

Sample Period Financial Crisis Period

1/4/2006–4/27/2010 9/10/2008–4/23/2009

n Change Interval Test Hypothesis Test T2

HT11 HT12 HT13 HT2 P-value

Normal 1 45.595** 45.303** 12.828** 23.510** 1.24e-06

t 2 43.889** 39.115** 13.012** 22.984** 1.02e-05

Clayton 1 36.274** 35.918** 12.119** 17.333** 3.14e-05

Note: a ** denotes the significant levels of 1%.

www.ceep.cas.cn

Empirical Analysis

17

Interval Tests for Structural Breaks

06 07 08 09 10 11 12 13 14 15 16-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Dependent

Rela

tionship

Dynamic Changes in Dependence between Oil and Gold

time-varying

constant

• Change interval9/10/2008-4/23/2009

• Change point 4/27/2010

10/9/2013

• Various period Market boom

Financial crisis

Rapid recovery

Market reform

www.ceep.cas.cn

Conclusion

Theory study•Propose a new change interval test

Empirical study•Commodity properties are larger in economic boom period, and financial properties are larger in extreme risk period

•Exogenous economic shocks and the changes of internal mechanism may lead to structural changes

Other Application•Risk management

•Financial contagion

18

Interval Tests for Structural Breaks

www.ceep.cas.cn

BingYue Liu

Department of Statistics and FinanceUniversity of Science and Technology of ChinaEmail: [email protected]

Thank you for your attention.

Questions and comments are welcome.

![Solutions to deferred material Text and Tests 5 · The 95% confidence interval [CI] for is 2. The 95% confidence interval [CI] for is 3. ... n = 2176.91 people would be needed as](https://img.dokumen.tips/doc/110x75/5c37792209d3f2a60b8bc741/solutions-to-deferred-material-text-and-tests-5-the-95-confidence-interval.jpg)