Embed Size (px)

DESCRIPTION

Intertemporal Macroeconomics

Citation preview

1

Intertemporal Macroeconomics

Gernot Doppelhofer*

May 2009 Forthcoming in J. McCombie and N. Allington (eds.), Cambridge Essays in Applied Economics, Cambridge UP This chapter reviews models of intertemporal choice consumption demand and labour supply. We discuss optimal decisions by individuals at the microeconomic level and the implications for the aggregate economy. The chapter describes the equilibrium in a market-clearing neoclassical model and analyses effects of productivity and government sector shocks on optimal decisions by consumers and workers. Predictions from the benchmark neoclassical model are contrasted with alternative theories and aggregate data for the US and UK. JEL Code: D91, E12, E13, E21, E24, E62, H30 Department of Economics, Norwegian School of Economics and Business Administration (NHH), Helleveien 30, N-5045 Bergen, Norway; email: [email protected]. I thank Xavier Sala-i-Martin, whose macroeconomics lectures at Columbia University provided inspiration and guidance to the material in this chapter, Donald Robertson for helpful discussions and the derivation of the Keynes-Ramsey rule, and several cohorts of students at Cambridge for helpful feedback. I thank Bhaavit Agrawal for excellent research assistance, the Economics Department at UW-Madison for their hospitality while completing this chapter and Trinity College for financial support. All errors are mine.

2

Table of Contents 1 Introduction ................................................................................................................. 1 2 Static model of consumption and leisure choice......................................................... 2

2.1 Substitution and income effect ....................................................................... 3 3 Intertemporal Consumption Choice ............................................................................ 5

3.1 A two period model ....................................................................................... 5 3.2 Intertemporal substitution and income effects ............................................... 7 3.3 Intertemporal optimisation and the Euler equation ........................................ 8 3.4 Consumption functions in multi-period models .......................................... 10

3.4.1 Modigliani’s life cycle hypothesis (LCH) ............................................... 10 3.4.2. Friedman’s permanent income hypothesis (PIH) ...................................... 12

3.5 Role of uncertainty and Hall’s random walk hypothesis ............................. 14 3.6 Departures from classical consumers ........................................................... 15

4 Intertemporal Labour Demand and Supply ............................................................... 18 4.1 Labour Demand ................................................................................................. 18 4.2 Intertemporal labour supply ............................................................................... 18 4.3 Empirical Evidence of Labour Supply ............................................................... 20

5 Equilibrium in goods and labour market and productivity shocks ........................... 20 5.1 Aggregation........................................................................................................ 21 5.2 Productivity shocks ............................................................................................ 22

5.2.1 Permanent productivity shock ..................................................................... 22 5.2.2 Temporary productivity shock .................................................................... 22 5.2.3 Theoretical predictions and stylised facts ................................................... 24

6 Government............................................................................................................... 24 6.1 Effect of government spending .......................................................................... 25

6.1.1 Permanent change in government spending ............................................... 26 6.1.2 Temporary change in government spending ............................................... 27 6.1.3 Effects of government spending in Keynesian Model ................................ 28

6.2 Budget Deficits and Ricardian equivalence ....................................................... 28 6.3. Taxes ................................................................................................................. 29

7 Concluding Remarks ................................................................................................. 31 References .................................................................................................................... 32

1

1 Introduction This chapter gives an overview of the literature on intertemporal macroeconomics. We review models of individual, optimising behaviour by consumers and workers, discuss implications for aggregate variables and contrast the theoretical predictions with empirical facts for the US and UK economies. The advantage of using an optimising model is that we gain a better understanding of the aggregate economy. Instead of simply postulating ad hoc macroeconomic relations, we understand the microeconomic foundations of aggregate variables such as consumption and labour supply. Starting from microeconomic foundations ensures internal consistency of our macroeconomic models. The drawback of a microfounded approach is that going from individual to aggregate behaviour requires strong assumptions. We start by analysing the neo-classical model as a benchmark. Consumers choose optimally how much to consume and save over time given the path of income and the interest rate. Workers supply labour (demand leisure) each period, given the path of wages and the interest rate. Perfectly competitive firms hire labour at the market-clearing wage and we can derive the equilibrium in goods, labour and bond markets. Next we can analyse the effects of productivity shocks and changes in government spending and tax decisions on the model. We contrast the predictions of the model with empirical observations and discuss implications of alternatives theories. For reference, we list the following key aggregate quarterly data for the United States averaged over the 1959-96 period (from Barro 1997, Table 1.1).

Components of GDP Share of GDP Standard Deviation

Correlation with GDP

GDP 1.000 0.017 1.00 Consumption 0.589 0.008 0.83 Investment 0.203 0.065 0.93 Government spending 0.226 0.017 0.02 Other variables Employment - 0.010 0.81 Worker hours - 0.015 0.88 Output per employee - 0.011 0.84 Real wage - 0.011 0.48 Real Interest Rate - - 0.23 This chapter is organised as follows: Section 2 briefly describes a simple static model of consumption and leisure choice. Section 3 discusses models of intertemporal consumption choice. Section 4 introduces intertemporal supply and demand for labour and discusses empirical evidence. Section 5 derives the equilibrium in the neoclassical model and analyses the effect of productivity shocks on optimal choices. Section 6 introduces the government sector into the model and section 7 concludes.

2

2 Static model of consumption and leisure choice Consider first the optimal demand for consumption and leisure in a highly simplified static model of an economy. A representative1 individual has preferences over consumption and leisure are represented by a utility function

(1) )1,( lcu −

where c represents individual2 consumption and l the supply of labour. The total time endowment is normalised to 1 and (1-l) represents leisure. We assume that utility increases in both consumption and leisure, represented by positive marginal utilities uc>0 and u1-l>0, and that the ratio of marginal utilities uc/u1-l falls as the consumption/leisure ratio rises. The preferences can be represented by convex indifference curves shown in Figure 1. The individual prefers more consumption and more leisure (less work) and moderate amounts of both compared to extremes of only one of them. For each unit of labour l the consumer earns a wage w measured in terms of the homogenous final good3. The set of feasible choices (budget constraint) is therefore given by

(2) bwlc +=

where b is the stock of wealth which is independent of labour income. The budget constraint is shown as upward sloping line in figure 1 with slope w. Increases in initial wealth b correspond to upward parallel shifts of the constraint. The problem for the consumer is to maximise the utility function (1) subject to the budget constraint (2). Formally, we can set up the Lagrangian and find the optimal choices of consumption and leisure

[ ]cbwllculc

−++− λ)1,(max,

The first order conditions are uc=λ and u1-l=wλ, where λ is the Lagrange multiplier associated with the budget constraint (2). Combining those two conditions implies that at the optimum the marginal rate of substitution (MRS) between leisure and consumption equals the wage rate

wuuMRS

c

lcl == −

−1

,1

1 Aggregation of preferences across individuals requires very restrictive assumptions; see Deaton (1992) and section 5.1 below for a discussion. 2 Throughout this chapter the notation convention is that lowercase denotes individual and uppercase aggregate variables. Economy-wide prices such as the interest rate are written as lowercase. 3 This chapter abstracts from money and therefore does not discuss the role of nominal rigidities (sticky prices or wages). For an excellent discussion of such issues see Blanchard (1990).

3

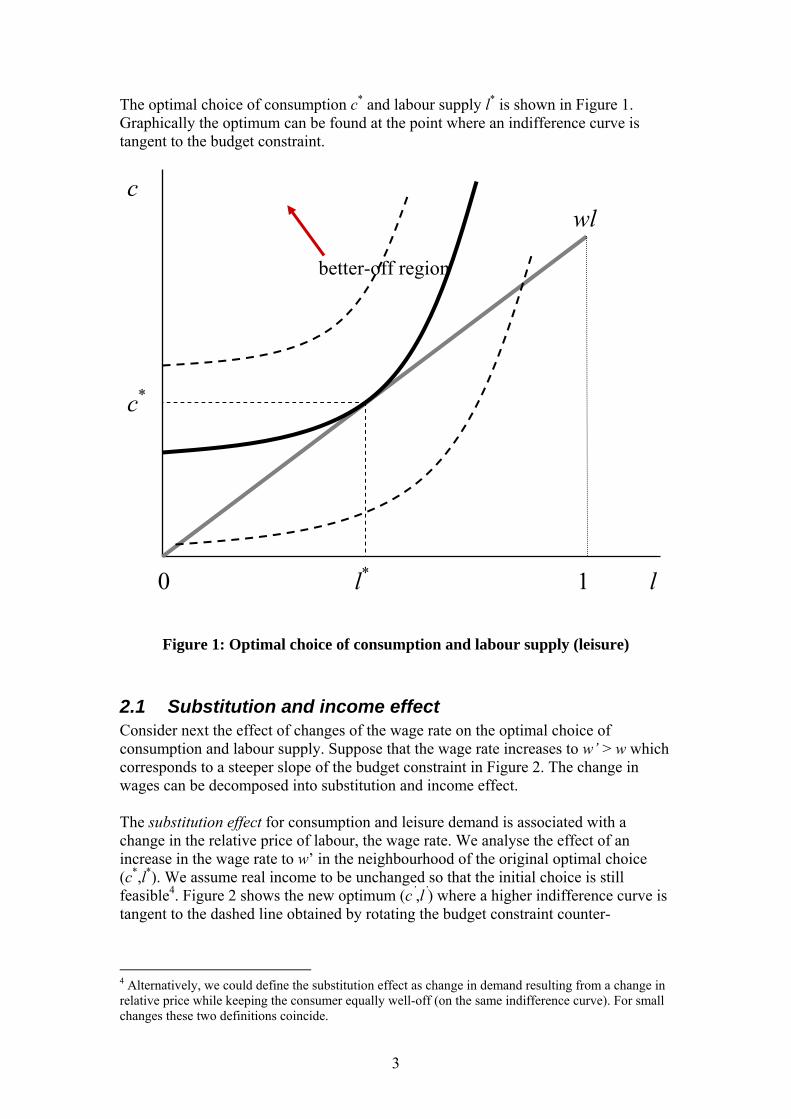

The optimal choice of consumption c* and labour supply l* is shown in Figure 1. Graphically the optimum can be found at the point where an indifference curve is tangent to the budget constraint.

Figure 1: Optimal choice of consumption and labour supply (leisure)

2.1 Substitution and income effect Consider next the effect of changes of the wage rate on the optimal choice of consumption and labour supply. Suppose that the wage rate increases to w’ > w which corresponds to a steeper slope of the budget constraint in Figure 2. The change in wages can be decomposed into substitution and income effect. The substitution effect for consumption and leisure demand is associated with a change in the relative price of labour, the wage rate. We analyse the effect of an increase in the wage rate to w’ in the neighbourhood of the original optimal choice (c*,l*). We assume real income to be unchanged so that the initial choice is still feasible4. Figure 2 shows the new optimum (c’,l’) where a higher indifference curve is tangent to the dashed line obtained by rotating the budget constraint counter-

4 Alternatively, we could define the substitution effect as change in demand resulting from a change in relative price while keeping the consumer equally well-off (on the same indifference curve). For small changes these two definitions coincide.

c

l1 0 l*

c*

wl

better-off region

4

clockwise around the initial point (c*,l*). Intuitively, the substitution effect induces the consumer to work more (enjoy less leisure) and increase consumption. The income effect (sometimes called wealth effect) is due to the higher wage at every level of labour supplied l. Figure 2 shows the parallel shift from the dashed line to the new (solid) budget constraint. Note that both lines share the same steeper slope w’. The income effect implies more demand for both consumption and leisure which are usually assumed to be normal goods (movement from c’,l’ to c**,l**). The total effect of an increase of wages is the combination of substitution and income effects: For consumption, the two effects reinforce each other and imply an rise from c* to c** in Figure 2. For leisure (and labour supply) substitution and income effect work in opposite directions and the overall effect is ambiguous depending on the relative strengths of substitution and income effects.

Figure 2: Substitution and income effect on consumption and labour resulting

from wage increase

c

l1 0 l**

c*

wl

w’l

c**

l* l’

c’

5

Empirically we observe increased levels of consumption and falling labour supply (measured by weekly hours) as economies are developing and wages are rising. For example, the average number of weekly hours in manufacturing has fallen from between 55 and 60 in 1890 to 42 in 1996 in the United States and has fallen from 60 in 1850 to 44 in 1994 for the UK (see Barro 1997, pp. 76-77). Similar secular declines of work hours can be observed in other countries over time, however the relationship appears to become weaker at high levels of income (weekly hours have not fallen in the US over the last 50 years).

3 Intertemporal Consumption Choice

3.1 A two period model Consider next the optimal choice of consumption over time. Suppose that individuals live for two periods, (denoted by subscripts 1 and 2). Each period, individuals earn income y and chose how much to consume c or alternatively save by purchasing bonds b paying a constant5 interest rate r. The budget constraint for the two periods are

2212

1101

)1()1(

bcrbybcrby+=+++=++

where b0 denotes the level of assets at the beginning of the individuals life and b2 at the end of its lifetime. The budget constraints for each period can be rewritten alternatively as intertemporal budget constraint

(4) r

br

ccrbr

yy+

++

+=+++

+11

)1(1

2210

21

which states that the present value6 of lifetime income and initial wealth equals the present value of lifetime spending. Individuals live for 2 periods and are assumed to care only about their own consumption in periods 1 and 2 (we will relax this assumption in section 3.5.2). Therefore, optimal assets in the final period of individuals life will not be positive, that is b2≤0, as long as consumers are not satiated. On the other hand, individuals are not allowed to leave behind debt, so b2≥0. In equilibrium each generation is therefore born with zero wealth (b0=0) and the intertemporal budget constraint therefore simplifies to

(5) r

ccr

yy+

+=+

+11

21

21

The intertemporal budget constraint (5) is shown in Figure7 3 as the black solid line that passes through the endowment point (y1,y2) and has slope –(1+r). Consumers can

5 Throughout this chapter we assume the interest rate to be fixed and known. In a more realistic model, the interest rate is determined in capital markets and changes over time. For a discussion of variable interest rates see for example Obstfeld and Rogoff (1996, pp. 76-78). 6 Given interest rate r the present value at time 0 of an amount Xt t periods in the future is defined as PV(Xt)≡Xt/(1+r)t. The term 1/(1+r)t can be viewed as the relative price of Xt in terms of current goods. 7 Such figures introduced by Irving Fisher (1907) are know as Fisher diagrams.

6

chose any combination of first and second period consumption (c1,c2) on this line and the optimal choice depends on preferences over consuming in the first or second period of their life. We assume diminishing marginal utility of consumption and individuals prefer to smooth consumption between time periods. Indifference curves in Figure 3 are therefore negatively sloped and convex to the origin. Figure 3 shows examples of different types of individuals: 1. Saver: consumers are relatively patient, they save in period 1 by chosing c1

*<y1 and consume their income and savings in period 2 giving c2

*>y2. 2. Borrower: consumers are relatively impatient, they chose c1

*>y1 and borrow in period 1 which they repay by saving in period 2 and hence c2

*<y2. 3. Autarkist: individuals consume at the endowment point and are neither saving nor borrowing, c1

*=y1 and c2*=y2.

Figure 3: Optimal consumption choice between periods 1 and 2

How does the optimal consumption choice respond to changes in income? Notice that individuals want to smooth consumption over time (because of diminishing marginal utility of consumption) and they can borrow and lend freely at interest rate r. Consumption each period is therefore a function of the present value of lifetime income, PV(y) ≡ y1 + y2/(1+r) in equation (5). An increase in income in one period only, say y1, leads to less than proportional increases of consumption each period. However, consumption moves proportional to changes in the present value of income.

c2

c10 c1*=y1

c2*=y2

slope −(1+r)

7

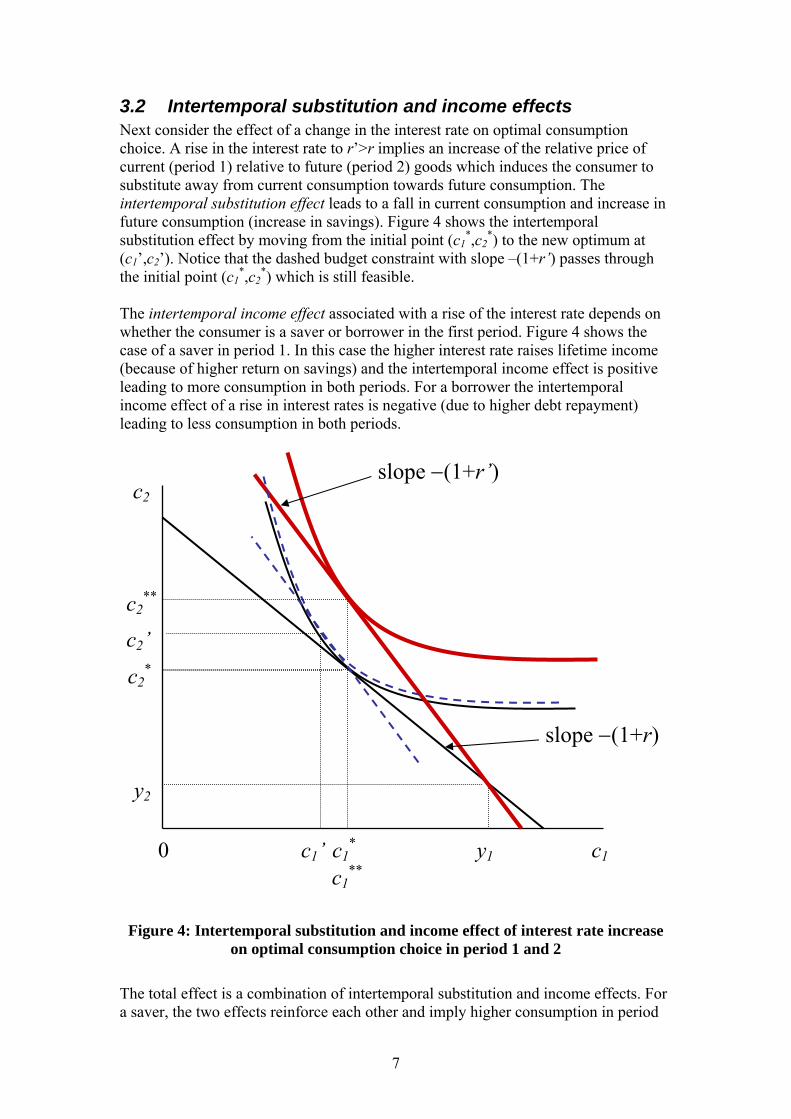

3.2 Intertemporal substitution and income effects Next consider the effect of a change in the interest rate on optimal consumption choice. A rise in the interest rate to r’>r implies an increase of the relative price of current (period 1) relative to future (period 2) goods which induces the consumer to substitute away from current consumption towards future consumption. The intertemporal substitution effect leads to a fall in current consumption and increase in future consumption (increase in savings). Figure 4 shows the intertemporal substitution effect by moving from the initial point (c1

*,c2*) to the new optimum at

(c1’,c2’). Notice that the dashed budget constraint with slope –(1+r’) passes through the initial point (c1

*,c2*) which is still feasible.

The intertemporal income effect associated with a rise of the interest rate depends on whether the consumer is a saver or borrower in the first period. Figure 4 shows the case of a saver in period 1. In this case the higher interest rate raises lifetime income (because of higher return on savings) and the intertemporal income effect is positive leading to more consumption in both periods. For a borrower the intertemporal income effect of a rise in interest rates is negative (due to higher debt repayment) leading to less consumption in both periods.

Figure 4: Intertemporal substitution and income effect of interest rate increase

on optimal consumption choice in period 1 and 2 The total effect is a combination of intertemporal substitution and income effects. For a saver, the two effects reinforce each other and imply higher consumption in period

c2

c1 0 c1*

c2*

y1

y2

c2**

c2’

c1’ c1

**

slope −(1+r’)

slope −(1+r)

8

2, but have opposite signs, hence ambiguous total effect on consumption in period 1. The new optimal point is (c1

**,c2**) in Figure 4. A borrower on the other hand reduces

c1 since both effects reinforce each other, but the overall change is ambiguous for c2. For the aggregate economy only the intertemporal substitution effect is relevant since there is no net saving or borrowing in equilibrium (see section 5 below). Aggregate consumption demand (denoted by superscript d) depends therefore negatively on the interest rate and positively on the present value of aggregate income

,...))(,()()(1

+−YPVrCd

3.3 Intertemporal optimisation and the Euler equation We can analyse the consumer’s problem more formally. Suppose that individuals have additively separable preferences over first and second period consumption: (6) )()(max 21, 21

cucucc

β+

where the period utility function u(.) is strictly concave u’>0, u’’<0 and β is the subjective discount factor measuring the degree of impatience of the individual. We assume that the individual discounts future utility with 0<β<1. The problem of the consumer is to maximise lifetime utility (6) subject to the intertemporal budget constraint (5). For example, we can use the substitution method and substitute for c2 from (5) into (6):

[ ]2111 ))(1()(max1

ycyrucuc

+−++ β

The necessary first-order condition for this problem is also called an intertemporal Euler equation8 (7) )(')1()(' 21 curcu β+= The Euler equation determines optimal consumption choice over time. The left hand side of equation (7) is the marginal utility of consumption in period 1 which measures how much the individual values one unit of consumption. If the individual saves one unit she would receive (1+r) units of consumption next period which would increase lifetime utility by the marginal utility of consumption (discounted by β) on the right hand side of (7). Alternatively, the Euler equation can be written as

rcucu

+=

11

)(')('

1

2β

which equates the marginal rate of substitution between c1 and c2 on the left hand side to the relative price 1/(1+r). This optimality condition can also be seen in Figure 3

8 It is named after the Swiss mathematician Euler who investigated dynamic systems more generally.

9

where the indifference curve representing the trade-off between current and future consumption is tangent to the intertemporal budget constraint with slope –(1+r). In order to further understand intertemporal consumption choice consider the following example of a power utility function

(8) θ

θ

−−

=−

11)(

1ccu

where the parameter θ>0 controls the curvature of the utility function and 1/θ measures the constant intertemporal elasticity of substitution (IES) of consumption between time periods. Utility function (8) is also called isoelastic utility function. The marginal utility of consumption in this case is simply θ−= ccu )(' and the Euler equation (7) becomes

( ) )1(/ 12 rcc += βθ To interprete this condition, rewrite the discount factor as β =1/(1+ρ), where ρ>0 is the rate of time preference. For small changes in consumption ∆c≡(c2-c1), the left hand side of this expression can be approximated by

cccccc /1)1/()/( 12 Δ+≅+Δ= θθθ For small values of r and ρ the right hand side of this expressions is approximately equal to ρρ −+≅++ rr 1)1/()1( . Combining the two approximations, the Euler equation (also known as Keynes-Ramsey rule) becomes

(9) )(1 ρθ

−=Δ rcc

The growth rate of consumption cc /Δ is determined by the difference between the interest rate and the rate of time preference and the strength of the response depends on the intertemporal elasticity of substitution 1/θ. Hall (1988) tests the empirical relationship between aggregate consumption and interest rates and finds only a weak relationship between these two variables. Hall’s estimates of the intertemporal elasticity of substitution (IES) are shown in Table 1. The estimates depend on which asset is used to calculate underlying interest rates. The first three rows of Table 1 are based on annualised postwar data of expected returns based on inflation expectations from the Livingston survey9. The point estimates range from 0.066 for returns on 400 S&P stocks to 0.346 for US Treasury bills. However, the estimated standard errors are so large that the point estimates are not statistically different from zero. The estimates based on the sample starting in 1924 and realised returns gives marginally significant, negative estimates of the IES.

9 The Livingston survey is based on expectations of many variables by a panel of economists.

10

Table 1: Hall’s (1988) estimates of intertemporal elasticity of substitution (IES) Interest rate based on IES estimate Standard error Sample T Bills (expected) 0.346 (0.337) 1959-83 Savings Accounts 0.271 (.330) 1959-83 Stocks 0.066 (0.050) 1959-83 T Bills (realised) -0.40 (0.20) 1924-40, 1950-83 Beaudry and Van Wincoop (1996) use panel data for US States instead of nationwide data. For the period 1953-91 they strongly reject the zero estimate of the IES and find estimates close to one. Several studies have also used microeconomic data to address problems of aggregation and lack of control for demographic and labour market effects. Attanasio and Weber (1993) and Blundell, Browning and Meghir (1994) find for both the US and the UK estimates of the IES just below one. Browning, Hansen and Heckman (1999) survey general equilibrium models and implied empirical estimates of the IES using micro data (see for example their Tables 3.1 and 3.2). They argue that the IES parameter is often poorly determined, and that there is evidence varies with demographic characteristics and wealth.

3.4 Consumption functions in multi-period models The analysis for the two period case can be generalised to many periods. The next two sections discuss the case of finite and infinite life-time.

3.4.1 Modigliani’s life cycle hypothesis (LCH) In the 1950s Franco Modigliani developed with co-authors the life cycle hypothesis (LCH) to describe consumption and savings behaviour over individuals’ lifetime10. Suppose that individuals live for T periods and each period t face a budget constraint

tttt bcrby +=++ − )1(1 Similar to the two-period case we can derive the intertemporal budget constraint saying that the present value of lifetime income and initial wealth equals the present value of lifetime spending

112

1

012

1

)1()1(...

1

)1()1(

...1

−−

−

++

+++

++

=+++

+++

+

TT

TT

TT

rb

rc

rcc

rbr

yr

yy

10 Here we follow the simple version presented in Modigliani’s (1986) Nobel lecture.

11

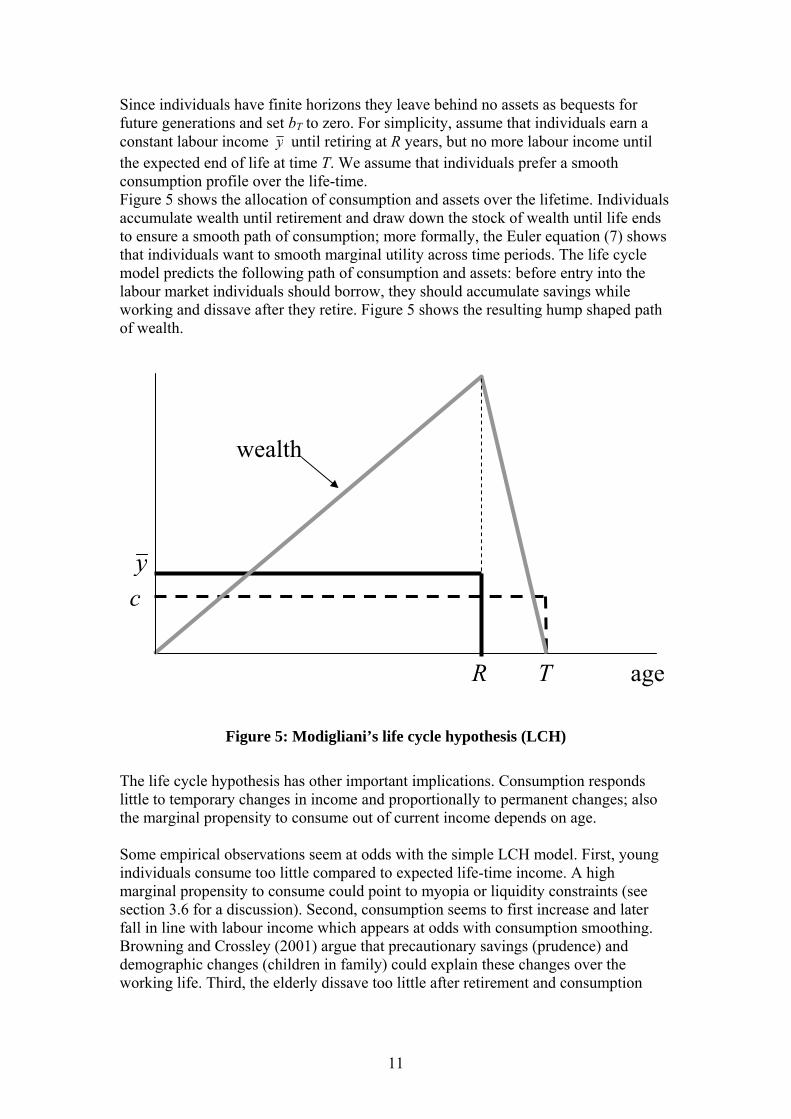

Since individuals have finite horizons they leave behind no assets as bequests for future generations and set bT to zero. For simplicity, assume that individuals earn a constant labour income y until retiring at R years, but no more labour income until the expected end of life at time T. We assume that individuals prefer a smooth consumption profile over the life-time. Figure 5 shows the allocation of consumption and assets over the lifetime. Individuals accumulate wealth until retirement and draw down the stock of wealth until life ends to ensure a smooth path of consumption; more formally, the Euler equation (7) shows that individuals want to smooth marginal utility across time periods. The life cycle model predicts the following path of consumption and assets: before entry into the labour market individuals should borrow, they should accumulate savings while working and dissave after they retire. Figure 5 shows the resulting hump shaped path of wealth.

Figure 5: Modigliani’s life cycle hypothesis (LCH)

The life cycle hypothesis has other important implications. Consumption responds little to temporary changes in income and proportionally to permanent changes; also the marginal propensity to consume out of current income depends on age. Some empirical observations seem at odds with the simple LCH model. First, young individuals consume too little compared to expected life-time income. A high marginal propensity to consume could point to myopia or liquidity constraints (see section 3.6 for a discussion). Second, consumption seems to first increase and later fall in line with labour income which appears at odds with consumption smoothing. Browning and Crossley (2001) argue that precautionary savings (prudence) and demographic changes (children in family) could explain these changes over the working life. Third, the elderly dissave too little after retirement and consumption

R T age

wealth

c y

12

falls discretely at retirement. These observations might be explained by precautionary savings motive or the importance of bequests (see section 6.2 below).

3.4.2. Friedman’s permanent income hypothesis (PIH) Suppose instead that generations are linked to each other. Assume that each generation lives for one period and cares about its own utility and the utility of the next generation:

...)()( :2

)()( :1

32

21

cucutcucut

ββ+=+=

Lifetime utility of generation born at time 1 is therefore

(10) ∑∞

=

−=+++1

13

221 )(...)()()(

tt

t cucucucu βββ

Since each generations cares about the next, each generation acts as if it was infinitely lived and had an infinite horizon. Notice that each generation discounts11 future utility with discount factor β. Similar to the life cycle model presented in the previous section, we can combine the budget constraints faced by each generation t = 1,2,.. into the intertemporal budget constraint

11

101

1 )1(lim

)1()1(

)1( −∞→

∞

=−

∞

=− +

++

=+++ ∑∑ T

T

Ttt

t

tt

t

rb

rcrb

ry

The left hand side shows the present value of current and future income over the infinite horizon (discounted at relative price r) plus initial assets. On the right hand side is the present value of consumption spending plus a term showing the present value of wealth as the horizon is pushed towards infinity. Remember that for the two-period and life cycle model consumers were not allowed to leave behind debts (bT < 0). In the infinite horizon case this condition is replaced by

0)1/(lim 1 ≥+ −∞→

TTT rb which states the present discounted value of assets must be

non-negative and that debt must not grow faster than the interest rate. Otherwise the consumer could finance infinite consumption by borrowing ever increasing amounts12. Furthermore, consumers will not find it optimal to accumulate savings at a faster rate than the interest rate or else the present value of savings would be unbounded. The optimal consumption path therefore satisfies the so-called transversality condition

11 Frank Ramsey (1928) viewed such discounting of future welfare as “ethically indefensible” in normative models. In a positive (descriptive) sense discounting would be consistent with “selfish” individuals preferring current to future consumption (see section 3.6 below for discussion). 12 This condition is also known as the No-Ponzi-game condition after the swindler Charles Ponzi who ran a pyramid scheme in Boston in the 1920s.

13

(11) 0)1(

lim 1 =+ −∞→ TT

T rb

With condition (11) satisfied the intertemporal budget constraint becomes

(12) ∑∑∞

=−

∞

=− +

=+++ 1

101

1 )1()1(

)1( tt

t

tt

t

rcrb

ry

The problem for an individual born at time 0 is to maximize utility (10) subject to the intertemporal budget constraint (12). The condition describing optimal consumption for the infinite horizon problem is the familiar intertemporal Euler equation13

)(')1()(' 1++= tt curcu β

The intuition is exactly the same as in the two period case: the marginal utility of consumption between periods t+1 and t equals the market valuation 1/(1+r). Along the optimal path the consumer is indifferent to consume or save the marginal unit. Consider the special case of β=1/(1+r). Then the Euler equation simplifies to (13) )(')(' 1+= tt cucu which implies that consumption is constant over time ccc tt == +1 . Because consumers discount future utility at the same rate as the market interest rate, consumers have no incentive to “tilt” the consumption path over time and hence consumption is constant (remember the Keynes-Ramsey rule in equation (9)). Substitute the constant level of consumption c in the intertemporal budget constraint (12) and solving gives:

)1()1()1( 0

11

11 rb

ry

rc

tt

t

tt ++

+=

+ ∑∑∞

=−

∞

=−

which says that the present value of consumption equals the present value of total wealth which equals the present value of life-time income plus initial wealth. Each period t=1,2,… individuals consume the annuity value14 of total wealth which Milton Friedman (1957) calls permanent income yP

(14) ⎟⎟⎠

⎞⎜⎜⎝

⎛++

++≡= −

∞

=

+∑ )1()1(1 1

0rb

ry

rryc t

ss

stptt

13 It is straightforward to extend the derivation of the intertemporal Euler from the two period model (section 3.3) to the life-cycle model with finite T periods. A formal derivation for the infinite horizon case is beyond the scope of this chapter. For a discussion of this case see for example Dixit (1990). 14 Consuming the annuity value leaves total wealth unchanged over time. Notice that we use

∑∞

=− +=+

11 /)1()1/(1

tt rrr in deriving (14).

14

Income y can be decomposed into permanent income yP and transitory income yT defined as (y - yP). According to Friedman’s permanent income hypothesis (PIH) consumption demand responds proportionally15 to changes in permanent income and not to at all to changes in transitory income. Friedman’s theory delivers strong empirical predictions. In a deterministic environment (with no shocks) consumption and current income would be unrelated over time. Furthermore, there would be a relationship between consumption and permanent income when observing individuals in a cross-section. This can explain the lower marginal propensity to consume and higher propensity to save out of current income among individuals with below average permanent income (for example, the difference between White and Black population in the United States).

3.5 Role of uncertainty and Hall’s random walk hypothesis Next let us analyse the choice of intertemporal consumption when consumers face uncertainty over future income and consumption due to the presence of random shocks. Suppose that individuals maximise the expected value of lifetime utility

⎭⎬⎫

⎩⎨⎧∑

∞

=

−

1

11,...,

)(Emax21 t

tt

cccuβ

where E1 denotes mathematical expectations conditional on information available at time 1. The expected value equals the probability weighted average of possible outcomes. The intertemporal budget constraint is still given by equation (12) stating that the realised (ex post) present values of consumption equal total realised wealth. The stochastic version of the Euler equation governing optimal consumption equates marginal utility of consumption in period 1 and expected discounted marginal utility in period 2

[ ])('E)1()(' 211 curcu β+= Hall (1978) tests the stochastic version of life-cycle and permanent income hypotheses theory by making the following simplifying assumptions: Assumption 1 Suppose the utility function is quadratic

0 with ,2/)( 2 >−= aacccu This assumption implies that marginal utility accu −=1)(' is linear in consumption. A consequence of this assumption is that the individual consumption decision exhibits certainty equivalence which implies individuals act as if future consumption was at its conditional mean value and ignore its variation. Assumption 2 Assume 1+ r = 1/β.

15 In Friedman’s (1957), consumption is proportional to permanent income ct

d = k(r,wealth,…) ytP. In

equation (14) the factor of proportionality k equals 1 since r=β. Note that we abstract from uncertainty about future income (see section 3.6).

15

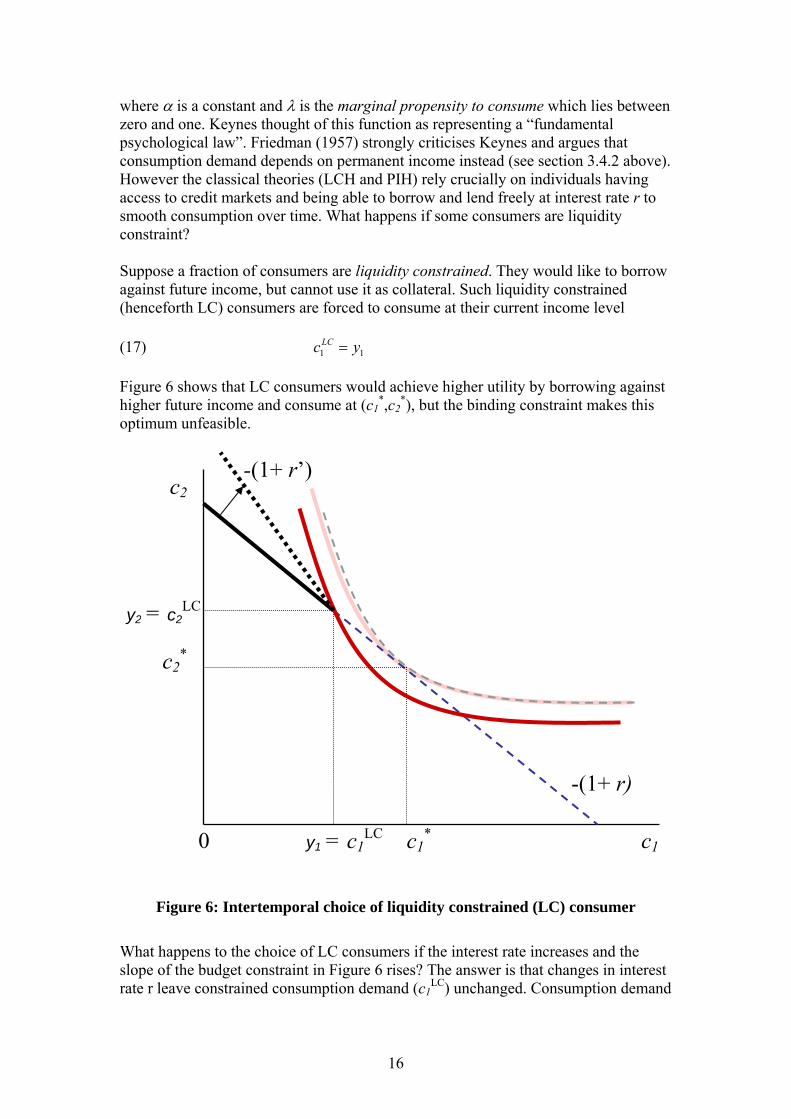

Assumption 2 ensures that consumers want to hold marginal utility and hence consumption constant over time. See discussion after equation (13) above. Under these two assumption the stochastic Euler equation becomes (15) ( )211 E cc = Equation (15) says that consumption follows a random walk and the best estimate of next period’s consumption is the current level of consumption. Intuitively individuals plan to smooth consumption over time (assumption 2) and use all information available at time 1 to make optimal forecasts of permanent income. An implication of this theory is that changes in consumption should be unpredictable and represent only surprise information (not known at time 1). Hall (1978) tests the theory using postwar aggregate US data and finds that past levels of consumption and income have no predictive power for future consumption. However, the pure LCH-PIH theory fails because lagged levels of S&P stock market prices help to predict changes in aggregate consumption. Flavin (1981) looks at the joint behaviour of aggregate consumption and income and finds that consumption exhibits excess sensitivity to anticipated changes in current income. On the other hand Campbell and Deaton (1989) find that consumption exhibits excess smoothness with regard to contemporaneous innovations to income. Notice that these two observations are not mutually contradicting each other since excess sensitivity refers to anticipated changes whereas excess smoothness is with regards to unexpected innovations (see Abel 1990 for discussion). Hall’s test of the random walk result relies on the maintained assumption of quadratic utility (assumption 1) and rejection of a test by the data could imply that the underlying LCH-PIH theories and/or the assumptions are wrong. Quadratic utility provides a good approximation to preferences if marginal utility is not responding strongly to fluctuations in consumption and is close to the linear certainty equivalence case. If marginal utility is very non-linear on the other hand, individuals strongly dislike uncertainty and will accumulate precautionary savings. Several studies investigate the importance of precautionary savings empirically and conclude that the answer depends crucially on preference parameters, the distribution of earnings and the individual’s age (see Attanasio, 1999).

3.6 Departures from classical consumers This section looks at deviations from classical (LCH and PIH) models of consumer behaviour and discusses empirical evidence. Keynes (1936) postulates a linear consumption function where aggregate consumption demand depends linearly on current aggregate income: (16) 11 YC λα +=

16

where α is a constant and λ is the marginal propensity to consume which lies between zero and one. Keynes thought of this function as representing a “fundamental psychological law”. Friedman (1957) strongly criticises Keynes and argues that consumption demand depends on permanent income instead (see section 3.4.2 above). However the classical theories (LCH and PIH) rely crucially on individuals having access to credit markets and being able to borrow and lend freely at interest rate r to smooth consumption over time. What happens if some consumers are liquidity constraint? Suppose a fraction of consumers are liquidity constrained. They would like to borrow against future income, but cannot use it as collateral. Such liquidity constrained (henceforth LC) consumers are forced to consume at their current income level (17) 11 ycLC = Figure 6 shows that LC consumers would achieve higher utility by borrowing against higher future income and consume at (c1

*,c2*), but the binding constraint makes this

optimum unfeasible.

Figure 6: Intertemporal choice of liquidity constrained (LC) consumer

What happens to the choice of LC consumers if the interest rate increases and the slope of the budget constraint in Figure 6 rises? The answer is that changes in interest rate r leave constrained consumption demand (c1

LC) unchanged. Consumption demand

c2

c10

-(1+ r’)

y2 = c2LC

y1 = c1LC

-(1+ r)

c1*

c2*

17

of LC consumers depends only on current income as in equation (17), and changes in the interest rate16 or future income are not relevant. Suppose next that a fraction λ of the population is liquidity constrained and behaves as in (17) and the remainder (1- λ) behaves like classical consumers from section 3.1 with consumption function c1

d(r, PV(y),..). Aggregate consumption is the weighted sum of the two terms (18) ))(,()1()1( 11111 yPVrcyccC ddLCTotal λλλλ −+=−+= or written more compactly as Keynesian consumption function (16)

11 YC K λα +≅ where ))(,()1( 1 yPVrcdλα −≡ is not constant, but function of the interest rate r and λ measures the fraction of LC consumers in the economy. Campbell and Mankiw (1989) test the validity of Euler equation (9). As alterantive they allow for the presence of “rule-of-thumb” consumers whose consumption growth is also affected by expected changes in income (compare this to Hall’s (1978) test) (19) 1111 )log()log( ++++ +Δ++=Δ tttt YrC ελσα Using 1953-86 US data Campbell and Mankiw estimate the share of rule-of-thumb consumers λ to be approximately one half. Does this imply that 50% of the US population is liquidity constrained? Not necessarily, since there are other reasons that consumption could depend on current income: these include life-cycle effects and precautionary motives discussed earlier, deviations from “standard” optimization (see below) or habit formation17. The estimate of σ is not statistically different from zero indicating little correlation between expected changes in consumption and ex ante real interest rates. This finding is consistent with Hall’s (1988) results shown in Table 1. Flavin’s (1981) findings of excess sensitivity of consumption to anticipated changes in current income are consistent with the presence of liquidity constraints. Hall and Mishkin (1982) use panel data on food expenditures and find that approximately 20% of US households are liquidity constrained. Hayashi (1987) points out that even if consumers are currently not constrained, the possibility of being constrained in the future shortens their effective planning horizon. Loewenstein and Thaler (1989) describe several anomalies in intertemporal choice including time-inconsistent preferences or nominal anchoring. Angeletos et al (2001) argue that the introduction of time-inconsistent preferences through hyperbolic discounting produces can help to explain the relatively low levels of liquid assets (and large credit card debt) over the life cycle. Hyperbolic consumers are less able to smooth consumption which is consistent with Flavin’s excess sensitivity result.

16 For a sufficiently high interest rate, liquidity constrained consumers become unconstrained and save in the first period. We assume the liquidity constraint binds also after changing the interest rate. 17 See Attanasio (1999) and Carroll (2001) for recent reviews of the literature.

18

4 Intertemporal Labour Demand and Supply

4.1 Labour Demand Consider first labour demand by competitive firms. Suppose that each period firms produce final output using a production function (20) AF(l)y = where F(.) exhibits positive, but diminishing returns to labour, F’(l)>0 and F’’(l)<0. Productivity is measured by the parameter A>0 which represents factors such as the weather or available knowledge that increase output for given private inputs. For any given labour input l an increase in productivity A raises output in equation (20). Suppose that perfectly competitive firms maximise profits

ddds

lwllAFwly

d−=−= )(maxπ

where ld represents the firm’s labour demand. The necessary first-order condition18 implies that firms hire labour up to the point where the marginal product of labour equals the real wage rate, w*=AF’(l). At this market clearing wage w* there is full employment. An increase in productivity A implies a higher marginal product of labour and hence the wage rate increases (see also section 5.2 below).

4.2 Intertemporal labour supply Consider next the intertemporal choice of labour supply by individuals in a simple 2 period model (which extends straightforward to several periods). Household earn wage income and consume and save in periods 1 and 2. Preferences over consumption and leisure are given by

(21) )1,(1

1)1,( max 2211lc,lculcu −

++−

ρ

where the period utility function u(c,l) has the same properties as equation (1). We assume lifetime utility to be additively separable between time period which implies marginal utilities are not a function of consumption and leisure choices across time. The discount factor is given by β = 1/(1+ρ), where ρ is the rate of time preference. Assuming that individuals earn labour income in both periods, the intertemporal budget constraint (IBC) equals

(22) 221121 11

11 lw

rlwc

rc

++=

++

which implies that the present discounted value of lifetime consumption equals lifetime labour income, both discounted at the interest rate r.

18 Optimal input demand here is static and depends only on current inputs and prices. They would become dynamic if inputs hired in previous periods were used to produce output in equation (20).

19

The necessary first-order conditions19 for maximising lifetime utility (21) subject to the intertemporal constraint (22) are

(23) 11

1

)()1( w

culu

c

l =−

(24) )(11)( 21 curcu cc ρ++

=

(25) 2

1

2

1

11

)1()1(

wwr

lulu

l

l

ρ++

=−−

Equation (23) represents the static optimal trade-off between consumption and leisure analysed in section 2.1. The consumer equalises the marginal rate of substitution between consumption and leisure to the equilibrium wage rate. Equation (24) is the same intertemporal Euler equation as equation (7) in section 3.3. Equation (25) is an intertemporal Euler equation for leisure: at the optimum the ratio of marginal utilities of leisure each period is set equal to the ratio of wages and a factor depending on the interest rate and the rate of time preference. What are the implications of equation (25)? If the interest rate r increases, individuals substitute out of work tomorrow into work today. Individuals face a higher return on saving today (period 1) which increases the incentive to work today and increase lifetime income. Alternatively, the present discounted value of second period wages is lower inducing individuals to work more today. Individual labour supply (denoted by superscript s) is therefore a positive function of relative wages w1/w2 and the interest rate r

,..)/w w,r(l s

)(21)(1

++

and the response depends on the intertemporal elasticity of substitution (IES) of the labour supply (Lucas and Rapping 1969). Notice that the Euler equation (25) can be obtained by substituting the static consumption/leisure trade-off (23) into the consumption Euler equation (24), so the three optimality equations are interdependent. Intuitively an optimal choice of leisure and consumption in each period and optimal consumption path over time implies an optimal intertemporal labour/leisure choice. Mankiw, Rotemberg and Summers (1985) test the validity of equations (22)-(25) for aggregate US data and find that the restrictions implied by the theory are strongly rejected by the data. These negative results are in line with rejections of tests of the intertemporal Euler equation (24) for aggregate consumption data (see Attanasio 1999).

19 Partial derivatives of utility with respect to consumption and leisure are denoted by cuuc ∂∂≡ /

and luul ∂∂≡ / , respectively. A good exercise is to verify the first-order conditions (23)-(25), by setting up the Lagrangian L = u(c1,1-l1) + u(c2,1-l2)/(1+r) + λ[w1l1 + w2l2/(1+r) - c1 - c2/(1+r)].

20

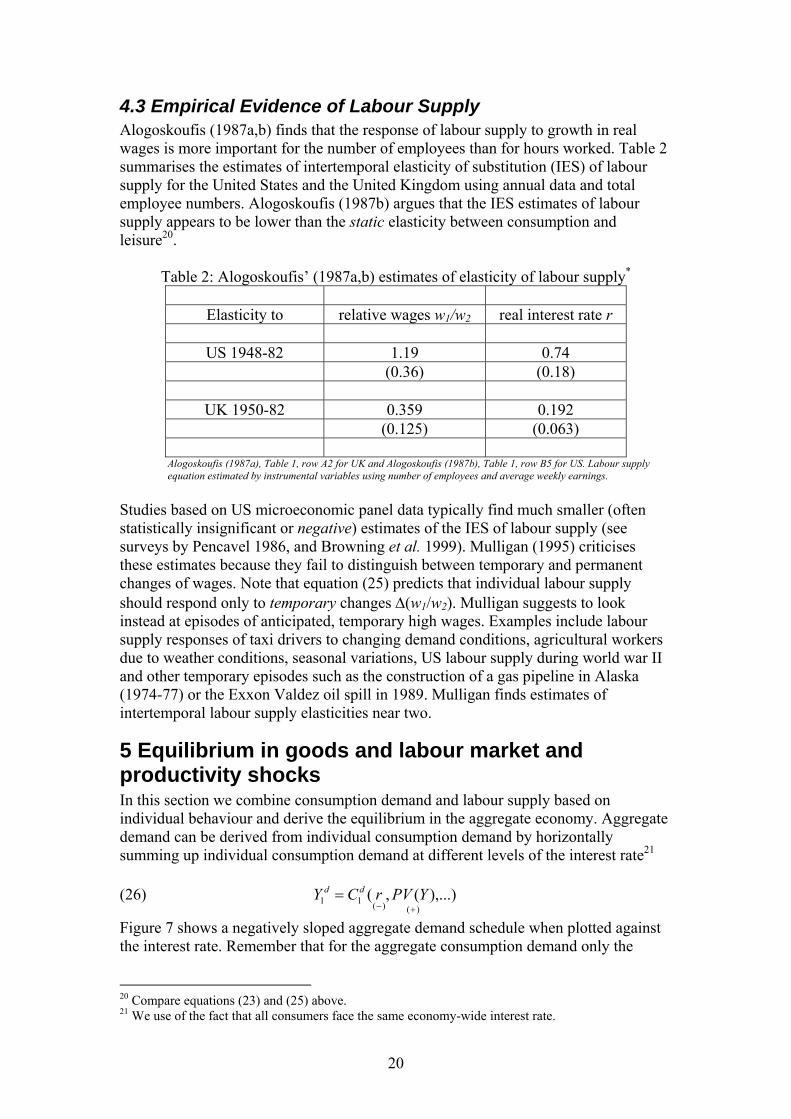

4.3 Empirical Evidence of Labour Supply Alogoskoufis (1987a,b) finds that the response of labour supply to growth in real wages is more important for the number of employees than for hours worked. Table 2 summarises the estimates of intertemporal elasticity of substitution (IES) of labour supply for the United States and the United Kingdom using annual data and total employee numbers. Alogoskoufis (1987b) argues that the IES estimates of labour supply appears to be lower than the static elasticity between consumption and leisure20.

Table 2: Alogoskoufis’ (1987a,b) estimates of elasticity of labour supply*

Elasticity to relative wages w1/w2 real interest rate r

US 1948-82 1.19 0.74 (0.36) (0.18)

UK 1950-82 0.359 0.192 (0.125) (0.063)

Alogoskoufis (1987a), Table 1, row A2 for UK and Alogoskoufis (1987b), Table 1, row B5 for US. Labour supply equation estimated by instrumental variables using number of employees and average weekly earnings.

Studies based on US microeconomic panel data typically find much smaller (often statistically insignificant or negative) estimates of the IES of labour supply (see surveys by Pencavel 1986, and Browning et al. 1999). Mulligan (1995) criticises these estimates because they fail to distinguish between temporary and permanent changes of wages. Note that equation (25) predicts that individual labour supply should respond only to temporary changes Δ(w1/w2). Mulligan suggests to look instead at episodes of anticipated, temporary high wages. Examples include labour supply responses of taxi drivers to changing demand conditions, agricultural workers due to weather conditions, seasonal variations, US labour supply during world war II and other temporary episodes such as the construction of a gas pipeline in Alaska (1974-77) or the Exxon Valdez oil spill in 1989. Mulligan finds estimates of intertemporal labour supply elasticities near two.

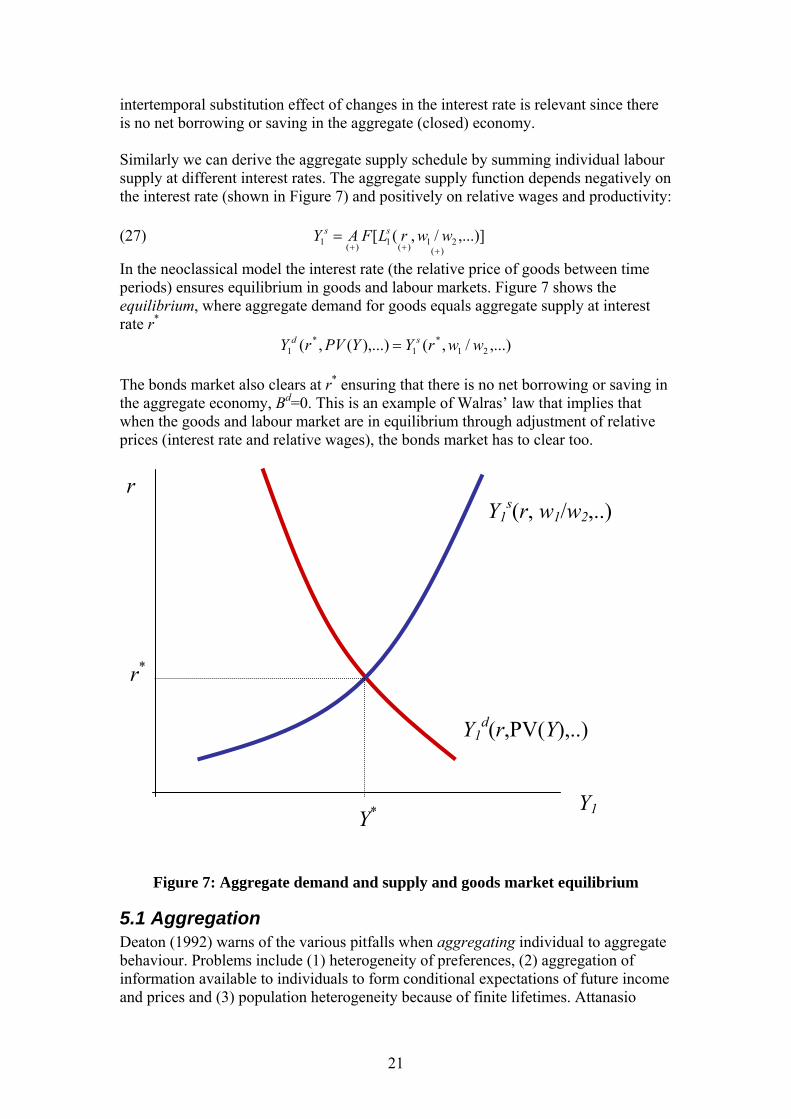

5 Equilibrium in goods and labour market and productivity shocks In this section we combine consumption demand and labour supply based on individual behaviour and derive the equilibrium in the aggregate economy. Aggregate demand can be derived from individual consumption demand by horizontally summing up individual consumption demand at different levels of the interest rate21 (26) ,...))(,(

)()(11+−

= YPVrCY dd

Figure 7 shows a negatively sloped aggregate demand schedule when plotted against the interest rate. Remember that for the aggregate consumption demand only the

20 Compare equations (23) and (25) above. 21 We use of the fact that all consumers face the same economy-wide interest rate.

21

intertemporal substitution effect of changes in the interest rate is relevant since there is no net borrowing or saving in the aggregate (closed) economy. Similarly we can derive the aggregate supply schedule by summing individual labour supply at different interest rates. The aggregate supply function depends negatively on the interest rate (shown in Figure 7) and positively on relative wages and productivity: (27) ,...)]/,([

)(21)(1)(1

+++= wwrLFAY ss

In the neoclassical model the interest rate (the relative price of goods between time periods) ensures equilibrium in goods and labour markets. Figure 7 shows the equilibrium, where aggregate demand for goods equals aggregate supply at interest rate r*

,...)/,(),...)(,( 21*

1*

1 wwrYYPVrY sd = The bonds market also clears at r* ensuring that there is no net borrowing or saving in the aggregate economy, Bd=0. This is an example of Walras’ law that implies that when the goods and labour market are in equilibrium through adjustment of relative prices (interest rate and relative wages), the bonds market has to clear too.

Figure 7: Aggregate demand and supply and goods market equilibrium

5.1 Aggregation Deaton (1992) warns of the various pitfalls when aggregating individual to aggregate behaviour. Problems include (1) heterogeneity of preferences, (2) aggregation of information available to individuals to form conditional expectations of future income and prices and (3) population heterogeneity because of finite lifetimes. Attanasio

r

Y1

Y1d(r,PV(Y),..)

Y1s(r, w1/w2,..)

r*

Y*

22

(1999) criticizes the practice of using aggregate macroeconomic data to estimate microeconomic (structural) parameters since these estimates are likely to be systematically biased. Recent business cycle research therefore often goes the opposite route of imposing parameters estimated from microeconomic relations when calibrating macroeconomic models. See the Prescott-Summers (1986) debate for a discussion of the pros and cons of this calibration approach.

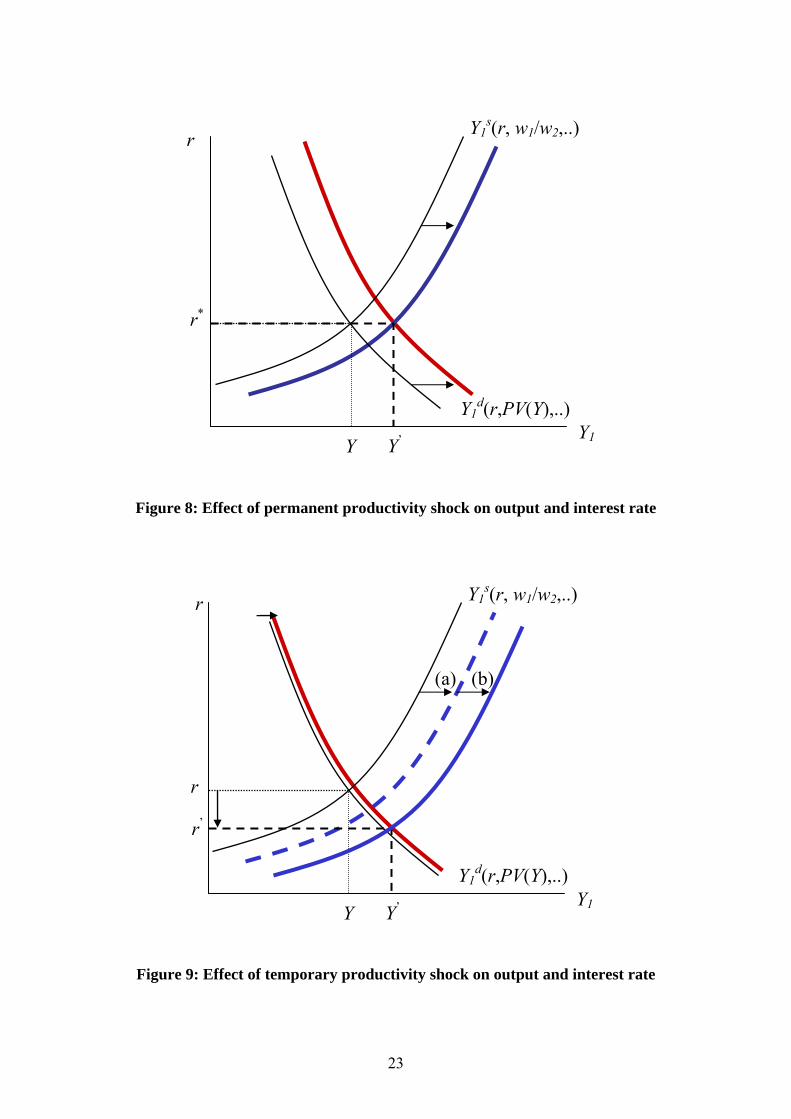

5.2 Productivity shocks What are the consequences of changes in productivity on aggregate demand and supply and the interest rate in equilibrium. Let us analyse permanent and temporary productivity changes in turn.

5.2.1 Permanent productivity shock Consider first a permanent productivity shock -- productivity increases in all periods from today onwards, ∆A1=∆A2=…>0. This case is shown in Figure 8. 1. The direct (mechanical) effect is an increase in output for every level of the labour

supply and for a given interest rate which is shown as rightward shift of the aggregate supply function.

2. The indirect effects (associated with economic decisions) are as follows: - labour supply remains unchanged since relative wages are the same; - consumption demand C1

d increases proportionally with changes in current income, since income changes are permanent, ΔC1

d = ΔY1 The total effect combines direct and indirect effects: output increases and the interest rate remains unchanged. This is the case because individuals have no incentive to change intertemporal decisions leaving the relative intertemporal price r unaffected. Notice that supply and demand curves shift by a similar amounts.

5.2.2 Temporary productivity shock Consider next a temporary increase in productivity, only ∆A1>0, future productivity A2,A3,… remains unchanged. Figure 9 shows the combination of the two effects: 1. The direct effect is the same as for a permanent increase in productivity above

leading to a rightward shift of aggregate supply (shift (a) in Figure 9). 2. The indirect effects are as follows:

- labour supply and hence aggregate supply increase because relative wages go up ∆(w1/w2)>0 (shift (b) in Figure 9); - current consumption and aggregate demand shifts by a small amount, ΔC1

d>0, due to an increase in transitory income.

The total effect is a rise in output and a fall of the interest rate. This is the case because individuals attempt to smooth consumption by saving some of the temporary income increases for the future. Notice that in equilibrium the amount consumed changes much more than the small shift of the consumption demand function22. This can be explained by the combined effect of lower interest rates and higher labour income due to higher labour supply. The strength of the effect depends as usual on the IES (see Table 1). 22 Distinguish between a shift of and a movement along the demand function.

23

Figure 8: Effect of permanent productivity shock on output and interest rate

Figure 9: Effect of temporary productivity shock on output and interest rate

r

Y1 Y1

d(r,PV(Y),..)

Y1s(r, w1/w2,..)

r*

Y’Y

r

Y1 Y1

d(r,PV(Y),..)

Y1s(r, w1/w2,..)

r

Y’Y

(a) (b)

r’

24

5.2.3 Theoretical predictions and stylised facts The model predicts a countercyclical response of real interest rates. For US data (see table in section1), interest rates are weakly procyclical which can be reconciled with the model by combining temporary and permanent productivity changes. Real wages are procyclical which is in line with the stylised facts. Empirically, the model predicts a procyclical response of labour supply to changes in productivity. Hansen and Wright (1992) observe that for the US the number of hours fluctuates much more than productivity. Together with the small variation in wages this implies a high IES to reconcile theory and aggregate data. Alternatively, Hansen and Wright argue that the standard neoclassical business cycle model can be augmented with the following features to produce a better empirical fit: (i) indivisible labour, (ii) preferences that are non-separable over time, (iii) home production and (iv) the importance of other shocks such as government spending for business cycles which we analyse next.

6 Government This section introduces the government into the intertemporal model. The government sector (local, state and federal levels combined) is a large part of our economies. Barro (1997, p.439) shows a ratio of total government expenditures23 to GDP averaged over the 1970-85 period of 35% for the US and 44% for the UK. Barro also argues that the size of the government sector strongly increased in the United States over the last 80 years which is in line with the long-run expansion of the share of government to GDP in developed economies. The government spends and collects revenue facing the following budget constraint each period: (28) PMBTrBVG sg

ttgttt /Δ+Δ+=++

Total spending on the left-hand side of (28) consists of spending on goods by the government G, transfers payments V, and interest payments on the stock of government bonds rBg. For simplicity we assume that government bonds pay the same interest rate r as financial markets. Total revenue on the right-hand side of (28) is given by revenue from taxes T, issuing government debt ΔB, and changing the money supply PM s /Δ . To simplify the discussion, we ignore revenue from printing money24 and set ΔMs = 0 in equation (28). Also we do not discuss transfers and set V=0 in (28), even though they are very important component of total public spending (exceeding 50% in the US). Large parts of transfers takes the form of redistributing through the social security system in the US (see also the chapter on “Pensions” in this volume) or between income groups in many European countries25. 23 Notice that total expenditures also include spending not counted as components of GDP, for example transfers payments. This explains the difference to the entry in the table of section 1. 24 This “inflation tax” is a relatively small component of revenue for low inflation countries. 25 Such transfers could distort several intertemporal decisions, for example retirement age, personal savings or decision to take on a job. These issues are however beyond the scope of this survey.

25

6.1 Effect of government spending This section discusses the effect of government spending on intertemporal decisions and the equilibrium in the neoclassical model of section 5. For now, assume that all taxes are lump-sum , that is they are independent of the individuals decision and do not distort economic decisions. An example of such a tax is the poll tax introduced by the Thatcher government in the 1980s. The more realistic case of distortionary taxes will be discussed in section 6.3. We also assume that government never issues any debt and Bt

g = 0 in all periods. This assumption is relaxed in section 6.2. Under these assumptions the government balances its budget every period and its budget constraint (28) is simply:

tt TG = Some types of government spending are likely to be productive. This would be reflected through a positive effect of spending G in aggregate supply:

),( GLAFY = with positive effect on output FG>0 and possibly positive effects on labour productivity as well. Examples of such productive spending are public goods such as police, roads and infrastructure or public education. Some other types of spending are not necessarily productive, but individuals may like them and they enter into their utility function u(c,G) with uG>0. Examples could be parks, public museums, spaceflights to the moon etc. For simplicity, we will focus on the part of government spending that is neither productive nor desirable, but is completely useless, such as buying goods and dumping them into the sea. The advantage of this extreme assumption is that it allows us to focus on the effect of government spending per se without additional effects on production or preferences26. Government spending is a component of the aggregate demand:

111 GCY dd += The intertemporal budget constraint of individuals reflects the reduction in disposable income from the taxes. Equation (5) becomes:

rcc

rTyTy

++=

+−

+−11

21

2211

Lump sum taxes affect individual demand for consumption and supply of labour in the same way as a fall in income in sections 2.1. Consumption demand falls and labour supply increases after an increase in taxes.

26 The effects on production and welfare can be added to the model; see for example Barro (1989).

26

6.1.1 Permanent change in government spending In the neoclassical model the effect of government spending depends on whether the change in government spending is permanent or temporary. Consider first a permanent change in government spending shown in Figure 10 below: 1. The direct effect is an increase aggregate demand for a given interest rate which is

shown as rightward shift (a) of the aggregate demand function. 2. The indirect effects are as follows:

- consumption demand C1d and hence aggregate demand fall by the same amount

as government spending and taxes increase since the implied fall in disposable income is permanent (shown as shift back of aggregate demand); - labour supply and aggregate supply shift (b) to the right because of the negative income effect (notice that relative wages are unchanged); - the resulting increase in permanent income leads to a shift (c) of consumption and aggregate demand.

The total effect of the permanent increase in government spending is an increase in output and an unchanged interest rate. The intuition for this result is that individuals have no incentive to alter their intertemporal decisions. Notice that supply and demand curves shift by a similar amounts and that despite the rise in output an increase in government spending and lump sum taxes means lower disposable income and (through the reduction in consumption and leisure) lower welfare27.

Figure 10: Permanent change in government spending

27 The negative welfare effects of government spending have to be qualified by potential positive effects on productivity and individual welfare discussed in section 6.1 above.

r

Y1

Y1d Y1

s

r*

Y’Y

(b)

(c)

(a)

27

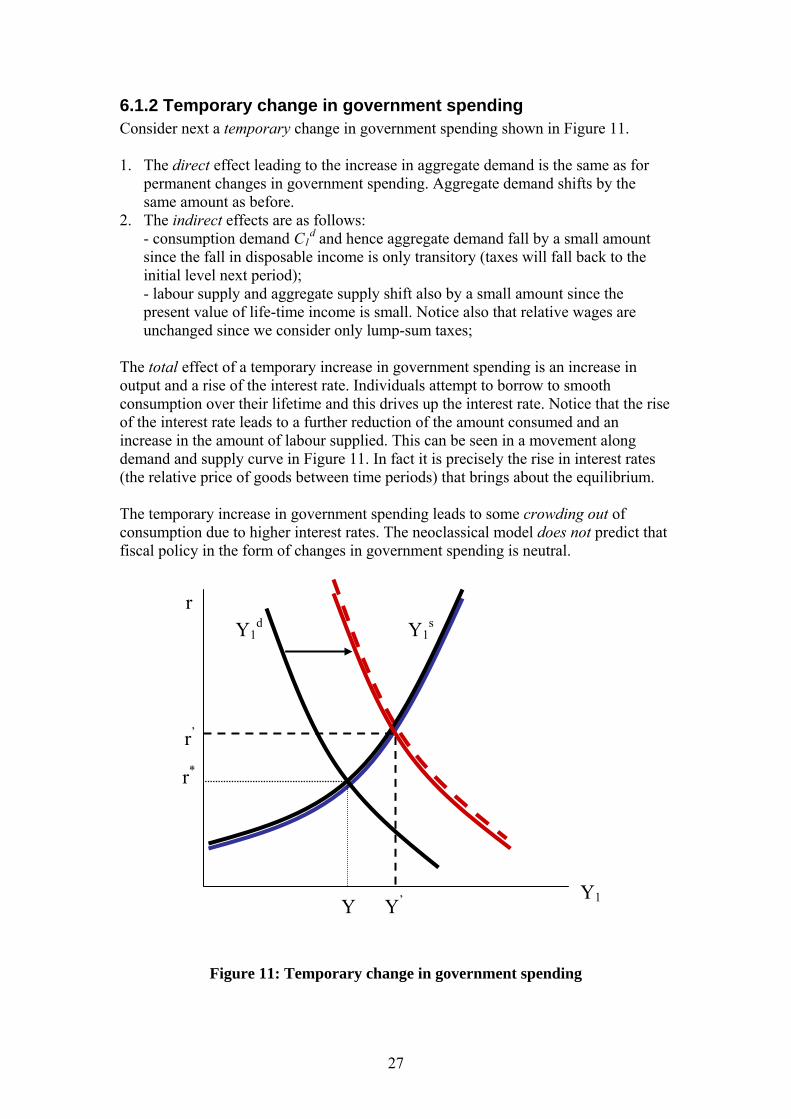

6.1.2 Temporary change in government spending Consider next a temporary change in government spending shown in Figure 11. 1. The direct effect leading to the increase in aggregate demand is the same as for

permanent changes in government spending. Aggregate demand shifts by the same amount as before.

2. The indirect effects are as follows: - consumption demand C1

d and hence aggregate demand fall by a small amount since the fall in disposable income is only transitory (taxes will fall back to the initial level next period); - labour supply and aggregate supply shift also by a small amount since the present value of life-time income is small. Notice also that relative wages are unchanged since we consider only lump-sum taxes;

The total effect of a temporary increase in government spending is an increase in output and a rise of the interest rate. Individuals attempt to borrow to smooth consumption over their lifetime and this drives up the interest rate. Notice that the rise of the interest rate leads to a further reduction of the amount consumed and an increase in the amount of labour supplied. This can be seen in a movement along demand and supply curve in Figure 11. In fact it is precisely the rise in interest rates (the relative price of goods between time periods) that brings about the equilibrium. The temporary increase in government spending leads to some crowding out of consumption due to higher interest rates. The neoclassical model does not predict that fiscal policy in the form of changes in government spending is neutral.

Figure 11: Temporary change in government spending

r

Y1

Y1d Y1

s

r*

Y’Y

r’

28

As an empirical example, consider a temporary increase in government spending during wartime. The model predicts that GDP increases, private consumption falls and labour supply increases during wartimes. These predictions are confirmed by Barro (1997, Table 2.2) when looking at data for the US in four wartime episodes: the two world-wars, the Korean and the Vietnam war. The model also predicts an increase of interest rates during wartime and possibly for some time after the war ends. Barro (1997, pp. 454-59) does not find empirical support for this prediction when comparing average interest rates during and immediately after the four war periods of the US cited above and the US Civil War. However, Barro finds that long-run nominal interest rates are on average 1.0 percentage points higher (relative to an average level of 3.5%) during wars the United Kingdom was fighting between 1730-1918.

6.1.3 Effects of government spending in Keynesian Model Consider now the effect of government spending in the Keynesian model where a fraction λ of consumers is liquidity constrained. As we discussed in section 3.7 the parameter λ can also be interpreted as the marginal propensity to consume (MPC) out of current income in the Keynesian aggregate consumption function (16). If government spending increases and disposable income falls because of higher lump-sum taxes, consumption demand falls by the MPC times the change in disposable income )( 11 TY −Δ×λ in the Keynesian model. Aggregate consumption is predicted to fall by the same amount irrespective of the duration of government spending increases (temporary or permanent). This stands in contrast to the neoclassical model that predicts a small shift in consumption demand resulting from temporary changes in government spending, but a one-for-one shift responding to permanent changes. The models have therefore also different implications for the behaviour of the real interest rate after changes in government spending.

6.2 Budget Deficits and Ricardian equivalence In this section we allow the government to issue debt Bg to finance its expenditures in the budget constraint (28). Since the government is a large part of the economy one might expect increases of the interest rate and resulting crowding out as consequence of more government borrowing. To focus solely on the effect of government borrowing, consider the following “Ricardian experiment”: 1. Suppose the government cuts taxes in period 1 ΔT1<0 and raises taxes the following period to pay for debt and interest (accumulated at rate r): 12 )1( TrT Δ+−=Δ ; 2. the path of government spending G1, G2, G3,… is left unchanged; 3. taxes after period 2, T3, T4,… are left unchanged. What are the effects of this Ricardian experiment in the different models that we analysed so far? The answer depends crucially on the time horizon of individuals.

29

First, consider individuals with an infinite horizon28 as in the Permanent Income Hypothesis (PIH) of section 3.5.2. The relevant part of the individuals budget constraint affected by the Ricardian experiment becomes:

...1

...1

2211

21 +

+Δ−

+Δ−=++

+rTyTy

rcc

Since the tax cut in period 1 is offset by a tax increase in period 2 to pay for the debt and interest )1/(21 rTT +Δ=Δ− , the lifetime budget constraint of the individual is not changed. Alternatively, the present value of future tax increases exactly offsets current tax cuts. In the PIH model debt issued by the government in period 1 does not constitute net wealth and leaves individual decision completely unaffected. This strong neutrality result is called Ricardian equivalence (Barro 1974). Second, suppose that individuals behave as in the life-cycle hypothesis (LCH) of section 3.5.1. The important difference to the PIH case above is that some consumers will die at the end of period 1 and will not be around to pay off the debt in period 2. If individuals do not care about future generation and do not leave behind any bequests then the tax cut increases disposable income of those consumers whose horizon is shorter than the time of future tax increases. Third, the Keynesian model predicts that liquidity constrained consumers consume all of the additional disposable income resulting from the tax cut in period 1. Consumption would increase by the marginal propensity to consume λ and labour supply would decrease. The empirical relevance of this resukt depends on the importance of liquidity constraints (see discussion in section 3.7). Bernheim (1989) criticises the assumption behind the Ricardian equivalence result that individuals behave as if living in an infinitely lived dynasty. If families are inter-related by marriage instead this would ultimately imply that all individuals are mutually related through some distant family link. The surprising conclusion is too much or super-neutrality (see Bernheim and Bagwell 1988). The PIH and life-cycle models differ mainly with respect to the empirical importance of bequests or intergenerational transfers more broadly, for example through parental investment in education of their children. Kotlikoff and Summers (1981) estimate the contribution of wealth accumulation due to intergenerational transfers to be sizeable compared to life-cycle savings. This leaves open the distribution of bequests across income groups and whether bequests are intentional.

6.3. Taxes Governments are taxing a variety of economic activities to collect revenue: income, consumption (VAT), profits, businesses, property, goods etc. Individual income taxes alone accounted for 42% of federal revenues in the US in 1991 (Barro 1997). In practice most taxes are distortionary and not lump-sum as we assumed so far.

28 More precisely the horizon over which individuals are planning equals the government’s horizon.

30

With lump-sum as well as distortionary taxes at rate τ, the individual’s budget constraint (5) becomes:

rc

cr

TyTy ~1~1

)1()1( 2

122

11 ++=

+−−

+−−τ

τ

where the after-tax interest rate is at rate )1(~ τ−= rr . To focus on the additional effect29 of the distortion we replace a lump-sum tax by a distortionary income tax. This will induce a negative substitution effect out of the taxed activity (work) into the non-taxed one (leisure). Note that this substitution effect comes in addition to a negative wealth effect from lump-sum taxation. Figure 11 shows the effect of replacing lump-sum by distortionary income taxes. First, there are only indirect effects since production is not taxed. Labour supply and hence aggregate supply shift left by amount (a) because of the negative substitution effect. Due to the fall in income consumption and aggregate demand shift left by the same amount (b). The total effect is a reduction in output, labour supply and consumption. The interest rate stays constant since intertemporal plans are not affected.

Figure 12: Effect of replacing lump-sum by distortionary income tax

29 Combining the results in sections 6.1 to 6.3 we can analyse the effect of a combination of policies. For example, a temporary increase in government spending in period 1 financed be distortionary taxes in period 2 can be viewed as (1) 11 TG Δ=Δ , (2) 21 TT Δ=Δ− and (3) 22 YT τ=Δ− .

r

Y1

Y1d

Y1s

r*

Y’ Y

(a)

(b)

31

7 Concluding Remarks This chapter discusses models of intertemporal models30 of consumption and labour markets. Microfounded models provide important insights into aggregate economic behaviour such as aggregate consumption and savings behaviour or labour market fluctuations. Aggregation problems from microeconomic behaviour are clearly an issue and should be taken into considerations in empirical work. The models discussed in this chapter are necessarily very simple and imply strong restrictions on aggregate data. Several alternatives and generalisations allowing for more realistic behaviour have been discussed. As usual in economic modelling there is a trade-off between theoretical simplicity and empirical fit.

30 Due to space constraints this chapter does not discuss investment and its implications for business cycle behaviour. See for example the chapters on investment in Barro (1997) or Romer (2001).

32

References Abel, A.B. (1990). “Consumption and Investment.” In B.M. Friedman and F.H. Hahn (eds.), Handbook of Monetary Economics. Vol. II. North-Holland: Elsevier. Alogoskoufis, G.S. (1987a). “Aggregate Employment and Intertemporal Substitution in the UK.” Economic Journal 97 (June): 403-15. Alogoskoufis, G.S. (1987b). “On Intertemporal Substitution and Aggregate Labor Supply.” Journal of Political Economy 95 (5), Oct., 938-60. Angeletos, G.-M., D. Laibson, A. Repetto, J. Tobacman, and S Weinberg (2001). “The Hyperbolic Consumption Model: Calibration, Simulation, and Empirical Evaluation.“ Journal of Economic Perspectives 15(3): 47-68. Attanasio, O.P. (1999). “Consumption.” In J.B. Taylor and M. Woodford (eds) Handbook of Macroeconomics, Vol. 1. North-Holland: Elsevier. Attanasio, O.P. and G. Weber (1993). “Consumption Growth, the Interest Rate and Aggregation.” Review of Economic`Studies 60: 631-49. Barro, R.J. (1974). “Are Government Bonds Net Wealth?” Journal of Political Economy 82: 1095-117. Barro, R.J. (1989). “The Neoclassical Approach to Fiscal Policy.” In R.J. Barro (ed.) Modern Business Cycle Theory. Cambridge: Harvard Univ. Press. Barro, R.J. (1997). Macroeconomics. 4th edition. Cambridge: MIT Press. Beaudry, P. and E. Van Wincoop (1996). “The intertemporal elasticity of substitutions: an exploration using a US panel of state data.” Economica 63: 495-512. Bernheim, B.D. (1989). “A Neoclassical Perspective on Budget Deficits.” Journal of Economic Perspectives 3(2): 55-72. Bernheim, B.D. and K. Bagwell (1988). “Is Everything Neutral?” Journal of Political Economy 96: 308-38. Blanchard, O.J. (1990). “Why Does Money Affect Output? A Survey.” In B.M. Friedman and F.H. Hahn (eds.), Handbook of Monetary Economics. Vol. 2. North-Holland: Elsevier. Blundell, R., M. Browning and C. Meghir (1994). “Consumer Demand and the Lifetime Allocation of Consumption.” Review of Economic`Studies 61:57-80. Browning, M and T.F. Crossley (2001). “The Life-Cycle Model of Consumption and Saving.” Journal of Economic Perspectives 15(3): 3-22.

33

Browning, M, L.P. Hansen and J.J. Heckman (1999). “Micro Data and general Equilibrium Models.” In J.B. Taylor and M. Woodford (eds.), Handbook of Macroeconomics. Vol. 1A. North-Holland: Elsevier. Campbell, J.Y. and A. Deaton (1989). “Why Consumption Is So Smooth.” Review of Economic Studies 56: 357-74. Campbell, J.Y. and N.G. Mankiw (1989). “Consumption, Income and Interest Rates: Reinterpreting the Time Series Evidence.” In: O.J. Blanchard and S. Fischer (eds.), NBER Macroeconomics Annual 1989: 185-216. Cambridge: MIT Press Campbell, J.Y. and A. Deaton (1989). “Why is Consumption so Smooth?” Review of Economic Studies 56: 357-74. Carroll, C. D. (2001), A Theory of the Consumption Function, With or Without Liquidity Constraints. Journal of Economic Perspectives 15 (3): 23-45. Deaton, A. (1992). Understanding Consumption. Oxford: Clarendon Press. Dixit, A. (1990). Optimization in Economic Theory. 2nd edition. Oxford: Oxford Univ. Press. Fisher, I. (1907). The Rate of Interest, New York: Macmillan. Flavin, M. (1981). “The Adjustment of Consumption to Changing Expectations About Future Income.” Journal of Political Economy 89: 974-1009. Friedman, M. (1957). A Theory of the Consumption Function. Princeton Univ. Press. Hall, R.E. (1978). Stochastic Implications of the Life Cycle-Permanent Income Hypothesis: Theory and Evidence. Journal of Political Economy 86(6), December, 971-87. Hall, R.E. (1988). “Intertemporal Substitution in Consumption.” Journal of Political Economy 96: 339-57. Hall, R.E. and F.S. Mishkin (1982). “The Sensitivity of Consumption to Transitory Income: Estimate From Panel Data on Households.” Econometrica 50: 461-81. Hansen, G.D. and R. Wright (1992). “The Labor Market in Real Business Cycle Theory.” Federal Reserve Bank of Minneapolis Quarterly Review, Vol. 16 (2), Spring. Available at http://minneapolisfed.org/research/qr/ Hayashi, F. (1987). “Tests for Liquidity Constraints: A Critical Survey and Some New Observations.” In: T.F. Bewley (ed.) Advances in Econometrics: Fifth World Congress, Vol. II: 91-120. Keynes, J.M. (1936). The General Theory of Employment, Interest, and Money. London: Macmillan.

34

Kotlikoff, L.J. and L.H Summers (1981). “The Role of Intergenerational Transfers in Aggregate Capital Accumulation.” Journal of Political Economy 89(4): 706-32. Loewenstein, G. and R.H. Thaler (1989). “Anomalies: Intertemporal Choice.” Journal of Economic Perspectives 3(4): 181-93. Lucas, R.E. Jr. and L. Rapping (1969). “Real Wages, Employment and Inflation.” Journal of Political Economy 77, September/October, 721-54. Mankiw, N.G., J.J. Rotemberg, and L.H. Summers (1985), “Intertemporal Substitution in Macroeconomics.” Quarterly Journal of Economics 100: 225-51. Modigliani, F. (1986). “Life Cycle, Individual Thrift, and the Wealth of Nations.” American Economic Review, 76(3), June, 297-313. Mulligan, C.B. (1995). "The Intertemporal Substitution of Work—What Does the Evidence Say?" University of Chicago, Population Research Center. Discussion-Paper 95-11. June. Mulligan, C.B. (1998). “Pecuniary Incentives to Work in the United States during World War II.” Journal of Political Economy 106(5): 1033-77. Obstfeld, M. and K. Rogoff (1996). Foundations of International Macroeconomics. MIT Press. Pencavel, J. (1986). “Labor Supply of Men: A Survey.” In: by: O.C. Ashenfelter and R. Layard (eds.) Handbook of Labor Economics, Vol 1. North-Holland: Elsevier. Prescott-Summers Debate (1986). Federal Reserve Bank of Minneapolis Quarterly Review, Vol. 10(4), Fall. Available at http://minneapolisfed.org/research/qr/ Ramsey, F. (1928). “A Mathematical Theory of Saving.” Economic Journal 38: 543-59. Romer, D. (2006). Advanced Macroeconomics. 3rd edition. McGraw-Hill.