Embed Size (px)

DESCRIPTION

A Report on Islami Bank

Citation preview

2013

1.0 Introduction:

The Jews in Jerusalem introduced a kind of banking in the form of money lending before the

birth of Christ. The word 'bank' was probably derived from the word 'bench' as during ancient

time Jews used to do money -lending business sitting on long benches.

First modern banking was introduced in 1668 in Stockholm as 'Savings Pis Bank’, which

opened up a new era of banking activities throughout the European Mainland.

In the South Asian region, early banking system was introduced by the Afgan traders

popularly known as Kabuliwallas. Muslim businessmen from Kabul, Afganistan came to

India and started money-lending business in exchange of interest sometime in 1312 A.D.

They were known as 'Kabuliawallas'. The financial system of Bangladesh consists of

Bangladesh Bank (BB) as the central bank, 4 nationalized commercial banks (NCB), and 5

government owned specialized banks, 30 domestic private banks, 10 foreign banks and 28

non-bank financial institutions. The financial system also embraces insurance companies,

stock exchanges and co-operative banks

1.1 Brief scenario of Bangladesh:

With the rapid growing competition (due to free market economy) among nationalized,

foreign and private commercial banks as to how the banks operates its banking operation and

how customer service can be made more attractive, the expectation of the customers has

immensely Increased. Reciprocating the sentiment, commercial/private banks are trying to

elevate their traditional banking service to a better standard, to meet the challenging needs,

demands. Side by side these banks have now concentrated their attention towards

diversification of their products for better performances and existence. For the above

circumstances, it has become necessary for Social Islami Bank Ltd, one of the leading

commercial banks, to focus its attention towards the improvement of the customer service.

That’s why it is quite justified to make an in-depth study about its operation and evaluate the

service provided by this bank and scope for its improvement. The study may help formulating

policy regarding the ideas relating to the feelings of the customers and bankers. Further more,

Social Islami Bank Ltd executives who are actually executing the policies undertaken by the

top management will have a chance to communicate their feelings and will have the feedback

about their dealing from the customers.

PRESIDENCYUNIVERSITY 1

2013

1.2 Significance of the Report:

The major motive of this study is to become familiar with the practical business world and to

attain practical knowledge about the overall Banking, which is so much essential for each and

every student to meet the extreme growing challenges in job market. This report finding’s

will be beneficial for the management in attempting to improve the overall service quality

and also to promote the company’s services to customers. So the study will be very useful for

the top management in improving the customer satisfaction. Besides, it would be a great

opportunity for me to attain practical knowledge on the various spheres of banking business.

So this study is very significant for both the company and me.

1.3 Origin Of The Report:

This report is one of the major parts of BBA Program offered by Presidency University

Bangladesh. In today’s world, education is not just limited to books and classrooms.

Education now-a-days is understanding the real world and applying knowledge and education

for the betterment of the society. So the Internship is such a way that helps to apply the

knowledge and understanding of the courses and to use them in a practical field. Social

Islami Bank Limited gives me this opportunity to be engaged there to gather practical

experience about the real business world and to observe different practical aspects of

education.

1.4 Objectives of the Report:

1. To understand the General Banking and Investment products used by the

Bashundhara Branch of Social Islami Bank Ltd.

2. To be acquainted with how bank perform its operation.

3. To focus on products, services and financial condition of SIBL.

4. To export strengths and weakness of SIBL in comparison with competitors.

5. To analysis general banking activities of Social Islami Bank Limited.

6. To analysis the financial performance of SIBL.

PRESIDENCYUNIVERSITY 2

2013

1.5 Methodology:

A certain methodology was followed in order to fulfill the objectives of the report,

making maximum utilization of the scopes and to avoid the limitations as much as

possible to prepare the final outcome of this report.

Sources of Information

I have collected the information/data from the following sources, which has helped me to

make this report. The source is divided into two parts:

a) Primary Source.

b) Secondary Source.

1 The “Primary Sources” are as follows:

Data collected for the first time is called primary data. The methods used to collect such data

include:

Face-to-face conversation with the respective officers and staffs of the Branch.

Informal conversation with the clients.

Practical work exposures from the different desks of the departments of the

Branch covered.

2 The “Secondary Sources” of data and information are:

The secondary data sources are annual reports, manuals, and brochures of Social Islami Bank

limited and different publications of Bank. To identify the implementation, supervision,

monitoring and repayment practice- interview with the employee and extensive study of the

existing files.

Methods used to collect secondary data include:

Annual Report of Social Islami Bank Ltd and

Internet.

PRESIDENCYUNIVERSITY 3

2013

Data Analysis and Reporting:

Data have been analyzed through proper quantitative and qualitative techniques and reported

from time to time to the concerned authority. After collecting data, they were coded and

processed, analyzed and graphically used MS word, MS Excel. Tables and graphs were used

to make the data meaningful and comparable.

1.6 Scope Of Study:

Internship experience plays a vital role for every student to implement their theoretical

knowledge and get a practical knowledge from any organization. A student can

implement this internship experience in his future work area. Social Islami Bank

Limited gives me the opportunity for gathering practical experience and preparation

of the report. Finally I prepared this report under the supervision Ms.Annesha Zeheen,

Lecturer, of Presidency University, Bangladesh

1.7 Limitation of the study

It is obvious that every study has some limitations. The study I have made is of great

importance and required me huge work. Those limiting factors that hampered my smooth

workings in bank and finally in preparing this report are as following:

Time Limitation: Within such a short period of time, it was not possible for me to study

everything about Social Islami Bank, Bashundhara Branch.

Confidentiality: In order to guard the secrecy of the bank, Social Islami Bank Ltd. is not

interested to disclose some certain information required for this report.

Lack of Co-operation: As the bank officials are so much busy that it difficult for them to co-

operate with me, which is also a constraint for this report.

PRESIDENCYUNIVERSITY 4

2013

The organization maintains strict confidentiality about their financial and other

information. They are afraid of any type of information leakage to their competitors. So

there was always difficulty to have appropriate information from them.

Duration of the study was too short to have a sound understanding of the overall

banking.

Scope of my study is so wide that analytical and comprehensive study is not possible.

Lack of sufficient books, papers and journals etc.

Web site of the Organization isn’t up to date to gather valuable information.

PRESIDENCYUNIVERSITY 5

2013

2.0 Introduction:

Social Islami Bank Limited was incorporated in Bangladesh in the year 1995 as a banking

company under the companies Act, 1994. Since its establishment, it has come forward as a

private commercial bank and very encourage has come forward as the stimulator of economic

activities in the country. The bank has been entrusted with the responsibility of undertaking

various steps related to the development of the country’s commercial, industrial and

agricultural sectors. The banking sector of a country is called the economic barometer of the

country. As a pioneer commercial bank in the private sector in Bangladesh, Social Islami

Bank provides considerable financial helps to the business sector that imports industrial

goods and/or exports excess production outside the country for profit. Thus for imports the

Social Islami Bank provides LIM (Loan against Import Merchandise) and LTR (Loan against

Trust Receipt) facility and for exports provides both pre shipment and post shipment

finances. Thus with these bank helps the prospects in the business sector has increased more

than ever before.

For coordinating my internship I have been place in Social Islami Bank Limited, Basundhara

Branch, Dhaka. There are 03 sections in Bashundhara Branch. They are: 1) General Banking,

2) Investment Department, 3) Cheque Clearance Department . I shall devote my utmost effort

and attention to learn banker’s functions. After completion of the internship, I will render my

all knowledge to present the report .

2.2 Historical Background of SIBL:

Social Islami Bank Limited (SIBL) is a banking company registered under the companies Act

1994 with its head office in 15 Dilkusha C/A, Dhaka-1000. The bank operates as a scheduled

bank under a banking license issued by the Bangladesh Bank, Central Bank of the country.

The Bank started its operation from 22, November 1995. SIBL is a capitalized new

generating Bank with an authorized capital and paid up capital of Taka 585 million in 2007

and also 585 million respectively as of December 2006. The bank under takes all types of

banking transaction to support the development of trade and commerce in the country. SIBL

services are also available for the entrepreneurs to set up new venture and BMRE of

industrial units. To provide clientele services in respect of international trade it has

established wide corresponded banking relationship with local and foreign bank stride and

financial interest home and abroad. Since the very inception, Social Islami Bank Ltd. is

PRESIDENCYUNIVERSITY 6

2013

working with the philosophy of serving the nationals as an ideal and unique financial house.

Every organization has some objectives of its own. The prime objective of Social Islami

Bank Ltd. is to earn profit throw undertaking Social Islami Bank Limited Page 9

the responsibility of providing financial help for the development of the country’s

commercial and industrial sector. Now the year 2012 is envisaged as a golden year of SIBL.

Adopting new strategic Business Policy, SIBL will leave no stone unturned to boost business

in all areas of operation to achieve its corporate goals.

2.3 Overview Of The Bank:

Social Islami Bank Ltd. (SIBL) became operational on 22 November 1995 with a clear

manifesto to demonstrate the operational meanings of participatory economy, banking and

financial activities as an integrated part of an Islamic code of life. SIBL is operating three-

sector Banking, such as, Formal, Non-Formal and Voluntary sector, SIBL is beginning a new

area of Islamic Banking having social, ethical and moral dimension in each of its activities

ranging from credit to construction, trading to transport, farming to fishing, manufacturing to

mining and so on. Some renowned personalities and institutions are sponsors and directors of

this bank, specially, the Founder Chairman Prof. Dr. M. A Mannan, who is an internationally

reputed. Islamic thinker and Professional Economist. He served in different important

capacities in different International Organizations including Asian Development Bank and

Islamic Development Bank. With his heartiest efforts and inspiration Ex-Secretary General of

O.I.C Dr. Hamid AI-Gabid and Deputy Speaker of Saudi Arabia and former Secretary

General of Rabeta, Dr. Abdullah Omar Nasseef, and Ex-Commerce Minister of Saudi Arabia

Salah Jamjoom took part in the establishment of the Bank.

Social Islami Bank Limited (SIBL) is a banking company registered under the companies Act

1994 with its heads office 15 Dilkusha C/A, Dhaka-1000. The bank operates as a scheduled

bank under a banking license issued by the Bangladesh Bank. The Bank started its operation

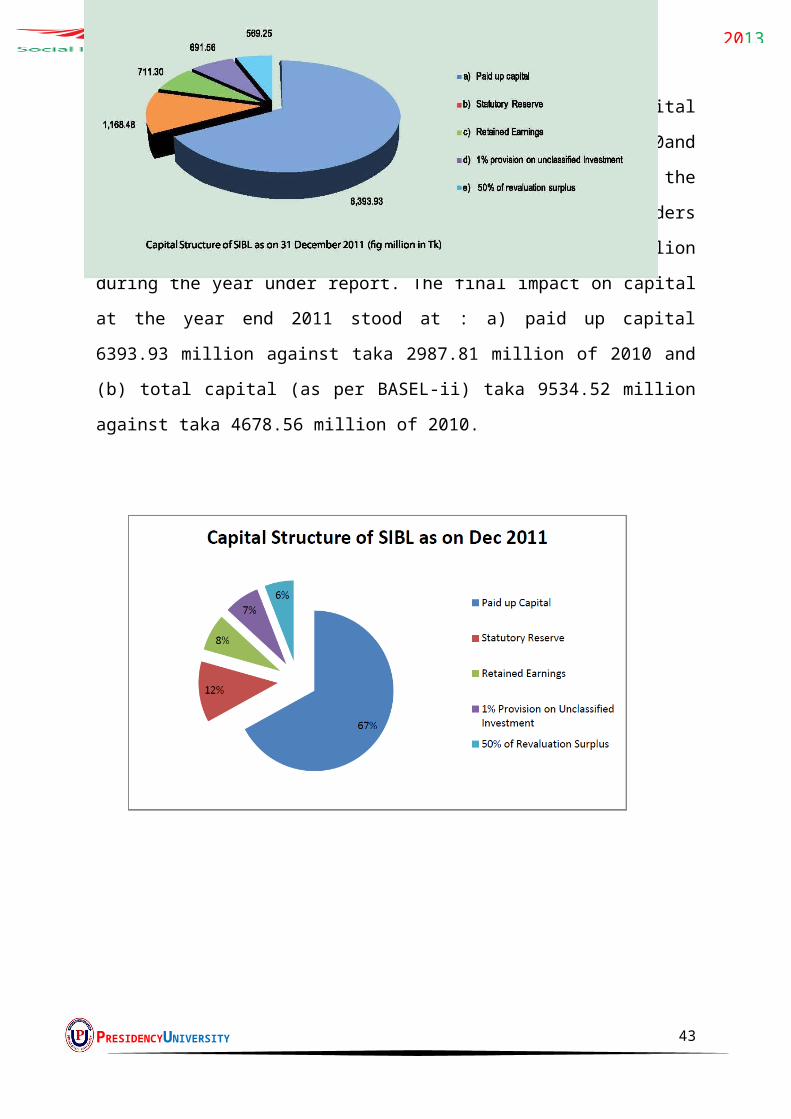

from 22, November 1995. The final impact on capital at the year end 2011 stood at : a)

aid up capital 6393.93 million against taka 2987.81 million of 2010 and (b) total

capital (as per BASEL-ii) taka 9534.52 million against taka 4678.56 million of 2010.

PRESIDENCYUNIVERSITY 7

2013

2.4 The Vision:

Social Islami Bank Limited started its journey with the concept of 21st Century Islamic

participatory three sector banking model: i) Formal Sector- Commercial banking with latest

technology; ii) Non-formal Sector-Family empowerment Micro-credit & Micro-enterprise

program and iii) Voluntary Sector- Social Capital mobilization through CASH WAQF and

others. Finally, “Reduction of Poverty Level” is the Vision, which is a prime object as started

in Memorandum of Association of the Bank with the commitment “Working Together for a

Caring Society.”

2.5 The Mission:

1. High quality financial services with the latest technology.

2. Fast, accurate and satisfactory customer service.

3. Balanced & sustainable growth strategy.

4. Optimum return on shareholders’ equity.

5. Introducing innovative Islamic banking products.

6. Attract and retain high quality human resource.

7. Empowering real poor families and create local income opportunities.

8. Providing support for social benefit organizations-by way of mobilizing funds and

social services.

2.6 Our Values:

1. Honesty .

2. Transparency.

3. Efficiency.

4. Accountability .

5. Reliability.

6. Innovation.

7. Flexibility.

8. Security.

9. Technology.

PRESIDENCYUNIVERSITY 8

2013

2.7 Goal:

Social Islami Bank has efficient and experienced staff for giving better service to its clients

along with modern technology.

Non-formal sector

The Bank’s special program is directed mainly to up-lift the socio-economic conditions of

rural and urban poor. In order to achieve this objective, Social Islami Bank Ltd. is involved in

the mobilization and utilization of local resources and the surplus labor mainly from within

and provide employment opportunities to the unemployed and the landless besides investing

in N.G.O. activities, educational, health expansion activities etc. Social Fellowship Program

for Students has already been introduced; Family health service cheque is being introduced.

Investment voluntary sector:

This Bank has a special program of development of various religious and social service

oriented institutions. Within this program, Mosque, Maktab, Waqf, Charitable organizations

etc. All properties under this program will be utilized in productive activities on participation

basis. Besides, Hajj (pilgrimage) and Kurbani (sacrifice of animals according to dictates of

Islam) schemes are included in the program of Social Islami Bank Ltd Cash Waqf Certificate

has already been introduced for the first time in history.

2.8 Product and service:

Mudaraba Term Deposit

Mudaraba Savings Deposit

Al-Wadia Current Account

Mudaraba Notice Deposit

Mudaraba Scheme Deposit

Mudaraba Hajj Savings Deposit

Mudaraba Monthly Savings Scheme

Mudaraba Special Deposit Pension Scheme (5 Years)

Mudaraba Monthly Profit Deposit Scheme

Mudaraba Education Deposit Scheme

PRESIDENCYUNIVERSITY 9

2013

Mudaraba Home Saving Scheme

Mudaraba Millinery Deposit Scheme

ATM Service

Locker Service

Online Banking

PRESIDENCYUNIVERSITY 10

2013

3.0 GENERAL BANKING:

General banking department aids in taking deposits and simultaneously provides some

ancillaries services. General banking is the front side banking services department. It

provides those customers who come frequently and those customers who come one time in

banking for enjoying ancillary services. In some general banking activities, there is no

relation between banker and customers who will take only one service from bank. On the

other hand, there are some customers with who banks are doing its business frequently. SIBL

(Social Islami Bank Limited) General banking is divided into five sections.

1. Account Opening activities

2. Bills and Clearing activities

3. Cash activities

4. Remittance activities

5. Closing of an Account activities.

3.1 Account Opening Section:

Under this section, SIBL officer opens different types of account on the request of clients.

The procedure of opening account is given below.

Procedure and rules to open a new account:

Mudaraba Saving Account (Code No: 134)

Before opening of a savings Bank Account the following formalities must the completed by

the customers:

1. Account opening From: To be filled in and signed by each account holder.

2. Latest passport size photograph (2 copies) for each account holder attested by the

introducer.

3. Account payee cheque in favor of the account holder or cash deposit.

4. Copy of Voter identity card/Ward Commissioner Certificate.

5. Introduction of account holder (Mandatory): To be signed by introducer with ID and

account number.

6. 1 (One) copy of nominee’s photograph (attested by the account holder).

PRESIDENCYUNIVERSITY 11

2013

7. Copy of voter identity card (nominee).

8. Initial deposit TK. 1000 (One thousand taka only)

After fulfilling above formalities, open an account for the client and provide the customer

with a deposit book and a checkbook.

Al-Wadiah Current account (Individual) – (Code No: 133)

1. Account opening From: To be filled in and signed by each account holder.

2. Latest passport size photograph (2 copies) for each account holder attested by the

introducer.

3. Attested copy of valid Trade license.

4. Attested copy of passport of the proprietor.

5. Company seal and TIN (Tax identification Number) Certificate.

6. Copy of Voter identity card.

7. Introduction of account holder (Mandatory): To be signed by introducer with ID and

account number.

8. 1 copy of nominee’s photograph (attested by the account holder).

Mudaraba Special Notice Account (Code No: 136)

1. Any company, business entity, debt of the govt. organization and trust or any person

can open this account.

2. This account is operated under Mudaraba principle.

3. Any amount can be withdrawn or transferred to al Wadiah current account or any

other accounts after placing a notice of seven days.

4. Cheque books are provided for these accounts.

5. The profit rate is comparatively lower.

PRESIDENCYUNIVERSITY 12

2013

3.2 Deposits Account by SIBL:

Mudaraba Saving Deposits (MSD) (Code No: 134)

These are profit bearing deposit account. The drawings are restricted in respect of both the

amount of withdrawal and the frequency there of so the payment of interest does not become

any compensating for the banker. Some time the restrictions are ignored against the

depositor’s written confirmation to forgo his claim for interest on the total balance for the

whole month of withdrawal.

Some Special Saving Scheme

1. Mudaraba Hajj Saving Scheme

2. Mudaraba Education Scheme

3. Mudaraba Millionaire Scheme

People of Bangladesh are the followers of Islam. They are mostly interested to make interest

free deposits. Taking these facts into consideration SIBL a joint venture Islami bank

introduced a monthly installment based “Mudaraba Millionaire Scheme”

PRESIDENCYUNIVERSITY 13

2013

Mudaraba Monthly Profit Deposit Scheme

The features of this scheme are as follows:

1. Tk. 1,00,000, 1,10,000, 1,20,000 or 1,25,000 or any amount multiple can be deposited

under this scheme.

2. The duration of the amount should be for Five years.

3. Profits shall be distributed under this scheme as follows:

1,00,000 Tk. 900 (Provisional)

1,10,000 Tk. 1000 (Provisional)

1,20,000 Tk. 1100 (Provisional )

1,25,000 Tk. 1150 (Provisional)

4. The payable profit will become due after 1 month of deposit. But the amount will be

deposited to account in the last week of the month.

5. Generally, a depositor cannot withdraw the amount before 5 years. But in unavoidable

circumstance the depositor can withdraw the amount and in that case the depositor

will have to submit the duly filled application form of the scheme.

Mudaraba Term Deposit

The term and condition Mudarabah is same as general Mudarabah excepting one that under

this arrangement the owner of the fund agrees keep the deposit remain with the Islami bank

for a particular time period (3 months/6 months/one year/two year/three year).

Al-Wadiah Current Deposit (Code No: 133)

I. AL WADIAH Current Deposit A/c’s are opened proper introduction with minimum

initial deposit fixed by the Bank.

II. AL WADIAH Deposit is accepted on AL WADIAH principles which mean al Amanat

with permission to use. According to this principle Bank can use the fund of the account

along with other funds as per Shariah at bank’s own risk. Account holders will not share any

profit/loss.

PRESIDENCYUNIVERSITY 14

2013

III. The Law and regulation of Bangladesh, usual customs and procedures common to

banks in Bangladesh including Islamic Banking Principles shall apply to and govern the

conduct of account opened with the Bank.

Cash Waqf Certificate

i. In this case the waqf concept of Islam has been borrowed by the Islami bank for deposit

mobilization purpose.

ii. The nature of account is donation type.

iii. The accountholder operate the account for benevolent purposes.

iv. He can withdraw any amount from the account for personal use or consumption.

v. Highest weightage is given to this account in distributing profit.

3.3 Bills and Clearing Section

SIBL Local Office branch performs the bill clearing function through Local office. SIBL

Local office acts as the agent of all SIBL branches for the clearing house of the Bangladesh

Bank. There are two types of cheque which are-

1. Inward clearing cheque

2. Outward clearing cheque

A. Inward Cheque

Inward cheques are those ones drawn the respective branch which have been presented on

other banks and will be cleared/honored through the clearing house of Bangladesh Bank. For

example the cheque drawn on SIBL Local Office Branch then the cheque is called inward

cheque of SIBL Local Office Branch.

Account treatment:

Dr. Cr.

SL NO. Particular Amount SL. NO. Particular Amount

01 Customer’s A/C *** 01 SIBL General A/C ***

PRESIDENCYUNIVERSITY 15

2013

B. Outward Cheques:

Outward cheques are those ones drawn on other bank branches which are presented on the

concerned branch for collection through clearing house of Bangladesh Bank. These cheques

are called outward cheques.

C. Outward bills for Collection (OBC):

By OBC, we mean that those cheques drawn on other which are not within the same clearing

house. Officer gives OBC seal on this type of cheques and later sends a letter to the manager

of the branch of the some bank located in the branch on which cheque has been drawn. After

collection of that bill branch advices the concerned branch in which cheques has been

presented to credit the customer account through Inter Branch Credit Advice (IBCA).

In absence of the branch of the same bank, officer sends letter to manager of the bank on

which the cheques is drawn. That bank will send pay order in the name of the branch. This is

the procedure of OBC mechanism.

D. Clearing:

The scheduled banks clear the cheques drawn upon one another through the clearing house.

SIBL is a scheduled Bank. According to the Article 37 (2) of Bangladesh Bank Order, 1972,

the banks which are the member of the clearinghouse are called as Scheduled Banks. This is

an arrangement by the central bank where everyday the representative of the member banks

gathers to clear the cheques. The place where the banks meet and settle their dues is called

the clearinghouse. The clearinghouse sits for two times a working day.

The SIBL Local office Br. sends the instruments through Inter Branch Debit Advice

(I.B.D.A). SIBL Local Office acts as an agent in this case. For this, Local Office branch gives

the following entries,

Account treatment:

Dr. Cr.

PRESIDENCYUNIVERSITY 16

2013

SL NO. Particular Amount SL. NO. Particular Amount

01 SIBL General A/C *** 01 Customer’s A/C ***

If the instrument is dishonored, the instrument is returned to the Local Office branch through

I.B.D.A. along with the following entries,

Account treatment:

Dr. Cr.

SL NO. Particular Amount SL. NO. Particular Amount

01 Customer’s A/C *** 01 SIBL General A/C ***

E. Receiving Cheques for Collection:

In SIBL, cheques of its customers are received for collection from other banks. In case of

receiving cheques, following points should be checked very carefully.

1. The cheques should not carry a date older than the receiving date for more than 6

months. In that case it will be a ‘stale cheque’ and it will not be allowed for

collection. Again the date of the cheque should not be more than 1 day’s forward than

the receiving date.

2. The amount in figures and words in both sides of the pay-in-slip should be same and it

should also be same with the amount mentioned in figures and words in the cheque.

3. The name mentioned in the cheque should be some in both sildes of the pay-in-slip

and it should be the same with the name mentioned in the cheque.

4. The cheque must be crossed.

F. Cheque and Crossing

A “Cheque” is a bill of exchange drawn on a specified banker and not expressed to be

payable other wise than on demand. (According to section-6, Negotiable Instrument Act,

1881).

A cheque may be classified into:

PRESIDENCYUNIVERSITY 17

2013

I. An open cheque which can be presented for payment by the holder at the counter of

the drawer’s bank.

II. A crossed cheque which can not be paid only through a collection banker.

Crossing cheque: A cheque is said to be crossed when two transverse parallel lines with or

without any words are drawn across the face.

Crossing may be general, special or restrictive.

Cash Section

The cash section of any branch plays very significant role in general banking department.

Because, it deals with most liquid assets the SIBL Local Office Branch has an equipped cash

section. This section receives cash from depositors and pay cash against cheque, draft, PO

and pay in slip over the counter.

1. Receiving Cash:

Any people who want to deposit money will fill up the deposit slip and give the form along

with the money to the cash officer over the counter. The cash officer counts the cash and

compares with the figure writer in the deposit slip. Then he put his signature on the slip along

with the ‘cash received’ seal and records in the cash receive register book against A/C

number.

At the end of the procedure, the cash officer passes the deposit slip to the counter section for

posting purpose and delivers the duplicate slip to the clients.

1. Account treatment:

Dr. Cr.

SL NO. Particular Amount SL. NO. Particular Amount

01 Cash A/C *** 01 Customer’s A/C ***

PRESIDENCYUNIVERSITY 18

2013

2. Disbursing Cash

The drawn who wants’ to receive money against cheque to the payment counter and presents

his cheque to the officer. He verifies the following information:-

I. Date of the cheque

II. Signature of the A/C hold

III. Material alteration

IV. Whether the cheque is crossed or not

V. Whether the cheque is endorsed or not

VI. Whether the amount in figure and in word correspondent or not

Then he checks the cheque from computer for further verification. Here the following

information is checked:

I. Whether there is sufficient balance or not

II. Whether there is stop payment instruction or not

III. Whether there is any legal obstruction (Garnishee Order) or not

After checking everything, if all are in order the cash officer gives amount to the hold and

records in the paid register.

Account treatment:

Dr. Cr.

SL NO. Particular Amount SL. NO. Particular Amount

01 Customer’s A/C *** 01 Cash A/C ***

The cash section of SIBL deals with all types of negotiable instruments, cash and other

instruments and treated as a sensitive section of the bank. It includes the vault which is used

as the store of cash instruments the vault is insured up to TK. 60 laces. If the cash stock goes

PRESIDENCYUNIVERSITY 19

2013

beyond this limit, the excess cash is then transferred to Head Office. When the excess cash is

transferred to SIBL Head Office the cash officer issues IBDA.

Account treatment:

Dr. Cr.

SL NO. Particular Amount SL. NO. Particular Amount

01 SIBL General A/C *** 01 Cash A/C ***

When cash is brought from SIBL Head Office then,

Account treatment:

Dr. Cr.

SL NO. Particular Amount SL. NO. Particular Amount

01 Cash A/C *** 01 SIBL General A/C ***

3.4 Remittance of Funds

Remittance of funds is ancillary services of SIBL. It aids to remit fund from one place to

another place on behalf of its customers as well as non-customers of bank .SIBL has its

branches in the major cities of the country and therefore, it serves as one of the best mediums

for remittance of funds from one place to another.

The main instruments used by SIBL, Local Office Branch for remittance of funds.

I. Pay Order/ Banker’s check.

II. Demand Draft.

III. Telegraphic Transfer.

PRESIDENCYUNIVERSITY 20

2013

Pay Order/ Banker’s check

The pay order is an instrument issued by bank, instructing itself a certain amount of money

mentioned in the instrument taking amount of money and commission when it is presented in

bank. Only the branch of the bank that has issued it will make the payment of pay order. The

banker’s cheque must come the branch for payment wherever it is presented.

Issuing of Pay Order:

The procedures for issuing a Pay Order are as follows:

1. Deposit money by the customer along with application form.

2. Give necessary entry in the bills payable (Pay Order) register where payee’s name,

date, Po no, etc is mentioned.

3. Prepared the instrument.

4. After scrutinizing and approval of the instrument by the authority, it is delivered to

customer. Signature of customer is taken on the counterpart.

Cancellation of a Pay Order:

If a buyer wants to cancel it, he should submit a letter of instrument in this regard and also

return the instrument.

Bank Draft:

The person intending to remit the money through a pay order has to deposit the money to be

remitted with the commission which the banker charges for its services. The amount of

commission depends on the amount to be remitted. On issue of the pay order, the remitter

does not remain a party to the instrument 1) Drawer branch 2) Drawer branch 3) Payee. This

is treated as the current liability of the bank as the banker on the presentation of the

instrument should pay the money. The banker event on receiving instructions from the

remitter cannot stop the payment of the instrument. Stop payment can be done in the

following cases:

PRESIDENCYUNIVERSITY 21

2013

a) Loss of draft before endorsement in this case, “Draft reported to be lost payee’s

endorsement requires verification” is marked.

b) Loss of draft after endorsement: In this case, the branch first satisfies itself about the

claimant and the endorsement in his favor.

Charges:

A commission of 0.15% is taken on the draft value & Tk.50 is taken as postal charge.

3.5 Closing of an Account

For two reasons, one can be closed. One is by banker and other is by the customer.

1. By banker: If any customer doesn’t maintain any transaction within six years and the

A/C balance becomes lower than the minimum balance, banker has the right to close

an a/C.

2. By customer: If the customer wants to close his A/C, he writes an application to the

manager urging him to close his close his A/C.

Different procedures are followed in cash of different types of A/C to close. Fixed deposit

A/C is closed after the termination of the period.

Closing process for current & saving A/C:

1. After receiving customer’s application the officer verifies the balance of the A/C.

2. He then calculates interest and other charges accumulated on the A/C.

3. If it bears a credit balance, the officer writes advice voucher. He gives necessary

accounting entries post to accounts section.

4. The balance is returned to the customer. And lastly the A/C is closed.

But in practice, normally the customers don’t close A/C willingly. At times, customers don’t

maintain any transaction for long time. Is this situation at first, the A/C becomes dormant and

ultimately it is closed by the bank.

PRESIDENCYUNIVERSITY 22

2013

4.1 Organ gram of SIBL

Managing Director

Additional Managing Director

Deputy Managing Director

Senior Executive Vice President

Executive Vice President

Senior Vice President

Vice President

Senior Assistant Vice President

Assistant Vice President

First Assistant Vice President

Senior Executive Officer

Executive Officer

Probationary Officer

Senior Officer

Officer

Junior officer

Assistant officer

Attendant officer

PRESIDENCYUNIVERSITY 23

2013

4.2 SIBL SWOT Analysis:

Strength:

Strength means the positive internal factor that a company can use to accomplish it

mission, goals, & objectives. They might include:

Good banker-customer relationship.

Online banking system.

Islami Shariah based banking system.

Energetic as well as smart work force.

Competitive profit provider comparing with other Islamic bank.

Strong financial position.

Efficient administration

Customer satisfaction

Service quality

Weakness:

Weakness means the negative internal factors that inhibit or restrict the

accomplishment of company’s mission goal & objectives. They might include:

Market share

Shortage of skill work force.

SIBL has lack of ATM booth.

Opportunity:

Opportunities are the external option that a firm can exploit to accomplish its mission. They might include:

Huge business area.

Introducing consumer credit scheme.

Growth of sales volume.

Introducing branch banking through online.

Develop relations and correspondence with foreign banks.

More concentrated Banking based on Islamic Shariah.

PRESIDENCYUNIVERSITY 24

2013

Threat:

Threats are negative external forces that restrict a company’s ability to achieve its

mission, goal, & objectives. Threat to the business can take variety type of forms

such as:

Entrance of new private commercial banks.

Bangladesh Bank has no well established Islami Banking Rules.

Govt. imposes high rate of taxes and VAT.

Political unrest and economic recession.

Technological advantages

PRESIDENCYUNIVERSITY 25

2013

5.0 The Financial Performance of the Bank :

The performances of the total Banking sector of the year 2011 could be evaluated in

the backdrop of ups and downs of the domestic and global economic trend. Volatile

money market paused as the big challenge for Bangladesh economy. The economy of

Bangladesh seemed a bit stable with persistent price hike of number of essential

commodities causing high inflation rate. The performance of SOCIAL ISLAMI

BANK LTD. for the year 2011was specially featured by lowering the classified

investment of 3.93% , increase of deposit by Tk. 2200.14 core . The management of

the bank was more conscious in proper assets liability management. Moreover, we

were able to find some well known corporate business houses and individual of the

country as our business partner. As a result, investment growth of the 2011 was

46.97%, much higher than the investment growth of 2010. As I will note from the

director’s Report, the Bank successfully completed the year of 2011 and tremendously

strengthened the financial indicator of the bank despite global financial crises. The

year 2011 was very eventful for us with opening of new 12 branches . In shah Allah ,

they will be ultimately able to reach at the desired level so that shareholder

expectation could be optimized.

PRESIDENCYUNIVERSITY 26

2013

PRESIDENCYUNIVERSITY 27

2013

5.2 SIBL Business Success 2011 :

SIBL maintained and achieved strong position in all key areas of operation despite

challenges in 2011. Capital of the Bank was Tk. 12.60 core at the very inception, and

by the year 2011 it has increased to Tk. 953.45 core.

Total deposits of the bank stood at Tk. 6685.25 core and total assets stood at tk.

8440.62 core as an 31 December, 2011 which indicate a growth of 49.05% and

53.00% respectively over that of the previous year.

The Bank achieved 46.97% growth in investment with a total investment portfolio of

tk. 5390.86 core in 2011 compared to tk. 3668.03 core in 2010.

Import business of the Bank stood at Tk 6819.85 core in 2011 with 72.83% growth

over that of the previous year . Total foreign remittance stood at tk. 513.49 core in

2011 with 367% growth over that of the previous year.

Total foreign Exchange business of the bank was tk. 10830.84 core in 2011 with

74.89% growth over that of the previous year.

The Classified investment was 3.93% of total investment. The Bank registered an

opening profit of tk 276.88 in the year 2011 with remarkable growth of 68.97%

compared to tk. 163.86 core in 2010.

PRESIDENCYUNIVERSITY 28

2013

5.3 Investment Income:

The bank has registered an income from investment of Taka 6922.20 million under

different modes of investment accounts in the year under review compared to Taka

3886.18 million of 2010 which is an increase of 78.12 from the previous year. A

comparative position on income received from different modes of investment in the

year 2011 and 2010 is given below:

PRESIDENCYUNIVERSITY 29

2013

5.4 Income from investment in share & securities:

Throughout the year , the country observed the capital market as unsupported , faded

and less confident to the investors irrespective of corporate and individual. SIBL had

an investment outstanding of taka 5241.36 million in Quoted and unquoted shares,

preference share, bond & Govt. security against taka 3049.72 million of 2010. Year

earning from this segment has been recorded at taka 171.11 million against taka

341.63 million of 2010. Despite massive fall of capital market, the bank saved its

portfolios successfully, however, an amount of taka 577.10 million has been provided

due to fall of market value on the closing date of 2011.

5.5 Capital Management :

The bank started journey in the year 1995 with a paid up capital of taka 118.36 million

and thereafter within 16 years it has built a total capital of taka 9534.52 million using

the external and internal sources. The table given below is the last 5 years history of

SIBL’s Capital journey efforts:

to comply with the international and to make the banks capital more stock absorbent ,

SIBL is compliant of risk based capital adequacy framework . The bank uses

standardized approach for assessing evaluation and calculating risk weighted assets

w.e.f. 2010. SIBL is always concerned about its capital and its due maintained and

accordingly, while forecasting the business growth and regularity capital requirement,

internal and external source of capital are considered in detail after capital impact

PRESIDENCYUNIVERSITY 30

2013

study. with success of the year 2009 and 2010and projected business growth in the

year 2011and ahead, the bank issued 1:1 Right shares among its share holders which

infected a fresh capital of taka 2987.81 million during the year under report. The final

impact on capital at the year end 2011 stood at : a) paid up capital 6393.93 million

against taka 2987.81 million of 2010 and (b) total capital (as per BASEL-ii) taka

9534.52 million against taka 4678.56 million of 2010.

PRESIDENCYUNIVERSITY 31

2013

5.6 Foreign Exchange Business :

Foreign Exchange Business stood at tk. 108308.30 million in 2011 against Tk.

61931.00 million in 2010 which is a sharp increases of 74.59% . the break-up of this

foreign exchange business is as under :

International Trade Financing (Export & Import):

One of the core activities of the bank is to facility international trade through export

and import financing. Over the last few years the foreign trade financing of the bank

has gained a stable expansion . The bank has been achieving significant growth in

both export and import financing despite global financial turmoil and worldwide

economic slowdown. During the year of 2011, the foreign trade businesses of the bank

has recorded a significant growth of 72%. Imported business increased by 73% of

which real value was taka 68198.50 million in 2011 against taka 39459.50 million in

2010. on the other hand , export business grew to taka 34975.00 million in 2011 which

is 64 percent higher than the export of taka 21372.20 million in 2010. The bank has 14

Authorized Dealer branches well equipped with highly trained professional to meet

different requirement of import and export based client :

The bank was involved in financing import business in the field capital machiery,

industrial raw materials , food grains ( Rice , wheat, sugar, pulses, garlic, onion,

spices), oil (soyaben, palm, lubricant ), motor vehicles , spare parts, garment

accessories, sports items, perfumery items, chemical, milk food etc.

PRESIDENCYUNIVERSITY 32

2013

in order to facilitate trade finance , establishing of “ Centralized Trade Processing Unit

was a timely decisions and has changed the total process of foreign exchange business

through speeding up the service and business potential of SIBL. we have centralized

Trade processing facilities based in Dhaka and Chittgong .

Financial Highlights Fig in million Taka

Year Deposits Investment FX_BusinessTotal Income

Total Expenses

Operating Profit

Profit after Tax

1995 124.73 0.21 0 1.73 6.15 (4.42) (4.42)

1996 417.81 211.50 342.95 19.3 38.23 (18.93) (18.93)

1997 645.51 368.31 699.48 51.37 56.84 (5.46) (5.47)

1998 2068.85 1171.40 1442.25 173.97 134.73 50.50 35.07

1999 3899.72 2192.03 1914.10 440.63 378.98 74.02 36.99

2000 4863.21 3522.25 3547.40 641.38 405.39 105.71 38.16

2001 10569.67 5499.25 6195.30 1214.25 613.29 302.00 144.39

2002 15141.34 7504.03 13520.07 1775.43 953.12 420.02 203.52

2003 19709.31 10059.11 19065.10 2385.84 1470.67 500.54 193.67

2004 19704.20 12887.30 18088.12 2458.25 1620.89 414.99 83.85

2005 16862.58 15096.83 17438.07 2199.65 1708.69 213.57 13.94

2006 16170.51 15312.90 23280.00 2530.90 1932.95 295.89 57.63

2007 19753.94 16440.26 23903.80 2995.45 2126.77 480.78 150.04

2008 24099.82 19951.30 33363.20 3363.08 2575.72 787.37 202.07

2009 31588.16 26580.58 39110.00 3781.26 2716.96 1064.31 431.52

2010 44850.77 36680.28 61931.00 5068.10 3429.47 1638.63 643.01

2011 66853.59 53908.57 105037.00 8512.22 5914.78 2597.43 1265.11

PRESIDENCYUNIVERSITY 33

2013

Credit Rating :

Year Long Term

Short Term

Outlook Rated by

2009 A+ ST-2 StableCRISL (Credit Rating Information Services Ltd.)

2010 A+ ST-2 StableCRISL (Credit Rating Information Services Ltd.)

2011 A+ ST-2 PositiveCRISL (Credit Rating Information Services Ltd.)

Profit Rates :

Sl No Name of Scheme Deposits Profit Rate (%)

Group A: Mudaraba Monthly Profit Scheme

01. Shachanda Protidin 13.50%

02. Shuborno Lata 13.50%

03. Shobuj Chaya 13.50%

Group B: Mudaraba Deposit Pension Scheme

01. Sonali Din 13.50%

02. Shukher Thikana 13.50%

03. Suborno Rekha 13.50%

04. Shobuj Shayanho 13.50%

Group C: Mudaraba Double Benefit Scheme (Shall be Double by 5 years 6 months)

01. Shamridhir Shopan 13.43%

Group D: Mudaraba Hajj Scheme

01. Kafela 13.50%

Group E: Mudaraba Cash Waqf Accounts

01. Cash Waqf Deposit Scheme 14.00%

PRESIDENCYUNIVERSITY 34

2013

5.7 SIBL 2012- A GOLDEN YEAR :

The year 2012 was envisaged as a golden year for SIBL. Adopting new strategic

business policy, SIBL will leave no stone unturned to boost business in all areas of

operation to achieve its corporate goals.

The Bank’s continuous effort has been to increase the shareholder’s value and be

valued as a compliant organization . SIBL emphasis on employment generation and

environment friendly and green banking for equitable distribution of resource over

geographical territory for sustainable growth of macro economy of the country. the

pro-active management team of SIBL with there talent and skill has been working to

continuously at success in the performance of the bank.

PRESIDENCYUNIVERSITY 35

2013

6.0 Analysis of the Findings :

Nature of customers:

Figure 1: Accounts preference of the SIBL customers

Interpretation: 23% customers have Mudaraba Savings Deposit, 47% customers have Al-

Wadia Current Deposit, 13% customers have Mudaraba Notice Deposit, and 7% customers

have Mudaraba Term Deposit and 10% customers have others. Here I have seen that most of

the customers prefer savings and current deposits than other accounts.

2. Customer Opinion about brand name “Social Islami Bank Limited”:

Figure 2: Customer opinion about Brand name

3. Reason for opening an account:

PRESIDENCYUNIVERSITY

47%

23%

13%

7%

10%

Al-Wadia current Deposit Mudaraba saving Deposit Mudaraba notice Deposit Mudaraba Term Deposit Others

30%

57%

13%

Fully Satisfaction Moderate Dissatisfaction

40%

10%7%

23%

7%

13%Superior ServiceAttractive ServiceType of account offer ConvenientReputation Others

36

2013

Figure 3: Reason for choice the SIIBL

Interpretation: around 7% with (2) respondents said that they have chosen the bank because

it is has a good reputation in the community such as “Shariah-based Islami Bank”. 40% (12)

respondents have said that it is a reliable bank and provide better service and 23% said they

prefer for convenient place. 13% and 1 0% respondents choose the bank because of attractive

rate and types of accounts offered respectively.

4. Respondent opinion about fees and service charges:

Figure 4: Customer opinion about fees and service charges.

Interpretation: Product and service charge is a sensitive issue in banking sector. 60%

respondents said this bank charge moderate value toward the customers. Moreover 33%

respondents were against the arguments because they felt that bank charge little bit higher.

Majority was medium value which they are able to pay to get the product or service and rest

of 7% respondents experienced that SIBL demand lower charges.

PRESIDENCYUNIVERSITY

60%

33%

7%

High ModerateLow

37

2013

5. Employee opinion about research and development:

Figure 5: Employee opinion about research and development

Interpretation: 50% of respondents of this branch said SIBL do not introduce new product for the actual and potential customers because they don’t have R&D department and about 17% respondents found some scheme of loan product against the assets.33% respondents have no reaction about the arguments.

6. Customer Opinion about their SLBL promotional Activity:

Figure 6: Customer Opinion about their SLBL promotional activity

Interpretation: 36% respondents expressed fully dissatisfaction about the promotional

program of SIBL. Opinion came from 33% respondents who are satisfied their current

advertisement activity and 17% respondent who are fully satisfied too. 7% respondents were

PRESIDENCYUNIVERSITY

Very good10%

Good7%

Average 33%

Poor50%

Very goodGoodAverage Poor

Fully Satisfied15%

satisfied30%

Neutral6%

Fuly dissatisfied34%

Dissatisfied 15%

Fully SatisfiedsatisfiedNeutralFuly dissatisfiedDissatisfied

38

2013

neutral about the question. 7% respondent expressed dissatisfaction about promotional

activity.

7. Customer opinion about their attention:

Figure 7: Customer opinion about their attention

Interpretation: Despite of their fewer advertisements, they have reached to its target customers quite successfully. By the analysis almost 66% (20) respondents knew about the bank through its current client. And rest 34% respondents have seen the different media advertisements and billboards.

8. Customer opinion about SIBL place:

Figure 8: Customer opinion about SIBL place

Interpretation: 36% respondents said SIBL have good with the locations. May be this is because it is a foreign exchange and Investment based site as well as a Shariah-based bank. That’s the reason people are happy with having transaction over here. They are having class services and up to date facilities, good communication facilities. On the other hand, 54% respondents said against with this issue and 10% respondents said no comments.

6.1 Customer Satisfaction

Customer satisfaction is the extent to which a product or service’s perceived performance

matches a buyer’s expectations. If the product or service’s performance falls short of

PRESIDENCYUNIVERSITY 39

2013

expectations, the buyer is dissatisfied. If performance matches or exceeds expectations, the

buyer is satisfied or delighted.

Expectations are based on customers past buying experiences, the opinion of friends and

associates, and marketer and competitor information and promises. Marketer must be careful

to set the right level of expectations. If they set expectations too low, they may satisfy those

who buy but fail to attract enough buyers. In contrast, if they raise expectations too high

buyers are likely to be disappointed. Dissatisfaction can arise either from a decrease in

product and service quality or from an increase in customer expectations. In either case, it

presents an opportunity for companies that can deliver superior customer value and

satisfaction.

Today’s most successful companies are rising expectations—and delivering quality product.

Such companies track their customers’ expectations, perceived company performance, and

customer satisfaction. Highly satisfied customers produce several benefits for the company.

Satisfied customers are fewer prices sensitive, remain customers for a longer period, and talk

favorably to others about the company and its products & services.

6.2 Findings on general banking activities:

Social Islami Bank is entirely a new banking system which is adopting for a better change in social economics condition and to make the banking function dynamic.

By the construction of capital production employment opportunities Investment and strong economical structure this branch I performing major role to meet up the demand of sociality.

1. The Clients of SIBL prefer to maintain Savings Account.

2. Social Islami Bank Limited has very good traditional documentation process for general

banking.

3. Customers like the brand name of Social Islami Bank Ltd. And fully satisfied with this.

4. Customers like for the superior service.

5. Customers like for the moderate service charge.

6.3 Major Findings on the research in client satisfaction:

PRESIDENCYUNIVERSITY 40

2013

1. Social Islami Bank Ltd. has very good traditional documentation process. Although they

are not following any high technology or so but they having a very good record of the

documents and filing system also the serial is been properly maintained too.

2. Majority of customers are an account holder of this bank because they have the opportunity

to choose various types of Shariah based Accounts. In this branch customers prefer savings

and current deposits and other accounts.

3. Customers like the brand name of Social Islami Bank Ltd. and fully satisfied with this.

4. This bank charges moderate value toward the customers. Majority are found to be medium

value which they are able to pay to get the product or service. Moreover credit card charge

also reasonable and has some clear conditions.

5. People are satisfied about the location of this branch and this place is suitable for financial

transaction.

6. Social Islami Bank Ltd. is not creative on their exterior design. Majority of respondent said

that bank is not good in terms of it’s the exterior decoration.

7. The bank is good in terms of its interior design. But there is no enough space inside the

bank to move freely. GB (general banking) has such small space that it is not enough for

attracting the customers.

8. SIBL customers could known about the bank through its current clients because lack of

advertisement they could not get enough information about the bank. Social Islami Bank Ltd.

invests little bit for promotional program.

9. Social Islami Bank Ltd. is operating the business in a very expert style with energetic and

well behave employees. They are very respectful to the Bangladesh Bank’s policies and very

much serious to fulfill customer satisfaction. Again, they are very cooperative to their

customers as well. They always try to help the customers at their best.

10. Social Islami Bank Ltd. is a reliable bank and provides better service to its customers.The

main objectives of the world famous and successful banking organizations are making of

profit through addressing the clients time to time with new paces of service instruments.

PRESIDENCYUNIVERSITY 41

2013

However my little experience carnal the through this internship. I had several thank

discussions with the clients and officials, which has helped me to know about the findings

and draw and the followings recommendations:

To make the Shariah inspection strengthens regarding all Investment of the bank. Official at

branch level should inspection strengthen regarding all Investment of the bank.

This branch provides advances towards the true entrepreneur with reconsidering

conventional system of security and collateral, moreover, the whole process should be

completed within an acceptable time.

Always should monitor the performance of its competitors.

Evaluate customers need from their perspective and explain logically the shortcomings.

Use of effective management information systems.

Investment decision make faster.

The management should consider revise the remuneration package in order to attract

quality human resource.

SIBL is running successfully and for its good deposit performance the bank occupies 2nd

position in the Investment Banking Sector. Taken all in all, it can be safely said that SIBL

action program is directed towards development of an authentic participatory economy

beyond market economy. The family empowerment credit program of Social Islami Bank is

gaining ground at the grass root field level in Bangladesh. Family empowerment micro credit

and micro enterprises program must be designed in a manner so as to make a) finance b)

production c) marketing d) trading e) local specific survey and research as well as moral

integrity in one package.

In SIBL approach, credit conveys the totality in life and clearly linked to social context and

cultural setting in conformity with Shariah. There is a better chance in provision for social

subsidy. De-secularizing credit may lead to rewriting new economics.

PRESIDENCYUNIVERSITY 42

2013

7.0 Recommendation:

Through my work experience at the Bashundhara Branch, Social Islami Bank Ltd., I

came across a few operational drawbacks – for which the following suggestions can be

put forward.

The internal decoration of the branch has scope for much improvement.

More employees should be appointed to manage the increasing customer pressure.

Leaflets containing SIBL’s product description should be made available at the

branches. This will help the prospective customers to be informed about existing and

new products, and reduce the hassle of counter staffs to describe new products. This

will eventually result in increased employee productivity.

Ensure high level customer service.

Bank should increase ATM Booth .

Bank should introduce consumer credit scheme.

More meetings, seminars, symposiums and get-together should be organized by the

Branches to develop the awareness among the clients of the Bank about Islamic

Banking and its advantages.

The employee of the branch should be trained continuously.

Furthermore, the customers also provided their own suggestions:

Provision of car loans.

Individual counters to provide one-stop service for cheque payments.

More social involvement by SIBL such as providing student scholarship, creating

more employment opportunities, rehabilitating the poor.

If the stated recommendations are carried out and the government pays attention to

the policy framework of the entire system, then that day would not be far when

Bangladesh can proudly focus more on the Islamic banking system than the

conventional banking.

PRESIDENCYUNIVERSITY 43

2013

7.1 Learning point:

In the Bashundhara Branch, Social Islami Bank Ltd. I have many things and got practical

experience about general banking and investment sector. Here I learned how to issue a

cheque to an account holder. Thus, I learn how to open current account and saving account,

required documents and papers for different types of account. I did work with clearing

department where I have learned how to clear the cheques through clearing house of

Bangladesh Bank, OBC etc.

At the end, I would like to say that in my internship period; I have learned official manners,

corporate environment and behavior, customer service, how to deal with customer and earned

satisfaction.

I think this is my main learning point to get a job in good organization and apply the

experience for better outcome.

PRESIDENCYUNIVERSITY 44

2013

7.2 Concluding Remark :

Islamic banking is now a reality in Bangladesh. It is functioning efficiently, smoothly and

satisfactorily despite facing various internal and external threats. The economics of the

country may be geared towards Islamic Principles and Teachings in order to realize the full

potential of Islamic banks in the long run. However, in the short run, the Islamic banks can

take a number of concrete steps to facilitate the Islamic banking in Bangladesh. This report

will give a clear idea about the activities, General banking, financial performance of SIBL.

Social Islami Bank ltd. is a non government commercial Bank in Bangladesh, which started

its business from 1995.It is a unique combination of Shariah & Islamic banking. Among non

government commercial banks, Social Islami Bank Ltd. is a milestone for economic

development. It has been playing an important role to eradicate the unemployment problem in

Bangladesh. But most of the people in our country have misconception about Islamic banking

specially Social Islami Bank Ltd. & other Islamic banks. They can not find any difference in

its operation between conventional commercial Banks and Islamic Banks because they have

no clear idea about the activities as well as investment mechanism of Islamic banks.

The Bank is committed to run its activities as per Islamic Shariah and thus it has different

investment(credit) modes, different repayment schedules, different disbursement procedure,

different mark up system. and also has a different Credit(Investment) policy. ‘Mark up’

means adding some additional value after purchasing the goods but before to sell the same to

another people. This system is accepted in Islamic Shariah because here money is converted

to goods.’ Money begets money’ is prohibited in Islamic Shariah. People is getting more

benefit from the dealings of Islamic banking because here quarterly interest is not charged

and there is no possibility of interest to be converted into principal. But it needs to mention

here that Islamic Banks like Social incurred huge loss in case of default cases. Islamic Banks

can’t charge extra amount on the residual principal of the overdue accounts like other

conventional banks but some compensation is imposed on the accounts to protect huge

accounts to be overdue/classified. It cannot take part in call money market. Mudaraba,

Musharaka are another mode of investment in Islamic Banking. But here honesty is the only

pre-requisite. For ensuring more benefit, more facility from Islamic banks like Social we

have to be honest and more sincere to repay the taken money from these banks in time.

PRESIDENCYUNIVERSITY 45

2013

7.3 Reference:

Statement of Affairs, Basundhara Branch, Social Islami Bank Ltd., as on 31/12/2012.

http://www.siblbd.com

http://www.siblbd.com/home/annual_reports

Annual Report of Social Islami Bank Ltd., Year 2010.

Annual Report of Social Islami Bank Ltd., Year 2011.

http://www.assignmentpoint.com/business/finance/a-report-on-social-islami-bank-

limited-part-1.html

http://www.siblbd.com/home/profile/product& service

PRESIDENCYUNIVERSITY 46

![Syllabus for ITE 478 – INTERNSHIP [part time ...Syllabus for ITE 478 – INTERNSHIP [part time] International Business - 5 Credits Syllabus for ITE 478 – INTERNSHIP [part time]](https://img.dokumen.tips/doc/110x75/5e60d0964a30a028c1420357/syllabus-for-ite-478-a-internship-part-time-syllabus-for-ite-478-a-internship.jpg)