Embed Size (px)

Citation preview

1st QUARTER 2016 2nd QUARTER 2016 3rd QUARTER 2016 4th QUARTER 2016

The Egyptian-British Chamber of Commerce

International Trade Report Q3 2016

Prepared by the Egyptian-British Chamber of Commerce

Nov 2016

Britain has a long history of strong shared interests with Egypt; the UK is the largest foreign investor in Egypt and total

trade volume between the two countries was over £1.5 billion in 2015.

Egypt’s preferential trade agreements, a highly competitive and skilled labour force, a young population (50% is under

the age of 35), low utility costs, proximity to key global markets, and a large domestic consumer market (90 million) make

it an ideal country to trade with.

The EBCC’s Quarterly Trade Report gives you our trade and economic outlook for the UK & Egypt, as well as statistical

information on trade in goods between Egypt and the UK for the period Q1 to Q3 2016 (January to September 2016).

UK Trade Confidence Index

-40

-30

-20

-10

0

10

20

30

40

50

Q1 08 Q3 08 Q1 09 Q3 09 Q1 10 Q3 10 Q1 11 Q3 11 Q1 12 Q3 12 Q1 13 Q3 13 Q1 14 Q3 14 Q1 15 Q3 15 Q1 16 Q3 16

% B

ALA

NC

E

Service Sector Manufacturing Sector

-- Recession --

In the third quarter, the proportion of firms reporting improved export

performance saw a sectoral divergence. While the number of manufacturers

enjoying an improved export performance rose in the quarter, the balance of

service sector firms reporting improvements fell to the lowest level in five years.

In the manufacturing sector, the balance* of firms reporting improvements in

export sales over the previous three months rose to +17% in Q3 2016 from +9%

in Q2 2016. This means that 17% more firms reported an increase over a

decrease. The balance of manufacturers reporting improved export orders also

rose, from +5% in Q2 to +12% in Q3. However, the services sector saw a

slowdown in growth in Q3, with the balance of firms reporting improvements

falling to +8% from +11% in the previous quarter. For advance export orders, the

balance fell for firms in the services sector, to +5% from +13%.

*Balance figures are determined by subtracting the percentage of companies reporting

decreases in a factor from the percentage of companies reporting increases.

Manufacturing

Export Sales

+17%

The adjacent graph

shows the balance of

firms reporting an

increase in export sales

compared to those

reporting a decrease

going back to Q1 2008.

The balance of

manufacturers reporting

increased export sales in

Q3 2016 rose from the

lowest post-recession

level in Q4 2015.

Source: British

Chambers of Commerce

Services

Export Sales

+8%

Overview

The Global Economy

The International Monetary Fund (IMF) has downgraded its

forecast for global growth for 2016 from 3.2% to 3.1% and

for 2017 from 3.5% to 3.4%.

The US economy, the world’s largest, grew at an annual rate

of 1.4% in Q2 2016, up from the growth of 0.8% recorded in

Q1. China’s economy, the world’s second-largest, grew by

6.7% in Q3 2016 in annual terms.

The Eurozone economy grew by 0.3% in Q2 2016, lower

than the growth of 0.5% recorded in Q1. The third official

estimate of UK economic growth revealed that the UK

economy grew by 0.7% in Q2 2016, up from the previous

estimate of 0.6%. Q2 GDP growth in annual terms was

revised down from 2.2% to 2.1%. The service sector and

consumer spending remain the main drivers of UK

economic growth.

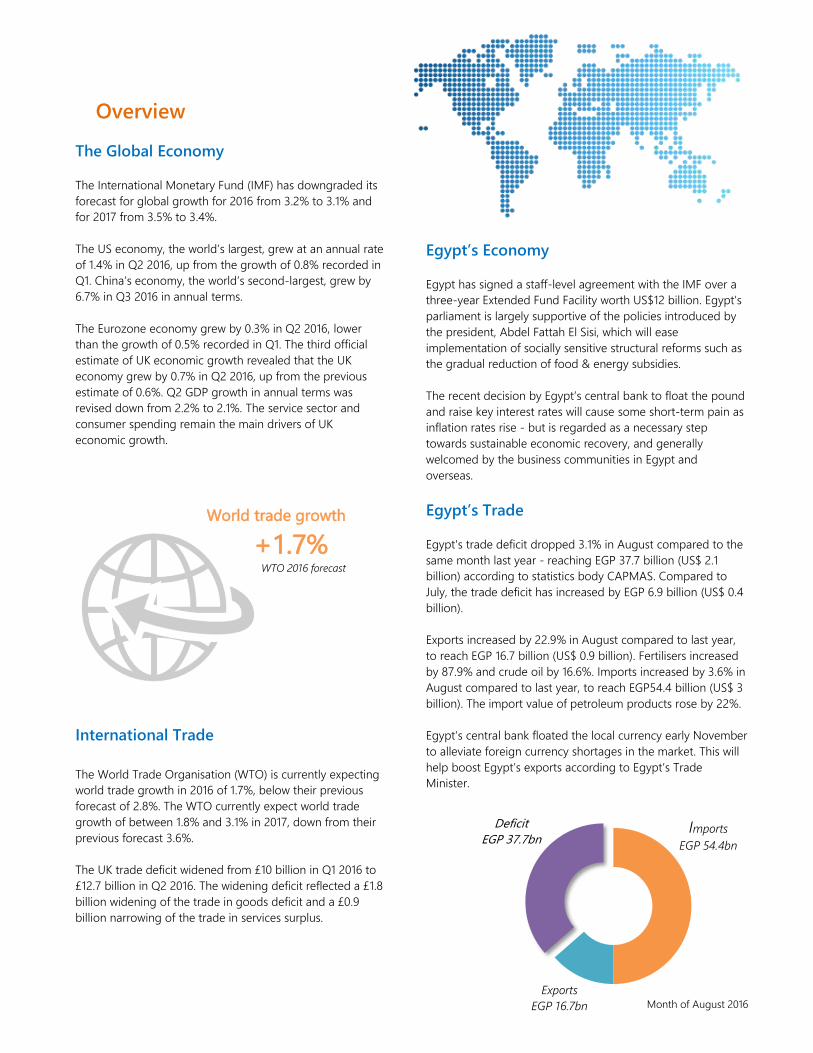

International Trade

The World Trade Organisation (WTO) is currently expecting

world trade growth in 2016 of 1.7%, below their previous

forecast of 2.8%. The WTO currently expect world trade

growth of between 1.8% and 3.1% in 2017, down from their

previous forecast 3.6%.

The UK trade deficit widened from £10 billion in Q1 2016 to

£12.7 billion in Q2 2016. The widening deficit reflected a £1.8

billion widening of the trade in goods deficit and a £0.9

billion narrowing of the trade in services surplus.

Egypt’s Economy

Egypt has signed a staff-level agreement with the IMF over a

three-year Extended Fund Facility worth US$12 billion. Egypt’s

parliament is largely supportive of the policies introduced by

the president, Abdel Fattah El Sisi, which will ease

implementation of socially sensitive structural reforms such as

the gradual reduction of food & energy subsidies.

The recent decision by Egypt’s central bank to float the pound

and raise key interest rates will cause some short-term pain as

inflation rates rise - but is regarded as a necessary step

towards sustainable economic recovery, and generally

welcomed by the business communities in Egypt and

overseas.

Egypt’s Trade

Egypt's trade deficit dropped 3.1% in August compared to the

same month last year - reaching EGP 37.7 billion (US$ 2.1

billion) according to statistics body CAPMAS. Compared to

July, the trade deficit has increased by EGP 6.9 billion (US$ 0.4

billion).

Exports increased by 22.9% in August compared to last year,

to reach EGP 16.7 billion (US$ 0.9 billion). Fertilisers increased

by 87.9% and crude oil by 16.6%. Imports increased by 3.6% in

August compared to last year, to reach EGP54.4 billion (US$ 3

billion). The import value of petroleum products rose by 22%.

Egypt’s central bank floated the local currency early November

to alleviate foreign currency shortages in the market. This will

help boost Egypt’s exports according to Egypt’s Trade

Minister.

Imports

EGP 54.4bn

Exports

EGP 16.7bn

Deficit

EGP 37.7bn

Month of August 2016

World trade growth

+1.7% WTO 2016 forecast

Export Documentation Index

Many types of exports require supporting commercial documentation. Chambers of Commerce issue certified trade

documentation required for exports outside the EU and as a result have amassed a significant dataset around UK goods

exports. The Egyptian-British Chamber of Commerce does the same but solely for UK goods exports to Egypt. The data

collected from this process shows an index of trade document certification.

World There is a decrease in the volume of UK trade documents certified on the quarter. Taking 2007 as a base year at 100, the

index for Q3 2016 stands at 121.69. This represents a decrease of 4.1% compared to Q2 2016. Year on year, trade

documentation increased by 5.3% (see table below).

Source: British Chambers of Commerce

Egypt Because of new export documentation decrees issued by the Egyptian government in December 2015 and early 2016 –

making it mandatory for overseas exporting companies to submit certain export documents when shipping goods to

Egypt – the Chamber saw a significant increase in UK export documentation in the first quarter of 2016. In Q2 2016 the

volume of UK trade documents certified for export to Egypt restored to levels last seen in 2007. In Q3, we witness a slight

slowdown in growth. This can largely be attributed to the persistent lack of foreign currency in the Egyptian market.

Taking 2007 as a base year at 100, Q3 2016 performed slightly worse at 88.95, but significantly better compared to

previous years.

Prior to 2016, the economic recession, but in particular the turmoil following Egypt’s revolution in 2011 caused a serious

drop in volume of trade documents between the UK and Egypt. With stability returning to Egypt, we saw significant

growth in 2014 that carried on into the beginning of 2015. Growth slowed in the latter half of 2015, largely as a result of a

lack of foreign currency in the Egyptian market. Please note: The newly introduced trade decrees mentioned earlier create a

discrepancy between documentation levels in 2016 compared to 2015 (see table below). A new trend will emerge as we look

at export documentation levels going forward.

Percentage Change (%)

Q3 2016

(2007 = 100)

Q3 2016

compared to Q2 2016

Q3 2016

compared to Q3 2015

Volume index of export

documentation 88.95 -16.6% +47.6%

Trade Outlook 2014 proved an exceptionally strong export documentation year with rapid recovery particularly in the last six months of

the year; in our previous reports we estimated that this upward trend would level out – and indeed drop - towards the

end of 2015, but that the strong performance during the first six months of 2015 would ensure an export documentation

outcome similar to 2014. Export documentation increased by 2% in 2015. We expect a significant increase in export

documentation in 2016 as a result of the newly introduced decrees, as mentioned above.

The HM Revenue & Customs (HMRC) trade statistics show that trade is picking up gradually in 2016; but is somewhat

volatile. UK exports to Egypt continue to out-perform Egyptian exports to the UK in terms of growth percentage. Q1 2016

saw strong figures for UK exports to Egypt, with year-on-year growth reaching close to 14% - on par with Q3 2016. Q2

Percentage Change (%)

Q3 2016

(2007 = 100)

Q3 2016

compared to Q2 2016

Q3 2016

compared to Q3 2015

Volume index of export

documentation 121.69 -4.1% +5.3%

2016 under-performed with a year-on-year drop of 0.8%. Egyptian exports to the UK are on a path to recovery.

Compared to the same period a year before, exports dropped by close to 12% in Q1 2016, and by 5.4% in Q2 2016. In the

current quarter, Egypt’s exports to the UK record a marginal drop of 2.3% year on year.

The recovery in 2014 and the beginning of 2015 can mainly be attributed to a return of political stability and increased

confidence in Egypt’s economic recovery post-Revolution. However, reform momentum faded towards the end of 2015

and continues to hinder trade growth in 2016. While some of the bans on outflow of foreign currency were lifted earlier

in 2016, foreign exchange shortages still curb production – and consequently the export of Egyptian value added goods.

Continuing delays in economic reforms as well as a lack of tourism and foreign investment dampen growth in 2016.

However, we expect trade to rebound in 2017, provided that that the Central Bank of Egypt continues to ease restrictions

on the outflow of foreign currency. In a move that was anticipated for several weeks, Egypt floated the pound earlier this

month in an attempt to stabilize its economy and bring much needed liquidity into the market. While the weakening of

the pound will inevitably cause some short-term pain, it will help the country in the long run, and is a welcome sign for

foreign investors. The central bank will eventually be able to fully dismantle foreign exchange restrictions, thereby

reducing disruptions to trade. A weaker currency will also boost Egypt’s external competitiveness and encourage foreign

investors back to the country.

These measures should help place Egypt’s external position on a more sustainable footing, particularly if backed up by

further economic reforms. A second phase of economic reforms - tackling food subsidies -is planned; the reforms look to

distribute food subsidies based on monthly income by linking the automated wage system to citizens’ national

identification numbers.

The devaluation of the pound and reduction/restructuring of subsidies were key demands by the International Monetary

Fund in order for Egypt to receive a loan of $12 billion over three years. The IMF has yet to officially ratify the loan, but it

is seen as crucial in helping to stabilize the country's economy.

Egypt’s Economy

2012/13 2013/14 2014/15 2015/16

GDP (% growth) 2.1 2.2 4 3.8

Export (US$bn) 25 24 21 20

Import (US$bn) 59 58 60 57

Inflation (%) 6.9 10.1 10.3 15.75 (Oct)

Exchange Rate (per $) 6.98 7.13 7.61 17.95 (Nov)

Population (% growth) 2 2.5 2.1 2.1

Source: Central Bank of Egypt

Economic Outlook

Sectors to Watch

Egypt’s Economic Outlook Oct. 2016 – World Bank

Egypt’s nascent recovery faded in FY16, owing to the

foreign exchange crunch, a drop in tourism, and an

unfavourable external environment. The government seeks

to implement measures that will address the ongoing

macro-imbalances (especially in the external and fiscal

accounts), introduce structural reforms to improve the

business environment, and redirect resources towards

social programs. This would be supported by a 3- year

Extended-Fund Facility (for which a Staff-Level Agreement

was reached in August and is pending IMF Board

approval). The government aims to implement reforms on

three main fronts: (1) exchange rate liberalization; (2) fiscal

consolidation, and (3) structural reforms to boost growth

and reduce unemployment. The program also aims to

strengthen the social safety nets to better protect the poor

and vulnerable groups.

Egypt’s growth was 4.3 percent in 9M FY16, in line with

the previous year, and double the rate during FY11-14,

but still below potential. Real growth in Egypt continues

to be below potential and is constrained by shortages in

hard currency, and sluggish growth in Europe (Egypt’s

main trading partner), as well as the lower international oil

prices that adversely impacted the Gulf (primary source of

remittances).

Additionally, key sectors continued to post negative growth,

particularly oil and gas extractives and tourism.

GDP is expected to grow by 3.8 percent in FY16, slightly

lower than the 4.2 percent growth achieved in FY15, before

rebounding gradually thereafter. Growth in FY16 is expected

to be entirely driven by domestic demand as consumption

remains resilient and public investments crowd-in the private

sector. Net exports, on the other hand, continue to be a drag

on growth due to the shortages in hard currency and - until

recently - an overvalued real exchange rate. Over the medium

term, growth is expected to pick up as economic reforms

progress and key sectors recover. The fiscal deficit is expected

to narrow over the medium term, assuming the government

implements the envisaged fiscal consolidation measures. On

the external front, Egypt’s accounts are likely to worsen in FY16

due to the sharp decline in tourism and lower transfers before

recovering slowly afterwards, provided that the CBE continues

to ease restrictions on foreign exchange.

In a press release issued on 4 November, the World Bank said

it welcomes Egypt’s recent economic and social reform

measures including the floatation of the currency, measures to

boost investment especially in Upper Egypt, adjusting energy

prices to reflect market conditions, and strengthening the

social safety net.

Source: World Bank

Energy & Mining Healthcare Education Retail & Trade Transportation Urban Planning

& Logistics

UK Trade Statistics: MENA & Egypt In the years prior to 2008, Egypt recorded a 7% share of MENA (Middle East & North Africa) trade with the UK on

average. As a result of the Arab Spring - and subsequent political and economic turmoil over the past four years -

Egypt’s percentage share of MENA trade with the UK dropped significantly. In the second half of 2015 the gradual

recovery witnessed in Q3 and Q4 2014 slowed. While Egyptian exports to the UK are on a path to gradual recovery in

2016, UK exports to Egypt are somewhat volatile. Q1 and Q3 2016 showed strong growth, but Q2 lagged with a year-on-

year decrease of almost 1%.

Yet both perform better this year than the MENA region at large. Egypt’s share of MENA imports from the UK increases

from 5% in 2015 to 6.2% in 2016. Egypt’s share of MENA exports to the UK increases from 5.6% to 6.3% year on year.

UK Exports to MENA & Egypt UK Exports to the MENA region drop by 6.8% in Q3 2016 compared to the same period in 2015. Exports to Egypt

rebound after a 1% drop in Q2. Morocco shows the largest growth (+103%) compared to the same period last year. A

significant decrease is recorded in the UAE (-15%), Saudi Arabia (-14%) and Qatar (-7%).

Q1- Q3 2016 Q1-Q3 2015 % change

MENA £13,966bn £14,993bn -6.8

Egypt £861m £750m 14.7

% share of MENA 6.2 5

UK Exports to MENA % Share

Source: HM Revenue & Customs

32%

25%

12%

6%

6%

3%

5%

2%

9%

UAE

Saudi Arabia

Qatar

Israel

Egypt

Kuwait

Morocco

Oman

Others

UK Imports from MENA & Egypt UK Imports from the MENA region decline by 13% in Q3 2016 compared to the same period a year earlier. Egyptian

exports to the UK see a marginal drop of 2.3% year on year. With the exception of Morocco (+77%) and UAE (+25%),

most MENA countries record a drop in export to the UK for Q3 2016 compared to the same quarter a year earlier; i.e.

Algeria (-69%), Kuwait (-37%), Saudi Arabia (-26%) and Kuwait (-25%).

Q1-Q3 2016 Q1-Q3 2015 % change

MENA £8,242bn £9,475bn -13

Egypt £516m £529m -2.3

% of MENA 6.3 5.6

UK Imports from MENA % Share

Source: HM Revenue & Customs

20%

6%

23%

14%

10%

6%

10%

5%6%

Qatar

Algeria

UAE

Saudi Arabia

Israel

Egypt

Morocco

Kuwait

Others

UK Trade Statistics: MENA & Egypt – Product Breakdown

UK Exports to Egypt

UK exports to Egypt picked up again in the third quarter of 2016 after a strong first quarter and significantly weaker

second quarter.

Egypt’s Industrial Development

As part of Egypt’s government’s proposals to increase infrastructure investment - and its ambitious development plans –

imports in industrial machinery lead the way in driving import growth both medium- and long-term. The quick

completion of the Suez Canal Corridor after just one year of work, commitment to these infrastructure projects is

somewhat proven. Construction is also underway on Egypt’s new road network (over 4000km) for which transport

equipment is needed. It is a sector that is expected to contribute 10% of import growth in the decade to 2030 according

to HSBC’s latest brief on UK trade with Egypt.

German industrial company Siemens signed an €8bn deal with Egypt earlier this year to supply gas and wind power

plants, with the aim of boosting domestic electricity generation by 50%. Against this background, the industrial

machinery sector is expected to contribute 18% of import growth in the decade to 2030.

As the Central Bank of Egypt tightened its control on import products in an effort to limit the outflow of foreign currency,

certain UK export products experienced a decline in demand in the short-term. The recently introduced new trade

decrees (available to download on our website) further make the import of certain finished goods administratively more

complex. The export of prepared foodstuffs for example continues to drop in Q3 2016 by 24% year on year (Q2 2016 saw

a drop of 30% year on year). The central bank’s recent decision to float the pound should alleviate foreign exchange

shortages and reduce restrictions on outflow of foreign currency as well as on imports of finished goods.

UK Exports to Egypt (Q3 2016) – by major product groups

Source: HM Revenue & Customs

9%

12%

19%

14%

46%

Food & beverages

Raw materials, petroleum & petroleum products

Chemicals, pharmaceuticals & related products

Textiles & manufactured goods

Machinery & transport equipment

Rank Commodity 2016 2015 % Change

1. Machinery & Mechanical Appliances (16), of which: 316,309,366 243,690,248 29.8

Machinery & Mechanical Appliances 253,907,906 175,709,249 44.5

Of which: Turbojets 103,792,743 70,074,562 48.1

Electrical Machinery & Equipment 62,401,460 67,980,999 -8.2

2. Chemicals (6), of which: 141,324,001 122,321,881 15.5

Pharmaceutical Products 83,340,419 57,187,503 45.7

3. Base Metals & Articles of Base Metal (15) 116,174,662 71,315,426 62.9

4. Transport & Equipment (17) 56,574,960 91,461,243 -38.1

5. Plastics, Rubber and Articles Thereof (7) 42,897,293 60,653,391 -29.3

6. Vegetable Products (2), of which:

Fruit & Vegetables

41,503,200

40,558,311

34,260,997

32,905,293

21.1

23.3

7. Medical & Other Instruments and Parts (18) 34,904,813 29,737,275 17.4

8. Paper & Paperboard (10) 34,872,197 33,189,340 5.1

9. Mineral Products (5) 27,067,835 16,119,165 67.9

10. Prepared Foodstuffs (4) 12,544,428 16,473,178 -23.8

11. Precious Stones, Metals & Jewellery (14) 11,457,118 8,190,214 39.9

12. Live Animals & Animal Products (1) 8,845,155 6,381,079 38.6

13. Textiles & Textile Articles (11) 6,482,761 6,318,808 2.6

14. Miscellaneous Manufactured Articles (20) 5,068,280 5,192,432 -2.4

15. Building Materials (13) 2,099,087 2,129,878 -1.4

16. Art & Antiques (21) 1,081,159 386,267 179.9

17. Leather, Hides & Skins (8) 469,891 514,782 -8.7

18. Fashion Accessories (12) 353,284 1,122,969 -68.5

19. Wood and Articles Thereof (9) 329,647 70,838 365.4

20. Animal or Vegetable Fats & Oils (3) 210,547 349,923 -39.8

21. Arms & ammunitions (19) 27,991 14,256 96.3

22. Other (22) 58,971 183,092 -67.8

Total 860,656,646 750,076,682 14.7 All figures are in £ thousand Source: HM Revenue & Customs

Full product index on page 13

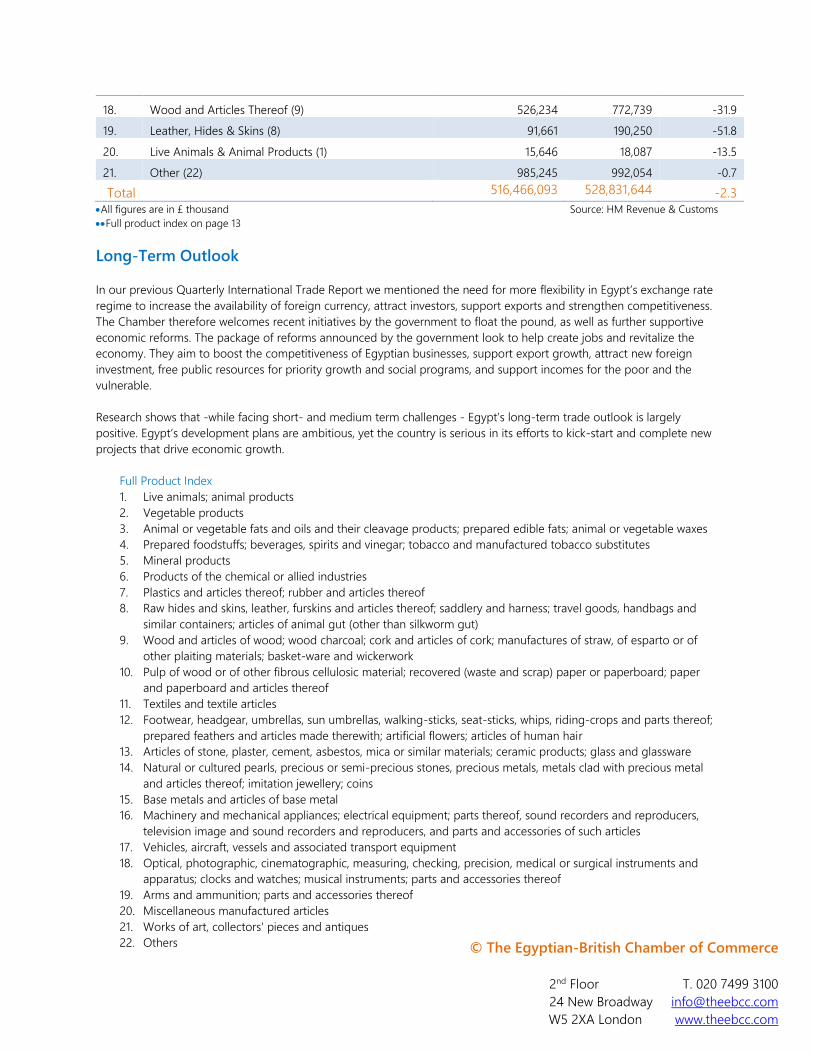

Egyptian Exports to the UK

Egypt’s exports to the UK are down by 2.3% this quarter compared to Q3 2015. While still down on the year, Egyptian

exports are recovering and we no longer see the average 20% decrease year on year that we witnessed last year .

Oil Consumption vs Export

One of the major factors in Egypt’s evolving energy sector has been the rise in consumption, which in turn has put

pressure on the status of the country as a net exporter. Egypt has gone from an importer to an exporter and back for a

number of years. It bought more oil and related products than it sold in 2007 and then again starting in 2012. In 2015

Egypt’s Ministry of Planning reported that 28.6m tonnes of crude oil, liquefied natural gas (LNG), natural gas and other

oil related products are estimated to be imported to Egypt in the 2015/16 fiscal year, at a total cost of $16bn. In terms of

natural gas, it has been a net exporter until very recently.

The surpluses in recent years were the result of increased production in the Western Desert and in offshore areas, but the

productivity of these finds has been falling and the assets cannot produce as much as before without major investments

in enhanced recovery techniques. Egypt’s refining output declined by 28% from 2009 to 2013. In 2013 Egypt’s refined

petroleum output stood at 445,000 bpd, which indicates that refinery utilisation was at 63%.

The drop in the price of oil, to a low of $36.05 in December 2015 for Brent, has affected Egypt’s energy outlook. While on

the one hand it has reduced the costs of the subsidy that needs to be paid, and freed up resources as a result, it also has

the potential to reduce investment in the sector, especially investment in more difficult areas or in finds that require

advanced technology. (source: Oxford Business Group)

R&D Key Driver behind Growth of Chemicals Sector

A projected leading sector in the Egyptian export recovery will be chemicals, with growth expected to average 9% per

year in 2016-2020. Demand is largely driven by the development of chemicals used in agriculture and fast moving

consumer goods. The agriculture sector currently carries out R&D to reclaim land from the desert and prepare it for

cultivation; a key government priority.

Representative of Egypt’s gradual move up the value chain, mineral manufacturers, chemicals and plastics will be some of

the largest contributors to export growth in the long-term. Research further shows that the animal products sector is one

to watch, accounting for 12% of total export growth in the 10 years to 2030.

0

200

400

600

800

1000

2013 2014 2015 Q3 2016 (6 Months)

Egypt's Crude Oil Exports to the UK in £m

Crude Oil Exports Other Exports

Egyptian Exports to the UK (Q3 2016) – by major product groups

Rank Commodity 2016 2015 % Change

1. Machinery & Mechanical Appliances (16) 157,470,259 176,223,761 -10.6

Machinery & Mechanical Appliances 30,333,156 69,105,574 -56.1

Of which: Turbojets 25,773,352 64,489,432 -60

Electrical Machinery & Equipment 127,137,103 107,118,187 18.7

Of which: Insulated Wire, Cable and Other

Insulated Electric Conductors

103,154,352 100,157,785 3

2. Vegetable Products (2), of which: 108,154,305 92,821,051 16.5

Fruit & Vegetables 103,118,655 86,850,402 18.7

3. Textiles & Textile Articles (11) 81,118,303 94,773,877 -14.4

4. Mineral Products (5), of which: 48,629,376 58,296,844 -16.6

Crude Oil 48,206,381 57,982,351 -16.9

5. Plastics, Rubber and Articles Thereof (7) 19,282,955 21,511,970 -10.4

6. Chemicals (6) 18,784,053 21,903,861 -14.2

7. Building Materials (13) 16,513,663 18,821,208 -12.3

8. Transport & Equipment (17) 16,262,576 4,275,845 280.3

9. Paper & Paperboard (10) 15,198,045 11,330,602 34.1

10. Medical & Other Instruments and Parts (18) 13,618,476 8,647,517 57.5

11. Precious Stones, Metals & Jewellery (14) 6,908,248 5,949,458 16.1

12. Base Metals (15) 6,468,133 5,571,652 16.1

13. Prepared foodstuffs (4) 2,997,425 1,194,468 150.9

14. Art & Antiques (21) 932,909 769,109 21.3

15. Miscellaneous Manufactured Items (20) 921,752 2,183,383 -57.8

16. Fashion Accessories (12) 916,095 2,306,464 -60.3

17. Animal or Vegetable Fats & Oils (3) 670,734 277,444 141.8

26%

11%

5%23%

35%

Agricultural products, food & beverages

Raw materials, petroleum & petroleum products

Chemicals, pharmaceuticals & related products

Textiles & other manufactured goods

Electrical appliances, power generators, transport and other

machinery

18. Wood and Articles Thereof (9) 526,234 772,739 -31.9

19. Leather, Hides & Skins (8) 91,661 190,250 -51.8

20. Live Animals & Animal Products (1) 15,646 18,087 -13.5

21. Other (22) 985,245 992,054 -0.7

Total 516,466,093 528,831,644 -2.3 All figures are in £ thousand Source: HM Revenue & Customs

Full product index on page 13

Long-Term Outlook

In our previous Quarterly International Trade Report we mentioned the need for more flexibility in Egypt’s exchange rate

regime to increase the availability of foreign currency, attract investors, support exports and strengthen competitiveness.

The Chamber therefore welcomes recent initiatives by the government to float the pound, as well as further supportive

economic reforms. The package of reforms announced by the government look to help create jobs and revitalize the

economy. They aim to boost the competitiveness of Egyptian businesses, support export growth, attract new foreign

investment, free public resources for priority growth and social programs, and support incomes for the poor and the

vulnerable.

Research shows that -while facing short- and medium term challenges - Egypt’s long-term trade outlook is largely

positive. Egypt’s development plans are ambitious, yet the country is serious in its efforts to kick-start and complete new

projects that drive economic growth.

Full Product Index

1. Live animals; animal products

2. Vegetable products

3. Animal or vegetable fats and oils and their cleavage products; prepared edible fats; animal or vegetable waxes

4. Prepared foodstuffs; beverages, spirits and vinegar; tobacco and manufactured tobacco substitutes

5. Mineral products

6. Products of the chemical or allied industries

7. Plastics and articles thereof; rubber and articles thereof

8. Raw hides and skins, leather, furskins and articles thereof; saddlery and harness; travel goods, handbags and

similar containers; articles of animal gut (other than silkworm gut)

9. Wood and articles of wood; wood charcoal; cork and articles of cork; manufactures of straw, of esparto or of

other plaiting materials; basket-ware and wickerwork

10. Pulp of wood or of other fibrous cellulosic material; recovered (waste and scrap) paper or paperboard; paper

and paperboard and articles thereof

11. Textiles and textile articles

12. Footwear, headgear, umbrellas, sun umbrellas, walking-sticks, seat-sticks, whips, riding-crops and parts thereof;

prepared feathers and articles made therewith; artificial flowers; articles of human hair

13. Articles of stone, plaster, cement, asbestos, mica or similar materials; ceramic products; glass and glassware

14. Natural or cultured pearls, precious or semi-precious stones, precious metals, metals clad with precious metal

and articles thereof; imitation jewellery; coins

15. Base metals and articles of base metal

16. Machinery and mechanical appliances; electrical equipment; parts thereof, sound recorders and reproducers,

television image and sound recorders and reproducers, and parts and accessories of such articles

17. Vehicles, aircraft, vessels and associated transport equipment

18. Optical, photographic, cinematographic, measuring, checking, precision, medical or surgical instruments and

apparatus; clocks and watches; musical instruments; parts and accessories thereof

19. Arms and ammunition; parts and accessories thereof

20. Miscellaneous manufactured articles

21. Works of art, collectors' pieces and antiques

22. Others © The Egyptian-British Chamber of Commerce

2nd Floor T. 020 7499 3100

24 New Broadway [email protected]

W5 2XA London www.theebcc.com