Embed Size (px)

Citation preview

International Macro Finance

Financial Crises: currency

Francesco Franco

Nova SBE

March 10, 2013

Francesco Franco International Macro Finance 1/21

Framework

I generation: anatomy

• Until the early 1990s, the prevailing intellectual framework forthinking about currency crises was the speculative-attackmodel developed by Krugman (1979) and Flood and Garber(1984)

• The speculative-attack model views currency crises as runs onforeign-exchange reserves at central banks

• the run need not be ascribed to the irrationality of marketparticipants, but that it can be explained, instead, by the veryrationality of their expectations

• the speculative attack is provoked by a monetary or fiscalpolicy that, by assumption, is incon- sistent with themaintenance of the fixed currency peg

Francesco Franco International Macro Finance 2/21

Framework

II generation: causes

• The limitation of the speculative-attack model in explainingthe underlying causes of currency crises became morefrustrating after the EMS crisis of 1992–93

• combination of mounting unemployment and the high interestrates imposed upon them by the German monetary-unificationshock

• nature of the fundamentals’ relationship with speculation:multiple equilibria and self-fulfilling

• The policymaker makes this decision by weighing the benefitsof maintaining the fixed peg against the costs of change,taking into account the broad economic environment

Francesco Franco International Macro Finance 3/21

Framework

Theory of reflexivity

• Fundamentals -> expectations -> fundamentals:formalization of animal spirits

• For a currency to be vulnerable to self-fulfilling speculation,the fundamentals must first put it in a state of fragility

• policies exogenous versus endogenous

Francesco Franco International Macro Finance 4/21

Framework

A small model

consider our model where PPP holds in two periods t = 1, 2 ,namely short (price are fixed) and long run (price are flexible)

mdt = pt + „yt ≠ ÷it

pt = pút + st

it = iút + Etst+1

≠ st

Francesco Franco International Macro Finance 5/21

Framework

A small model

in period t = 2 we have

p2

= s2

+ pú

and for simplicity we assume

p1

= s + pú

furthermore assume that i2

= iú, output is exogenous and allforeign variables are fixed

Francesco Franco International Macro Finance 6/21

Framework

A small model

The endogenous variables are i1

, s1

, s2

, p2

. Consider the quantity ofmoney compatible with a fixed exchange rate in t = 1, 2

m = s + pú + „y ≠ ÷iú

if exchange rate has changed then in t = 2

m2

= s2

+ pú + „y ≠ ÷iú

which impliess2

= s + m2

≠ m

that states that in the Long Run the exchange rate is proportionalto the quantity of domestic money

Francesco Franco International Macro Finance 7/21

Framework

A small model

now in t = 1m

1

= s1

+ pú + „y ≠ ÷i1

combining with the UIP i1

= iú + E1

s2

≠ s1

and subtracting m

i1

= iú ≠ 1÷(m

1

≠ m)

an increase in the quantity of money decreases the nominal interestrate in the first period, finally

s1

=1÷(m

1

≠ m) + s + (m2

≠ m)

the exchange rate in period one depends on the quantity of moneyin t = 1, 2 (can u see the overshooting)

Francesco Franco International Macro Finance 8/21

Speculative Attacks

I generation: exogenous policy

Consider a CB that controls M = mmH and for simplicitymm = 1. Now in the assets side you have both Domestic Bonds Dand Foreign Bonds R = sBF which is a residual as for the momentwe assume no sterilization

Mt = Dt + Rt

Francesco Franco International Macro Finance 9/21

Speculative Attacks

I generation: exogenous policy

• Assume that the reserves must stay above a floorRt > R, t = 1, 2

• the “run” equilibrium as discussed by Diamond and Dybvig(1983, 1995):

• At the beginning of t = 1, agents address their demands for Ragainst domestic currency to the central bank

• Demand is served by the bank at rate s as long as someforeign-exchange reserves remain available

• When exhausted, demanders are then randomly allocated in aqueue, which determines the order in which they will beserved, and at which rate

• The following ones are faced with a di�erent rate, the shadowflexible exchange rate, which is determined by thepost-devaluation monetary conditions

Francesco Franco International Macro Finance 10/21

Speculative Attacks

I generation: exogenous policy

The shadow flexible exchange rate is the exchange rate thatprevails when the central bank holds no reserves in excess of thefloor:

s1

=1÷(ln (D

1

+ R) ≠ m) + s + (ln (E1

D2

+ R) ≠ m)

ands2

= s + ln (E1

D2

+ R) ≠ m

where E1

D2

is the period-two level of domestic credit expected inperiod one

Francesco Franco International Macro Finance 11/21

Speculative Attacks

I generation: exogenous policy

The central point of the speculative-attack model is that a run isan equilibrium if and only if private agents expect it to beassociated with a devaluation, that is, if the shadow flexibleexchange rate is higher than the fixed rate:

st > s

Private agents, knowing that the domestic currency is about to bedevalued, will try to outrun the devaluation: rational behavior

Francesco Franco International Macro Finance 12/21

Speculative Attacks

I generation: exogenous policy

Figure : Speculative attackFrancesco Franco International Macro Finance 13/21

Speculative Attacks

I generation: exogenous policy

• The occurence of a speculative attack is determined by thecurrent and the expected stance of monetary policy

• insights: the exchange rate—unlike foreign-exchangereserves—does not jump at the time of the attack

• you can break the speculative attack if LLR in forex

Francesco Franco International Macro Finance 14/21

Speculative Attacks

Ii generation: self-fulfilling equilibria

assume that the second-period monetary policy depends on thegovernment’s decision whether or not to devalue in the first period:

monetary authorities choose D f in the second period if they havemanaged to maintain the fixed peg in the previous period, and D d ifthey have not. The reaction function of the monetary authorities maythus be written as

! no devaluation in period one " D2 = D f

(R) #$ a devaluation in period one " D2 = D d .

Let us assume that monetary policy is more expansionary in periodtwo if a devaluation has occurred in period one, that is, D d > D f. Thiscan be the case, as argued by Obstfeld (1986), if the government is cutoff from external borrowing after a devaluation and has to monetize itspublic debt to a larger extent than before (an argument modeled byVan Wijnbergen, 1991). Or it may be that the government, havingforegone the benefits of its commitment to the fixed currency peg,switches to the optimal monetary policy under floating, which may bemore expansionary than the policy required to maintain the fixed peg.9

If we assume, furthermore, that (D1, D f) is in region I of Figure 1, andthat (D1, D d) is in region III, then the model admits two equilibria. Inthe first equilibrium, the domestic currency is not attacked in periodone, and the authorities maintain the fixed peg in period two by imple-menting a moderate expansion of domestic credit. In the secondequilibrium, the domestic currency is attacked in period one, and theauthorities validate the attack ex post by a more vigorous expansion ofdomestic credit. The fate of the currency is then determined by the“animal spirits” of speculators, or to put it more formally, by an exoge-nous sunspot variable coordinating their expectations on one equilibriumor the other.

Self-fulfilling speculative attacks are observationally equivalent toattacks based on fundamentals—the behavior of speculators looks thesame, and in both cases, the attack is justified ex post by an expansion-ary shift in period-two monetary policy—but they imply very differentviews of the role of speculation. In the previous section’s model,speculation was purely the reflection of an underlying fundamentalsproblem, for which the responsibility lay squarely with the domesticauthorities. This section’s model, however, allows an interpretation ofthe crisis that is less favorable to speculators, because it is their collec-tive behavior that causes the collapse of the currency. The domesticpolicymaker is partly responsible for the crisis by making himself or

9 The monetary policy chosen under floating is not necessarily optimal, however;consider, for example, the case in which opting out involves a switch to discretion.

18

Figure : Policy Rule

where Dd > Df : Region I and Region III are two equilibria

Francesco Franco International Macro Finance 15/21

Speculative Attacks

II generation: self-fulfilling equilibria

In fact the authority could do something...increase the interest rateor sterilize:

ln(D1

+ R) < m + min [÷ (m ≠ ln(E1

D2

+ R)) , 0]

i1

= iú + E1

s2

≠ s, R1

> R

The rule insures to be in region I or II of the figure. If they do notit must be for a good reason.

Francesco Franco International Macro Finance 16/21

Speculative Attacks

II generation: self-fulfilling equilibria with macro

simplifying assumptions:• monetary authorities can sterilize reserves flows

instantaneously and set the quantity of money in periods oneand two at any desired level

• s1

= s• cares about unemployment u

Francesco Franco International Macro Finance 17/21

Speculative Attacks

II generation: self-fulfilling equilibria with macro

• The amount of the devaluation, if it takes place, is µ. Thismeans that if there is a devaluation m

2

= m + µ,s2

= ¯s + µand fi = µ

• There is a Phillips Curve

u2

= flu1

≠ – (fi ≠ Efi)

• The authorities have a loss function

L = (u2

)2 + ”C

where ” is a dummy variable indicating the policymaker’s decision,and C is the cost of opting out of the fixed-exchange-ratearrangement

Francesco Franco International Macro Finance 18/21

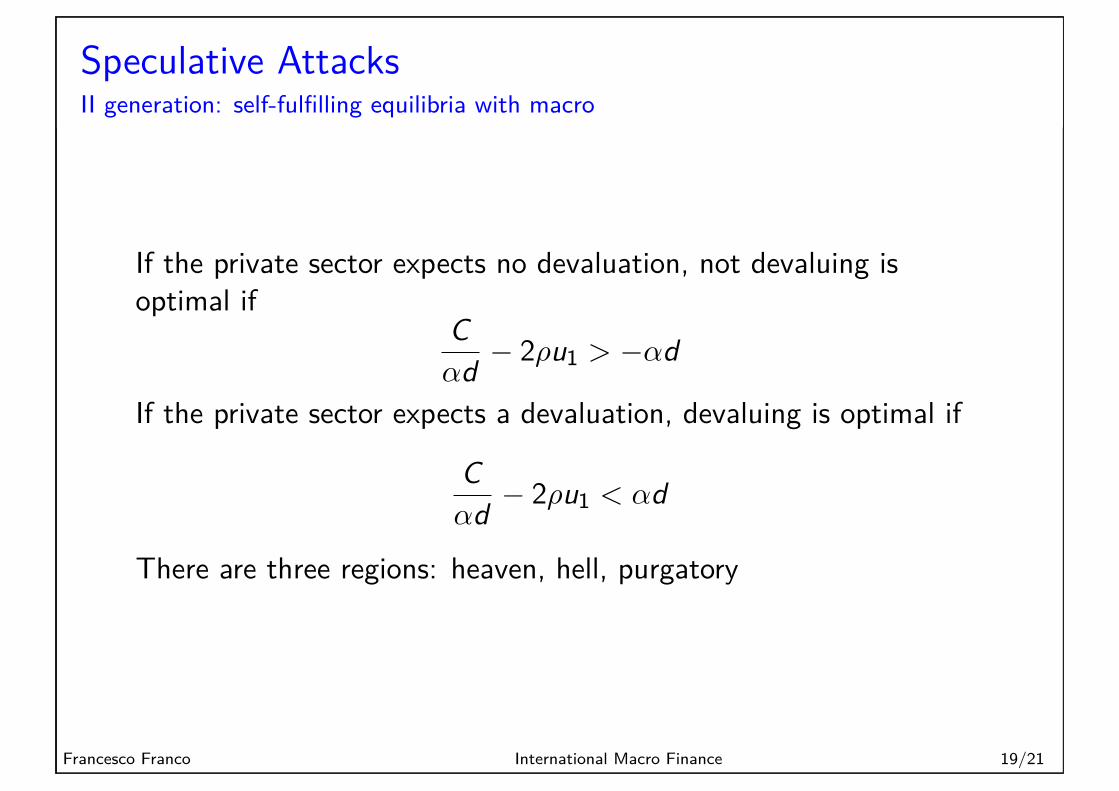

Speculative Attacks

II generation: self-fulfilling equilibria with macro

If the private sector expects no devaluation, not devaluing isoptimal if

C–d ≠ 2flu

1

> ≠–d

If the private sector expects a devaluation, devaluing is optimal if

C–d ≠ 2flu

1

< –d

There are three regions: heaven, hell, purgatory

Francesco Franco International Macro Finance 19/21

Speculative Attacks

II generation: self-fulfilling equilibria with macro in EMU

Speculative attack

Balance of payment crisis, Sovereign debt crisis...

Figure: Speculative attack on sovereign

Francesco Franco International Finance 17/98

Figure : The LLR to break multiplicity

Francesco Franco International Macro Finance 20/21

Readings

(*) Olivier Jeanne, SPECIAL PAPERS IN INTERNATIONALECONOMICS No. 20, March 2000, Currency Crises: aperspective on recent theoretical developmentsObsteld-Rogo�, chapter 8.4.2Paul de Grauwe, The European Central Bank as a lender oflast resort, Vox 18 August 2011.

Francesco Franco International Macro Finance 21/21