Embed Size (px)

Citation preview

Chartered Professional Accountants of Canada, CPA Canada, CPA are trademarks and/or certification marks of the Chartered Professional Accountants of Canada.

© 2019, Chartered Professional Accountants of Canada. All Rights Reserved. 2019-01-15

Intermediate Management Accounting

Primer

Table of Contents

INTRODUCTION ............................................................................................................. 1

PART 1: ROLE OF THE MANAGEMENT ACCOUNTANT .............................................. 1

Cost classifications ................................................................................................... 1

Cost flows used in manufacturing systems and the schedule of cost of goods manufactured ............................................................................................................ 2

Cost estimation ......................................................................................................... 3

Statistical regression approach ............................................................................. 4

Cost-volume-profit analysis ....................................................................................... 4

The CVP model .................................................................................................... 4

Taxes and the CVP equation ................................................................................ 6

Multi-product CVP analysis ................................................................................... 7

Practice questions .................................................................................................... 7

PART 2: CAPACITY ...................................................................................................... 12

Support department cost allocation ........................................................................ 12

Allocation methods ............................................................................................. 12

Job order costing .................................................................................................... 13

Components and steps of a job order costing system ........................................ 13

Normal overhead rates and denominator activity ............................................... 13

Single plant-wide versus multiple overhead cost pools ...................................... 14

Accounting entries underlying job order costing ................................................. 16

Joint and by-product costing ................................................................................... 16

Joint cost allocation methods.............................................................................. 16

Practice questions .................................................................................................. 17

PART 3: PROCESS COSTING ..................................................................................... 22

Illustration of a typical process costing system at a soft drink manufacturing plant 22

Spoilage .................................................................................................................. 26

Transferred-in costs ................................................................................................ 26

Indirect cost allocation systems .............................................................................. 26

ABC systems .......................................................................................................... 27

The ABC cost hierarchy ...................................................................................... 27

Practice questions .................................................................................................. 29

PART 4: VARIOUS COSTING METHODS AND BUDGETING ..................................... 35

Variable (direct), absorption (full) and throughput costing ....................................... 35

Performance evaluation ...................................................................................... 38

Budgeting ................................................................................................................ 38

The master budget ............................................................................................. 39

Pricing ..................................................................................................................... 41

Cost information and short- and long-term pricing .............................................. 41

Practice questions .................................................................................................. 43

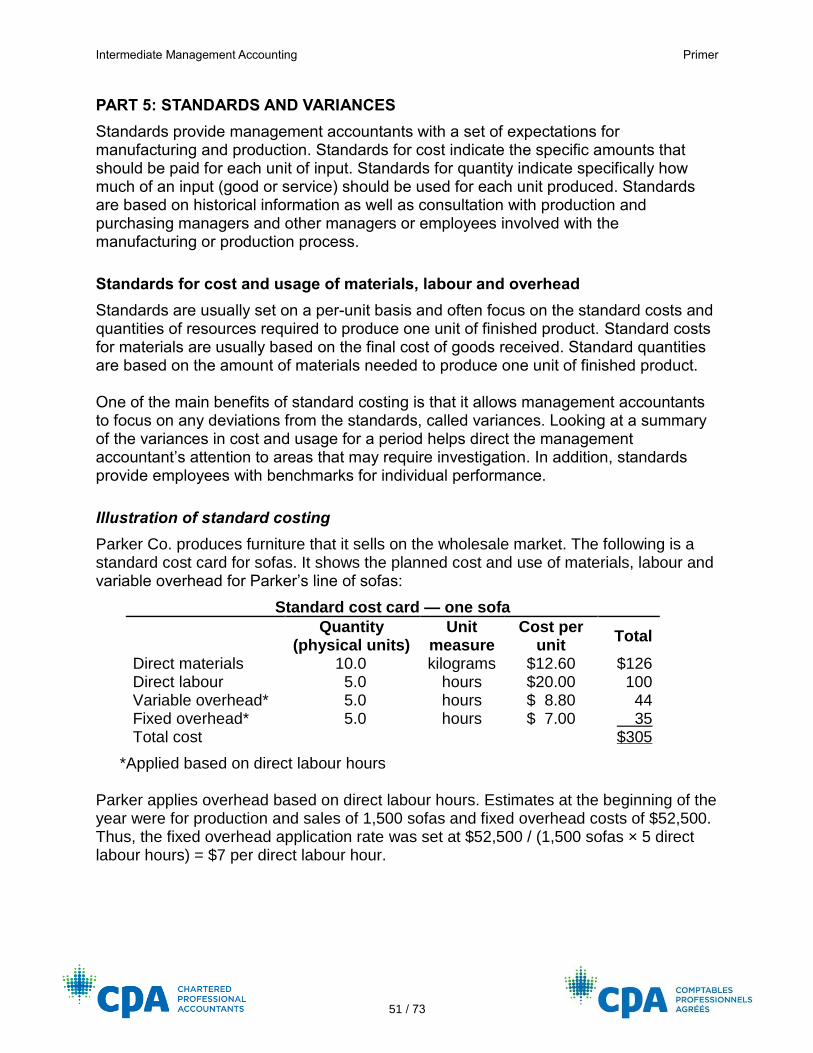

PART 5: STANDARDS AND VARIANCES..................................................................... 51

Standards for cost and usage of materials, labour and overhead ........................... 51

Illustration of standard costing ............................................................................ 51

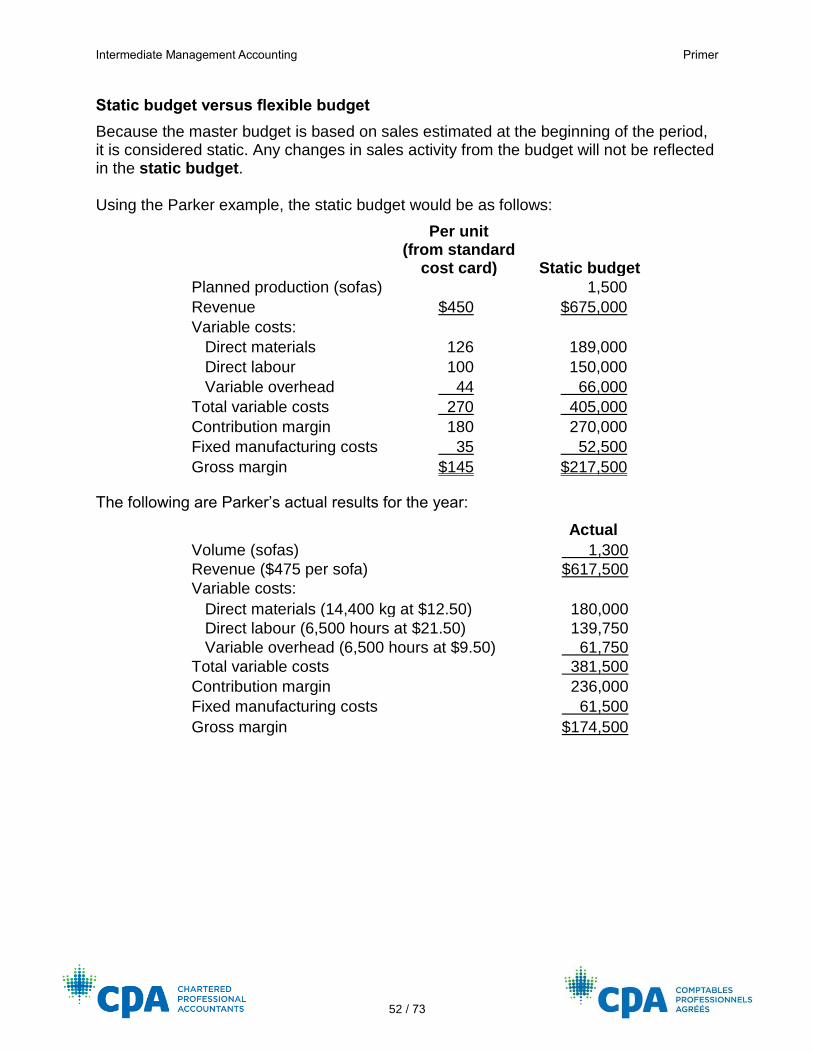

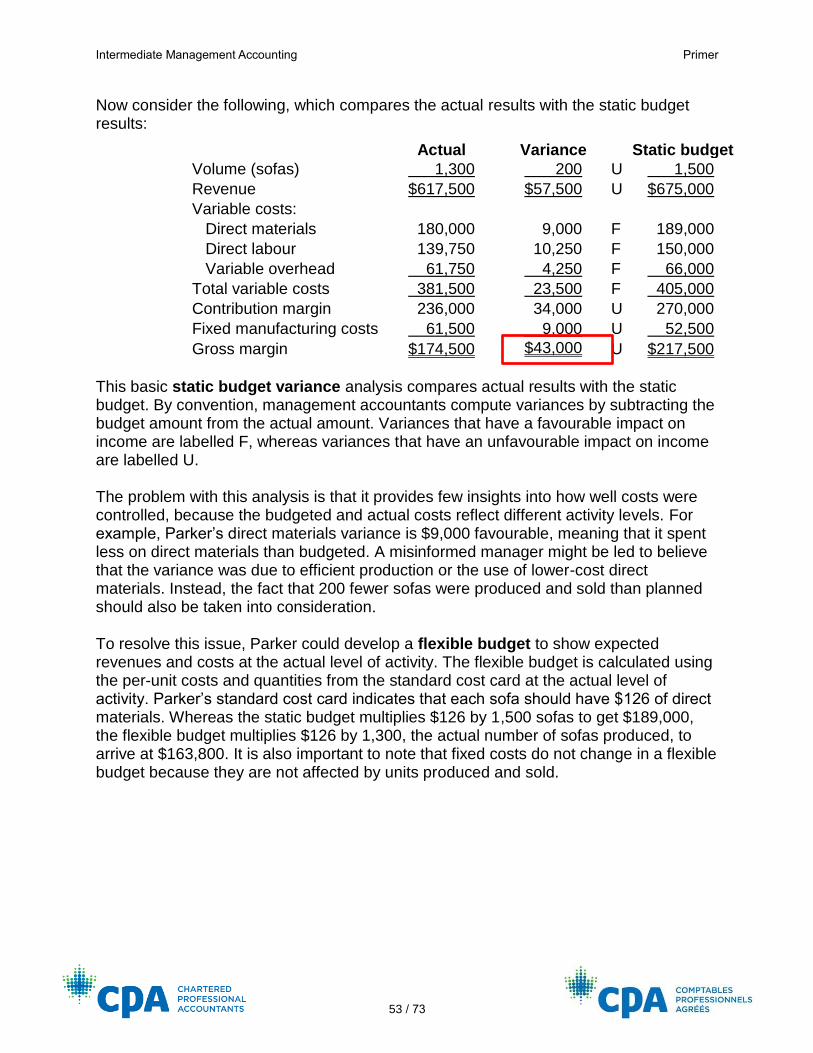

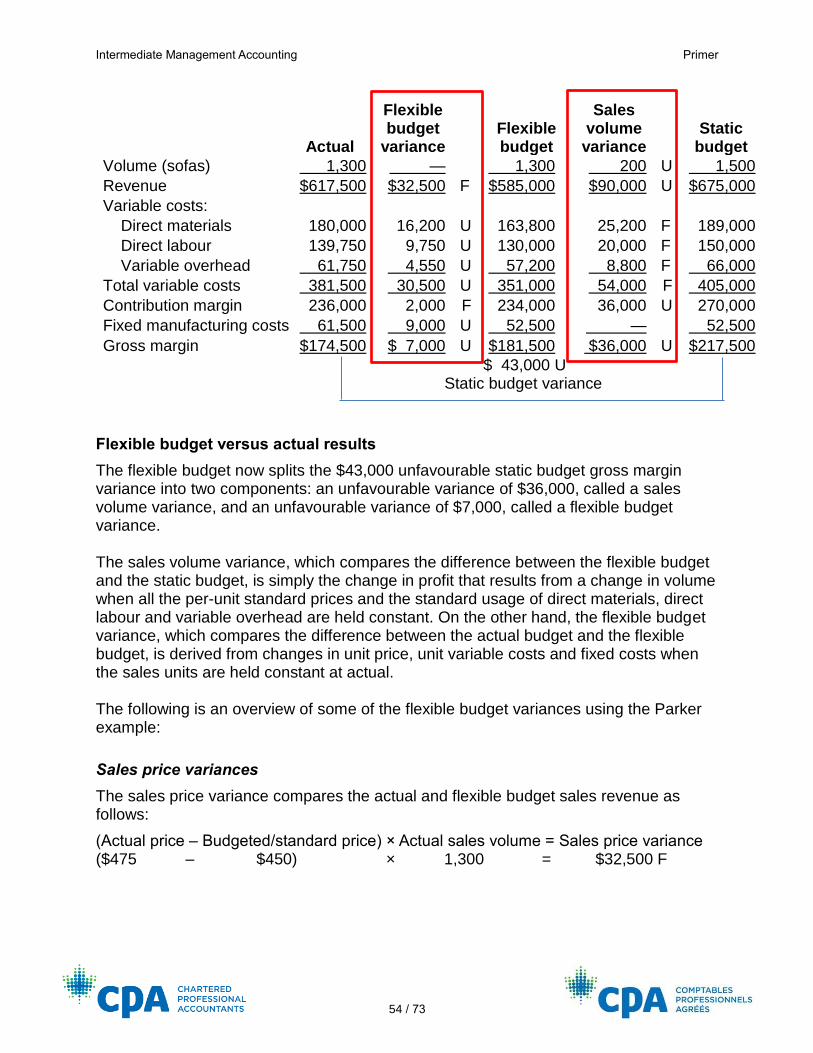

Static budget versus flexible budget ....................................................................... 52

Flexible budget versus actual results ...................................................................... 54

Sales price variances ......................................................................................... 54

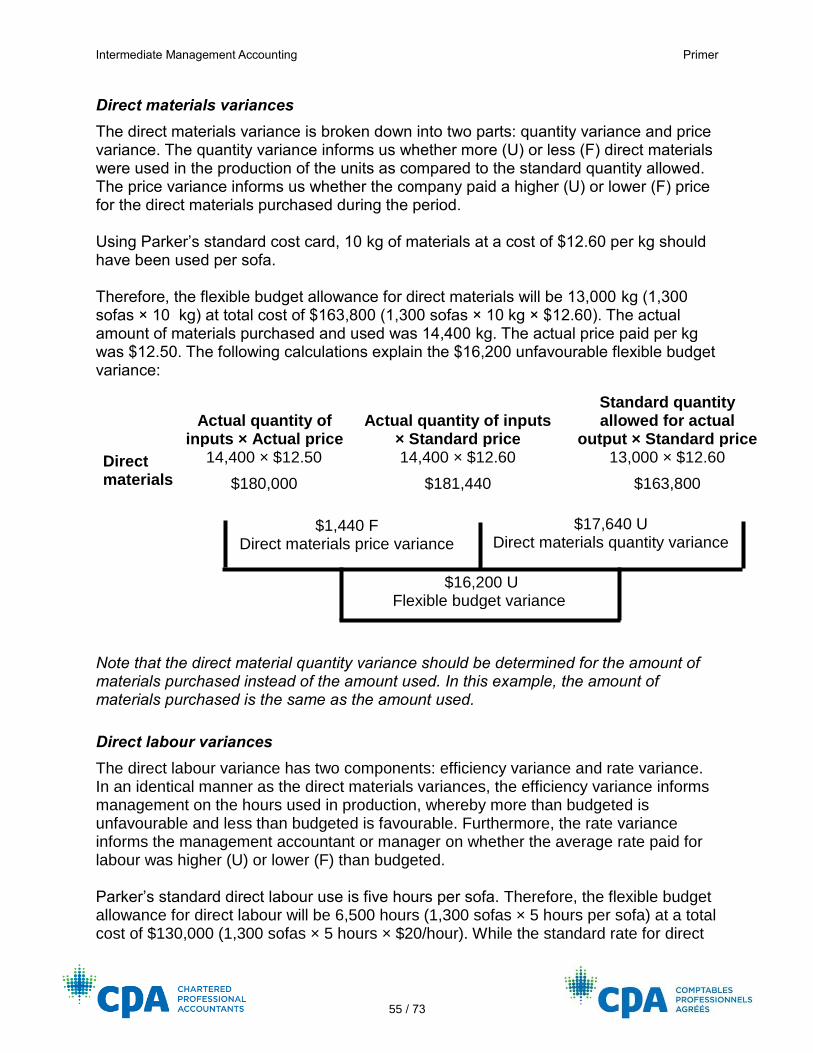

Direct materials variances .................................................................................. 55

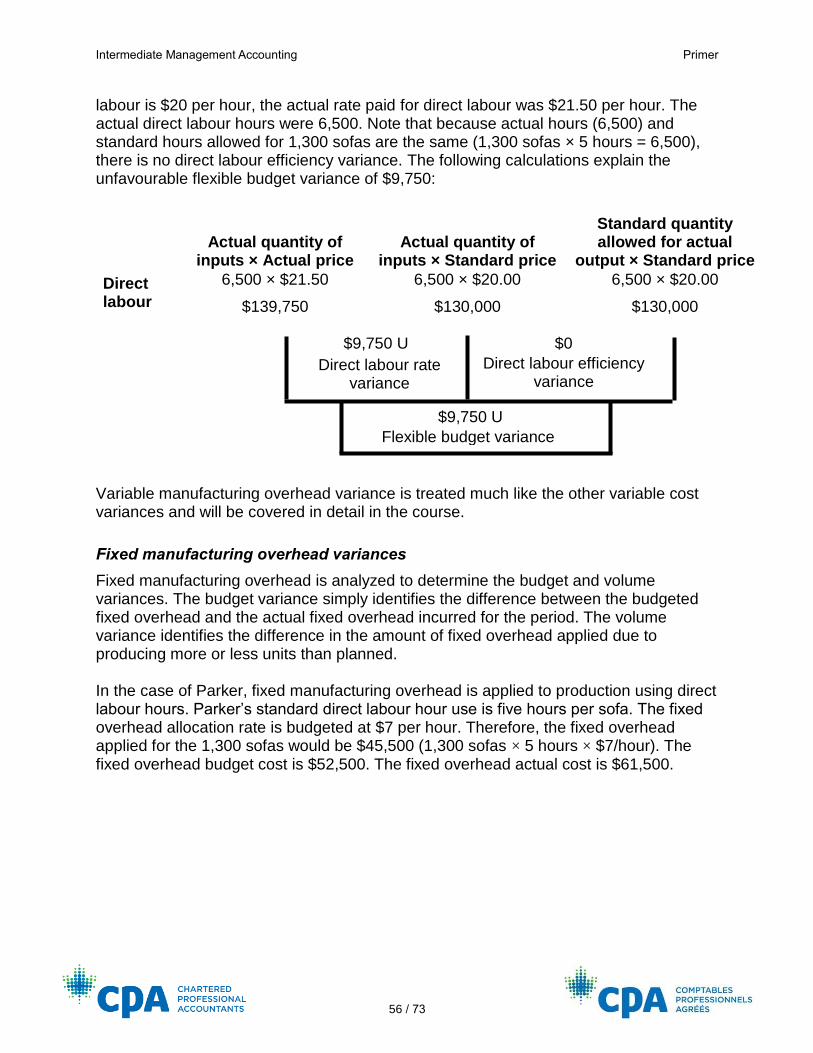

Direct labour variances ....................................................................................... 55

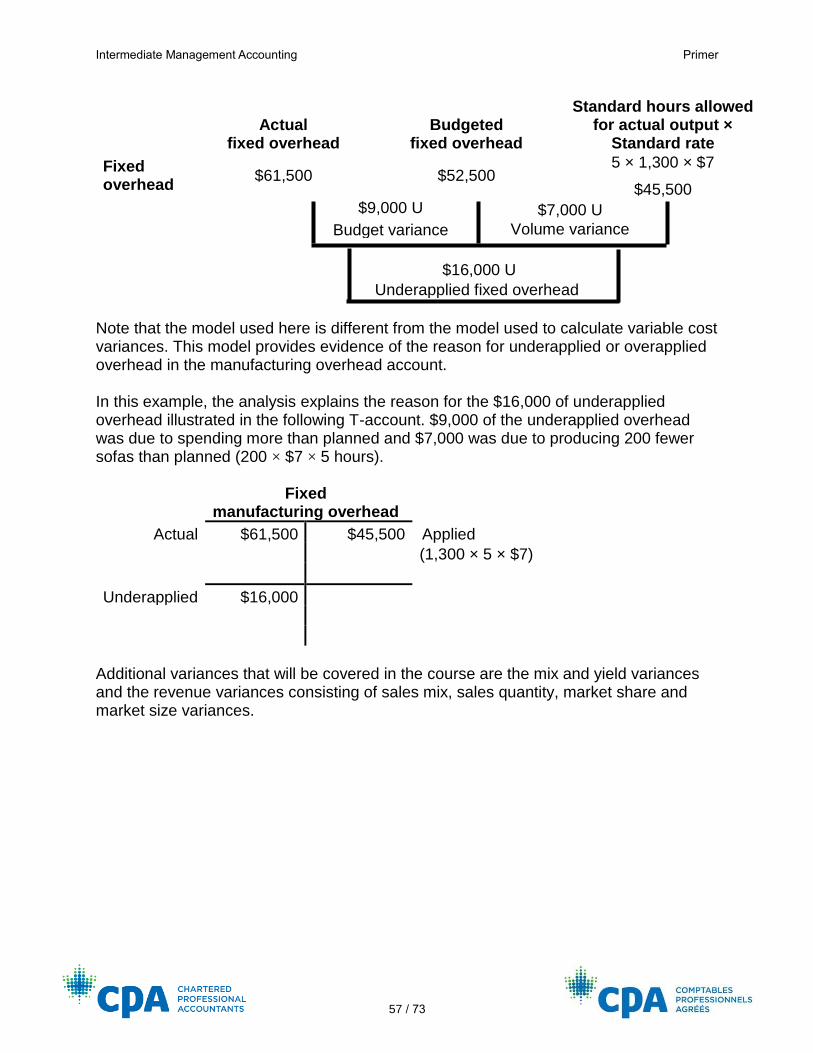

Fixed manufacturing overhead variances ........................................................... 56

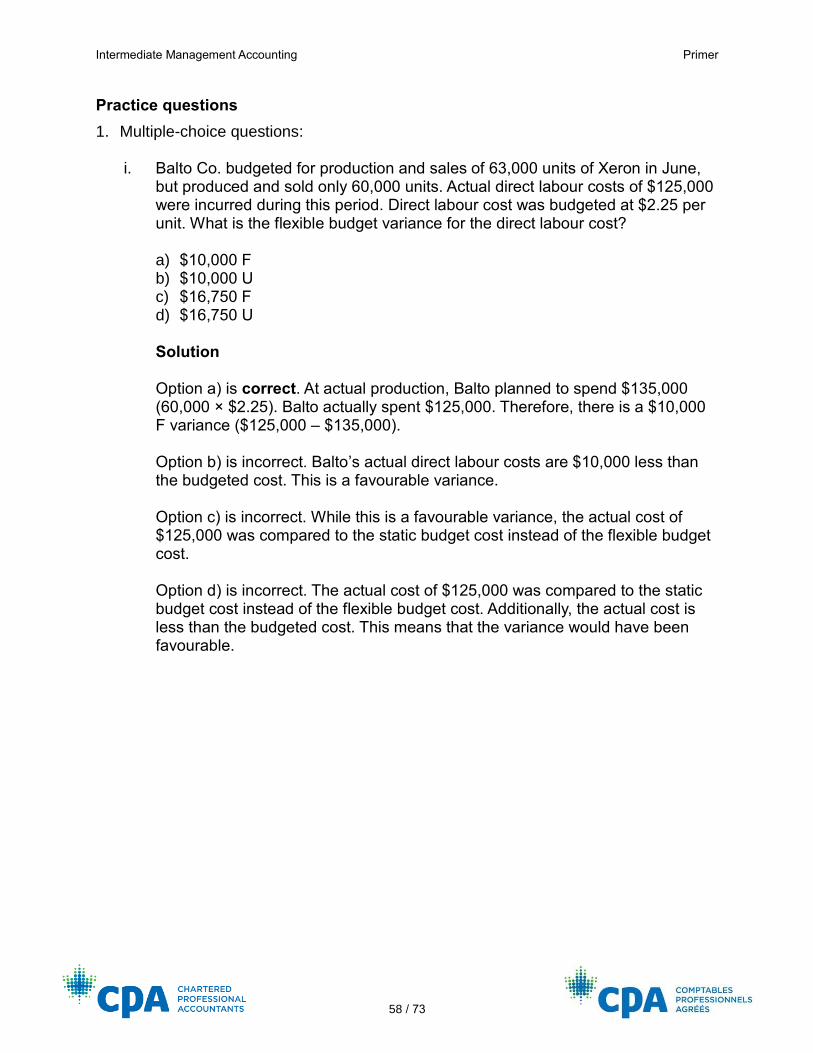

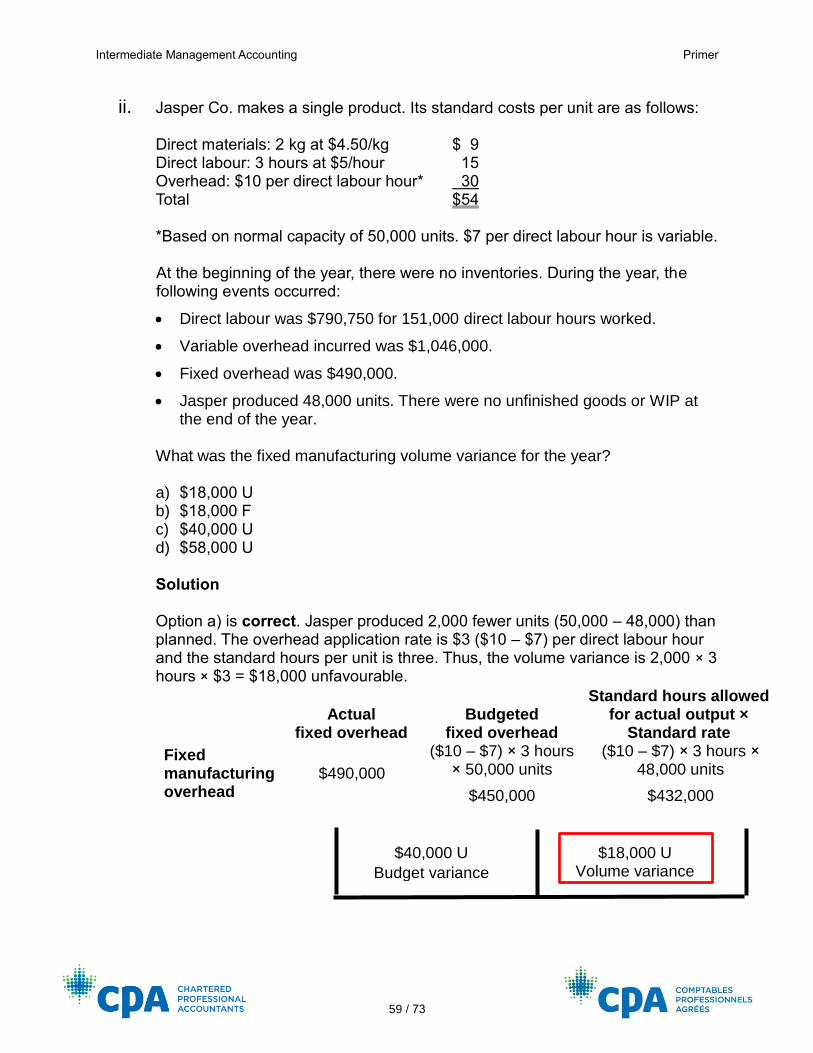

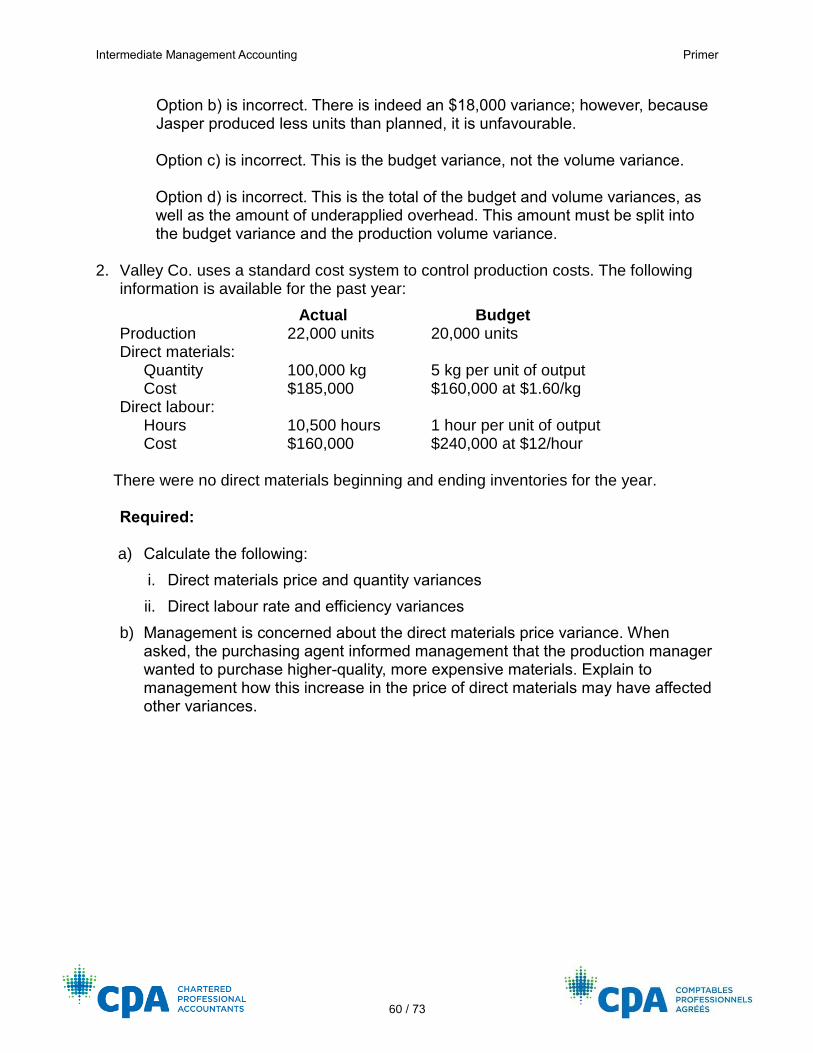

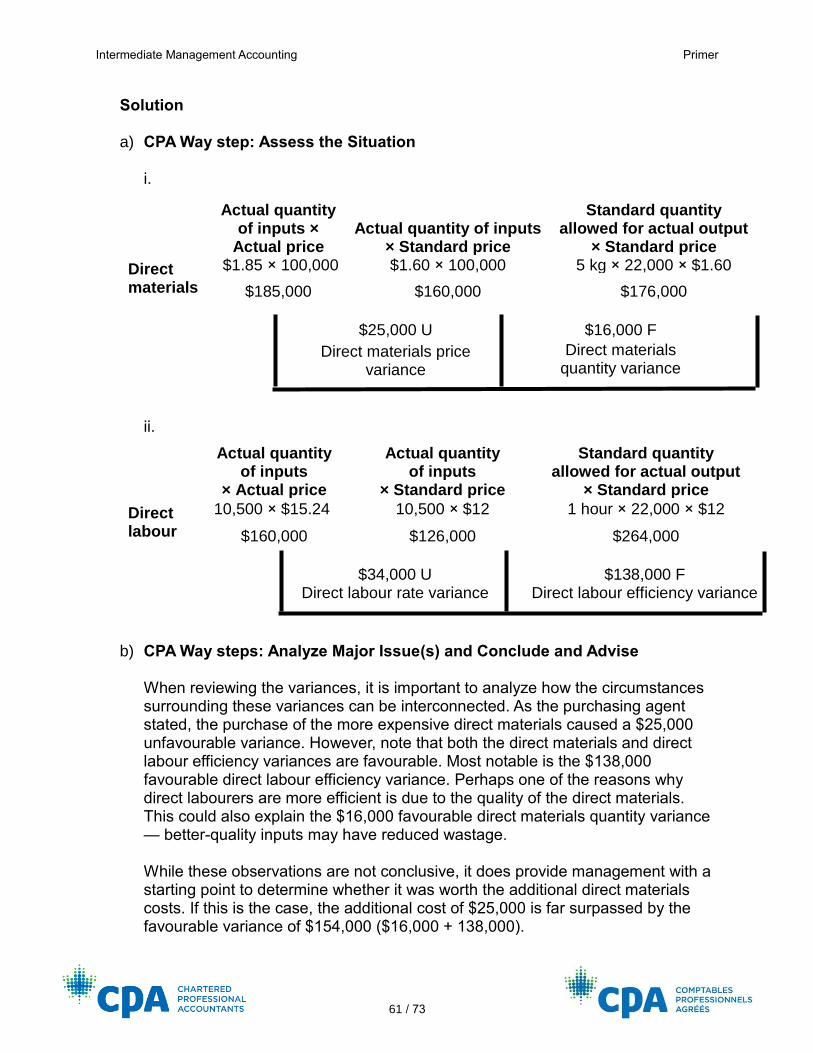

Practice questions .................................................................................................. 58

PART 6: RELEVANT COSTS ........................................................................................ 62

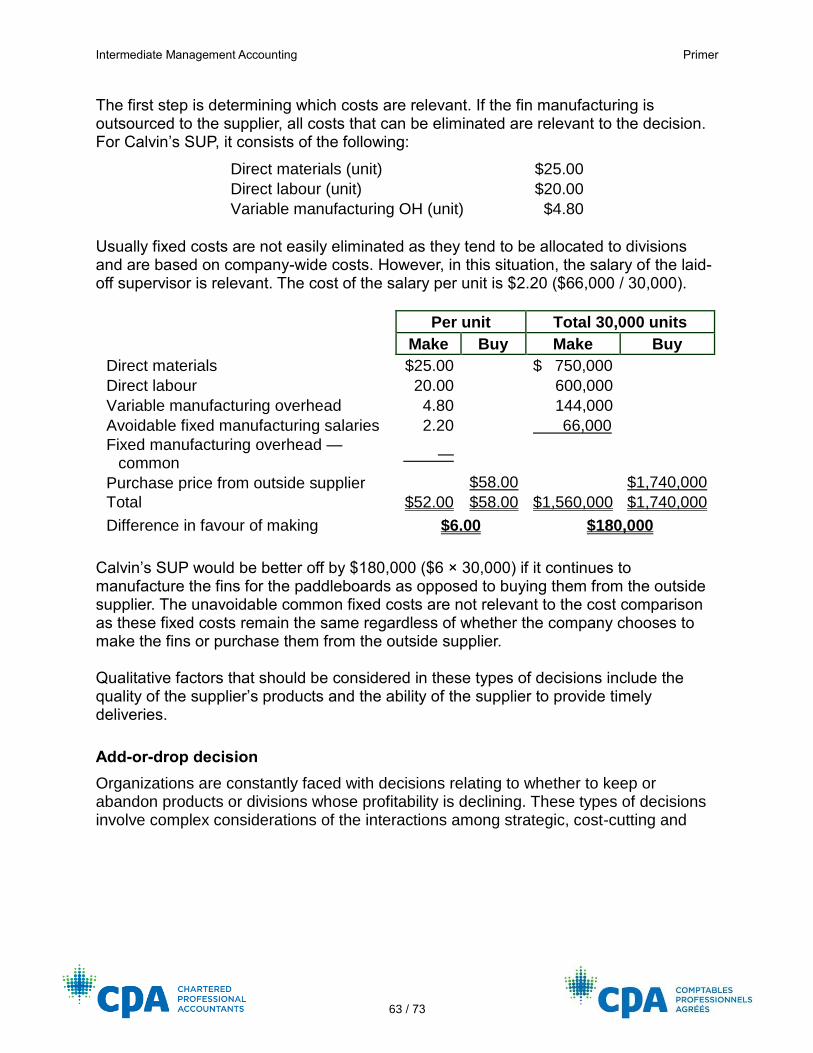

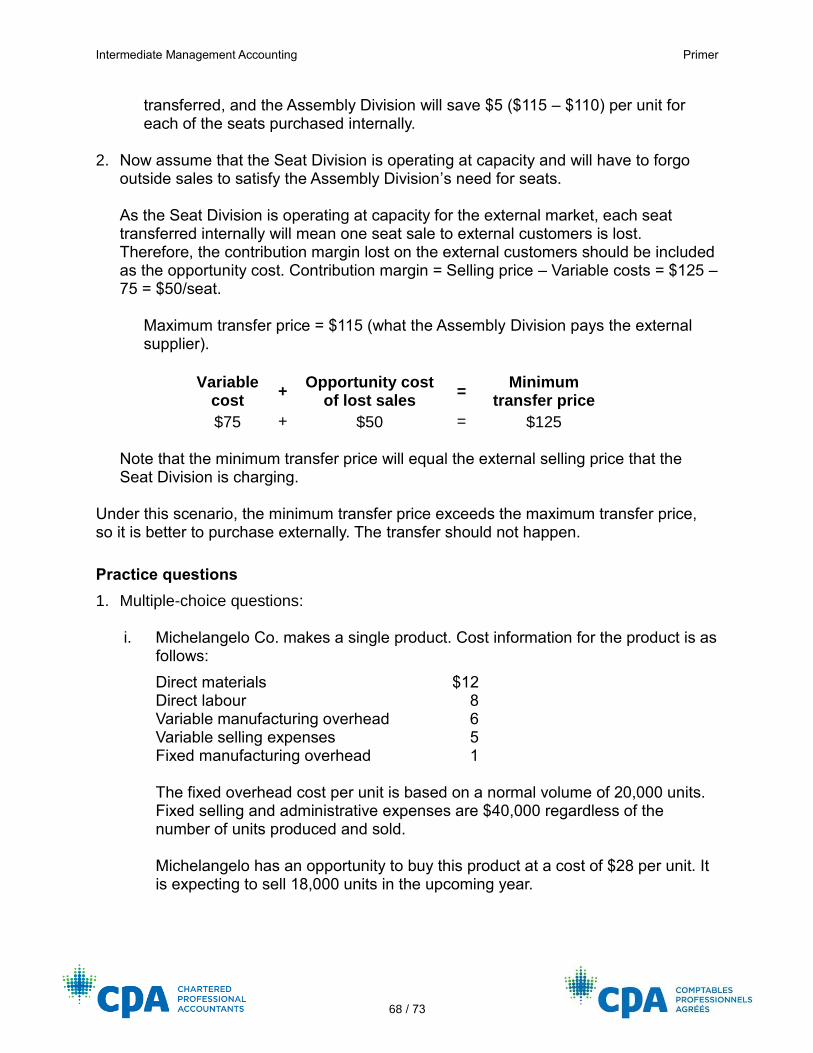

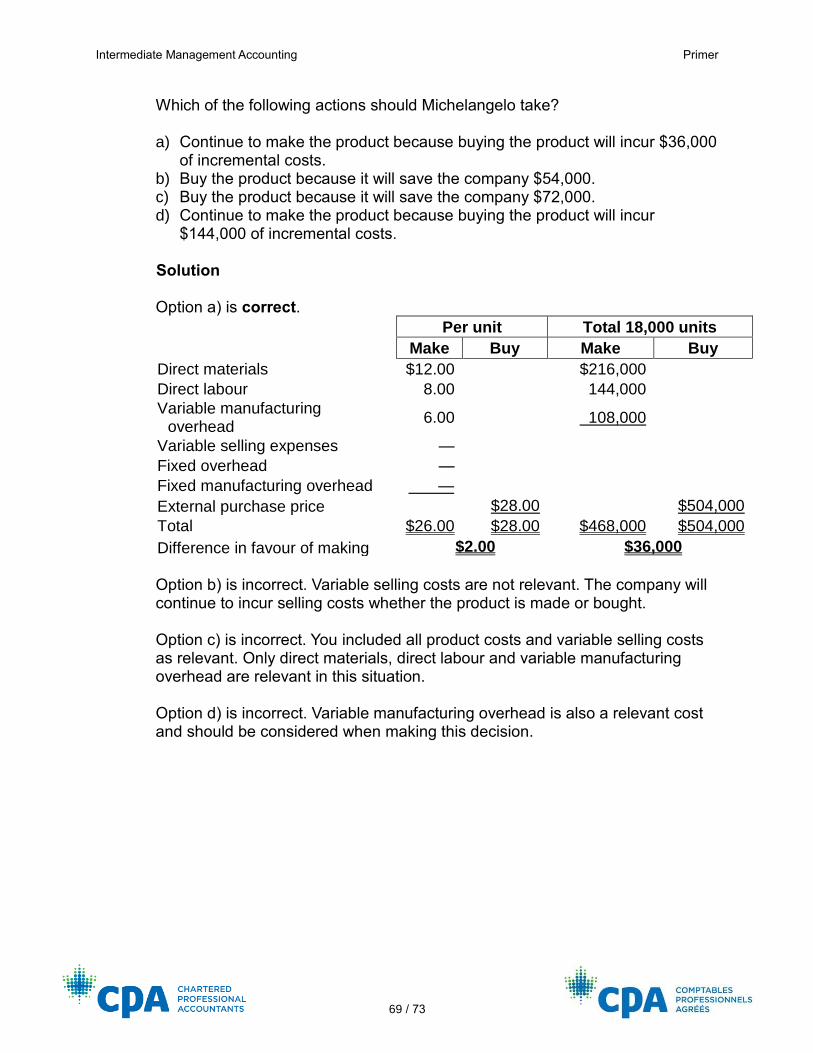

Make-or-buy decision.............................................................................................. 62

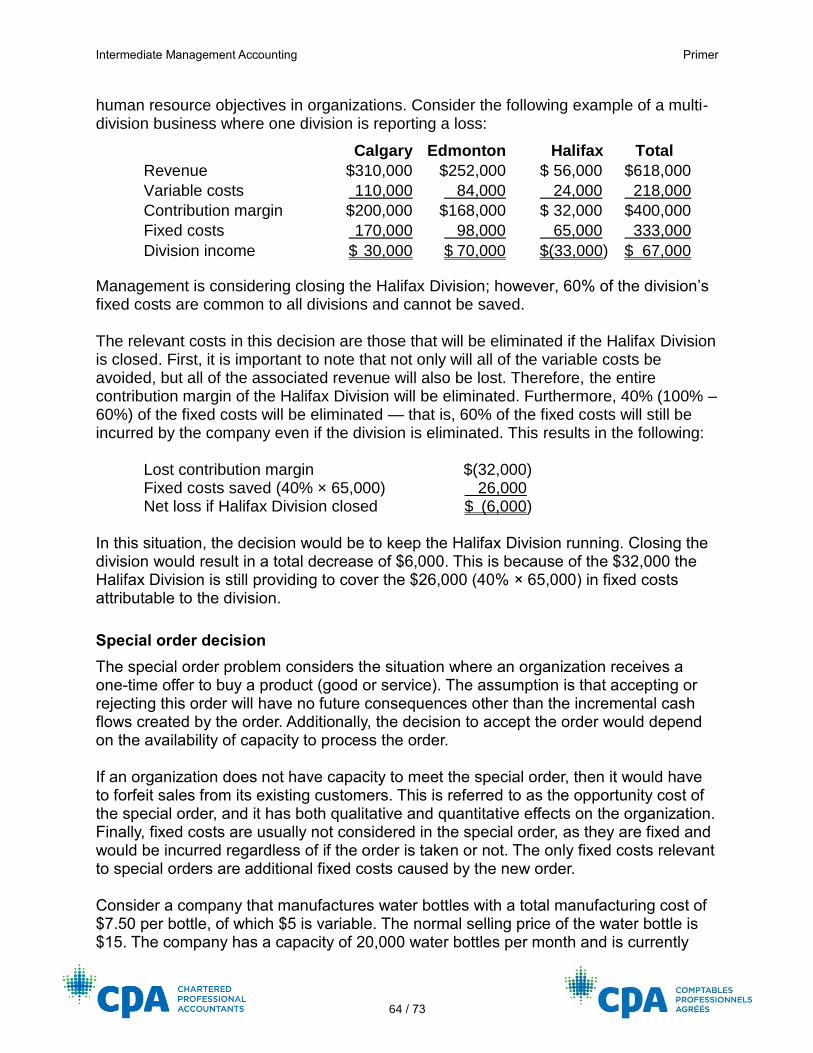

Add-or-drop decision............................................................................................... 63

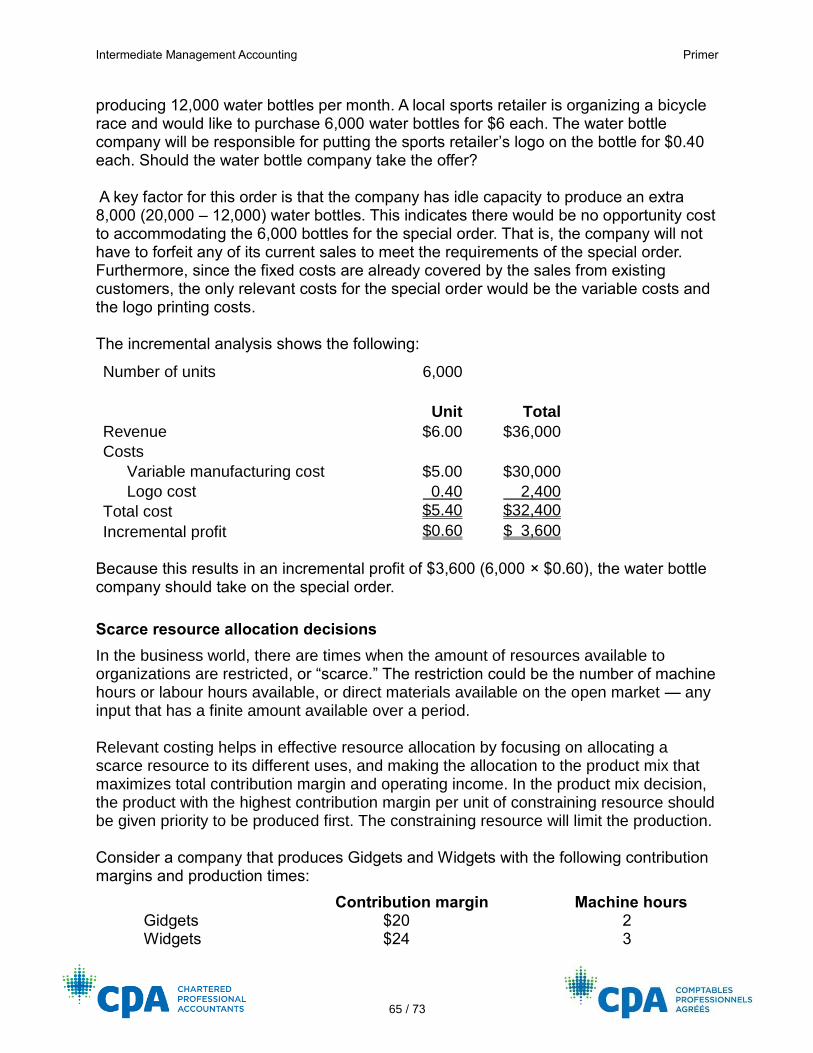

Special order decision............................................................................................. 64

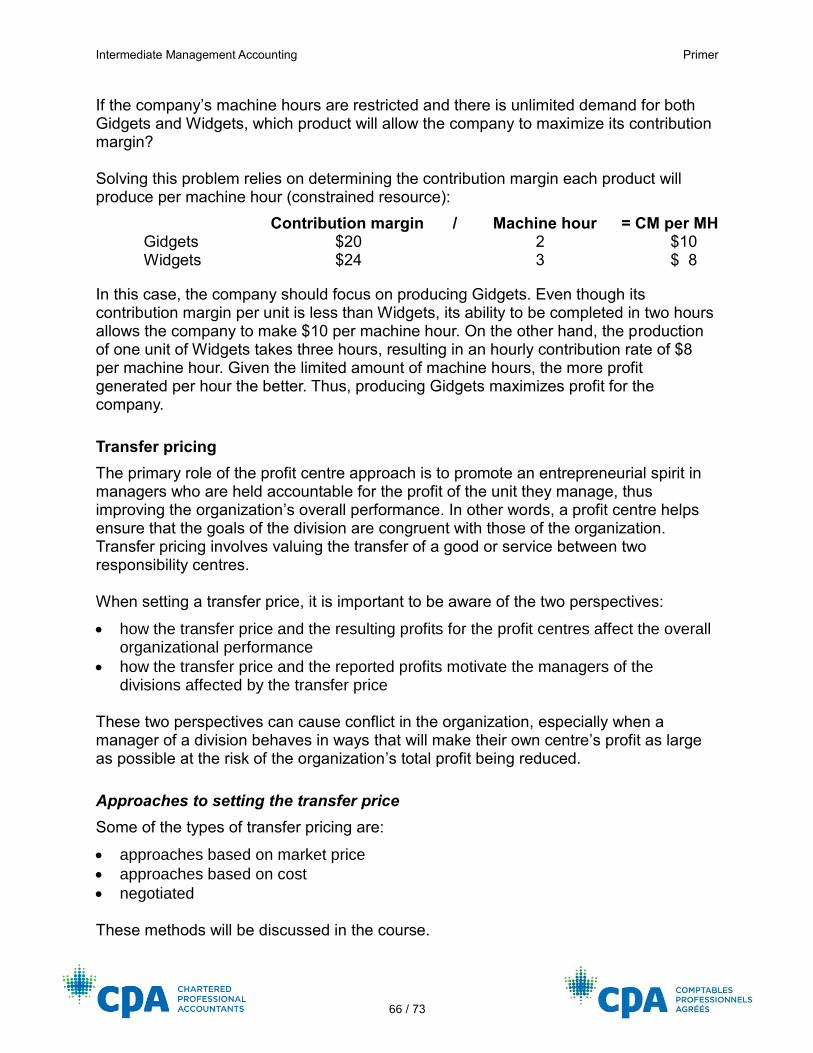

Scarce resource allocation decisions ...................................................................... 65

Transfer pricing ....................................................................................................... 66

Approaches to setting the transfer price ............................................................. 66

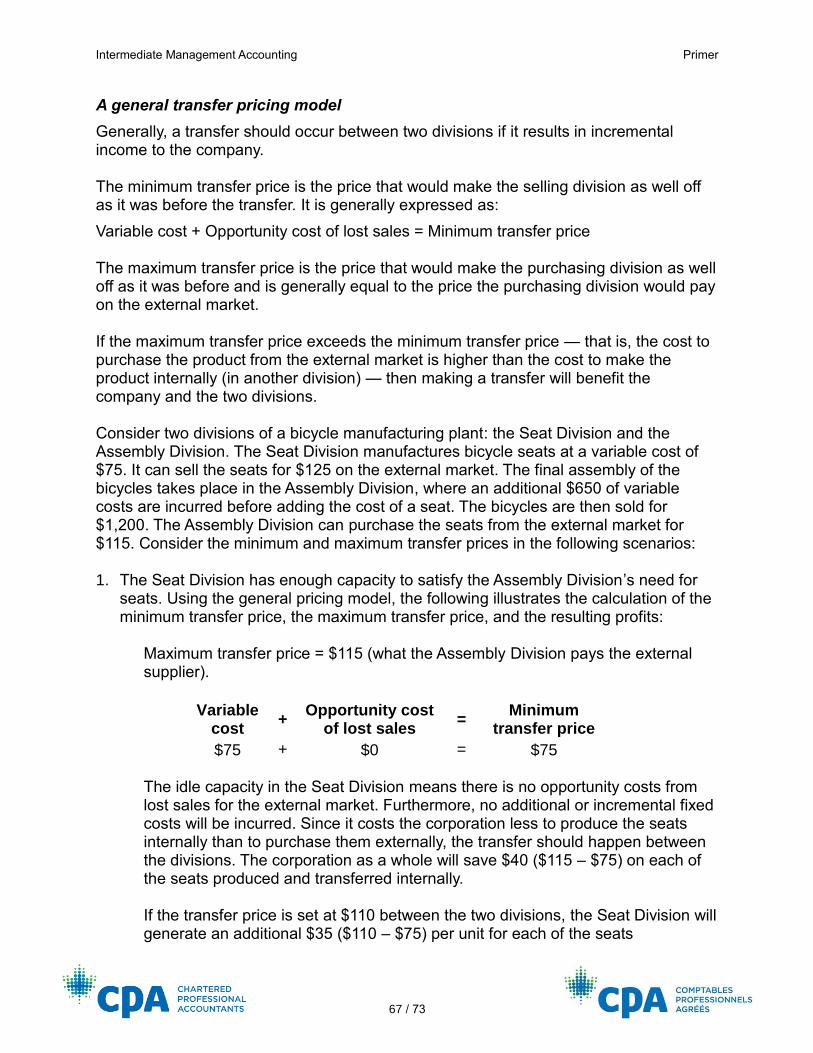

A general transfer pricing model ......................................................................... 67

Practice questions .................................................................................................. 68

Intermediate Management Accounting Primer

1 / 73

PRIMER

INTRODUCTION

Intermediate Management Accounting expands on the introductory course with an emphasis on costs for management decision-making. This will include exploring cost-volume-profit analysis, job costing, process costing and activity-based costing. In addition, Intermediate Management Accounting will touch on variable versus absorption costing, budgeting and pricing. Finally, it looks in detail at variance analysis then touches on uncertainty, linear programming and transfer pricing.

PART 1: ROLE OF THE MANAGEMENT ACCOUNTANT

One of the key roles of the management accountant is to support the decision-making process of the organization. This includes the following tasks:

• recording and evaluating costs

• developing information to support planning and control

• developing, implementing and operating performance measurement systems

Cost classifications

Management accounting has its own terminology that is used for more effective and concise communication. Knowledge of these terms is also essential in this course, as they are used throughout.

• Cost terms used in costing system design

o Product (or inventoriable) and period costs: A distinction is made between a cost incurred to produce a product (product cost) and all other operating costs (period costs).

o Cost object: A cost object is anything to which a cost can be traced, such as a product, a part of the organization (division or department), a project, a client, an event or even the entire organization.

o Direct and indirect costs: A direct cost is any cost that can be uniquely and unambiguously traced to a cost object in an economic and convenient way. All other costs are indirect.

• Cost terms used to describe and predict cost behaviour

o Fixed cost: A cost that does not change in total over the relevant range of activity.

Intermediate Management Accounting Primer

2 / 73

o Variable cost: A cost that increases in constant proportion with changes in activity level while the cost per unit stays the same within the relevant range of activity.

o Relevant range: The normal range of activity in which a company expects to operate. Management accounting decisions are made based on the cost behaviour within this range of activity.

• Cost terms used in manufacturing costing systems

o Prime and conversion costs: Prime costs generally consist of direct material and direct labour. Conversion costs generally consist of direct labour and manufacturing overhead.

• Cost terms used in planning and control

o Controllable versus non-controllable costs: The idea of controllable and uncontrollable costs relates to responsibility accounting where managers are responsible only for those costs they can control.

o Discretionary versus engineered costs: Engineered costs, such as materials, labour and equipment costs are driven by a cause-and-effect relationship (materials are driven by production, selling costs are driven by sales). Discretionary costs such as advertising and research and development are, instead, subject to periodic budget allocations.

• Cost terms used in decision-making

o Opportunity cost: The benefit forgone when a resource is used for one purpose instead of another or one course of action is taken over another.

o Sunk cost: A cost that has already been incurred and cannot be changed by any decision made now or in the future.

o Relevant cost: A relevant cost (or revenue) is a cost (or revenue) that differs among the alternatives being considered and that will be incurred in the future.

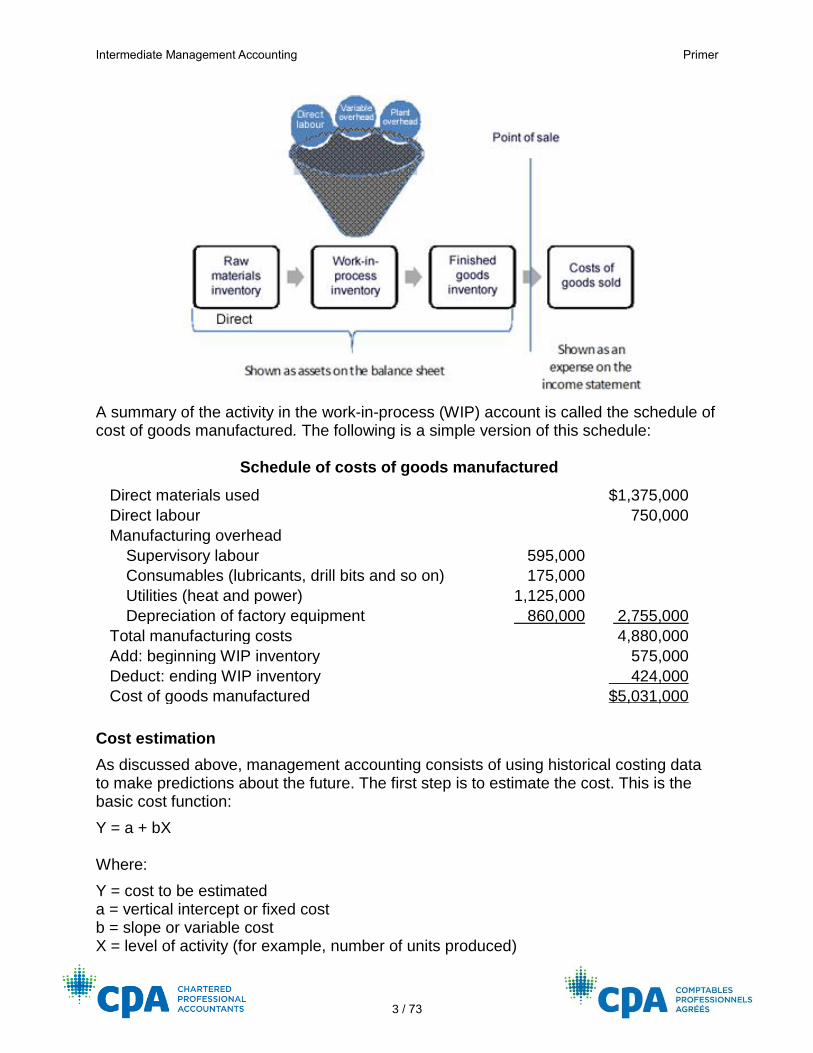

Cost flows used in manufacturing systems and the schedule of cost of goods manufactured

The following diagram illustrates the flows of costs through the various accounts used in a manufacturing system. Note the key accounts used to record these costs and the financial statements on which each account appears.

Intermediate Management Accounting Primer

3 / 73

A summary of the activity in the work-in-process (WIP) account is called the schedule of cost of goods manufactured. The following is a simple version of this schedule:

Schedule of costs of goods manufactured

Direct materials used $1,375,000

Direct labour 750,000

Manufacturing overhead

Supervisory labour 595,000

Consumables (lubricants, drill bits and so on) 175,000

Utilities (heat and power) 1,125,000

Depreciation of factory equipment 860,000 2,755,000

Total manufacturing costs 4,880,000

Add: beginning WIP inventory 575,000

Deduct: ending WIP inventory 424,000

Cost of goods manufactured $5,031,000

Cost estimation

As discussed above, management accounting consists of using historical costing data to make predictions about the future. The first step is to estimate the cost. This is the basic cost function:

Y = a + bX Where:

Y = cost to be estimated a = vertical intercept or fixed cost b = slope or variable cost X = level of activity (for example, number of units produced)

Intermediate Management Accounting Primer

4 / 73

There are a number of cost estimation methods including judgment and data approaches. Judgment approaches include engineering estimates, account analysis and the conference method, while data approaches include the high-low method, visual fit and statistical regression analysis. You may have covered many of these in your introductory course, so this primer will only touch on the statistical regression approach.

Statistical regression approach

The statistical regression approach fits an equation to the observed data using the criterion of minimizing the sum of the squared differences between the values predicted by the regression equation and the original data. The data is entered into a software package such as Microsoft Excel. The software then analyzes the data by applying regression analysis. The summary output provided by this tool consists of the following key regression statistics:

• The adjusted R-square (R2), which is a “best-fit” criterion also known as a goodness-of-fit measure (called the coefficient of determination). This measures the amount of variability in the dependent variable (Y) that is explained by changes in the independent variable (X).

• The estimated coefficients consisting of the intercept or fixed cost and the X variable or variable cost.

• The t-statistic, which is a formal statistical test of the hypothesis. For this course it can be assumed that, if the absolute value of the t-statistic is 2.00 or greater, a statistically significant relationship exists between the independent variable and the dependent variable.

There are several limitations of using historical costing data when making cost estimates. These limitations will be covered in the course.

Cost-volume-profit analysis

Managers use cost-volume-profit (CVP) analysis to assist in making decisions based on the relationship between costs and revenues and how changes in either affect the bottom line.

The CVP model

The basic CVP model is:

(Px) – (Vx) – F = OI

Intermediate Management Accounting Primer

5 / 73

Where:

P = selling price per unit V = variable cost per unit F = total fixed cost x = number of units produced and sold OI = operating income This equation allows the decision maker to answer a number of questions relating to profitability. One of these is the ability to identify the number of units (x) that must be made and sold to cover fixed costs (break-even point) and/or provide a target operating income. Contribution margin is the term used to identify how much revenue remains after deducting all variable costs. It is calculated as follows:

• Contribution margin (CM) per unit = P – V

• Contribution margin ratio = CM/P

Example Selling price: $4 per unit Variable costs: $2.50 per unit Fixed costs: $150,000 1. How many units must be sold to break even?

Using the CVP formula note that at break-even net income is $0. ($4x) – ($2.5x) – $150,000 = 0 Solve for x: $1.5x – $150,000 = 0 $1.5x = $150,000 x = $150,000 / $1.5 x = 100,000 units must be sold to break even. Break-even can also be calculated as follows: Break-even in units = F/CM = $150,000 / $1.5 = 100,000 units 2. How many units must be sold to earn a pre-tax operating income of

$100,000?

($4x) – ($2.5x) – $150,000 = $100,000

Intermediate Management Accounting Primer

6 / 73

Solve for x: $1.5x – $150,000 = $100,000 $1.5x = $250,000 x = $250,000 / $1.5x x = 166,667 units must be sold to earn a pre-tax operating income of $100,000. Achieving a target pre-tax operating income can also be calculated as follows: Units for target OI = (F + OI)/CM = ($150,000 + $100,000)/$1.5 = 166,667

Additionally, the break-even point or point to achieve desired income can be solved in dollars. Besides simply multiplying the break-even units by the selling price per unit, the CVP formula can be rewritten as follows:

Revenues to break even = F/CM ratio

For this example, CM ratio = 1.5/4 = 37.5%

$150,000 / 37.5% = $400,000 sales revenue is required to break even.

Revenues to achieved desired operating income = (F + OI)/CM ratio

For this example, ($150,000 +$100,000)/37.5% = $666,667 sales revenue is required to achieve the target operating income. Note that this is an estimate. If 166,667 units are required, then in dollars this would be 166,667 × $4 = $666,668. Also, note that you can’t sell part units so the number of units to break even must always be rounded up to the nearest whole number.

Taxes and the CVP equation

If taxes are to be considered, the CVP equation is expressed as follows: Units for target NI = {F + [NI / (1 – tax rate)]} / CM Operating income = NI / (1 – tax rate) Where after-tax net income = [(Px – Vx) – F] × (1 – tax rate)

Example Selling price: $4 per unit Variable costs: $2.50 per unit Fixed costs: $150,000 Tax rate: 30% How many units must be sold to earn an after-tax net income of $100,000? {F + [NI / (1 – tax rate)]} / CM {$150,000 + [$100,000 / (1 – 0.3)]} / $1.50 ($150,000 + $142,857.16)/$1.50 = 195,239 units (rounded up)

Intermediate Management Accounting Primer

7 / 73

Multi-product CVP analysis

CVP analysis can be used where a company produces and sells more than one product. In those situations, the units are combined in a bundle based on the projected sales mix. The contribution margin of the bundle is the denominator of the break-even equation while the numerator is the total fixed costs. As with calculating unit break-even point, bundle break-even is always rounded up to the nearest complete bundle. Once the break-even in sales mix bundles has been determined, the bundles are broken apart and each product in the mix is multiplied by the number of bundles.

Example Product A (200 units) Product B (100 units)

Per unit Total Per unit Total Firm total

Revenue $100 $20,000 $ 250 $ 25,000 $ 45,000

Variable cost 40 8,000 100 10,000 18,000

Contribution margin

$ 60 $12,000 $ 150 $ 15,000 $ 27,000

Fixed cost 21,600

Operating income $ 5,400

The sales mix based on the sales volume is: two units of Product A are sold for every unit of Product B. 200:100 = 2:1 The contribution margin using the sales mix is:

(2 × $60) + (1 × $150) = $270 per bundle of product

Then use the F/CM equation to arrive at the break-even bundles: $21,600 / $270 = 80 bundles. Each bundle consists of two units of Product A and one unit of Product B.

(2 × 80) = 160 units of Product A (1 × 80) = 80 units of Product B

Practice questions

1. Multiple-choice questions: i. The following selected data from April were taken from Elfin Inc.’s financial

statements:

Cost of goods available for sale $ 79,000 Manufacturing overhead 20,000 Cost of goods manufactured 69,000 Finished goods inventory — beginning 10,000 Direct materials used 16,000 Sales 130,000 Direct labour 23,000

Intermediate Management Accounting Primer

8 / 73

WIP inventory — beginning 15,000 Cost of goods sold 71,000

What was the WIP inventory at the end of April?

a) $5,000 b) $10,000 c) $15,000 d) $44,000

Solution Option a) is correct. Cost of goods manufactured is calculated as follows:

Direct materials used $16,000 Direct labour 23,000 Manufacturing overhead 20,000 Total manufacturing costs $59,000 Beginning WIP inventory 15,000 Less: ending WIP inventory 5,000* Cost of goods manufactured $69,000 *59,000 + 15,000 – 69,000 = 5,000 Option b) is incorrect. This is the difference between cost of goods manufactured and the sum of direct material used, direct labour and manufacturing overhead costs. Opening WIP inventory was not taken into account. Option c) is incorrect. This is beginning WIP. Option d) is incorrect. This is the sum of direct materials used, direct labour and manufacturing overhead less the beginning WIP inventory. Cost of goods manufactured was not taken into account.

ii. In which of the following lists of costs would all costs be classified as direct costs when manufacturing ice cream?

a) Supplies to clean the mixing tanks, wages of shift supervisor, cream b) Chocolate flavouring, plant utilities costs, powdered milk c) Plastic pails for the finished product, wages of the worker who runs the

assembly line, vanilla flavouring d) Equipment maintenance costs, janitorial costs, marshmallow sauce

Intermediate Management Accounting Primer

9 / 73

Solution Option c) is correct. Plastic pails and vanilla flavouring are direct ingredients and the wages of the worker who runs the assembly line is direct labour. Option a) is incorrect. Both the supplies to clean the mixing tanks and the wages of the shift supervisor are manufacturing overhead costs. Option b) is incorrect. The plant utilities costs are a manufacturing overhead cost. Option d) is incorrect. Both equipment maintenance and janitorial costs are manufacturing overhead costs.

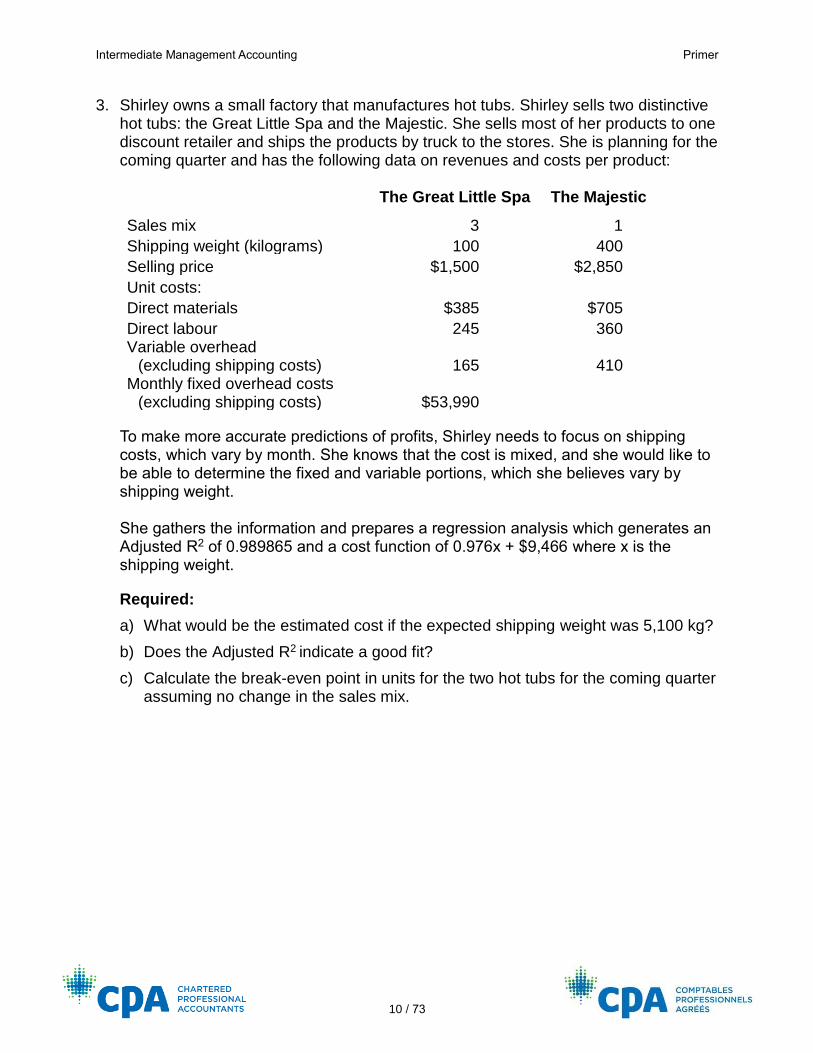

2. ALF Inc. is starting to manufacture metal desks. It has been determined that the market demand can be 7,000, 8,000 or 9,000 units. To start up, ALF obtained a $3 million term loan at 6%. Other information is as follows:

Selling price per desk $200 Variable cost per desk $50 Total fixed costs $1,000,000 (includes interest on the term loan)

Required:

a) What is ALF’s break-even point in units and in dollars?

b) There is a risk that ALF may have to take out an additional loan for $1,500,000 at the same rate as its current loan. If so, what is the minimum level of demand (7,000, 8,000 or 9,000 units) at which ALF must operate?

Solution

a) CPA Way step: Assess the Situation

Break-even in units = $1,000,000 ÷ ($200 – $50) = 6,667 units Break-even in sales dollars = $1,000,000 ÷ [($200 – $50) ÷ $200] = $1,333,333 Or 6,667 units × $200 = $1,333,400

b) CPA Way steps: Analyze Major Issue(s) and Conclude and Advise

An additional loan of $1,500,000 at 6% annual interest will require $1,500,000 × 0.06 = $90,000 in additional profits to pay the interest. ($1,000,000 + $90,000) / ($200 – $50) = 7,267 units Thus ALF must operate at a minimum level of 8,000 units to pay the loan interest.

Intermediate Management Accounting Primer

10 / 73

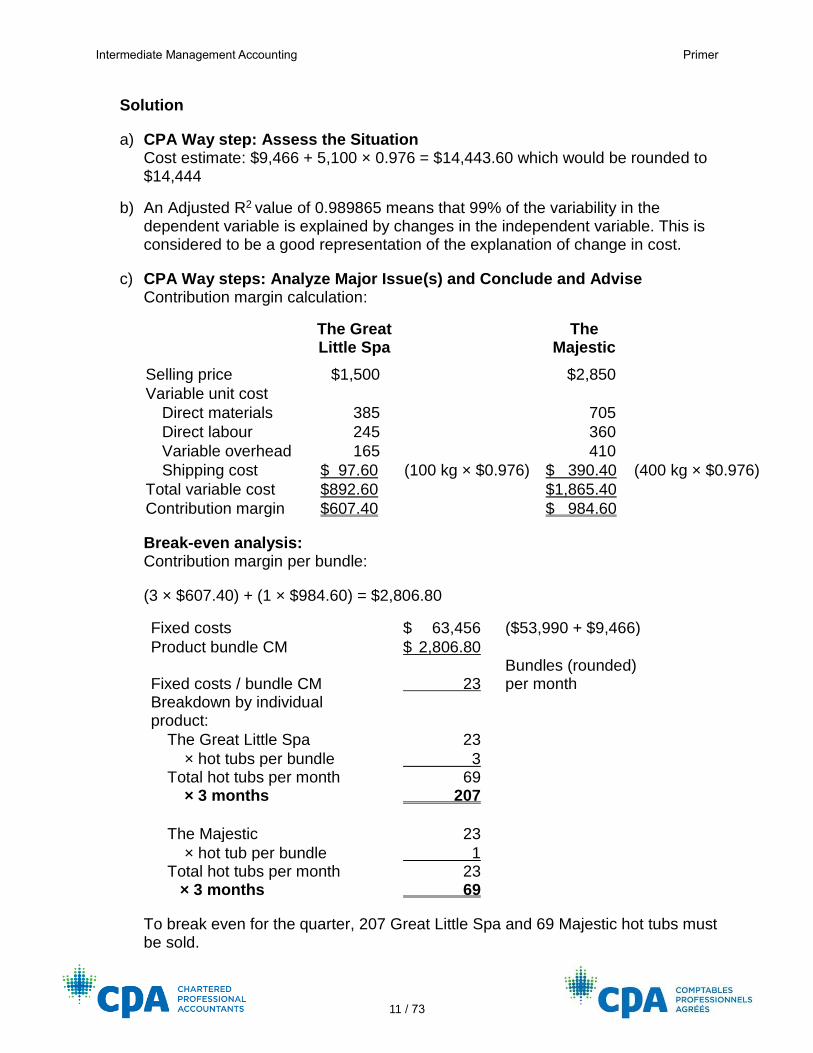

3. Shirley owns a small factory that manufactures hot tubs. Shirley sells two distinctive hot tubs: the Great Little Spa and the Majestic. She sells most of her products to one discount retailer and ships the products by truck to the stores. She is planning for the coming quarter and has the following data on revenues and costs per product:

The Great Little Spa The Majestic

Sales mix 3 1

Shipping weight (kilograms) 100 400

Selling price $1,500 $2,850

Unit costs: Direct materials $385 $705

Direct labour 245 360 Variable overhead

(excluding shipping costs) 165 410 Monthly fixed overhead costs

(excluding shipping costs) $53,990

To make more accurate predictions of profits, Shirley needs to focus on shipping costs, which vary by month. She knows that the cost is mixed, and she would like to be able to determine the fixed and variable portions, which she believes vary by shipping weight. She gathers the information and prepares a regression analysis which generates an Adjusted R2 of 0.989865 and a cost function of 0.976x + $9,466 where x is the shipping weight.

Required:

a) What would be the estimated cost if the expected shipping weight was 5,100 kg?

b) Does the Adjusted R2 indicate a good fit?

c) Calculate the break-even point in units for the two hot tubs for the coming quarter assuming no change in the sales mix.

Intermediate Management Accounting Primer

11 / 73

Solution

a) CPA Way step: Assess the Situation Cost estimate: $9,466 + 5,100 × 0.976 = $14,443.60 which would be rounded to $14,444

b) An Adjusted R2 value of 0.989865 means that 99% of the variability in the dependent variable is explained by changes in the independent variable. This is considered to be a good representation of the explanation of change in cost.

c) CPA Way steps: Analyze Major Issue(s) and Conclude and Advise Contribution margin calculation:

The Great Little Spa

The Majestic

Selling price $1,500 $2,850

Variable unit cost

Direct materials 385 705

Direct labour 245 360

Variable overhead 165 410

Shipping cost $ 97.60 (100 kg × $0.976) $ 390.40 (400 kg × $0.976)

Total variable cost $892.60 $1,865.40

Contribution margin $607.40 $ 984.60

Break-even analysis: Contribution margin per bundle:

(3 × $607.40) + (1 × $984.60) = $2,806.80

Fixed costs $ 63,456 ($53,990 + $9,466)

Product bundle CM $ 2,806.80

Fixed costs / bundle CM 23 Bundles (rounded) per month

Breakdown by individual product:

The Great Little Spa 23

× hot tubs per bundle 3 Total hot tubs per month

× 3 months 69 207

The Majestic 23

× hot tub per bundle 1 Total hot tubs per month

× 3 months 23 69

To break even for the quarter, 207 Great Little Spa and 69 Majestic hot tubs must be sold.

Intermediate Management Accounting Primer

12 / 73

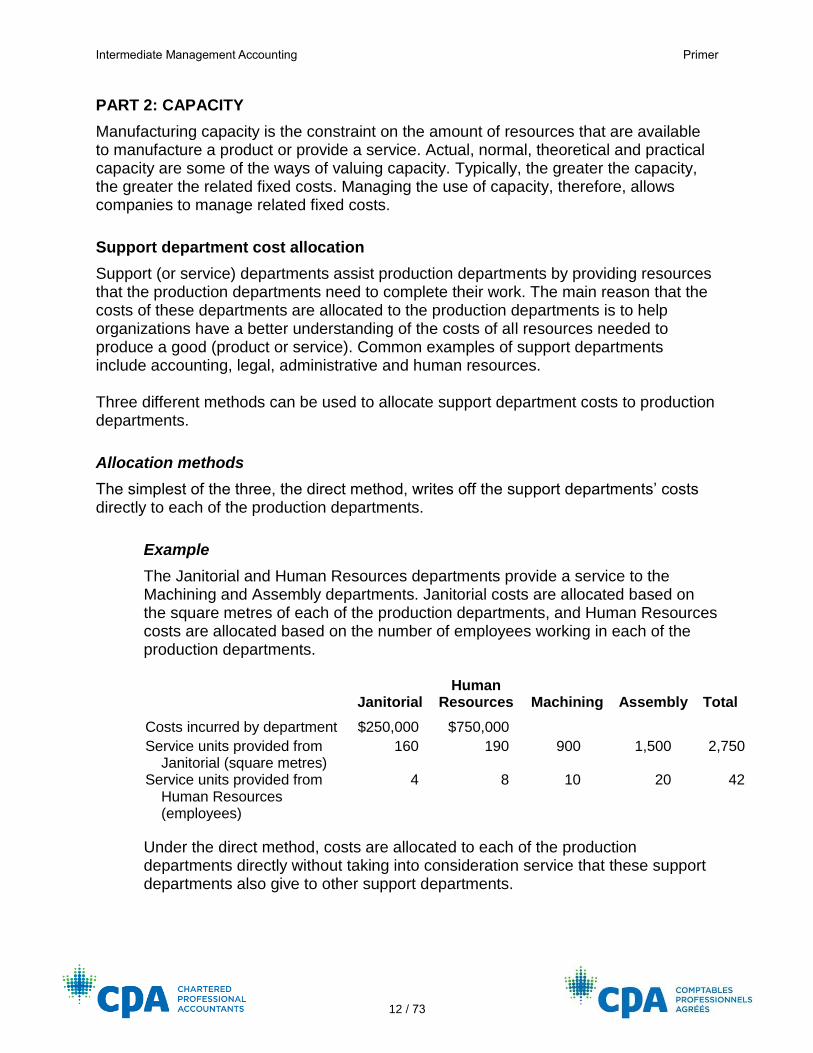

PART 2: CAPACITY

Manufacturing capacity is the constraint on the amount of resources that are available to manufacture a product or provide a service. Actual, normal, theoretical and practical capacity are some of the ways of valuing capacity. Typically, the greater the capacity, the greater the related fixed costs. Managing the use of capacity, therefore, allows companies to manage related fixed costs.

Support department cost allocation

Support (or service) departments assist production departments by providing resources that the production departments need to complete their work. The main reason that the costs of these departments are allocated to the production departments is to help organizations have a better understanding of the costs of all resources needed to produce a good (product or service). Common examples of support departments include accounting, legal, administrative and human resources. Three different methods can be used to allocate support department costs to production departments.

Allocation methods

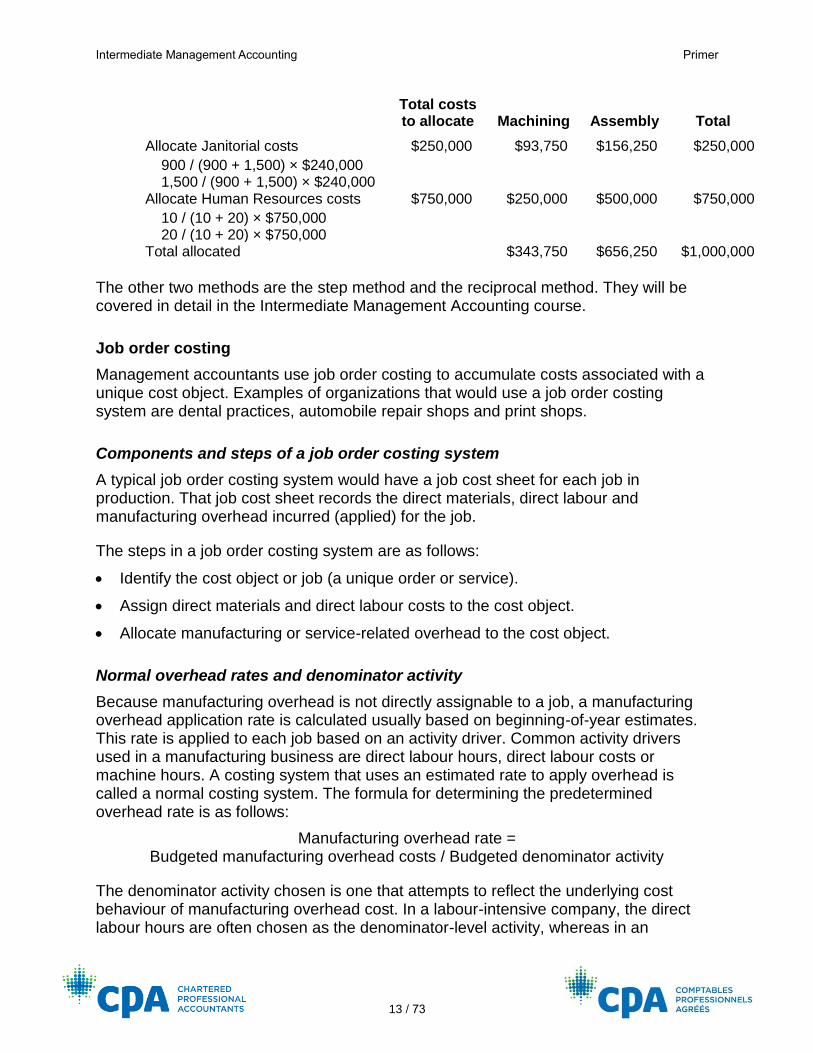

The simplest of the three, the direct method, writes off the support departments’ costs directly to each of the production departments.

Example

The Janitorial and Human Resources departments provide a service to the Machining and Assembly departments. Janitorial costs are allocated based on the square metres of each of the production departments, and Human Resources costs are allocated based on the number of employees working in each of the production departments.

Janitorial Human

Resources Machining Assembly Total

Costs incurred by department $250,000 $750,000

Service units provided from Janitorial (square metres)

160 190 900 1,500 2,750

Service units provided from Human Resources (employees)

4 8 10 20 42

Under the direct method, costs are allocated to each of the production departments directly without taking into consideration service that these support departments also give to other support departments.

Intermediate Management Accounting Primer

13 / 73

Total costs to allocate Machining Assembly Total

Allocate Janitorial costs $250,000 $93,750 $156,250 $250,000

900 / (900 + 1,500) × $240,000 1,500 / (900 + 1,500) × $240,000

Allocate Human Resources costs $750,000 $250,000 $500,000 $750,000

10 / (10 + 20) × $750,000 20 / (10 + 20) × $750,000

Total allocated

$343,750 $656,250 $1,000,000

The other two methods are the step method and the reciprocal method. They will be covered in detail in the Intermediate Management Accounting course.

Job order costing

Management accountants use job order costing to accumulate costs associated with a unique cost object. Examples of organizations that would use a job order costing system are dental practices, automobile repair shops and print shops.

Components and steps of a job order costing system

A typical job order costing system would have a job cost sheet for each job in production. That job cost sheet records the direct materials, direct labour and manufacturing overhead incurred (applied) for the job.

The steps in a job order costing system are as follows:

• Identify the cost object or job (a unique order or service).

• Assign direct materials and direct labour costs to the cost object.

• Allocate manufacturing or service-related overhead to the cost object.

Normal overhead rates and denominator activity

Because manufacturing overhead is not directly assignable to a job, a manufacturing overhead application rate is calculated usually based on beginning-of-year estimates. This rate is applied to each job based on an activity driver. Common activity drivers used in a manufacturing business are direct labour hours, direct labour costs or machine hours. A costing system that uses an estimated rate to apply overhead is called a normal costing system. The formula for determining the predetermined overhead rate is as follows:

Manufacturing overhead rate = Budgeted manufacturing overhead costs / Budgeted denominator activity

The denominator activity chosen is one that attempts to reflect the underlying cost behaviour of manufacturing overhead cost. In a labour-intensive company, the direct labour hours are often chosen as the denominator-level activity, whereas in an

Intermediate Management Accounting Primer

14 / 73

automated company, machine hours are usually chosen. Common choices for activity level are historic actual, estimated, average, and practical capacity of the cost driver.

The amount of manufacturing overhead applied to a job will equal the manufacturing overhead rate multiplied by the actual denominator activity specific to the job.

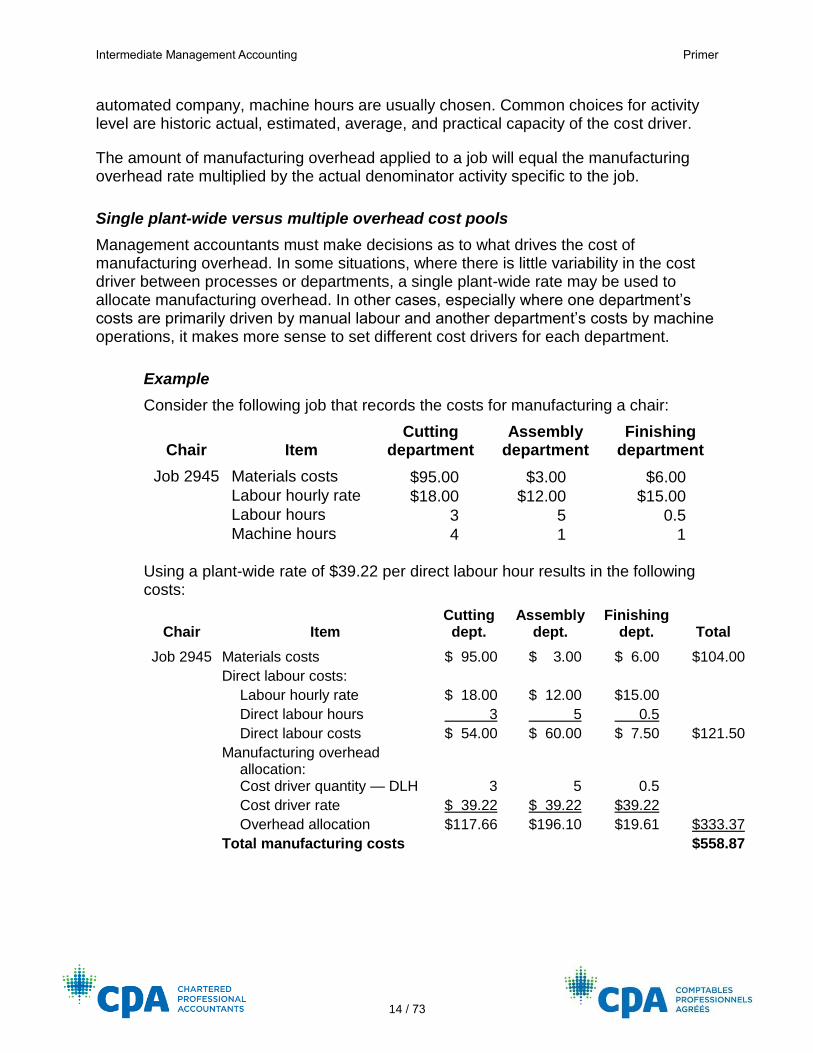

Single plant-wide versus multiple overhead cost pools

Management accountants must make decisions as to what drives the cost of manufacturing overhead. In some situations, where there is little variability in the cost driver between processes or departments, a single plant-wide rate may be used to allocate manufacturing overhead. In other cases, especially where one department’s costs are primarily driven by manual labour and another department’s costs by machine operations, it makes more sense to set different cost drivers for each department.

Example

Consider the following job that records the costs for manufacturing a chair:

Chair Item Cutting

department Assembly

department Finishing

department

Job 2945 Materials costs $95.00 $3.00 $6.00 Labour hourly rate $18.00 $12.00 $15.00 Labour hours 3 5 0.5 Machine hours 4 1 1

Using a plant-wide rate of $39.22 per direct labour hour results in the following costs:

Chair Item Cutting dept.

Assembly dept.

Finishing dept. Total

Job 2945 Materials costs $ 95.00 $ 3.00 $ 6.00 $104.00

Direct labour costs: Labour hourly rate $ 18.00 $ 12.00 $15.00

Direct labour hours 3 5 0.5

Direct labour costs $ 54.00 $ 60.00 $ 7.50 $121.50

Manufacturing overhead allocation:

Cost driver quantity — DLH 3 5 0.5

Cost driver rate $ 39.22 $ 39.22 $39.22

Overhead allocation $117.66 $196.10 $19.61 $333.37 Total manufacturing costs $558.87

Intermediate Management Accounting Primer

15 / 73

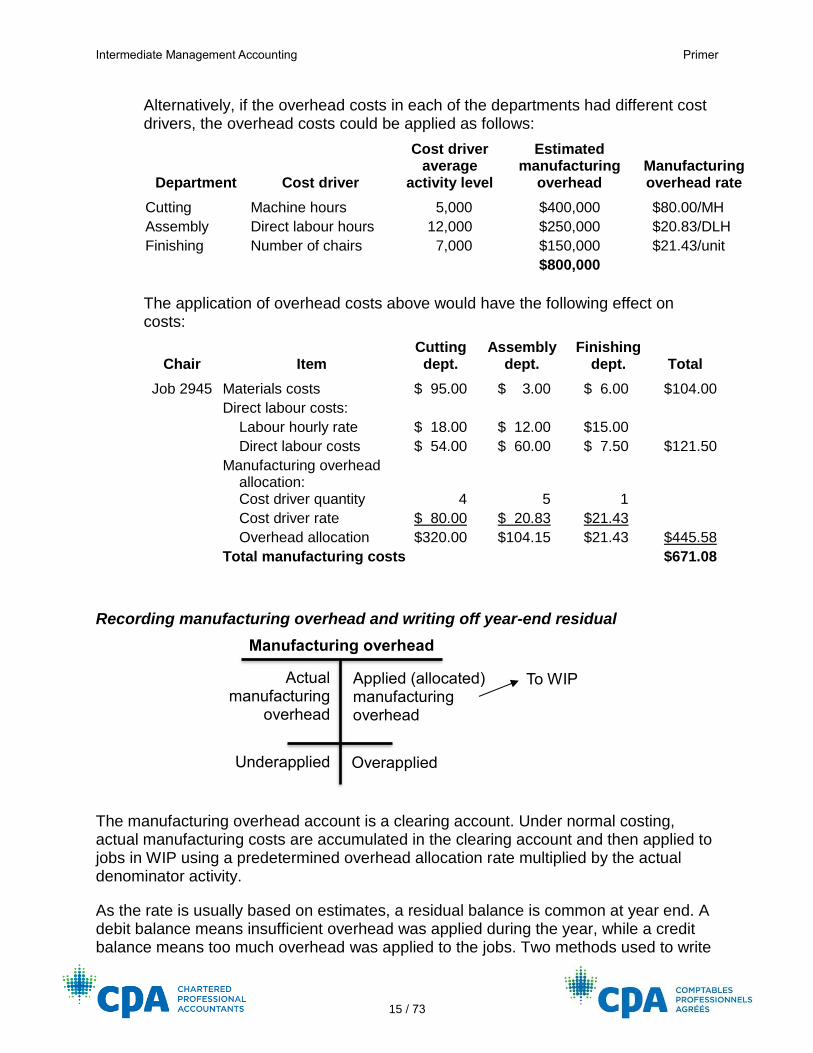

Alternatively, if the overhead costs in each of the departments had different cost drivers, the overhead costs could be applied as follows:

Department Cost driver

Cost driver average

activity level

Estimated manufacturing

overhead Manufacturing overhead rate

Cutting Machine hours 5,000 $400,000 $80.00/MH

Assembly Direct labour hours 12,000 $250,000 $20.83/DLH

Finishing Number of chairs 7,000 $150,000 $21.43/unit $800,000

The application of overhead costs above would have the following effect on costs:

Chair Item Cutting dept.

Assembly dept.

Finishing dept. Total

Job 2945 Materials costs $ 95.00 $ 3.00 $ 6.00 $104.00 Direct labour costs:

Labour hourly rate $ 18.00 $ 12.00 $15.00

Direct labour costs $ 54.00 $ 60.00 $ 7.50 $121.50

Manufacturing overhead allocation:

Cost driver quantity 4 5 1

Cost driver rate $ 80.00 $ 20.83 $21.43

Overhead allocation $320.00 $104.15 $21.43 $445.58

Total manufacturing costs $671.08

Recording manufacturing overhead and writing off year-end residual

The manufacturing overhead account is a clearing account. Under normal costing, actual manufacturing costs are accumulated in the clearing account and then applied to jobs in WIP using a predetermined overhead allocation rate multiplied by the actual denominator activity.

As the rate is usually based on estimates, a residual balance is common at year end. A debit balance means insufficient overhead was applied during the year, while a credit balance means too much overhead was applied to the jobs. Two methods used to write

Actual manufacturing

overhead

Manufacturing overhead

Underapplied

Applied (allocated) manufacturing overhead

Overapplied

To WIP

Intermediate Management Accounting Primer

16 / 73

off this amount are the direct charge to cost of goods sold method and the prorating based on ending balances method.

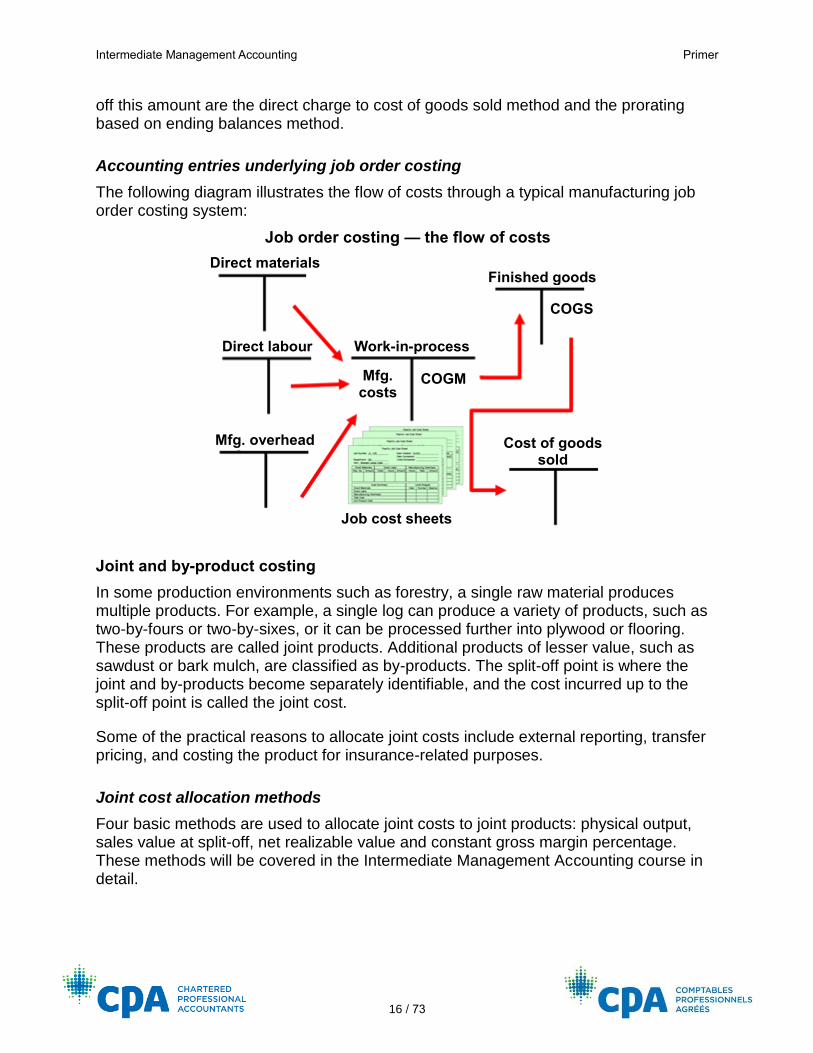

Accounting entries underlying job order costing

The following diagram illustrates the flow of costs through a typical manufacturing job order costing system:

Joint and by-product costing

In some production environments such as forestry, a single raw material produces multiple products. For example, a single log can produce a variety of products, such as two-by-fours or two-by-sixes, or it can be processed further into plywood or flooring. These products are called joint products. Additional products of lesser value, such as sawdust or bark mulch, are classified as by-products. The split-off point is where the joint and by-products become separately identifiable, and the cost incurred up to the split-off point is called the joint cost.

Some of the practical reasons to allocate joint costs include external reporting, transfer pricing, and costing the product for insurance-related purposes.

Joint cost allocation methods

Four basic methods are used to allocate joint costs to joint products: physical output, sales value at split-off, net realizable value and constant gross margin percentage. These methods will be covered in the Intermediate Management Accounting course in detail.

Direct materials

Job order costing — the flow of costs

Finished goods

Direct labour Work-in-process

Mfg. costs

Mfg. overhead

Job cost sheets

Cost of goods sold

COGM

COGS

Intermediate Management Accounting Primer

17 / 73

Practice questions

1. Multiple-choice questions:

i. When are departmental overhead rates generally preferred to plant-wide overhead rates?

a) When activities of each of the various departments in the plant are not homogenous

b) When all products passing through various departments require the same manufacturing effort in each department

c) When most of the overhead costs are fixed d) When all products passing through the various departments require a

different amount of direct materials in each department

Solution

Option a) is correct. A unique rate should be established for each department to better reflect the level of activity and consumption when activities across departments are different.

Option b) is incorrect. If the same effort is required throughout, then a plant-wide rate would be preferred.

Option c) is incorrect. If the overhead costs are fixed, they will not vary based on the different drivers used by departmental overhead rates.

Option d) is incorrect. The amount of direct materials is unlikely to be a driver of the overhead cost allocation, so it is irrelevant in deciding between departmental and plant-wide rates.

ii. The following is an excerpt from DellCo’s accounting information system:

Indirect factory materials $ 48,000

Direct manufacturing materials 114,000

Indirect office wages 14,000

Manufacturing overhead applied 182,000

Factory depreciation 86,000

Office depreciation 14,000

Direct office wages 32,000

Factory supervisors’ salaries 36,000

Factory supplies 7,000

Intermediate Management Accounting Primer

18 / 73

Based on the information above, what value will be debited to the WIP account regarding manufacturing overhead?

a) $177,000 b) $182,000 c) $191,000 d) $205,000

Solution

Option b) is correct. Manufacturing overhead is applied to WIP by crediting the manufacturing overhead account and debiting WIP.

Option a) is incorrect. This is the total of indirect factory materials, factory depreciation, factory supervisors’ salaries and factory supplies costs, not the amount applied. The manufacturing overhead is applied using a predetermined rate.

Option c) is incorrect. This is the total of indirect factory materials, indirect office wages, factory depreciation, factory supervisors’ salaries and factory supplies costs, not the amount applied. In addition, indirect office wages would not be part of the manufacturing overhead.

Option d) is incorrect. This is the total of indirect factory materials, indirect office wages, factory depreciation, office depreciation, factory supervisors’ salaries and factory supplies costs, not the amount applied. In addition, indirect office wages and office depreciation would not be part of the manufacturing overhead.

Intermediate Management Accounting Primer

19 / 73

2. Renaissance Wood Products Ltd. manufactures wooden knife blocks. The marketing manager wants to set the selling price of these blocks. There are two distinct designs. The simpler design is the curve block, which holds four knives. The more complicated design is the square block, which holds eight knives. The production manager has just completed a production run of 350 of the curve blocks. The following data pertain to this run of curve blocks:

Opening inventory, direct materials $500

Purchases of direct materials $1,000

Ending inventory, direct materials $625

Direct labour to make the blocks was 52.50 hours at $25/hour

Budgeted indirect costs for the year (for all jobs)

Supplies such as glue and stain $ 840

Hydro 1,230

Machine maintenance 1,250

Machine depreciation 3,000

Indirect labour 16,630

Total budgeted indirect costs $22,950

Machine hours is the cost driver for the indirect costs. The budgeted machine hours for the year are based on the production of 4,200 curve blocks at 0.30 hours each and 3,600 square blocks at 0.50 hours each. The machine hours used to produce the 350 curve blocks are the same as the budgeted level.

Renaissance’s pricing policy is to mark up its products by 50% of product cost.

Required:

a) CPA Way step: Assess the Situation

i) Calculate the total cost for 350 curve blocks.

ii) Calculate a unit cost per block.

b) CPA Way steps: Analyze Major Issue(s) and Conclude and Advise Advise management on the appropriate selling price for the curve block product.

Intermediate Management Accounting Primer

20 / 73

Solution

a) i) Direct materials $ 875.00 ($500.00 + $1,000.00 – $625.00) Direct labour 1,312.50 (52.50 × $25.00) Manufacturing overhead 787.501 Total cost $2,975.00

1 To calculate the manufacturing overhead, the first step is to determine the predetermined rate by dividing the total budgeted indirect costs by the total machine hours for the year.

Total machine hours = 4,200 × 0.30 = 1,260 hours = 3,600 × 0.50 = 1,800 hours Total 3,060 hours $22,950 ÷ 3,060 = $7.50 per hour

Next, determine how many machine hours were used to manufacture the 350 curve blocks:

350 × 0.30 = 105 hours

The overhead applied to the production of curve blocks was 105 hours × $7.50/hour = $787.50.

ii) Unit cost for each curve block = $2,975/350 = $8.50

b) Based on Renaissance’s pricing policy, the selling price of each curve block should be $8.50 × 1.5 = $12.75.

Intermediate Management Accounting Primer

21 / 73

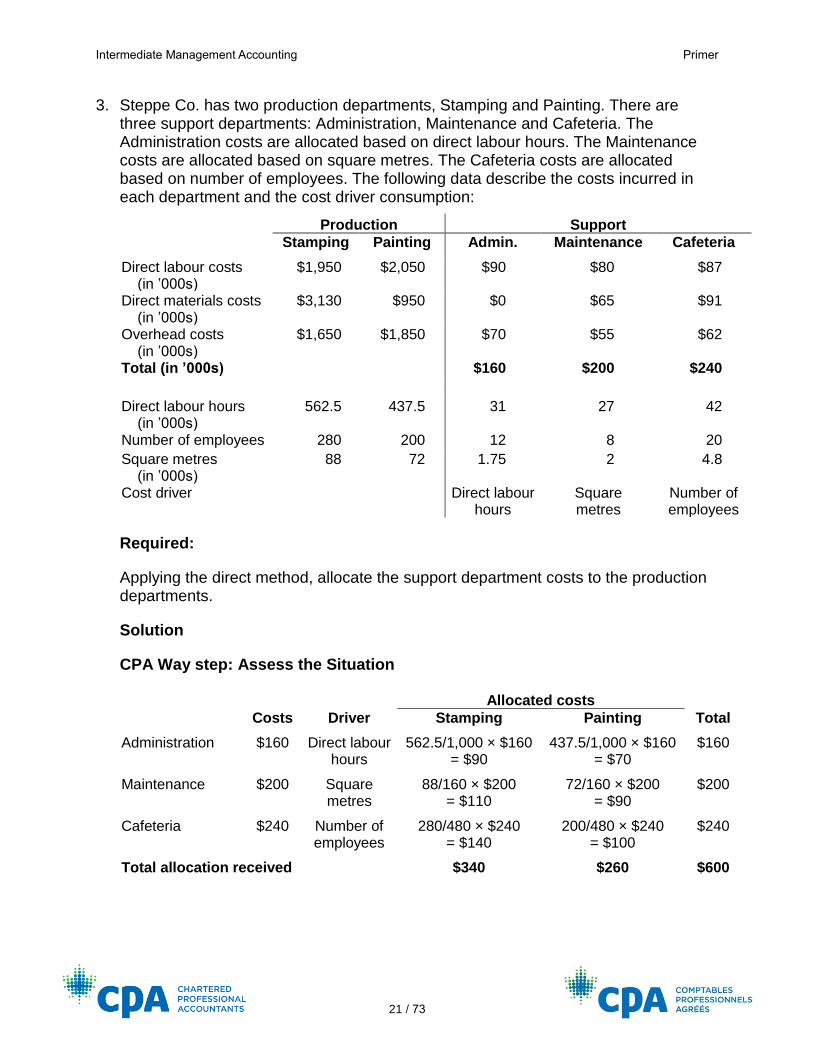

3. Steppe Co. has two production departments, Stamping and Painting. There are three support departments: Administration, Maintenance and Cafeteria. The Administration costs are allocated based on direct labour hours. The Maintenance costs are allocated based on square metres. The Cafeteria costs are allocated based on number of employees. The following data describe the costs incurred in each department and the cost driver consumption:

Production Support

Stamping Painting Admin. Maintenance Cafeteria

Direct labour costs (in ’000s)

$1,950 $2,050 $90 $80 $87

Direct materials costs (in ’000s)

$3,130 $950 $0 $65 $91

Overhead costs (in ’000s)

$1,650 $1,850 $70 $55 $62

Total (in ’000s) $160 $200 $240

Direct labour hours (in ’000s)

562.5 437.5 31 27 42

Number of employees 280 200 12 8 20

Square metres (in ’000s)

88 72 1.75 2 4.8

Cost driver Direct labour hours

Square metres

Number of employees

Required:

Applying the direct method, allocate the support department costs to the production departments.

Solution

CPA Way step: Assess the Situation

Allocated costs

Costs Driver Stamping Painting Total

Administration $160 Direct labour hours

562.5/1,000 × $160 = $90

437.5/1,000 × $160 = $70

$160

Maintenance $200 Square metres

88/160 × $200 = $110

72/160 × $200 = $90

$200

Cafeteria $240 Number of employees

280/480 × $240 = $140

200/480 × $240 = $100

$240

Total allocation received $340 $260 $600

Intermediate Management Accounting Primer

22 / 73

PART 3: PROCESS COSTING

Process costing is a costing system suitable for costing the mass production of identical products (for example, packaging soft drinks and manufacturing plastic bottles). Instead of costing individual units or jobs as is done in job costing, total costs are simply divided by the number of units produced to compute the cost per unit. The purpose of job and process costing is to cost products and services. However, some of the differences are as follows:

Job order costing Process costing

Products Each product is unique. Each product is the same as all others.

Cost accumulation Costs are collected and recorded for each job.

Costs are collected and recorded by department/process.

Reporting of costs Costs are accumulated and reported on the job cost sheet.

Costs are reported on the department production report.

Unit costs Unit costs are calculated for each job.

Unit costs are calculated for each department.

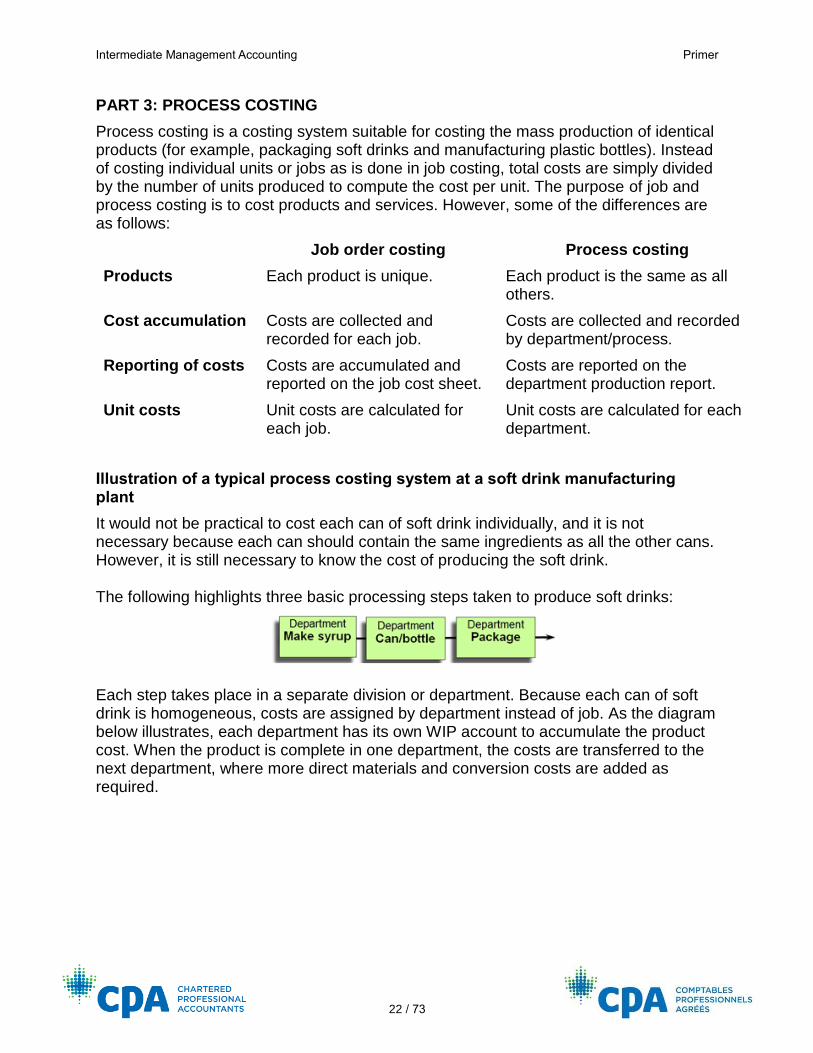

Illustration of a typical process costing system at a soft drink manufacturing plant

It would not be practical to cost each can of soft drink individually, and it is not necessary because each can should contain the same ingredients as all the other cans. However, it is still necessary to know the cost of producing the soft drink. The following highlights three basic processing steps taken to produce soft drinks:

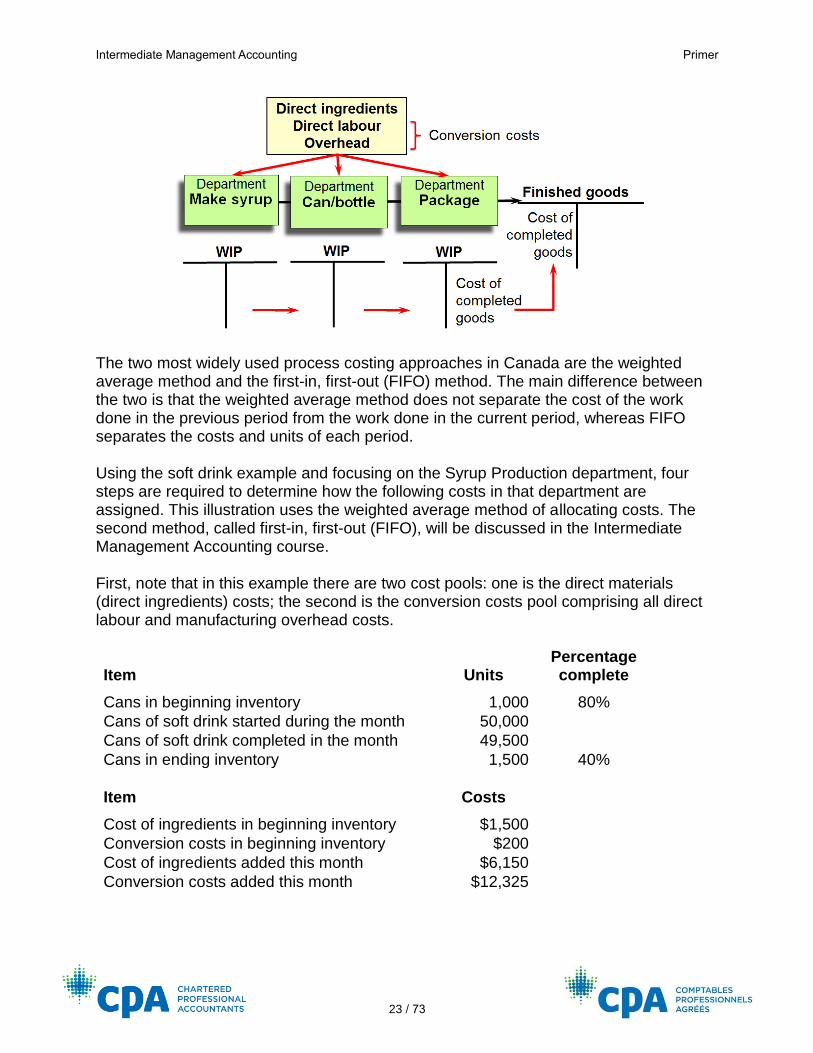

Each step takes place in a separate division or department. Because each can of soft drink is homogeneous, costs are assigned by department instead of job. As the diagram below illustrates, each department has its own WIP account to accumulate the product cost. When the product is complete in one department, the costs are transferred to the next department, where more direct materials and conversion costs are added as required.

Intermediate Management Accounting Primer

23 / 73

The two most widely used process costing approaches in Canada are the weighted average method and the first-in, first-out (FIFO) method. The main difference between the two is that the weighted average method does not separate the cost of the work done in the previous period from the work done in the current period, whereas FIFO separates the costs and units of each period. Using the soft drink example and focusing on the Syrup Production department, four steps are required to determine how the following costs in that department are assigned. This illustration uses the weighted average method of allocating costs. The second method, called first-in, first-out (FIFO), will be discussed in the Intermediate Management Accounting course. First, note that in this example there are two cost pools: one is the direct materials (direct ingredients) costs; the second is the conversion costs pool comprising all direct labour and manufacturing overhead costs.

Item Units Percentage complete

Cans in beginning inventory 1,000 80%

Cans of soft drink started during the month 50,000 Cans of soft drink completed in the month 49,500 Cans in ending inventory 1,500 40%

Item Costs

Cost of ingredients in beginning inventory $1,500 Conversion costs in beginning inventory $200 Cost of ingredients added this month $6,150 Conversion costs added this month $12,325

Intermediate Management Accounting Primer

24 / 73

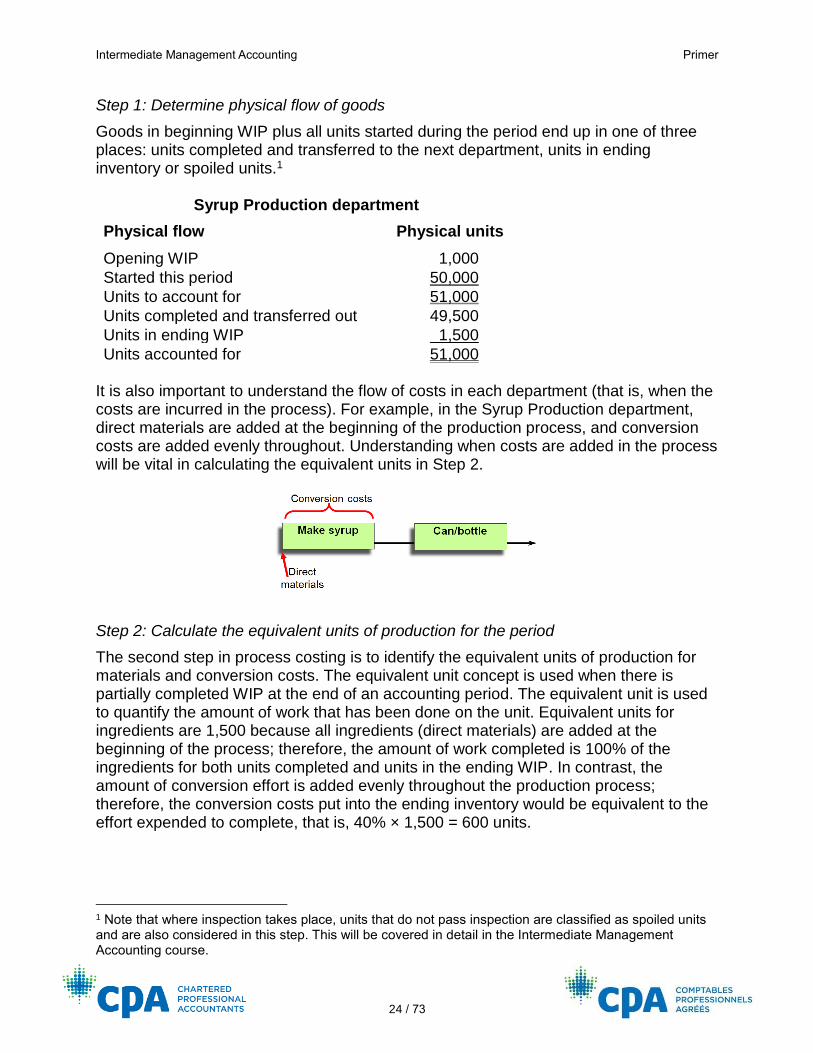

Step 1: Determine physical flow of goods

Goods in beginning WIP plus all units started during the period end up in one of three places: units completed and transferred to the next department, units in ending inventory or spoiled units.1

Syrup Production department

Physical flow Physical units

Opening WIP 1,000

Started this period 50,000

Units to account for 51,000

Units completed and transferred out 49,500

Units in ending WIP 1,500

Units accounted for 51,000 It is also important to understand the flow of costs in each department (that is, when the costs are incurred in the process). For example, in the Syrup Production department, direct materials are added at the beginning of the production process, and conversion costs are added evenly throughout. Understanding when costs are added in the process will be vital in calculating the equivalent units in Step 2.

Step 2: Calculate the equivalent units of production for the period

The second step in process costing is to identify the equivalent units of production for materials and conversion costs. The equivalent unit concept is used when there is partially completed WIP at the end of an accounting period. The equivalent unit is used to quantify the amount of work that has been done on the unit. Equivalent units for ingredients are 1,500 because all ingredients (direct materials) are added at the beginning of the process; therefore, the amount of work completed is 100% of the ingredients for both units completed and units in the ending WIP. In contrast, the amount of conversion effort is added evenly throughout the production process; therefore, the conversion costs put into the ending inventory would be equivalent to the effort expended to complete, that is, 40% × 1,500 = 600 units.

1 Note that where inspection takes place, units that do not pass inspection are classified as spoiled units and are also considered in this step. This will be covered in detail in the Intermediate Management Accounting course.

Intermediate Management Accounting Primer

25 / 73

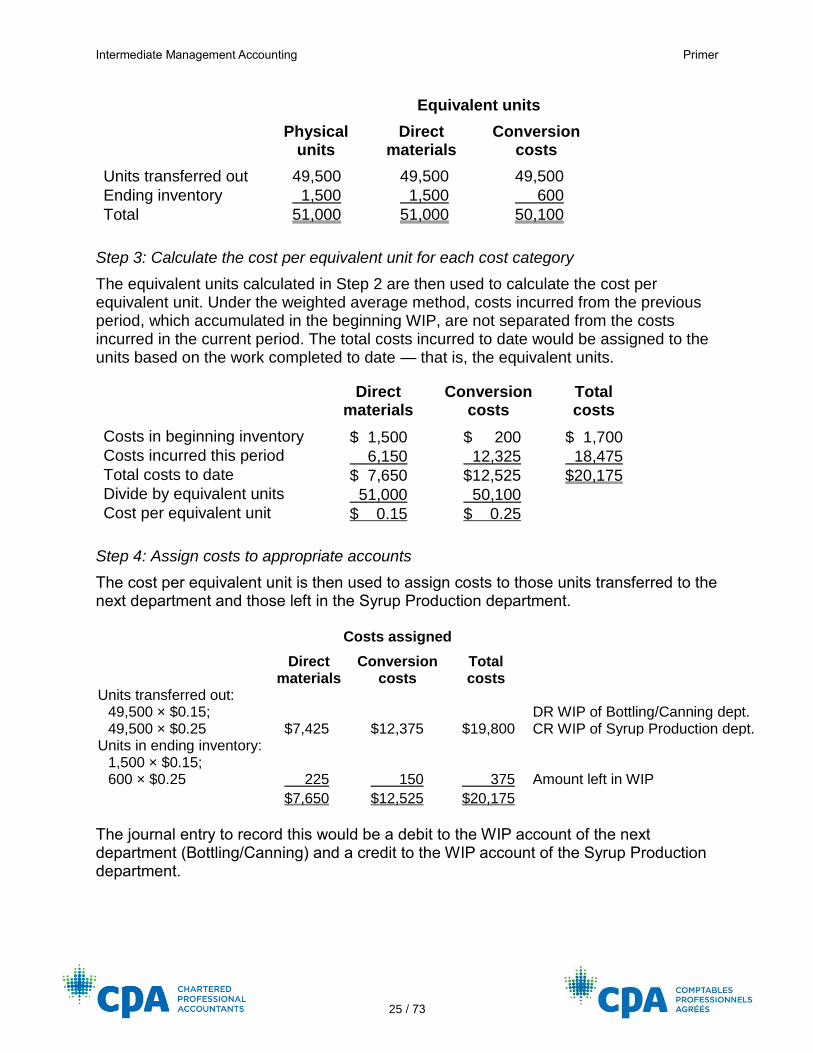

Physical units

Equivalent units

Direct materials

Conversion costs

Units transferred out 49,500 49,500 49,500

Ending inventory 1,500 1,500 600

Total 51,000 51,000 50,100

Step 3: Calculate the cost per equivalent unit for each cost category

The equivalent units calculated in Step 2 are then used to calculate the cost per equivalent unit. Under the weighted average method, costs incurred from the previous period, which accumulated in the beginning WIP, are not separated from the costs incurred in the current period. The total costs incurred to date would be assigned to the units based on the work completed to date — that is, the equivalent units.

Direct materials

Conversion costs

Total costs

Costs in beginning inventory $ 1,500 $ 200 $ 1,700 Costs incurred this period 6,150 12,325 18,475 Total costs to date $ 7,650 $12,525 $20,175 Divide by equivalent units 51,000 50,100 Cost per equivalent unit $ 0.15 $ 0.25

Step 4: Assign costs to appropriate accounts

The cost per equivalent unit is then used to assign costs to those units transferred to the next department and those left in the Syrup Production department.

Costs assigned

Direct materials

Conversion costs

Total costs

Units transferred out: 49,500 × $0.15; 49,500 × $0.25 $7,425 $12,375 $19,800

DR WIP of Bottling/Canning dept. CR WIP of Syrup Production dept.

Units in ending inventory: 1,500 × $0.15; 600 × $0.25 225 150 375 Amount left in WIP

$7,650 $12,525 $20,175 The journal entry to record this would be a debit to the WIP account of the next department (Bottling/Canning) and a credit to the WIP account of the Syrup Production department.

Intermediate Management Accounting Primer

26 / 73

Spoilage

Spoilage is identified at a point of inspection and can be classified as either abnormal or normal. Abnormal spoilage is spoiled units above the number that is expected or normal for the process. Normal spoilage contributes to the cost of the good units produced, whereas abnormal spoilage is reported as a period cost in the period incurred. The cost of spoiled units is based on the percentage of completion at the point where the units were inspected.

Transferred-in costs

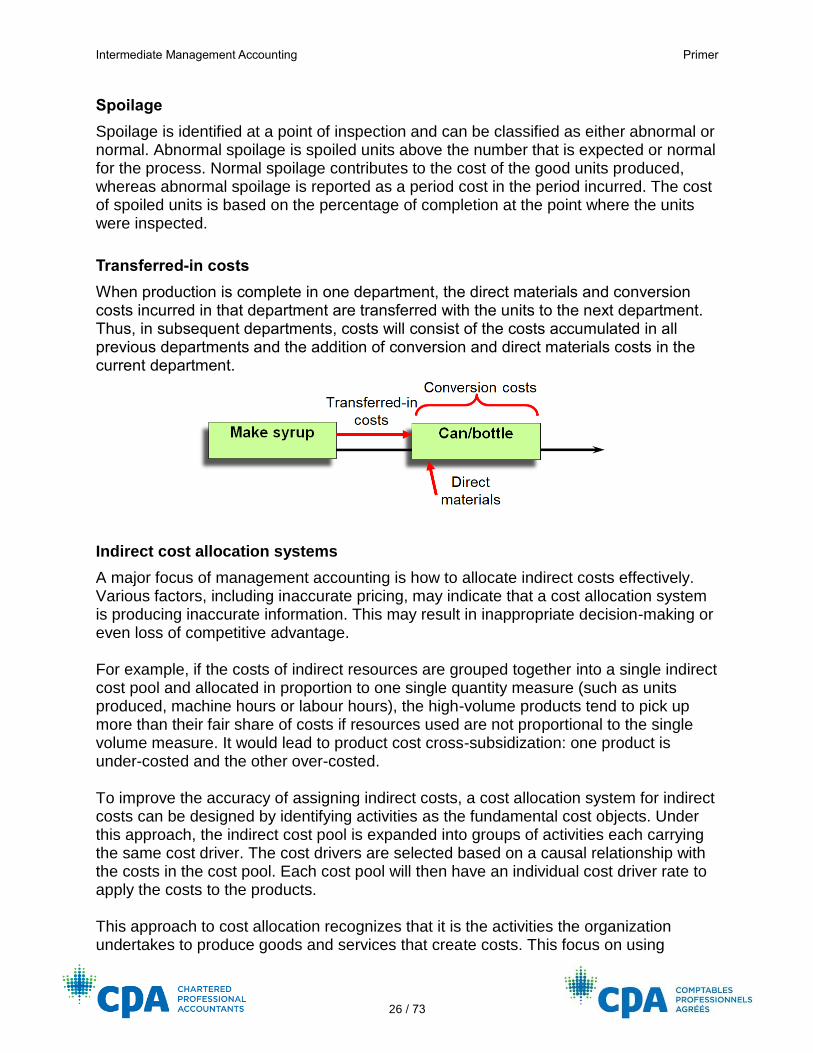

When production is complete in one department, the direct materials and conversion costs incurred in that department are transferred with the units to the next department. Thus, in subsequent departments, costs will consist of the costs accumulated in all previous departments and the addition of conversion and direct materials costs in the current department.

Indirect cost allocation systems

A major focus of management accounting is how to allocate indirect costs effectively. Various factors, including inaccurate pricing, may indicate that a cost allocation system is producing inaccurate information. This may result in inappropriate decision-making or even loss of competitive advantage. For example, if the costs of indirect resources are grouped together into a single indirect cost pool and allocated in proportion to one single quantity measure (such as units produced, machine hours or labour hours), the high-volume products tend to pick up more than their fair share of costs if resources used are not proportional to the single volume measure. It would lead to product cost cross-subsidization: one product is under-costed and the other over-costed. To improve the accuracy of assigning indirect costs, a cost allocation system for indirect costs can be designed by identifying activities as the fundamental cost objects. Under this approach, the indirect cost pool is expanded into groups of activities each carrying the same cost driver. The cost drivers are selected based on a causal relationship with the costs in the cost pool. Each cost pool will then have an individual cost driver rate to apply the costs to the products. This approach to cost allocation recognizes that it is the activities the organization undertakes to produce goods and services that create costs. This focus on using

Intermediate Management Accounting Primer

27 / 73

activities as the cost driver for indirect costs is called activity-based costing (ABC). Under a carefully constructed ABC system, the actual use of the resources will be reflected, thus improving the accuracy of cost allocation.

ABC systems

In ABC, an activity is any event that causes overhead costs to be incurred. The costs of performing these activities are accumulated in an activity cost pool. There must be a cause-and-effect relationship between the activity measures and the costs of the activities. Any of the cost estimation methods discussed in Part 1 can be used to establish and measure the relationship between the costs of an activity and the activity measure.

The ABC cost hierarchy

Activity-based costs can be classified into one of the following ABC cost hierarchy elements:

• Unit-level costs vary directly with the level of production. They are often called variable costs.

• Batch-level costs are incurred whenever a batch or group of units is processed, regardless of the number of units. An example is setting up machines for a production run.

• Product-sustaining costs are incurred without regard to the number of batches or units produced. Examples include costs of developing and advertising a product line.

• Customer-sustaining costs are incurred to provide a service to specific customers. Examples include the cost of sales representative visits to a customer or of sending out catalogues.

• Facility-sustaining costs benefit all business functions. They are incurred to enable an organization to continue, regardless of customers, products, batches or units. An example is head office administrative costs. These costs are not usually allocated, because there is no apparent cause-and-effect relationship with activity levels.

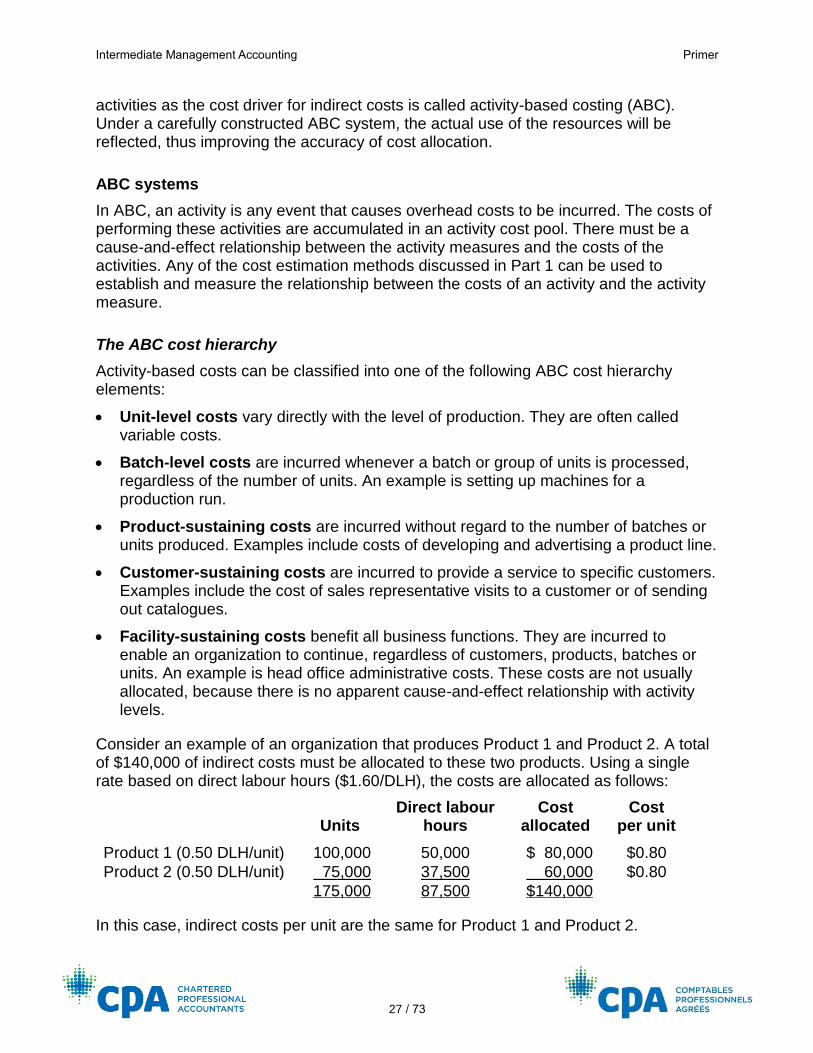

Consider an example of an organization that produces Product 1 and Product 2. A total of $140,000 of indirect costs must be allocated to these two products. Using a single rate based on direct labour hours ($1.60/DLH), the costs are allocated as follows:

Units

Direct labour hours

Cost allocated

Cost per unit

Product 1 (0.50 DLH/unit) 100,000 50,000 $ 80,000 $0.80

Product 2 (0.50 DLH/unit) 75,000 37,500 60,000 $0.80

175,000 87,500 $140,000

In this case, indirect costs per unit are the same for Product 1 and Product 2.

Intermediate Management Accounting Primer

28 / 73

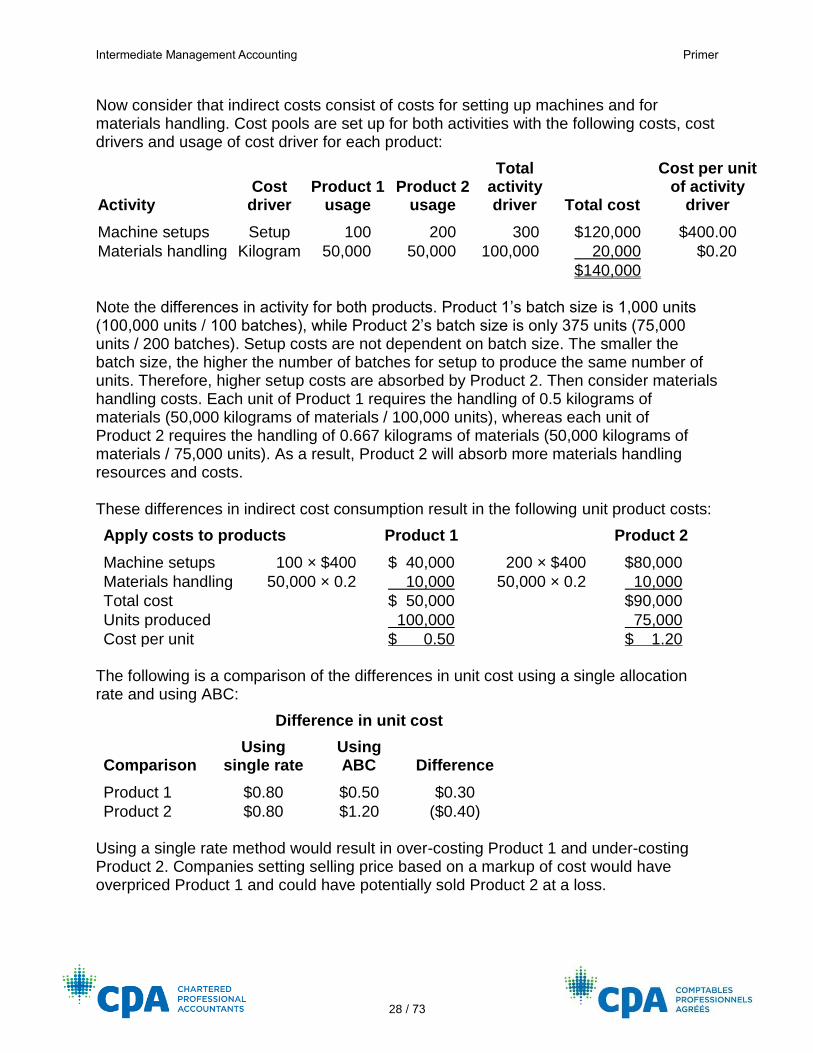

Now consider that indirect costs consist of costs for setting up machines and for materials handling. Cost pools are set up for both activities with the following costs, cost drivers and usage of cost driver for each product:

Activity Cost

driver Product 1

usage Product 2

usage

Total activity driver Total cost

Cost per unit of activity

driver

Machine setups Setup 100 200 300 $120,000 $400.00

Materials handling Kilogram 50,000 50,000 100,000 20,000 $0.20

$140,000 Note the differences in activity for both products. Product 1’s batch size is 1,000 units (100,000 units / 100 batches), while Product 2’s batch size is only 375 units (75,000 units / 200 batches). Setup costs are not dependent on batch size. The smaller the batch size, the higher the number of batches for setup to produce the same number of units. Therefore, higher setup costs are absorbed by Product 2. Then consider materials handling costs. Each unit of Product 1 requires the handling of 0.5 kilograms of materials (50,000 kilograms of materials / 100,000 units), whereas each unit of Product 2 requires the handling of 0.667 kilograms of materials (50,000 kilograms of materials / 75,000 units). As a result, Product 2 will absorb more materials handling resources and costs. These differences in indirect cost consumption result in the following unit product costs:

Apply costs to products Product 1

Product 2

Machine setups 100 × $400 $ 40,000 200 × $400 $80,000

Materials handling 50,000 × 0.2 10,000 50,000 × 0.2 10,000

Total cost $ 50,000 $90,000

Units produced 100,000 75,000

Cost per unit $ 0.50 $ 1.20 The following is a comparison of the differences in unit cost using a single allocation rate and using ABC:

Difference in unit cost

Comparison Using

single rate Using ABC Difference

Product 1 $0.80 $0.50 $0.30

Product 2 $0.80 $1.20 ($0.40) Using a single rate method would result in over-costing Product 1 and under-costing Product 2. Companies setting selling price based on a markup of cost would have overpriced Product 1 and could have potentially sold Product 2 at a loss.

Intermediate Management Accounting Primer

29 / 73

Practice questions

1. Multiple-choice questions:

i. Which of the following best describes the calculation of equivalent units for a period?

a) The number of units actually finished for the period b) The number of units that the direct materials and/or conversion expended

would have completed to 100% c) The number of units actually finished plus the unfinished units in WIP at the

end of the period d) The number of units started in the period less the unfinished units in WIP at

the end of the period Solution Option b) is correct. Equivalent units represent the efforts and resources to start and complete a unit. Thus, the time and resources put into two units that are 50% complete represent the time and resources to start and complete one unit (2 × 50% = 100%). Option a) is incorrect. This only covers the units of the finished products. Partially completed units should be converted into equivalent units based on the amount of work that has been done. Option c) is incorrect. This describes the physical units of the finished units and the units in WIP. Partially completed units should be converted into equivalent units based on the amount of work that has been done. Option d) is incorrect. This calculates the physical units started and finished.

ii. Using ABC, how would the costs of inspecting the quality of the product be accounted for?

a) As an organization-sustaining activity b) As a product-level activity c) As a batch-level activity d) As a unit-level activity

Intermediate Management Accounting Primer

30 / 73

Solution Option c) is correct. A batch-level cost is incurred whenever a batch or group of units is processed. The cost of inspecting is the same. A batch of product is inspected before being moved forward to the next step in the process. Option a) is incorrect. An organization-sustaining activity, such as general administration costs, supports the entire organization. Inspection of product quality supports activities at a lower level. Option b) is incorrect. A product-level activity, such as design, supports individual products or services regardless of the number of units or batches produced. Therefore, it is not limited to one batch, whereas inspecting a batch of products for quality would be. Option d) is incorrect. Inspection is done on a number of units, but the cost is not driven by the unit. The cost is driven by the number of batches, not by the number of units in the batch.

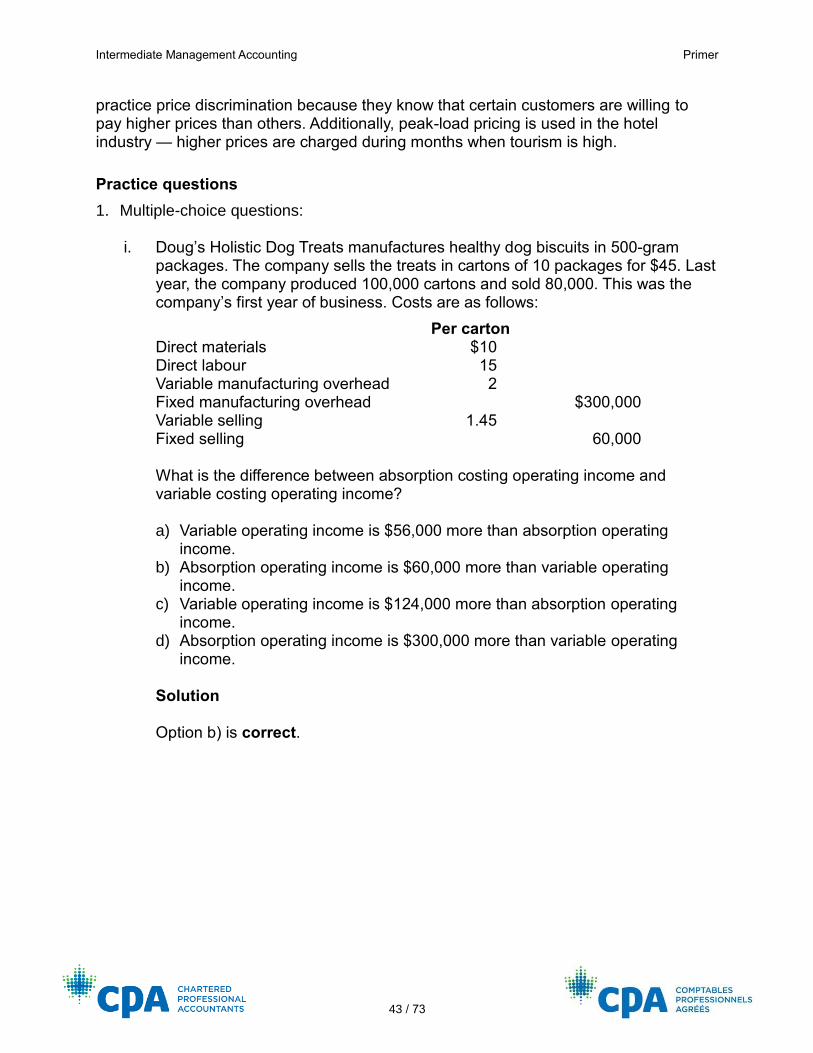

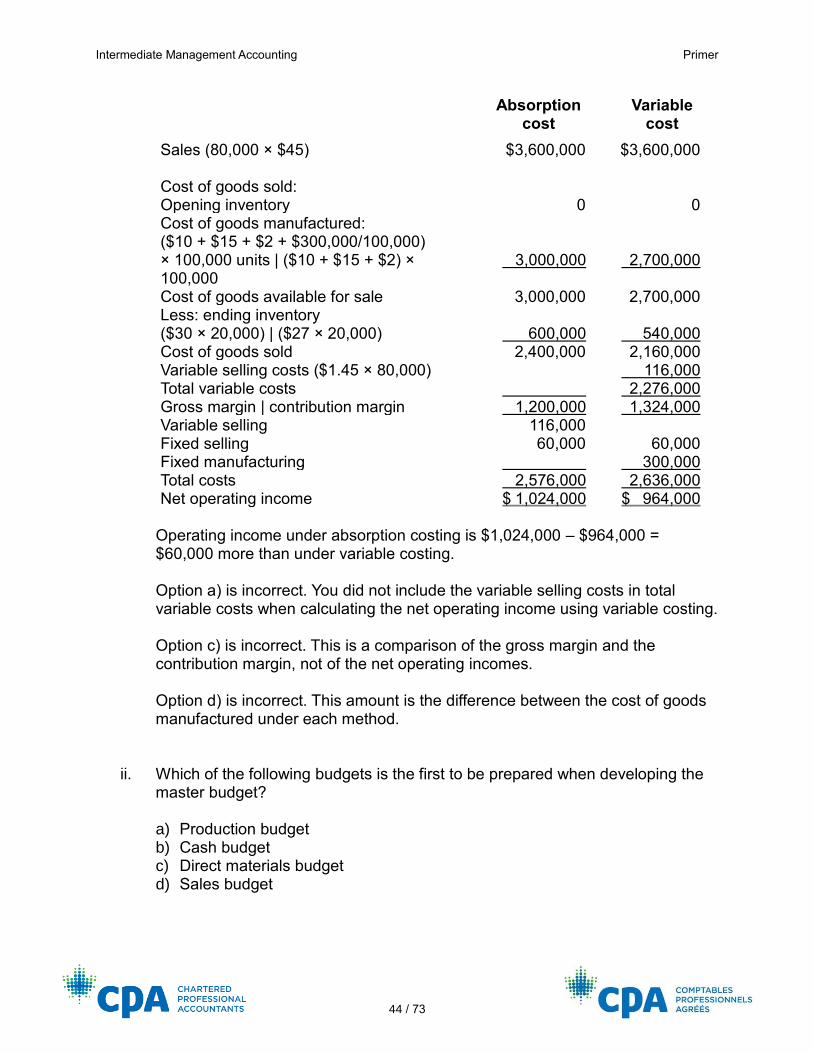

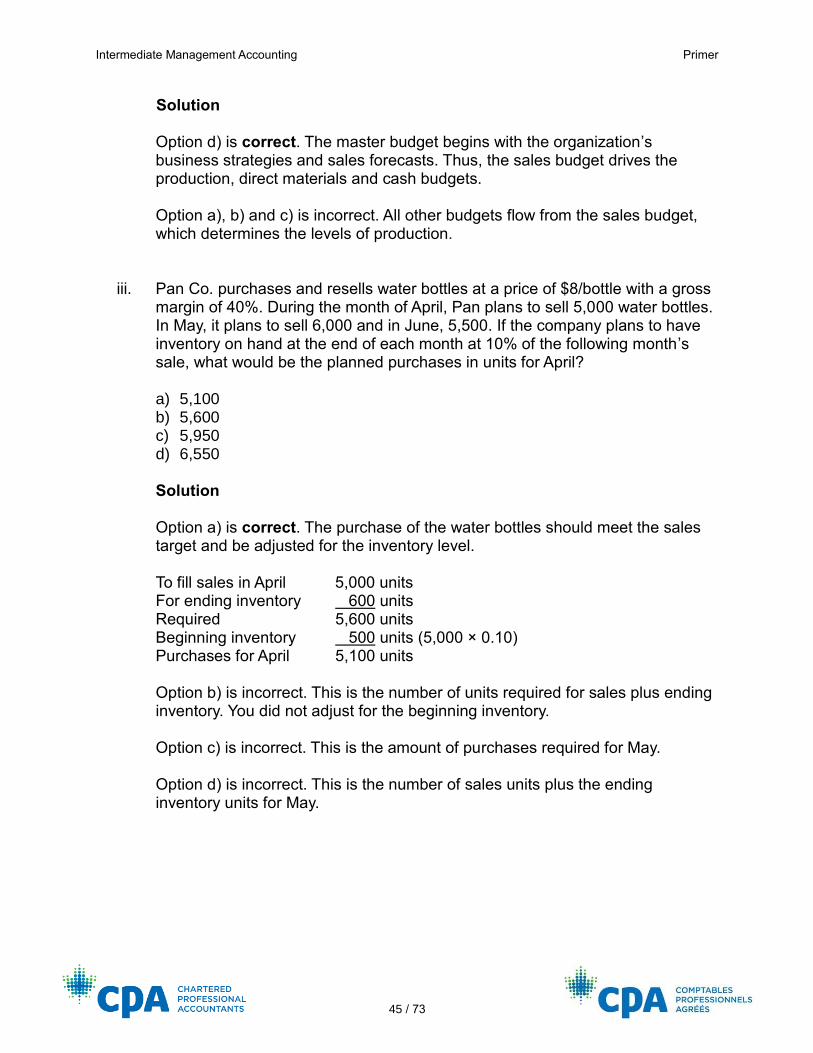

2. Clyde’s Cleaning Supplies makes a liquid industrial cleaner for the shipbuilding industry. The ingredients for the liquid cleaner pass through the Mixing department and the Finishing department, where the cleaner is put into containers. The information for the Mixing department for March is as follows:

Beginning WIP 4,000 litres

Units started 18,000 litres

Units completed 19,000 litres

Beginning WIP direct ingredients $7,400

Beginning WIP conversion $1,200

Direct ingredients added during the month $33,300

Conversion costs added during the month $30,832

The company uses the weighted average method of process costing. Beginning WIP was 20% complete as to conversion. Direct ingredients are added at the beginning of the process. All conversion costs are incurred evenly throughout the process. Ending WIP was 60% complete. Before the cost accountant had a chance to prepare the production report, the company president added up all of the costs for the month and divided by the units transferred. This resulted in a unit cost of $3.828 for the month. The president is concerned about rising costs because the original budget for the month was a unit cost of $3.40.

Intermediate Management Accounting Primer

31 / 73

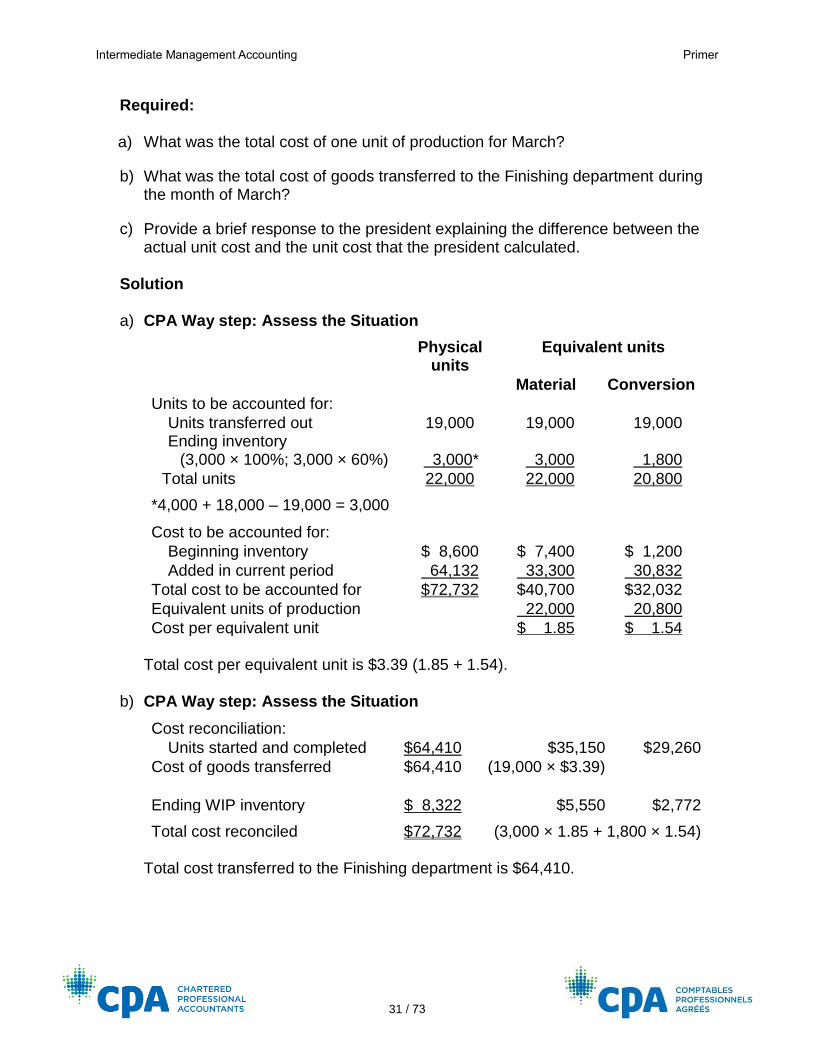

Required: a) What was the total cost of one unit of production for March?

b) What was the total cost of goods transferred to the Finishing department during the month of March?

c) Provide a brief response to the president explaining the difference between the actual unit cost and the unit cost that the president calculated.

Solution a) CPA Way step: Assess the Situation

Physical

units Equivalent units

Material Conversion

Units to be accounted for: Units transferred out 19,000 19,000 19,000 Ending inventory

(3,000 × 100%; 3,000 × 60%) 3,000* 3,000 1,800

Total units 22,000 22,000 20,800

*4,000 + 18,000 – 19,000 = 3,000

Cost to be accounted for: Beginning inventory $ 8,600 $ 7,400 $ 1,200

Added in current period 64,132 33,300 30,832

Total cost to be accounted for $72,732 $40,700 $32,032

Equivalent units of production 22,000 20,800

Cost per equivalent unit $ 1.85 $ 1.54 Total cost per equivalent unit is $3.39 (1.85 + 1.54).

b) CPA Way step: Assess the Situation

Cost reconciliation: Units started and completed $64,410 $35,150 $29,260

Cost of goods transferred $64,410 (19,000 × $3.39)

Ending WIP inventory $ 8,322 $5,550 $2,772

Total cost reconciled $72,732 (3,000 × 1.85 + 1,800 × 1.54) Total cost transferred to the Finishing department is $64,410.

Intermediate Management Accounting Primer

32 / 73

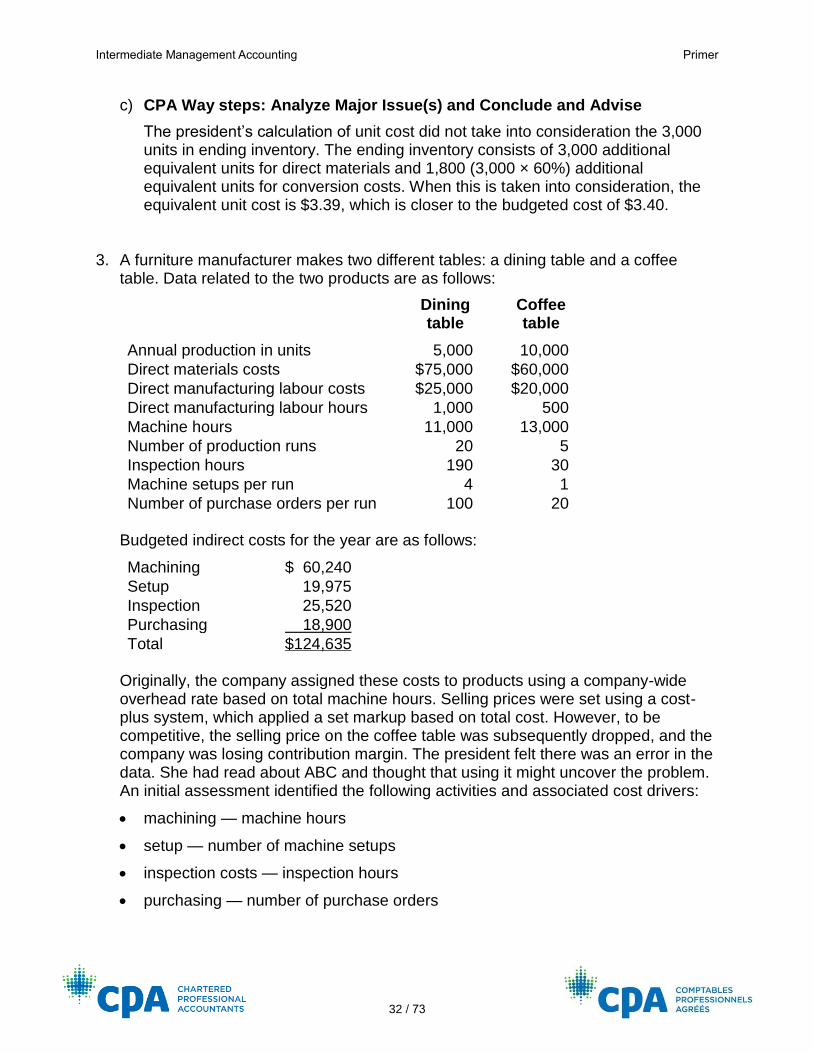

c) CPA Way steps: Analyze Major Issue(s) and Conclude and Advise

The president’s calculation of unit cost did not take into consideration the 3,000 units in ending inventory. The ending inventory consists of 3,000 additional equivalent units for direct materials and 1,800 (3,000 × 60%) additional equivalent units for conversion costs. When this is taken into consideration, the equivalent unit cost is $3.39, which is closer to the budgeted cost of $3.40.

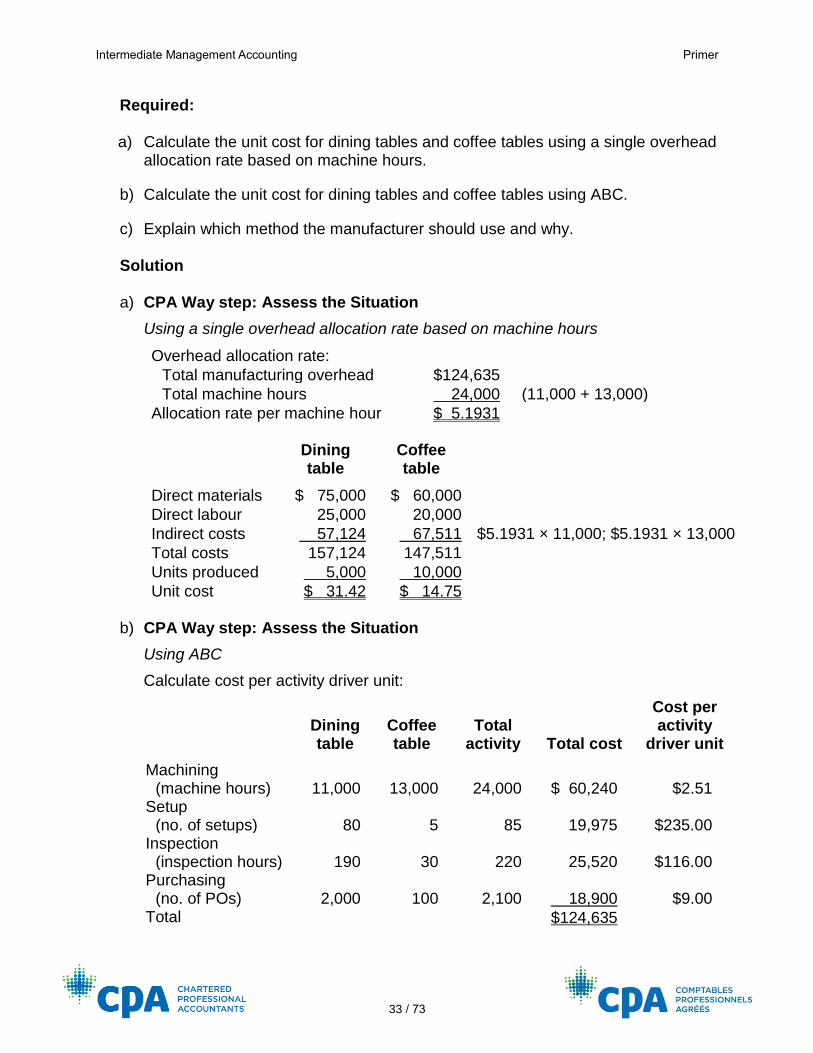

3. A furniture manufacturer makes two different tables: a dining table and a coffee table. Data related to the two products are as follows:

Dining table

Coffee table

Annual production in units 5,000 10,000

Direct materials costs $75,000 $60,000

Direct manufacturing labour costs $25,000 $20,000

Direct manufacturing labour hours 1,000 500

Machine hours 11,000 13,000

Number of production runs 20 5

Inspection hours 190 30

Machine setups per run 4 1

Number of purchase orders per run 100 20 Budgeted indirect costs for the year are as follows:

Machining $ 60,240

Setup 19,975

Inspection 25,520

Purchasing 18,900

Total $124,635 Originally, the company assigned these costs to products using a company-wide overhead rate based on total machine hours. Selling prices were set using a cost-plus system, which applied a set markup based on total cost. However, to be competitive, the selling price on the coffee table was subsequently dropped, and the company was losing contribution margin. The president felt there was an error in the data. She had read about ABC and thought that using it might uncover the problem. An initial assessment identified the following activities and associated cost drivers:

• machining — machine hours

• setup — number of machine setups

• inspection costs — inspection hours

• purchasing — number of purchase orders

Intermediate Management Accounting Primer

33 / 73

Required: a) Calculate the unit cost for dining tables and coffee tables using a single overhead

allocation rate based on machine hours.

b) Calculate the unit cost for dining tables and coffee tables using ABC.

c) Explain which method the manufacturer should use and why. Solution a) CPA Way step: Assess the Situation

Using a single overhead allocation rate based on machine hours

Overhead allocation rate: Total manufacturing overhead $124,635 Total machine hours 24,000 (11,000 + 13,000)

Allocation rate per machine hour $ 5.1931

Dining table

Coffee table

Direct materials $ 75,000 $ 60,000 Direct labour 25,000 20,000 Indirect costs 57,124 67,511 $5.1931 × 11,000; $5.1931 × 13,000

Total costs 157,124 147,511 Units produced 5,000 10,000 Unit cost $ 31.42 $ 14.75

b) CPA Way step: Assess the Situation

Using ABC

Calculate cost per activity driver unit:

Dining table

Coffee table

Total activity Total cost

Cost per activity

driver unit

Machining (machine hours) 11,000 13,000 24,000 $ 60,240 $2.51

Setup (no. of setups) 80 5 85 19,975 $235.00

Inspection (inspection hours) 190 30 220 25,520 $116.00

Purchasing (no. of POs) 2,000 100 2,100 18,900 $9.00

Total $124,635

Intermediate Management Accounting Primer

34 / 73

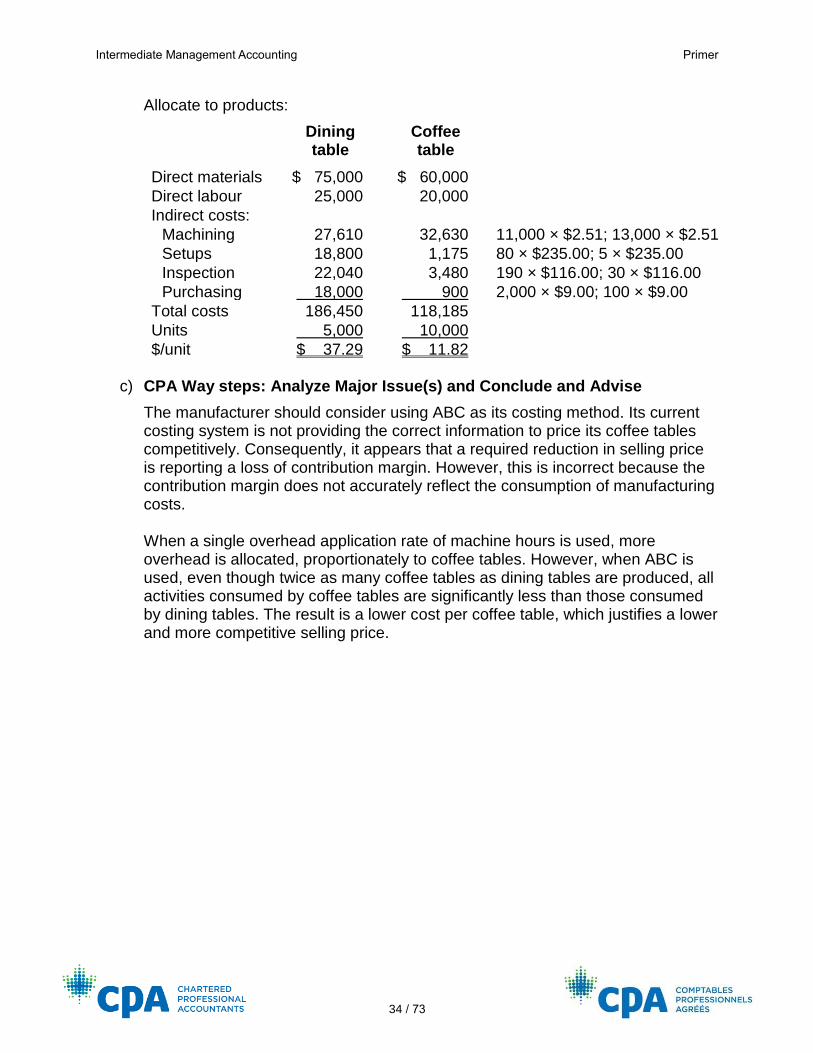

Allocate to products:

Dining table

Coffee table

Direct materials $ 75,000 $ 60,000 Direct labour 25,000 20,000 Indirect costs:

Machining 27,610 32,630 11,000 × $2.51; 13,000 × $2.51

Setups 18,800 1,175 80 × $235.00; 5 × $235.00

Inspection 22,040 3,480 190 × $116.00; 30 × $116.00

Purchasing 18,000 900 2,000 × $9.00; 100 × $9.00

Total costs 186,450 118,185 Units 5,000 10,000 $/unit $ 37.29 $ 11.82

c) CPA Way steps: Analyze Major Issue(s) and Conclude and Advise

The manufacturer should consider using ABC as its costing method. Its current costing system is not providing the correct information to price its coffee tables competitively. Consequently, it appears that a required reduction in selling price is reporting a loss of contribution margin. However, this is incorrect because the contribution margin does not accurately reflect the consumption of manufacturing costs. When a single overhead application rate of machine hours is used, more overhead is allocated, proportionately to coffee tables. However, when ABC is used, even though twice as many coffee tables as dining tables are produced, all activities consumed by coffee tables are significantly less than those consumed by dining tables. The result is a lower cost per coffee table, which justifies a lower and more competitive selling price.

Intermediate Management Accounting Primer

35 / 73

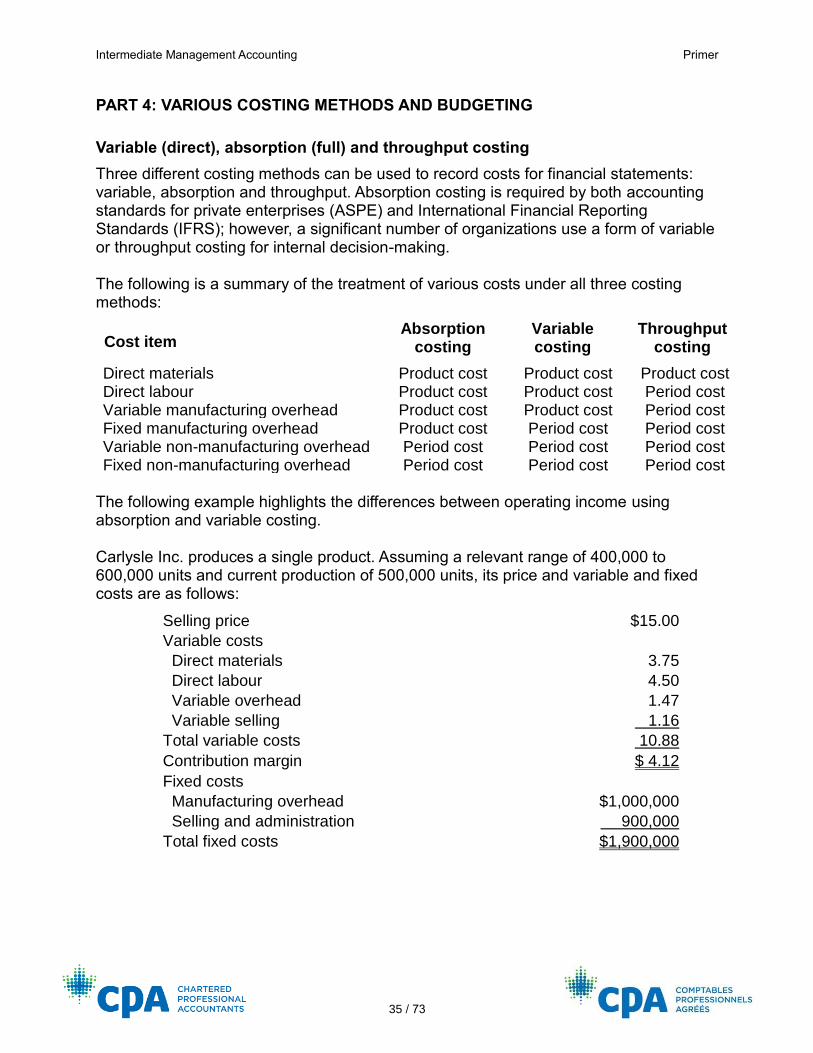

PART 4: VARIOUS COSTING METHODS AND BUDGETING

Variable (direct), absorption (full) and throughput costing

Three different costing methods can be used to record costs for financial statements: variable, absorption and throughput. Absorption costing is required by both accounting standards for private enterprises (ASPE) and International Financial Reporting Standards (IFRS); however, a significant number of organizations use a form of variable or throughput costing for internal decision-making. The following is a summary of the treatment of various costs under all three costing methods:

Cost item Absorption

costing Variable costing

Throughput costing

Direct materials Product cost Product cost Product cost Direct labour Product cost Product cost Period cost Variable manufacturing overhead Product cost Product cost Period cost Fixed manufacturing overhead Product cost Period cost Period cost Variable non-manufacturing overhead Period cost Period cost Period cost Fixed non-manufacturing overhead Period cost Period cost Period cost

The following example highlights the differences between operating income using absorption and variable costing. Carlysle Inc. produces a single product. Assuming a relevant range of 400,000 to 600,000 units and current production of 500,000 units, its price and variable and fixed costs are as follows:

Selling price $15.00

Variable costs

Direct materials 3.75

Direct labour 4.50

Variable overhead 1.47

Variable selling 1.16

Total variable costs 10.88

Contribution margin $ 4.12

Fixed costs

Manufacturing overhead $1,000,000

Selling and administration 900,000

Total fixed costs $1,900,000

Intermediate Management Accounting Primer

36 / 73

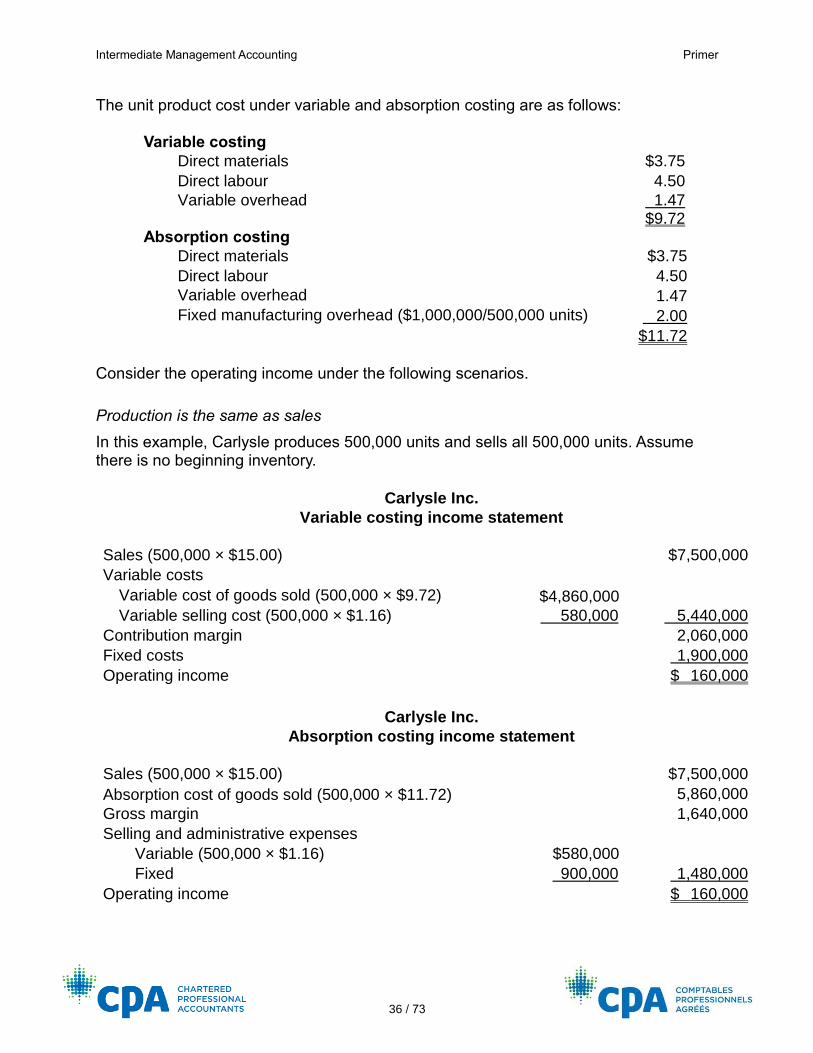

The unit product cost under variable and absorption costing are as follows:

Variable costing

Direct materials $3.75

Direct labour 4.50

Variable overhead 1.47 $9.72

Absorption costing

Direct materials $3.75

Direct labour 4.50

Variable overhead 1.47

Fixed manufacturing overhead ($1,000,000/500,000 units) 2.00

$11.72

Consider the operating income under the following scenarios.

Production is the same as sales

In this example, Carlysle produces 500,000 units and sells all 500,000 units. Assume there is no beginning inventory.

Carlysle Inc.

Variable costing income statement

Sales (500,000 × $15.00) $7,500,000

Variable costs

Variable cost of goods sold (500,000 × $9.72) $4,860,000 Variable selling cost (500,000 × $1.16) 580,000 5,440,000

Contribution margin 2,060,000

Fixed costs 1,900,000

Operating income $ 160,000

Carlysle Inc.

Absorption costing income statement

Sales (500,000 × $15.00) $7,500,000

Absorption cost of goods sold (500,000 × $11.72) 5,860,000

Gross margin 1,640,000

Selling and administrative expenses

Variable (500,000 × $1.16) $580,000

Fixed 900,000 1,480,000

Operating income $ 160,000

Intermediate Management Accounting Primer

37 / 73

Note that the variable costing income statement only considers variable manufacturing costs as product costs. Fixed manufacturing overhead is expensed in the period incurred, making it a period cost. In contrast, absorption costing considers all manufacturing costs to be product costs. As such, fixed manufacturing costs of unsold inventory are carried as an asset in the inventory account until the product is sold. In this example, because all inventory produced is sold, there is no difference in operating income between both options.

Production is greater than sales

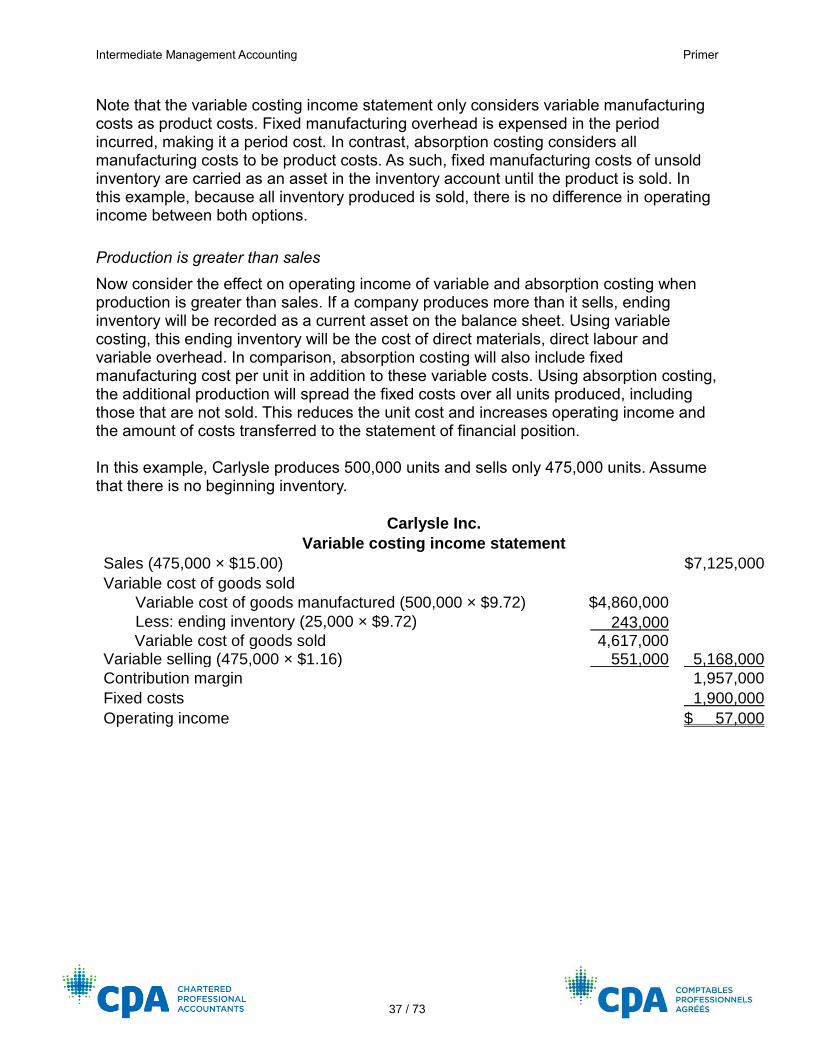

Now consider the effect on operating income of variable and absorption costing when production is greater than sales. If a company produces more than it sells, ending inventory will be recorded as a current asset on the balance sheet. Using variable costing, this ending inventory will be the cost of direct materials, direct labour and variable overhead. In comparison, absorption costing will also include fixed manufacturing cost per unit in addition to these variable costs. Using absorption costing, the additional production will spread the fixed costs over all units produced, including those that are not sold. This reduces the unit cost and increases operating income and the amount of costs transferred to the statement of financial position. In this example, Carlysle produces 500,000 units and sells only 475,000 units. Assume that there is no beginning inventory.

Carlysle Inc.

Variable costing income statement

Sales (475,000 × $15.00)

$7,125,000

Variable cost of goods sold

Variable cost of goods manufactured (500,000 × $9.72) $4,860,000

Less: ending inventory (25,000 × $9.72) 243,000

Variable cost of goods sold 4,617,000

Variable selling (475,000 × $1.16) 551,000 5,168,000

Contribution margin

1,957,000

Fixed costs 1,900,000

Operating income $ 57,000

Intermediate Management Accounting Primer

38 / 73

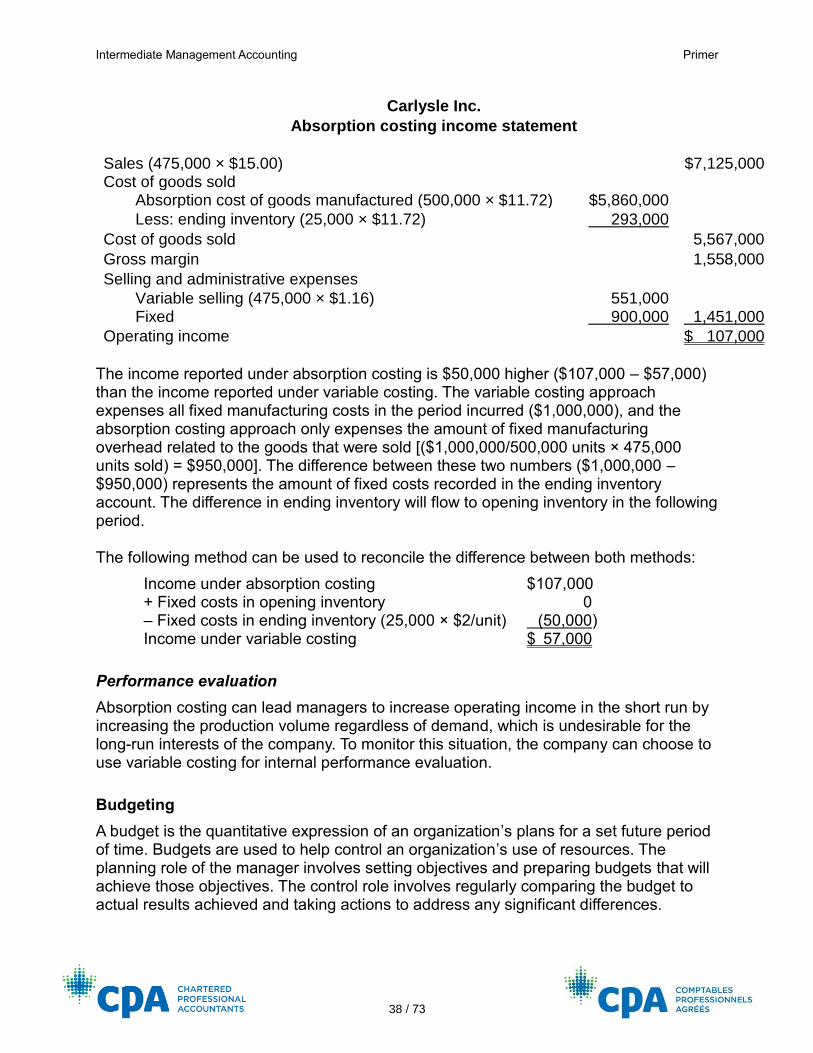

Carlysle Inc.

Absorption costing income statement

Sales (475,000 × $15.00)

$7,125,000

Cost of goods sold

Absorption cost of goods manufactured (500,000 × $11.72) $5,860,000

Less: ending inventory (25,000 × $11.72) 293,000

Cost of goods sold 5,567,000

Gross margin

1,558,000

Selling and administrative expenses

Variable selling (475,000 × $1.16) 551,000

Fixed 900,000 1,451,000

Operating income

$ 107,000

The income reported under absorption costing is $50,000 higher ($107,000 – $57,000) than the income reported under variable costing. The variable costing approach expenses all fixed manufacturing costs in the period incurred ($1,000,000), and the absorption costing approach only expenses the amount of fixed manufacturing overhead related to the goods that were sold [($1,000,000/500,000 units × 475,000 units sold) = $950,000]. The difference between these two numbers ($1,000,000 – $950,000) represents the amount of fixed costs recorded in the ending inventory account. The difference in ending inventory will flow to opening inventory in the following period. The following method can be used to reconcile the difference between both methods:

Income under absorption costing $107,000 + Fixed costs in opening inventory 0 – Fixed costs in ending inventory (25,000 × $2/unit) (50,000) Income under variable costing $ 57,000

Performance evaluation

Absorption costing can lead managers to increase operating income in the short run by increasing the production volume regardless of demand, which is undesirable for the long-run interests of the company. To monitor this situation, the company can choose to use variable costing for internal performance evaluation.

Budgeting

A budget is the quantitative expression of an organization’s plans for a set future period of time. Budgets are used to help control an organization’s use of resources. The planning role of the manager involves setting objectives and preparing budgets that will achieve those objectives. The control role involves regularly comparing the budget to actual results achieved and taking actions to address any significant differences.

Intermediate Management Accounting Primer

39 / 73

The budget is usually prepared by a budget committee consisting of managers who control the costs and revenues of the organization. An operating budget is prepared for the company’s fiscal year, and a capital budget can span several years.

The master budget

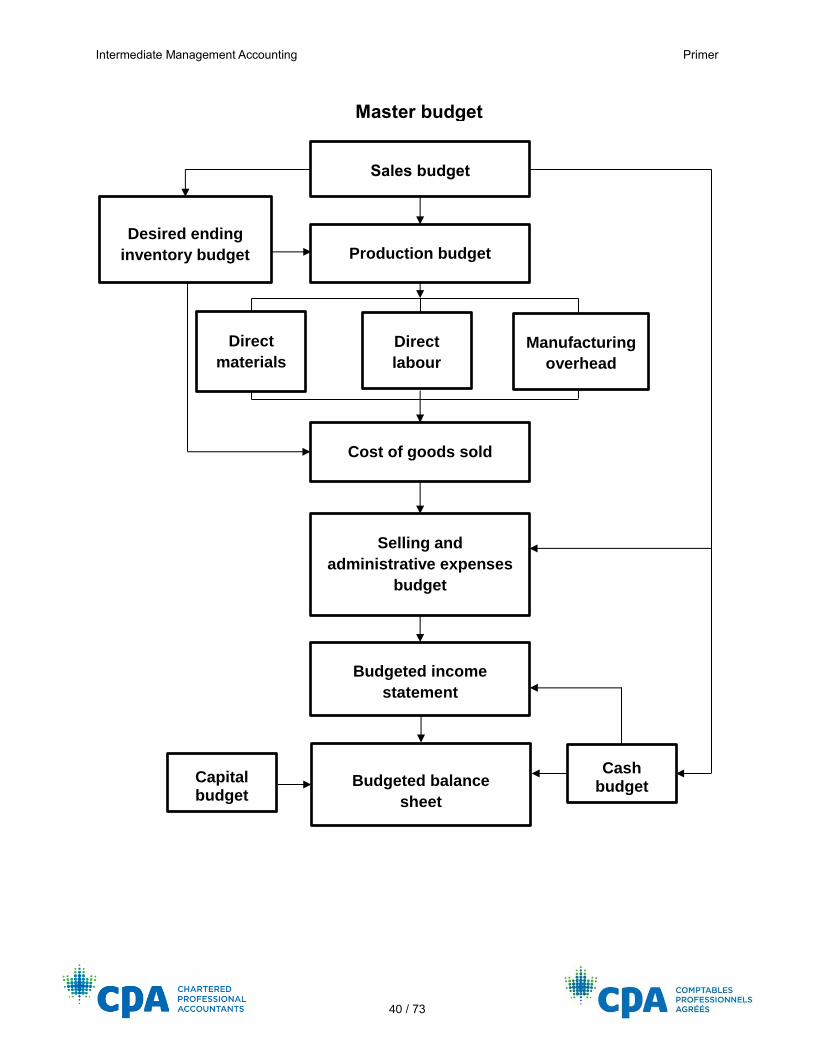

The master budget is the overall budget plan. It begins with the organization’s business strategies and sales forecasts. The organization’s objectives result in a formal sales budget that identifies the planned level of sales for the organization’s products. The sales budget, combined with the organization’s inventory policy, results in the production plan for a manufacturing company and a purchase plan for a merchandising company.

For manufacturing companies, details of the production plan trigger the activities needed to support production. These activity triggers may include the need to acquire additional machinery or to hire or lay off employees and the amount and timing of raw materials for production. The sales budget can also be used to estimate selling and administration expenses to complete the budgeted income statement. Cash collections estimated based on the sales budget, together with cash disbursements, will be used to develop the cash budget and the balance in accounts receivable/payable for the statement of financial position. The following diagram summarizes the components and interrelationships of the master budget components for a manufacturing company.

Intermediate Management Accounting Primer

40 / 73

Sales budget

Production budget

Direct

materials

Direct

labour

Desired ending

inventory budget

Cost of goods sold

Selling and

administrative expenses

budget

Budgeted income

statement

Budgeted balance

sheet

Cash budget

Capital budget

Master budget

Manufacturing

overhead

Intermediate Management Accounting Primer

41 / 73

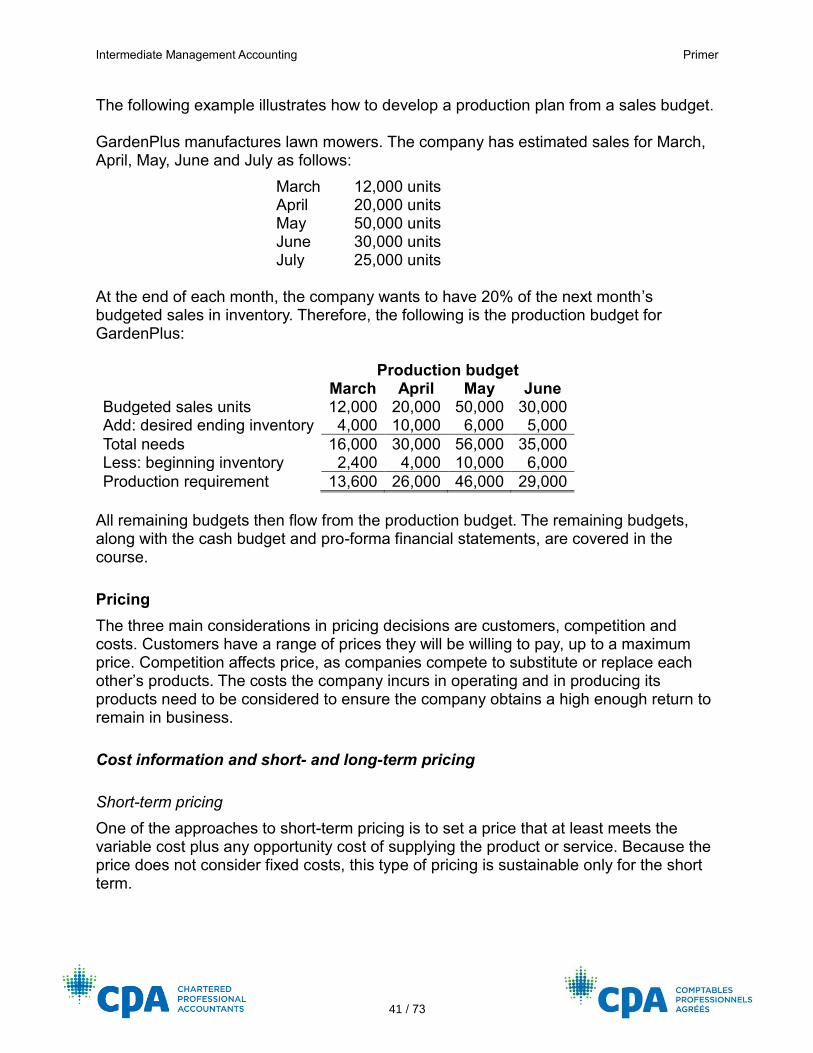

The following example illustrates how to develop a production plan from a sales budget. GardenPlus manufactures lawn mowers. The company has estimated sales for March, April, May, June and July as follows:

March 12,000 units April 20,000 units May 50,000 units June 30,000 units July 25,000 units

At the end of each month, the company wants to have 20% of the next month’s budgeted sales in inventory. Therefore, the following is the production budget for GardenPlus: Production budget March April May June Budgeted sales units 12,000 20,000 50,000 30,000 Add: desired ending inventory 4,000 10,000 6,000 5,000

Total needs 16,000 30,000 56,000 35,000 Less: beginning inventory 2,400 4,000 10,000 6,000

Production requirement 13,600 26,000 46,000 29,000

All remaining budgets then flow from the production budget. The remaining budgets, along with the cash budget and pro-forma financial statements, are covered in the course.

Pricing

The three main considerations in pricing decisions are customers, competition and costs. Customers have a range of prices they will be willing to pay, up to a maximum price. Competition affects price, as companies compete to substitute or replace each other’s products. The costs the company incurs in operating and in producing its products need to be considered to ensure the company obtains a high enough return to remain in business.

Cost information and short- and long-term pricing

Short-term pricing

One of the approaches to short-term pricing is to set a price that at least meets the variable cost plus any opportunity cost of supplying the product or service. Because the price does not consider fixed costs, this type of pricing is sustainable only for the short term.

Intermediate Management Accounting Primer

42 / 73

Long-term pricing