Embed Size (px)

Citation preview

©20

12 CliftonLarsonA

llen LLP

©

Interest Rate RiskFor Internal AuditorsFor Internal Auditors

Dean Rohne, CPA, CIA

[email protected]@cliftonlarsonallen.com

©2012 CliftonLarsonAllen LLP1 111

Session Objectives

• Review recent regulatory guidance on interest rate riskrisk

• Introduce proposed accounting requirement on liquidity risk and interest rate risk

• Review specific questions on the recent interest rate• Review specific questions on the recent interest rate risk exam questionnaire

• Discuss specific testing internal auditors can perform to address interest rate risk

©2012 CliftonLarsonAllen LLP2

Number of Problem Credit Unions

©2012 CliftonLarsonAllen LLP3

Problem Credit Union Insured Shares

©2012 CliftonLarsonAllen LLP4

CAMEL 4/5 by Assets

©2012 CliftonLarsonAllen LLP5

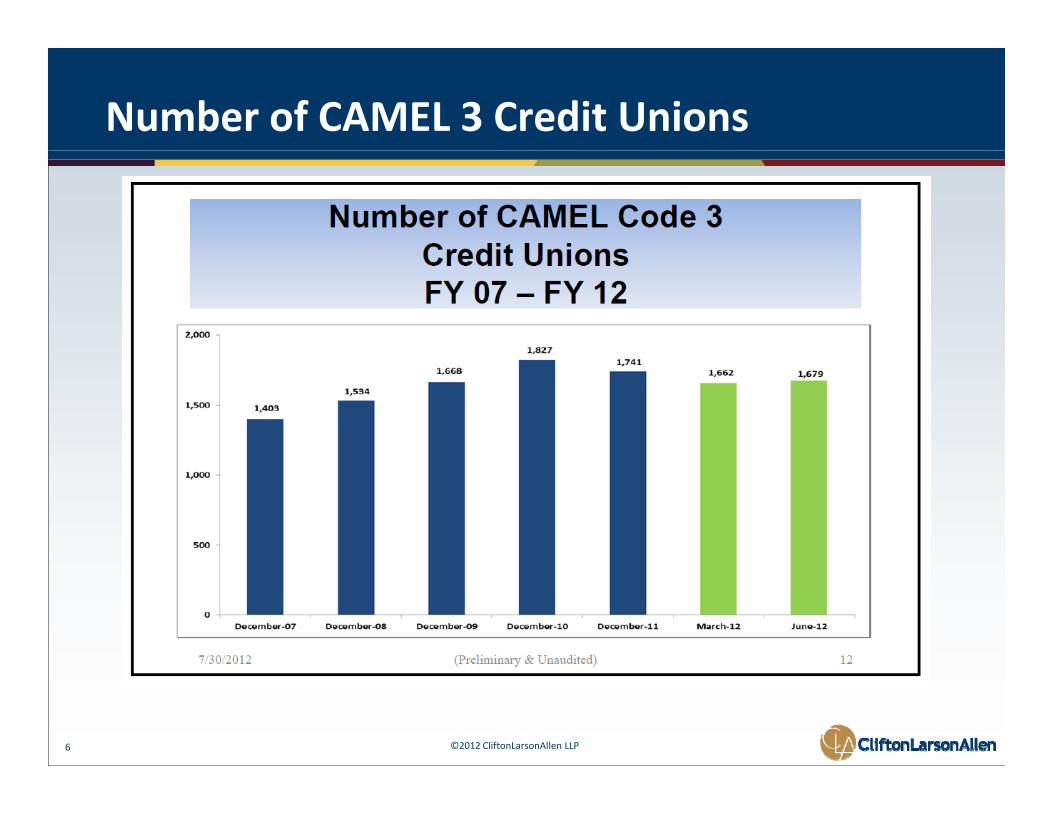

Number of CAMEL 3 Credit Unions

©2012 CliftonLarsonAllen LLP6

CAMEL 3 by Insured Shares

©2012 CliftonLarsonAllen LLP7

CAMEL 3 by Asset Size

©2012 CliftonLarsonAllen LLP8

CAMEL Code by Asset Size

©2012 CliftonLarsonAllen LLP9

Definitions

• Asset Liability Management (ALM)– Managing risks that are present due to mismatches– Managing risks that are present due to mismatches between the assets and liabilities.

• Interest Rate Risk (IRR)( )– The vulnerability of a credit union’s financial condition to adverse movements in market interest rates.

• Liquidity Risk– The risk that a credit union will not be able to meet its

t d f t h fl d ll t l dcurrent and future cash flow and collateral needs.

©2012 CliftonLarsonAllen LLP10

Session Expectations

• Session designed to discuss testing internal auditors could performcould perform.

• Internal auditors should consider the need to utilize• Internal auditors should consider the need to utilize a specialist as deemed necessary based on the complexity of the credit union.p y

©2012 CliftonLarsonAllen LLP11

©20

12 CliftonLarsonA

llen LLP

©

Recent Regulatory Guidance

©2012 CliftonLarsonAllen LLP12121212

Recent Regulatory Guidance

• NCUA Letter to Credit Unions 12‐CU‐05– Issued May 2012– Issued May 2012

– Requires certain federally insured credit unions to adopt a written policy on interest rate risk (IRR) management and a program to implement it effectively.

– Rule affects 45% of the credit unions , but 96% of credit union assetsunion assets.

©2012 CliftonLarsonAllen LLP13

12‐CU‐05

• Why did NCUA amend the existing rule?– FICUs have recently experienced increased exposure to– FICUs have recently experienced increased exposure to IRR due to:◊ Changes in balance sheet composition

• IRR from first mortgages and long‐term investments grew substantially during the most recent interest rate cycle.

◊ Increased uncertainty in financial markets

– Prior regulations did not specifically address IRR management and practices.

With these increases there is a need for strengthening– With these increases there is a need for strengthening policies and programs related to IRR management

©2012 CliftonLarsonAllen LLP14

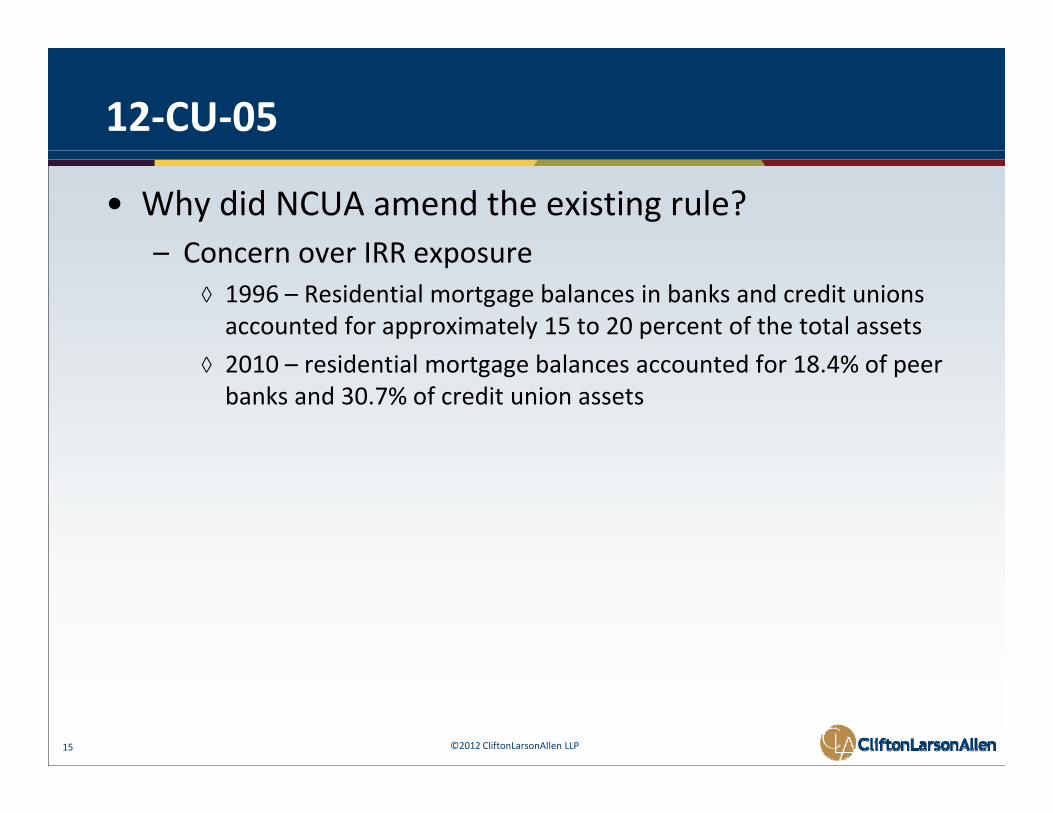

12‐CU‐05

• Why did NCUA amend the existing rule?– Concern over IRR exposure– Concern over IRR exposure

◊ 1996 – Residential mortgage balances in banks and credit unions accounted for approximately 15 to 20 percent of the total assets

20 0 id i l b l d f 8 % f◊ 2010 – residential mortgage balances accounted for 18.4% of peer banks and 30.7% of credit union assets

©2012 CliftonLarsonAllen LLP15

SIRRT Ratio Defined

• Supervisory Interest Rate Risk Threshold (SIRRT)– Takes into account longer term maturities for both first mortgage loans and investments

Whil fi t t l b l dit i b l– While first mortgage loan balances on credit union balance sheets have declined the amount of investments with longer maturities has increased.

©2012 CliftonLarsonAllen LLP16

SIRRT Ratio

©2012 CliftonLarsonAllen LLP17

Number of CUs Covered by 12‐CU‐05

©2012 CliftonLarsonAllen LLP18

Assets Covered by 12‐CU‐05

©2012 CliftonLarsonAllen LLP19

Exposure

©2012 CliftonLarsonAllen LLP20

12‐CU‐05

• Addresses the following:– IRR Policy– IRR Policy

– IRR Oversight and Management

– IRR Measurement and Monitoringg

– Internal Controls

– Decision‐Making Based on IRR Measurement Systems

©2012 CliftonLarsonAllen LLP21

12‐CU‐05

• Addition Guidance for Large Credit Unions with Complex or High Risk Balance SheetsComplex or High Risk Balance Sheets– Defined as credit unions with assets over $500 million

– These credit unions should consider:◊ Policy which provides for the use of outside parties to validate the tests and limits with the risk exposure and complexity of the credit union

◊ IRR measurement systems to report compliance with policy limits at both risk to earnings and net economic value of equity based on a number of defined interest rate scenarios

◊ Effect of changes to key assumptions such as slower or faster prepayments

◊ Enhanced levels of separation between risk taking and risk

©2012 CliftonLarsonAllen LLP22

◊ Enhanced levels of separation between risk taking and risk assessment.

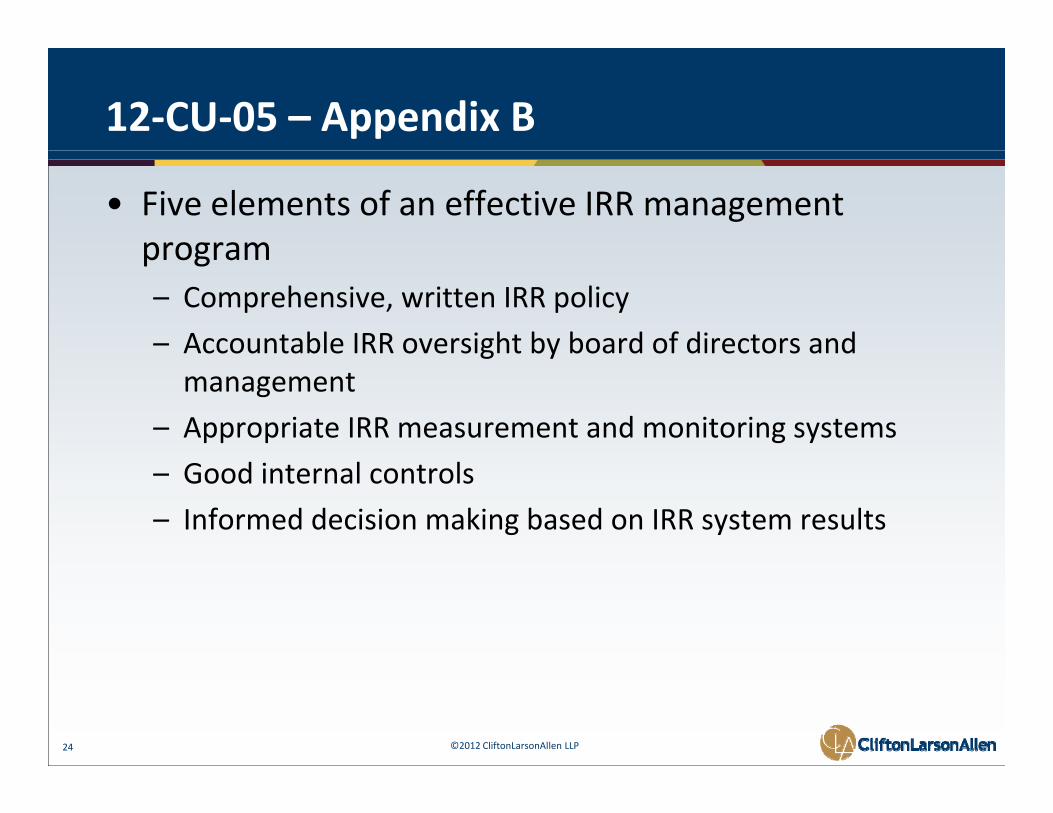

12‐CU‐05 – Appendix B

• Designed to help credit unions meet NCUA’s expectationsexpectations

• Acknowledges it is not possible for a “one size fits all” policy for all credit unionsall policy for all credit unions

• Policy requires specialized judgments based on the credit union’s business objectives and ability to j ywithstand risk– Puts this responsibility with the board of directors

– Provides framework of five fundamental elements of an effective IRR management program

©2012 CliftonLarsonAllen LLP23

12‐CU‐05 – Appendix B

• Five elements of an effective IRR management programprogram– Comprehensive, written IRR policy

– Accountable IRR oversight by board of directors and g ymanagement

– Appropriate IRR measurement and monitoring systems

– Good internal controls

– Informed decision making based on IRR system results

©2012 CliftonLarsonAllen LLP24

12‐CU‐05 – IRR Questionnaire

• Contains four parts that might not all be completed based on complexity of the credit unionbased on complexity of the credit union.

• Part B addresses certain ratios– 17‐4 Test17 4 Test

◊ Quick way to identify potential capital issues based on repricing of loans and investments

◊ E ti t l i l f th f ll i i i i◊ Estimates loss in value of the following given an increase in interest rates• Fixed rate real estate loans

V i bl t l t t l• Variable rate real estate loans

• Investment securities

©2012 CliftonLarsonAllen LLP25

12‐CU‐05 – IRR Questionnaire

• Part B addresses certain ratios (continued)– Short Term Liabilities/Total Shares & Borrowings– Short Term Liabilities/Total Shares & Borrowings

◊ Short term liabilities must be less than 50% of total deposits and borrowings

Sh li bili i i l d◊ Short term liabilities includes:• Shares with a maturity less than one year

• Borrowings with a maturity less than one year

– Complex Assets/Total Assets◊ Defined as adjustable rate mortgages, balloon/hybrid mortgages, agency/GSE mortgage backed securities, other mortgage backed g y/ g g , g gsecurities

◊ Total must be less than 17% of total assets be not be considered complex

©2012 CliftonLarsonAllen LLP26

p

12‐CU‐05 – IRR Questionnaire

• Part C– Consists of a limited scope review to address the following– Consists of a limited scope review to address the following

◊ Policies and Procedures

◊ Board Oversight

◊ IRR Management

◊ IRR Measurement

◊ IRR Componentsp

◊ Internal Controls

◊ Use in Decision Making

©2012 CliftonLarsonAllen LLP27

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire

• Includes detailed questions that address the• Includes detailed questions that address the following:– Sources of balance sheet complexitySources of balance sheet complexity

◊ Large proportion of mortgage loans in:• Hybrid instruments

N f i t• Non‐conforming mortgages

• Adjustment rate mortgages

◊ Investment portfolio composed primarily of CMS and other t l t d itimortgage related securities

◊ Use of non‐maturity shares in pricing strategy of the credit union

◊ Significant amount of complex borrowings

©2012 CliftonLarsonAllen LLP28

◊ Use of derivatives in managing interest rate risk

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– IRR Policy– IRR Policy

◊ Written policy

◊ Identify who has primary responsibility for implementing

◊ Frequency of reporting

◊ IRR limits

◊ Short‐term and long‐term exposureg p

◊ Limits based on shocks

◊ Reporting and action time frames when over a limit

◊ Annual evaluation◊ Annual evaluation

◊ Internal controls

©2012 CliftonLarsonAllen LLP29

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– IRR Oversight and Management– IRR Oversight and Management

◊ Board of director oversight• Effective?

• Assessed adequacy of controls

• Assessed reliability of the measurement methods

• Provided adequate information

• Adequate training on IRR to meet responsibilities

◊ Management responsibilities• Adequate measuring systems

• Understand and evaluate IRR exposures

• Established internal controls

• Prepare contingency plans

©2012 CliftonLarsonAllen LLP30

• Aware of modeling assumptions

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– IRR Measurement and Monitoring– IRR Measurement and Monitoring

◊ Risk Measurement Systems• Assumptions make sense and can they be supported?

• Changes to assumptions documented?

• Analysis have enough depth to adequately address IRR?

◊ Risk Measurement Methods• Methods adequate based on complexity of the credit union?

◊ GAP Analysis• Does management understand how GAP analysis is calculated and how it is used?

• Is the credit union within policy limits

©2012 CliftonLarsonAllen LLP31

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– IRR Measurement and Monitoring (continued)– IRR Measurement and Monitoring (continued)

◊ Income Simulation• Measure net interest income and/or net income?

• Does management have ability to describe how income simulation is calculated and used by the credit union?

• Is the credit union within policy limits?

◊ A t V l ti◊ Asset Valuation• Does the credit union use NCUA’s asset valuation table?

• Does management have ability to describe how asset valuation is calculated and used by the credit unioncalculated and used by the credit union

◊ Net Economic Value (NEV)• Understand use of NEV?

i hi li li i ?

©2012 CliftonLarsonAllen LLP32

• Within policy limits?

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– Components of IRR Measurement Methods– Components of IRR Measurement Methods

◊ Chart of Accounts

◊ Aggregation of Data Input

◊ Account Attributes

◊ Present Value Discounting Methodology

◊ Prepayment Assumptionsp y p

◊ Repricing Sensitivity Assumptions

◊ Decay Rates of Non‐maturity Shares Assumptions

©2012 CliftonLarsonAllen LLP33

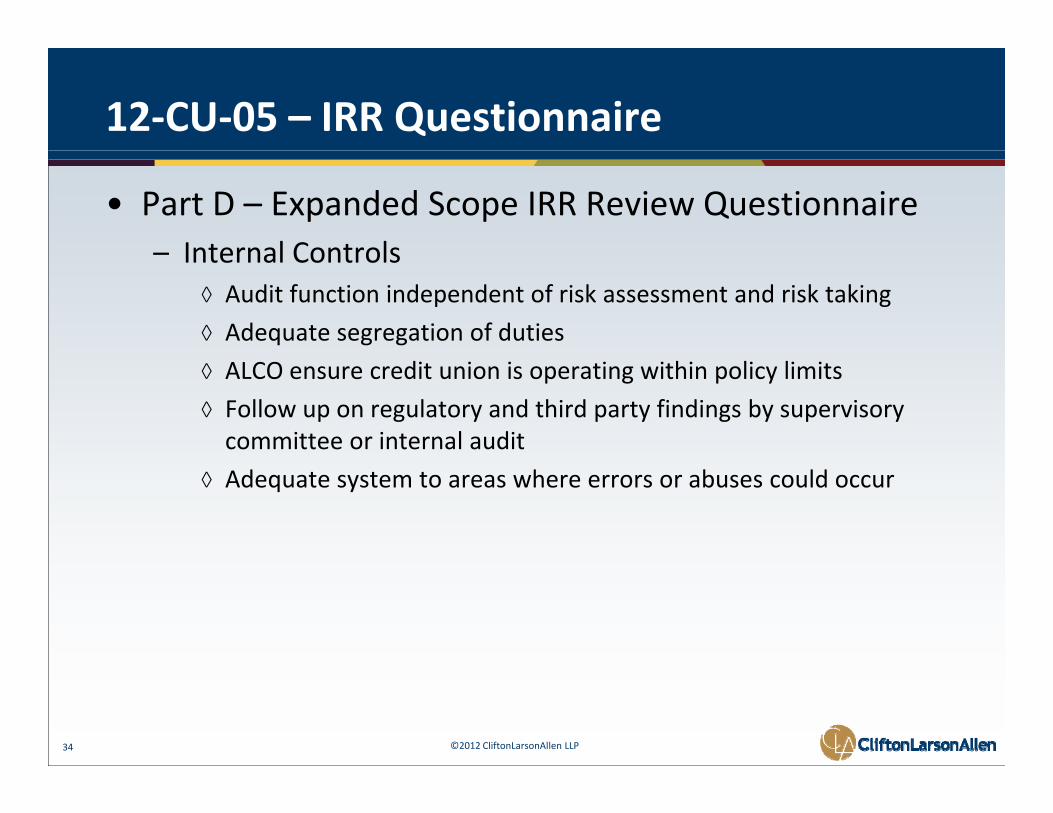

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– Internal Controls– Internal Controls

◊ Audit function independent of risk assessment and risk taking

◊ Adequate segregation of duties

◊ ALCO ensure credit union is operating within policy limits

◊ Follow up on regulatory and third party findings by supervisory committee or internal audit

◊ Adequate system to areas where errors or abuses could occur

©2012 CliftonLarsonAllen LLP34

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– Decision Making Informed by IRR Measurement Systems– Decision‐Making Informed by IRR Measurement Systems

◊ Does management use the results of IRR measurement systems to assist in making decisions in the following areas:

O ti d i i• Operating decisions

• Changing balance sheet structure

• Funding options

P i i• Pricing strategy

• Business plans

◊ Does management proactively identify steps to address negative d ?trends?

©2012 CliftonLarsonAllen LLP35

12‐CU‐05 – IRR Questionnaire

• Part D – Expanded Scope IRR Review Questionnaire– Additional guidance for large credit unions with higher risk– Additional guidance for large credit unions with higher risk or complex balance sheets◊ In addition to the items described above does the credit union:

• Fully understand all parts of IRR

• Periodically obtain a third party validation including the reasonableness of the assumptions

i k i d d i f diff• Measure risk to earnings and NEV under a variety of different interest rate scenarios

• Disaggregate data down to the account level?

• Adequately test changes to assumptions on IRR measurement results• Adequately test changes to assumptions on IRR measurement results

• Enhanced levels of separation between risk taking and risk assessment?

©2012 CliftonLarsonAllen LLP36

©20

12 CliftonLarsonA

llen LLP

©

Proposed changes to ASC Topic 825ASC Topic 825

©2012 CliftonLarsonAllen LLP37373737

Financial Instruments (Topic 825)

• Disclosures about Liquidity Risk and Interest Rate RiskRisk– Proposed accounting standing Issued June 27, 2012 with comments due September 25, 2012

– Why was this issued as a proposed standard◊ Stakeholders’ feedback on a proposed standard related to derivatives indicated there are risks inherent within classes ofderivatives indicated there are risks inherent within classes of financial instruments and the way an entity managements those risks.

◊ No single amount or measurement is possible to disclose this risk◊ No single amount or measurement is possible to disclose this risk

– Effective date◊ Not set, will be determined as Financial Accounting Standards

( )

©2012 CliftonLarsonAllen LLP38

Board (FASB) considers feedback on the proposed changes.

Financial Instruments (Topic 825)

• Disclosures required are determined based on whether the entity is a financial institutionwhether the entity is a financial institution.– Financial institution defined as reportable segments whose primary business includes:◊ Earning income from interest based on earning assets an interest paid on borrowed funds

◊ Provides insurance

©2012 CliftonLarsonAllen LLP39

Financial Instruments (Topic 825)

• Disclosures would provide information about the risks and uncertainties a credit union would have inrisks and uncertainties a credit union would have in meeting financial obligations.– Would require quantitative and narrative disclosure q qrelated to a credit union’s exposure to IRR.

©2012 CliftonLarsonAllen LLP40

Financial Instruments (Topic 825)

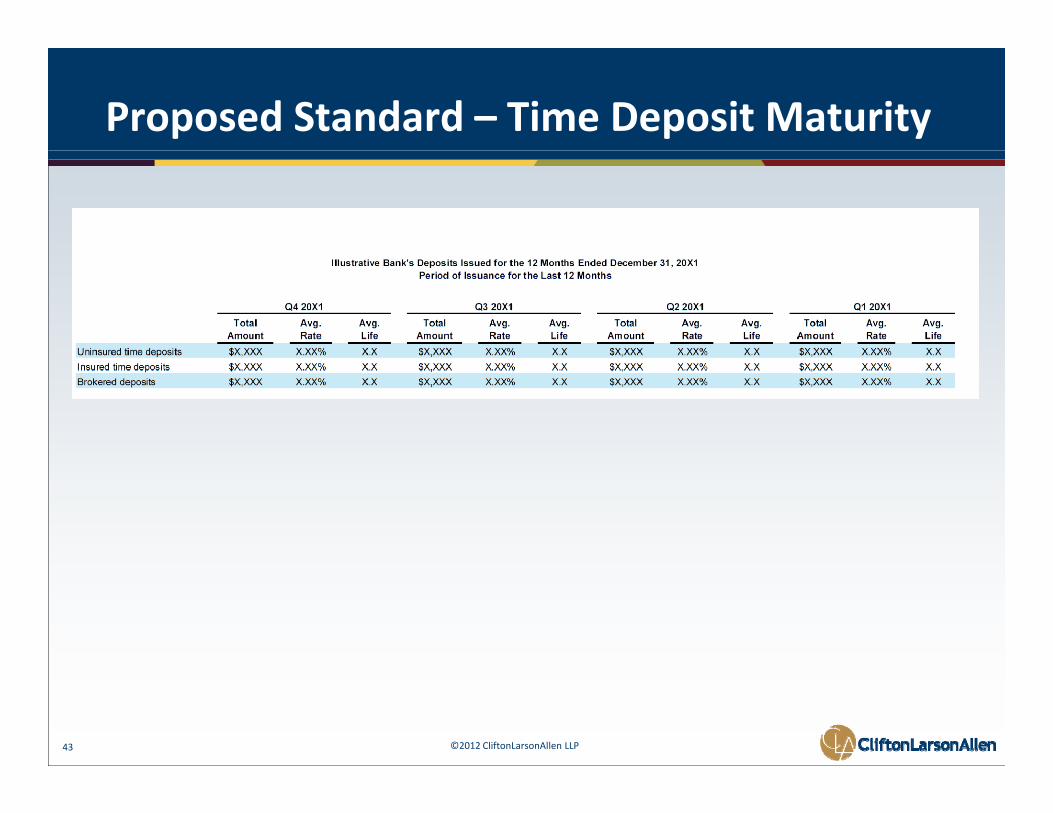

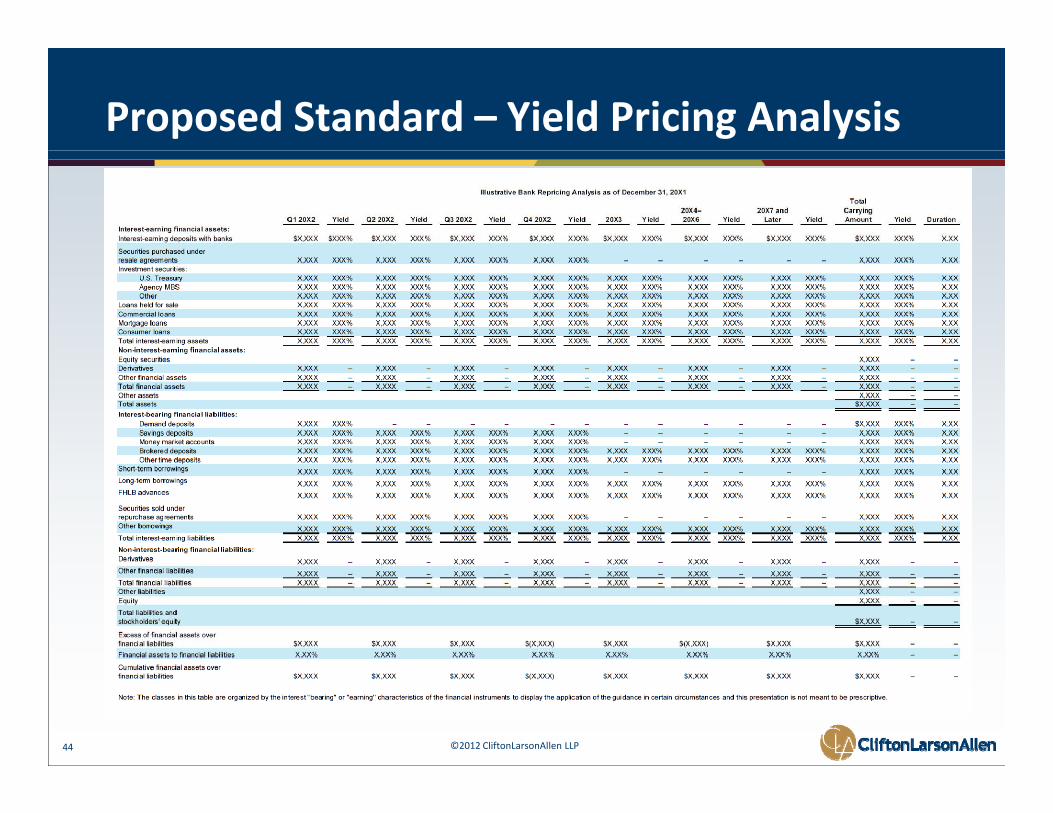

• Disclosures for financial institutions– Liquidity Gap Maturity Analysis– Liquidity Gap Maturity Analysis

– Issuance of Time Deposits

– Available Liquid Fundsq

– Repricing Gap Analysis

– Interest Rate Sensitivity

©2012 CliftonLarsonAllen LLP41

Proposed Standard – Liquidity GAP Maturity

©2012 CliftonLarsonAllen LLP42

Proposed Standard – Time Deposit Maturity

©2012 CliftonLarsonAllen LLP43

Proposed Standard – Yield Pricing Analysis

©2012 CliftonLarsonAllen LLP44

Proposed Standard – Available Liquid Funds

©2012 CliftonLarsonAllen LLP45

Proposed Standard – Interest Rate Sensitivity

©2012 CliftonLarsonAllen LLP46

What Should Internal Auditors Do?

• Verify the Credit Union has implemented the requirements of 12‐CU‐05requirements of 12 CU 05

• Determine whether management is aware of proposed changes and ASC Topic 825proposed changes and ASC Topic 825

• Assess whether IRR should be included in the scope of an internal audit plan based on the internal audit pdepartments risk assessment

©2012 CliftonLarsonAllen LLP47

What Should Internal Auditors Do?

• If testing IRR within your credit union consider the following:following:– Use a specialist as needed

– Utilize the examiner checklist to identify any regulatory y y g yissues◊ Internal control issues

◊ Management understanding of IRR present◊ Management understanding of IRR present

◊ Board understanding and involvement

©2012 CliftonLarsonAllen LLP48

Contact UsFollow our blog for current

discussions on credit unions.

www larsonallen com/blog

Dean Rohne, CPA, CIAdean rohne@ cliftonlarsonallen com www.larsonallen.com/blog

www.twitter.com/cliftonlarsonallen

dean.rohne@ cliftonlarsonallen.com

800‐657‐4477

www.facebook.com/cliftonlarsonallen

www.linkedin.com/companies/

cliftonlarsonallen

©2012 CliftonLarsonAllen LLP49