Embed Size (px)

Citation preview

Chapter Outline

• 5.1 Types of Rates• 5.2 Zero Rates• 5.3 Bond Pricing• 5.4 Determining zero rates• 5.5 Forward rates • 5.6 Forward rate agreements• 5.7 Theories of term structure• 5.8 Day count conventions

Chapter Outline

• 5.9 Quotations• 5.10 Treasury Bond Futures• 5.11 Eurodollar futures• 5.12 The LIBOR zero curve• 5.13 Duration• 5.14 Duration-based hedging strategies

5.1 Types of Rates

• Treasury rates• LIBOR rates• Repo rates

5.2 Zero Rates

A zero rate (or spot rate), for maturity T is the rate of interest earned on an investment that provides a payoff only at time T

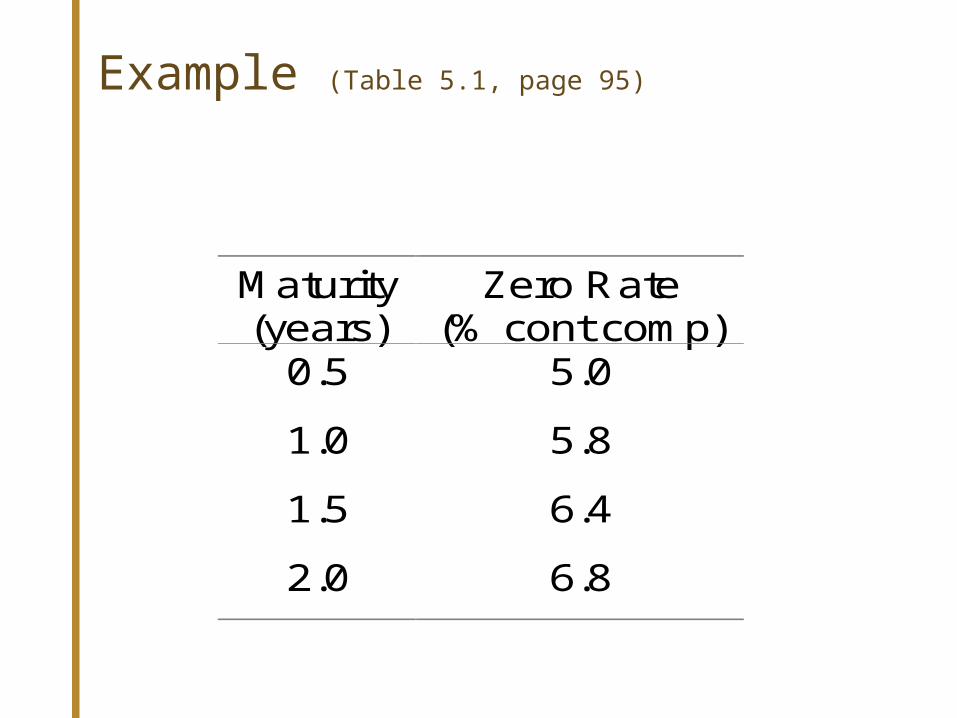

Example (Table 5.1, page 95)

Maturity(years)

Zero Rate(% cont comp)

0.5 5.0

1.0 5.8

1.5 6.4

2.0 6.8

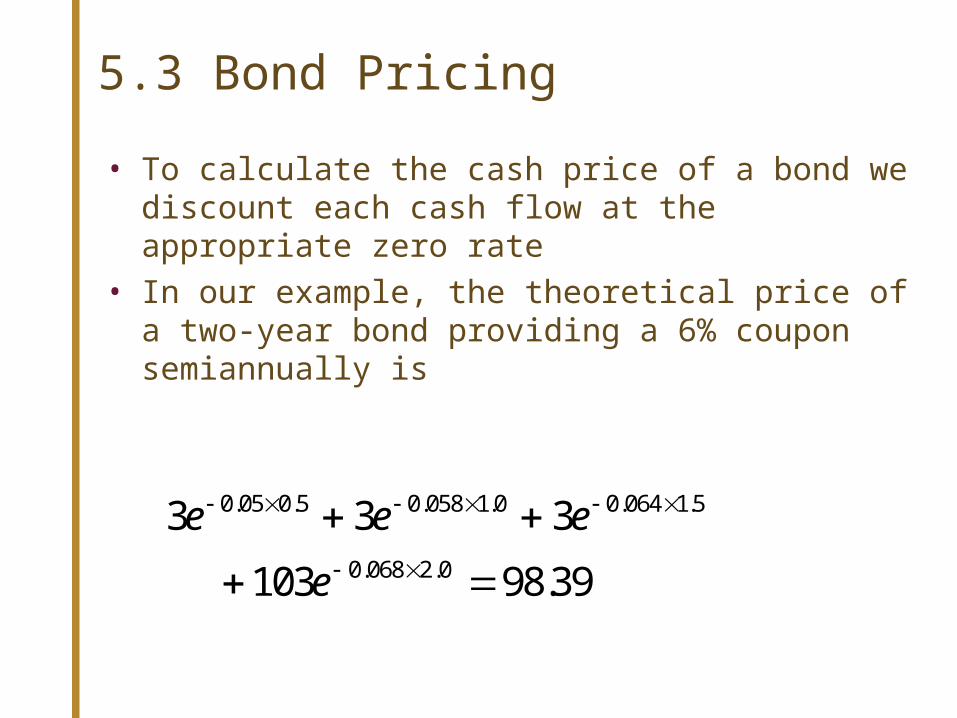

5.3 Bond Pricing

• To calculate the cash price of a bond we discount each cash flow at the appropriate zero rate

• In our example, the theoretical price of a two-year bond providing a 6% coupon semiannually is

3 3 3

103 98 39

0 05 0 5 0 058 1 0 0 064 1 5

0 068 2 0

e e e

e

. . . . . .

. . .

Bond Yield

• The bond yield is the discount rate that makes the present value of the cash flows on the bond equal to the market price of the bond. aka YTM

• Suppose that the market price of the bond in our example equals its theoretical price of 98.39

• The bond yield is given by solving

to get y=0.0676 or 6.76%.3 3 3 103 98 390 5 1 0 1 5 2 0e e e ey y y y . . . . .

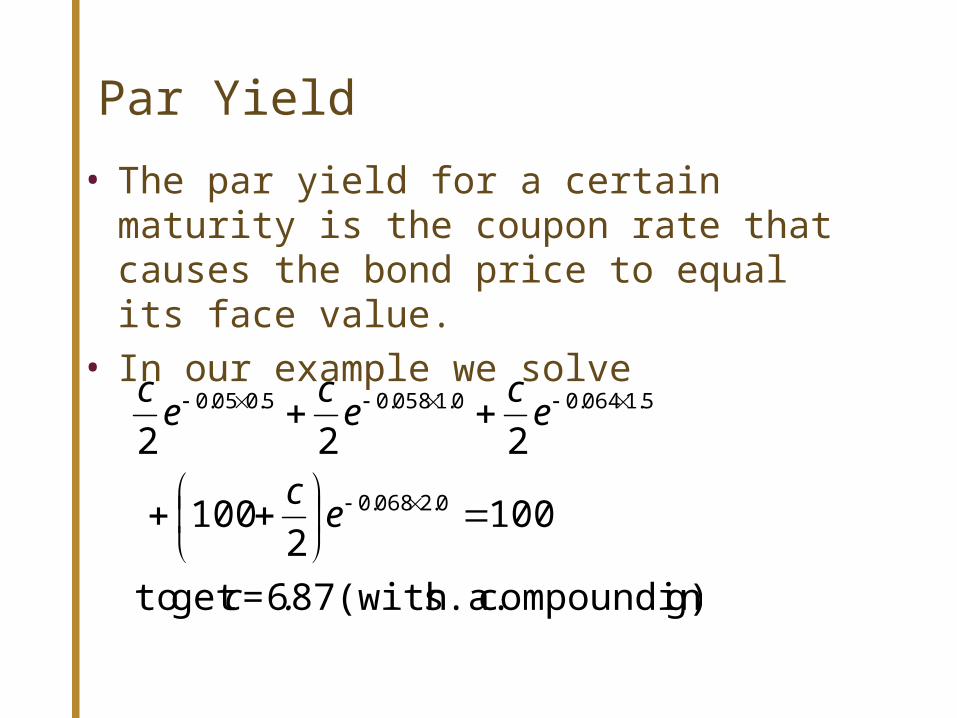

Par Yield

• The par yield for a certain maturity is the coupon rate that causes the bond price to equal its face value.

• In our example we solve

g)compoundin s.a.(with 876get to

1002

100

222

0.2068.0

5.1064.00.1058.05.005.0

.c=

ec

ec

ec

ec

Par Yield continued

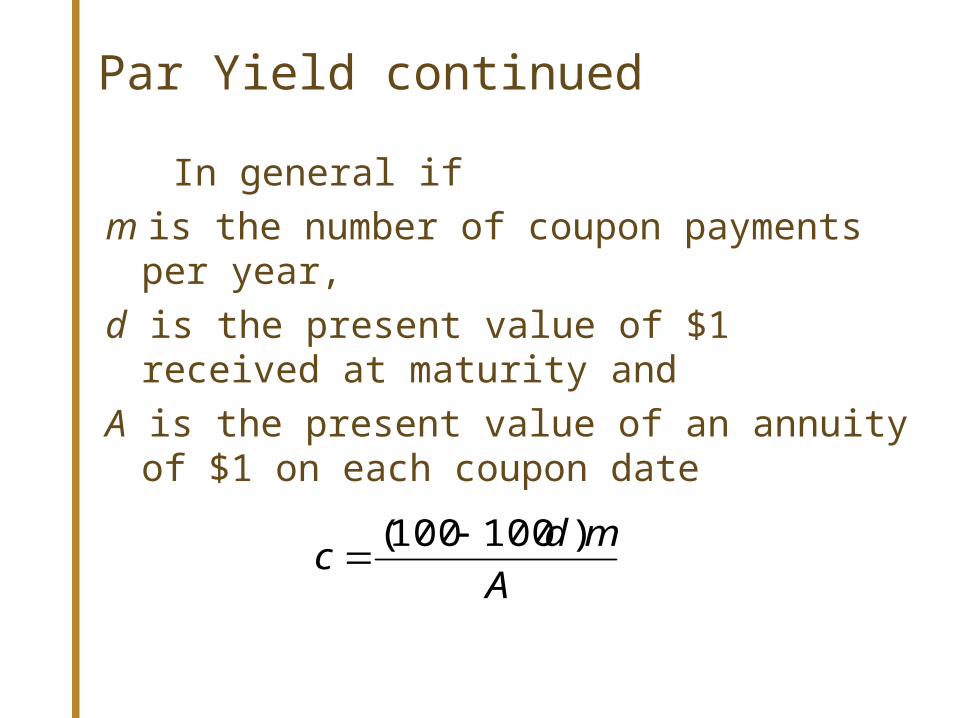

In general if

m is the number of coupon payments per year,

d is the present value of $1 received at maturity and

A is the present value of an annuity of $1 on each coupon date

A

mdc

)100100(

5.4 Determining Treasury Zero Rates

• Treasury zero rates can be calculated from the prices of instruments that trade.

• One way to do this is the bootstrap method.• To see how this works, consider the following

example:

Sample Data for Determining the Zero Curve (Table

5.2, page 97)

Bond Time to Annual Bond

Principal Maturity Coupon Price

(dollars) (years) (dollars) (dollars)

100 0.25 0 97.5

100 0.50 0 94.9

100 1.00 0 90.0

100 1.50 8 96.0

100 2.00 12 101.6

Half the stated coupon is paid every 6 months.

•An amount 2.5 can be earned on 97.5 during 3 months.

•The 3-month rate is 4 times 2.5/97.5 or 10.256% with quarterly compounding

•This is 10.127% with continuous compounding

The Bootstrapping the Zero Curve

• Similarly the 6 month and 1 year rates are 10.469% and 10.536% with continuous compounding Bond Time to Annual Bond

Principal Maturity Coupon Price

(dollars) (years) (dollars) (dollars)

100 0.25 0 97.5

100 0.50 0 94.9

100 1.00 0 90.0

100 1.50 8 96.0

100 2.00 12 101.6

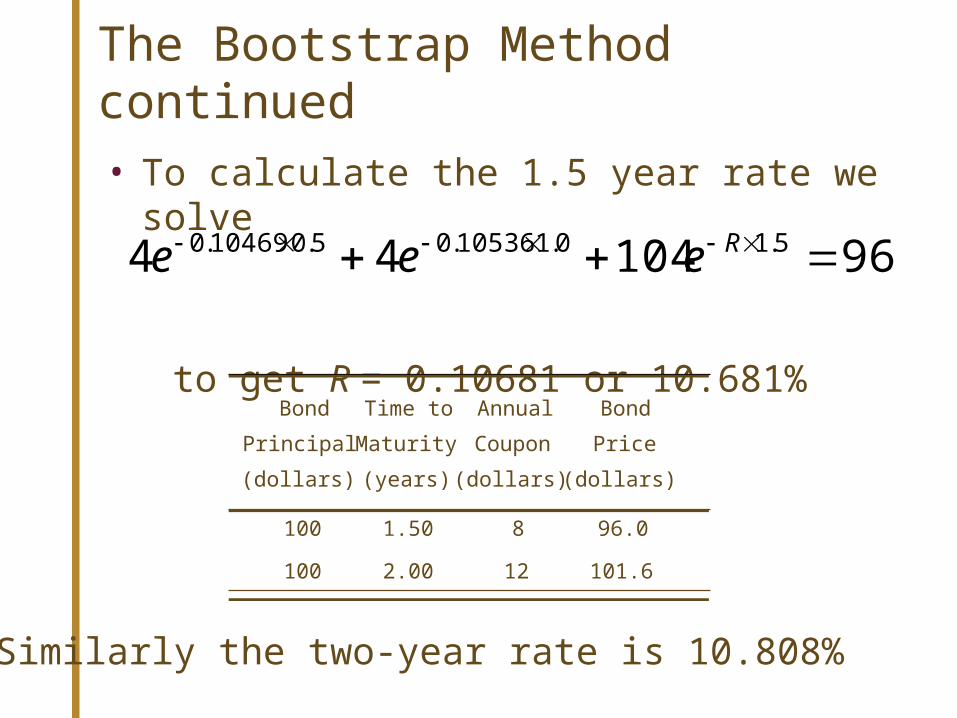

The Bootstrap Method continued

• To calculate the 1.5 year rate we solve

to get R = 0.10681 or 10.681%

9610444 5.10.110536.05.010469.0 Reee

Bond Time to Annual Bond

Principal Maturity Coupon Price

(dollars) (years) (dollars) (dollars)

100 1.50 8 96.0

100 2.00 12 101.6

•Similarly the two-year rate is 10.808%

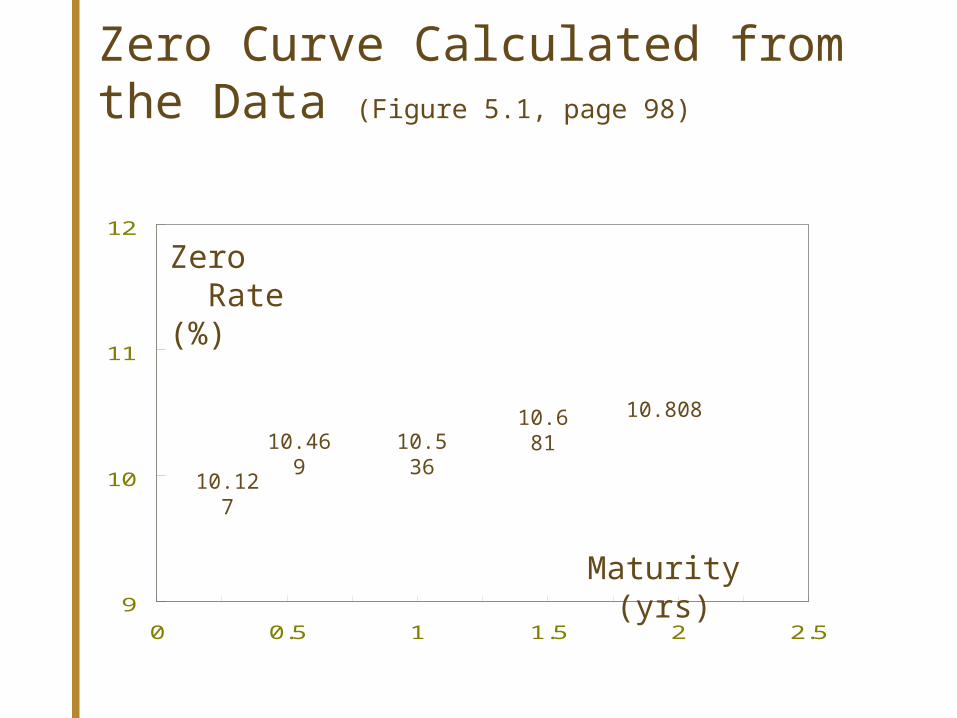

Zero Curve Calculated from the Data (Figure 5.1, page 98)

9

10

11

12

0 0.5 1 1.5 2 2.5

Zero Rate (%)

Maturity (yrs)

10.127

10.469 10.536

10.681

10.808

5.5 Forward Rates

The forward rate is the future zero rate implied by today’s term structure of interest rates

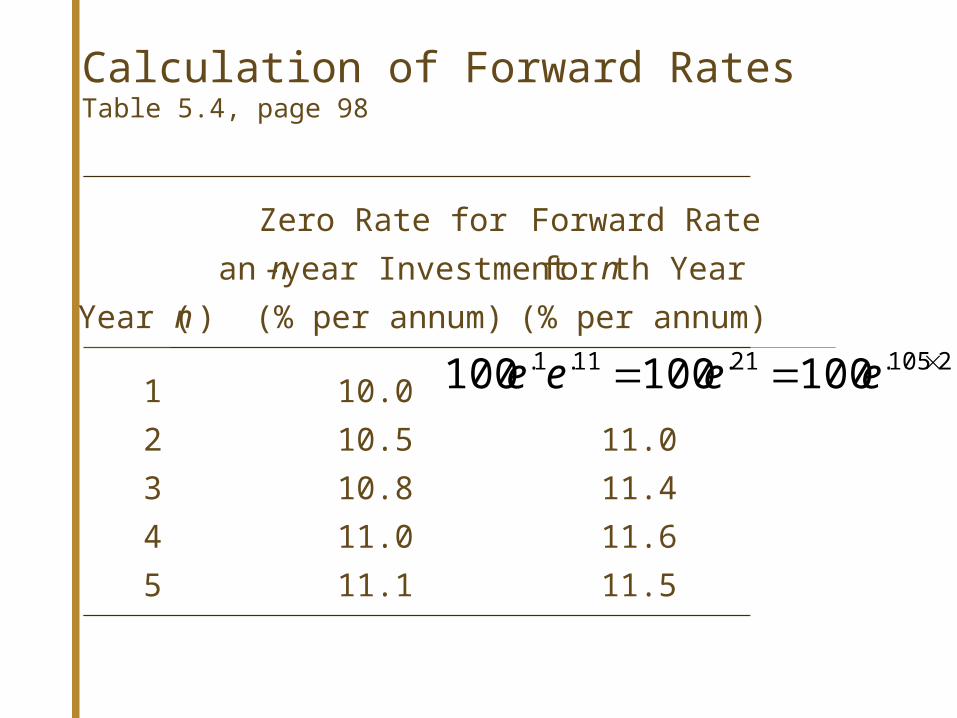

Calculation of Forward RatesTable 5.4, page 98

Zero Rate for Forward Rate

an n -year Investment for n th Year

Year (n ) (% per annum) (% per annum)

1 10.0

2 10.5 11.0

3 10.8 11.4

4 11.0 11.6

5 11.1 11.5

2105.21.11.1. 100100100 eeee

Formula for Forward Rates

• Suppose that the zero rates for maturities T1 and T2 are R1 and R2 with both rates continuously compounded.

• The forward rate for the period between times T1 and T2 is

R T R T

T T2 2 1 1

2 1

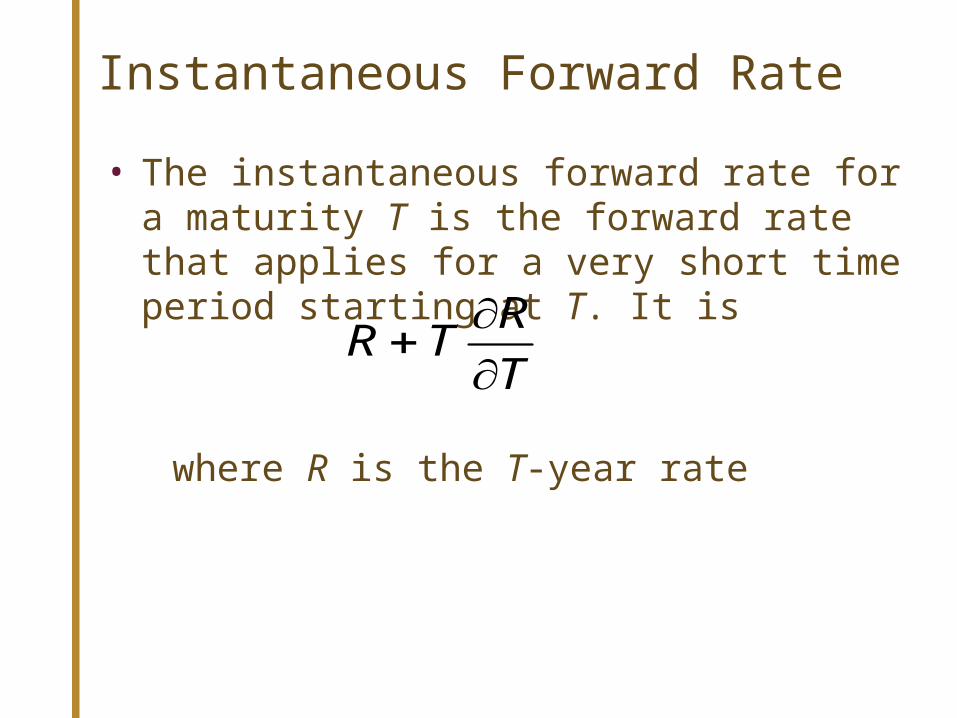

Instantaneous Forward Rate

• The instantaneous forward rate for a maturity T is the forward rate that applies for a very short time period starting at T. It is

where R is the T-year rate

R TR

T

Upward vs. Downward SlopingYield Curve

• For an upward sloping yield curve:

Fwd Rate > Zero Rate > Par Yield

• For a downward sloping yield curve

Par Yield > Zero Rate > Fwd Rate

Forward Rate Agreement

• A forward rate agreement (FRA) is an agreement that a certain rate will apply to a certain principal during a certain future time period

Forward Rate Agreementcontinued (Page 100) • An FRA is equivalent to an agreement where

interest at a predetermined rate, RK is exchanged for interest at the market rate

• An FRA can be valued by assuming that the forward interest rate is certain to be realized

• We can make arbitrage arguments

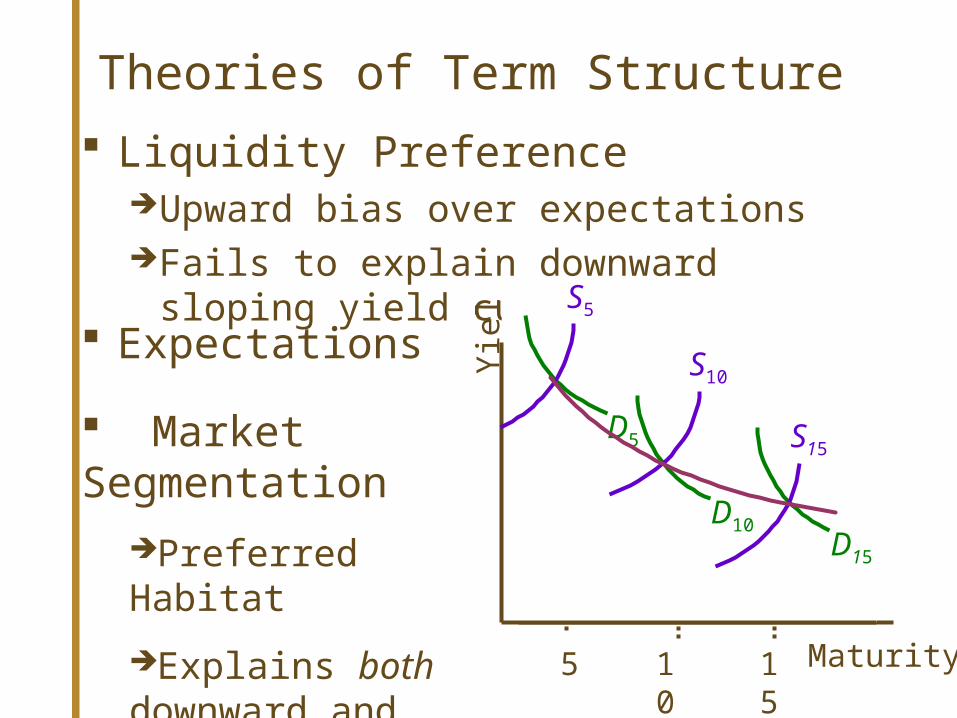

Theories of Term Structure

Yie

l d

Maturity5 10 15

Liquidity PreferenceUpward bias over expectationsFails to explain downward sloping yield curve

Market Segmentation

Preferred Habitat

Explains both downward and upward sloping yield curves

D5

D10

D15

S5

S10

S15 Expectations

D5

D10D15

S10

S15

S5

Day Count Conventions in the U.S. (Pages 102-103)

Treasury Bonds:

Corporate Bonds:

Money Market Instruments:

Actual/Actual (in period)

30/360

Actual/360

The interest earned between two dates is:

period referencein earnedinterest period referencein days ofnumber

datesbetween days ofnumber

5.9 Treasury Bond Price Quotes in the U.S

Cash price = Quoted price + Accrued Interest since last coupon date

Treasury Bill Quote in the U.S.

If Y is the cash price of a Treasury bill that has n days to maturity the quoted price is

360100

nY( )

This is referred to as the discount rate

5.10 Treasury Bond FuturesPage 104

Cash price received by party with short position = Quoted futures price × Conversion factor + Accrued

interestEach contract is for the delivery of $100,000 face value

of bonds.Suppose the quoted futures price is 90-00, the conversion factor

is 1.3800 and the accrued interest at the time of delivery is $3 per $100 of face value:

90×1.38 + 3.00 = $127.2 per $100 of face value or $127,200

Conversion Factor

The conversion factor for a bond is approximately equal to the value of the bond on the assumption that the yield curve is flat at 6% with semiannual compounding

CBOTT-Bonds & T-Notes

Factors that affect the futures price:– Delivery can be made any time during the

delivery month– Any of a range of eligible bonds can be

delivered– The wild card play

• If Z is the quoted price of a Eurodollar futures contract, the value of one contract is

10,000[100-0.25(100-Z)]• A change of one basis point or 0.01 in a Eurodollar

futures quote corresponds to a contract price change of $25

5.11 Eurodollar Futures (Page 110)

Eurodollar Futures continued

• A Eurodollar futures contract is settled in cash• When it expires (on the third Wednesday of the

delivery month) Z is set equal to 100 minus the 90 day Eurodollar interest rate (actual/360) and all contracts are closed out

Forward Rates and Eurodollar Futures (Page 111)

• Eurodollar futures contracts last out to 10 years• For Eurodollar futures we cannot assume that the

forward rate equals the futures rate

Forward Rates and Eurodollar Futures continued

A "convexity adjustment" often made is

Forward rate = Futures rate

where is the time to maturity of the

futures contract, is the maturity of

the rate underlying the futures contract

(90 days later than ) and is the

standard deviation of the short rate changes

per year (typically is about

1

2

0 012

21 2

1

2

1

t t

t

t

t

. )

• Duration of a bond that provides cash flow c i at time t i is

where B is its price and y is its yield (continuously compounded)

• This leads to

tceBi

i

ni

yti

1

yDB

B

Duration

Duration Continued

• When the yield y is expressed with compounding m times per year

• The expression

is referred to as the “modified duration”

my

yBDB

1

D

y m1

Convexity

The convexity of a bond is defined as

CB

B

y

c t e

B

B

BD y C y

i iyt

i

n

i

1

1

2

2

2

2

1

2

so that

( )

Duration Matching

• This involves hedging against interest rate risk by matching the durations of assets and liabilities

• It provides protection against small parallel shifts in the zero curve

5.14 Duration-based hedging strategies

Hedging in Interest Rate Futures

• A mortgage lender who has agreed to loan money in the future at prices set today can hedge by selling those mortgages forward.

• It may be difficult to find a counterparty in the forward who wants the precise mix of risk, maturity, and size.

• It’s likely to be easier and cheaper to use interest rate futures contracts however.

Duration Hedging

• As an alternative to hedging with futures or forwards, one can hedge by matching the interest rate risk of assets with the interest rate risk of liabilities.

• Duration is the key to measuring interest rate risk.

• Duration measures the combined effect of maturity, coupon rate, and YTM on bond’s price sensitivity– Measure of the bond’s effective maturity– Measure of the average life of the security– Weighted average maturity of the bond’s cash

flows

Duration Hedging

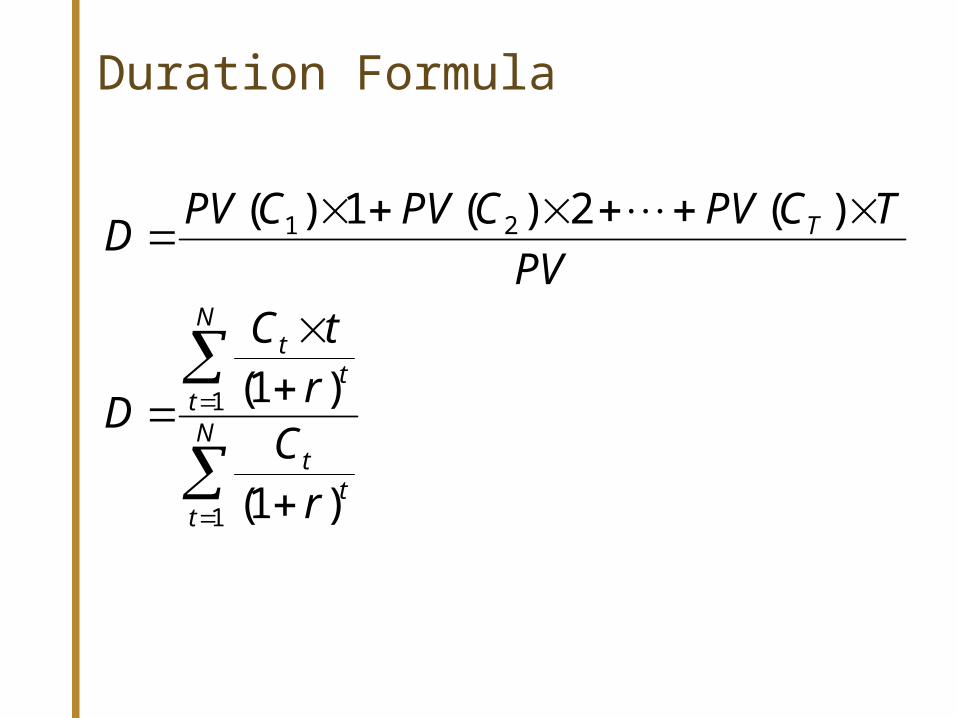

Duration Formula

N

tt

t

N

tt

t

T

r

Cr

tC

D

PV

TCPVCPVCPVD

1

1

21

)1(

)1(

)(2)(1)(

Calculating Duration

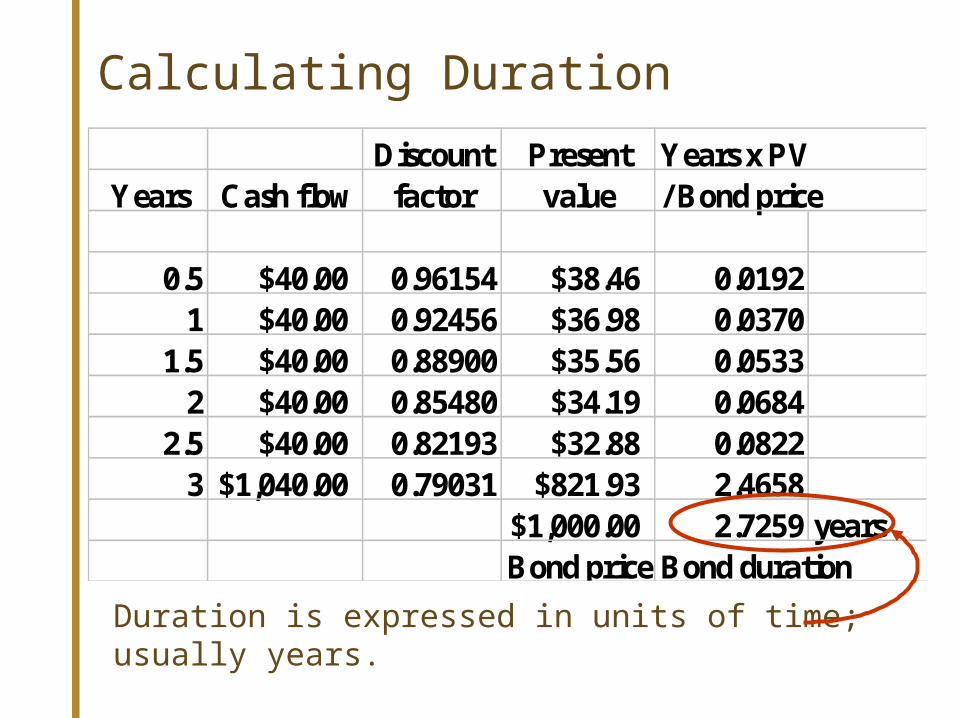

Calculate the duration of a three-year bond that pays a semi-annual coupon of $40, has a $1,000 par value when the YTM is 8% semiannually.

Discount Present Years x PVYears Cash flow factor value / Bond price

0.5 $40.00 0.96154 $38.46 0.01921 $40.00 0.92456 $36.98 0.0370

1.5 $40.00 0.88900 $35.56 0.05332 $40.00 0.85480 $34.19 0.0684

2.5 $40.00 0.82193 $32.88 0.08223 $1,040.00 0.79031 $821.93 2.4658

$1,000.00 2.7259 yearsBond price Bond duration

Calculating Duration

Duration is expressed in units of time; usually years.

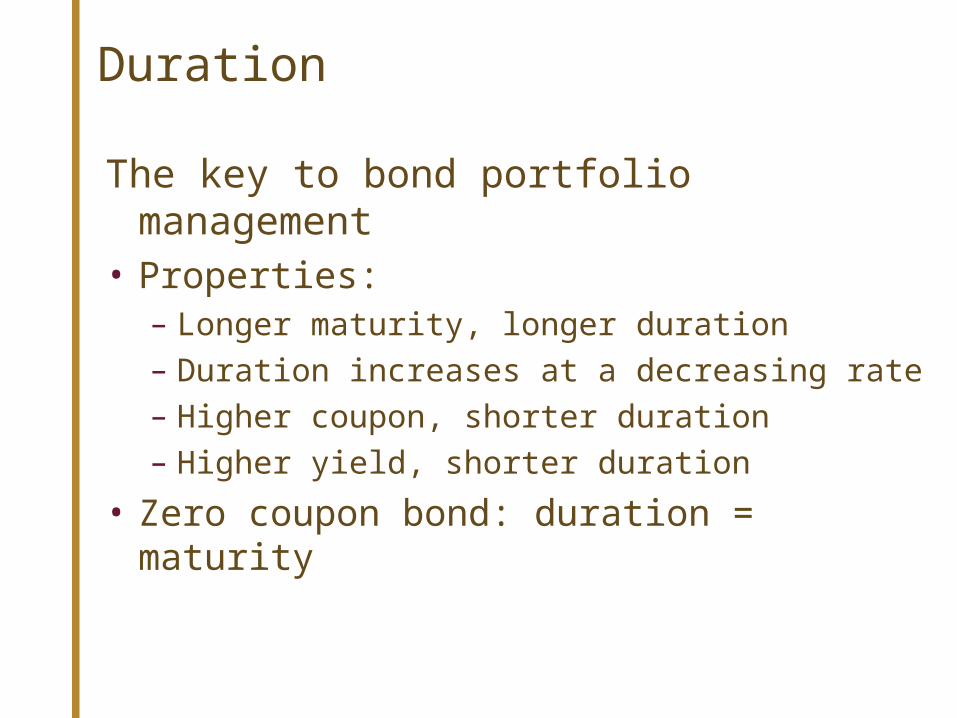

Duration

The key to bond portfolio management• Properties:

– Longer maturity, longer duration

– Duration increases at a decreasing rate

– Higher coupon, shorter duration

– Higher yield, shorter duration

• Zero coupon bond: duration = maturity

5.25

• On August 1 a portfolio manager has a bond portfolio worth $14 million. The duration of the portfolio in October will be 7.1 years.

• The December Treasury bond futures price is currently 91-12 and the cheapest-to-deliver bond will have a duration 0f 8.8 years at maturity

• How should the manager immunize the portfolio against changes in interest rates over the next two months?

5.25

• The treasurer should short Treasury bond futures contract.

• If bond prices go down, this futures position will provide offsetting gains.

• The number of contracts that should be shorted is

3.888.8375,91

1.7000,10