Embed Size (px)

Citation preview

Interest Capitalization Example(adopted from textbook)

1) First, identify when and how much the firm paidfor actual building expenditures during the year

Interest Capitalization Example

1) First, identify when and how much the firm paidfor actual building expenditures during the year

Jan 1: $210,000Mar 1: 300,000May 1: 540,000Dec 31: 450,000

Interest Capitalization Example

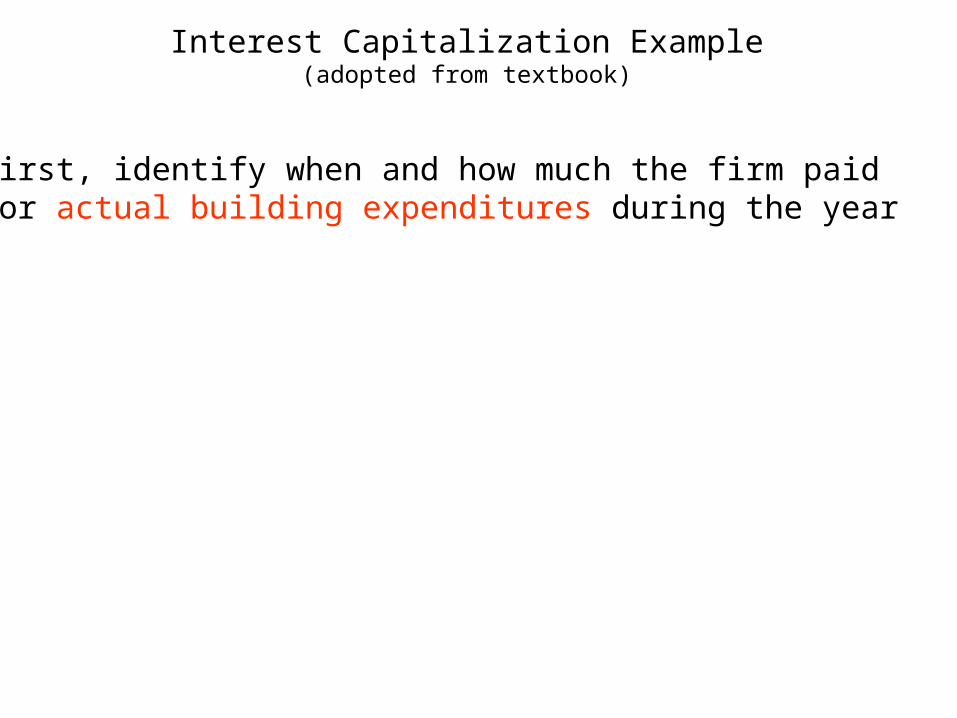

2) Second, compute weighted-average funding needs to make these expenditures

Jan 1: $210,000Mar 1: 300,000May 1: 540,000Dec 31: 450,000

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

This method assumes the firm borrows $210,000 for the full year then $300,000 for 10 months of the year then $540,000 for 8 months of the year, in order to make this payment schedule.

Jan 1: $210,000Mar 1: 300,000May 1: 540,000Dec 31: 450,000

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Note that this method also assumes that the firm borrows $450,000 on the last day of the year. This will not accrue interest during this particular year, so we will ignore it.

Interest Capitalization Example

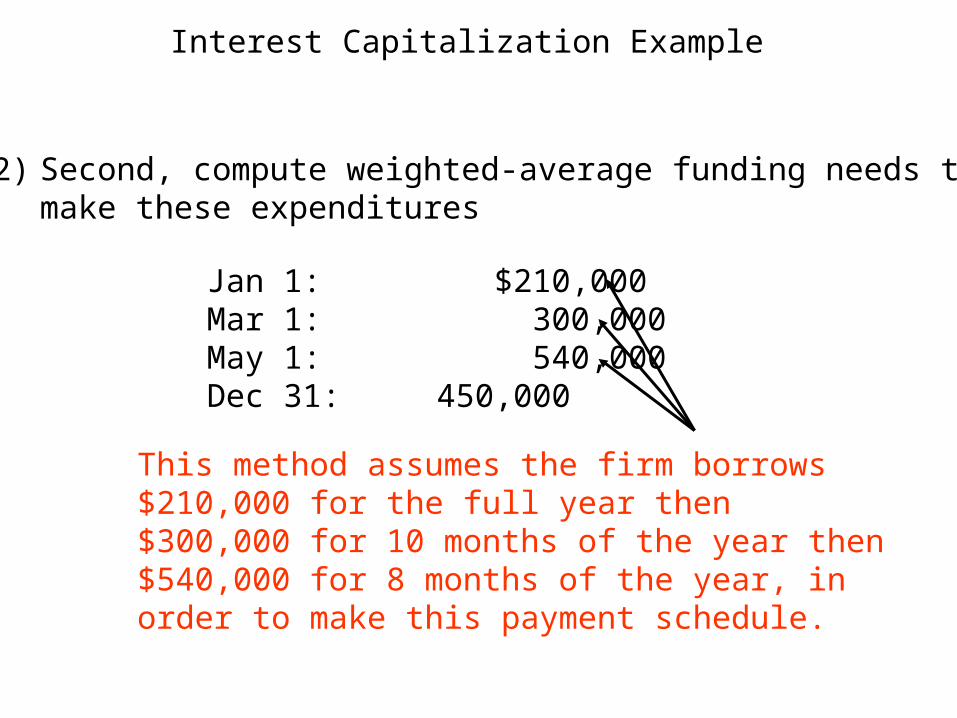

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000

Mar 1 300,000

May 1 540,000

Dec 31 450,000

Total

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000 12 mos./12 mos.

Mar 1 300,000

May 1 540,000

Dec 31 450,000

Total

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000 12/12 $210,000

Mar 1 300,000

May 1 540,000

Dec 31 450,000

Total

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000 12/12 $210,000

Mar 1 300,000 10/12 250,000

May 1 540,000

Dec 31 450,000

Total

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000 12/12 $210,000

Mar 1 300,000 10/12 250,000

May 1 540,000 8/12 360,000

Dec 31 450,000

Total

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000 12/12 $210,000

Mar 1 300,000 10/12 250,000

May 1 540,000 8/12 360,000

Dec 31 450,000 0/12 0

Total

Interest Capitalization Example

2) Second, compute weighted-average funding needs to make these expenditures

Date Amount Interest Accrual period

Weighted-Average

Funding Needs

Jan 1 $210,000 12/12 $210,000

Mar 1 300,000 10/12 250,000

May 1 540,000 8/12 360,000

Dec 31 450,000 0/12 0

Total 820,000

This represents the average amount of funding (borrowing) the company had to pay interest on, during the year, for the ongoing project.

Interest Capitalization Example

3) Third, map company’s existing debt to the amount of weighted average funding needs you just computed

Interest Capitalization Example

3) Third, map company’s existing debt to the amount of weighted average funding needs you just computed

December 31 debt outstanding:

• 15%, 3 year note to finance construction $750,000• 10%, 5 year note $550,000• 12%, 10 year bonds $600,000

Total funds available from debt $1,900,000

Interest Capitalization Example

3) Third, map company’s existing debt to the amount of weighted average funding needs you just computed

December 31 debt outstanding:

• 15%, 3 year note to finance construction $750,000• 10%, 5 year note $550,000• 12%, 10 year bonds $600,000

Construction funding needs = $820,000 (computed earlier)

Interest Capitalization Example

3) Third, map company’s existing debt to the amount of weighted average funding needs you just computed

December 31 debt outstanding:

• 15%, 3 year note to finance construction $750,000• 10%, 5 year note $550,000• 12%, 10 year bonds $600,000

Construction funding needs = $820,000 (computed earlier)

• $750,000 from 15% construction note

Interest Capitalization Example

3) Third, map company’s existing debt to the amount of weighted average funding needs you just computed

December 31 debt outstanding:

• 15%, 3 year note to finance construction $750,000• 10%, 5 year note $550,000• 12%, 10 year bonds $600,000

Construction funding needs = $820,000 (computed earlier)

• $750,000 from construction note• $70,000 remaining from both 10% note and 12% bonds

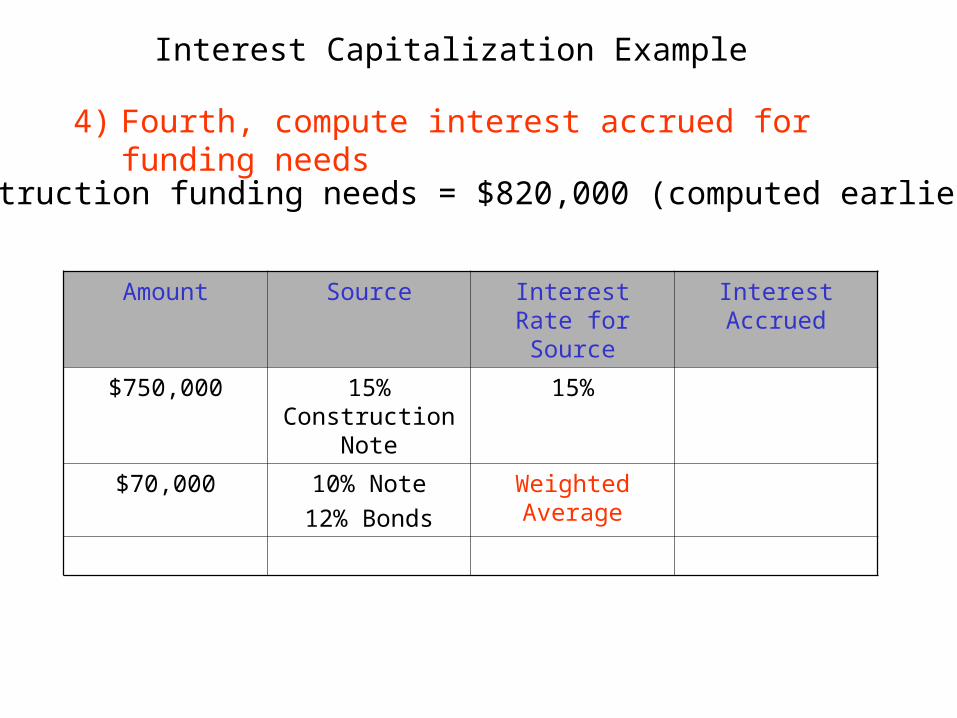

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

$70,000 10% Note

12% Bonds

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average:

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average: Debt Type Principal Interest

10% Note $550,000

12% Bonds

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average: Debt Type Principal Interest

10% Note $550,000 $55,000

12% Bonds

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average: Debt Type Principal Interest

10% Note $550,000 $55,000

12% Bonds $600,000

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average: Debt Type Principal Interest

10% Note $550,000 $55,000

12% Bonds $600,000 $72,000

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average: Debt Type Principal Interest

10% Note $550,000 $55,000

12% Bonds $600,000 $72,000

Totals $1,150,000 $127,000

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

Weighted Average: Debt Type Principal Interest

10% Note $550,000 $55,000

12% Bonds $600,000 $72,000

Totals $1,150,000 $127,000

127,0001,150,000

= 11.04%

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15%

$70,000 10% Note

12% Bonds

11.04%

Weighted Average:

127,0001,150,000

= 11.04%

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15% 112,500

$70,000 10% Note

12% Bonds

11.04% 7,728

Total $120,228

Interest Capitalization Example

4) Fourth, compute interest accrued for funding needs

Construction funding needs = $820,000 (computed earlier)

Amount Source Interest Rate for Source

Interest Accrued

$750,000 15% Construction Note

15% 112,500

$70,000 10% Note

12% Bonds

11.04% 7,728

Total $120,228

This is “avoidable” interest.

Interest Capitalization Example

5) Fifth, capitalize lesser of total interest paid by firm and “avoidable” interest

Interest Capitalization Example

5) Fifth, capitalize lesser of total interest paid by firm and “avoidable” interest

• Avoidable interest $120,228• Total interest paid:

Interest Capitalization Example

5) Fifth, capitalize lesser of total interest paid by firm and “avoidable” interest

• Avoidable interest $120,228• Total interest paid:

15% Construction Note

750,000 x 0.15 112,500

10% Note 550,000 x 0.10 55,000

12% Bonds 600,000 x 0.12 72,000

Total $239,500

Interest Capitalization Example

5) Fifth, capitalize lesser of total interest paid by firm and “avoidable” interest

• Avoidable interest $120,228• Total interest paid: $239,500