Embed Size (px)

Citation preview

Integration or Segmentation of the Canadian Stock Market: Evidence Based on the APTAuthor(s): George Koutoulas and Lawrence KryzanowskiSource: The Canadian Journal of Economics / Revue canadienne d'Economique, Vol. 27, No. 2(May, 1994), pp. 329-351Published by: Wiley on behalf of the Canadian Economics AssociationStable URL: http://www.jstor.org/stable/135750 .

Accessed: 04/06/2014 19:16

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and Canadian Economics Association are collaborating with JSTOR to digitize, preserve and extendaccess to The Canadian Journal of Economics / Revue canadienne d'Economique.

http://www.jstor.org

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation of the Canadian stock market: evidence based on the APT

GEORGE KOUTOULAS University of Lethbridge LAWRENCE KRYZANOWSKI Concordia University

Abstract. The domestic and international arbitrage pricing theories are modified to encom- pass the hypotheses that the Canadian and global North American equity markets are com- pletely or partly integrated (segmented). The exchange rate determination literature is used to identify potentially priced binational factors, and the sensitivities and factor prices are es- timated using non-linear SUR. The two equity markets are only partly integrated (segmented). Canadian stock returns are influenced by the pure domestic components of the term structure and lagged industrial production and by the pure international components of the differential in the Canada/u.s. leading indicators and the interest rate of eurodeposits.

Integration ou segmentation du marche boursier canadien: resultats bases sur la theorie des prix en situation d'arbitrage. Les auteurs modifient la theorie des prix en situation d'arbitrage au niveau national et international pour etudier les hypotheses que les marches boursiers canadien et nordamericain sont completement integr6s ou partiellement integres (i.e., segmentes). On utilise la litterature sur la determination des taux de change pour identifier certains facteurs binationaux potentiellement enregistr6s dans les prix, et les prix des facteurs sont calibres en utilisant des techniques de regression non-lineaire du type SUR.

Les deux marches sont seulement partiellement integres (i.e. segmentes). Les rendements sur les actions en bourse au Canada sont influences par les composantes purement domestiques de la structure des taux d'intret 'a diverses echeances et par le niveau de la production industrielle (avec un delai), mais aussi par les composantes purement internationales du diff6rentiel dans les indicateurs avanc6s entre le Canada et les Etats-Unis et les taux d'interet sur les Eurodepots.

We are grateful to two anonymous referees of this journal for their helpful comments. Financial support from FCAR (Fonds pour la formation de Chercheurs et l'Aide a la Recherche) and SSHRC

(Social Sciences and Humanities Research Council of Canada) is gratefully acknowledged. All remaining errors are the authors' responsibility.

Canadian Journal of Economics Revue canadienne d'Economique, XXVII, No. 2 May mai 1994. Printed in Canada Imprim6 au Canada

0008-4085 / 94 / 329-51 $1.50 ? Canadian Economics Association

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

330 George Koutoulas and Lawrence Kryzanowski

I. INTRODUCTION

National economies are becoming more internationalized through increased trade and the mutual cooperation of national governments to minimize impediments to the free flow of goods, services, and financial, physical, and human capital. For example, the members of the European community are currently attempting to integrate completely their economies into one large market economy. Casual em- piricism suggests that capital markets are being impacted and more countries are losing full control over their macroeconomic policy instruments (such as interest rate levels) as internationalization increases. The real implications for financial de- cisions of whether or not financial assets are priced in a national or international context are well known and need not be addressed further herein.

According to Jorion and Schwartz (1986, 604): 'integration imposes restrictions on the pricing of assets, by ruling out relationships between expected returns and purely domestic factors ... Complete segmentation implies that only national fac- tors ... should enter the pricing of assets.' Jorion and Schwartz used the Stehle (1977) methodology to test the Capital Asset Pricing Model (CAPM) and the Inter- national Capital Asset Pricing Model (ICAPM) developed and estimated by Solnik (1974a, 1974b) using monthly returns for a sample of only Canadian stocks.1 They concluded that the Canadian equity market is not completely integrated (or seg- mented) relative to a global North American equity market. Unlike the Stehle study, which used the Fama-MacBeth procedure to test if the u.s. equity markets are in- tegrated or segmented relative to a world equity market, Jorion and Schwartz used maximum likelihood estimation to eliminate the errors-in-variable problem associ- ated with the Fama-MacBeth procedure. Unfortunately, using the CAPM and ICAPM

requires that their respective unobservable domestic and world market portfolios be identifiable (Roll 1977). Furthermore, the CAPM and ICAPM do not allow for explicit and unambiguous tests of the very plausible hypotheses of partial integration and partial segmentation. This fact led Jorion and Schwartz (1986, 613) to conclude their paper as follows: 'The methodology could be extended to more general multi- factor asset pricing models, and it would be interesting to see whether purely na- tional factors also lead to rejection or integration.'

The deficiencies inherent in earlier empirical tests of capital market integra- tion and segmentation can be rectified by modifying the more general and less restrictive International Arbitrage Pricing Theory (IAPr). This model was developed by Solnik (1983),2 and tested by Cho, Eun, and Senbet (1986) using unidentified factors and factor analysis. Unfortunately, various methodological problems are associated with the use of factor analysis for 'identifying' the factors for tests of integration/segmentation using the IAPT. The number of factors identified as being

1 Owing to differences in consumption baskets across countries and exchange rate uncertainties, the ICAPM predicts that investors will hold different optimal portfolios, especially hedge portfolios (Adler and Dumas 1983).

2 The IAPT iS more general because it allows for more factors to influence returns. It is less restric- tive, since it is based on an arbitrage argument, not investor preferences.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 331

significant using the tests associated with factor analysis generally exceeds the number of priced factors (usually one).3 Measurement error in the factor load- ings results from the well-known two-pass procedure required for the construction of mimicking portfolios. As Burmeister and McElroy (1988) show, avoiding this source of measurement error positively affects the robustness of the resulting esti- mations. As shown by Anderson (1984) and Conway and Reinganum (1988), the properties of the estimates for the factor loadings are unknown if the errors are not jointly normal, the estimates of the factor loadings are not unique, the estimated factor scores (prices of risk) are not invariant to the way assets are partitioned to portfolios, and the first factor obtained from the first portfolio may not be the same as the first factor derived from the second portfolio. Furthermore, the use of factor analysis as a statistical tool without any simultaneous grounding in economic theory (intuition) may lead to non-interpretable and non-operational findings.

Gultekin, Gultekin, and Penati (1989) examine whether the Japanese and u.s. capital markets are integrated or segmented. The authors use a multi-index APM with identified factors (as well as factor analysis with unidentified factors) to test whether or not the enactment of the Foreign Exchange and Foreign Trade Control Law in 1980 had a significant impact on eliminating capital controls and thus assisted in integrating the financial markets of the two countries. Their findings support the segmentation hypothesis prior to the law's enactment and the integration hypothesis thereafter.

The purpose of this paper is three-fold: first, to generalize the Solnik (1983) IAPI and the Ross (1976) APT with domestic factors into comprehensive forms in which the competing hypotheses of complete and partial market integration and segmentation are nested within the two models; second, to identify the priced North American macroeconomic factors; and third, to test empirically whether or not the Canadian equity market is integrated or segmented relative to a global North American market.4 Unlike previous studies, the binational factors from the Frankel (1979) exchange rate determination model are used herein.

The remainder of the paper is organized as follows: Section ii derives the model and the hypotheses to be tested. Section iII describes the data. Section iv presents and discusses the empirical results. Section v concludes the paper.

3 The maximum likelihood ratio test tends to overstate the significant number of factors, and the x2 test not only reduces the marginal impact of a particular factor as the number of factors in- creases but does not provide any indication about the exactness of the model (Dhrymes, Friend, Gultekin, and Gultekin 1985). Chen (1983) reports that the number of priced factors is not in- variant to rotation. If the factor structure contains k factors, then the number of priced factors may be lower than k. Based on Monte Carlo simulations, Brown (1989) demonstrates that factor analysis understates the significance of the risk premia on factors beyond the first one (i.e., it is biased towards choosing one factor even if an exact k-factor model is prespecified). This con- firms the Kryzanowski and To (1983) and Trzcinka (1986) findings that at least one priced factor (mimicking portfolio) exists in the factor structure.

4 Testing whether the u.s. equity market is integrated or segmented relative to a North American market is an interesting topic which is left for further research. One possible scenario is that, while the Canadian equity market may be integrated relative to a North American market, the u.s. equity market may not be. This would be the case if the barriers that Canadian investors face within a North American market are non-binding, while the barriers that u.s. investors face within the same North American market are binding.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

332 George Koutoulas and Lawrence Kryzanowski

II. THEORETICAL DERIVATION OF THE IAPT-BASED TESTS

FOR INTEGRATION AND SEGMENTATION

The IAPT can be derived as follows. Suppose that the returns on the set of n assets follow the following international linear factor model (LFM):

R= E(R,,) + bilIlt + *+ biKIKt + Fit, t1; ,n (1)

where Rit is the random return of the ith asset for the period ending at time t; E(Rit) is the rational expectation of the random return of asset i given information at the beginning of time t; Ij is the zero-mean international common factorj; bij is the sensitivity of asset i to the jth factor; and Fi is the idiosyncratic risk of asset i, where E(Fi/Ij) = 0 for Vi, j, and E(F?) = o2 < oo.

If investors have homogeneous beliefs about the LFM, then non-arbitrage argu- ments dictate the following pricing equation:

E(Rit) = Aot + Albil + * * * + AKbiK, i=1,...,n, (2)

where Aj is the price of risk for undertaking the systematic risk of the factor j associated with holding asset i, and A0 is the risk-free rate. Solnik (1983) demon- strates that equation (2) is valid irrespective of the chosen numeraire (such as the Canadian dollar herein), provided that the exchange rates follow the k-factor model of equation (1). Substituting equation (2) into (1) yields the following approximate pricing system of n-equations:

K

kit ' Kot + E bij(ljt + Aj) + fit, _ .n (3) j=1 t ,....

Shanken (1985) refers to this approximate relationship as the arbitrage APT. Dybvig (1983) estimated a conservative bound of 0.015 per cent per month. As shown in Connor (1984), Wei (1988), and Burmeister and McElroy (1988), including the residual market factor (RMF) in (3) yields an exact APT. The RMF iS intended to capture the pervasive macrofactors (international and/or domestic) omitted from the system (3).

To test the integration hypothesis, the complete IAPT model described by equation (3) is augmented to allow for the possible influence and pricing of domestic factors, Dg. The augmented system becomes

K G

it= Aot + E bij(Ijt + Aj) + E Cig(Dgt + Og) + fit, (4) j=1 g=1

i=1, ... , T

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 333

where cig is the sensitivity of asset i to the domestic factor, g, and 0g is the price of risk associated with factor g.

The E(I1jt, Dgt) all may not be equal to zero, since one country's national factors may constitute some non-significant portion of the international factors. The corre- lation between the domestic and world market portfolios in tests of the segmented versus integrated hypothesis was first noted by Stehle (1977). His suggested so- lution, which was also used by Jorion and Schwartz (1986) and Gultekin et al. (1989), is to use projections to separate the pure national factors from the pure international factors. To do so, regressions of the form

Dgt = ato+alIt + vgtl g = 1, ..., G (5)

are run to obtain the fitted values, Vgt, for every g = 1, . . ., G. The fitted values, which are the components of the domestic factors that are orthogonal to the inter- national factors, can then be used as measures of the pure national factors.5 The Vgt replace the Dgt in equation (4) to obtain

K G

kit= Aot + E bi1(I + Aj) + E cig (Vgt + 0g) + sit, (6) j=1 g=1

t= 1, ..., T.

The hypothesis of complete integration can be tested by examining whether the 0g = 0, V g. Partial integration is easily tested by examining whether some of the Os are significantly different from zero.

To test the segmentation hypothesis, the domestic APT (where only national factors enter the LFM) is augmented to allow for the possible influence and pricing of international factors as follows:

G K

kit = Aot + E cig(Dgt + Og) + E bij(Ujt + Ai) + Htit, (7) g=1 j=1

n

t=1, ..., T

where the Ujt are the pure international factors. The following regressions,

iit =0o+ 6Igt+Uit, j = 1, ..., K, (8)

are run to obtain the fitted values Uit, Vj. The hypothesis of complete segmentation (i.e., Ho: Aj = 0, V j), and the hypothesis of partial segmentation (where some of the As are different than zero) is easily tested.

5 As in any two-step procedure, orthogonalization in the first step results in an errors-in-variables problem in the implicit second-pass regression estimation. As a result, the reported t-statistics are biased towards significance (Bodurtha 1986).

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

334 George Koutoulas and Lawrence Kryzanowski

Theoretically, if the modified IAPr given by the system of equations (6) pre- dicts that the Canadian equity market is completely integrated relative to a North American equity market (i.e., 0g = 0 for every g = 1, . .. , G and some Aj not equal to zero), then the domestic APT given by the system of equations (7) should reject both the complete and the partial segmentation hypotheses (i.e, all or some of the Ajs should be significant and all Ogs should be equal to zero). Conversely, if the domestic Avr predicts that the Canadian equity market is completely seg- mented relative to a North American equity market, then the IAPT should reject both the complete and partial integration hypotheses. If the IAPT predicts that the Canadian equity market is partly integrated relative to a North American equity market, however, then the domestic APT should also predict the partial segmenta- tion of the Canadian equity market relative to a North American equity market. Thus, the two models (IAPT and the domestic APT) are competitors for modelling asset prices only if the extreme hypothesis of either complete market integration or segmentation is true. Otherwise, the two models are equivalent. Therefore, past studies that include variables (like the exchange rate and interest rates on eurode- posit rates) are implicitly assuming partial integration. For example, Brown and Otsuki (1989) modelled the Japanese equity market using these variables because of the internalization of the Japanese economy (primarily due to its large export market).6 The international APT and domestic APT models given by the system of equations (6) and (7), respectively, are estimated herein using the iterated non-linear seemingly unrelated regression (NSUR) technique.7 The NSUR method assumes a full error covariance matrix. As shown by Gallant (1985), the NSUR estimator is strongly consistent and asymptotically normal even in the absence of normally distributed errors. If errors are normally distributed, this estimator is also maximum likelihood. In our application, n = 50 and T = 228.

Tests of any hypotheses that use asset pricing models (or any theoretical model) are joint tests of at least three hypotheses. The first hypothesis is the validity of the model (which in our case is supported by considerable empirical evidence), the second is the validity of the actual hypothesis being tested, and the third is the assumption that the computed test-statistics are drawn from the hypothesized distri- butions (which is a problem using factor analysis). In addition, since the APT does not specify which factors should enter the LFM (which is somewhat rectified herein by using those factors in the Frankel 1979 exchange rate determination model), the additional hypothesis of whether the chosen macrofactors are the true factors is also jointly tested. Therefore, while a specific set of tests may accept or reject segmentation or integration, the inference may actually be due to the failure of any

6 Other studies that include international factors in the APr include Bodurtha et al. (1989) for u.s. stocks and Hamao (1989) for Japanese stocks.

7 By estimating models (6) and (7) using NSUR, both the factor betas and prices of risk are jointly estimated. This avoids the classic two-step Fama-MacBeth procedure where the betas are first estimated and then the prices of risk are estimated. As is well known, the two-step procedure introduces an error-in-variables problem into the estimation. As shown by Shanken (1992), as long as the factors are serially independent, joint estimation procedures automatically adjust for the errors-in-variable problem.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 335

one or combination of the other implicit maintained hypotheses. Unfortunately, no easy solution exists for this problem, since testing of each hypothesis separately is virtually impossible. By performing multiple statistical tests and letting the data choose from many intuitively plausible macrofactors, the researcher hopes to min- imize the possibility of failure coming from the falsity of the implicit maintained hypotheses.

To estimate the system of equations in (6) (and in (7)), the variables that con- stitute the international factors, 1js (and the national factors, Dg), must be deter- mined. Since general factors are expected to come from the variables that affect the macroeconomy, some of the potential candidates for the domestic factors are output, interest rates, money supply, and inflation. To identify potential binational factors, recall that the IAPr is valid only if the exchange rates of the countries involved and the returns of the equities follow the same linear factor structure. Therefore, a priori information on the structure of exchange rates can be used to identify potential 'international' (binational) common factors. Since the IAPT described by equations (1) and (2) is derived under the hypothesis of complete market integra- tion, the common factors included in (1) and priced by (2) are 'international' (or binational) factors if the integration versus segmentation of the Canadian equity market relative to the North American market is being examined.

These binational factors can be determined explicitly from the following general form of an exchange rate determination model:

M

St = Edq(Xqt -Xqt) + St, (9) q=1

where st is the log of the spot rate; Xqt and Xq*t are the logs of the qth domestic and foreign macroeconomic variables, respectively; dq is the sensitivity coefficient of the spot rate to the difference of the qth domestic and foreign macroeconomic variables; and wt is an estimation error. Equation (9) encompasses all significant exchange rate models as different restrictions on the coefficients. In Frankel (1979), equation (9) takes the form,

St = (mt - m*) - 4(Yt - y) - ca(rt - rt) + /(irt -t ir) + Ut, (10)

where st is the log of the spot rate; mt and m* are the logs of the money supply at home (Canada) and abroad (u.s.), respectively; yt and y7 are the logs of output at home and abroad, respectively; rt and rt* are the logs of one plus the domestic and foreign interest rates, respectively; Filt and 117 are the current rates of expected long-run inflation at home and abroad, respectively; and Ut is an estimation error.

Taking conditional expectations of equation (9) at time t yields

M

Et(st) = > dqEt(Xqt - (11t) q=1

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

336 George Koutoulas and Lawrence Kryzanowski

Subtracting equation (11) from equation (9) yields

M

St = Et(st) + E dq[(Xt -Xt)-Et(Xt -Xt)] + t. (12) q=1

Equation (11) is the LFM for the exchange rate of an integrated economy where the binational common factors are the terms specified in the brackets. These factors are mean zero, and they conform to previous expectations of what kinds of variables should constitute the binational factors. Projections to filter out the pure (bi)national factors are required, since the national and binational factors are correlated.

Based on Frankel (1979), some of the binational factors, which can be used, are the following innovations:

Flt = [(mt - mt) - Et(mt - mt)], F2t = [(yt - yt) - Et(yt - yt)]

F3t = [(rt - rt)- Et(rt - rt)], F4t = [(lrt - 7r') - Et(irt - r*)].

III. DATA

The monthly rates of return on all stocks traded on the Toronto Stock Exchange (TSE) from January 1969 through March 1988 are used herein to calculate the returns on fifty size-ranked portfolios. These portfolios are used in order to gain the maximum dispersion in returns (Poon and Taylor 1991), since small-cap firms have higher betas and average returns than their larger counterparts. Thus, using a large number of portfolios tends to increase dispersion in betas, which leads to more precise estimates.

The macroeconomic factors used to obtain the innovations which affect stock returns are all taken from Statistics Canada's CANSIM Mini Base. All the variables used herein are defined in table 1. The growth rates of most variables (except for the interest rate variables) are calculated by taking the first differences in their logarithms. The innovations are estimated as the forecast errors of a multivariate model fitted for each of the macroeconomic series using Akaike's (1976) mul- tivariate state-space procedure. Brown and Otsuki (1989) and Kryzanowski and Zhang (1992) have utilized this innovative method to produce forecast errors that are mean zero and serially uncorrelated.

Since no widely accepted theories exist for linking stock market performance and specific economic variables, economic intuition, findings from past empirical studies, and frequently published macroeconomic variables in the popular business media are used to determine which macroeconomic variables might affect stock returns. Innovations for two groups of macroeconomic variables, which are designed to capture the real, monetary and financial sectors of the domestic (Canadian) and international (North American) economies, are estimated. The first group of national factors, which capture the real sector of the Canadian economy, includes industrial production, gross domestic product and the Canadian composite leading index. The

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 337

TABLE 1 Macroeconomic variables

Nationala Description

EW Equally-weighted index of all stocks listed on the Toronto Stock Exchange (TSE)

GDP Gross domestic product INDEX Index of 10 leading inidicators INDUS Industrial production INFLAT Change in the Consumer Price Index (CPI) LINDUS The lag of industrial production MONEY Money supply (Ml) PREM Yield on long-teim corporate bonds less the yield

on long-term government bonds TERM Yield on long-term government bonds less

the yield on 91-day Treasury bills TSE300 The Toronto Stock Exchange 300 stock index

Internationalb

DINDUS Differential in Can/u.s. industrial production DINDEX Differential in Can/u.s. leading indices DINFLAT Differential in Can/u.s. inflation rates DLINDUS The lag of DINDUS

DMONEY Differential in Can/u.s. money supply DPREM Differential in Can/u.s. risk premium DTERM Differential in Can/u.s. term structure EURO Interest rate on eurodollar deposits in London SP500 Standard and Poor's 500 stock index

a The 'pure' domestic component of each of these variables is indi- cated by the addition of a 'D' to the designation for the domestic variable. For example, the 'pure' domestic component of INDEX iS

denoted by INDEXD.

b The 'pure' international component of each of these variables is indicated by the addition of an 'I' to the designation for the inter- national variable. For example, the 'pure' international component of DINDEX is denoted by DINDEXI.

monetary sector of the Canadian economy is captured by the money supply and inflation (as measured by the change in the Consumer Price Index or cpi). The financial sector is captured by different interest rate variables, such as the yields on long-term Canada's, long-term corporates and ninety-one-day Treasury bills. These yields are used to create two additional variables, the term structure variable, TERM,

which is defined as the difference in the yields on long-term government bonds and ninety-one-day Treasury bills, and the risk premium variable, RISK, which is defined as the difference between the yields on long-term corporate bonds and long-term government bonds.

Except for Kryzanowski and Zhang (1992), all previous studies have used the TERM and RISK variables directly as innovations. For example, Chen, Roll, and Ross (1986) assume that both of these variables are sufficiently uncorrelated because they are differences in interest rates and therefore can be considered innovations.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

338 George Koutoulas and Lawrence Kryzanowski

These variables are not mean zero, however, because the term structure is upward sloping more often than it is downward sloping, and the risk premium for holding the more risky corporate bonds instead of the less risky government bonds is always positive. Therefore, these variables do not satisfy the mean-zero property of proper innovations. McElroy and Burmeister (1988) used the term structure variable directly as an innovation because the mean of this variable was equal to zero in their sample. They modified the risk premium variable by adding a constant to make the sample mean equal to zero. Both of these variables are fitted herein using the state-space procedure (Akaike 1976) to determine their innovations.

The second group of variables contains 'international' (binational) macroeco- nomic factors which are constructed from both Canadian and u.s. macroeconomic variables. The only variable that is truly international is the interest rate offered on three-month u.s. dollar deposits in London. This eurorate, which is intended to capture term structure effects, was used by Gultekin, Gultekin, and Penati (1989). The other 'international' variables are constructs similar to the ones used in tests of exchange rate determination. The differentials in the growth rates of the Cana- dian and u.s. composite leading indices and industrial production are binational factors that capture real economic activity in North America. The binational mon- etary sector is captured by the growth differentials in the Canadian and u.s. money supplies and inflation rates. The financial sector is captured by the differentials in the term structure and risk premium variables of the two countries. Each of these differentials in the macroeconomic variables and the eurorate is fitted using the state-space procedure to obtain the binational innovations.

The interpretation of the binational innovations is straightforward, as is demon- strated by the following example. Suppose Xt and Xt* are the growth rates at time t of the Canadian and u.s. macroeconomic variable, respectively. The binational factor is DXt = (Xt - Xt*). Fitting this variable with the state-space procedure yields the following binational innovation:

[DXt - Et(DXt)] = (Xt - Xt*) - E(Xt - Xt*) = (Xt - E(Xt)) - (Xt - E(Xt*)),

where Et( ) is the conditional expectation operator based on the information at time t. This binational innovation is just the differential innovation of Xt and Xt* across the two countries.

Summary statistics for the innovations are reported in table 2. The t-statistics for testing the null hypothesis that the innovations are mean zero indicate that none of the macroeconomic innovations has non-zero means. The Kolmogorov D-statistics for testing the null hypothesis of normally distributed innovations is rejected for only the following four variables: term structure, term structure differential, money differential, and the eurorate. Fisher's kappa-test statistics and the Ljung and Box Q-statistics for testing the null hypothesis that the innovations are white noise are rejected for only one variable; namely, the differential in the Canadian and u.s. money supply.

To ensure that each domestic factor does not contain information embodied in any of the other domestic factors, a series of sequential regressions is performed.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 339

TABLE 2 Summary statistics for the innovations based on the multivariate state-space procedure

Variable Mean Std Dev. t: Mean = oa D: normalb k: Fisherc Q(6)C

GDP -4.73E-05 0.005873 -0.1218 0.03397 6.7242 8.93 INDEX 8.06E-06 0.010601 0.0115 0.03351 7.0368 4.53 INDUS 0.000211 0.012002 0.0267 0.05486 6.0326 7.19 INFLAT -4.75E-05 0.003269 -0.2205 0.04966 6.8520 9.66 MONEY 4.81E-06 0.013579 0.0054 0.06081 6.6306 3.51 PREM 0.000014 0.002058 0.1049 0.08874 7.7895 8.38 TERM 0.000210 0.007439 0.4287 0.11153 4.4487 6.38 DINDEX 1.93E-06 0.008655 0.0034 0.04771 5.7827 3.62 DINDUS -4.30E-06 0.011832 -0.0055 0.04580 7.3583 5.82 DINFLAT 0.000010 0.003663 0.0435 0.04302 6.0130 4.19 DMONEY 0.000259 0.036335 0.1081 0.13206 7.6717 5.72 DPREM 0.000012 0.001995 0.0956 0.06970 6.9337 1.62 DTERM 0.000325 0.009378 0.5247 0.10231 5.4066 6.95 REURO -.000933 0.003269 -0.2205 0.04966 5.0303 0.78

a The null hypothesis of zero mean cannot be rejected for all variables at the 0.10 significance level.

b The null hypothesis of normality cannot be rejected for all but the TERM, DTERM and DMONEY variables at the 0.10 significance level.

c The null hypothesis of white noise cannot be rejected for all the variables except for PREM, DMONEY, DINDUS and INDEX at the 0.10 significance level (using the Fisher k- statistic). The Ljung and Box Q-statistics indicate that the null is not rejected for any of the variables.

Specifically, the second domestic factor is regressed against the first domestic factor and the residual from this regression is used as the second factor. Then the third domestic factor is the residual of a regression of itself on the first and second domestic factors. The same procedure is followed for the rest of the domestic factors to get orthogonalized domestic factors by construction. The same methodology is followed to orthogonalize each of the international factors to the other international factors. Then equations (6) and (7) are estimated using the orthogonalized domestic and international factors to determine the pure domestic component of each of the domestic factors and the pure international component of each of the international factors. Except for a few subperiods, the results are robust when the factors are not completely orthogonalized, probably because the innovations from using the state-space procedure have nearly zero correlations.

IV. EMPIRICAL RESULTS

1. Selection of the macroeconomic variables To determine which macroeconomic innovations enter the international LFM, a series of linear regressions is performed. In these regressions, the dependent variables are the total returns on the Toronto Stock Exchange 300 stock composite index (TSE300), the equally weighted (Ew), and value-weighted (vw) stock indices of all

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

340 George Koutoulas and Lawrence Kryzanowski

the stocks listed on the TSE, and the fifty equally weighted size-ranked portfolios. The independent variables are the innovations of the international factors identified in table 1. Although the LFM states that stock returns at time t should be affected only by the macroeconomic innovations at time t, lagged values are also used as independent variables in the stepwise regressions. As noted by Chen, Roll, and Ross (1986), this procedure may capture non-synchronous information arrival, where the information for some variables may lag equity returns by one month. The variables that are significant for most of the portfolios and the market indices are selected as being the binational macroeconomic factors.

The selected international LFMS for the three market indices are reported in table 3. The last column of the table reports the average parameter values of the LFM for the fifty size-ranked portfolios. The binational factors that enter the LFMS

significantly for the sample period from March 1969 to March 1988 are as follows: the lag of the differential in the industrial production innovations of Canada and the United States (DLINDEX), the differential in the composite leading indices (DINDEX),

and the interest rate innovation on eurodollar deposits (EURO). These factors together explain approximately 15 to 20 per cent of the variation in the returns on the market indices and 10 per cent of the variation in the returns on the fifty portfolios. The t-values indicate that these three variables are strongly significant individually in the regressions. Also, the F-values indicate that the overall regressions are very significant.

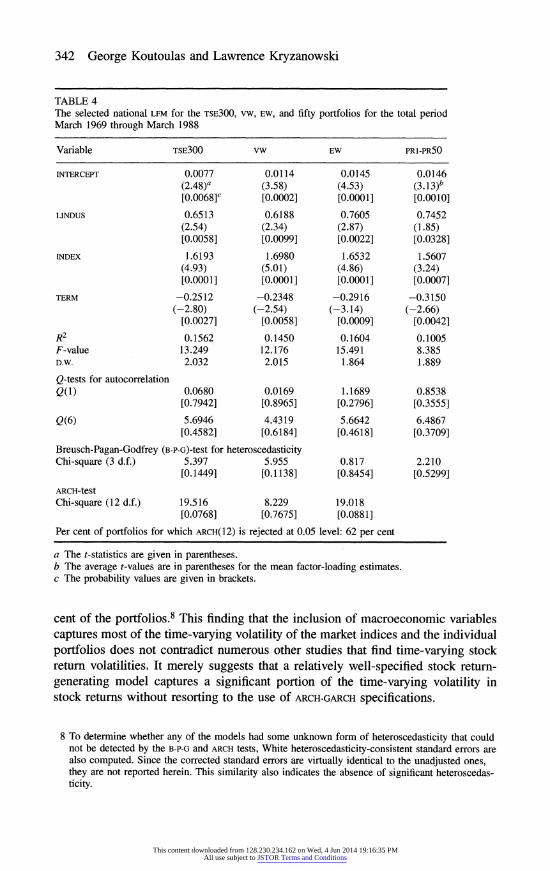

The domestic LFM for the three indices and the mean parameter estimates of the LFMS for the fifty portfolios are reported in table 4. Based on the mean t-values, the three significant domestic factors are the lag of industrial production (LINDUS),

the term structure (TERM), and the Canadian leading index (INDEX). These factors combined explain approximately 16 per cent of the variation in the returns on the market indices and 10 per cent for the portfolio returns.

Since an international factor may be significant in the international LFM because of its domestic component and a domestic factor may be significant in the domestic LFM because of its international component, the LFMS for the market indices and the fifty size-ranked portfolios are re-estimated with each factor decomposed into its pure component. The results from these regressions, which are reported in table 5, indicate that the pure international component of the term structure is insignificant in the LFMS for the market indices and the fifty size-ranked portfolios. Kryzanowski and Zhang (1992) found that, while the term structure variable is priced in the Canadian equity market over the period from February 1956 to March 1988, its beta became insignificant when the LFM with the APT restrictions was estimated. One possible reason may be the fact that only the domestic component of the term structure is significant and priced, while its international component is irrelevant for pricing Canadian stocks. Inclusion of both components in the LFM may have an overall diluting effect on the significance of the term structure beta coefficient. The other variable, which is significant at the market level but insignificant at the portfolio level, is the pure international component of the differential in industrial production. The D.W. (Durbin-Watson) statistics of these regressions are close to

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 341

TABLE 3 The selected international LFM for the TSE300, vw, EW, and fifty portfolios for the total period March 1969 through March 1988

Variable TSE300 VW EW PR1-PR50

INTERCEPT 0.0062 0.0100 0.0127 0.0116 (2.08)a (3.19) (4.01) (2.73)b [0.0190]c [0.0008] [0.0001] [0.0034]

DLINDUS 0.6655 0.5836 0.5760 0.5944 (2.66) (2.20) (2.14) (1.65) [0.0042] [0.0143] [0.0165] [0.0502]

DINDEX 1.6750 1.5705 1.6797 1.7636 (4.89) (4.33) (4.57) (3.24) [0.0001] [0.0001] [0.0001] [0.0007]

REURO -1.8571 -1.6018 -1.5394 -1.2869 (-5.21) (-4.25) (-4.03) (-2.36)

[0.0001] [0.0001] [0.0001] [0.0095]

R2 0.2059 0.1566 0.1569 0.0983 F-value 19.441 13.928 13.959 8.152 D.W. 1.893 1.953 1.871 1.824

Q-tests for autocorrelation Q(1) 0.6040 0.1069 1.8079 0.7072

[0.4370] [0.7437] [0.1787] [0.40031

Q(6) 6.5500 2.5140 6.9660 5.2120 [0.3644] [0.8669] [0.3240] [0.5169]

Breusch-Pagan-Godfrey (B-P-G)-test for heteroscedasticity Chi-square (3 d.f.) 3.789 4.773 3.066 3.329

[0.2852] [0.1892] [0.2544] [0.3436]

ARCH(1 2)-test Chi-square (12 d.f.) 18.246 6.844 7.197

[0.1084] [0.8677] [0.8443]

Per cent of portfolios for which ARCH(12) is rejected at 0.05 level: 60 per cent

a The t-statistics are given in parentheses. b The average t-values are in parentheses for the mean factor-loading estimates. c The probability values are given in brackets.

two, indicating no apparent misspecification due to serial correlation. The overall power of the regressions is very strong, as evidenced by the high F-statistics.

For all the models in tables 3, 4, and 5 there is no evidence of serial correlation or heteroscedasticity in the error terms at traditional significance levels based on the D.W. statistics, the Ljung and Box Q-statistics, and the Breusch-Pagan-Godfrey (B-P-G) test-statistics. The significance of ARcH(12) cannot be accepted at the 0.05 level for the international LFM for the TSE300, VW, EW, and 60 per cent of the portfolios. For the domestic LFM, ARCH(12) errors cannot be accepted for all three market indices and for 62 per cent of the portfolios at the 0.05 level. The same holds true for the complete LFM, except that ARcH(12) cannot be accepted for 49 per

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

342 George Koutoulas and Lawrence Kryzanowski

TABLE 4 The selected national LFM for the TSE300, vw, EW, and fifty portfolios for the total period March 1969 through March 1988

Variable TSE300 VW EW PR1-PR50

INTERCEPT 0.0077 0.0114 0.0145 0.0146 (2.48)a (3.58) (4.53) (3.13)b [0.0068]c [0.0002] [0.0001] [0.0010]

LINDUS 0.6513 0.6188 0.7605 0.7452 (2.54) (2.34) (2.87) (1.85) [0.0058] [0.0099] [0.0022] [0.0328]

INDEX 1.6193 1.6980 1.6532 1.5607 (4.93) (5.01) (4.86) (3.24) [0.0001] [0.0001] [0.0001] [0.0007]

TERM -0.2512 -0.2348 -0.2916 -0.3150 (-2.80) (-2.54) (-3.14) (-2.66)

[0.0027] [0.0058] [0.0009] [0.0042]

R2 0.1562 0.1450 0.1604 0.1005 F-value 13.249 12.176 15.491 8.385 D.W. 2.032 2.015 1.864 1.889

Q-tests for autocorrelation Q(1) 0.0680 0.0169 1.1689 0.8538

[0.7942] [0.8965] [0.2796] [0.3555]

Q(6) 5.6946 4.4319 5.6642 6.4867 [0.4582] [0.6184] [0.4618] [0.3709]

Breusch-Pagan-Godfrey (B-P-G)-test for heteroscedasticity Chi-square (3 d.f.) 5.397 5.955 0.817 2.210

[0.14491 [0.1138] [0.8454] [0.5299]

ARCH-test

Chi-square (12 d.f.) 19.516 8.229 19.018 [0.0768] [0.7675] [0.0881]

Per cent of portfolios for which ARCH(12) is rejected at 0.05 level: 62 per cent

a The t-statistics are given in parentheses. b The average t-values are in parentheses for the mean factor-loading estimates. c The probability values are given in brackets.

cent of the portfolios.8 This finding that the inclusion of macroeconomic variables captures most of the time-varying volatility of the market indices and the individual portfolios does not contradict numerous other studies that find time-varying stock return volatilities, It merely suggests that a relatively well-specified stock return- generating model captures a significant portion of the time-varying volatility in stock returns without resorting to the use of ARCH-GARCH specifications.

8 To determine whether any of the models had some unknown form of heteroscedasticity that could not be detected by the B-P-G and ARCH tests, White heteroscedasticity-consistent standard errors are also computed. Since the corrected standard errors are virtually identical to the unadjusted ones, they are not reported herein. This similarity also indicates the absence of significant heteroscedas- ticity.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 343

TABLE 5 The complete LFM for the three market indices and the fifty size-ranked portfolios for the total period March 1969 through March 1988

Variable TSE300 VW EW PR1-PR50

INTERCEPT 0.0058 0.0098 0.0122 0.0120 (2.14)a (3.35) (4.16) (2.86)b [0.0165]c [0.0005] [0.0001] [0.0023]

DLINDUSI 1.3073 1.1479 1.1201 1.1651 (2.85) (2.36) (2.28) (1.31) [0.0024] [0.0097] [0.0117] [0.0957]

LINDUSD 1.2147 1.1476 1.4368 1.8363 (2.68) (2.38) (2.96) (2.47) [0.0039] [0.0089] [0.0017] [0.0071]

DINDEXI 1.6274 1.5278 1.6322 1.1295 (5.14) (4-54) (4.83) (3.25) [0.0001] [0.0001] [0.0001] [0.0007]

INDEXD 1.5776 1.5287 1.6322 1.5379 (5.39) (5.34) (5.20) (3.09) [0.0001] [0.0001] [0.0001] [0.001 1]

DTERMI -0.1205 -0.0941 -0.1910 -0.2369 (-1.21) (-0.892) (-1.79) (-1.38)

[0.1128] [0.1868] [0.0369] [0.0845]

TERMD -0.3511 -0.3472 -0.3493 -0.6457 (-3.27) (-3.04) (-4.40) (-2.86)

[0.0006] [0.0013] [0.0001] [0.0023]

REURO -1.8652 -1.6104 -1.5483 -1.5905 (-5.69) (-4.62) (-4.40) (-2.78)

[0.0001] [0.0001] [0.0001] [0.0029]

R2 0.3390 0.2906 0.2987 0.1679 F-value 16.192 12.935 13.446 6.053 D.W. 2.078 2.108 1.871 1.949

Q-tests for autocorrelation Q(1) 0.3882 0.7077 0.8937 0.2390

[0.5332] [0.4002] [0.3445] [0.6249]

Q(6) 7.5762 3.5200 7.3582 7.5670 [0.2708] [0.7413] [0.2889] [0.2715]

Breusch-Pagan-Godfrey (B-P-G)-test for heteroscedasticity Chi-square (7 d.f.) 10.375 8.538 9.824 4.607

[0.1683] [0.2875] [0.1987] [0.2029]

ARCH-test Chi-square (12 d.f.) 15.906 6.455 10.284

[0.1956] [0.8914] [0.5911]

Per cent of portfolios for which ARCH(12) is rejected at 0.05 level: 49 per cent

a The t-statistics are given in parentheses. b The average t-values are in parentheses for the mean factor-loading estimates. c The probability values are given in brackets.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

344 George Koutoulas and Lawrence Kryzanowski

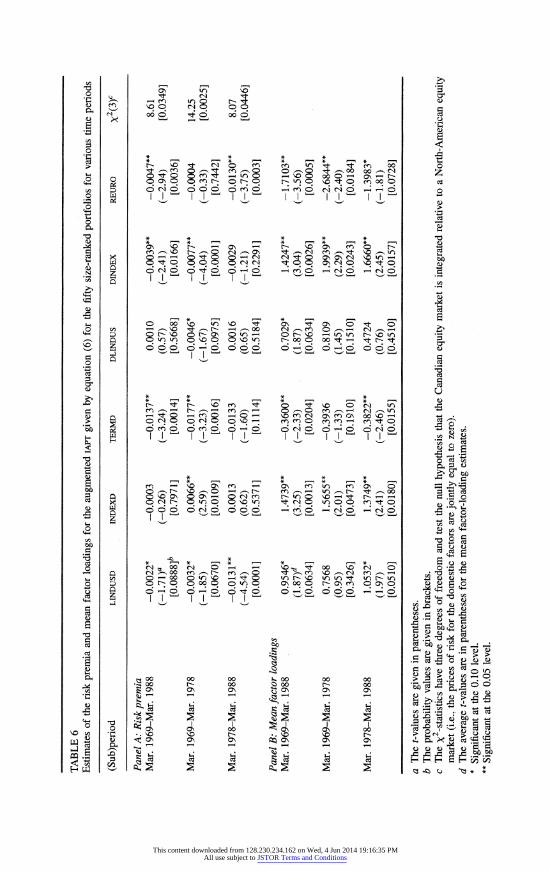

2. Tests of the segmentation and integration hypotheses The estimated risk premia and mean factor loadings for the augmented IAPT given by equation (6) are reported in table 6. The three international factors, REURO, DINDEX,

and DLINDUS and the domestic components of LINDUS, INDEX, and TERM (denoted by LINDUSD, INDEXD, and TERMD, respectively) are the independent variables of the model, and the fifty equally weighted size-ranked portfolios are the dependent vari- ables. The NSUR estimates of the risk premia are reported in panel A. For the period from March 1969 to March 1988 two international factors, REURO and DINDEX, and the domestic components of two domestic factors, LINDUSD and TERMD, are signifi- cant. Therefore, the complete integration hypothesis, Ho (i.e., some 'international' factor(s) is (are) priced and all pure domestic factors are not priced), is rejected in favour of the partial integration hypothesis where some 'international' factor(s) is (are) priced and at least one pure domestic factor is priced.9 To test whether the Canadian equity market is becoming more integrated relative to the North Amer- ican equity market, subperiod estimates of the risk premia for the augmented IAPr

are presented. For both subperiods, the Canadian equity market was only partly integrated relative to a North American equity market, since some of the binational and some of the domestic risks were priced. Interestingly, the risk premia appear to be time-varying. Overall, the partial integration hypothesis cannot be rejected for the Canadian equity market.

The mean factor loadings for the augmented IAPT are reported in panel B of table 6. All the factors are significant. Subperiod estimates of the factor loadings indicate that the betas are time-varying. This result confirms what has already been found in the literature using factor analysis (e.g., Cho and Taylor 1987).

The estimated risk premia and mean factor loadings for the augmented IAPr with the residual market included as an additional factor, which is intended to capture the influence of any omitted domestic and international macroeconomic variables, are reported in panels A and B, respectively, of table 7.10 For the entire period, the estimates of the risk premia for the domestic component of the term structure vari- able, TERMD, and the international factors, DINDEX and REURO, are significant. This indicates that the partial integration hypothesis cannot be rejected for the Canadian equity market. The residual market factor (RMF) is found to be significant for the subperiod from March 1969 to March 1978. This finding indicates that there are some omitted domestic and/or international factors which are priced. The entire sample estimates of the mean factor loadings for the augmented IAPT with the RMF

9 The prediction that perfect market segmentation or perfect integration is fully rejected is valid if the pure domestic and pure international factors do not capture any omitted international and domestic factors, respectively. If they do, then perfect segmentation and perfect integration may be rejected even if they are true.

10 Since the residual market factor captures any of the omitted domestic and/or international factor(s), and is orthogonal to the factors, the pure domestic and international factors should not capture the effect of missing international and domestic factors, respectively. Thus, a rejection of complete integration or complete segmentation should be unambiguous with respect to the omitted variables problem discussed in footnote 9.

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

c~ U o6 ( .8 o c6 cs

W) It c 00 It0,00 0

o 0 C C C o 6 Ci M 6

;~~~~~~~~~~~~r 'I C\ 8n m C ̂Xo> r- 0 (O

-o * * * * * t0 (0 * * * t _* * t

U

X o o ~~~~~~~~~t C> c N " C> OC It aCN -; 0fi O

0 r- O. O .0 0 -N t O N O,

0 ? t

0 t 9

~ C;6 &).6 6 46 4C; 14 Ci6 14 d6

44 I

0 00 oo t( 'I It 0 It ON D t 0

O\0 c0 rd - 0\0 - ~ rt O N CA cz

o. t~~~~~~~~~~~~~tn n .o r)- \0 O.0vd) td f tn 0C00 \0 00 0 0 0 0 00 0 0 0 Q

CD666 64c)6 66oiC5 C 0-0 64C;C6 66o (

Q~~~~~~~~~~~~~C - 0 b t *N I I t * t ? 0 n

= t O F n ? ? sCs (<} f?1 n ̂ N-n C)

* ~~~~~~~n OC> ? * O) C) ?*Ocn It O) 0

40.

(0 co(0\

-1) *;S O C) O O C) O t* O O0 0 0 C O f 4. 0

0 C; C) C' C, It' C5~-- C5 C; C;C ; C 0) ~~~~~ -0 \0~~~~~~~~~~)C~~~ ONe~~~~~N0N o0'-0- ~ Cl -- -

~~~~~~~~~~~~~~~~~~~~~~~toS -o 0~~~~~~~~~~~~~~~~~~~ 0~~~~~~~~~~~~~~~~~~~~~~~~~~04

(0 * * * * .; Co co co 00 co

* co * 0

O oN o\ ( oo o 0 \ o o ,oN 0 O- o C o N o IN o N--

Q itE~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~t

o 66 6N oo6 -No * *c too - *N o * 0 ( QOV Dto4Eb?V r 0 UN}t

UN -o2~~~~~~~~~~-q -

O0 0(O0F O O ?Q O O m 0 08 00 0 b o n O o O Q , 3

Ne -t * . (0 * .* l* o (0

-o j- =

(;0 0E U N B t

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

00~~~~~~~~~~~ 000 f 0)

-0 C-)00 00

00)* C It *

40 ) o * o , * oo *

i r~ N t * - -*t *N "I o N

000N 0gt O n 8 f Z

9 8 o ^ o X o o > o X t O o o o ~~~~~~~C c - > 't C oC .t

r- 00~~~~~~~~~~~~~~~~~~~~0

~~~~~~~~~* * * * * 0 0) *

*e * o * * *

e N

en 0

C> 00

n C> oNtC ) -NN e 0 e 00c n Oo

s~~~~~~~~C . .no .n .c .o . . o. . ctn0 C ON0 - 0 e)

00 00 W') r- ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0

1/) *1 O * ? *O , O --I - N O -1

1* t *( Cl ON Cl C"l \ N * 00

0) >< '~~~~~0 W' 0r- r

olfO ONe t-t-

0) '- o 'o.o-o,s 0 o o g

en~~~~~0 ~~~~~~~~~~~~~~~~~~~~~~~3 C3 ci C5C

O ~~~~~~~ ~ ~ ~~~-.,* *~~~~~~~~~6-.

~~~~~~~C;

O. Y R 00 00N _N Xi Cl Xt '(N.O

:5~~ ~ 3~ o.o0 . . . m>o.N oo

u Ir -

e^

- 6 6-6 6~-.J -d666

0)~~~~~~~~~~0k U S o o o o-, o o o ,o, o- , o o o o- o- 0o

0) * o ^ 00> 4 'N 00 - O^ 0 Nt n 0 )- \,C 0 0

t s O. > * O b O. O > O. N ~~~~~~~~00 .4 > O. - O 5 4 oO.. ~~~~~~~~C 5 C; T -? i? 1?- 1 6?l C- 4.??i;e -~~~ ~~00N~6.-J 0 0NN NLrOfj'

t S =~~~~~~~~~~~~~~~~~~~~~t

1 CN N d - *- - N Cl

0) -oN .---t 0 ~N o 00 ~ 0~~ N 0)0o 1o z

Q0 0'- Q000 00 0N 0ONC - ~ 01

000 -0 000 ll -e0N0 -IO -C

-i : 8oo O8??v eOo .0 * *; o

Ut oo o o o on n

4 4* 0* * * * 0 o N 00 *t 0 (1 l '- _ '( 't 0 O0)0)

a oCon CA oo o 0 0'N 0 N 00-\0

0~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~0

0) P0 1) 0) ) * o . 0 -= O e.E Q = 8 R X OO~~

Nc' ,0 S0 N _0 _0 N * 0) HO N ON WO ON ON v.

6~~~) 0 ).Y Y -=

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

o x -o c: o ti00 00~~~~~~~~~~~~~~~~~~0 *- S 66 \66

.o ~~~~~~~~~~~~~~~~~~~ * " -- *0

,- , - * )

42~~~~~~~~~~~~~~~~ 00 0 0 Co C n t CN

C-C ooo ^o~ n ON

.2 o 0CN ) 0 C o o n

O~~~~~~~~~~~ C~~~~~~~~~~~~~~~C 4 0 ) C C 00 - n - C "I 00 c ) ? 0 0)

W) 00~~~~~~~~~~~~0

.o2 6- 1-1, 6 '' I .-' 6-',

(CO

o n~~~~~~~~~~~~c

42 * 4

- -) m t oO -~ 0 N O ( 00 OC o 2 o CN,^~~ ,- t_ ? 0?-C \0,-C'- o t CC,C Q'C C C 0 00 COt_ f Ct 0~ ^ O 0ot_ ^N C t

t .t~~~~~~~~~~~~t

CO >

0~~~~~~~~~~~~~~~~~~0

0*

o N o o o N v e o N ? z~~~~~~~~~~~~~~O 5

O O t , 0. R .o 0't T0N U0

0) 0 0 0)0N 0

CO Z- x,,I1 x x ,.

~~C'N - TO> ?t>mN t00tO CO ci, O'\ s O ) 0 )) t- 000 CO; 0 66 6cr O ^O -io oci 666 N - 4 i 6

'2 s m0-0?0 0' N 0 T - _-'

c 8 O O 2 ot8? :4

0 o0oC i c

o | | | 8 E t X~~2C- ;~~~~~~~~~~~~~~~~~~~~~~) 0)

os

d oo o :> 2:> <>> o *X<=-= Boo)

O l O l 8 < F F ' 0 i F F F | 8 D t '3 z 8 0 Ci

n~~~~ -e 0 - csc x c --

5'. (IC Z 0)COCO s s

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

00~~~~~~~~~ 42 00 O It O m m O 00 O W) 0 0 0 C

N ?

i~~C ^OC - 9 N \O -

4. C0 t

t9 C CC; C; 00ot N1N0 00C10 Z

-4 99 r 999 NC1 00-9 N00r m~~~~~~~~~~" 0X 0o nno mto 0o mN 'I 4

ffi 2~~~~~~~W O 0 'IC' o toO - o' ooo 4 oX0 0) 9c WN 'CIC 9ClN9 I 9O 9 9009 90 9 C

00 m m

0~~~~~~~~~~~~~~~~~~~

to

0)* C T0* * * _ 0 CN 00 m C,,4 ,c -4 rN - - * , oo C 0)

- O ^ O s 9 tr Oc ^ t - 0) 9 9 r O - ot 9 O C o oo tr o o -o

- W

0 i IC

._~~~~~~~~~~~< O ON C-OeN Otz O ^

30 O 0\~ CCNt N It 'N O O 42

O O. ~~~~~~~~~~~~~~~~~~~00 m O - ' t W .tNO ?O onO

Q k 00 00 00 o 00 ' 00 0 ,0 , c

0~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~0t

otv ON oN Q rooN o .:

o~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~z

0 ) U 00 00

.0* * * ,* =

Ct O

1-~~0 Cf tCO ?N N oOn o1 00 O 19 _ 0)O4 ? O 00- Cl ^,~0 (tN- 9 C,)-<- ? C,. 0 -? )C

O # [-1-O,OO O

1009 0 1OO110Cf)mOa

g 4 * * ~ ~ ~ ~~~~ * - o?r

;~~O 00 CN Cl o o N N 00 00 C,l r CO V ) O 00 1-00-[ N14_ ' D

0) OO .. L

Ct ~ ~ ON ;- -C ON *Ct Cl -N %

LD ~ ~ 9 99 t 9= 00f) NLt LN ?

; = X XX g X

XN 0 4 XtL

s~~~~~~O ?O ON ON 0)0)\ |D*Y

0) mO ON ON XO 00 N

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 349

factor are statistically different from zero. The time-variation of the betas is again confirmed.

The estimated risk premia and mean factor loadings of the augmented domestic APT, given by equation (8), are reported in table 8. The estimated risk premia re- ported in panel A indicate that the complete segmentation hypothesis, HIo - some domestic factor(s) is (are) priced and all 'international' factors are not priced - is rejected since the domestic factor TERM has a priced risk and two of the 'in- ternational' factors, REURO and the 'international' component of the leading index (DINDEXI), are priced risks. However, the partial segmentation hypothesis cannot be rejected, since at least one of the domestic factors is priced. All the mean factor loadings are significant and time-varying, as indicated by the subperiod estimates.

The estimates of the risk premia and mean factor loadings for the augmented APT with the RMF included as an independent variable are reported in table 9. Based on panel A, the factors, DINDEXI and RMF, are priced risks for the entire period from March 1969 to March 1988. Since it is not known whether the RMF factor is capturing the influence of omitted domestic and/or binational factors, there is ambiguity regarding partial segmentation. For both subperiods, however, the esti- mated risk premia clearly indicate that the partial segmentation hypothesis cannot be rejected. Therefore, for the whole period, the partial segmentation hypothesis cannot be rejected, and the RMF factor has to include domestic omitted variables. The mean factor loadings are strongly significant, especially over the March 1978 to March 1988 subperiod.

V. CONCLUDING REMARKS

In this paper, the hypotheses that the Canadian equity market is completely (partly) integrated and segmented relative to a global North American equity market are tested using modified forms of the IAPT and APT models. For the period from March 1969 through March 1988 both models indicated that the Canadian equity market is only partly integrated (or equivalently, partly segmented) with the American equity market. The Canadian macroeconomic factors found to influence Canadian stock returns are the pure domestic component of the term structure and the lag of the industrial production index. The North American macroeconomic factors affecting Canadian returns are the pure 'international' components of the differential in the Canada/u.s. leading indicators, and the interest rate on u.s. dollar deposits in London (i.e., eurodeposits).

REFERENCES

Adler, M., and B. Dumas (1989) 'International portfolio choice and corporation finance: A synthesis.' Journal of Finance 38, 925-84

Akaike, H. (1976) 'Canonical correlations analysis of time series and the use of an infor- mation criterion.' In Advances and Case Studies in System Identification, ed. R. Mehra and D.G. Laniotis (New York: Academic Press)

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

350 George Koutoulas and Lawrence Kryzanowski

Anderson, T.W. (1984) An introduction to Multivariate Statistical Analysis (New York: John Wiley)

Bodurtha, N. (1986) 'Discussion.' Journal of Finance 41, 614-16 Bodurtha, J.N., D.C. Cho, and L.W. Senbet (1989) 'Economic forces in the stock market.'

Global Finance Journal 1, 21-46 Brown, S. (1989) 'The number of factors in security returns.' Journal of Finance 44,

1247-62 Brown, S., and T. Otsuki (1989) 'Macroeconomic factors and the Japanese equity mar-

kets: The CAPMD project.' Working Paper, New York University Burmeister, E., and M. McElroy (1988) 'Joint estimation of factor sensitivities and risk

premia for the arbitrage pricing theory.' Journal of Finance 43, 721-35 Chen, N., R. Roll, and S. Ross (1986) 'Economic forces and the stock market.' Journal of

Business 59, 383-403 Cho, C., C. Eun, and L. Senbet (1986) 'International pricing theory: an empirical investi-

gation.' Journal of Finance 41, 313-29 Conway, D., and M. Reinganum (1988) 'Stable factors in security returns: identification

using cross-validation.' Journal of Business and Economic Statistics 6, 1-15 Dhrymes, P.J., I. Friend, M.N. Gultekin, and N.B. Gultekin (1985) 'New tests of the APT

and their implications.' Journal of Finance 40, 659-74 Frankel, J. (1979) 'On the mark: a theory of floating exchange rates based on real interest

differentials.' American Economic Review 69, 610-22 Gallant, R. (1985) 'Seemingly unrelated nonlinear regressions.' Journal of Econometrics

3, 35-50 (1987) Nonlinear Statistical Models (New York: John Wiley)

Gultekin, M., B. Gultekin, and A. Penati (1989) 'Capital controls and international capital market segmentation: the evidence from the Japanese and American stock markets.' Journal of Finance 44, 849-70

Hamao, Y. (1989) 'An empirical investigation of the APT using Japanese data.' Japan and the World Economy

Jorion, P., and E. Schwartz (1986) 'Integration vs. segmentation in the Canadian stock market.' Journal of Finance 41, 603-14

Kryzanowski, L., and M.C. To (1983) 'General factor models and the structure of security returns.' Journal of Financial and Quantitative Analysis 18, 31-52

Kryzanowski, L., and H. Zhang (1992) 'Economic forces and seasonality in security returns.' Review of Quantitative Finance and Accounting 2, 227-44

McElroy, M., and E. Burmeister (1988) 'Arbitrage pricing theory as a restricted nonlinear multivariate regression model.' Journal of Business and Economic Statistics 6, 29-42

Poon, S., and S.J. Taylor (1991) 'Macroeconomic factors and the U.K. stock market.' Journal of Business Finance and Accounting 18, 619-36

Roll, R. (1977) 'A critique of the asset pricing theory's tests - Part 1: On past and poten- tial testability of the theory.' Journal of Financial Economics 4, 129-76

Ross, S. (1976) 'The arbitrage theory of capital asset pricing.' Journal of Economic Theory 13, 341-60

Shanken, J. (1985) 'Multi-beta CAPM or equilibrium APT?: A reply.' Journal of Finance 40, 1189-96

- (1992) 'On the estimation of beta-pricing models.' Review of Financial Studies 5, 1-34

Solnik, B. (1974a) 'An equilibrium model of the international capital market.' Journal of Economic Theory 8, 400-24

- (1974b) 'The international pricing of risk: An empirical investigation of the world capital structure.' Journal of Finance 29, 48-54

- (1983) 'International arbitrage pricing theory.' Journal of Finance 38, 449-57

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions

Integration or segmentation 351

Stehle, R. (1988) 'An empirical test of the alternative hypotheses of national and interna- tional pricing of risky assets.' Journal of Finance 32, 493-502

Trzcinka, C. (1986) 'On the number of factors in the Arbitrage Pricing Model.' Journal of Finance 41, 347-68

Wheatley, S. (1988) 'Some tests of international equity integration.' Journal of Financial Economics 21, 177-212

Wei, J. (1988) 'An asset-pricing theory unifying the CAPM and APT.' Journal of Finance 43, 881-92

This content downloaded from 128.230.234.162 on Wed, 4 Jun 2014 19:16:35 PMAll use subject to JSTOR Terms and Conditions