Embed Size (px)

Citation preview

1

Insurance Supervisory Approach

09 February 2018

January 2018

Welcome and Introduction

• Evolution of our supervisory approach under Solvency II

• Providing clarity on our key areas of focus

• Setting expectations for the next 18-24 months

• International recognition of high standards of supervision post BREXIT

• Collaboration

09 February 2018 2

Agenda

09 February 2018 3

Insurance Regulatory Approach for the next 18-24 months

Q&A on Insurance Regulatory Approach

Insurance Distribution Directive

Q&A on Insurance Distribution Directive

09 February 2018 4

Authorisations

Supervision (Prudential and Conduct)

Enforcement

Insurance Regulatory Approach – GFSC Functions

Insurance

Regulatory

and

Supervisory

Plan

Insurance Supervisory Approach Overview

09 February 2018 5

Governance

Underwriting

Systems and

data

Reserving

InvestmentsReinsurance

Group

Contagion

Capital/SCR

Reporting

Quality

Assurance

Performance

of Auditors

Performance

of Actuaries

Resolvability &

Recovery plans

Conduct

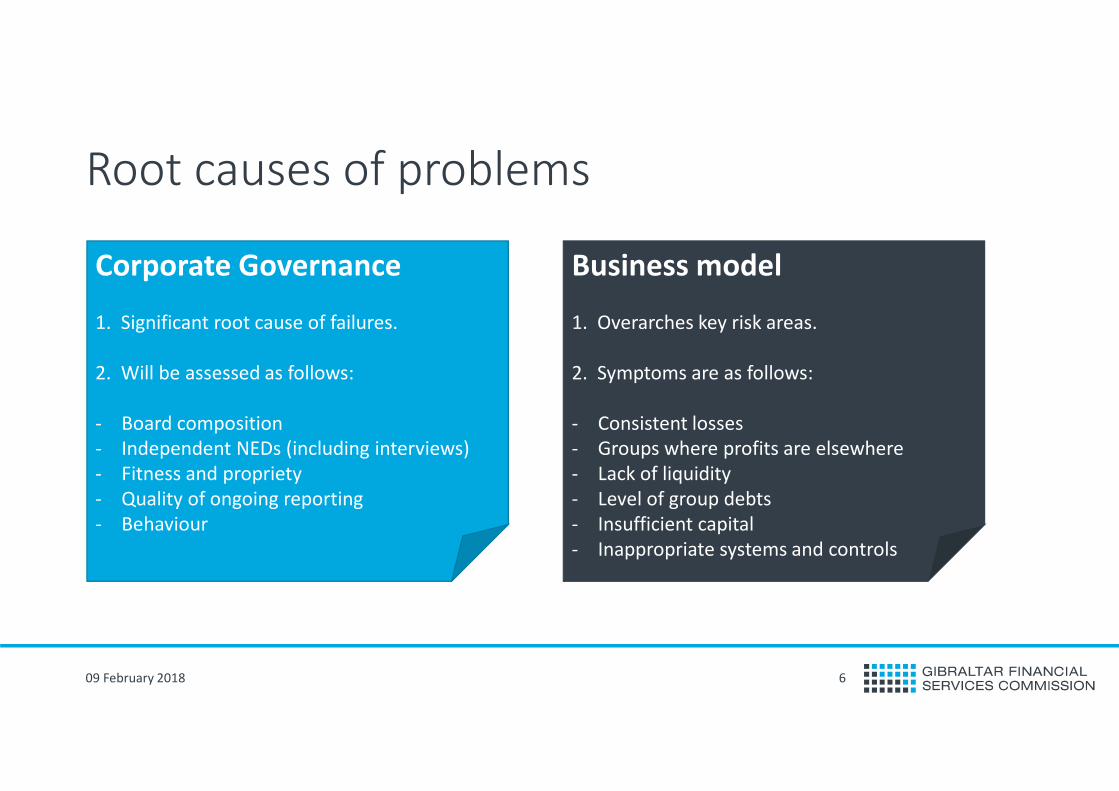

Root causes of problems

09 February 2018 6

Corporate Governance

1. Significant root cause of failures.

2. Will be assessed as follows:

- Board composition

- Independent NEDs (including interviews)

- Fitness and propriety

- Quality of ongoing reporting

- Behaviour

Business model

1. Overarches key risk areas.

2. Symptoms are as follows:

- Consistent losses

- Groups where profits are elsewhere

- Lack of liquidity

- Level of group debts

- Insufficient capital

- Inappropriate systems and controls

Authorisations

09 February 2018 7

•How does the firm

make revenue

•Can it sustain

stressed situations

•Key Processes

(UW, claims, etc.)

• Does it make

sense for the

entity to set up in

Gibraltar?

• What markets do

they want to

access?

•F&P

assessments

•Interviews

•Head office

assessments

• Access to

additional funding

in stressed

situations

• Capital

management

policies Access to

CapitalGovernance

Adequacy

of business

model

Rationale

for setting

up in

Gibraltar

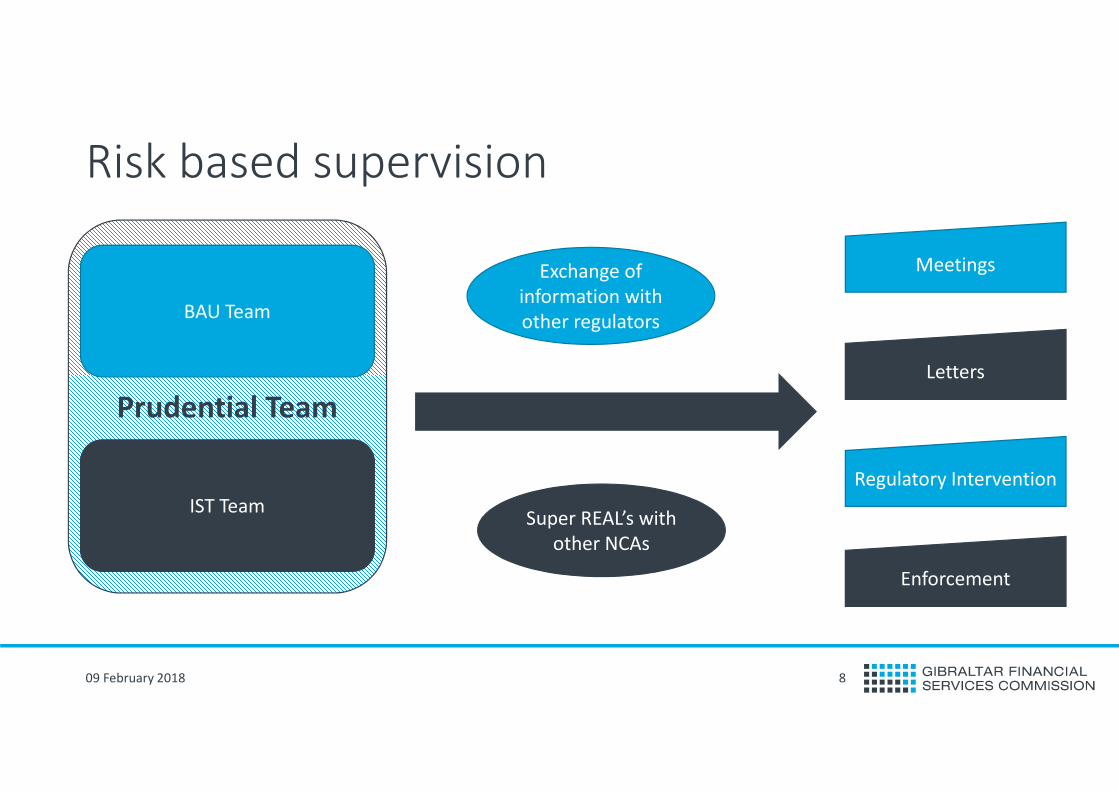

Prudential Team

Risk based supervision

09 February 2018 8

IST Team

BAU Team

Super REAL’s with

other NCAs

Meetings

Letters

Regulatory Intervention

Enforcement

Exchange of

information with

other regulators

Prudential supervision overview

09 February 2018 9

BAU

QRTs

Financial

Statements

ORSA

Reserve

reports

Technical

leads will

focus on risk

areas

Focus areas

will intersect

with BAU

work

Conduct of Business SupervisionFocus areas for 2018-2019

09 February 2018 10

Policyholder

Protection

IDD

Implement

-ation

Delegated

Authorities

Product

Oversight

and Governance

ComplaintsOutsourcing

Claims

Handling

Reserving

09 February 2018 11

Independent Reserving Reports

Actuarial reconciliations

Actuarial Function Holder Reports

Board / Committee minutes

Expectations:

• Cover all lines – live and discontinued (unless actuarially justified

and documented, and with express consent of the Board)

• Actuaries have relevant business and jurisdictional experience

• Ordinarily expect reserving at least independent best estimate

• Clear reconciliation to financial statements and Solvency II figures

• Notifiable event if reserving below independent best estimate

• Report covering all the tasks of the SII actuarial function?

• Limitations identified? Clear recommendations.

• Ownership by AFH of: i. outsourcing to independent actuaries, ii.

mitigating limitations

• AFH important, but Board has ultimate ownership

• Evidence of internal reserving process

Underwriting

09 February 2018 12

Underwriting

framework

MonitoringForward looking plans

• Risk selection

• Pricing

• Policy coverage

• Aggregation management

• Risk appetite statements

• Timely reactions to market

events (e.g. Ogden rate)

• Ongoing appropriateness of

underwriting framework

• Strategic impacts due to

competitors, distributors,

service providers

• Forecast loss ratios (SCR

assumptions, ORSA) vs

prior year loss ratios

• Actuarial justification for

any improvements

• Actual vs Expected analysis

Prioritise prudential resource towards firms:

• Material improvements in forecast loss ratio

• High growth rates

• Low solvency coverage

Identification supported by peer comparisons,

market benchmarks, collaboration with other

regulators

Capital / SCR Appropriateness

09 February 2018 13

• Risk profile analysis,

• Standard formula appropriateness assessment,

• SCR result supported by robust stress testing,

• Clear SCR coverage appetites (minimum and target),

• Clear statements on economic capital

Own Risk and Solvency Assessment (ORSA)

Reviews

Discussions of potential capital add-on proceedings

where standard formula is not appropriate

Solvency II Approvals and ongoing appropriateness reviews for:

• Internal Models

• Internal Model Change

• Undertaking Specific Parameters (USPs)

• Volatility Adjustment (VA)

• Ancillary Own Funds (AOF)

Group contagion

09 February 2018 14

Risk and areas of focus

Key risks identified to date:

How GFSC will approach:

RPTsStrip out

profits

Going

concern

Lack of

visibility

Outsourcing

controlsGovernance

Peer group

analysis

Review of

controls

Prudent Person

Principle

Impairment

reviews

Business model

analysis

Quarterly

reporting

Recovery and resolution

09 February 2018 15

Recovery and resolution plans

• Firms need to be ready to respond to challenges

• Minimum expectation is inclusion of recovery options and risks to resolution within ORSA.

• Should cover potential stress scenarios

• Should consider key suppliers and activities

• Should assess potential costs of plan

• RRPs will be escalated where concerns towards resolvability.

What are indicators of

a stress scenario

What are procedures

for informing Board

What contingency

plans are in place

Systems and data

09 February 2018 16

Expectations

• Data is complete, accurate, and appropriate

• Sufficient quality and timeliness of data for

purposes:

• Underwriting

• Reserving

• Capital modelling

• Reporting

• Oversight of data from delegated authorities

• Can systems manage and validate multiple

data sources

• Are systems appropriate for number of

distributors and COB

Risk

indicators

from….

Auditor’s Management Letters

Financial Statements

Reserving reports – Uncertainty comments

Actuarial Function Holder Reports

Assessment of Data Quality

Internal Audit Reports

Regulatory reporting quality

Investments

09 February 2018 17

Risk and areas of focus

Key risk identified to date:

- Lack of liquidity by some licensees

SII Prudent Person Principle

1. Currently being raised with firms

2. Data analytics to be used for industry wide review

Group debtors

Group investments

Property investments

Liquidity and concentration

concerns from:

Reinsurance / Co-insurance

09 February 2018 18

Quota share

Excess of Loss (XoL)

ADC/LPT Covers

Co-insurance

Review ORSAs and underlying contracts:

Focus on insurers where:

• Reinsurance use is high

• SCR coverage is low

• There are large reinsurance concentrations

• Asset liquidity is low (reinsurance will impact liquidity)

Reinsurance may just be a very expensive

form of capital

- Is it always loss absorbing in times of stress?

• Additional risk from capitalisation clauses (PPOs) and minimum and deposit premiums

• Commissions structures (incl. sliding scales) and contractual

limits on contracts

• Extent of risk transfer following loss corridors and commutation clauses, and appropriateness of SCR modelling

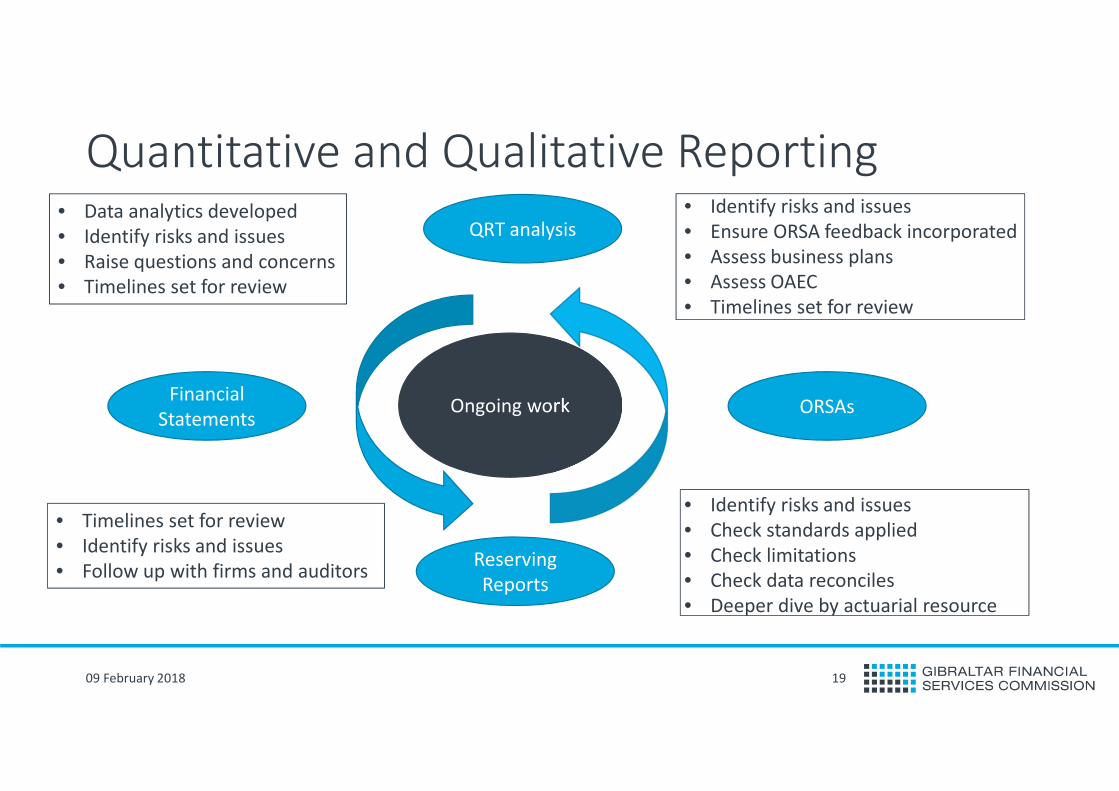

Quantitative and Qualitative Reporting

09 February 2018 19

Ongoing work ORSAsFinancial

Statements

Reserving

Reports

QRT analysis

• Timelines set for review

• Identify risks and issues

• Follow up with firms and auditors

• Identify risks and issues

• Check standards applied

• Check limitations

• Check data reconciles

• Deeper dive by actuarial resource

• Identify risks and issues

• Ensure ORSA feedback incorporated

• Assess business plans

• Assess OAEC

• Timelines set for review

• Data analytics developed

• Identify risks and issues

• Raise questions and concerns

• Timelines set for review

Professional service providers

09 February 2018 20

Auditors

Actuaries

Work performed is critical in supporting regulatory oversight

Expect firms to follow ISAs and industry best practice

Should appropriately consider work of experts

Will be considered in our QA visits

Work performed is critical in supporting regulatory oversight

We will consider quality of reports to licensees

We will coordinate with governing bodies

We will consider application of standards

What we expect from you/what you can expect from us

Collaborative approach

• No surprises

• Early engagement

• Regular dialogue

• Maintain accessibility - transparent, open and pragmatic approach to issues

09 February 2018 21

09 February 2018 22

Questions

Comments

23

Insurance Distribution DirectiveJanuary 2018

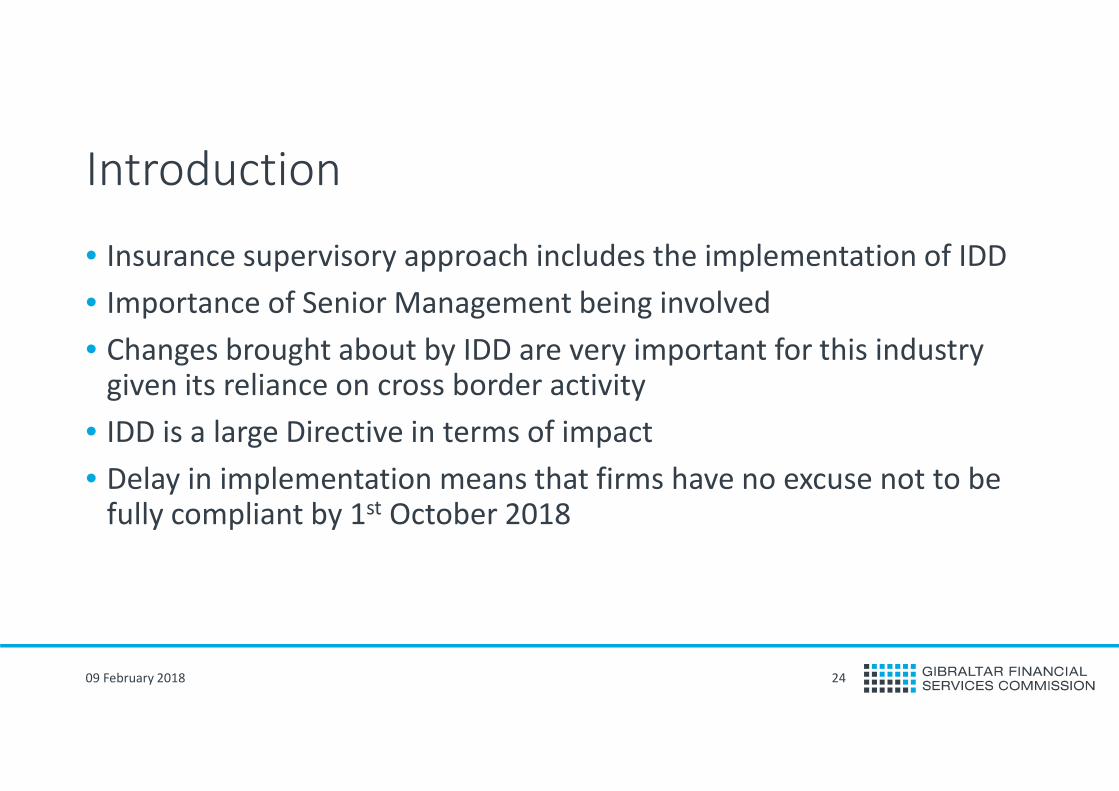

Introduction

• Insurance supervisory approach includes the implementation of IDD

• Importance of Senior Management being involved

• Changes brought about by IDD are very important for this industry given its reliance on cross border activity

• IDD is a large Directive in terms of impact

• Delay in implementation means that firms have no excuse not to be fully compliant by 1st October 2018

09 February 2018 24

Agenda

09 February 2018 25

Key Features of the IDD

Conduct of Business

Product oversight and governance

Knowledge and Competence

Enforcement powers

Passporting

Supervisory strategy

Next Steps

Questions?

IDD key Features from a consumer perspective

Greater transparency

(price and costs)

Better and more comprehensible

information (IPID)Cross-selling

Transparency & business conduct

All distribution channels caught

Stronger safeguards

(investment products

suitability)

Fair competition

09 February 2018 26

Who does it apply to?

Insurance Intermediaries

Insurance Companies

Insurance Distributors

Ancillary Insurance Intermediaries

09 February 2018 27

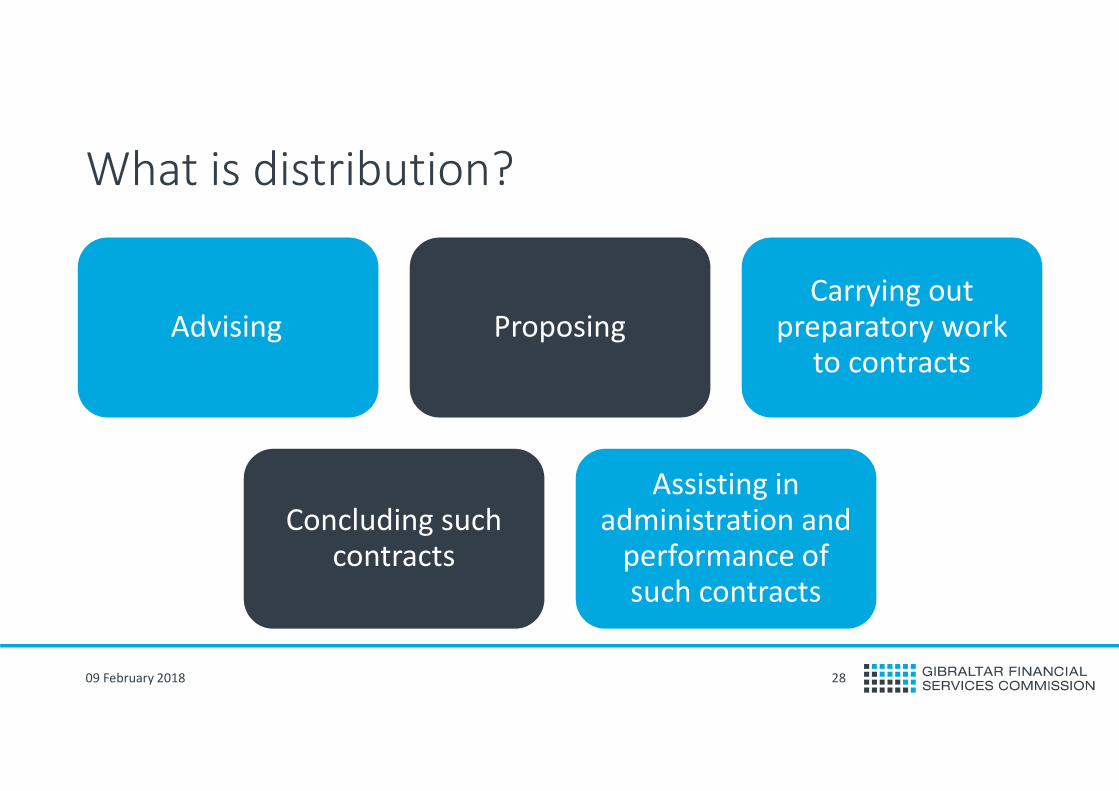

What is distribution?

Advising ProposingCarrying out

preparatory work to contracts

Concluding such contracts

Assisting in administration and

performance of such contracts

09 February 2018 28

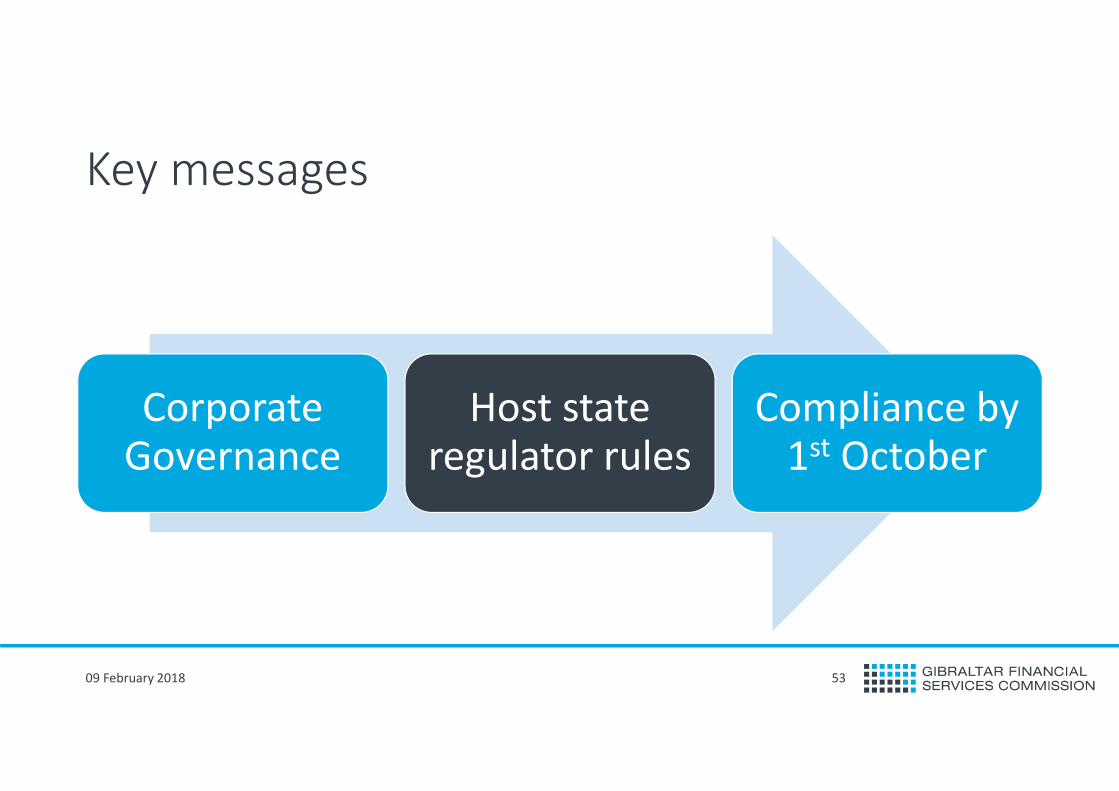

IDD – Areas for you to consider

Corporate Governance

Host state regulator rules

Compliance by 1st October

Conduct of Business

09 February 2018 30

Objectives

In terms of Conduct of Business requirements, IDD seeks to:

Improve regulation in the retail insurance market

Strengthen consumer protection, in particular with regard to the distribution of insurance-based investment products.

09 February 2018 31

General Principles

The new regime will introduce two general principles:

Insurance distributers must "always act honestly, fairly and professionally in

accordance with the best interests of customers

All information must be "fair, clear and not misleading."

09 February 2018 32

09 February 2018 33

Requirements

COB

Requirements

Product

Oversight &

Governance

Advice

Cross

SellingInsurance

Product

Information

Document (IPID)

Conflicts of

interest & Transparency

Enhanced

Requirements

for IBIPs

Product Oversight and Governance

Requirements

09 February 2018 34

Product Manufacturer

Recital 55

• “In order to ensure that insurance products meet the needs of the target market, insurance undertakings, and in the

Member States where insurance intermediaries manufacture insurance products for sale to customers, insurance

intermediaries should maintain, operate and review a process for the approval of each insurance product”

Article 25

• “Insurance undertakings, as well as intermediaries which manufacture any insurance product for sale to customers,

shall maintain, operate and review a process for the approval of each insurance product, or significant adaptations of

an existing insurance product, before it is marketed or distributed to customers.”

Regulations

• “Insurance intermediaries shall be considered manufacturers where an overall analysis of their activity shows that

they have a decision-making role in designing and developing an insurance product for the market.”

09 February 2018 35

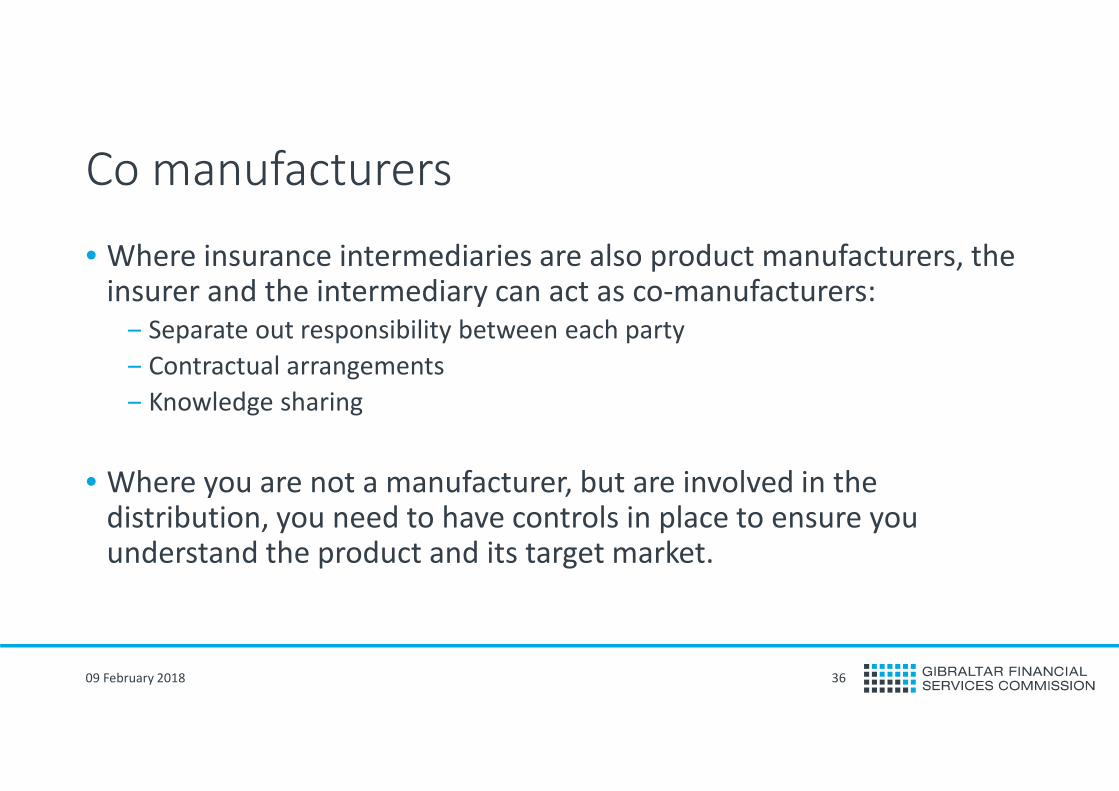

Co manufacturers

• Where insurance intermediaries are also product manufacturers, the

insurer and the intermediary can act as co-manufacturers:

‒ Separate out responsibility between each party

‒ Contractual arrangements

‒ Knowledge sharing

• Where you are not a manufacturer, but are involved in the

distribution, you need to have controls in place to ensure you

understand the product and its target market.

09 February 2018 36

Requirements – Article 25

09 February 2018 37

Product Testing Product Approval

Process

Management

Involvement

Appropriateness

of Distribution

channels

Product

monitoring and

review

Target Market

What do these requirements mean for you?

New processes

Updating internal policies and processes

Training within the organisation

Embedding of the processes

Training of distributors

New contractual arrangements

09 February 2018 38

Knowledge and Competence

New knowledge and competence requirements

Sets high standard – based on a benchmark

Appropriate in relation to the products offered

Continuing Professional and development requirements

Onus on Firms to ensure staff meet standards and support staff

Establishing a benchmark

Establish a high standard

Qualifications; examples from industry

Firms need to assess all individuals currently selling or in relevant management

position

Firms need to establish if other qualifications meet this benchmark

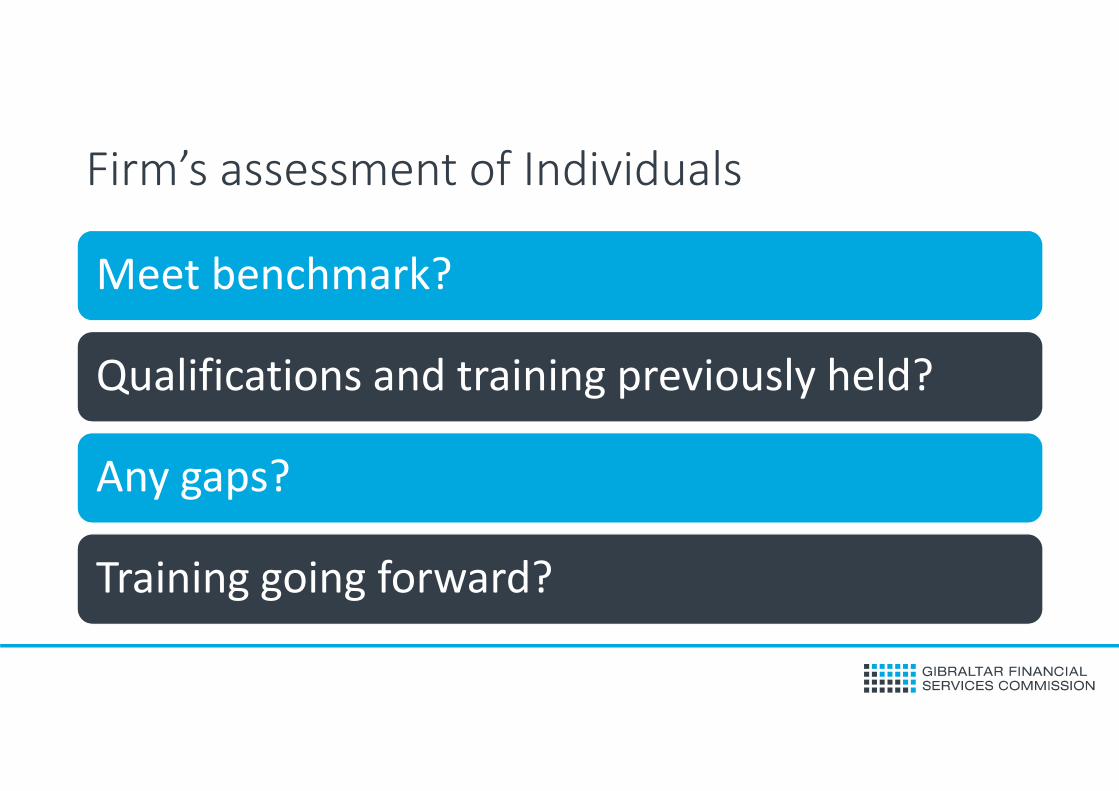

Firm’s assessment of Individuals

Meet benchmark?

Qualifications and training previously held?

Any gaps?

Training going forward?

Examples of support for new employees

Listening in on discussions with clients

Peer review of advice

Providing support and time for studies

Providing a robust induction and training programme

Usually 6 months to be competent dependent on products

Ongoing training

15 hours minimum CPD

Structured training covering areas in Annex I

Covers products offered by firm

Understand firm’s internal policies

Keep up to date with market and industry developments

Firms need to document staff CPD and ensure compliance

Enforcement Powers

09 February 2018 45

Enforcement powers

Administrative sanctions and other measures shall be effective, proportionate and dissuasive

Order the entity or individual to cease any conduct which constitutes a breach and desist

from any repetition of the conductPower to revoke the licence

For investment based insurance products there are further powers:

•Publish statement on nature of breach

•Financial penalties – Up to €5m / 5% of annual turnover / 2x profits gained from non-compliant activity

The directive requires us to take all measures necessary to ensure that the provisions are implemented

Administrative sanctions may be imposed for all infringements of the provisions within the directive and local regulations

09 February 2018 46

Passporting

09 February 2018 47

Passporting

Firms can passport across the EU to carry out the activity of insurance distribution

Insurance companies need to ensure that firms distributing their products are registered to carry out the activities of insurance distribution in the member state in which they operate

There is an obligation for firms and individuals to comply not only with the local requirements, but also with the host state requirements which can differ from jurisdiction to jurisdiction

09 February 2018 48

Host state – New powers

If breach occurs –GFSC Obligation to consider any action or measures we may want to take to remediate situation

If host member state considers that despite any action taken by GFSC consumers are detrimentally impacted or our actions are in their view insufficient – it can take separate action to prevent further irregularities

09 February 2018 49

Next Steps

09 February 2018 50

Supervisory Strategy

• Collaborative

‒ With industry

‒ Within the GFSC

‒ With host state regulators

• Focused on higher risk areas

‒ Implementation plans by firms

‒ Product oversight and governance

‒ Transparency

• Tailored to the firm being reviewed

09 February 2018 51

Next steps

Currently

• Working with highest impact firms around IDD implementation preparedness

IDD Workshops

• Provide focus for firms to ensure compliance with requirements by implementation date

31 March 2018

• Follow up with high impact firms to ensure on track to be IDD compliant by 1 October 2018

30 June 2018

• FSC to consider all the implementation plans to be satisfied that all firms are on route to meeting the implementation deadline of 1 October 2018

September 2018

• Ensure that we are confident that compliant on key areas: Corporate Governance and Product governance, training and Competency, Conduct and passporting (general good) requirements or have action plans in place.

09 February 2018 52

Key messages

09 February 2018 53

Corporate Governance

Host state regulator rules

Compliance by 1st October

Useful information

Dedicated email address:

[email protected] website page:

http://www.fsc.gi/firms/idd

09 February 2018 54

09 February 2018 55

Questions

Comments