Embed Size (px)

Citation preview

Insurance Sector

Digital Transformation July 2018

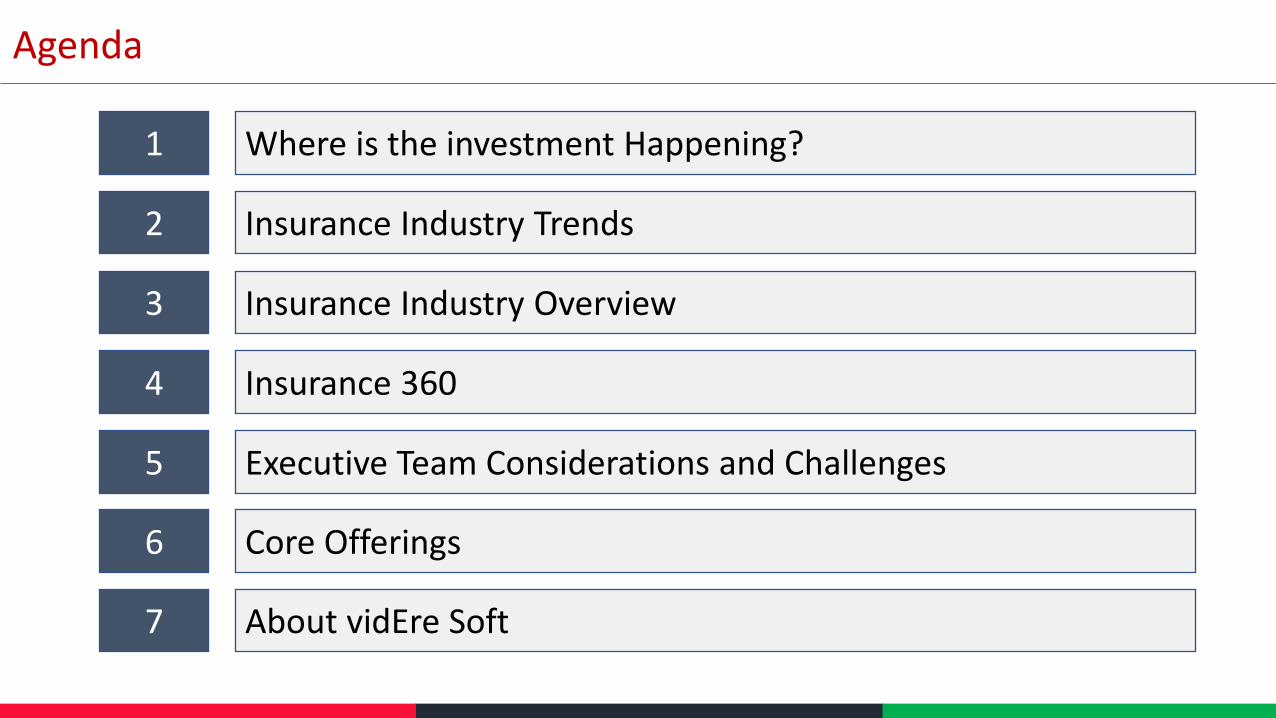

Agenda

1 Where is the investment Happening?

2 Insurance Industry Trends

3 Insurance Industry Overview

4 Insurance 360

5 Executive Team Considerations and Challenges

6 Core Offerings

7 About vidEre Soft

Where is the Investment Happening?

Where are VC’s investing their funds

• Internet-First Insurers – Life • Employers Insurance – Benefits & Insurance • Enablers – Back-end Solutions

• Distribution Platforms –Property & Casualty

Source: Tracxn

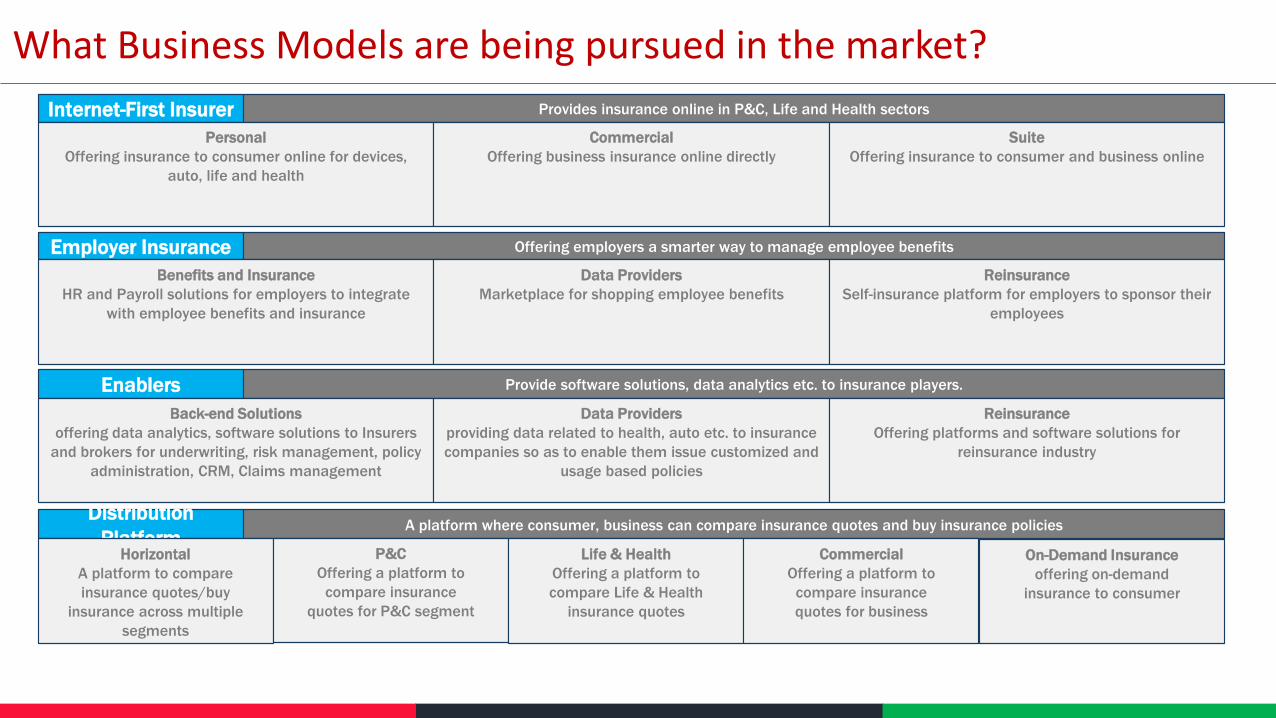

What Business Models are being pursued in the market?

Enablers Provide software solutions, data analytics etc. to insurance players.

Back-end Solutions

offering data analytics, software solutions to Insurers

and brokers for underwriting, risk management, policy

administration, CRM, Claims management

Data Providers

providing data related to health, auto etc. to insurance

companies so as to enable them issue customized and

usage based policies

Reinsurance

Offering platforms and software solutions for

reinsurance industry

Employer Insurance Offering employers a smarter way to manage employee benefits

Benefits and Insurance

HR and Payroll solutions for employers to integrate

with employee benefits and insurance

Data Providers

Marketplace for shopping employee benefits

Reinsurance

Self-insurance platform for employers to sponsor their

employees

Internet-First Insurer Provides insurance online in P&C, Life and Health sectors

Personal

Offering insurance to consumer online for devices,

auto, life and health

Commercial

Offering business insurance online directly

Suite

Offering insurance to consumer and business online

Distribution

Platform A platform where consumer, business can compare insurance quotes and buy insurance policies

Horizontal

A platform to compare

insurance quotes/buy

insurance across multiple

segments

P&C

Offering a platform to

compare insurance

quotes for P&C segment

Life & Health

Offering a platform to

compare Life & Health

insurance quotes

Commercial

Offering a platform to

compare insurance

quotes for business

On-Demand Insurance

offering on-demand

insurance to consumer

Insurance Industry Trends

Trends (McKinsey)

Personal Lines

• Greater Commoditization due to transparency and social purchases

• Decreasing Profitability due to lack of diversification

• Automated Underwriting due to guidance from talented senior underwriters and predictive modelling

• Greater Loss Control due to usage of telematics to proactively control loss and manage risk

Commercial Lines

• Virtual Business Affinity Groups due to Social networking among small business owners for predictable

risk

• Automated Underwriting due to guidance from talented senior underwriters and predictive modelling

• Business Model Transformation due to real-time data from sensors and devices

Individual Life,

Annuities and

Retirement

• New products for seniors due to ageing population and the need to manage retirement and longevity

• Insurers to step onto government turf due to strained government support for sick and political challenges

• Better Risk Management due to greater availability of medical and behavioral data

• Tailored Products due to increased voluntary coverage

Automation Telematics Self Service Social Analytics

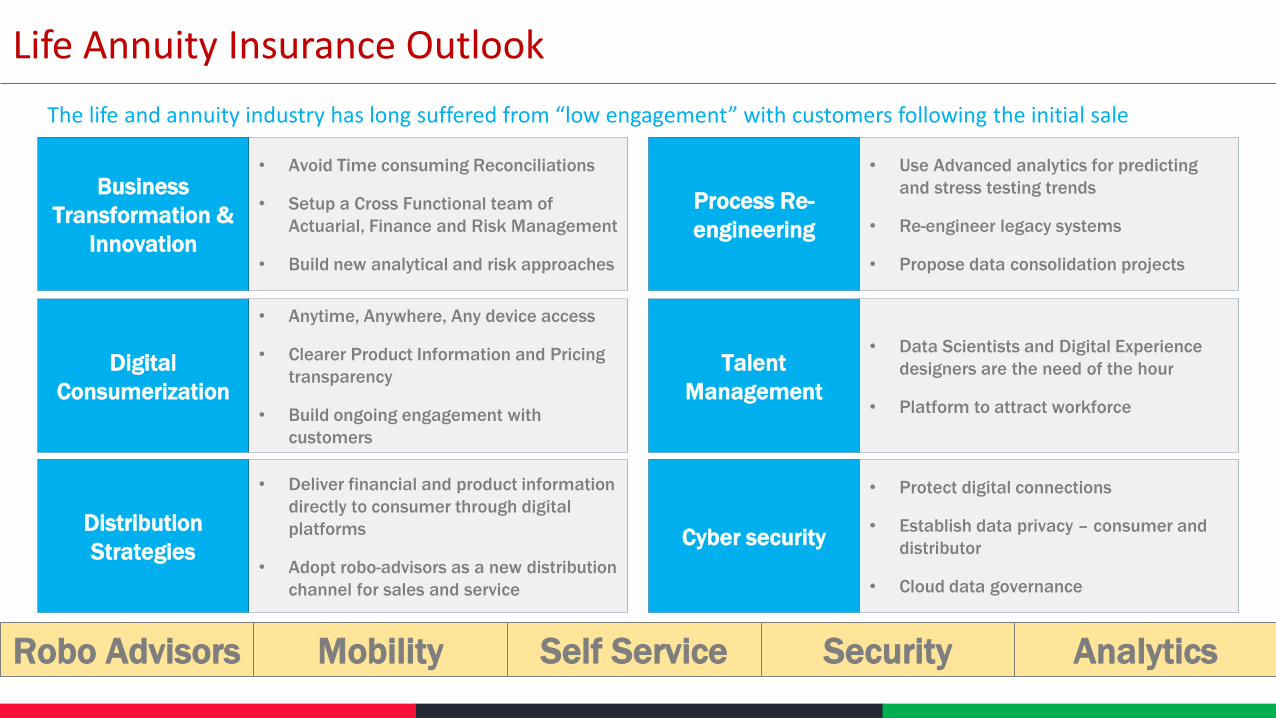

Life Annuity Insurance Outlook

Business

Transformation &

Innovation

Digital

Consumerization

Distribution

Strategies

• Avoid Time consuming Reconciliations

• Setup a Cross Functional team of

Actuarial, Finance and Risk Management

• Build new analytical and risk approaches

• Anytime, Anywhere, Any device access

• Clearer Product Information and Pricing

transparency

• Build ongoing engagement with

customers

• Deliver financial and product information

directly to consumer through digital

platforms

• Adopt robo-advisors as a new distribution

channel for sales and service

Process Re-

engineering

Talent

Management

Cyber security

• Use Advanced analytics for predicting

and stress testing trends

• Re-engineer legacy systems

• Propose data consolidation projects

• Data Scientists and Digital Experience

designers are the need of the hour

• Platform to attract workforce

• Protect digital connections

• Establish data privacy – consumer and

distributor

• Cloud data governance

Robo Advisors Mobility Self Service Security Analytics

The life and annuity industry has long suffered from “low engagement” with customers following the initial sale

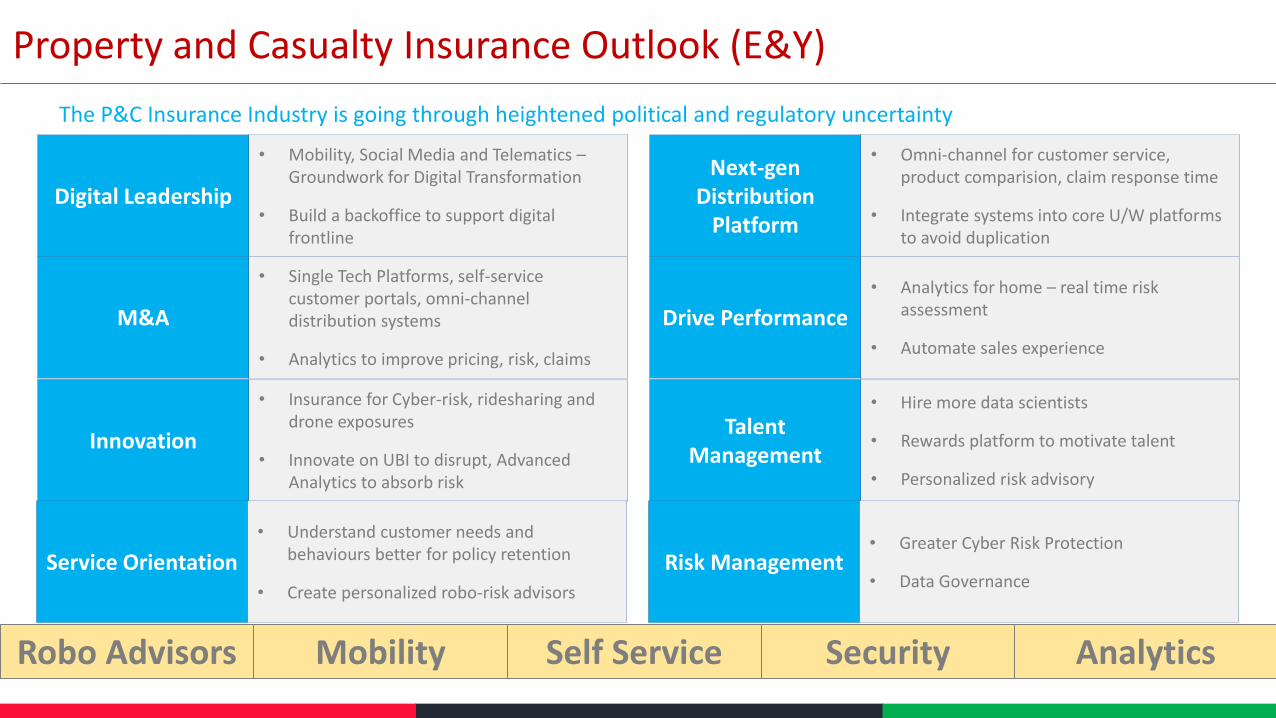

Property and Casualty Insurance Outlook (E&Y)

Digital Leadership

M&A

Innovation

• Mobility, Social Media and Telematics – Groundwork for Digital Transformation

• Build a backoffice to support digital frontline

• Single Tech Platforms, self-service customer portals, omni-channel distribution systems

• Analytics to improve pricing, risk, claims

• Insurance for Cyber-risk, ridesharing and drone exposures

• Innovate on UBI to disrupt, Advanced Analytics to absorb risk

Service Orientation

• Understand customer needs and behaviours better for policy retention

• Create personalized robo-risk advisors

Next-gen Distribution

Platform

Drive Performance

Talent Management

• Omni-channel for customer service, product comparision, claim response time

• Integrate systems into core U/W platforms to avoid duplication

• Analytics for home – real time risk assessment

• Automate sales experience

• Hire more data scientists

• Rewards platform to motivate talent

• Personalized risk advisory

Risk Management • Greater Cyber Risk Protection

• Data Governance

Robo Advisors Mobility Self Service Security Analytics

The P&C Insurance Industry is going through heightened political and regulatory uncertainty

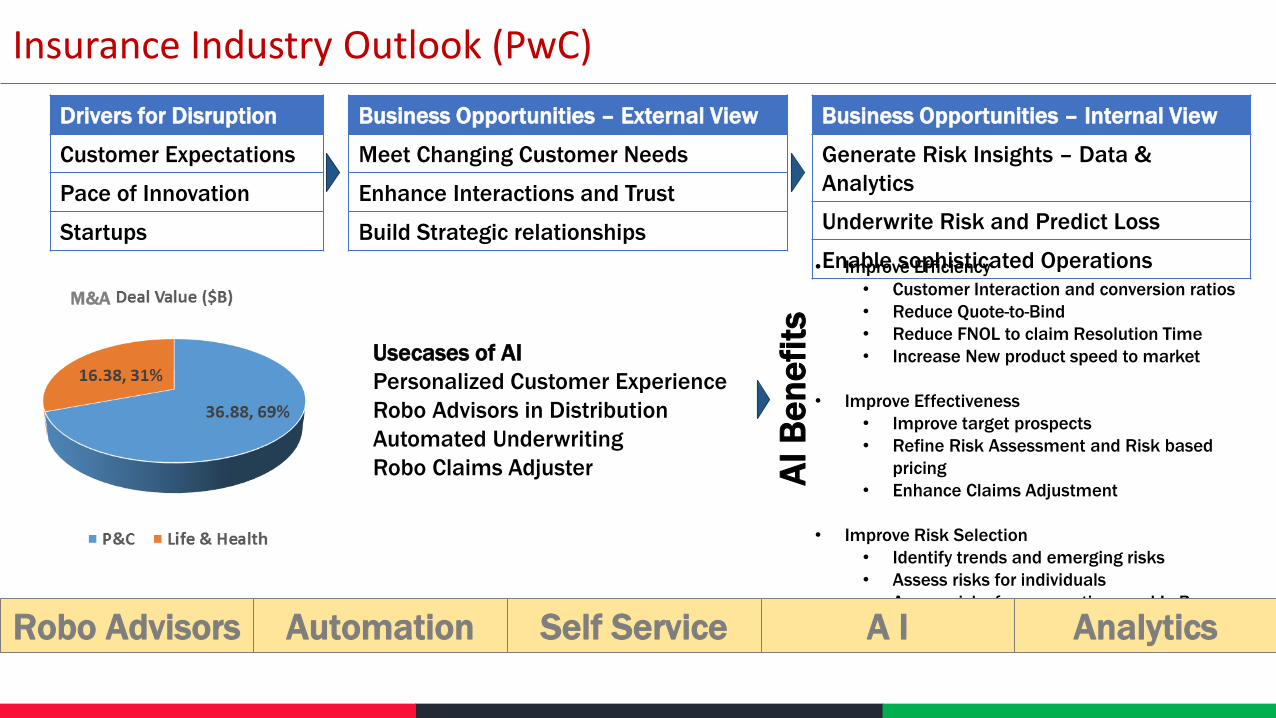

Insurance Industry Outlook (PwC)

M&A

Drivers for Disruption

Customer Expectations

Pace of Innovation

Startups

Business Opportunities – External View

Meet Changing Customer Needs

Enhance Interactions and Trust

Build Strategic relationships

Business Opportunities – Internal View

Generate Risk Insights – Data &

Analytics

Underwrite Risk and Predict Loss

Enable sophisticated Operations

Usecases of AI

Personalized Customer Experience

Robo Advisors in Distribution

Automated Underwriting

Robo Claims Adjuster

• Improve Efficiency

• Customer Interaction and conversion ratios

• Reduce Quote-to-Bind

• Reduce FNOL to claim Resolution Time

• Increase New product speed to market

• Improve Effectiveness

• Improve target prospects

• Refine Risk Assessment and Risk based

pricing

• Enhance Claims Adjustment

• Improve Risk Selection

• Identify trends and emerging risks

• Assess risks for individuals

• Assess risks for corporations and LoBs

Robo Advisors Automation Self Service A I Analytics

AI

Be

ne

fits

Other Investment Areas

• Actuarial

• Analytics

• Artificial Intelligence

• Backoffice for Digital

• Customer Need Analysis

• Cyber security

• Direct to Consumer

• Data Consolidation

• Data Governance

• Data Privacy

• Drones

• Enable Sophisticated Operations

• Finance Management

• Home Analytics

• Omni-Channel

• Platform Re-engineer

• Predict Loss

• Real Time Risk Assessment

• Reconciliations

• Ride Sharing

• Risk Advisory

• Risk Insights

• Risk Management

• Robo Advisors

• Self Service

• Single Tech Platforms

• Social Media

• Telematics

• U/W Systems Integration

• Underwrite Risk

• Usage Based Insurance

• Workforce Acquisition Platform

Insurance Industry Overview

Core Insurance Offerings

Core Re-Insurance Offerings

Insurance 360

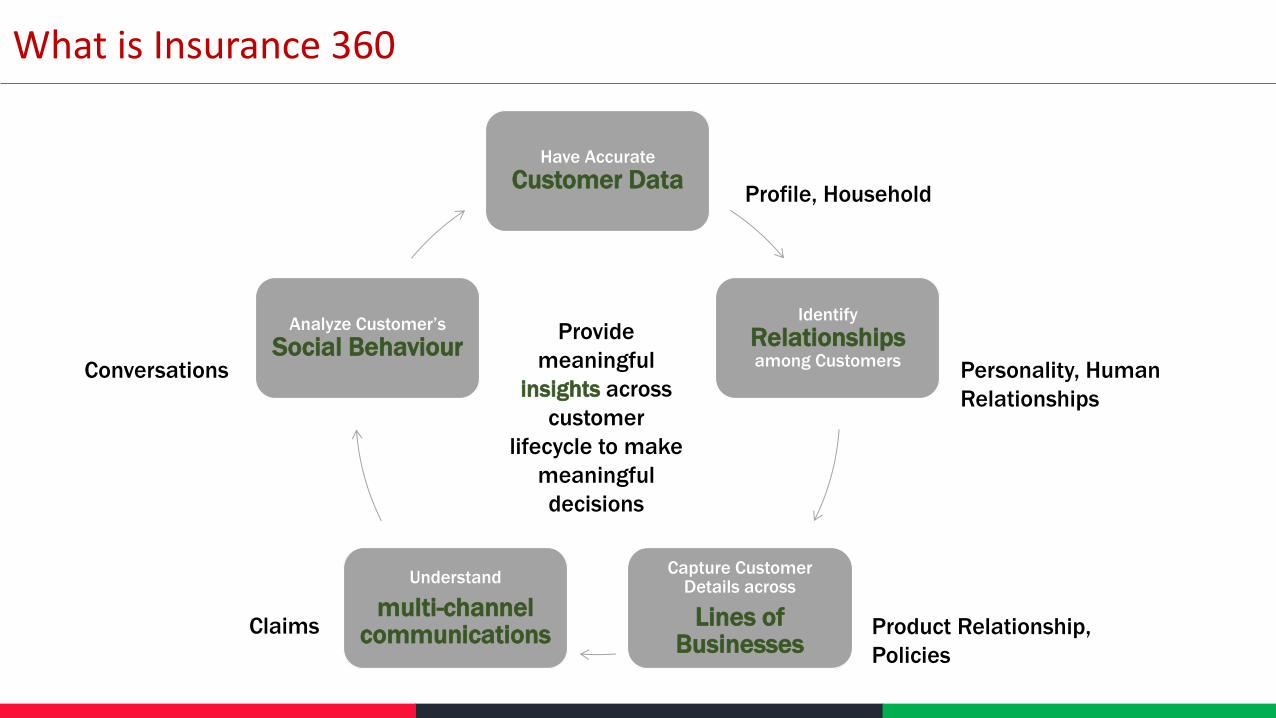

What is Insurance 360

Have Accurate

Customer Data

Identify

Relationships among Customers

Capture Customer Details across

Lines of Businesses

Understand

multi-channel communications

Analyze Customer’s

Social Behaviour

Profile, Household

Personality, Human

Relationships

Product Relationship,

Policies

Claims

Conversations

Provide

meaningful

insights across

customer

lifecycle to make

meaningful

decisions

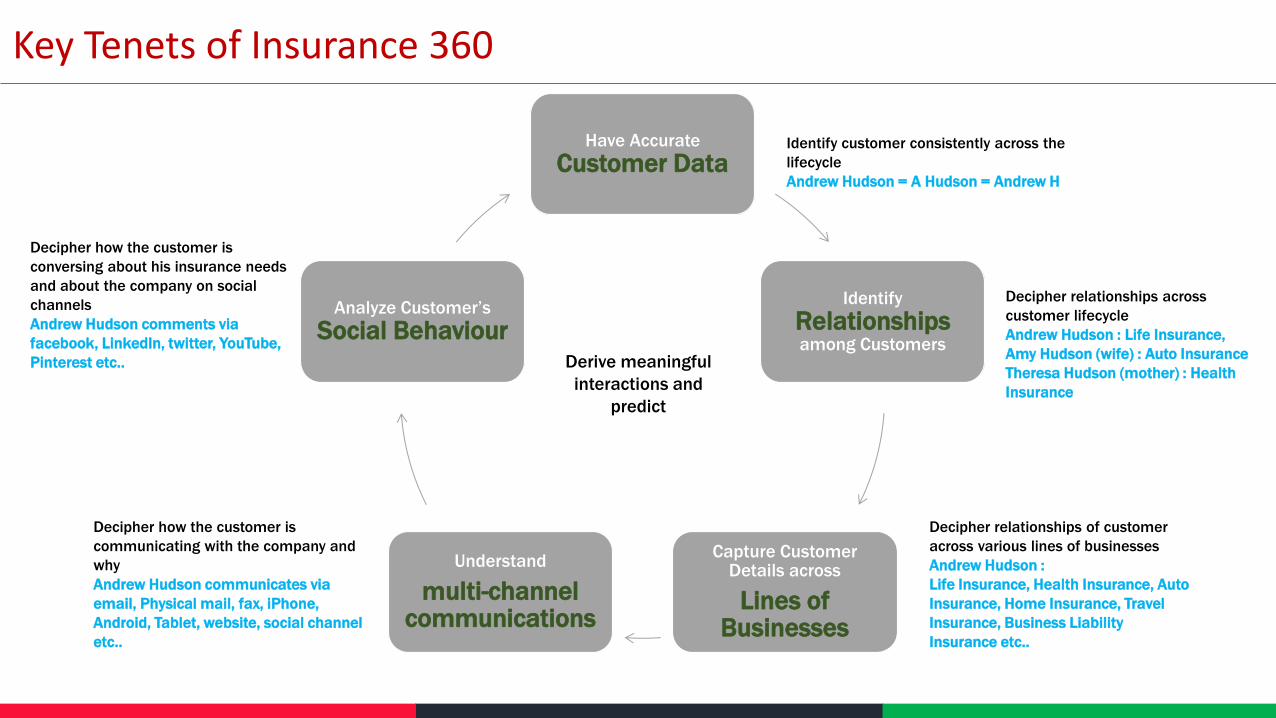

Key Tenets of Insurance 360

Have Accurate

Customer Data

Identify

Relationships among Customers

Capture Customer Details across

Lines of Businesses

Understand

multi-channel communications

Analyze Customer’s

Social Behaviour

Identify customer consistently across the

lifecycle

Andrew Hudson = A Hudson = Andrew H

Decipher relationships across

customer lifecycle

Andrew Hudson : Life Insurance,

Amy Hudson (wife) : Auto Insurance

Theresa Hudson (mother) : Health

Insurance

Decipher relationships of customer

across various lines of businesses

Andrew Hudson :

Life Insurance, Health Insurance, Auto

Insurance, Home Insurance, Travel

Insurance, Business Liability

Insurance etc..

Decipher how the customer is

communicating with the company and

why

Andrew Hudson communicates via

email, Physical mail, fax, iPhone,

Android, Tablet, website, social channel

etc..

Decipher how the customer is

conversing about his insurance needs

and about the company on social

channels

Andrew Hudson comments via

facebook, LinkedIn, twitter, YouTube,

Pinterest etc.. Derive meaningful

interactions and

predict

Key Enablers

Have Accurate

Customer Data

Identify

Relationships among Customers

Capture Customer Details across

Lines of Businesses

Understand

multi-channel communications

Analyze Customer’s

Social Behaviour

6. MDM, Datawarehouse, Datascience

3. RPA, AI & Machine

Learning

4. Mobile

Enablement

5. Socialytics

1. Analytics

2. Datascience, AI, Self Service

Executive Team Considerations

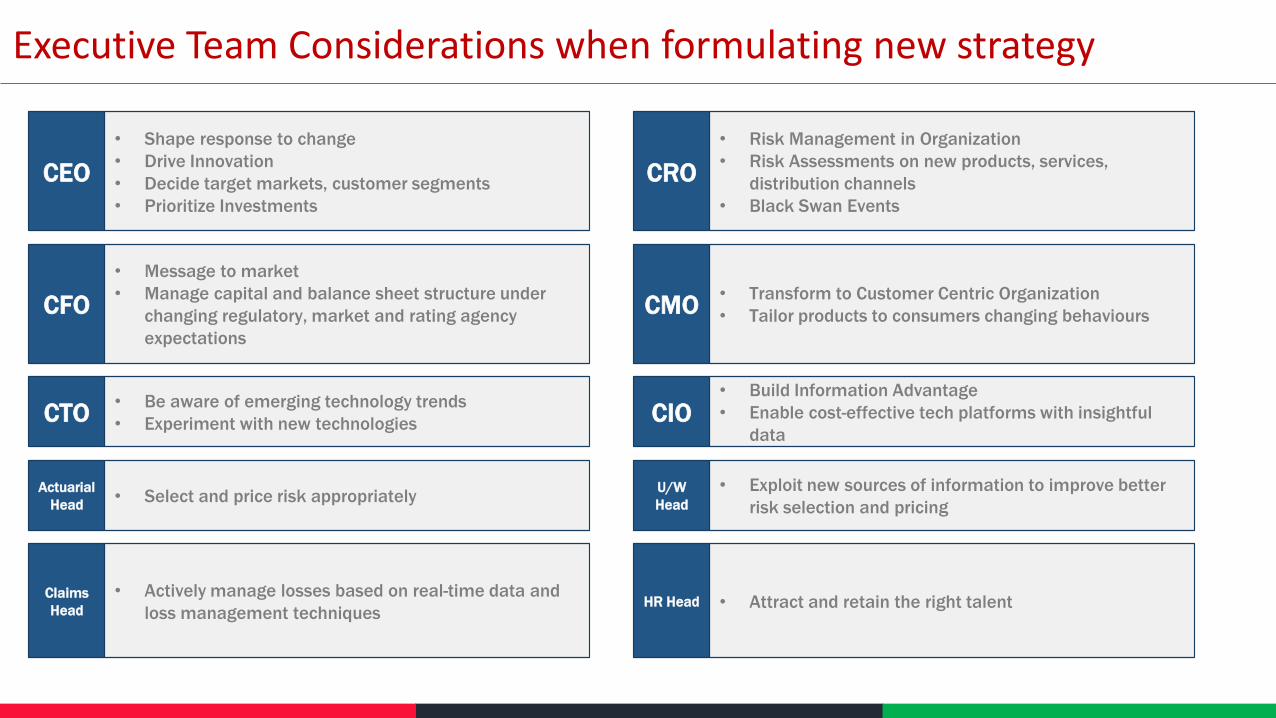

Executive Team Considerations when formulating new strategy

• Shape response to change

• Drive Innovation

• Decide target markets, customer segments

• Prioritize Investments

• Risk Management in Organization

• Risk Assessments on new products, services,

distribution channels

• Black Swan Events

• Message to market

• Manage capital and balance sheet structure under

changing regulatory, market and rating agency

expectations

• Transform to Customer Centric Organization

• Tailor products to consumers changing behaviours

CEO CRO

CFO CMO

• Be aware of emerging technology trends

• Experiment with new technologies CTO • Build Information Advantage

• Enable cost-effective tech platforms with insightful

data CIO

• Select and price risk appropriately Actuarial

Head

• Exploit new sources of information to improve better

risk selection and pricing

U/W

Head

• Actively manage losses based on real-time data and

loss management techniques

Claims

Head • Attract and retain the right talent HR Head

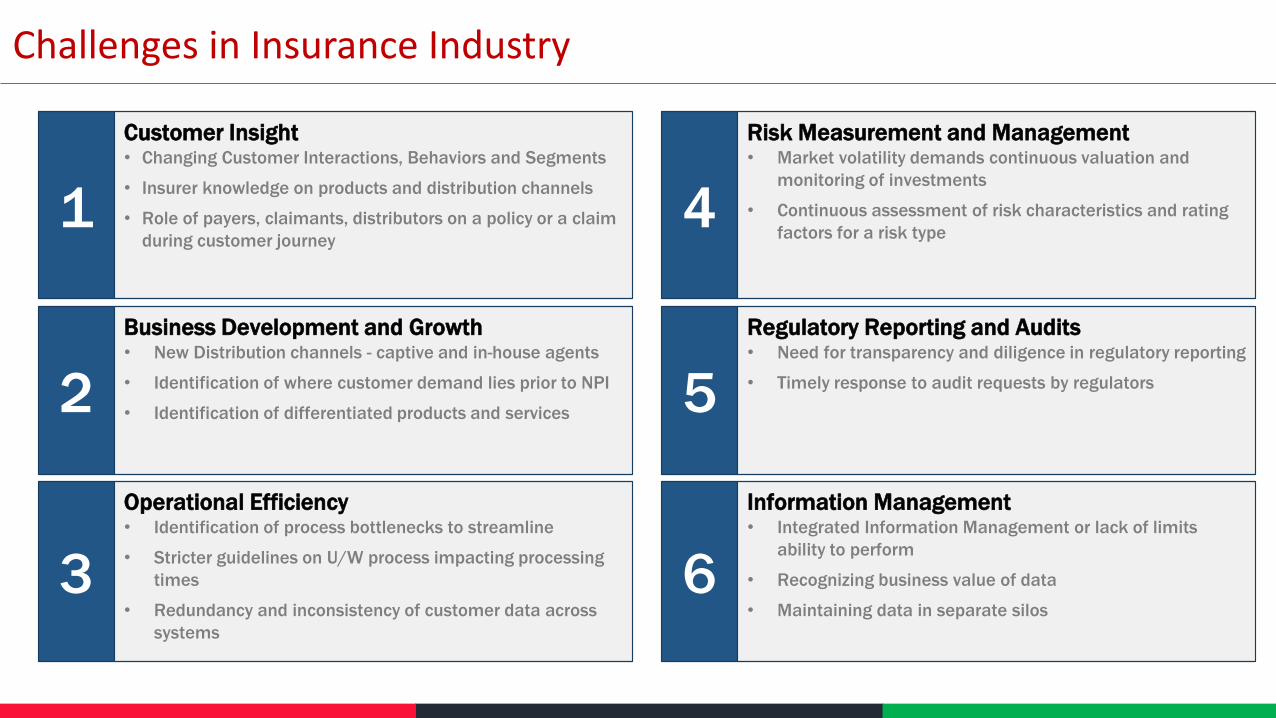

Challenges in Insurance Industry

1

2

3

Customer Insight • Changing Customer Interactions, Behaviors and Segments

• Insurer knowledge on products and distribution channels

• Role of payers, claimants, distributors on a policy or a claim

during customer journey

Business Development and Growth • New Distribution channels - captive and in-house agents

• Identification of where customer demand lies prior to NPI

• Identification of differentiated products and services

Operational Efficiency • Identification of process bottlenecks to streamline

• Stricter guidelines on U/W process impacting processing

times

• Redundancy and inconsistency of customer data across

systems

4

5

6

Risk Measurement and Management • Market volatility demands continuous valuation and

monitoring of investments

• Continuous assessment of risk characteristics and rating

factors for a risk type

Regulatory Reporting and Audits • Need for transparency and diligence in regulatory reporting

• Timely response to audit requests by regulators

Information Management • Integrated Information Management or lack of limits

ability to perform

• Recognizing business value of data

• Maintaining data in separate silos

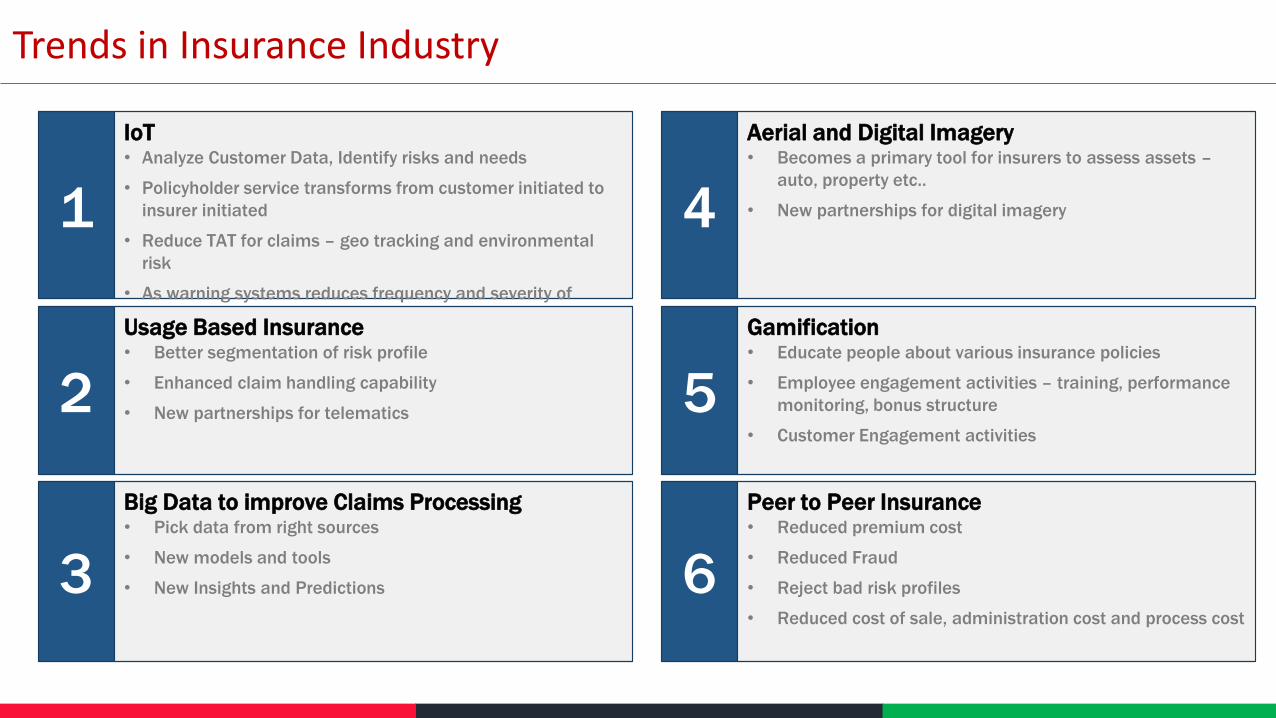

Trends in Insurance Industry

1

2

3

IoT • Analyze Customer Data, Identify risks and needs

• Policyholder service transforms from customer initiated to

insurer initiated

• Reduce TAT for claims – geo tracking and environmental

risk

• As warning systems reduces frequency and severity of

claims

Usage Based Insurance • Better segmentation of risk profile

• Enhanced claim handling capability

• New partnerships for telematics

Big Data to improve Claims Processing • Pick data from right sources

• New models and tools

• New Insights and Predictions

4

5

6

Aerial and Digital Imagery • Becomes a primary tool for insurers to assess assets –

auto, property etc..

• New partnerships for digital imagery

Gamification • Educate people about various insurance policies

• Employee engagement activities – training, performance

monitoring, bonus structure

• Customer Engagement activities

Peer to Peer Insurance • Reduced premium cost

• Reduced Fraud

• Reject bad risk profiles

• Reduced cost of sale, administration cost and process cost

Core Offerings

A Framework for Self Service and Analytics for Insurance

Operations Self Service

Digital Marketing Messaging Event Detection Lead Management Campaigns Offer Management

Analytics

Marketing Sales Pricing Underwriting Claims Operations Actuarial

Campaign decision and

tracking

Channel Spend

Optimization

Loss Modelling Fraud Analysis Claims Propensity

Modelling

Contact Center

Analytics

Price Optimization

Prospect Analysis Agent Reward and

Compensation

Pure Premium

Models

Automated

Underwriting

Claim Fraud Detection IVR Review Economic Modelling

Campaign Effectiveness /

ROI

Agent Productivity Price Optimization Expense Allocation Automated Adjuster

Alerts & Triggers

Call Volume

Forecasting

Solvency II

Customer Segmentation &

Targeting

Forward and

Compensation Analytics

Competitive Market

Analysis

Risk Analytics Expense Management Capacity Planning Igloo Modelling

Customer Acquisition,

Churn and Retention

Reserve Analysis Staffing Optimization Prophet Modelling

Cross-Sell/Up-Sell Subrogation

Effectiveness

Mathematical Reserve

Calculation

IBNR Estimation &

ultimate claims cost

IoT Platform, Data Mining, Data Management, Reporting, Dashboards, Visualization, Model Development and Recalibration

Big Data Platform

Behavioral Data Descriptive Data Interaction Data Deep History Master Data Complex Datasets Social Data

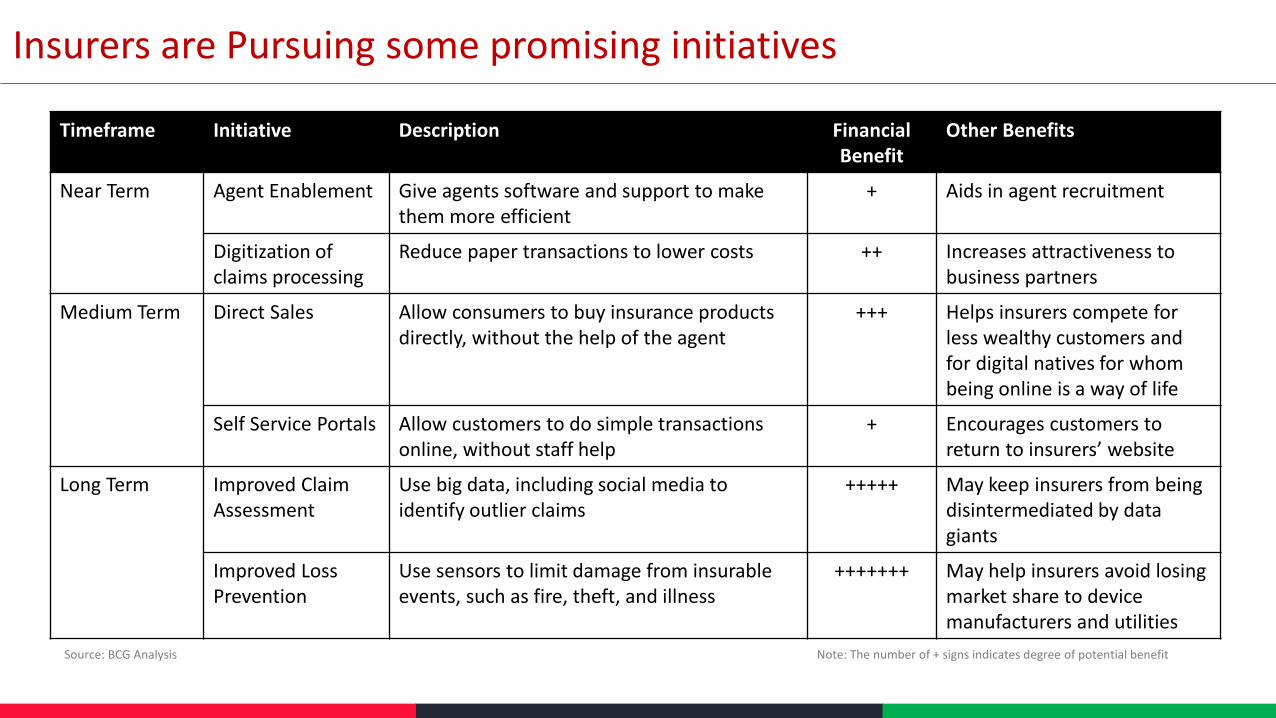

Insurers are Pursuing some promising initiatives

Timeframe Initiative Description Financial Benefit

Other Benefits

Near Term Agent Enablement Give agents software and support to make them more efficient

+ Aids in agent recruitment

Digitization of claims processing

Reduce paper transactions to lower costs ++ Increases attractiveness to business partners

Medium Term Direct Sales Allow consumers to buy insurance products directly, without the help of the agent

+++ Helps insurers compete for less wealthy customers and for digital natives for whom being online is a way of life

Self Service Portals Allow customers to do simple transactions online, without staff help

+ Encourages customers to return to insurers’ website

Long Term Improved Claim Assessment

Use big data, including social media to identify outlier claims

+++++ May keep insurers from being disintermediated by data giants

Improved Loss Prevention

Use sensors to limit damage from insurable events, such as fire, theft, and illness

+++++++ May help insurers avoid losing market share to device manufacturers and utilities

Source: BCG Analysis Note: The number of + signs indicates degree of potential benefit

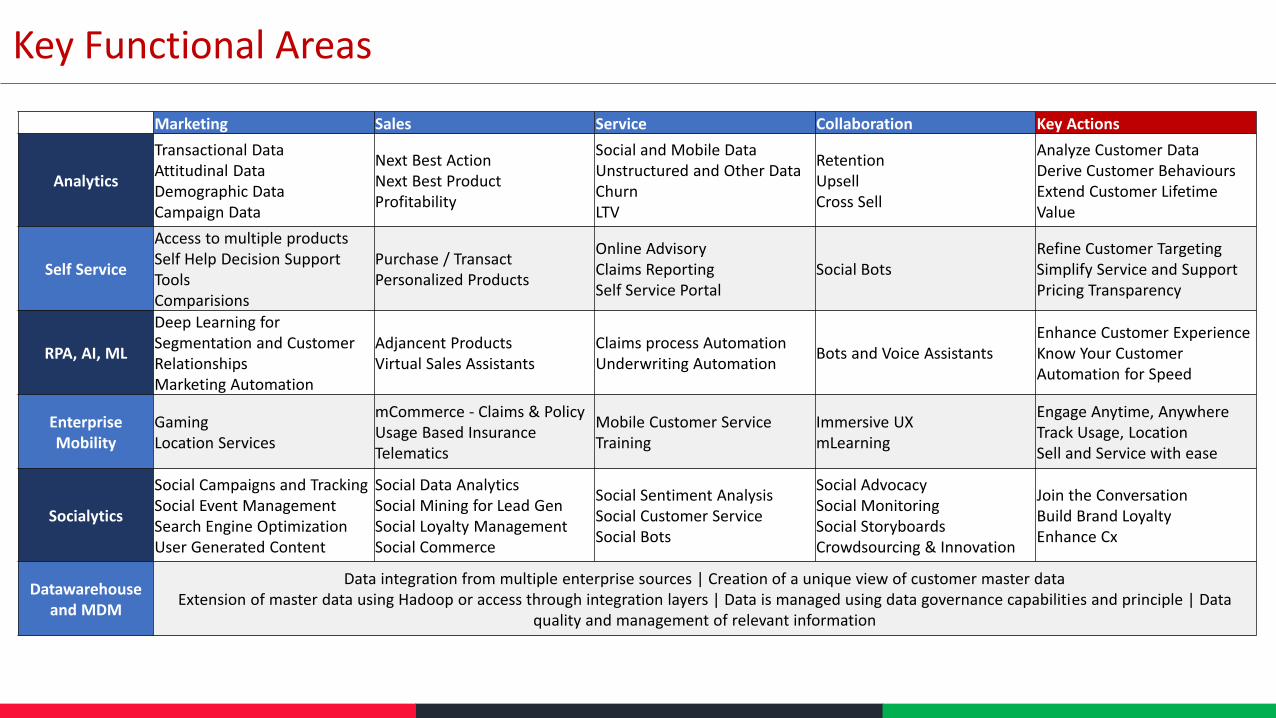

Key Functional Areas

Marketing Sales Service Collaboration Key Actions

Analytics

Transactional Data Attitudinal Data Demographic Data Campaign Data

Next Best Action Next Best Product Profitability

Social and Mobile Data Unstructured and Other Data Churn LTV

Retention Upsell Cross Sell

Analyze Customer Data Derive Customer Behaviours Extend Customer Lifetime Value

Self Service

Access to multiple products Self Help Decision Support Tools Comparisions

Purchase / Transact Personalized Products

Online Advisory Claims Reporting Self Service Portal

Social Bots Refine Customer Targeting Simplify Service and Support Pricing Transparency

RPA, AI, ML

Deep Learning for Segmentation and Customer Relationships Marketing Automation

Adjancent Products Virtual Sales Assistants

Claims process Automation Underwriting Automation

Bots and Voice Assistants Enhance Customer Experience Know Your Customer Automation for Speed

Enterprise Mobility

Gaming Location Services

mCommerce - Claims & Policy Usage Based Insurance Telematics

Mobile Customer Service Training

Immersive UX mLearning

Engage Anytime, Anywhere Track Usage, Location Sell and Service with ease

Socialytics

Social Campaigns and Tracking Social Event Management Search Engine Optimization User Generated Content

Social Data Analytics Social Mining for Lead Gen Social Loyalty Management Social Commerce

Social Sentiment Analysis Social Customer Service Social Bots

Social Advocacy Social Monitoring Social Storyboards Crowdsourcing & Innovation

Join the Conversation Build Brand Loyalty Enhance Cx

Datawarehouse and MDM

Data integration from multiple enterprise sources | Creation of a unique view of customer master data Extension of master data using Hadoop or access through integration layers | Data is managed using data governance capabilities and principle | Data

quality and management of relevant information

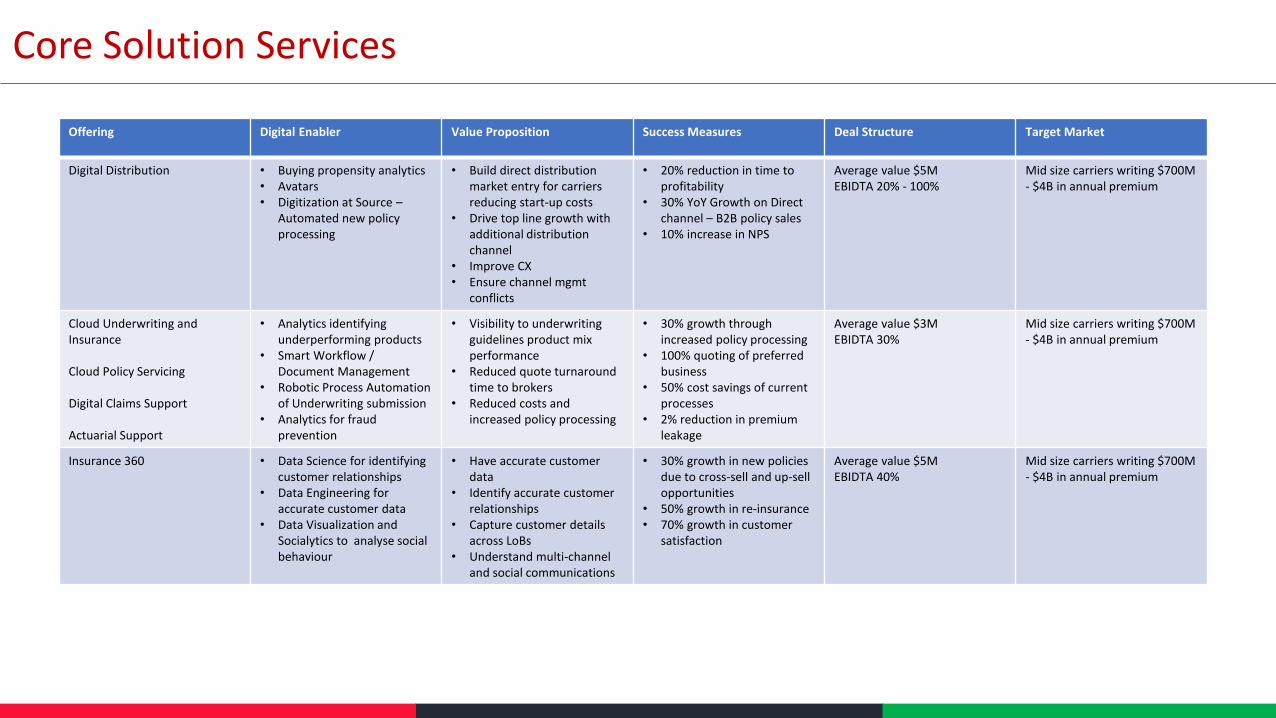

Core Solution Services

Offering Digital Enabler Value Proposition Success Measures Deal Structure Target Market

Digital Distribution • Buying propensity analytics • Avatars • Digitization at Source –

Automated new policy processing

• Build direct distribution market entry for carriers reducing start-up costs

• Drive top line growth with additional distribution channel

• Improve CX • Ensure channel mgmt

conflicts

• 20% reduction in time to profitability

• 30% YoY Growth on Direct channel – B2B policy sales

• 10% increase in NPS

Average value $5M EBIDTA 20% - 100%

Mid size carriers writing $700M - $4B in annual premium

Cloud Underwriting and Insurance Cloud Policy Servicing Digital Claims Support Actuarial Support

• Analytics identifying underperforming products

• Smart Workflow / Document Management

• Robotic Process Automation of Underwriting submission

• Analytics for fraud prevention

• Visibility to underwriting guidelines product mix performance

• Reduced quote turnaround time to brokers

• Reduced costs and increased policy processing

• 30% growth through increased policy processing

• 100% quoting of preferred business

• 50% cost savings of current processes

• 2% reduction in premium leakage

Average value $3M EBIDTA 30%

Mid size carriers writing $700M - $4B in annual premium

Insurance 360 • Data Science for identifying customer relationships

• Data Engineering for accurate customer data

• Data Visualization and Socialytics to analyse social behaviour

• Have accurate customer data

• Identify accurate customer relationships

• Capture customer details across LoBs

• Understand multi-channel and social communications

• 30% growth in new policies due to cross-sell and up-sell opportunities

• 50% growth in re-insurance • 70% growth in customer

satisfaction

Average value $5M EBIDTA 40%

Mid size carriers writing $700M - $4B in annual premium

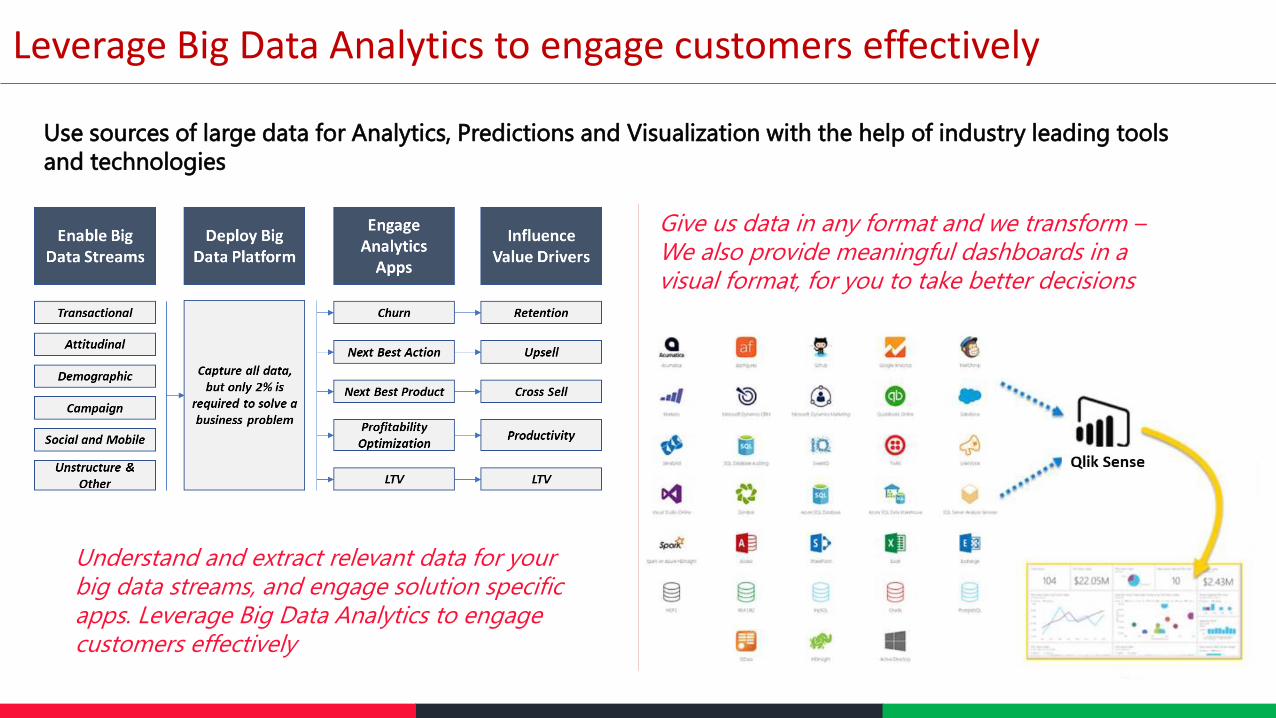

Leverage Big Data Analytics to engage customers effectively

Use sources of large data for Analytics, Predictions and Visualization with the help of industry leading tools

and technologies

Give us data in any format and we transform – We also provide meaningful dashboards in a visual format, for you to take better decisions

Understand and extract relevant data for your big data streams, and engage solution specific apps. Leverage Big Data Analytics to engage customers effectively

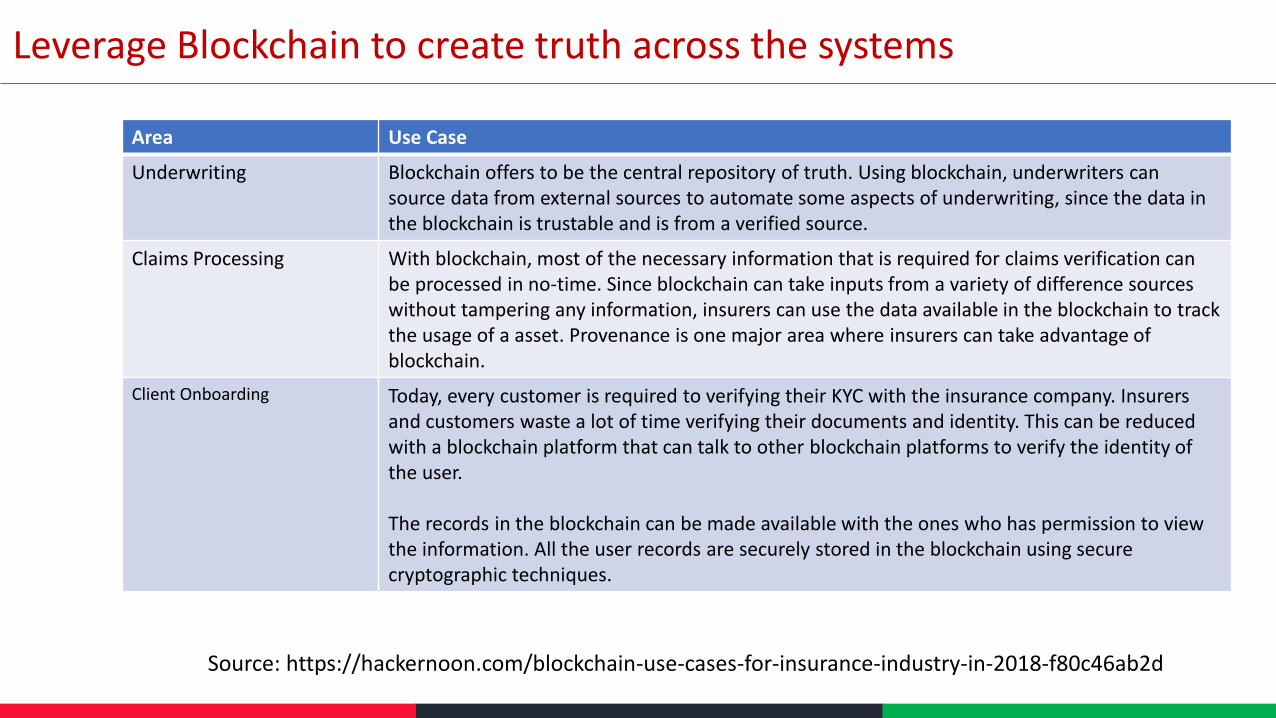

Leverage Blockchain to create truth across the systems

Area Use Case

Underwriting Blockchain offers to be the central repository of truth. Using blockchain, underwriters can source data from external sources to automate some aspects of underwriting, since the data in the blockchain is trustable and is from a verified source.

Claims Processing With blockchain, most of the necessary information that is required for claims verification can be processed in no-time. Since blockchain can take inputs from a variety of difference sources without tampering any information, insurers can use the data available in the blockchain to track the usage of a asset. Provenance is one major area where insurers can take advantage of blockchain.

Client Onboarding Today, every customer is required to verifying their KYC with the insurance company. Insurers and customers waste a lot of time verifying their documents and identity. This can be reduced with a blockchain platform that can talk to other blockchain platforms to verify the identity of the user. The records in the blockchain can be made available with the ones who has permission to view the information. All the user records are securely stored in the blockchain using secure cryptographic techniques.

Source: https://hackernoon.com/blockchain-use-cases-for-insurance-industry-in-2018-f80c46ab2d

About vidEre Soft

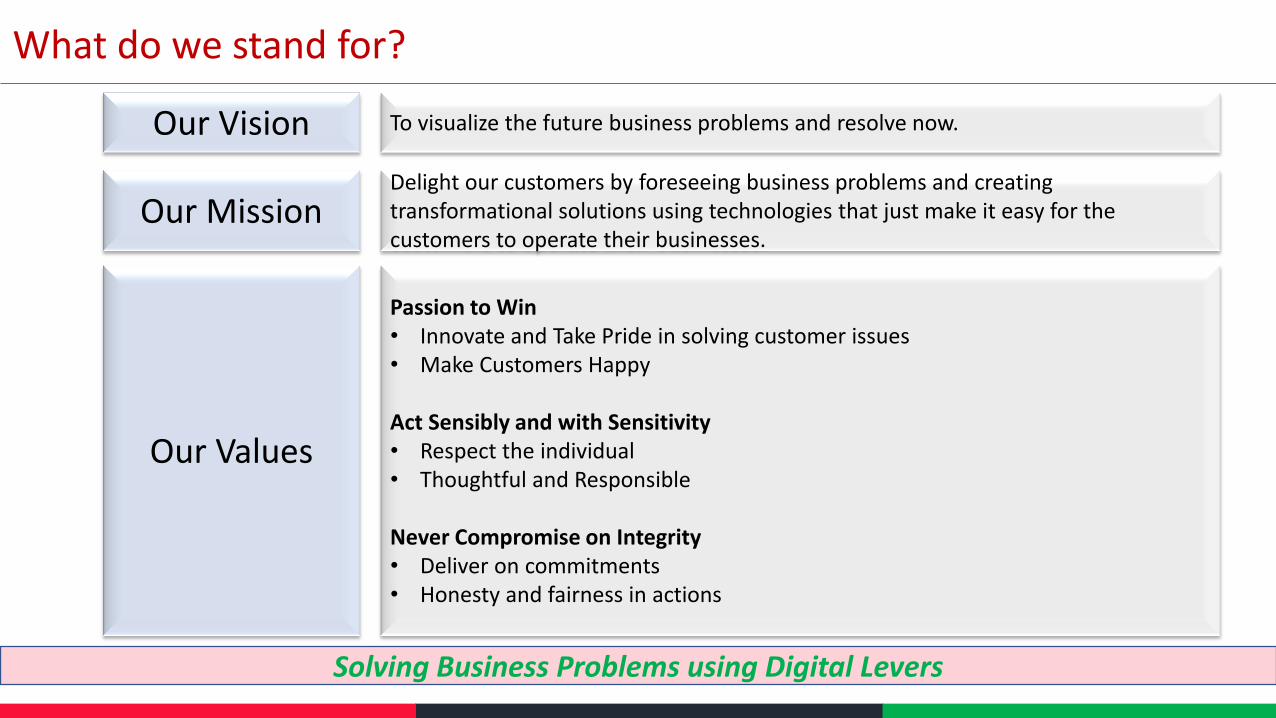

What do we stand for?

To visualize the future business problems and resolve now.

Delight our customers by foreseeing business problems and creating transformational solutions using technologies that just make it easy for the customers to operate their businesses.

Our Vision

Our Mission

Passion to Win • Innovate and Take Pride in solving customer issues • Make Customers Happy Act Sensibly and with Sensitivity • Respect the individual • Thoughtful and Responsible Never Compromise on Integrity • Deliver on commitments • Honesty and fairness in actions

Our Values

Solving Business Problems using Digital Levers

Defining Digital @ vidEre

A client interfaces with various systems. These system touch points could be internal (employee, board) or external (customer, partner/supplier).

Digital is a design, for the clients’ systems, to easily conduct business electronically, that brings in customer delight, through

simplicity of engagement and efficiency of experience.

This design when implemented on Client’s Business Systems and integrated with supporting systems through the use of technology is called Digital Transformation.

Employee, Board/Share-holders, Customers, Partners/Suppliers are the 4 pillars of any Digital Transformation.

The Outcome of Digital Transformation is “Customer Value Creation”

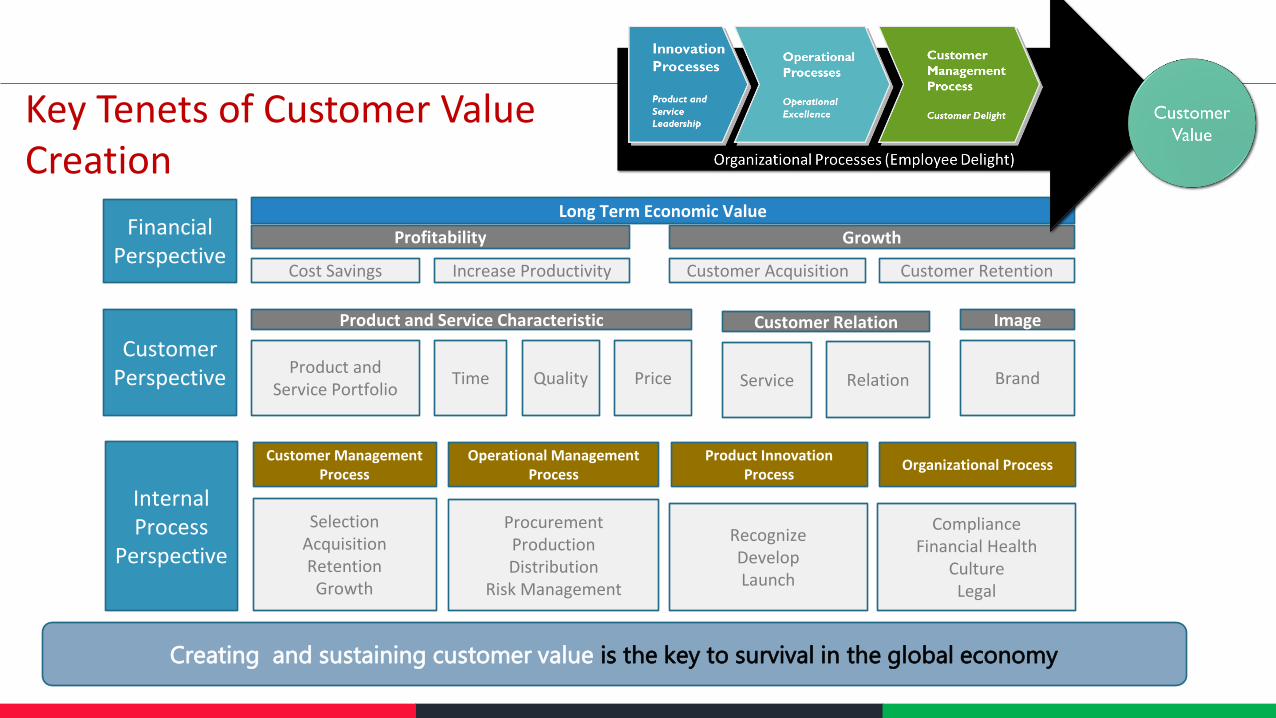

Key Tenets of Customer Value Creation

Financial Perspective

Customer Perspective

Internal Process

Perspective

Cost Savings Increase Productivity Customer Acquisition Customer Retention

Profitability Growth

Long Term Economic Value

Product and Service Portfolio

Time

Product and Service Characteristic

Quality Price Service Relation

Customer Relation

Brand

Image

Selection Acquisition Retention

Growth

Customer Management Process

Procurement Production Distribution

Risk Management

Operational Management Process

Recognize Develop Launch

Product Innovation Process

Compliance Financial Health

Culture Legal

Organizational Process

Creating and sustaining customer value is the key to survival in the global economy

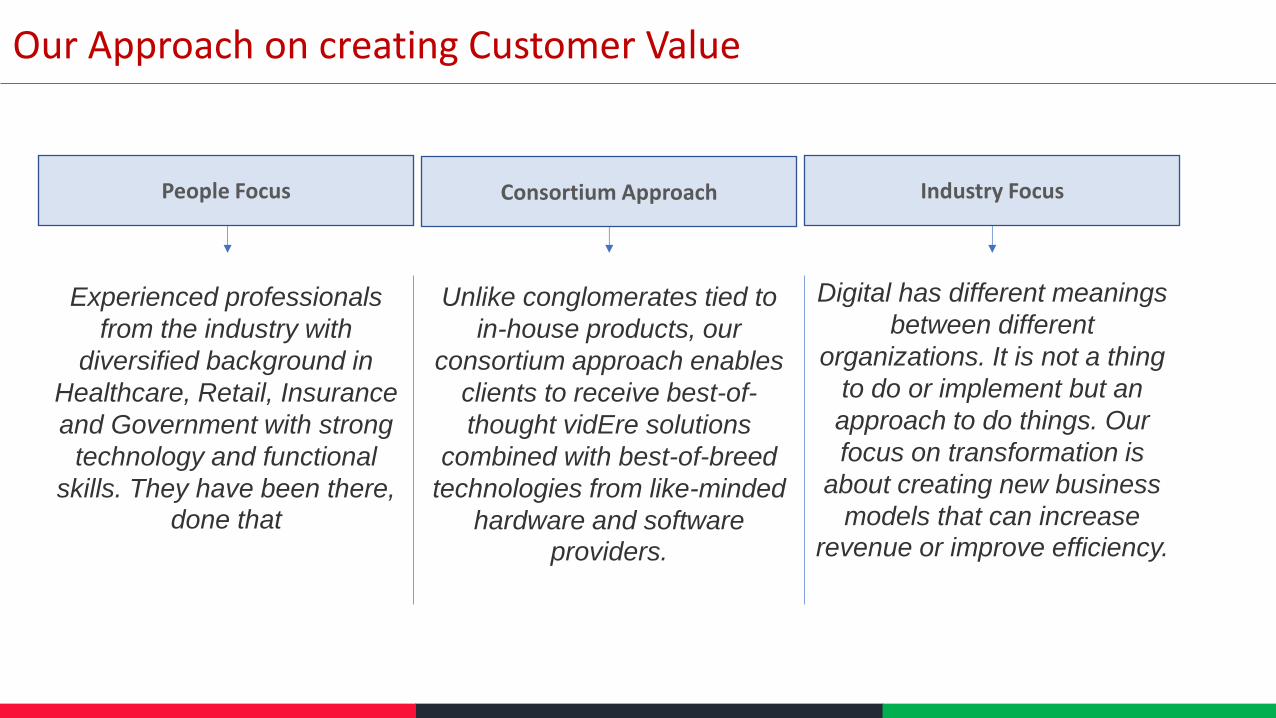

Our Approach on creating Customer Value

Experienced professionals

from the industry with

diversified background in

Healthcare, Retail, Insurance

and Government with strong

technology and functional

skills. They have been there, done that

Unlike conglomerates tied to

in-house products, our

consortium approach enables

clients to receive best-of-

thought vidEre solutions

combined with best-of-breed

technologies from like-minded

hardware and software providers.

Digital has different meanings

between different

organizations. It is not a thing

to do or implement but an

approach to do things. Our

focus on transformation is

about creating new business

models that can increase revenue or improve efficiency.

People Focus Consortium Approach Industry Focus

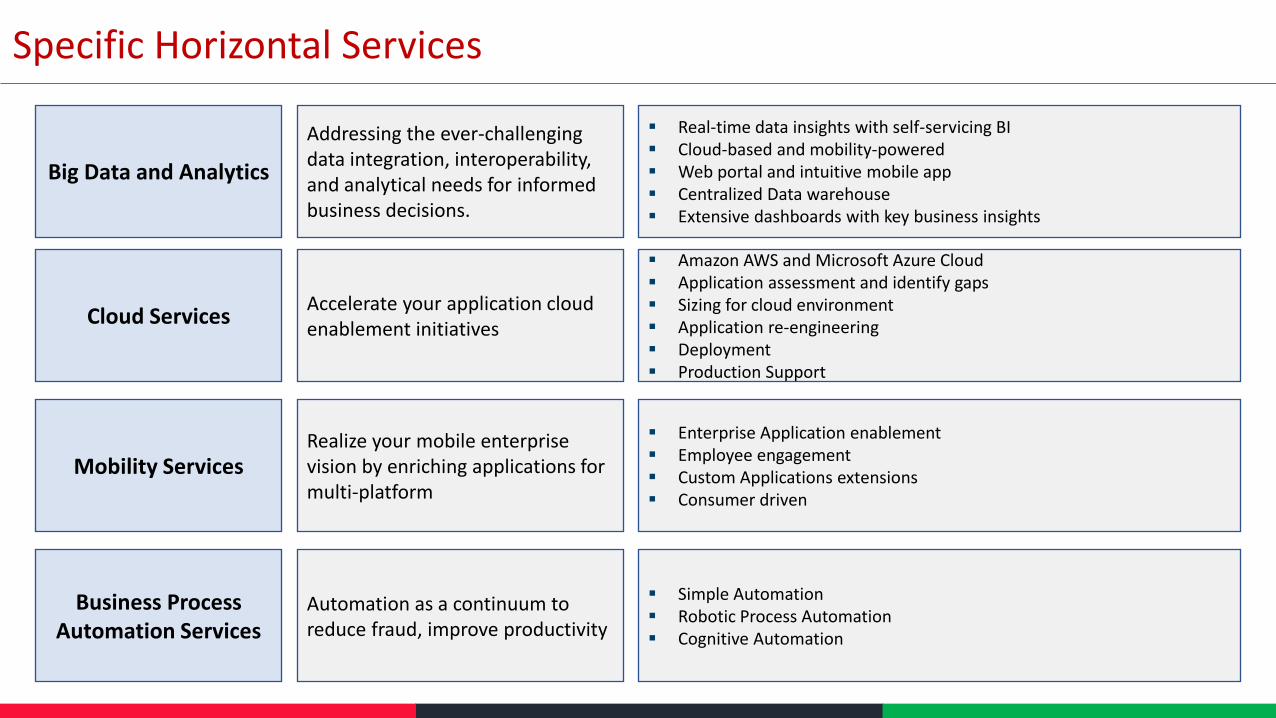

Specific Horizontal Services

Big Data and Analytics

Real-time data insights with self-servicing BI Cloud-based and mobility-powered Web portal and intuitive mobile app Centralized Data warehouse Extensive dashboards with key business insights

Addressing the ever-challenging data integration, interoperability, and analytical needs for informed business decisions.

Cloud Services

Amazon AWS and Microsoft Azure Cloud Application assessment and identify gaps Sizing for cloud environment Application re-engineering Deployment Production Support

Accelerate your application cloud enablement initiatives

Mobility Services

Enterprise Application enablement Employee engagement Custom Applications extensions Consumer driven

Realize your mobile enterprise vision by enriching applications for multi-platform

Business Process Automation Services

Simple Automation Robotic Process Automation Cognitive Automation

Automation as a continuum to reduce fraud, improve productivity