Embed Size (px)

Citation preview

INSTRUCTOR

The author gratefully acknowledges the assistance of busy agents, leadership, and

KWRI leaders and staff who gave generously of their precious time to provide

insights, data, quotes, and editing time to this project.

Many of the top distressed property specialist agents who participated have literally

invented their businesses while building them. Some practiced in previous distressed

markets. Others were newly arrived agents who have boldly pioneered much of what

is taught here— about how to survive and thrive in unusual times.

While Keller Williams Realty, Inc. (KWRI) has taken due care in the preparation of all

course materials, we do not guarantee their accuracy now or in the future. KWRI makes

no express or implied warranties with regard to the information and programs presented

in the course, or in this manual, and reserves the right to make changes from time to

time.

This manual and any course in which it is used may contain hypothetical exercises that

are designed to help you understand how Keller Williams calculates profit sharing

contributions and distributions under the MORE System, how Keller Williams

determines agents’ compensation under the Keller Williams Compensation System, and

how other aspects of a Keller Williams Market Center’s financial results are determined

and evaluated. Any exercises are entirely hypothetical. They are not intended to enable

you to determine how much money you are likely to make as a Keller Williams Licensee

or to predict the amount or range of sales or profits your Market Center is likely to

achieve. Keller Williams therefore cautions you not to assume that the results of the

exercises bear any relation to the financial performance you can expect as a Keller

Williams Licensee and not to consider or rely on the results of the exercises in deciding

whether to invest in a Keller Williams Market Center. If any part of this notice is unclear,

please contact Keller Williams’ legal department.

Material excerpted from The Millionaire Real Estate Agent appears courtesy of The

McGraw-Hill Companies. The Millionaire Real Estate Agent is copyright © 2003–2004

Rellek Publishing Partners, Ltd. All rights reserved.

Material excerpted from Shift appears courtesy of McGraw-Hill. Shift is copyright ©

2010, 2009 Rellek Publishing Partners, Ltd. All rights reserved.

Copyright Notice

All other materials are copyright © 2016 Keller Williams Realty, Inc. or its licensors. All

rights reserved. No part of this publication and its associated materials may be

reproduced or transmitted in any form or by any means without the prior permission of

KWRI.

Note: When calling or emailing prospective customers, comply with federal and state Do Not Call (DNC) and spam laws and the policies of your local Market Center.

Our education offers associates the ability to grow as individuals while growing your business.

Deep discount on your continuing education as a KW Associate

Customer support 7 days a week via phone, chat, and email

Tablet-friendly course delivery, available anytime, anywhere

Leverage your time and energy to get the best education available

Multi-state packages 5-day free trial – Unlimited access, no

credit card required

Commercial & residential courses Monthly payment plan option

4.8/5 star student rating 98% state exam pass rate

Save 20% at KWU.TheCEShop.com

with promotional code: KW20

Series Objectives................................................................................................................. 7

Working with Buyers Objectives ..................................................................................... 8

Graduate Study: Where to Look Next ............................................................................ 9

Getting the Most Out of This Experience ................................................................... 13

Why a Buyer Boom? ........................................................................................................ 15

Get Your Unfair Share! ................................................................................................... 16

Which Way to Go ............................................................................................................ 17

Why the Buyer Side? ........................................................................................................ 18

Seven Benefits for Buyers ............................................................................................... 21

Five Buyer Realities: Keys to Success ............................................................................ 24

Great Opportunity to Learn and Earn .......................................................................... 26

It’s Your Choice: Choose to Act .................................................................................... 32

Mindset: Distressed Is a Different World ..................................................................... 33

Take a Critical Look at Your Market ............................................................................. 44

Personal Shift—Through the Homeowner’s Eyes ...................................................... 48

The Distressed Property Process—Foreclosure and More ........................................ 52

Know Your State Laws and Regulations ...................................................................... 53

The Distressed Property Timeline ................................................................................. 55

Three Types of Buyers .................................................................................................... 63

How to Find and Attract Buyers .................................................................................... 65

How to Find Properties .................................................................................................. 69

Auction Opportunities .................................................................................................... 72

Special Needs of Investors ............................................................................................. 74

Lead Conversion Real-Play ............................................................................................ 78

Buyer Service Cycle, Distressed Version ...................................................................... 83

Make Offers That Close ................................................................................................. 84

Closing ............................................................................................................................... 93

Some Final Service Suggestions ..................................................................................... 96

From Aha’s to Achievement ........................................................................................ 102

Don’t Forget Your Evaluation!.................................................................................... 103

This guide is one of three in a series from Keller Williams University (KWU) called

SHIFT Tactic 11: Distressed Properties. The course manuals in the series are:

SHIFT Tactic 11: Distressed Properties: Listing Short Sales

SHIFT Tactic 11: Distressed Properties: Listing REOs

SHIFT Tactic 11: Distressed Properties: Working with Buyers

SHIFT Tactic 11: Distressed Properties provides an overview of how the distressed

property market—the “market of the moment”—works, and how to gain a foothold

in short sale and REO (bank-owned property) and win all the business you want.

These markets can grow dramatically as they evolve with ever-changing market

conditions. Now you will learn from the top agents who have succeeded in this

market as they share their experiences and their wisdom.

The three-guide series titled SHIFT Tactic 11: Distressed Properties is meant to help

you learn how to pursue your real estate business differently—to succeed with buyers

and sellers of distressed properties. These course manuals will show you:

Skills you will need to excel in this market and how to develop them

Mindset challenges you will face and how to deal with them

Resource demands in the distressed property business

Action steps to take now to propel your business forward

Research calls were made to Keller Williams associates and leadership in Canada.

Their comments, and data generated in the SHIFT 2 Tour research in early 2009,

showed that distressed properties represent a very small percentage of Canadian

transactions—in the worst cases, less than 5 percent. Therefore, these courses focus

entirely on U.S. markets.

At the conclusion of this guide, Working with Buyers, you will

See the Opportunity: Understand the power and scope of the buyer side

opportunity in distressed properties.

Know Buyer Motivation: Understand why buyers need agents to help them

take advantage of this market, and how to provide the help they need.

Grasp the Market Background and Foreclosure Process: Have a working

understanding of distressed markets, how they came to be, and how they affect

agents and consumers. Be able to effectively consult about this with your

clients.

Know What Changes to Expect: Learn where to watch for information on

new industry trends and government policies that will change your market.

Know How to Be a Local Economist: Know how to analyze your market.

Are there likely to be more distressed properties or less? What factors will

determine what happens? How may prices be affected?

Know Sources of Buyer Business: Learn how to find and attract buyers to

distressed properties.

Understand Investor Needs: Learn how to address the special needs of

investors.

Be a Better Partner with Listing Agents: Learn the importance of a winning

mindset in cooperating with REO and short sale listing agents.

Know How to Improve Offer Acceptance and Close Rates: Learn tips for

helping ensure offers are accepted and transactions close.

Make a Sound Choice: Discover what aspect of the distressed property

business you will focus on—is working with buyers the best option for you?

These three guides are not the last word on any of these topics. They are offered as

strong “undergraduate level” material. They help you define and build your

foundation in distressed property. So where do you go to take your learning to the

next level? Here are paths you can take after attending this course:

Distressed property markets, like all markets, are always changing. In distressed

property markets, agents need to be especially watchful of changes.

It flags an area where you need to monitor change

carefully. Wherever possible, we’ll point you to where you

can get more information on the topic.

Guard your consultant and fiduciary role. Stay on top of

the following:

Law: Federal, state, and local laws governing

foreclosure and possible solutions for homeowners

facing foreclosure

Industry Regulations: Your local real estate board and

MLS’s standards for listing, marketing, and closing

distressed property sales

Market Trends: Be especially watchful for important

turns of events that impact market pricing and sales

volume. For example, are defaults in your market

increasing or decreasing?

Your Business Mix: Default trends may be especially

important to you if your business is built mainly on

listing and selling short sales, or if you are balancing a

mix of traditional and distressed property business

The tools of the Career Growth Initiative are a synergistic system that fuel the Four

Conversations with evidence.

V i s i o n T o o l s

Listing Management: A yearly plan for profitability through growth in market share.

Listings (Monthly): Monthly tracking with adjustments to help you achieve your yearly goal.

Pipeline (Buyers/Sellers): Identify on a daily basis whether your activities will turn your goals into reality.

V a l u e a n d V a l i d i t y T o o l s

Agent Trend: Report that tracks your growth in market share and critical

levers in your business to assess performance and opportunities.

Agent Language of Real Estate (LORE): Provides evidence of your value

by comparing the growth of your business to that of your board, your

subdivision, your Market Center, your Region, etc.

Local Expert: The story of your expertise to underscore your validity to clients.

T h r i v i n g T o o l s

GCI: Track your GCI against your expenses to identify your Break-even Day. INSTRUCTOR:

Walk students through the Growth Initiative tools and the four conversations.

TELL: Your CGI focus will lend to your validity as the Local Expert. If you haven’t

met with your TL to set up your CGI Calculator, please get with your TL!

Lis t ing

Management

L is t ings

(Monthly)

Pipel ine

(Buyers /Sel le rs) VALUE GCI

Agent

Trend

Agent

LORE

Local

Expert

When you are able to quantify and communicate the benefits of the value you

deliver, you will create a Wall of Value in your business that attracts listings and

creates closings.

C o m m u n i c a t e V a l u e

Look for ways to share your Wall of Value to grow your business:

Listing and Pre-Listing Presentations

Buyer Consultations

Marketing materials

Conversations with allied resources

For more, go to the Career Growth Initiative page on KWConnect.com

There are often three types of people in a typical training class. Which one are you?

Has to be there, doesn’t want to be there, and doesn’t know why

they’re there.

A day in training is better than a day on the job.

Excited and curious about the new knowledge, skills, and tools

they will discover in class.

Instructor:

Review the

three types of

learners. Point

out that

Prisoners and

Vacationers

don’t get

much of

anything out

of class.

Explorers who

embrace

learning for

earning sake,

participate

fully, and

commit to

implementing

what they

learn are the

true winners

in class.

Remind them

(and yourself)

that this is a

DOing class!

Okay, so what happened? In 2006 the real estate market began experiencing what

would become an historic shift in real estate values in the United States.

From 2000 to 2006, according to The Skinny on the Housing Crisis by attorney and

business writer Jim Randel, “Home prices across the United States increased by 15

percent per year and 3 million new households became new homeowners. During

that same period, mortgage debt rose from $6 trillion in 2000 to $13 trillion in

2006—premised on the belief that housing values would always go up.”

As this course will show you in chapter 3, “always go up” never happens.

Up markets are inevitably followed by down markets. In the three years from mid-

2006 to mid-2009, the median price of homes in the United States declined 30

percent and one in four homes with a mortgage were worth less than the amount of

mortgage debt on the property.

This value plunge, in the face of continuing low interest rates, leads to a resurgence

of buying—at depressed prices. Many other factors also come into play, and this

course covers them. Market shifts have occurred in the past and, in the ever-evolving

world of real estate, they will shift again. This course will help prepare you to work

with buyers of distressed properties whenever a shift occurs.

In a shifted market, buyers look for great deals and consider buying foreclosed

properties—and they will need you to help them.

Low prices of foreclosed properties across the country create a breakthrough with

buyers. It’s called a buyer’s market and finally buyers, previously hesitant about

buying in a downward-moving market for fear of timing it wrong, shift gears. Pent-

up buyer demand is begins being released. Both individuals seeking homes and

investors seeking cash flow and appreciation appear in increasing numbers—in some

cases, creating multiple offer situations for distressed properties.

Buyers come in various types, with varying motivations, and have lots of questions

that need answering. Are they experienced investors looking to expand their

collection of income-producing rental homes? Or, are they beginner investors—

homeowners looking to take their first leap into the rental world? Are they current

homeowners who suddenly find they can afford to move up in a way they used to

believe was not possible? Or, are they one of the most prominent groups today, first-

time buyers, looking to take advantage of a big new tax break and tempted by lower

prices than they’ve ever seen?

Property starts to sell. As Gary Keller likes to say, “You need to get your unfair

share.” Is becoming an agent who works exclusively with buyers your best plan of

action? What do you need to know about how distressed properties are listed and

sold?

As banks consolidate and are pressured for time by more and more foreclosed

inventory, it becomes harder, but not impossible, to find listing relationships and

easier to go for the buyer side opportunity.

As mentioned previously, all three guides that comprise the SHIFT Tactic 11:

Distressed Properties series present options for working in distressed property

markets. They look at both the listing side and the buyer side—what you need to

know, what you need to do, and how to do it.

A shifted market is your chance to make a decision about which way to go.

As you learn what you need to know and do to succeed, you will see that there are

just three paths to follow:

Listing Side: Focus on listing short sales or REOs—top listing agents tend

to specialize in one or the other.

Buyer Side: Focus on the buyer side—learn about the opportunities and

needs of buyers in this market; learn about short sales, REOs, and auctions—

and be able to sell all types of distressed properties.

Both Sides: Build a team that works both sides—by listing distressed

properties and working the buyer side with a focused buyer agent or agents.

Let’s look deeper into why the buyer side can be a great opportunity for you.

Any of these paths can lead to a very successful, profitable business. Each has its

own special rewards–and some risks. This guide takes the view that the buyer side is

the way to go because it is:

Faster – the quickest way to get involved and make money today

Cheaper – there is less financial risk than on the listing side

(especially less risk than listing REO properties)

Easier – while you need to know and follow the rules and guidelines that get

offers accepted and deals closed, the listing agents have way more to learn and

deal with.

And most importantly, buyers need you now more than ever to navigate this

potentially confusing, frustrating, and ultimately satisfying landscape!

What’s working in your favor if you choose to work the buyer side? Besides eager

buyers, what makes working in a shifted market the faster, cheaper, easier way to go?

Ample short sale and/or REO inventory to sell in most markets.

Motivated parties—on all sides of these transactions.

Economic stability could return as the government responds to the shift.

Working on the buyer side of distressed property sales can be the best part of

operating in a tough real estate environment. The reasons have to do with both

motivation and money!

Institutions and individuals list a lot of property for sale, and motivated buyers start

to gobble it up. In some markets, multiple offers on these properties can be

common. Although the flow of inventory may slow some—and there can still be

plenty of inventory if you look for it.

Distressed property is a term with largely negative connotations, and for good

reason. Keep in mind that what agents, in particular, need to focus on are the

positive motivational forces at work in these markets.

Motivated sellers needing short sales

(providing the lender agrees to the price).

Motivated institutional lenders holding REO properties.

Motivated investors seeking a great deal—one-off, or in volume purchases.

They may want to buy rental property for cash flow or investment property

they can fix and flip when values rise.

Motivated move-up buyers seeking to step up to that dream home that is

suddenly affordable!

Motivated first-time buyers are not unique to distressed markets, but very

low prices are especially appealing to these consumers.

Motivated real estate agents looking to build businesses damaged by market

shifts that cut their sales volume.

Buyers can also being motivated by emerging positive economic news in a shifted

market.

Recovery in real estate sales seems to track with other positive economic factors

including:

The U.S. government may implement stimulus programs that pump money

into state and local economies for improvement projects.

Stability could begin to return to the banking industry.

Steadying private and public employment may begin to occur (corporate profit

improvement in many sectors, government job growth).

You can succeed with these buyers, but you must build distressed property-specific

knowledge and skills. This includes knowing the clear benefits for buyers who want

distressed property—and the top keys for successfully buying it.

The difference now is you need to know some rules and phenomena that are

different than in more balanced markets. Getting that knowledge fast and

communicating it well turns you into what SHIFT calls “the local economist”—the

agent who helps people see the opportunity in these times.

This is what opportunity is made of for buyers, in headline form. You should

understand and be articulate about each of these stories in depth—as they relate to

your local market:

All pricing is local but short sale and REO prices do go below the rest of the current

market—anywhere from 10 percent to 40 percent less, according to top distressed

property agents.

Declining prices relative to income make move ups more affordable. Postponed

“dream home” purchases are suddenly possible for people who never expected the

affordability levels that a shifted market creates. Home affordability may rise

significantly.

Major national lenders may move very aggressively to avoid having foreclosed

properties on their books. This can create major opportunities for agents skilled at

working with buyers of distressed properties.

Financing is available, though it may be harder to get than it was before the market

shifted. Lower home prices do mean a given amount of cash down builds more

equity than before. Example: Your $20,000 down meant 10 percent equity in a

$200,000 property. The market has driven that home to $150,000. You buy it, and

now have one-third more equity than you would have had before.

REO and Short Sale listing agents—though they cannot make decisions about final

sale prices—are highly motivated to get property priced right by banks and asset

managers. They are also motivated to attract strong buyer agents who they will train

to know the REO or Short Sale selling business. Some listing agents work both short

sales and REOs. The majority tend to specialize in one or the other.

Distressed sellers want out from under their problems. They are not enjoying their

situation and want to make changes as fast as possible—especially changes that

relieve them of personal, financial, and emotional pressure. Many of them qualify for

a short sale of their property. But, even sellers with equity want to move quickly—

before the market or personal circumstances put them in a situation they don’t want.

Waiting means trying to time the market better, and if buyers do, they may miss the

bottom and end up buying on the way back up.

In either REO or short sale buying, you and your client are going to encounter the

bank-mandated “As Is” Addendum, or some similar disclaimer. This is standard

procedure in distressed property markets.

Banks are looking for a non-negotiated clean sale. One of the keys is working with

buyers who understand—and accept—that reality.

This can be a tough concept for buyers and agents raised in traditional markets.

Buyers must be preapproved in writing and must have documented proof of funds

for any cash involved in their offer for distressed property. The old “prequalified”

standard means nothing in this market.

Submitting poorly documented financing or cash and sloppily rendered contract

forms just won’t work. It’s bad practice anytime, but it’s an even worse error in the

unforgiving world of distressed property deals. Everyone is too busy. Listing agents

will turn back paperwork to the buyer agent—lenders have made it clear they won’t

look at it. Buyers and their agents who generate it must do it right the first time—or

they will have no deal.

In short sales particularly, where a lender has not cleared the title, there is a risk of

liens and claims interfering with clear title to a property.

In sales of bank-owned (REO) properties, this issue rarely crops up—the lender as

first lien holder will clear all claims in taking the property back from the defaulting

owner.

But, it’s always good practice to read and understand preliminary title reports in the

distressed property world. The risk of not doing so is way higher than in traditional

sales.

Most agents agree working with buyers is the easiest way to get involved in the

market of the moment. You can learn and earn more quickly than on the listing side—

and the commissions tend to be higher for the buyer side, in both REO and short

sales.

In interviews for this guide, it was said many times by top agents—in slightly

different ways: “If you think this (distressed property) is going to be like traditional

real estate, think again.” This is wisdom hard-won by top agents working this tough

market.

You’ve already seen this is not traditional real estate as you probably learned it. Be

prepared to learn new things—standards, rules, and transaction methods. Distressed

property markets are governed by some unique rules of the road. They’re definitely

different—and you need to learn them as quickly and thoroughly as possible.

Markets of the moment get their name because they come and go. They can return

again—as overall and local conditions change. Many of the agents who are most

successful in these markets get ahead because they recognize “the shift” before

others do; they learn what to change about their practice, and how to make offers

and closings happen.

But even those whose market—or their own awareness of it—develops late can get

in the game and dramatically improve their income. In distressed property, like any

market, opportunity presents itself—to learn and earn.

As taught in SHIFT, one of the strongest cards you can play in building any real

estate practice is to be a committed learner—with a special focus on the history and

current conditions of your local real estate market.

Gary Keller, in SHIFT, calls this commitment “becoming the local economist.”

Being a great buyer agent in a shifted market means being a student of the market as

you would at any time—but with a major in pricing and in distressed properties!

Learn the market—on your own, and from those who are already mastering it. Read

everything you can get your hands on in the news media. They may not have it right,

but they are writing what people are reading, hearing, and watching.

Before you can truly help buyers in these markets, you must know both the truth

about the market and what buyers’ impressions and beliefs about it are.

Becoming a distressed property expert means you must be a committed learner—the

same as you are in your traditional real estate practice. The distressed property

business is filled with specialized processes, programs, and tools you need to know to

be successful.

Opportunities to learn are everywhere. You can get a jump-start with experienced

distressed property listing agents—if you are serious and committed. As you will see,

no one wants distressed property buyer agents to learn better, or faster, than

distressed property listing agents.

Market shifts often mean agents with traditional real estate practices see their income

threatened. When the shift turns downward-moving markets into distressed markets,

there’s a new opportunity to earn—learn the new environment, accept it, and earn

within it.

The table on the following page was assembled with data provided by agent and

owner Debbie Zois of Las Vegas, and by a preferred vendor, First American Title

Insurance Company. Notice the dramatic bottom-line difference! Even if the listing

agent pays no referral, the buyer side is well ahead.

Listing Agent Buyer Agent

Occupancy Check 10 Gas 150

Rekey 100 Time to research properties

Property Setup Visit 15

Lockbox – Combo 15

Water On – Deposit 600

Electric On – Deposit 1000

Monthly Water (x4) 120

Monthly Electric (x4) 400

Trash Out/Clean 500

Biweekly Yard (x4) 240

Biweekly Inspection (x4) 100

Electronic Lockbox 75

Interior BPO 75

Collect/Convey Contractor Estimate 45

Submit Offers 35

Monthly Marketing Update (x4) 60

Interior BPO Update (60 day) 55

Gas On – Deposit 55

Gas Bill 25

REO Trans Fee 125

Reimbursable After 90 Days 3,040

Total Property Cost (550) (150)

Sales Price 200,000 Sales price 200,000

2% Commission 4,000 3% Commission 6,000

Outsourcer’s Referral Fee 1.25% (2,500)

Commission on HUD-1 1,500 6,000

90% Split 1,350 90% Split 5,400

E&O 37 E&O 37

Commission Before Expenses 1,313 Commission Before Expenses 5,363

Property Cost 550 Property Cost 150

NET COMMISSION 763 NET COMMISSION 5,213

REO and short sale listing agent teams are building their buyer agent and listing

agent resources.

Listing agents are consistently frustrated with the mindset and inexperience in

distressed property of agents bringing buyers to their listings. They have learned that

one of the best ways to meet the challenge of poorly educated buyer agents is to

recruit and train their own!

Learn who the bigger players are. Approach them about the skills, experience, and

mindset you offer—your ability to perform now, and your willingness to learn and

do.

Many top REO listing agents have realized the sales and income opportunity that the

buyer side of their business affords. Teams doing more buyer side conversions are

financially ahead of the curve with about the same number of deals. They are using

buyers to accelerate their financial results.

These top agents are looking for smart buyer agents to sell their listings. In many

cases, they may also be looking to hire capable buyer agents to be part of their sales

team.

Top distressed property agents understand that people who have not done this

business have a hard time understanding why listing agents are reluctant to give

relationship referrals, much less active roles in their teams, to more agents.

Agents who focus on distressed properties make a huge investment of time and

money in their relationships. Their customers, most of the time, are big institutions

with large networks. If one agent does something damaging that reflects on them,

they can lose more than a deal—they can lose scores or even hundreds of potential

listings.

A top agent shared the model below for mentoring an interested agent (with general

real estate experience) during a sort of probationary period. Here are the steps:

Shadowing – Shadow one of the experienced listing or buyer agents for thirty

days—watching offers handled, addenda completed, and sitting in on

negotiation conversations.

Co-listing – Assigning the person as co-listing agent on 3–5 listings—

handling everything to do with that listing—cleanouts, cash for keys,

maintenance and repair, security, showings, and more.

Recommending – Recommend that person to a lender or asset manager (one

you already have a relationship with) to get listings.

While the focusing on the buyer side of distressed property can be a lucrative way to

get into distressed property—without the upfront cost of maintaining REO listings,

and without some of the negotiation challenges of listing shorts sales—the buyer side

can lead to a listing business too.

Markets of the moment aren’t well understood by people who haven’t been in them.

Those who haven’t experienced them need to get up to speed to be successful.

For every agent who was in the business in the late 1980’s or early 1990s, depending

on location, and recognized the current opportunity early, there are many more for

whom distressed property is a new reality.

Change creates choices. It’s worth repeating that you have the following three

choices to make about how you will excel in this distressed property market. Now is

the time to decide and take advantage of this opportunity that may or may not be

around for a while. It’s your choice; are you ready to choose?

Listing Side: Focus on listing short sales or REOs—top listing agents tend to

specialize in one or the other.

Buyer Side: Focus on the buyer side—learn about the opportunities and

needs of buyers in this market, learn about short sales, REOs, and auctions—

and be able to sell all types of distressed properties.

Both Sides: Build a team that works both sides—by listing distressed

properties and working the buyer side with a focused buyer agent or agents.

Whichever way you choose to go, it’s imperative to understand the landscape of

distressed properties.

So how did we get in this market situation? And what are people’s perceptions of this

market? To be successful with your buyers, you must demonstrate your knowledge

and expertise in these two areas; the mindset and the market.

The mindsets of the players in these markets – Sellers, banks, asset

managers, buyers, and agents all have their own motivations and

viewpoints—and they really impact how the business is done.

The distressed market phenomenon – It was created by a “perfect storm”

of economic and other factors that came together early in the 2000s. You

need to know that story and how to relate it to your local market when

consulting with buyers.

One of the first things distressed property expert agents discover is the special

mindsets of all parties involved. They are different from traditional market

viewpoints. The following table shows a summary of some of the top points of

difference from a mindset perspective.

The right hand column of the table emphasizes the importance of studying the

distressed market to become the best advocate for your buyers, to bring sales to

closing, and to work cohesively with listing agents and lenders.

Things are different in ways that impact all the parties involved in a transaction—and

the transaction process itself.

Consumers in

General

Eager and positive about buying

or selling.

Stressed about whether to and how to

take action given the market on the

sale side—and feeling urgency to buy

at great prices on the buyer side.

Sellers

Seeking return on investment and

equity to power their next home

purchase.

Institutions and consumers seeking

either whatever they can get, or an

escape from crisis.

Buyers Seeking the right home at a

reasonable price.

Seeking the very best possible deal,

or a steal.

Lenders

Generally open to making loans and

into creating products and policies

to encourage borrowing.

Lending criteria is dramatically

tightened; loans hard to get. They

have also taken on role of sellers of

distressed property—either before

foreclosure (short sale) or after

(REO.).

Agents Eager to jump in; generally able to

master transaction basics.

Often poorly informed about

transaction basics; often not well

qualified to coach their clients—or

unaware of the need to.

Transaction

Processes

Taught widely, in real estate

schools and by brokers. Generally

consistent and use standard

board or MLS documents.

Timelines generally consistent.

Only recently being taught. More

complex, with varying timelines

and requirements. Lenders in

charge of transaction process.

Special documents required by lenders

and agents to protect themselves and

clients.

Distressed property business is different—mindsets of all the players have shifted

from traditional market views. Making the shift yourself requires some breakthrough

thinking.

One picture of personal transformation was first introduced by Gary Keller in his

“Six Personal Perspectives” It appears in a range of Keller Williams University

courses for both leadership and agents, including the course Quantum Leap.

Moving from “E” to “P” is shorthand for deliberately shifting from a business style

based on entrepreneurial mindset to a style based on a purposeful, or by design,

mindset. It applies very well to the transformation agents need to make to become

successful in the distressed property business.

Think of the “E” world as the world of traditional real estate transactions you

probably learned in licensing and broker classes—the world that is the comfort zone

of most agents. Think of “P” as the world of distressed property listings and sales,

where many things are new—markets, mindsets, and transaction processes.

The E to P model says there are five breakthrough ingredients that move you above

the ceiling. These ingredients define the “purposeful style” you will need to succeed:

Clarity of purpose

Knowing your options

Choosing your model to proceed

Putting systems in place

Creating accountability for your performance (with an accountability partner)

Think about activities in traditional markets that

represent the way things are normally done—

methods that might come “naturally” to people

wanting to sell real estate.

Write down what it is specifically about the shift

into distressed property sales that requires these

things:

Clarity of purpose

__________________________________________________________

__________________________________________________________

Knowing your options

__________________________________________________________

__________________________________________________________

Choosing your model to proceed

__________________________________________________________

__________________________________________________________

Putting systems in place

__________________________________________________________

_________________________________________________________

Creating accountability for your performance

__________________________________________________________

__________________________________________________________

Experts say the last distressed property wave that affected the United States was

driven by factors more complicated than supply and demand alone.

Gary Keller has been a teacher throughout his real estate career. In speeches and

interviews, he referred to America’s distressed property markets as driven by a

“perfect storm.” The elements include economics, government policies, consumer

choices, and financial engineering by investment companies and lenders.

U.S. government pushes for increased home ownership – 1990s U.S.

government policies pushed expanded home ownership dramatically.

Lender aggressiveness – Lenders chose to make more loans, encouraged by

that policy shift. The boom in lending, new home building, and home reselling

from about 2000 to 2007 included softened lending standards and a host of

new mortgage lending products never seen before. Variable rates, nothing

down, and little or no borrower documentation programs brought people to

home ownership under terms they either did not think through or did not fully

understand.

Securitizing mortgage loans for giant investors – As lending expanded,

financial institutions turned resold home loans into elaborate investment

products—sold to institutions worldwide to generate income for them and

make more money available for lending. Critics say the process included

strategies to hide the risk to investors that was inherent in the types of loans

being made to home buyers.

Low interest rates – Historically low interest rates throughout the late 1990s

and early 2000s generally spurred lending and borrowing.

Building boom – Lending policies and the low cost of money also triggered a

boom in residential construction led by national home building companies.

Lots of new inventory attracted as many investors as homeowners. Not all the

inventory sold.

Decreasing equity – To compound these problems, through a wave of

refinancing, many consumers reduced their equity in their home—at a time

when the inevitable market decline was about to reduce their home’s value.

When the resulting lower equity meets declining market values, homeowners’

equity shrinks fast—and then disappears.

Being a top-flight agent for buyers of distressed property starts with understanding

what is going on in foreclosure—what precedes it, and what follows it.

Distressed property markets fit in the context of normal market movement over

time. They are a phenomenon of a buyer’s market, and the special circumstances that

come into play when property values experience a sustained decline.

Generally, one of the underlying fundamentals of real estate and investment markets

is that things go up and things go down. Then they go up again.

Balanced markets—when supply and demand are well-matched—become sellers’

markets when too much demand for inventory available, and then often revert to

buyers’ markets when demand eases and supply exceeds the number of buyers

available.

Note: The end point data for 2009 in the chart is based on NAR’s projections for year- end 2009

inventory and units sold.

Nationally the rapid transition from a sellers’ to a buyers’ market began in early 2006.

The supply (inventory) and demand (sales) lines crossed somewhere in 2007 and we

entered the strongest buyers’ market since the late 1980s and early 1990s. In some

places, the shift happened sooner; in others, it happened later—this is always the case.

The buyers’ market began at different points in time depending on where you were.

Because all real estate is local, the answer to the question “how long will the buyer’s

market last” will vary.

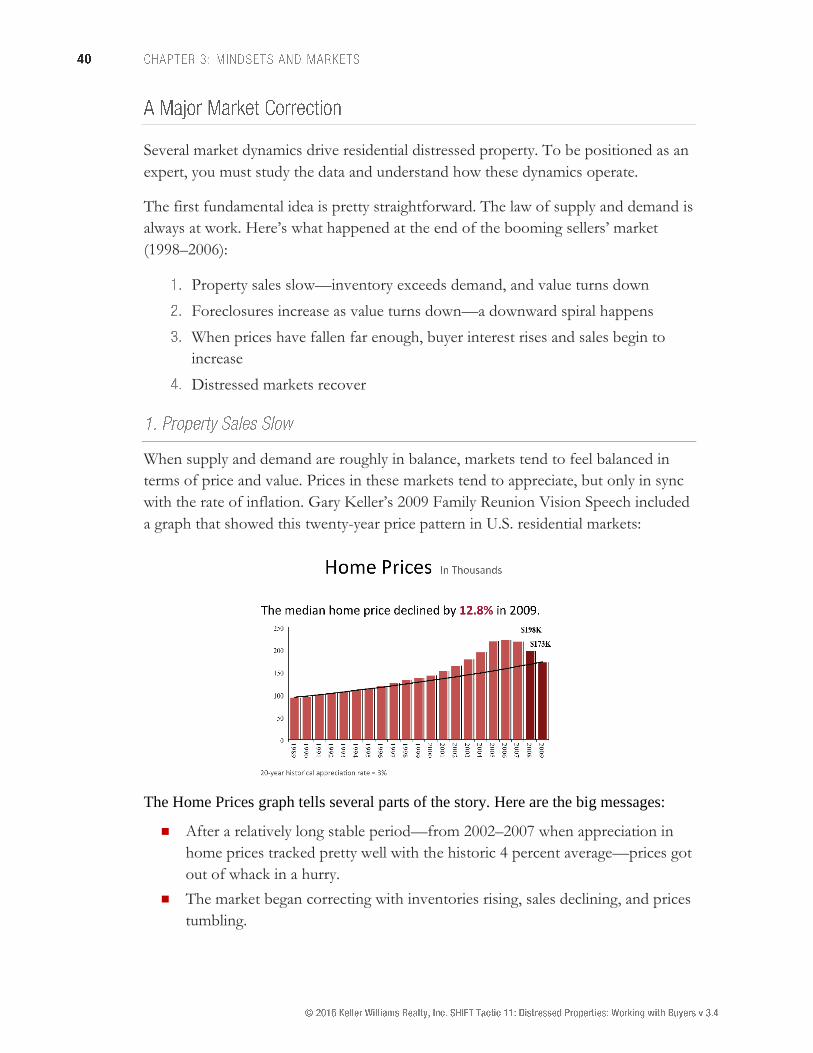

Several market dynamics drive residential distressed property. To be positioned as an

expert, you must study the data and understand how these dynamics operate.

The first fundamental idea is pretty straightforward. The law of supply and demand is

always at work. Here’s what happened at the end of the booming sellers’ market

(1998–2006):

Property sales slow—inventory exceeds demand, and value turns down

Foreclosures increase as value turns down—a downward spiral happens

When prices have fallen far enough, buyer interest rises and sales begin to

increase

Distressed markets recover

When supply and demand are roughly in balance, markets tend to feel balanced in

terms of price and value. Prices in these markets tend to appreciate, but only in sync

with the rate of inflation. Gary Keller’s 2009 Family Reunion Vision Speech included

a graph that showed this twenty-year price pattern in U.S. residential markets:

The Home Prices graph tells several parts of the story. Here are the big messages:

After a relatively long stable period—from 2002–2007 when appreciation in

home prices tracked pretty well with the historic 4 percent average—prices got

out of whack in a hurry.

The market began correcting with inventories rising, sales declining, and prices

tumbling.

The perfect storm of market conditions, described in the opening of this course,

contributed to intensify the buyers’ market.

The big price correction markets have been experiencing is impacted by the volume

of foreclosed properties hitting the market. The chart below shows what happens

when foreclosure rates accelerate.

Decreasing prices eventually draw increased buyer interest. When prices have

decreased sufficiently, things begin to shift again.

There is a certain tipping point when sales increase, and it’s centered on affordability.

That is, when consumers can afford to buy a home, they will.

Top agent and owner Gene Rivers, Tallahassee, Florida, compiled data from top

metropolitan markets across his home state, and his analysis revealed a very

important trend in his market. He noticed that where prices had decreased by, in this

case, about 20 percent or more during the past year, sales were increasing again at

that point in time. Conversely, in markets where price declines had been small (not

shown), sales were continuing to go down at that time.

The study is a clue to how recovery happens.

Median Sales Price Real Estate Sales

Statewide &

Metropolitan Statistical

Areas (MSAs)

Year

End

2008

Year

End

2007

%

Chg

Year

End

2008

Year

End

2007

%

Chg

Statewide $187,800 $234,300 -20 124,215 129,855 -4

Fort Lauderdale $278,000 $363,100 -23 6,377 6,127 4

Fort Myers-Cape Coral $158,200 $254,700 -38 8,217 5,723 43

Fort Pierce-Port St.

Lucie $153,600 $226,100 -32 4,332 3,376 28

Orlando $201,500 $248,900 -19 16,659 17,143 -3

Punta Gorda $139,100 $186,900 -26 2,530 2,436 4

Sarasota-Bradenton $225,900 $286,300 -21 7,661 8,013 -4

Tampa-St. Petersburg-

Clearwater $169,500 $208,900 -19 23,615 24,310 -3

West Palm Beach-

Boca Raton $302,800 $369,400 -18 6,953 6,971 -

To round out this section on perspective, it’s important to note that because all real

estate is local, there may be areas in where a combination of factors is driving buyer

demand for traditional resales.

These may be areas where good paying jobs are plentiful and where younger

professionals who are first-time buyers are flooding the market looking for deals.

Sooner or later, property values decline in any market to the point where they

become attractive again to investors and resident buyers. The challenge is to know

when it will happen. It’s up to buyers to turn the market, and it’s up to you to help

them be confident and motivated to purchase in this market.

Historically low mortgage interest rates

Growing home affordability for buyers

Knowing the national trends sets the stage for the real payoff—The ability to

describe the local market picture to buyers.

1. State what’s going on in your local market today.

Take a moment to critically analyze what’s going on in

your local market today. Write down your thoughts on the

following questions, then discuss them with a partner and

then again as a class.

Affordability is based on sales price, interest rate,

and income, What is your median sales price? How has

it changed?

_________________________________________

_________________________________________

What is the current interest rate?

_________________________________________

_________________________________________

What is the state of your local economy? Median

income? Employment? Growth?

_________________________________________

_________________________________________

What is the current inventory of distressed property? Is

it increasing or decreasing?

_________________________________________

_________________________________________

Are both sellers and buyers motivated at this time?

Explain.

_________________________________________

_________________________________________

Are first-time home buyers taking advantage of the

incentive? Explain.

_________________________________________

_________________________________________

2. Rate your local economist skills.

What basic elements of the distressed market story

can you tell?

Do you know relevant national historic statistics

that describe how markets became distressed?

Do you know where your local market stands

today? What percentage of sales is distressed? Of

those, what percentage are REOs and what

percentage are short sales?

What component is traditional resale? Are there any

special local stats you can cite—like the Florida

example in the course—that show the relationship

between prices and sales volume?

Topic Talking Point

Important to:

Perspective?

Pricing?

Urgency?

Sources

Rate Your

Communication

Skill

Low 15 High

U.S. Market

Trends

Markets always shift

over time

Perspective SHIFT chart

Percent of Sales

Distressed and

Trend (State or

Local)

How dominant are

distressed sales

Pricing RealtyTrac;

Mortgage

Bankers Assn

Historic Average

Sales Price Trend

How markets have

been correcting

Pricing Gary Keller

Vision Speech

Local Area

Absorption Rate

Your chances of

selling

Urgency Your MLS

Exceptions:

“Thriving Pocket

Markets”

Some sellers may

have above average

opportunities in

otherwise down

times

Pricing Your own

homework;

input from

mentors

What steps do you take now to improve your skill in knowing and communicating

this vital information to your clients?

________________________________________________________________

________________________________________________________________

This chapter is included in all three guides in the SHIFT Tactic 11: Distressed

Properties series. Why? Because these guides are stand-alone, and whichever course

you pick up first, a good basic understanding of what happens to distressed

properties is essential—from the time a homeowner faces a missed payment until the

property is foreclosed and moved to a new owner in some way.

The fundamental process at work that creates distressed inventory is foreclosure.

Foreclosure is a legal process that happens on a timeline. Some things happen before

it begins; some happen after it ends. Foreclosure happens because homeowners—for

a wide variety of reasons—stop paying back their loans, and their lender declares

them in default. If they do not find another option, they lose their home.

Let’s examine all parties and all steps involved in the process, from beginning to end.

You’ll get an appreciation for how distressed properties come to exist—both the

legal side and the personal and emotional side of it. You’ll also see where buyer

interest arises.

What’s happening in distressed property markets today is, more than anything, about

circumstances and recent history—markets always are. Knowing this world from the

consumer’s perspective is a key ingredient in becoming an expert. Understanding the

human and economic root causes behind distressed property markets goes a long

way toward building your credibility.

As has become common in this market, a homeowner has an event in their lives that

causes a “personal shift.” In any of these events or situations, foreclosure is a deeply

personal experience. The primary causes of this personal shift, which lead to

distressed situations, are:

Negative Equity from Market Shifts

Unemployment

Personal Crisis

Consumer Overconfidence

Let’s explore the primary causes of personal shift one at a time.

A negative equity situation arises when a homeowner finds the market value of their

property is less than the amount they owe on their mortgage. When a homeowner

purchases with a very high percentage of debt, a relatively small downward shift in

market value can wipe out their equity.

A homeowner with significant equity can borrow against that equity. When

appreciating markets are increasing overall value (and equity), this seems to make

sense. But declining markets reverse the process. Unlike refinancing—a personal

financial decision—downward market movement leaves the homeowner with a sense

of helplessness. Eventually, this feeling can turn to fear if the declining value

situation becomes acute.

This bar chart illustrates how owner equity can disappear. In this illustration, the

down payment was 10 percent and the market shifted down 20 percent. In the

shifted market, the difference between value and debt has become negative equity.

Here’s what changed in the chart example:

Value Arbitrarily set at 100 Market declined 20%; value now 80

Debt

Set at 90—property was

purchased with 10%

cash down

Most mortgages pay interest first and

principal later; debt is virtually the same

in early years

Equity

Value was 100 minus 90

owed leaving 10 in

equity

Turned from positive 10 to negative 10

Clearly, significant value declines can create negative equity and negative equity

severely limits whether and how homeowners can sell. But why are borrowers

defaulting in record numbers? The Wall Street Journal (May 29, 2009) offered this

perspective:

Why do borrowers default? Many have assumed it’s because mortgage payments are

too high. But a new paper from the Federal Reserve Bank of Atlanta argues that

unaffordable loans—with high mortgage payments relative to income from the time

they’re originated—are “unlikely to be the main reason that borrowers decide to

default.” Instead, unemployment and future home price declines are likely to play a

bigger role. The paper looks at loans that are unaffordable from the time they’re

originated, and not at loans that may start with low “teaser” rates before jumping

higher. Here’s a summary of their findings.

By the way, the U.S. Department of Labor reports the length of people’s unemployed

stretches (measured in weeks) is getting longer. Here’s the picture from 1940 to 2010.

Unemployment 1 point increase

(i.e., 8% to 9%)

10%–20% more

delinquencies

Debt-to-

Income Ratio 10% increase

7%–11% more

delinquencies

Home Prices 10% decline in home prices 50% greater probability

of default

On top of all this financial and economic shifting, personal crises happen, as always.

Some are about health and family; some are triggered by the slowing economy.

Common homeowner crises include:

Unforeseen large medical expenses

Unplanned job transfers

Death in the family

Divorce

Job loss

All these events bring financial challenges that may force homeowners to become

potential foreclosures in a shifted market.

Much is being written and broadcast these days about what role confidence, or lack

of it, plays in distressed markets and foreclosures. Here are two views you may hear

in the marketplace.

Naive Confidence Can Help

Much is being written in these times about the role of consumer confidence in

down and distressed markets—and in market recovery. Experts seem to agree

that there is some level of consumer confidence, or exuberance, which is the

hallmark of recovering and rising markets. Writers in major news organizations

have taken to calling this mindset “naive confidence”—the willingness to

overlook risks in favor of rewards in markets.

Overconfidence Can Hurt

In a shifted market that has become distressed property-focused, opinions

abound about why any or all of the players made the choices they made that

contributed to the result.

One example of this opinion appeared in The San Diego Union-Tribune and has

been reprinted in other major daily newspapers. It appeared in the Austin American-

Statesman on May 4, 2009. The commentary is based on a 2006 book by a San Diego

State University professor, Jean Twenge, titled Generation Me. Quoting the book,

“People were very overconfident about what size mortgage they could afford and the

same thing affected the bankers who were giving the loans. Everybody was

overconfident and didn’t anticipate the downside, so when the downside came it was

worse than anyone imagined.”

Now that you have a better understanding from the homeowners’ viewpoint, let’s look at

the complete timeline of events.

Foreclosure is a process that happens over varying timelines, depending on local

laws. Local timeline differences can have a big impact on important distressed sale

details, so you must know your local foreclosure timeline and what governs it.

The process begins with the point where a homeowner first misses a payment—or

knows they are about to do so—and ends after foreclosure, with the sale of bank-

owned properties and the possible transfer of properties to the Federal Deposit

Insurance Corporation (FDIC) when banks fail.

This process is described on a timeline and with definitions that appear on the

following pages. It includes both pre-foreclosure and post-foreclosure events.

The timeline of the process can be different in some

states, so be sure to know your own state laws and

regulations, and seek answers if you need them.

The foreclosure legal process can be completed in as little

as 90–120 days. In others, it may extend to as long as

twelve months or more.

The foreclosure process and state and local laws governing

how it happens are a full-day class in their own right.

Check around. Chances are local title companies, your

local board, or real estate schools are offering a

foreclosure course.

If you decide to take a foreclosure course from a national

vendor, be alert to whether they have modified it to

include steps that are the right ones for your local market.

If they have not, you’ll need to get that information from a

highly reliable local source—your Team Leader, an expert

agent in your Market Center, or a title company are your

best bet.

The timeline chart summarizes the critical details you must learn to be a distressed

property expert. Though this course focuses on REOs, this chapter addresses all

steps in the timeline. Make note of how many steps’ terminology or internal timelines

vary, according to local law or regulation of some kind.

The description of the timeline establishes three categories for the items that appear:

Personal Shift (PS) – Things that involve or impact the homeowner directly.

For example, the homeowner or individual seller faces a challenge such as a job

loss, excessive medical bills, etc., that causes them to be unable to make their

loan payment.

Market Shift (MS) – Things relating to the status of the property itself of the

institution that holds the loan. For example, the market changes, home values

decline, lending regulations change, inventory increases, etc.

Buyer Interest (BI) – Points of time when buyers become interested in

making a purchase of distressed property. Arises at a number of different

points along the way, indicated by the groups of buyers. When a property first

shows up as a potential distressed property, you alert your buyers about its

availability and then buyer interest occurs.

The items in each category are numbered PS, MS, BI, so you can refer back and forth

to the diagram and the descriptions.

These are things that involve or impact the homeowner personally.

The diagram assumes the homeowner occupies the home as their primary residence.

The first sign of trouble comes when the homeowner misses a mortgage payment.

Homeowners miss payments for any number of reasons. Typically, it happens

because of:

Personal Crisis – job loss, unwanted and expensive job relocation, divorce,

death in the family, or illness resulting in high medical bills

Market Shift – market value declines to the point where the home is worth less

than the owner’s loan balance

Depending on the lender, and local foreclosure laws, the homeowner will receive a

Notice of Default within 60–90 days after one or more payments are missed. The

notice is a formal letter from the lender advising the homeowner that their loan and

ownership are in jeopardy. Default is what causes lenders to trigger the foreclosure

process—in order to recover their losses, or get the homeowner quickly back on track.

Deed in Lieu – This is very legal, but may also be very risky for the owner in

default. Why? A deed in lieu of foreclosure does not necessarily clear away all

other judgments against a property owner. The former owner may think they

have escaped further demands only to find other parties (not part of the deed

in lieu deal) coming after them for other money they owe.

Deed in lieu of foreclosure agreements usually only happen if the parties can

agree the property being signed over has value equal to the amount of the debt!

Loan Modification – In 2009, the U.S. government introduced the Home

Affordable Refinance Program (HARP). The program is designed to help

homeowners with little equity, who are current on their mortgage payments to

restructure their home loads. HARP works to keep more homeowners out of

foreclosure and in their homes.

The lender follows up with a written notice that they will foreclose by a certain date.

A representative of the lender posts a foreclosure notice on the outside of the

property, which states that the lender has taken possession and all inquiries until

further notice must be directed to them.

If no sale has been arranged, and if the homeowner has not walked away from the

property before foreclosure, they will be forcibly evicted on order of the lender. A

local sheriff or constable typically enforces the eviction.

In some states there are provisions for homeowners to escape foreclosure by making

repayment arrangements with the lender to “catch up” on the amount in arrears.

That’s redemption. In some states, there is also a reinstatement period that can

actually extend beyond the foreclosure date and even beyond a trustee or sheriff’s

sale, or auction, of the property. In these rare situations, if the homeowner completes

catch-up arrangements, a person who bought the home at auction may even have to

give it back to the owner. The auction winner gets their money back.

These are things relating to the status of the property itself or of the institution that

holds the loan.

A mortgage deed is a contract that states the amount due on a loan to buy the

property, the term of the loan, rate of interest charged, and how payments on the

balance are to be made. It usually also says what will happen if the payments are not

made! Conventional loans come in many different types and sizes—though not as

many as before the current distressed property crisis.

Homeowners can also get mortgage loans from the U.S. government’s Federal

Housing Administration (FHA) or Veterans Administration (VA). The loans often

have different (frequently tighter) requirements about down payments and property

condition than conventional loans.

Another difference: FHA and VA will not approve a short sale unless the

homeowner has actually defaulted. Some conventional lenders will approve a short

sale without a default.

A short sale is basically a negotiated settlement between the lender and homeowner

in which the lender agrees to accept a buyer’s offer for less than the homeowner’s

total loan balance.

The trustee sale, or sheriff’s sale, is a common vehicle for getting foreclosed

properties sold to buyers—frequently to investors who are regulars at these auctions.

The buyers typically must pay cash for their winning bid, either on the spot or very

shortly afterward. The sales are often referred to as “courthouse steps” sales.

This is another auction format—usually arranged by a lender that holds foreclosed

property. A professional auctioneer is hired and property to be auctioned is listed for

preview on the Internet. Sometimes the preview properties are held open briefly so

interested parties can go inside.

If there’s no short sale or auction sale of any kind, the property will remain bank

owned. The bank will typically turn the property over to either its own asset

management arm or a third-party asset manager. Their job is to manage and market

the property—you will sometimes hear the term “M and M Firm” used to describe

them. They may list property directly for sale, yet they typically turn to specialized

REO listing agents to list and sell lender-owned homes.

Listing bank-owned real estate (REO) can be a big business for distressed property

specialist agents, albeit with low profit margins. It is, along with auctions and short

sales, one of the three main ways distressed properties are marketed and sold.

This is where you come in as an agent for the buyer. REO properties are listed on

MLS and are sold, usually, with the same standard contract approved by your local

real estate board or MLS—with some very important exceptions and additions.

On relatively rare occasions, banks fail. If they are federally chartered, they are taken

over by the chartering authority, under the direction of the FDIC. The FDIC then

seeks real estate brokers to help sell the properties, or it may return to the prelist

auction step and try to sell properties before seeking the help of brokers and agents.

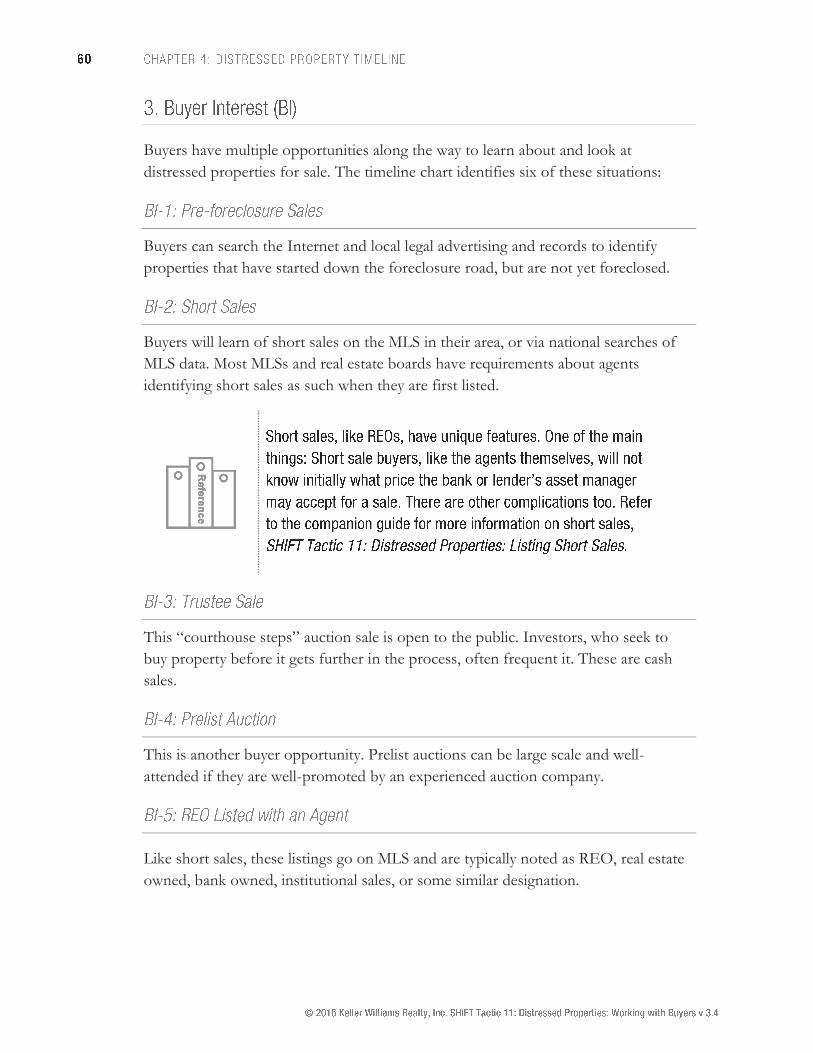

Buyers have multiple opportunities along the way to learn about and look at

distressed properties for sale. The timeline chart identifies six of these situations:

Buyers can search the Internet and local legal advertising and records to identify

properties that have started down the foreclosure road, but are not yet foreclosed.

Buyers will learn of short sales on the MLS in their area, or via national searches of

MLS data. Most MLSs and real estate boards have requirements about agents

identifying short sales as such when they are first listed.

This “courthouse steps” auction sale is open to the public. Investors, who seek to

buy property before it gets further in the process, often frequent it. These are cash

sales.

This is another buyer opportunity. Prelist auctions can be large scale and well-

attended if they are well-promoted by an experienced auction company.

Like short sales, these listings go on MLS and are typically noted as REO, real estate

owned, bank owned, institutional sales, or some similar designation.

Under its federal charter, the FDIC will assume control if a bank that owns real

estate fails. The FDIC will then either hire a real estate broker and other firms to

market or manage these properties, or it will go back to the prelist step first and try

to sell it that way before going the listing route.

Using the timeline chart as a tool, get with a partner, and

you as the agent explain the timeline clearly to your

partner (who is the buyer). Switch roles and repeat.

The chart is detailed. How would you simplify or

streamline it for a client? Which points would you

emphasize for an REO client and why?

Buyers are buyers, but distressed markets put the spotlight on some special buyer

traits and requirements. You must know who the buyers are and what’s motivating them—

specifically. Buyers in these markets fall into three main categories.

Move-up buyers

First-time buyers

Investors with different levels of experience

Once you know the type of buyer you’re working with, you must find the right property for

them. This chapter addresses both finding buyers and finding property for them and

concludes with a real-play of live lead calling and appointment setting—including some

recommended scripts to use with distressed property buyers in different categories.

Most people buy a home to be their primary residence—in most cases, it’s their only

residence.

Every day, more and more people of all means are waking up to the huge buyer

opportunity in today’s market—particularly in distressed property. This category

covers people looking to buy a home they’ll live in.

Many of today’s buyers see the market as a chance to move up—and you should be

running your marketing to speak to that desire. Any seller today has ample

opportunity to more than make up any loss they may have in selling by taking

advantage of a great buy!

A $8,000 tax credit for first-time home buyers helped in distressed markets. First-

time buyers became more active—to the point where they have become more than

50 percent of all U.S. home buyers!

First-time buyers are also attracted to the outstanding deals that can be had in

distressed property. The smartest buyer agents market aggressively for first-time

buyers. Top agents in just about every market acknowledge that first-time buyers are

an important part of their audience.

Keller Williams agents have some important advantages and tools to use in attracting

all-important first-time buyers.

While buyers who want a primary residence still dominate, there are plenty of other

buyers who seek residential investment property. They see this market as a chance to

try owning rental property for cash flow and possible long-term appreciation.

Their range of experience in investing is wide—from property owners looking to get into

their first rental property for cash flow and long-term return, to more experienced

investors looking to add to their existing stable of income producing properties. In

some situations, these experienced investors may be looking to fix and flip

properties.

You’ll want to make yourself stand out to buyers of all types. Model what other top agents do. Use specific techniques (below) to lead generate for buyers of distressed properties.

Use Best Buy Marketing

In a buyers’ market, people want deals. No one is in a better position to

point the great deals out than you. Follow this SHIFT teaching point.

Create and distribute continuously updated “best buy lists”—on your

website(s) and in print. Let buyers know you know the market—and

where the best opportunities are to buy now.

Be the Local Economist

Market history—Charts and graphs.

Law of supply and demand—Demonstrate the transition from seller

to buyer markets visually.

Absorption rates—Chart them; show where sellers stand with their

chances of selling. This is very important information for buyers.

In and out of the market charts and the chasing the market chart—

Be sure buyers understand that you know what sellers and their agents

are thinking!

Market timing illustrations—Like the “where is the bottom?” exercise,

or “the pendulum” from SHIFT.

Buying in the safe zone—This is another SHIFT concept. It illustrates

how smart investors buy on the trend—without waiting for the turn they

can never hope to hit, except with dumb luck.

Sharing your

agent-branded

KW App?

1. Get the Keller

Williams Real

Estate app

from Apple

App Store or

Google Play

Store.

2. In the app, use

“Agent

Search” to find

and select your

name.

3. Toggle “Make

this my agent”

button to

“Yes”

4. Use “Share

App” to share

with your

contacts!

Find More on

KWConnect.com

Offer Classes with Distressed Property Emphasis

Linda McKissack of Denton, Texas, is a 7th Level Keller Williams agent and

owner of Market Centers in the Southwest and Midwest United States. She is

also a residential property investor. Linda never misses a chance to encourage

agents to put their real estate knowledge to use by hosting local seminar

sessions for buyers.

Topics Linda suggests you learn to teach include:

The Millionaire Real Estate Investor—Hold an investment talk based on

Gary Keller’s The Millionaire Real Estate Investor (a great resource). Know its

message and encourage small investors to get into buying real estate for cash

flow and long-term or short-term profit.

SHIFT—Use the excellent teaching outline of SHIFT to educate consumers

on what’s happening to their market, and their home’s value—and how they

can best benefit financially.

Your First Home—Help first-time home buyers get closer to their dream of

home ownership.

Start an Investment Book Club—Use other great real estate investment

books including Building Wealth One House at a Time, by John Schaub, to teach

investor principles.

And, Linda always urges her audience to be aggressive and confident. Even with

years of experience, she still says she crams at the last minute to make every

presentation as strong as it can be, and to bolster her confidence.

Get in the Path of Buyers—Open House Opportunities

Top listing agents, especially on the REO side, can’t believe how many agents

are passing up the chance to use distressed properties to market themselves to

buyers who want REO and short sale values.

Study the market, know the story nationally and how it applies locally, and get

out there in front of buyers. If you don’t, it’s a major missed opportunity.

Get into relationships with your local top REO listing agents and offer to

hold their listings open. Consider offering a buyer tour of distressed listings.

And here’s another open house idea from 7th Level agent Bruce Hardie: set

up your office temporarily in an open house in a distressed area. Post a sign

“Distressed Property Information Center,” or “Get Foreclosure Sale

Information Here.”

Use Custom Email Campaigns from the MyKW.com Intranet

The Keller Williams Intranet site MyKW.Com, under the Marketing tab,

provides prewritten email campaigns for both first-time and move-up buyers.

Shifted markets can be challenging times for lenders. Buyers want to buy, but loans

are may not be as easy to find as they used to be. You’ll need to roll up your sleeves

and work for your buyer to find loans.

While lenders have been watching their balance sheets much more carefully—and

tightening lending standards in the process—more and more buyers are turning to

government-backed FHA and VA loans for mortgage money.

According to the Mortgage Bankers Association, “a primary reason government-

insured loans have retained a high share of the purchase market is that these loans

typically require lower down payments than conventional loans. In addition, lending

standards tend to be tighter for conventional loans, especially for loans that require

private mortgage insurance.”

Major lenders with a lot of REO inventory have realized selling this property is a

huge opportunity to make loans, and they are pushing this with listing agents. Many

top REO listing agents shared stories of how lenders are getting aggressive and