Embed Size (px)

Citation preview

First Quarter of 2011

Institutional Presentation

2

Agenda

1. Investment Highlights2. Strategic Positioning3. GRV acquisition4. Financial Highlights5. Appendix

Index

Agenda

1. Investment Highlights

3

Agenda

Business Model: Main Characteristics

CETIP and GRV Highlights

4

Provide critical market infrastructure

Credit

Strong barriers to entry

Same client base

Core mission

Strong diversification

Less diversified

Growth driver

Client

AssetClasses

Strong operating leverage and cash flow generation

High growth and high margin profile

Relatively high integrated model

Resilient and predictable cash generative business with low execution risk

Business Model

Competition

AgendaCompetition: Barriers to entry

5

Ne

w P

layers

/ com

pe

titors

Network effect (>10,000 clients) &

System integration with customers

Reputation

(“Ativo Cetipado”)

Strong relations with banks and assets managers

Broad portfolio of services and asset classes served

Scale and Regulatory framework

Low prices compared to different alternatives

Network effect (> 5,000 clients) &

System integration with customers

Nationwide integration of DMV’s

Database

Current system works well for all participants

Nationwide system with zero fraud

+ = Dominant

position

Stable Prices

Agenda

6

Registration - Fixed income instruments

Financial Institutions- CDs, IDs, others- Loans participants (CCBs)- Real estate financing (CCI, LCI, others)- Agribusiness financing (LCA, CCA, others)- Export financing- Others

Corporations- Corporate Bonds, Debentures, Commercial

Papers- OTC Derivatives

Custody- Debentures- Quota of Funds- Other assets held in custody

Transactions (custody services)- Management of Corporate

Events

Monthly Utilization- Connectivity Fee

12%*

14%* 9%*

15%*

(*) % of revenue (1Q11)

Business Model

Others- CIP services

8%*

GRV

- GRV Contracts

- SNG Vehicle (Liens)

- Selling Information

14%*

23%*

5%*

Agenda

7

Revenue Drivers (Gross Revenues)

Depository & Repository Services

• Bps (usual); R$/unit (exception)

• Structured and non-structured

• 1Q11 average margin on volume ($) – 0.06 bps

• R$ / unit

• 1Q11 average margin – R$ 0.86 / transaction

Registrar Services

• Bps (usual); R$/unit (exception)

• Intra vs. extra group; tenors

• 1Q11 average margin on volume ($) – 0.09 bps

• R$/contract (usual); bps (exception)

• Structured and non-structured

• 1Q11 average margin – R$ 44.68 / contract

Clearing & Settlement

• Bps (cap & floor)

Processing

• R$/transfer (decreasing fees schedule)

Connectivity

• Increasing fees schedule / customer

• Number of customers and level of activity

• 1Q11 average margin – R$ 1,019 / customer/month

Liens

• R$/lien

• 1Q11 average margin – R$ 25.00 / lien

Auto Loans Contracts

• R$/contract

• 1Q11 average margin – R$ 22.30 / contract

Fixe

d

Inco

me

OTC

D

eriv

ativ

esD

epo

sito

rySe

curi

ties

A

ctio

ns

7

AgendaMultiple Growth Drivers

(Source: Brazilian Central Bank)

Credit Growth in Brazil

326.8 336.4 384.4 418.3 498.7607.0

732.6936.0

1277.31414.3

1705.2

26%25%

22%24% 25%

28%31%

33%

40%

44%47%

0

200

400

600

800

1000

1200

1400

1600

1800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Volume (R$ billion) % GDP

8

Agenda

9¹ Volumes for other countries in 2007Source: BIS, Global Insight, Oliver Wyman analysis

18,3

13,6 13,2

7,0

4,1

0,4

2,8

Annual Volume of OTC Derivatives Trading per Country1 Growth Drivers

UnitedStates

Japan Germany Italy Mexico Brazil’07

Brazil‘12

• Increase in usage of fixed rate debt

• Lengthening of tenors

• Progressive regulatory environment

• Increase in variety of underlying assets and sophistication of managers and investors

• Development of collaterization and tools for fair value calculation

CAGR 63%

Multiple of GDP

Underdeveloped capital markets – OTC Derivatives

Agenda

10

Underdeveloped capital markets – Fixed Income

0,11,6

5,17,2

9,0

14,116,0

29,6

44,3

Corporate Bonds¹

Debt outstanding as % of GDP (Sep/2010)

Turk

ey

¹ Exclude bonds issued by financial institutionsSource:Oliver Wyman, McKinsey, Brazilian Central Bank, International Monetary Fund , Bank for International Settlement

Mortgage Loans

Debt outstanding as % of GDP (2007)

Bra

zil

Au

stra

lia

Mex

ico

Sou

th A

Fric

a

UK

Jap

an

Un

ited

Sta

tes

Spai

n

Developed markets average 18%

Best emerging economies average 8%

2 3,5 3

11

16

26

36

5962

69

86

Turk

ey

‘07

Bra

zil

Mex

ico

Ch

ile

Sou

th A

Fric

a

Jap

an

Irel

and

Spai

n

Un

ited

Sta

tes

‘10

Bra

zil

UK

Developed markets average 64%

Best emerging economies average 12%CAGR

21%

AgendaUnderdeveloped capital markets – Auto Finance

Note: ¹New vehicles sales; ²Includes leasingSource: Fenabrave, BACEN, EIV, ANFAVEA, ANEF, CNW Marketing Research, CETIP, ACEA and UBS (not including motorcycles and light trucks)

New Car Sales¹ Million

Car penetrationCars / population (%)

1,61,8

2,3

2,7 2,8

3,4

2005 2006 2007 2008 2009 2010

CAGR 16% 50 48 47

44

25 23

15

France United Kingdom

EU United States

Korea BrazilRussia

90

61

% Vehicles Financed – 2009 (Includes Leasing) Total Vehicles Financing ²

59,177,4

111,6

139,1157,1

179,4CAGR 25%

2005 2006 2007 2008 2009 2010

2.4% 3.0% 4.1% 4.8% 5.4% 5.8%% GDP

11

Agenda

12

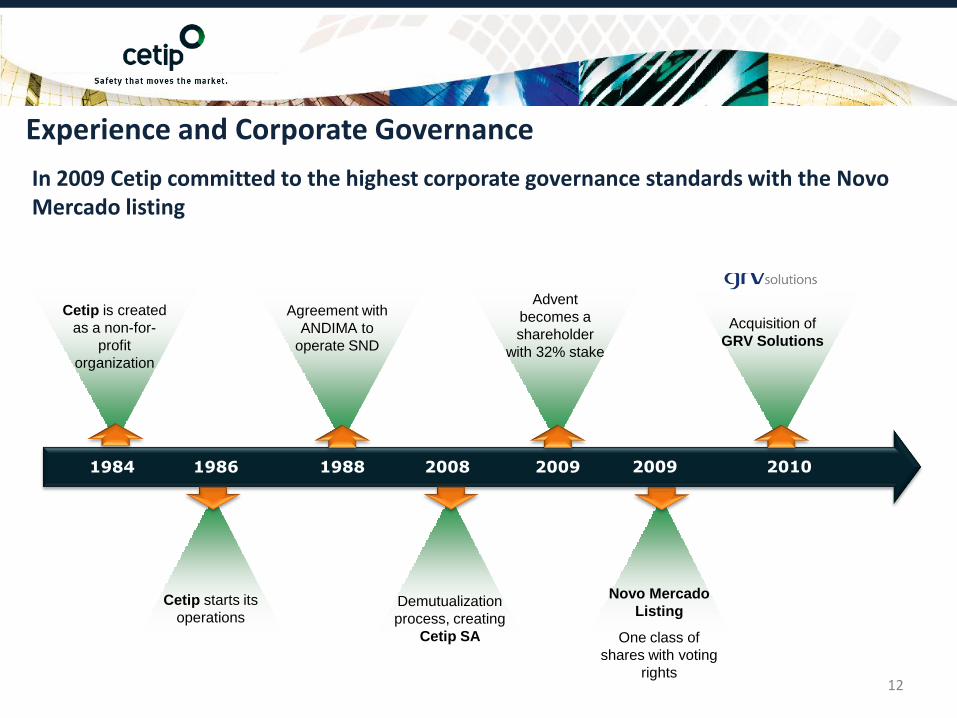

In 2009 Cetip committed to the highest corporate governance standards with the Novo Mercado listing

Experience and Corporate Governance

Cetip starts its

operations

Cetip is created

as a non-for-

profit

organization

1984 1986

Agreement with

ANDIMA to

operate SND

1988

Demutualization

process, creating

Cetip SA

2008

Advent

becomes a

shareholder

with 32% stake

2009 2009

Acquisition of

GRV Solutions

Novo Mercado

Listing

One class of

shares with voting

rights

2010

Agenda

13

Experience and Corporate Governance

Key Management Corporate Governance

Luiz Fernando Vendramini Fleury (CEO)Former CEO of IBI Bank / Redecard

Francisco Carlos Gomes (CFO)Former CFO of Bovespa, created CBLC

Wagner Anacleto (COO)Formerly at BM&FBovespa and CBLC

Carlos Eduardo Ratto Pereira (Commercial & Product Development Director)Formerly at BankBoston, Bank of America, Banco Itaú and HSBC Bank

Maurício Rebouças dos Santos (CIO)Formerly at Mercabolsa (Portugal), ANDIMA (Selic manager)

Carlos Menezes (Self regulation Director)Formerly at Unibanco and BPN Brasil Bank

Fabricio Bossle (Credit Operations Director)Formerly at GRV Solutions and Delloitte

Board

Committees

Self Regulation Board

Board of Directors

Pricing Committee

Self Regulation Officer

CEO

Credit Operations

Shareholders

CFO and Investor Relations

Commercial & Product

Development

Chief Operations

Officer

Chief Technology

Officer

Executive Bodies

Agenda

14

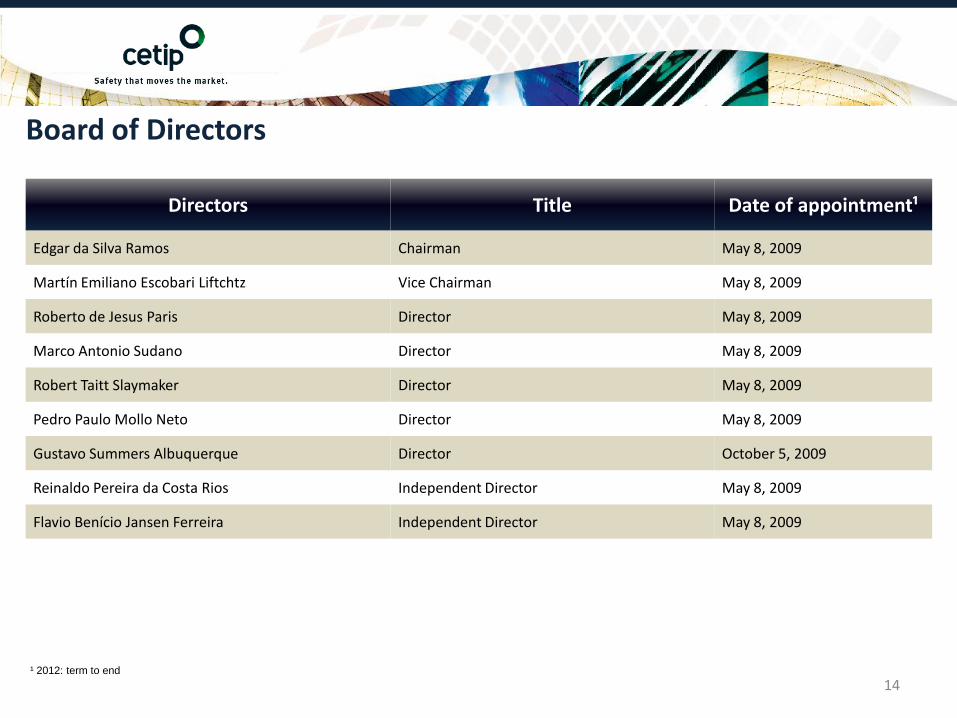

Board of Directors

Directors Title Date of appointment¹

Edgar da Silva Ramos Chairman May 8, 2009

Martín Emiliano Escobari Liftchtz Vice Chairman May 8, 2009

Roberto de Jesus Paris Director May 8, 2009

Marco Antonio Sudano Director May 8, 2009

Robert Taitt Slaymaker Director May 8, 2009

Pedro Paulo Mollo Neto Director May 8, 2009

Gustavo Summers Albuquerque Director October 5, 2009

Reinaldo Pereira da Costa Rios Independent Director May 8, 2009

Flavio Benício Jansen Ferreira Independent Director May 8, 2009

¹ 2012: term to end

Agenda

15

2. Strategic Positioning

Agenda

III. Develop connected businesses

• Renewal CIP contract and GRV acquisition

16

StrategyI. Continuous improvement on current core business

Improve quality of services and systems

• Depository

Introduction of new functionalities

• Resettable swaps and forwards

Broaden asset classes served

• Bank Corporate Bonds (LF)

• Structured Notes (COE)*

• OTC Equity Derivatives

Innovation: Introduction of new services

• MtM and Collateral Management

• Securities lending

1

2

3

4

1 Trading of fixed income securities

• Corporate bonds

• Bank corporate bonds (LF)

Trading of cash instruments

New exchange traded derivatives

Clearing & Settlement platform for specific OTC Derivatives

2

3

4

IV. Enlarge and develop the customer base

• Bill the beneficial owners and increase customer base by the connected business

V. Reinforce relationship with stakeholders

• Competitive prices, state of the art services, product innovation and flexibility

VI. Rationalize costs and maximize operational leverage

• Efficient capital structure

(*) Pending approval by the Brazilian Central Bank.

I. Expand the core business to adjacent layers

Agenda

17

2011 Strategic initiatives

Integrate

GRV

Roll Out

Real

Estate

Solutions

Roll Out

Collateral

Management

Develop right

strategy for our

new trading

fixed income

platform

Agenda

18

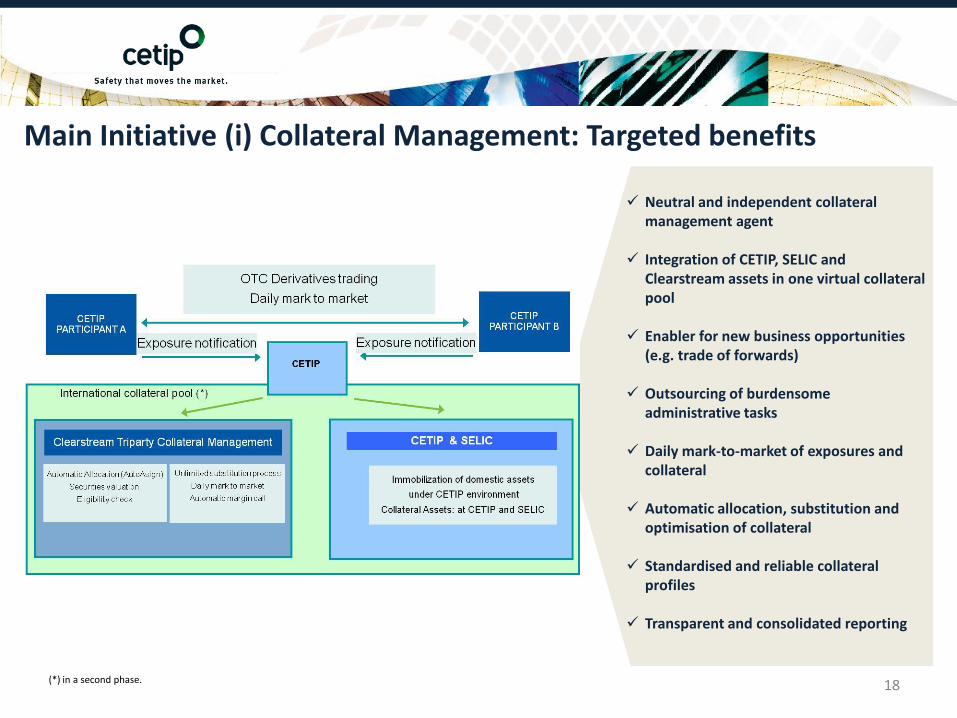

Neutral and independent collateral management agent

Integration of CETIP, SELIC and Clearstream assets in one virtual collateral pool

Enabler for new business opportunities (e.g. trade of forwards)

Outsourcing of burdensome administrative tasks

Daily mark-to-market of exposures and collateral

Automatic allocation, substitution and optimisation of collateral

Standardised and reliable collateral profiles

Transparent and consolidated reporting

Main Initiative (i) Collateral Management: Targeted benefits

(*) in a second phase.

Agenda

19

Main Initiative (ii) Electronic Trading Platform: Fixed Income

On November 11, CETIP and Deutsche Böerse AG

signed a non-binding letter of intention (LOI) to possibly

establish an electronic platform, initially focused on

fixed income security trading. The scope of the possible

strategic partnership will include joint promotion and

commercialization of an electronic trading platform for market participants, and the

parties will define the type of partnership to be established according to their

needs, as well as the market understanding. The scope of the agreement has not

yet been defined.

Agenda

20

Main Initiative (iii) SNG Real Estate

With the acquisition of GRV, we may jointly enhance and continue the project of developing a

platform to standardize and automatize registration of the real estate financing contracts,

integrating real estate notaries, lenders and consumers. SNG Real Estate will allow more agility

and security in the process of real estate registration in Brazil, as well as better management of

credit approval process.

Seller

Buyer

Lien

Registration

Protocol NotaryBank

Agenda

21

Main Initiative (iv) Letra Financeira

Main Characteristics

• Private and Public Offering;

• Remuneration: Fixed; DI; SELIC; IPCA; IGP-M; INPC; IGP-DI;

• Minimum term : 2 years;

• Compulsory requirement: exempt

Historical Growth – Balance outstanding

R$ billion

1,0 2,3 4,0

5,9 8,5

12,4

18,320,3 21,1

31,0

43.0

47,3

54,3

Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 Jan-10 Feb-11 Mar-11

• Approved by Brazilian Central Bank on February 2010

• Public Placement regulation approved by Brazilian Securities and Exchange Commission – CVM on December 2010

– Effective introduction on January 17, 2011

Source: CETIP and Brazilian Central Bank (BACEN).

Agenda

22

3. GRV acquisition

Agenda

23

Investment Highlights

Focus on registration/custody.

Serves the same client base.

Provides mission critical market infrastructure.

Natural Extension of our Core Business

Preservation of high growth rates and high margin profile.High Growth, High Margins

Nationwide network with zero fraud track record.

Operates online with 27 DMVs and 8,000 clients.Strong Barriers to Entry

Highly accretive.

Optimizes capital structure.Attractive Deal Structure

CETIP will continue committed to the highest Corporate Governance standards, being listed at the Novo Mercado

Agenda

24

GRV deal

Highlights Description

Source: GRV, CETIPNote: ¹ Two years grace on amortization. First 12 installments equivalent to 0.80% of issue amount; 47 amortization installments of 1.88% of issue amount and the last installment -

2.04% of issue amount

• GRV was valued at R$2.0 billion– R$1.0 billion in cash at closing– R$445 million to be paid in CETIP shares– R$555 million in 3 equal installments

• The equal installments will be paid: R$185 million on 30/Dec/2011, R$185 million on 30/Dec/2012 and R$185 million on 31/May/2013. Values are adjusted by IGP-M+2% p.a.

• Issue Amount: R$900 million• Cost: DI + 2.0% p.a.• Total Tenure: 7 years¹

• Underwriters: Bradesco, Itaú, Santander, Votorantim

Payment Conditions

Price

Debentures

Agenda

25

Debt Issuance

Extraordinary Amortization

Debentures• DI +2%• 7 years

Installments• IGPM+2%• 3 equal installments

R$900 million R$555 million

2/3 = 0.50% 1/3 = 0.75%

R$ 185 mm R$ 185 mm R$ 185 mm

01/01/1900 02/01/1900 03/01/190012/31/2011 12/31/2012 05/31/2013

1 2 3 4 5 6 70

1.88%

0.80%

~ R$16 mm

~R$7 mm

~R$18 mm(2.04%)

R$ 900 mm

Princip

al

Grace Period

Agenda

26

4. Financial Highlights

Agenda

27

1 – Derivatives market share is 75% (weighted average based on nominal values Source: CETIP, GRV and BM&FBovespa2 - Other includes: fees for corrections, distribution, info services and GRV Patio3- Depository comprises Custody and Transactions revenues.

Total 15,5% 4,4% 12,2% 10,5% 7,3% 2,6% 1,3% 0,8% 3,7% 25,9% 15,8% 100,0% 100,0% 100,0%

CETIP Market

Share100%

98%100% 100% 100% 70%

100%16% 91%

100%67%

100% 58% 42%

CETIP +

GRV

CETIP

Stand

Alone

GRV

Stand

Alone

53,6% 20,4% 100,0%

23,2% 39,8% 0,0%

3,4% 5,9% 0,0%

0,0% 0,0% 0,0%

3,7% 6,4% 0,0%

0,6% 1,0% 0,0%

15,4% 26,5% 0,0%

Fund

Transfer

Time

Deposits

Interbank

DepositsOther

Corporate

Bonds &

Securitization

Instruments

Quotas of

fundsSwaps Forwards Options TED´s Liens Contracts

Auto LoanFixed Income Instruments OTC Derivatives

Registrar

Services

Depository &

Repository

Services

Trading

Clearing

&Settlement

Processing

Other

Connectivity

Fee

(% of Q11

Revenues)

45%

Agenda

28

Financial Highlights

Net Revenues – R$ mm Adjusted Op. Expenses (ex-D&A) – R$ mm &% of Net Revenues

+ 52.5%

35.341.7 44.8

60.0

44.2

1Q10 2Q10 3Q10 4Q10 1Q11

31.1% 33.2% 30.4% 35.1% 25.5%

+1.1%

113.5 125.6 147.2

171.2 173.1

1Q10 2Q10 3Q10 4Q10 1Q11

Note: 2010 financial information is unaudited combined pro-forma and was based on reasonable premises. For complete disclosure on the adjustments and premises taken into consideration,

please access 1Q11 Earnings Release at www.cetio.com.br/ri

Agenda

29

Financial Highlights

48.7 57.7 61.9

85.0 77.5

1Q10 2Q10 3Q10 4Q10 1Q11

Adjusted EBITDA (R$ mm) & Margin (%) Adjusted Net Income (Cash Earnings) – R$ mm

78.2 83.9 102.4

111.2 128.9

1Q10 2Q10 3Q10 4Q10 1Q11

69.6% 64.9%68.9% 66.8% 74.5%

+ 59.3%

EPS/R$ 0.20 0.23 0.25 0.34 0.31

Note: 2010 financial information is unaudited combined pro-forma and was based on reasonable premises. For complete disclosure on the adjustments and premises taken into consideration,

please access 1Q11 Earnings Release at www.cetio.com.br/ri

AgendaRevenue Breakdown (%)

30

16% 13% 12% 11% 12%

12% 12% 11% 12% 14%

14%13% 13% 14%

15%

7%7%

7% 8%9%

7%7% 7%

9%8%

31%29% 28% 25%

23%

8% 14% 17% 15% 14%

5% 5% 5% 5% 5%

1Q10 2Q10 3Q10 4Q10 1Q11

Registration

Custody

Monthly Utilization

Transactions

Others

SNG Vehicle

GRV Contracts

Selling Information

130.0 144.1 166.8 194.6 196.9GR

GR:Gross revenues in R$mm.

Agenda

31

Adjusted Operating Expenses Breakdown (ex-D&A)

Note: Combined pro-forma for CETIP and GRV

57% 57% 53%62%

54%

32% 31%32%

25%27%

10% 11% 13% 11%13%

1% 1% 1% 5%

1Q10 2Q10 3Q10 4Q10 1Q11

35.3 41.7 44.8 60.0 44.2

+ 25.0%

- 26.4%

Other expenses/revenues

Taxes

Expenses incurred on equipment and system rental

General and administrative expenses

Outsourced services

Personnel

(% and R$ mm)

Agenda

32

(16.1) (42.1) 0.1 (23.6)

40.0

- 7.3 13.0 17.2

Reconciliation of Adjusted Net Income (Cash Earnings) – R$ mm

121.6

77.5

EB

ITD

A

D&

A

Fin

an

cia

l R

es

ult

Eq

uit

y in

th

e r

esu

lt o

f asso

cia

te

Inco

me

Ta

x &

So

cia

l C

on

trib

.

NE

T I

NC

OM

E

No

n r

ec

urr

ing

exp

en

se

s

Sto

ck

Op

tio

n

Go

od

will a

mo

rtiz

ati

on

: ta

x c

red

it

CA

SH

EA

RN

ING

S

Cash Earnings

Inta

ng

ible

go

od

wil

l a

mo

rtiz

ati

on

Agenda

33

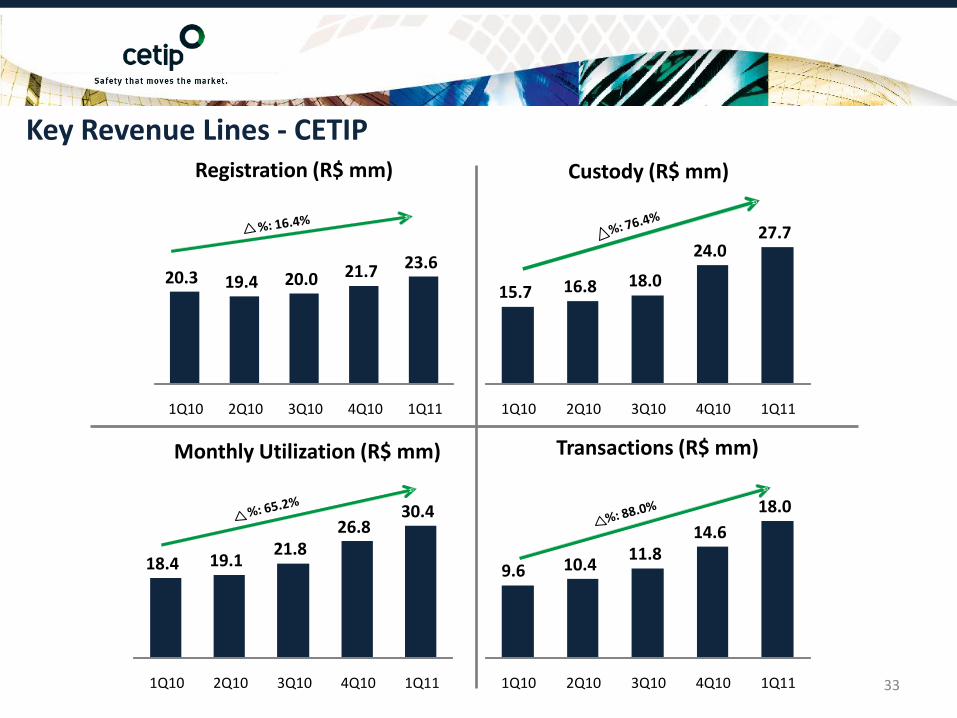

Key Revenue Lines - CETIP

20.3 19.4 20.0 21.7 23.6

1Q10 2Q10 3Q10 4Q10 1Q11

Registration (R$ mm)

15.7 16.8 18.0

24.0 27.7

1Q10 2Q10 3Q10 4Q10 1Q11

Custody (R$ mm)

18.4 19.1 21.8

26.8 30.4

1Q10 2Q10 3Q10 4Q10 1Q11

Monthly Utilization (R$ mm)

9.6 10.4 11.8

14.6

18.0

1Q10 2Q10 3Q10 4Q10 1Q11

Transactions (R$ mm)

Agenda

34

Key Revenue Lines - GRV

Note: Contract Additions began in September 2009.

39.8 41.146.2

49.344.8

1Q10 2Q10 3Q10 4Q10 1Q11

SNG Vehicles (R$ mm)

10.2

20.0

28.5 30.127.2

1Q10 2Q10 3Q10 4Q10 1Q11

GRV Contracts (R$ mm)

Agenda

35

52%

23%

56%

12% 68%

37%

30%

5% 3%

1Q10 4Q10 1Q11

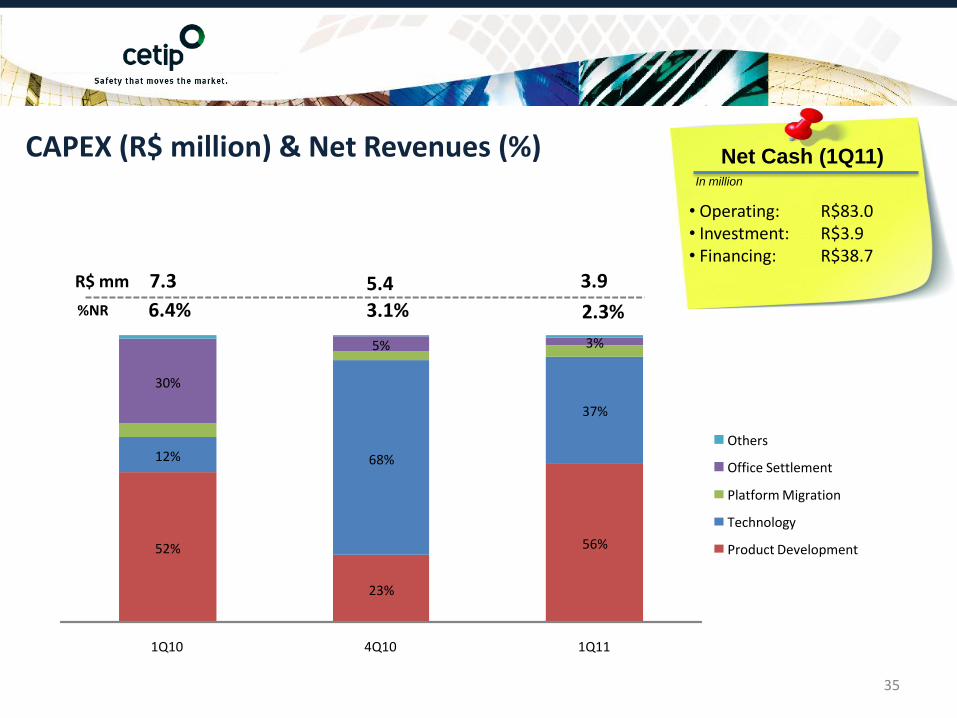

CAPEX (R$ million) & Net Revenues (%)

%NR

R$ mm 7.3 5.4 3.9

• Operating: R$83.0• Investment: R$3.9• Financing: R$38.7

Net Cash (1Q11)In million

6.4% 3.1% 2.3%

Others

Office Settlement

Platform Migration

Technology

Product Development

Agenda

36

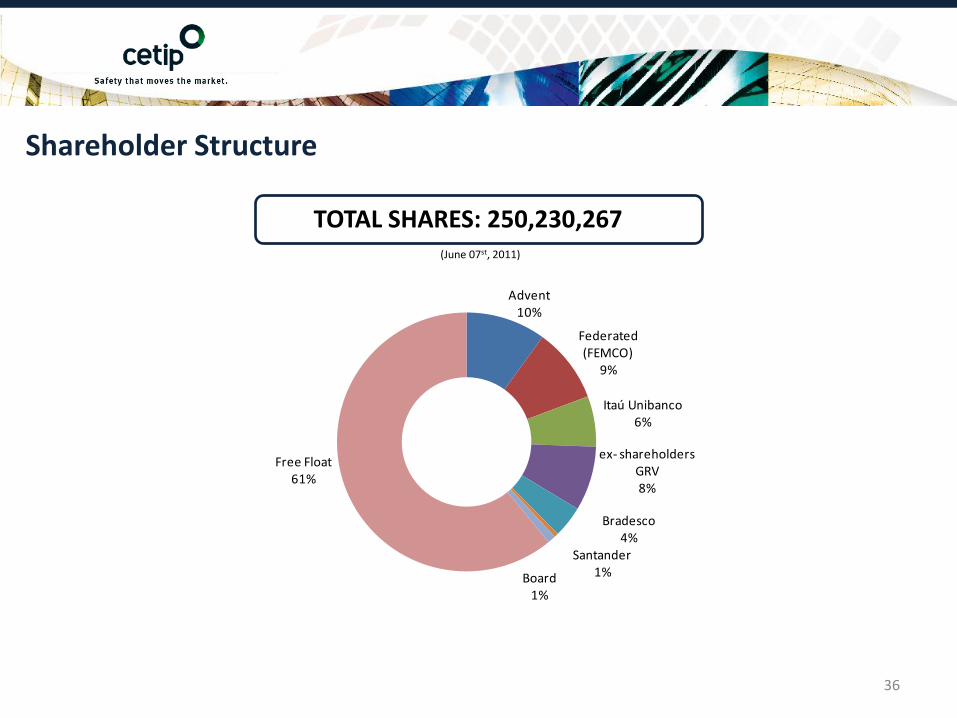

Shareholder Structure

(June 07st, 2011)

Advent10%

Federated (FEMCO)

9%

Itaú Unibanco6%

ex- shareholders GRV8%

Bradesco4%

Santander1%Board

1%

Free Float61%

TOTAL SHARES: 250,230,267

Agenda

-

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

2,00

7,00

12,00

17,00

22,00

27,00

Oct-0

9

No

v-09

De

c-09

De

c-09

Jan-1

0

Jan-1

0

Feb

-10

Feb

-10

Mar-1

0

Mar-1

0

Ap

r-10

Ap

r-10

May-1

0

May-1

0

May-1

0

Jun

-10

Jun

-10

Jul-1

0

Jul-1

0

Au

g-10

Au

g-10

Sep

-10

Sep

-10

Oct-1

0

Oct-1

0

No

v-10

No

v-10

De

c-10

De

c-10

Jan-1

1

Jan-1

1

Feb

-11

Feb

-11

Mar-1

1

Mar-1

1

Ap

r-11

Ap

r-11

May-1

1

May-1

1

Jun

-11

Vo

lum

e (R

$ m

m)

Pri

ce (R

$)

Volume-R$mm Price-R$

37

Price vs. Volume

Source: Bloomberg

CTIP3 (R$) vs. Volume (R$ mm): (10/30/09 – 06/15/11)

Agenda

5. Appendix

38

AgendaRegistration Revenue – R$ million

39

Fixed Income

OTC Derivatives

Others

15.312.6 13.2

15.1 16.2

4.6

5.6 5.24.6

5.40.4

1.2 1.62.1

2.0

1Q10 2Q10 3Q10 4Q10 1Q11

+ 8.9%

+16.4%

AgendaCustody Revenue – R$ million

40

15.716.8

18.0

24.0

27.7

1Q10 2Q10 3Q10 4Q10 1Q11

+76.4%

+ 15.3%

AgendaRevenues and Volumes of Transactions and Monthly Utilization

9.6 10.4 11.814.6

18.0

1Q10 2Q10 3Q10 4Q10 1Q11

+88.0%

8,8279,118

9,3959,705

9,934

1Q10 2Q10 3Q10 4Q10 1Q11

+12.5%

18.4 19.121.8

26.830.4

1Q10 2Q10 3Q10 4Q10 1Q11

+65.2%

+23.2%

+2.4%+13.3%

Transactions – Revenues (R$ million)

Monthly Utilization – Number of Participants Monthly Utilization – Revenues (R$ million)

41

13.3 14.4 16.219.8 21.0

1Q10 2Q10 3Q10 4Q10 1Q11

+57.8%

+6.1%

Transactions – Quantity (million)

AgendaDIs and CDBs - Volumes and Revenues

339398 439

638 601

1Q10 2Q10 3Q10 4Q10 1Q11

814 756896

1,351

1,091

1Q10 2Q10 3Q10 4Q10 1Q11

11.4

7.7 7.4 6.87.9

1Q10 2Q10 3Q10 4Q10 1Q11

+34.1% -30.1%

+77.2%

2.73.2 3.3

4.8 4.6

1Q10 2Q10 3Q10 4Q10 1Q11

+68.2%

-19.3%

-5.7%

+17.6%

-5.9%

CDB – Volume (R$ billion) CDB – Revenue (R$ million)

DI – Revenue (R$ million)DI – Volume (R$ billion)

42

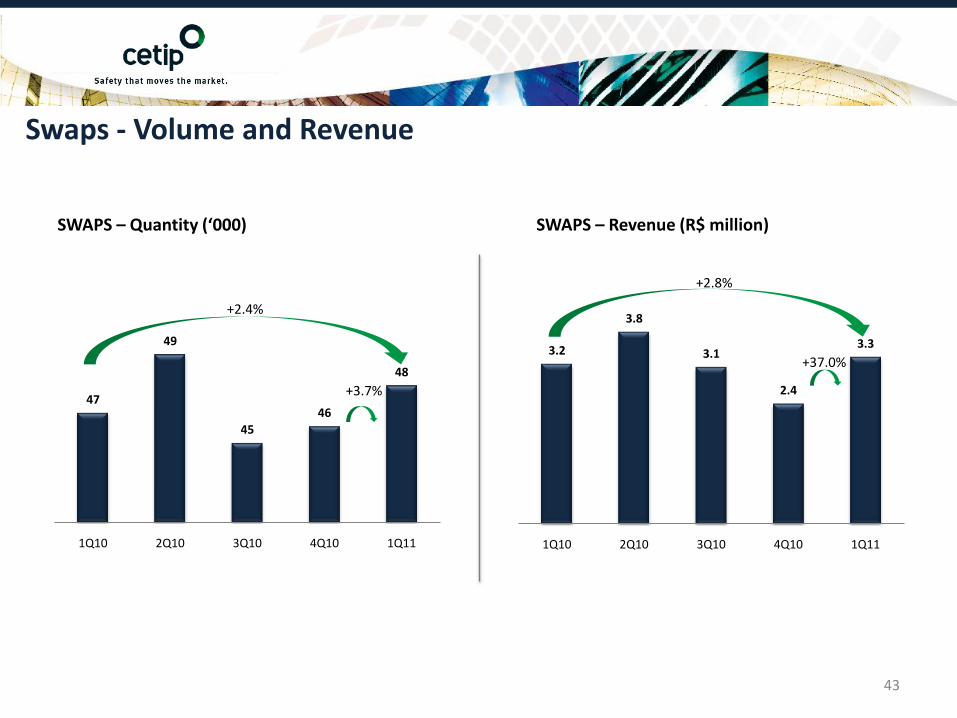

AgendaSwaps - Volume and Revenue

SWAPS – Quantity (‘000) SWAPS – Revenue (R$ million)

47

49

45

46

48

1Q10 2Q10 3Q10 4Q10 1Q11

+2.4%

+3.7%

3.2

3.8

3.1

2.4

3.3

1Q10 2Q10 3Q10 4Q10 1Q11

+37.0%

43

+2.8%

AgendaDebentures and Investment fund-quota – Volumes and Revenues

288

301

317

331342

1Q10 2Q10 3Q10 4Q10 1Q11

+18.6%

9.8 10.4 11.0

14.2 14.8

1Q10 2Q10 3Q10 4Q10 1Q11

+51.2%

656 690 713 766 803

1Q10 2Q10 3Q10 4Q10 1Q11

+22.4%

2.5 2.6 2.8

3.53.8

1Q10 2Q10 3Q10 4Q10 1Q11

+53.4%

+3.3%

+4.8%

+4.6%

+6.5%

Debentures – Average Volume (R$ billion) Debentures – Revenue (R$ million)

Investment fund-quota – Revenue (R$ million)Investment fund-quota – Average Volume (R$ billion)

44

AgendaCETIP: CIP – Revenue and Volume

18.320.0

23.3 24.6 23.8

1Q10 2Q10 3Q10 4Q10 1Q11

6.6

6.2

7.07.2

7.0

1Q10 2Q10 3Q10 4Q10 1Q11

+5.8%

+30.0%

- 1.9%-3.5%

359323

300

391

45Note: Revenue refers only to services of SITRAF – Transfer Funds System.

Processed EFTs(Quantity – MM)

Processed EFTs/day(Quantity - thousand)

Processed EFTs CIP – Revenue (R$ million)

383

AgendaGRV Market Information

46

Source: GRV Solutions and Fenabrave.

(million)

SNG Vehicle 1Q11 4Q10 1Q10 1Q11/4Q10 1Q11/1Q10

Number of vehicles sold 4.0 4.7 3.5 -14.6% 13.0%

New 1.3 1.6 1.2 -16.7% 6.3%

Used 2.7 3.1 2.3 -13.6% 16.6%

Number of Vehicles Financed 1.8 2.2 1.8 -18.5% 1.2%

New 0.9 1.1 0.9 -19.6% -1.3%

Used 0.9 1.1 0.9 -17.4% 3.8%

% Vehicles financed / vehicles sold 45% 47% 50% - -

GRV Contracts

Contracts Additions (Units) 1.2 1.5 0.5 -18.9% 139.4%

% Contracts additions / vehicles financed 68% 68% 29% - -

Volume Change (%)

Agenda

47

Legal Disclaimer

This material was issued by CETIP S.A. – Balcão Organizado de Ativos e Derivativos (“CETIP”). CETIP is authorized to operate by the Brazilian Securities

and Exchange Commission (CVM) and regulated by both the CVM and the Brazilian Central Bank. The information herein is only for reference purposes, as

CETIP has based this material on information obtained from sources it considers reliable, and CETIP may alter the content of this material at any time

without prior notice. CETIP is in no way responsible for losses arising from the direct or indirect use of this material or the consequences thereof. Although,

in some cases, this material may contain the opinions and future expectations of CETIP, there may be a series of risks, uncertainties and other material

factors that may cause real results to differ significantly from CETIP’s expectations. CETIP assumes no responsibility to update or alter this content, be it

due to new information, future events or other situations. Likewise, CETIP does not hereby provide any specific recommendations of a legal, tax, regulatory

or other nature not included the scope of this material. Clients contract any the services herein at their exclusive discretion and risk, and CETIP is only

responsible for communicating new products and services. The examples included herein symbolize hypothetical, simulated situations and are merely

illustrative. Their behavior may or may not represent real market situations, and CETIP is in no way liable for these cases or for the results of real cases.

This material was created by CETIP’s Products division according to applicable regulations and does not contain all the operating procedures and technical

details of the services herein presented. This content may differ from other disclosure materials issued by CETIP, and should not be used in any way as an

update of previous materials disclosed by CETIP. Nothing herein restricts or excludes and applicable legal responsibility of clients, according to legislation

and regulations. This material is the property of CETIP, and reproduction, in whole or in part, of this content, by any means, without express prior consent as

per Law no. 9,610/1998 is expressly prohibited. Due to the characteristics of the markets it serves, CETIP does not have a guaranty fund or other

mechanisms do indemnify losses, and for this reason no fees or contributions are charged for this purpose.

Investor [email protected]