Embed Size (px)

Citation preview

Student Loans Webinar: Inspiring Responsible BorrowingColleen MacDonald KrumwiedeMay 31, 2017

• Research on Debt Levels • Financial Behavior• Reasonable Debt Levels• Resources for Average Incomes Post Graduation• Communicating through the Life Cycle of the Loan• Review school examples

Today’s Objectives

• $1.26 trillion in total U.S. student loan debt• 43.3 million Americans with student loan debt• Student loan delinquency rate of 11.6%• Average monthly student loan payment (for borrower aged

20 to 30 years): $351• Median monthly student loan payment (for borrower aged 20

to 30 years): $203

Key Facts on Debt Levels

Sources: “Household Debt and Credit Report” by Center for Microeconomic Data https://www.newyorkfed.org/microeconomics/hhdc.html

National Student Loan Debt

Average in 2015

• $30,100 average debt• 7 in 10 seniors have debt• State by State Data

Distribution of Borrowers by Amount of Outstanding Education Debt, 2014• $22,191 average debt• 43% students graduate

with some debt

Sources: The Institute for College Access & Success & Federal Reserve Bank of New York Consumer Credit Panel/Equifax & College Board

Financial Behavior Can Affect Ability to Repay

• Marshmallow Experiment – Walter Mischel

• Child gets 1 marshmallow nowor

• Wait 15 min. and can have 2

• Results with 600+ kids• 66% only got 1• 33% delayed gratification to get 2

Instant Gratification vs. Delayed Gratification

• Component of Emotional Intelligence • Intrinsic vs. extrinsic locus of control• Self-regulation

• Can be taught to college students• Brains developing until age 25

• Key components: • Trust a reward is real• Reward must be worth the wait• Predictable and structured environment

Behavior Modification: Delay Gratification

How Much Can People Afford to Repay?

Graduates Afford to Repay

US Department of Education

• < 10% of your discretionary income

College Board

• < 10-15% of gross monthly income

Sources: US Department of Education &

College Board

Parents Afford to Repay

US Department of Education

• < 20% of your discretionary income

College Board

• < 37% of gross monthly income

Sources: US Department of Education &

College Board

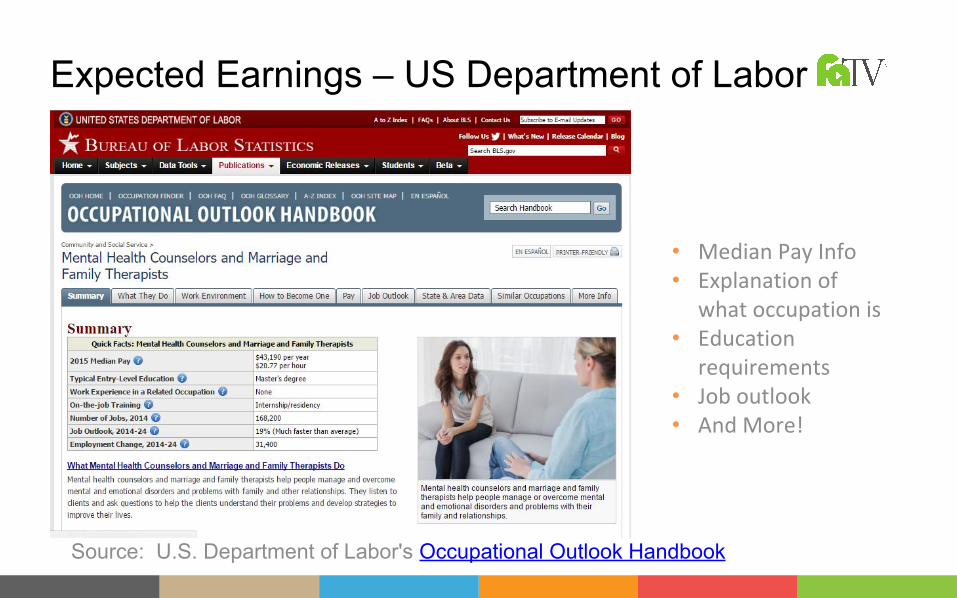

How to Project Your Earnings?

Source: U.S. Department of Labor's Occupational Outlook Handbook

Expected Earnings – US Department of Labor

••

•

••

Source: Salary.com

Expected Earnings – Salary.com

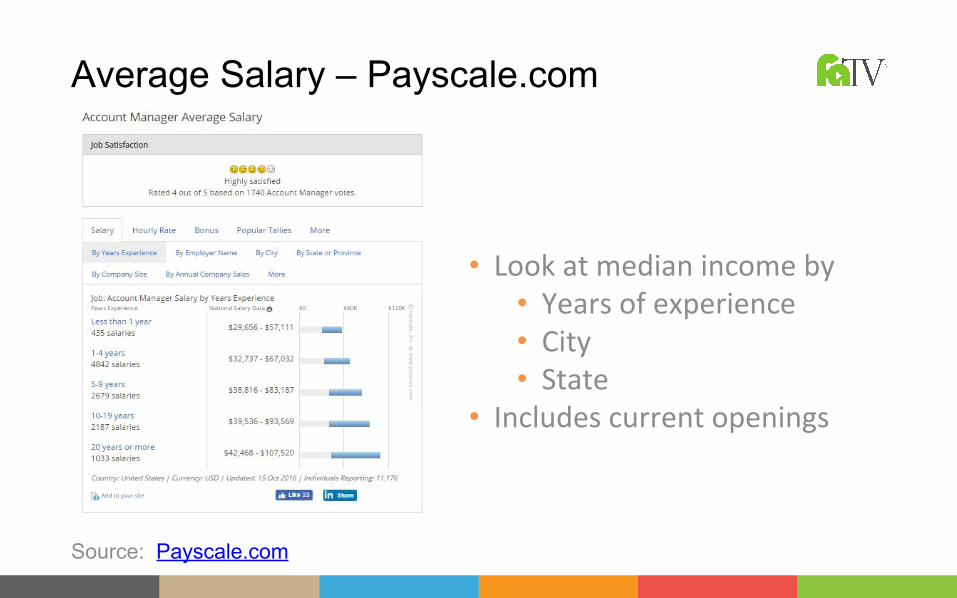

•

•

•

Source: Payscale.com

Average Salary – Payscale.com

••••

•

Repayment Calculators

Source: StudentLoans.gov

FSA Repayment Estimator

Source: YouCanDealWithIt.com

YouCanDealWithIt from PHEAA

Source: Navient.wealthmsi.com

Repayment Calculators

Provider Website Pros Cons FATV Rating

Federal Student Aid StudentLoans.gov Instant integration with personal loan

information

Lower utilization of graphs and visual aids;Issues with manual input

A

SimpleTuition PaybackSmarter.comIncludes tabs with multiple repayment plan options;Integration with NSLDS information

Requires creation of account for full customization. A-

PHEAA YouCanDealWithIt.com Asks questions and provides info on multiple repayment plan options

Outdated/broken links to find personal loan information. Results show on different page from inputs

B+

Navient Navient.wealthmsi.com

Highlights benefits of inflated payments and graphs annual cost and payments, Simple approach with results on same page as inputs.

No integration with NSLDS; Limited information on repayment plan options

B

Communication Opportunities

Communicate through the Loan Life Cycle• At initial financial aid application• When awarding• At each disbursement• Before re-applying for aid• Whenever awarded additional loan funds• Before graduation• At graduation• At the 5th month before repayment

• Suggest Optional Online Loan Counseling Session

• Remind that borrowers when they can still decline or reduce

• Send links to average salaries

• Provide links to repayment calculator

Types of Information to Convey

• Share videos that explain loan terms, repayment, and more

• Inform them of statistics from your school, state, or national

• Send funny memes, videos, or stories about over borrowing

Types of Information to Convey

Real School Case Studies

Denver SeminaryEncouraging Limited Borrowing

Location: Littleton, COSchool Type: 2-year private non-profitEnrollment: 929 (graduate-only) FT Students on Financial Aid: 57%Average Debt in 2015: $31,200Cohort Default Rate: 0.4%

Case Study: Denver Seminary

Results: Decreased average borrowing by $1,200 per year

Western Governors UniversityEncouraging Limited Borrowing

Location: Salt Lake City, UTSchool Type: 4-year private non-profitEnrollment: 70,504 (54,735 undergraduate) FT Beginning Undergrads on Financial Aid: 84%Average Debt in 2015: $19,050Cohort Default Rate: 4.5%

Case Study: Western Governors University

Results: Decreased average borrowing by $3,200 per year