Embed Size (px)

Citation preview

CONSUMER PRODUCTS & RETAIL

B G L C O . C O M J A N U A R Y | 2 0 1 7

J O H N R . T I L S O NM A N AG I N G D I R E C TO R & G R O U P H E A D3 1 2 . 6 5 8 . 1 6 0 0J T I L S O N @ B G LC O. C O M

ALEXANDER N. [email protected]

REBECCA A. DICKENSCHEIDTDIRECTOR OF [email protected]

2

3

1 1

1 6

M A C R O E N V I R O N M E N T

H O M E E N V I R O N M E N T

A U TO M OT I V E A F T E R M A R K E T

A B O U T U S

TA B L E O F C O N T E N T S

INSIDER

Unemployment

Consumer Confidence

Housing Starts

Source: The University of Michigan.

Source: U.S. Census Bureau. Source: U.S. Census Bureau.

4.7%4%

5%

6%

7%

8%

9%

10%

11%

Jan-

05

Jun-

06

Dec

-07

Jun-

09

Dec

-10

Jun-

12

Dec

-13

Jun-

15

Dec

-16

1,226

795

417

0

500

1,000

1,500

2,000

2,500

Jan-

05

Jun-

06

Dec

-07

Jun-

09

Dec

-10

Jun-

12

Dec

-13

Jun-

15

Dec

-16

(In T

hous

ands

)

Total In Structures with 1 Unit In Structures with 5 Units or More

98.1

50

60

70

80

90

100

110

Jan-

05

Jul-

06

Jan-

08

Jul-

09

Jan-

11

Jul-

12

Jan-

14

Jul-

15

Jan-

17

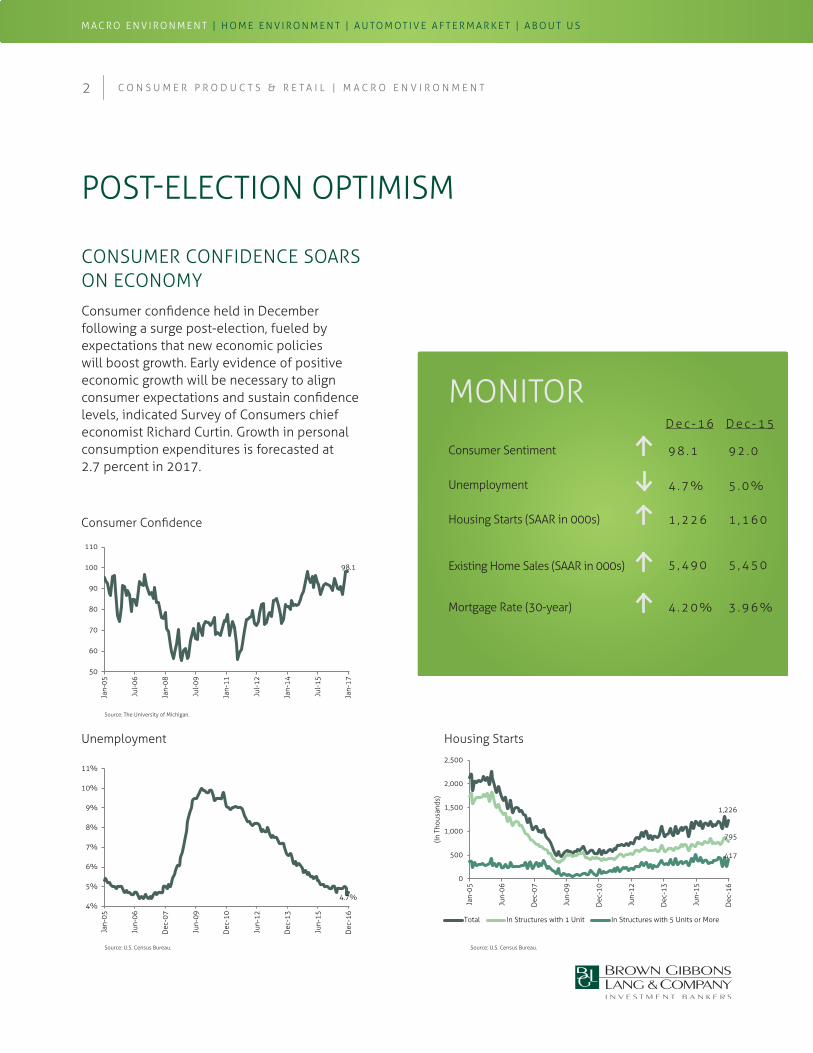

POST-ELECTION OPTIMISM

CONSUMER CONFIDENCE SOARS ON ECONOMY

Consumer confidence held in December following a surge post-election, fueled by expectations that new economic policies will boost growth. Early evidence of positive economic growth will be necessary to align consumer expectations and sustain confidence levels, indicated Survey of Consumers chief economist Richard Curtin. Growth in personal consumption expenditures is forecasted at 2.7 percent in 2017.

MONITOR

Consumer Sentiment

Unemployment

Housing Starts (SAAR in 000s)

Existing Home Sales (SAAR in 000s)

Mortgage Rate (30-year)

2 C O N S U M E R P R O D U C T S & R E T A I L | M A C R O E N V I R O N M E N T

D e c - 1 6 D e c - 1 5

9 8 . 1 9 2 . 0

4 . 7 % 5 . 0 %

1 , 2 2 6 1 , 1 6 0

5 , 4 9 0 5 , 4 5 0

4 . 2 0 % 3 . 9 6 %

3

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

HOME ENVIRONMENT

3 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

MARKET UPDATE

4 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T

Portfolio reshaping is continuing in the Home Goods market as industry participants look to M&A to sharpen focus on core, growth-generating businesses. Industry players are conducting portfolio reviews and shedding non-core, slower-growth, or underperforming brands and using the proceeds to fund growth.

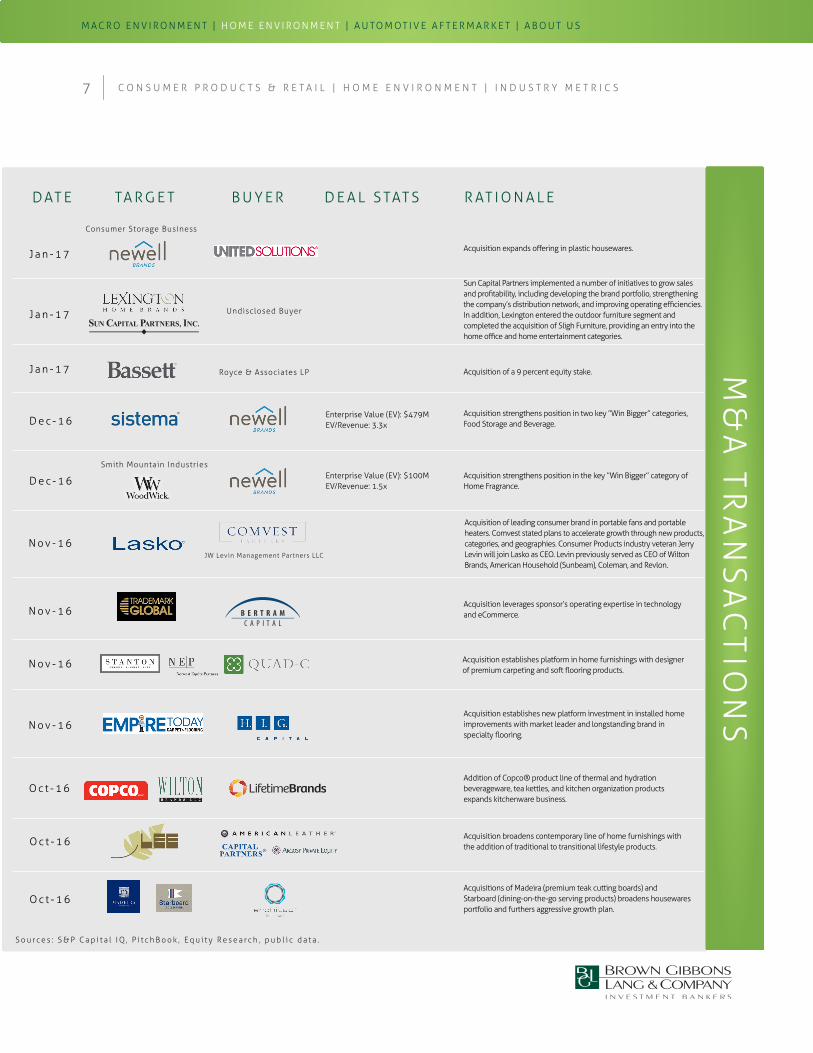

Newell Brands (NYSE:NWL) is culling its portfolio following the transformational $18 billion Jarden acquisition in April 2016, aiming to shed about 10 percent of its portfolio, or about $1.5 billion in sales. In July 2016, Newell sold its Window Coverings business comprised of the Levolor and Kirsch brands to Hunter Douglas (ENXTAM:HDG) for $270 million. Announced in October 2016, the pending sale of its Tool Business to Stanley Black & Decker (NYSE:SWK) is expected to fetch $1.95 billion. In January 2017, the company reached an agreement with United Solutions to sell its Consumer Storage Container business (Home Solutions). Other businesses targeted for divestiture by the first half of 2017 include Winter Sports, known for the K2 brand (Outdoor Solutions segment); and its Heaters, Humidifiers, and Fans (Consumer Solutions) business.

These efforts will advance the company’s Growth Game Plan announced last October. “The combination of Newell Rubbermaid and Jarden has created a unique platform for transformative value creation and the actions we are taking to reshape the company will unlock this opportunity, bringing greater investment and growth to our highest potential categories like Writing, Home Fragrance, Baby, Food Storage & Preparation, Appliances & Cookware, and Outdoor & Recreation,” said Mark Tarchetti, Newell Brands President. “The choices we are making will strengthen the underlying growth and performance of our most strategic businesses and over time enable us to scale our core categories through external development.”

In December 2016, Newell announced the acquisitions of food container manufacturer Sistema and Smith Mountain Industries, maker of WoodWick® brand candles, citing a strategic fit within “Win Bigger” business lines of Food Storage and Home Fragrance. The combined price tag for the two companies was $579 million.

In a November 2016 analyst presentation1, Newell identified portfolio priorities Baby, Writing, and Appliances which are driving strong global growth, posting gains of 10.4 percent, 9.4 percent, and 8.9 percent, respectively2—segments where acquisitions continue to be essential in value creation: in Baby, the 2014 acquisition of Baby Jogger from the Riverside Company and in Writing, Elmer’s Products, acquired from Berwind Corporation in 2015.

“Newell Brands new strategic plan establishes a clear set of investment priorities, a new organization design for the company, and a sharp set of portfolio choices that will focus our resources on the businesses with the greatest potential for growth and value creation,” says Newell CEO Michael Polk.

With the acquisition of the Levolor and Kirsch brands, Hunter Douglas will gain two longstanding brands and boost its presence in the home center channel in North America where it has a limited presence, according to a company statement. Commenting on the acquisition, Hunter Douglas CEO Ron Kass said: “Levolor is an exciting addition to the Hunter Douglas portfolio that allows us to supplement our longstanding position in the specialty dealer channel with a strengthened position in the home center channel. Together these businesses will allow us to better service the unique needs of each of these distribution channels and consumer market segments.”

1 M o r g a n S t a n l e y G l o b a l C o n s u m e r a n d R e t a i l C o n f e r e n c e , N o v e m b e r 2 0 1 62 C o r e s a l e s g r o w t h y e a r t o d a t e t h r o u g h e n d o f Q 3 2 0 1 6

PORTFOLIO HONING IGNITES M&A

5

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , C o m p a n y F i l i n g s , E q u i t y R e s e a r c h , p u b l i c d a t a .

MARKET UPDATE

5 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T

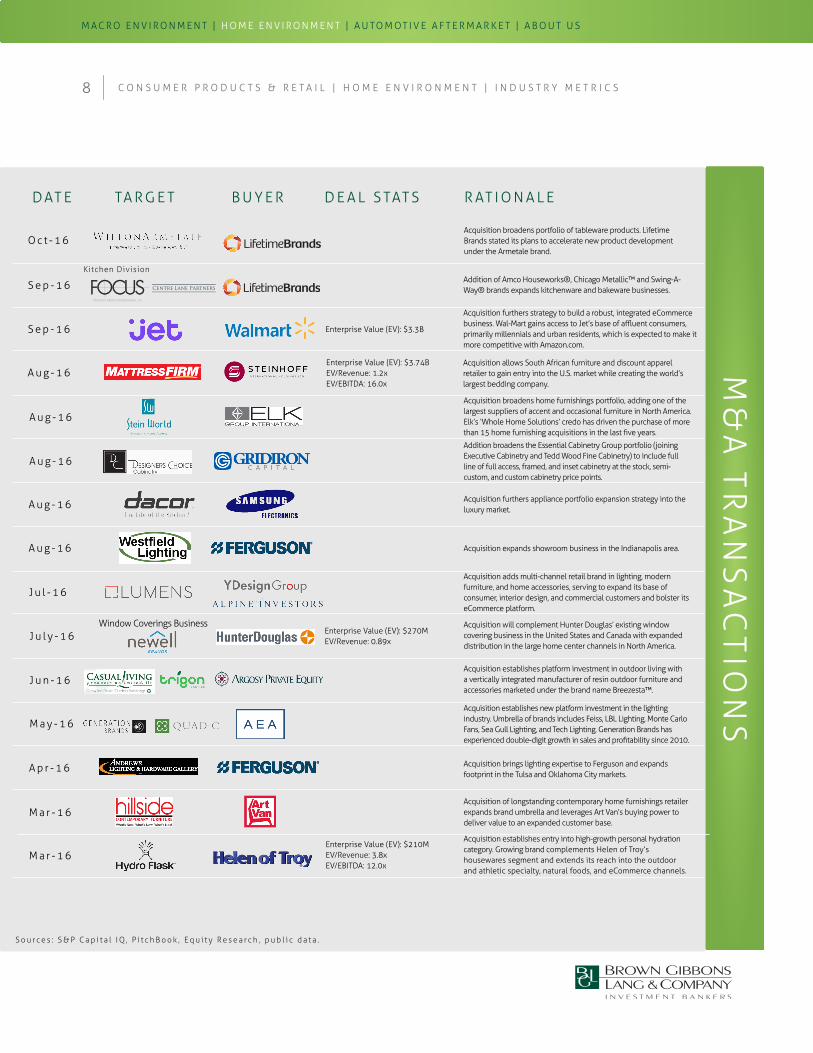

Focus Products Group (FPG), a portfolio company of Centre Lane Partners, divested three housewares brands in September 2016, announcing the sale of its Kitchen Division to Lifetime Brands (NasdaqGS:LCUT). Lifetime Brands was acquisitive in 2016, adding five brands in three acquisitions with the purchase of Amco Houseworks®, Swing-A-Way®, and Chicago™Metallic from FPG, and in separate transactions, the Copco and Armetale product lines from Wilton Industries.

“We’re focusing on acquiring companies with strong brands that are in the same businesses and adjacent categories or with deep penetration in this specific category to support our growth,” said Lifetime Brands CEO Jeffrey Siegel, commenting on the acquisitions. All five brands are in categories where Lifetime is already well established, Siegel indicated.

Chicago Metallic produces high end bakeware, a category where Lifetime “lacked a strong brand”. Amco Houseworks and Swing-A-Way are additive to Lifetime’s kitchenware business. The 114-year old Armetale brand will extend Lifetime’s line of tableware products, with opportunities identified to accelerate new product development. Copco’s innovation in thermal and hydration beverageware was a draw, a category which Lifetime identified as showing “explosive growth”, citing Copco’s double-digit growth in the segment.

PORTFOLIO HONING IGNITES M&A

Just as acquisitions are a primary tool to boost revenue in a slow organic growth environment, divestitures are increasingly in vogue as companies look to prune non-core or underperforming businesses and reinvest proceeds to fund core business activities and pursue new markets. Divestments are seen as a key way to fund growth, presenting a dynamic backdrop for M&A, according to an E&Y Global Corporate Divestment study, which revealed nearly half of company executives surveyed were planning a divestiture within the next two years.

DIVESTMENT KEY TO FUNDING GROWTH

*Source: 2016 ”Global Corporate Divestment Study”. E&Y survey of 900 corporate executives and 100 private equity executives surveyed between September and November 2015. Consumer Products, Financial Services, and Life Sciences and Technology were the primary focus of nine industry sectors represented.

49Pe r c e n t o f

c o m p a n i e s p l a n n i n g t o d i v e s t w i t h i n t h e

n e x t t w o y e a r s .

70Pe r c e n t o f

c o m p a n i e s u s i n g d i v e s t m e n t s t o f u n d

g r o w t h .

84Pe r c e n t w h o b e l i e v e d i v e s t m e n t c r e a t e d

l o n g - t e r m v a l u e i n t h e r e m a i n i n g

b u s i n e ss .

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , C o m p a n y F i l i n g s , E q u i t y R e s e a r c h , p u b l i c d a t a .

CASE STUDYAcquisitive Lifetime Brands (NasdaqGS:LCUT) is accelerating growth through acquisitions, purchasing iconic brands Amco Houseworks®, Swing-A-Way®, and Chicago™Metallic from Focus Products Group in September 2016. Focus Products Group is a portfolio company of Centre Lane Partners. BGL’s Consumer Products & Retail team served as the exclusive financial advisor to Focus Products Group in the transaction.

Amco has been a recognized signature brand in stainless steel tools and gadgets for more than 45 years, with an offering that includes fruit and vegetable slicers, squeezers, mixing bowls, measuring cups, and spoons, as well as professional-grade utensils. Swing-A-Way can openers first made their launch in 1938, and the line was expanded to include corkscrews, vegetable peelers, and jar openers. Chicago™Metallic has been providing home bakers with commercial-grade, quality bakeware products for more than 100 years. Each brand’s quality reputation and premium positioning have solidified longstanding relationships with many of the nation’s leading department stores, and gourmet and specialty, mass, and online retailers.

Commenting on the transaction, Lifetime CEO Jeffrey Siegel said: “We are excited to expand our portfolio of brands with three distinguished names that complement our market-leading kitchenware and bakeware businesses. This acquisition meets our criteria of well-known and longstanding brands; premium positioning in the marketplace; established relationships with blue-chip customers; and significant opportunities for growth.”

Lifetime is anticipating immediate synergy opportunities from the acquisition, Seigel said, adding, “These three brands fit perfectly into our platform, and we have the resources to quickly enhance their performance. Since they are in categories where Lifetime is already established, we expect the acquisition to provide immediate gross margin dollars without an accompanying increase in SG&A.”

6 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T | C A S E S T U D Y

“ This acquisition meets our criteria of well-known and longstanding brands; premium positioning in the marketplace; established relationships with blue-chip customers; and

significant opportunities for growth.”

Jeffrey Siegel CEO, Lifetime Brands

7

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

7 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T | I N D U S T R Y M E T R I C SM

&A

TR

AN

SA

CT

ION

S

DAT E TA R G E T B U Y E R D E A L S TAT S R AT I O N A L E

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , E q u i t y R e s e a r c h , p u b l i c d a t a .

O c t - 1 6Addition of Copco® product line of thermal and hydration beverageware, tea kettles, and kitchen organization products expands kitchenware business.

N o v - 1 6Acquisition establishes new platform investment in installed home improvements with market leader and longstanding brand in specialty flooring.

N o v - 1 6 Acquisition establishes platform in home furnishings with designer of premium carpeting and soft flooring products.

O c t - 1 6 Acquisition broadens contemporary line of home furnishings with the addition of traditional to transitional lifestyle products.

O c t - 1 6Acquisitions of Madeira (premium teak cutting boards) and Starboard (dining-on-the-go serving products) broadens housewares portfolio and furthers aggressive growth plan.

D e c - 1 6 Acquisition strengthens position in the key ”Win Bigger” category of Home Fragrance.

Enterprise Value (EV): $100MEV/Revenue: 1.5x

Smith Mountain Industries

J a n - 1 7

J a n - 1 7 Royce & Associates LP Acquisition of a 9 percent equity stake.

D e c - 1 6Enterprise Value (EV): $479MEV/Revenue: 3.3x

Acquisition strengthens position in two key ”Win Bigger” categories, Food Storage and Beverage.

N o v - 1 6

Acquisition of leading consumer brand in portable fans and portable heaters. Comvest stated plans to accelerate growth through new products, categories, and geographies. Consumer Products industry veteran Jerry Levin will join Lasko as CEO. Levin previously served as CEO of Wilton Brands, American Household (Sunbeam), Coleman, and Revlon.

JW Levin Management Partners LLC

N o v - 1 6

J a n - 1 7Acquisition expands offering in plastic housewares.

Consumer Storage Business

Undisclosed Buyer

Sun Capital Partners implemented a number of initiatives to grow sales and profitability, including developing the brand portfolio, strengthening the company’s distribution network, and improving operating efficiencies. In addition, Lexington entered the outdoor furniture segment and completed the acquisition of Sligh Furniture, providing an entry into the home office and home entertainment categories.

Acquisition leverages sponsor’s operating expertise in technology and eCommerce.

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

8 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T | I N D U S T R Y M E T R I C SM

&A

TR

AN

SA

CT

ION

S

DAT E TA R G E T B U Y E R D E A L S TAT S R AT I O N A L E

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , E q u i t y R e s e a r c h , p u b l i c d a t a .

A u g - 1 6

Acquisition broadens home furnishings portfolio, adding one of the largest suppliers of accent and occasional furniture in North America. Elk’s ‘Whole Home Solutions’ credo has driven the purchase of more than 15 home furnishing acquisitions in the last five years.

M a r - 1 6Acquisition of longstanding contemporary home furnishings retailer expands brand umbrella and leverages Art Van’s buying power to deliver value to an expanded customer base.

A p r - 1 6 Acquisition brings lighting expertise to Ferguson and expands footprint in the Tulsa and Oklahoma City markets.

A u g - 1 6 Acquisition expands showroom business in the Indianapolis area.

M a y - 1 6

Acquisition establishes new platform investment in the lighting industry. Umbrella of brands includes Feiss, LBL Lighting, Monte Carlo Fans, Sea Gull Lighting, and Tech Lighting. Generation Brands has experienced double-digit growth in sales and profitability since 2010.

A u g - 1 6 Acquisition furthers appliance portfolio expansion strategy into the luxury market.

A u g - 1 6

Addition broadens the Essential Cabinetry Group portfolio (joining Executive Cabinetry and Tedd Wood Fine Cabinetry) to include full line of full access, framed, and inset cabinetry at the stock, semi-custom, and custom cabinetry price points.

J u n - 1 6Acquisition establishes platform investment in outdoor living with a vertically integrated manufacturer of resin outdoor furniture and accessories marketed under the brand name Breezesta™.

J u l y - 1 6Acquisition will complement Hunter Douglas’ existing window covering business in the United States and Canada with expanded distribution in the large home center channels in North America.

Window Coverings Business Enterprise Value (EV): $270MEV/Revenue: 0.89x

M a r - 1 6

Acquisition establishes entry into high-growth personal hydration category. Growing brand complements Helen of Troy’s housewares segment and extends its reach into the outdoor and athletic specialty, natural foods, and eCommerce channels.

Enterprise Value (EV): $210MEV/Revenue: 3.8xEV/EBITDA: 12.0x

J u l - 1 6

Acquisition adds multi-channel retail brand in lighting, modern furniture, and home accessories, serving to expand its base of consumer, interior design, and commercial customers and bolster its eCommerce platform.

A u g - 1 6Enterprise Value (EV): $3.74BEV/Revenue: 1.2xEV/EBITDA: 16.0x

Acquisition allows South African furniture and discount apparel retailer to gain entry into the U.S. market while creating the world’s largest bedding company.

S e p - 1 6Addition of Amco Houseworks®, Chicago Metallic™ and Swing-A-Way® brands expands kitchenware and bakeware businesses.

Kitchen Division

S e p - 1 6 Enterprise Value (EV): $3.3B

Acquisition furthers strategy to build a robust, integrated eCommerce business. Wal-Mart gains access to Jet’s base of affluent consumers, primarily millennials and urban residents, which is expected to make it more competitive with Amazon.com.

O c t - 1 6Acquisition broadens portfolio of tableware products. Lifetime Brands stated its plans to accelerate new product development under the Armetale brand.

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

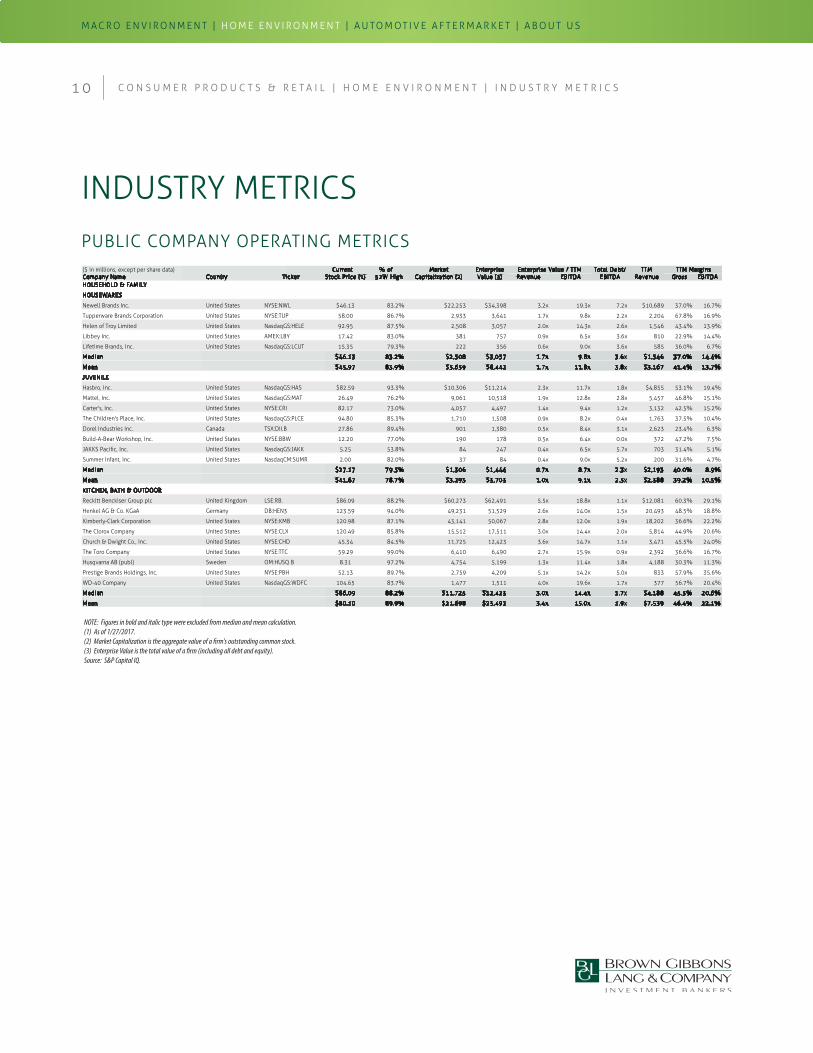

INDUSTRY METRICS

9 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T | I N D U S T R Y M E T R I C S

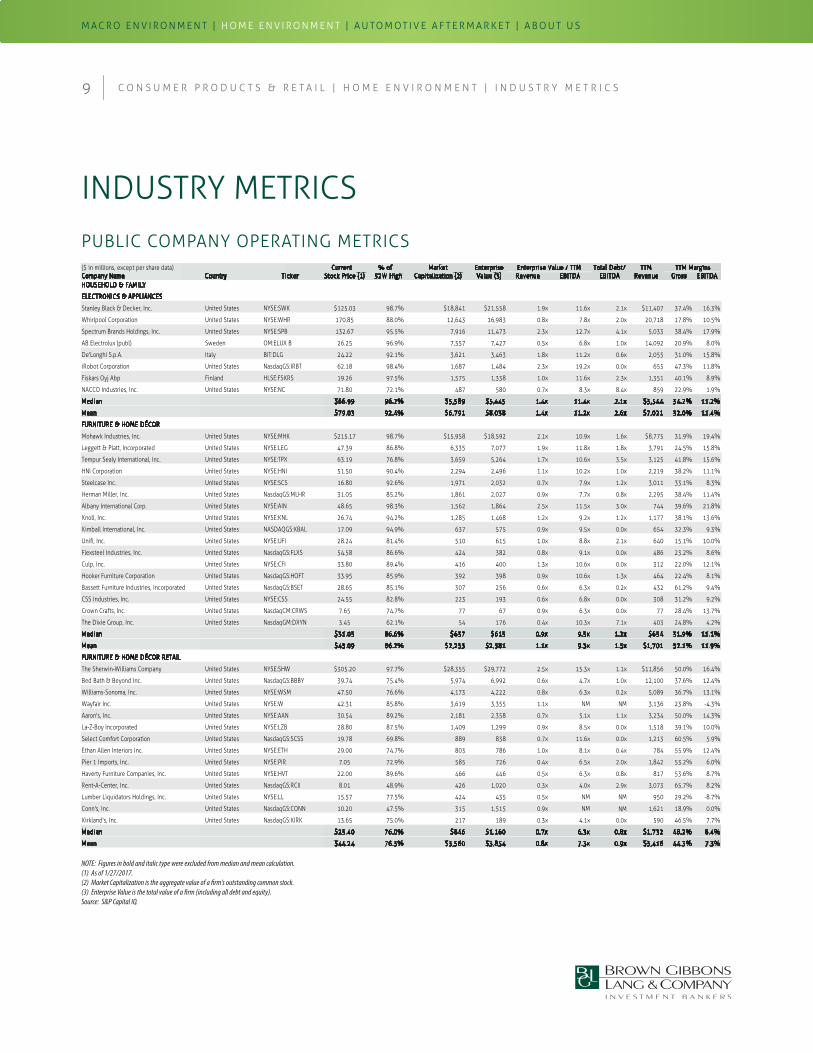

PUBLIC COMPANY OPERATING METRICS

NOTE: Figures in bold and italic type were excluded from median and mean calculation.(1) As of 1/27/2017.(2) Market Capitalization is the aggregate value of a �rm's outstanding common stock.(3) Enterprise Value is the total value of a �rm (including all debt and equity).Source: S&P Capital IQ.

($ in millions, except per share data) Current % of Market Enterprise Total Debt/ TTMCompany Name Country Ticker Stock Price (1) 52W High Capitalization (2) Value (3) Revenue EBITDA EBITDA Revenue Gross EBITDAHOUSEHOLD & FAMILY

ELECTRONICS & APPLIANCES

Stanley Black & Decker, Inc. United States NYSE:SWK $125.03 98.7% $18,841 $21,558 1.9x 11.6x 2.1x $11,407 37.4% 16.3%

Whirlpool Corporation United States NYSE:WHR 170.85 88.0% 12,643 16,983 0.8x 7.8x 2.0x 20,718 17.8% 10.5%

Spectrum Brands Holdings, Inc. United States NYSE:SPB 132.67 95.5% 7,916 11,473 2.3x 12.7x 4.1x 5,033 38.4% 17.9%

AB Electrolux (publ) Sweden OM:ELUX B 26.25 96.9% 7,557 7,427 0.5x 6.8x 1.0x 14,092 20.9% 8.0%

De'Longhi S.p.A. Italy BIT:DLG 24.22 92.1% 3,621 3,463 1.8x 11.2x 0.6x 2,055 31.0% 15.8%

iRobot Corporation United States NasdaqGS:IRBT 62.18 98.4% 1,687 1,484 2.3x 19.2x 0.0x 655 47.3% 11.8%

Fiskars Oyj Abp Finland HLSE:FSKRS 19.26 97.5% 1,575 1,338 1.0x 11.6x 2.3x 1,351 40.1% 8.9%

NACCO Industries, Inc. United States NYSE:NC 71.80 72.1% 487 580 0.7x 8.3x 8.4x 859 22.9% 1.9%

Median $66.99 96.2% $5,589 $5,445 1.4x 11.4x 2.1x $3,544 34.2% 11.2%

Mean $79.03 92.4% $6,791 $8,038 1.4x 11.2x 2.6x $7,021 32.0% 11.4%

FURNITURE & HOME DÉCOR

Mohawk Industries, Inc. United States NYSE:MHK $215.17 98.7% $15,958 $18,592 2.1x 10.9x 1.6x $8,775 31.9% 19.4%

Leggett & Platt, Incorporated United States NYSE:LEG 47.39 86.8% 6,335 7,077 1.9x 11.8x 1.8x 3,791 24.5% 15.8%

Tempur Sealy International, Inc. United States NYSE:TPX 63.19 76.8% 3,659 5,264 1.7x 10.6x 3.5x 3,125 41.8% 15.6%

HNI Corporation United States NYSE:HNI 51.50 90.4% 2,294 2,496 1.1x 10.2x 1.0x 2,219 38.2% 11.1%

Steelcase Inc. United States NYSE:SCS 16.80 92.6% 1,971 2,032 0.7x 7.9x 1.2x 3,011 33.1% 8.3%

Herman Miller, Inc. United States NasdaqGS:MLHR 31.05 85.2% 1,861 2,027 0.9x 7.7x 0.8x 2,295 38.4% 11.4%

Albany International Corp. United States NYSE:AIN 48.65 98.3% 1,562 1,864 2.5x 11.5x 3.0x 744 39.6% 21.8%

Knoll, Inc. United States NYSE:KNL 26.74 94.2% 1,285 1,468 1.2x 9.2x 1.2x 1,177 38.1% 13.6%

Kimball International, Inc. United States NASDAQGS:KBAL 17.09 94.9% 637 575 0.9x 9.5x 0.0x 654 32.3% 9.3%

Unifi, Inc. United States NYSE:UFI 28.24 81.4% 510 615 1.0x 8.8x 2.1x 640 15.1% 10.0%

Flexsteel Industries, Inc. United States NasdaqGS:FLXS 54.58 86.6% 424 382 0.8x 9.1x 0.0x 486 23.2% 8.6%

Culp, Inc. United States NYSE:CFI 33.80 89.4% 416 400 1.3x 10.6x 0.0x 312 22.0% 12.1%

Hooker Furniture Corporation United States NasdaqGS:HOFT 33.95 85.9% 392 398 0.9x 10.6x 1.3x 464 22.4% 8.1%

Bassett Furniture Industries, Incorporated United States NasdaqGS:BSET 28.65 85.1% 307 256 0.6x 6.3x 0.2x 432 61.2% 9.4%

CSS Industries, Inc. United States NYSE:CSS 24.55 82.8% 223 193 0.6x 6.8x 0.0x 308 31.2% 9.2%

Crown Crafts, Inc. United States NasdaqCM:CRWS 7.65 74.7% 77 67 0.9x 6.3x 0.0x 77 28.4% 13.7%

The Dixie Group, Inc. United States NasdaqGM:DXYN 3.45 62.1% 54 176 0.4x 10.3x 7.1x 403 24.8% 4.2%

Median $31.05 86.6% $637 $615 0.9x 9.5x 1.2x $654 31.9% 11.1%

Mean $43.09 86.2% $2,233 $2,581 1.1x 9.3x 1.5x $1,701 32.1% 11.9%

FURNITURE & HOME DÉCOR RETAIL

The Sherwin-Williams Company United States NYSE:SHW $305.20 97.7% $28,355 $29,772 2.5x 15.3x 1.1x $11,856 50.0% 16.4%

Bed Bath & Beyond Inc. United States NasdaqGS:BBBY 39.74 75.4% 5,974 6,992 0.6x 4.7x 1.0x 12,100 37.6% 12.4%

Williams-Sonoma, Inc. United States NYSE:WSM 47.50 76.6% 4,173 4,222 0.8x 6.3x 0.2x 5,089 36.7% 13.1%

Wayfair Inc. United States NYSE:W 42.31 85.8% 3,619 3,355 1.1x NM NM 3,136 23.8% -4.3%

Aaron's, Inc. United States NYSE:AAN 30.54 89.2% 2,181 2,358 0.7x 5.1x 1.1x 3,234 50.0% 14.3%

La-Z-Boy Incorporated United States NYSE:LZB 28.80 87.5% 1,409 1,299 0.9x 8.5x 0.0x 1,518 39.1% 10.0%

Select Comfort Corporation United States NasdaqGS:SCSS 19.78 69.8% 889 838 0.7x 11.6x 0.0x 1,213 60.5% 5.9%

Ethan Allen Interiors Inc. United States NYSE:ETH 29.00 74.7% 803 786 1.0x 8.1x 0.4x 784 55.9% 12.4%

Pier 1 Imports, Inc. United States NYSE:PIR 7.05 72.9% 585 726 0.4x 6.5x 2.0x 1,842 53.2% 6.0%

Haverty Furniture Companies, Inc. United States NYSE:HVT 22.00 89.6% 466 446 0.5x 6.3x 0.8x 817 53.6% 8.7%

Rent-A-Center, Inc. United States NasdaqGS:RCII 8.01 48.9% 426 1,020 0.3x 4.0x 2.9x 3,073 65.7% 8.2%

Lumber Liquidators Holdings, Inc. United States NYSE:LL 15.57 77.5% 424 435 0.5x NM NM 950 29.2% -8.7%

Conn's, Inc. United States NasdaqGS:CONN 10.20 47.5% 315 1,515 0.9x NM 1,621 18.9% 0.0%

Kirkland's, Inc. United States NasdaqGS:KIRK 13.65 75.0% 217 189 0.3x 4.1x 0.0x 590 46.5% 7.7%

Median $25.40 76.0% $846 $1,160 0.7x 6.3x 0.8x $1,732 48.2% 8.4%

Mean $44.24 76.3% $3,560 $3,854 0.8x 7.3x 0.9x $3,416 44.3% 7.3%

NM

TTM MarginsEnterprise Value / TTM

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

1 0 C O N S U M E R P R O D U C T S & R E T A I L | H O M E E N V I R O N M E N T | I N D U S T R Y M E T R I C S

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

NOTE: Figures in bold and italic type were excluded from median and mean calculation.(1) As of 1/27/2017.(2) Market Capitalization is the aggregate value of a �rm's outstanding common stock.(3) Enterprise Value is the total value of a �rm (including all debt and equity).Source: S&P Capital IQ.

($ in millions, except per share data) Current % of Market Enterprise Total Debt/ TTMCompany Name Country Ticker Stock Price (1) 52W High Capitalization (2) Value (3) Revenue EBITDA EBITDA Revenue Gross EBITDAHOUSEHOLD & FAMILY

HOUSEWARES

Newell Brands Inc. United States NYSE:NWL $46.13 83.2% $22,253 $34,398 3.2x 19.3x 7.2x $10,689 37.0% 16.7%

Tupperware Brands Corporation United States NYSE:TUP 58.00 86.7% 2,933 3,641 1.7x 9.8x 2.2x 2,204 67.8% 16.9%

Helen of Troy Limited United States NasdaqGS:HELE 92.95 87.5% 2,508 3,057 2.0x 14.3x 2.6x 1,546 43.4% 13.9%

Libbey Inc. United States AMEX:LBY 17.42 83.0% 381 757 0.9x 6.5x 3.6x 810 22.9% 14.4%

Lifetime Brands, Inc. United States NasdaqGS:LCUT 15.35 79.3% 222 356 0.6x 9.0x 3.6x 585 36.0% 6.7%

Median $46.13 83.2% $2,508 $3,057 1.7x 9.8x 3.6x $1,546 37.0% 14.4%

Mean $45.97 83.9% $5,659 $8,442 1.7x 11.8x 3.8x $3,167 41.4% 13.7%

JUVENILE

Hasbro, Inc. United States NasdaqGS:HAS $82.59 93.3% $10,306 $11,214 2.3x 11.7x 1.8x $4,855 53.1% 19.4%

Mattel, Inc. United States NasdaqGS:MAT 26.49 76.2% 9,061 10,518 1.9x 12.8x 2.8x 5,457 46.8% 15.1%

Carter's, Inc. United States NYSE:CRI 82.17 73.0% 4,057 4,497 1.4x 9.4x 1.2x 3,132 42.5% 15.2%

The Children's Place, Inc. United States NasdaqGS:PLCE 94.80 85.3% 1,710 1,508 0.9x 8.2x 0.4x 1,763 37.5% 10.4%

Dorel Industries Inc. Canada TSX:DII.B 27.86 89.4% 901 1,380 0.5x 8.4x 3.1x 2,623 23.4% 6.3%

Build-A-Bear Workshop, Inc. United States NYSE:BBW 12.20 77.0% 190 178 0.5x 6.4x 0.0x 372 47.2% 7.5%

JAKKS Pacific, Inc. United States NasdaqGS:JAKK 5.25 53.8% 84 247 0.4x 6.5x 5.7x 703 31.4% 5.1%

Summer Infant, Inc. United States NasdaqCM:SUMR 2.00 82.0% 37 84 0.4x 9.0x 5.2x 200 31.6% 4.7%

Median $27.17 79.5% $1,306 $1,444 0.7x 8.7x 2.3x $2,193 40.0% 8.9%

Mean $41.67 78.7% $3,293 $3,703 1.0x 9.1x 2.5x $2,388 39.2% 10.5%

KITCHEN, BATH & OUTDOOR

Reckitt Benckiser Group plc United Kingdom LSE:RB. $86.09 88.2% $60,273 $62,491 5.5x 18.8x 1.1x $12,081 60.3% 29.1%

Henkel AG & Co. KGaA Germany DB:HEN3 123.59 94.0% 49,231 51,529 2.6x 14.0x 1.5x 20,493 48.5% 18.8%

Kimberly-Clark Corporation United States NYSE:KMB 120.98 87.1% 43,141 50,067 2.8x 12.0x 1.9x 18,202 36.6% 22.2%

The Clorox Company United States NYSE:CLX 120.49 85.8% 15,512 17,511 3.0x 14.4x 2.0x 5,814 44.9% 20.6%

Church & Dwight Co., Inc. United States NYSE:CHD 45.34 84.5% 11,725 12,423 3.6x 14.7x 1.1x 3,471 45.5% 24.0%

The Toro Company United States NYSE:TTC 59.29 99.0% 6,410 6,490 2.7x 15.9x 0.9x 2,392 36.6% 16.7%

Husqvarna AB (publ) Sweden OM:HUSQ B 8.31 97.2% 4,754 5,199 1.3x 11.4x 1.8x 4,188 30.3% 11.3%

Prestige Brands Holdings, Inc. United States NYSE:PBH 52.13 89.7% 2,759 4,209 5.1x 14.2x 5.0x 833 57.9% 35.6%

WD-40 Company United States NasdaqGS:WDFC 104.65 83.7% 1,477 1,511 4.0x 19.6x 1.7x 377 56.7% 20.4%

Median $86.09 88.2% $11,725 $12,423 3.0x 14.4x 1.7x $4,188 45.5% 20.6%

Mean $80.10 89.9% $21,698 $23,492 3.4x 15.0x 1.9x $7,539 46.4% 22.1%

TTM MarginsEnterprise Value / TTM

INDUSTRY METRICS

PUBLIC COMPANY OPERATING METRICS

1 1

1 1 C O N S U M E R P R O D U C T S & R E T A I L | A U T O M O T I V E A F T E R M A R K E T

AUTOMOTIVE AFTERMARKET

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

CONSOLIDATION

The U.S. automotive aftermarket, sized at $257.4 billion in 2015, is forecasted to grow 3.7 percent annually through 2019 to $296.3 billion, representing an increase of nearly $39 billion, according to the 2016 Joint Channel Forecast Model produced by the Automotive Aftermarket Suppliers Association (AASA) and the Auto Care Association. “Despite strong new vehicle sales, moderating gas prices and improved miles driven are conditions conducive to continued steady growth,” said Bill Hanvey, CEO of the Auto Care Association, in a release from Auto Care News. “Why? The average age of light vehicles, now up to 11.6 years is the oldest ever, and the age mix of vehicles continues to favor older vehicles, creating a robust sweet spot for service and repair.” “The automotive aftermarket is a large and stable industry whose impressive growth, even through the Great Recession, is forecasted to continue,” said Bill Long, president and chief operating officer, AASA.

M&A activity is rising against a backdrop of steady demand and volume growth, with consolidation continuing across the value chain as industry participants seek scale, technology, premiumization, and channel diversification.

1 2 C O N S U M E R P R O D U C T S & R E T A I L | A U T O M O T I V E A F T E R M A R K E T

2016 saw a number of transaction announcements involving corporate acquirers:

Polaris Industries (NYSE:PII) solidified its market entry with the largest acquisition in its history, picking up Transamerican Auto Parts Company in November, a defensive diversification play the company is betting will produce synergies with its off-road vehicle business.

Icahn Enterprises (NasdaqGS:IEP) paid $1.27 billion for Pep Boys in February, a vertical integration play for automotive aftermarket platform Auto Plus, acquired in December 2015.

O’Reilly Automotive (NasdaqGS:ORLY), Genuine Parts Company (NYSE:GPC), and AutoPlus each announced acquisitions during the last 12 months.

Private equity has shown increasing interest—drawn to the sector’s size and fragmentation, enthusiast consumer base, and recession resistance—with sponsors aggressively pursuing platforms and accretive acquisitions for existing investments.

Notable recent private equity investment activity:

Goldman Sachs Merchant Banking acquired K&N Engineering from Gryphon Investors in October 2016.

Huron Capital Partners acquired Drake Automotive Group in January 2016 and followed with the add-on acquisition of Fender Gripper in November of the same year. The sponsor is executing on its stated strategy to grow Drake through acquisitions of additional products and licenses.

TA Associates’ platform Truck Hero acquired Husky Liners in October 2016. The deal is Truck Hero’s tenth acquisition since its founding in 2007.

The Sterling Group formed Highline Aftermarket with the acquisitions of DYK Automotive (February 2016) and Automotive Aftermarket Holdings Corporation (April 2016).

J.W. Childs is building out its motorcycle enthusiast platform with RevZilla Motorsports, acquired in March 2016, complementing foundational asset Cycle Gear, which it acquired in January 2015.

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , C o m p a n y F i l i n g s , E q u i t y R e s e a r c h , p u b l i c d a t a .

CASE STUDYGoldman Sachs Merchant Banking is tapping the auto aftermarket with the October 2016 acquisition of K&N Engineering, a California-based manufacturer of premium performance air and oil filtration products. Gryphon Investors exited its five-year investment in the sale.

K&N has been a trusted brand among auto enthusiasts for more than 50 years. The company is regarded as a brand leader in the performance filter market and offers an extensive line of air filters, air intakes, oil filters, cabin air filters, exhausts, and accessories.

K&N has demonstrated a track record of profitable growth, increasing its penetration in growing eCommerce and DIFM channels and building a growing DTC business. The company has expanded internationally and operates offices in the U.S., the U.K., and the Netherlands.

K&N completed a number of strategic acquisitions, including AEM Air Filters in 2009, and under Gryphon’s ownership, Spectre Performance in 2013 and AIRAID in 2015.

K&N reported revenue of approximately $194 million for the twelve months ended June 2016.

1 3 C O N S U M E R P R O D U C T S & R E T A I L | A U T O M O T I V E A F T E R M A R K E T | C A S E S T U D Y

Enterprise Value: $610 million

Enterprise Value/Revenue: 3.1xEnterprise Value/EBITDA: 10.5x

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , C o m p a n y F i l i n g s , E q u i t y R e s e a r c h , p u b l i c d a t a .

M&

A T

RA

NS

AC

TIO

NS

R AT I O N A L EDAT E TA R G E T B U Y E R D E A L S TAT S

Enterprise Value (EV): $340M

Enterprise Value (EV): $1.27BEV/Revenue: .60xEV/EBITDA: 15.6x

1 4 C O N S U M E R P R O D U C T S & R E T A I L | A U T O M O T I V E A F T E R M A R K E T | I N D U S T R Y M E T R I C S

S o u r c e s : S & P C a p i t a l I Q , P i t c h B o o k , E q u i t y R e s e a r c h , p u b l i c d a t a .

Fe b - 1 6Acquisition adds East Coast full line distributor of import auto parts, expanding footprint with six locations serving the northern Virginia-Washington DC area.

R AT I O N A L EDAT E TA R G E T B U Y E R D E A L S TAT S

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

Acquisition establishes entry into the North American aftermarket parts space with addition of vertically integrated manufacturer and retailer of Jeep and truck accessories.

N o v - 1 6Enterprise Value (EV): $665MEV/Revenue: .89xEV/EBITDA: 9.0x

Acquisition expands footprint in Pittsburgh with five locations. A u g - 1 6

Acquisition of eCommerce retailer of premium apparel, accessories, and parts extends Cycle Gear platform focused on serving motorcycle enthusiasts.

M a r - 1 6

Acquisition advances vertical integration strategy with synergistic opportunities for automotive aftermarket company Auto Plus.

Enterprise Value (EV): $1.27BEV/Revenue: .60xEV/EBITDA: 15.6x

Fe b - 1 6

Acquisition of eCommerce retailer for BMW performance parts and accessories establishes ECS as premier destination for BMW parts online.

J u l - 1 5

Enterprise Value (EV): $340MD e c - 1 5

Acquisition of automotive aftermarket parts distributor operating more than 240 stores and over 22 distribution centers across the United States. Company is pursuing an acquisition growth strategy buying East End Auto Parts in 2015 and in 2016, Industrial Engine & Supply and Greene’s Auto Parts.

D e c - 1 5 Acquisition establishes entry into the direct-to-installer automotive parts market in the United States.

Huron Capital is executing on its stated strategy to grow Drake through acquisitions of additional products and licenses, adding branded protective fender covers, trunk mats, and carpet underlayments for the classic car, off-road, and late-model muscle car markets.

N o v - 1 6

Acquisition expands offering with addition of branded custom-fit floor and cargo liners marketed under Extang, TruXedo, BedRug, UnderCover, Advantage, Retrax, BAK, A.R.E., N-FAB. The deal is Truck Hero’s 10th acquisition since its founding in 2007.

O c t - 1 6

Acquisition establishes platform in automotive aftermarket.J a n - 1 6

A u g - 1 5 Acquisition expands retail footprint with three locations in Pennsylvania. Lebzelters is the world’s oldest Goodyear dealer.

Fe b - 1 6 Acquisition establishes platform in automotive aftermarket. Enterprise Value (EV): $137M

J a n - 1 7 Acquisition adds 22 locations, expanding APH’s footprint to 121 corporate stores. APH enters Montana and South Dakota.

Acquisition broadens automotive aftermarket platform. Sterling renamed the company Highline Aftermarket.

Auto AftermarketHoldings Corporation A p r - 1 6

O c t - 1 6 Acquisition establishes platform in automotive aftermarket. Enterprise Value (EV): $610MEV/Revenue: 3.1xEV/EBITDA: 10.5x

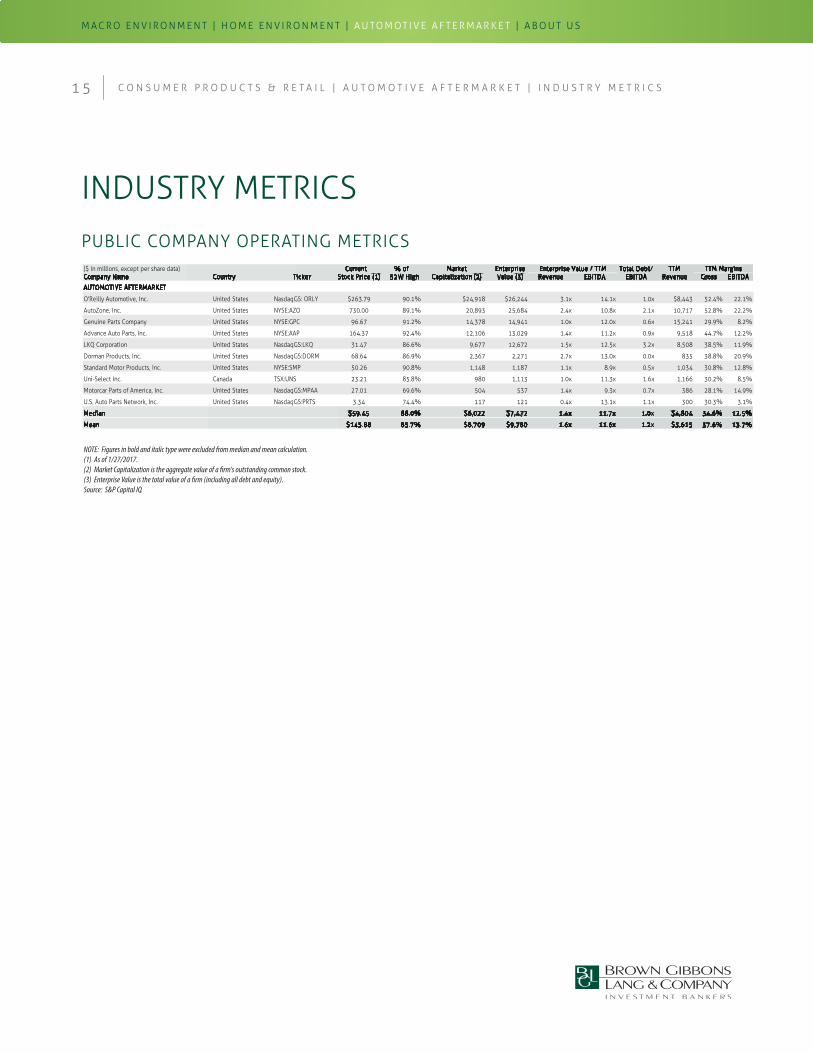

INDUSTRY METRICS

1 5 C O N S U M E R P R O D U C T S & R E T A I L | A U T O M O T I V E A F T E R M A R K E T | I N D U S T R Y M E T R I C S

PUBLIC COMPANY OPERATING METRICS

NOTE: Figures in bold and italic type were excluded from median and mean calculation.(1) As of 1/27/2017.(2) Market Capitalization is the aggregate value of a �rm's outstanding common stock.(3) Enterprise Value is the total value of a �rm (including all debt and equity).Source: S&P Capital IQ.

($ in millions, except per share data) Current % of Market Enterprise Total Debt/ TTMCompany Name Country Ticker Stock Price (1) 52W High Capitalization (2) Value (3) Revenue EBITDA EBITDA Revenue Gross EBITDA

AUTOMOTIVE AFTERMARKET

O'Reilly Automotive, Inc. United States NasdaqGS: ORLY $263.79 90.1% $24,918 $26,244 3.1x 14.1x 1.0x $8,443 52.4% 22.1%

AutoZone, Inc. United States NYSE:AZO 730.00 89.1% 20,893 25,684 2.4x 10.8x 2.1x 10,717 52.8% 22.2%

Genuine Parts Company United States NYSE:GPC 96.67 91.2% 14,378 14,941 1.0x 12.0x 0.6x 15,241 29.9% 8.2%

Advance Auto Parts, Inc. United States NYSE:AAP 164.37 92.4% 12,106 13,029 1.4x 11.2x 0.9x 9,518 44.7% 12.2%

LKQ Corporation United States NasdaqGS:LKQ 31.47 86.6% 9,677 12,672 1.5x 12.5x 3.2x 8,508 38.5% 11.9%

Dorman Products, Inc. United States NasdaqGS:DORM 68.64 86.9% 2,367 2,271 2.7x 13.0x 0.0x 835 38.8% 20.9%

Standard Motor Products, Inc. United States NYSE:SMP 50.26 90.8% 1,148 1,187 1.1x 8.9x 0.5x 1,034 30.8% 12.8%

Uni-Select Inc. Canada TSX:UNS 23.21 85.8% 980 1,113 1.0x 11.3x 1.6x 1,166 30.2% 8.5%

Motorcar Parts of America, Inc. United States NasdaqGS:MPAA 27.01 69.6% 504 537 1.4x 9.3x 0.7x 386 28.1% 14.9%

U.S. Auto Parts Network, Inc. United States NasdaqGS:PRTS 3.34 74.4% 117 121 0.4x 13.1x 1.1x 300 30.3% 3.1%

Median $59.45 88.0% $6,022 $7,472 1.4x 11.7x 1.0x $4,804 34.6% 12.5%

Mean $145.88 85.7% $8,709 $9,780 1.6x 11.6x 1.2x $5,615 37.6% 13.7%

TTM MarginsEnterprise Value / TTM

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

GLOBAL CONSUMER PRODUCTS & RETAIL

1 6 C O N S U M E R P R O D U C T S & R E T A I L | A B O U T U S

FOCUS AREAS

• Furniture & Home Décor

• Decorative Lighting

• Kitchen & Bath

• Outdoor

• Fitness & Functional

• Performance

• Distribution & Logistics

• Youth / Juvenile

• Food & Treats

• Accessories

• Supplies & Consumables

• Supplements

WHO WE ARE

• Outdoor

• Recreation

• Sporting Goods

• Fitness & Functional

• Independent investment banking advisory firm focused on the middle market since 1989

• Senior bankers with significant experience and tenure; partners average over 20 years of experience

• Offices in Chicago, Cleveland, and Philadelphia

• Founding member and U.S. partner of Global M&A Partners, Ltd., the world’s leading partnership of investment banking firms focusing on middle market transactions

• Deep industry experience across core sectors of focus, including: Business Services, Consumer, Environmental & Industrial Services, Healthcare & Life Sciences, Industrials, and Real Estate

Sell-Side Advisory

Acquisitions & Divestitures

Public & Private Mergers

Special Committee Advice

Strategic Partnerships & Joint Ventures

Fairness Opinions & Fair Value Opinions

All Tranches of

Debt & Equity Capital for:

Growth

Acquisitions

Recapitalizations

Dividends

General Financial & Strategic Advice

Balance Sheet

Restructurings

Sales of Non-Core Assets or Businesses

§363 Auctions

OUTDOOR & ACTIVE LIFESTYLE APPAREL PET

HOMEENVIRONMENT

The information contained in this publication was derived from proprietary research conducted by a division or owned or affiliated entity of Brown Gibbons Lang & Company LLC. Any projections, estimates or other forward-looking statements contained in this publication involve numerous and significant subjective assumptions and are subject to risks, contingencies, and uncertainties that are outside of our control, which could and likely will cause actual results to differ materially. We do not expect to, and assume no obligation to update or otherwise revise this publication or any information contained herein. Neither Brown Gibbons Lang & Company LLC, nor any of its officers, directors, employees, affiliates, agents or representatives makes any representation or warranty, expressed or implied, as to the accuracy, completeness or fitness of any information contained in this publication, and no legal liability is assumed or is to be implied against any of the aforementioned with respect thereto. This publication does not constitute the giving of investment advice, nor a part of any advice on investment decisions and nothing in this publication is intended to be a recommendation of a specific security or company, nor is any of the information contained herein intended to constitute an analysis of any company or security reasonably sufficient to form the basis for any investment decision. Brown Gibbons Lang & Company LLC, its affiliates and their officers, directors, employees or affiliates, or members of their families, may have a beneficial interest in the securities of a specific company mentioned in this publication and may purchase or sell such securities in the open market or otherwise. Nothing contained in this publication constitutes an offer to buy or sell or the solicitation of an offer to buy or sell any security.

LEADING INDEPENDENT FIRM COMPREHENSIVE CAPABILITIES

M&A ADVISORY PRIVATE PLACEMENTS

FINANCIAL ADVISORY

For questions about content and circulation, please contact editor, Rebecca Dickenscheidt, at [email protected] or 312-513-7476.

Primary Research

Industry Benchmarking

Operating Advisor Network

White Papers

Industry Surveys

RESEARCH

E C O M M E R C E / DTC F O C U S

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

GLOBAL CONSUMER PRODUCTS & RETAIL

1 7 C O N S U M E R P R O D U C T S & R E T A I L | A B O U T U S

DEDICATED LEADERSHIP

CONTACTS

• Leads BGL’s Consumer Products & Retail practice

• Over 25 years of investment banking and corporate finance experience

• Former Managing Director at Banc One Capital Markets (JP Morgan Chase)

• Former Managing Director at First Chicago Capital Markets, founding the Detroit office for the firm in 1996

• Began investment banking career in 1990 with American National Bank & Trust Company, a subsidiary of First National Bank of Chicago

• Serves on the National Board of Directors for the Gift of Adoption Fund

• Over 13 years of M&A and corporate finance experience

• Former senior banker within the Consumer and Retail group at KeyBanc Capital Markets

• M&A and corporate finance attorney for Wilmer Cutler Pickering Hale and Dorr LLP and Calfee, Halter & Griswold LLP

• B.S., University of Illinois

• M.B.A., Northwestern University Kellogg School of Management

• Eagle Scout

• B.A., Colgate University

• J.D., Boston College Law School

J O H N T I L S O NM a n a g i n g D i r e c t o r

G r o u p H e a d

A L E X T E E T E RD i r e c t o r

PROFESSIONAL EXPERIENCEPROFESSIONAL EXPERIENCE

EDUCATIONEDUCATION

PROFESSIONAL EXPERIENCE

M AC R O E N V I R O N M E N T | H O M E E N V I R O N M E N T | A U TO M OT I V E A F T E R M A R K E T | A B O U T U S

• Backcountry Camping, Hunting, Fly Fishing, Golf

• Lives in Winnetka, Illinois with his wife, three children, dog, and two cats

OUTSIDE INTERESTS

• Triathalons, Skiing, Backcountry Hiking/Camping, Scuba Diving

• Lives in Shaker Heights, Ohio with his wife, two children, and dog

EDUCATIONEDUCATION

OUTSIDE INTERESTS

B O B K E N TM a n a g i n g D i r e c t o r

F i n a n c i a l S p o n s o r C o v e r a g e

• Over 20 years of M&A and corporate finance experience

• Former Managing Director in the Financial Sponsors Group at Stifel Investment Banking

• Investment banking positions at Banc of America Securities in San Francisco and Charlotte and at Brown Brothers Harriman in New York

• A.B., Princeton University

• Diploma in Accounting and Finance from the London School of Economics

• M.B.A., Darden School of Business at the University of Virginia

• Chartered Financial Analyst

PROFESSIONAL EXPERIENCE

• Travel, NFL Football, Guitar, Coaching, Squash

• Lives in Bryn Mawr, Pennsylvania with his wife, son, and goldfish

EDUCATIONEDUCATION

OUTSIDE INTERESTS

One Magnif icent Mile 980 N. Michigan Avenue Suite 1880 Chicago, IL 60611p. 312.658.1600

One Cleveland Center1375 East 9th StreetSuite 2500 Cleveland, OH 44114p. 216.241.2800

C H I C A G O C L E V E L A N D

One Liberty Place 1650 Market StreetSuite 3600 Philadelphia , PA 19103p. 610.941.2765

P H I L A D E L P H I A

![Download [1.95 MB]](https://img.dokumen.tips/doc/110x75/5866d9ef1a28ab31408b908c/download-195-mb.jpg)