Embed Size (px)

Citation preview

Innovative Partnerships in Financial Inclusion - Banking on Change

14 August 2013

How BANKING On Change fits within Barclays Business Strategy

Mark Thain – Barclays UK

‘Go-To’ Bank

Respect Integrity Service Excellence Stewardship

Becoming the ‘Go-To’ Bank

Citizenship

The way we do business

Contributing to growth

Supporting ourcommunities

Purpose

Helping people achieve their ambitions – in the right way

Values

Supporting our communities

Barclays ApproachBarclays is committed to invest resources, time and expertise in community programmes that enhance the employability, enterprise and financial literacy skills of the next generation.

By closely aligning our community investment programmes with our skills and expertise as a bank, we can have most impact in society

We partner with respected NGOs, charities, businesses and our own customers and clients.

Barclays is helping 5 million disadvantaged young people,

by 2015, develop the skills they need to fulfill their potential.

OUR PARTNERSHIP MODEL

Michael Kaddu – Barclays Uganda

Financial InclusionWhat is the situation?

Today, more than 2.5 billion people globally are considered financially excluded with no access to basic financial services, such as savings, bank accounts, or credit.

Access to even the most basic financial services can help households increase their assets, better manage their incomes for investment in their own smallbusiness, improve their access to education and health services, and protect themselves from any number of possible shocks and hazards, such as illness or a failed harvest.

Focusing on young people the situation globally is even more prevalent:

• 1.2 billion people are aged 15 to 24, but only 4.2million young people have access to financial services

• Unemployment rates for young people are 2-3 times higher than adults

• 28% of young workers are paid less than $1.25 a day

Click icon to add picture

Banking on Change: A collaborative Partnership

Shared Goals

• Improve quality of life for poor people through increasing access to financial services

• Focus on a savings-led approach to microfinance as the basis for financial inclusion

• Harness skills and expertise of all three partners to deliver shared value for business and society

Get to know the lead persons

Partners and Bank develop work plan through joint VSLA visits

Joint training, linkage material, product knowledge shared, Bank account application support

Monitoring of group accounts, support to apply for credit/OD facility, ongoing support to evaluate product support

Working with the Partners

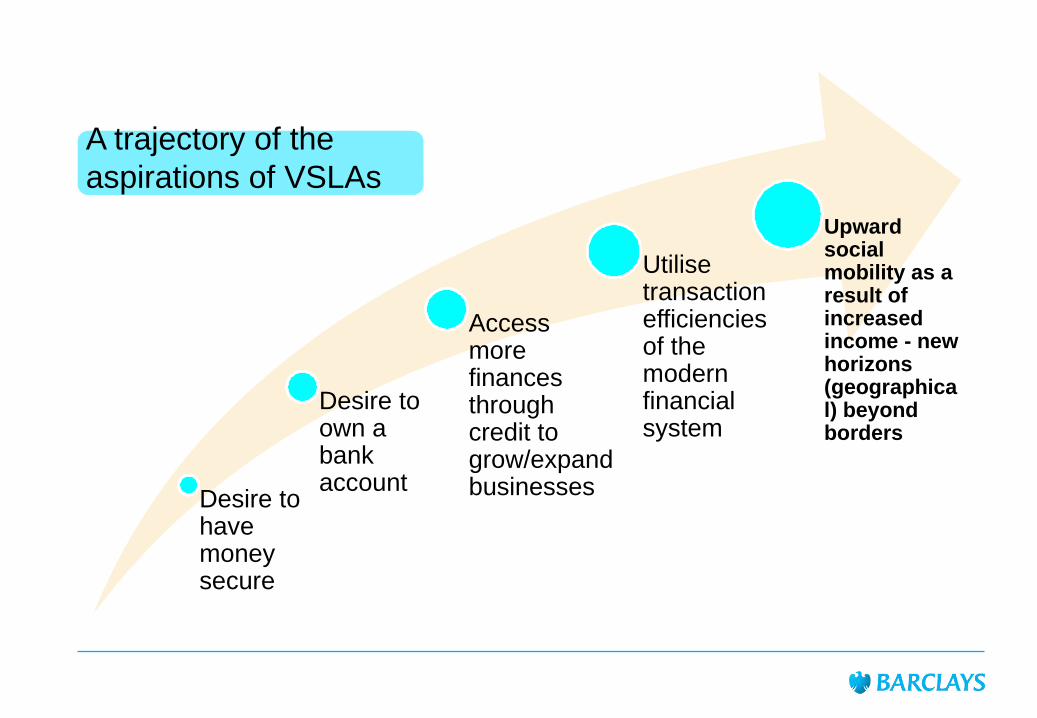

Desire to have money secure

Desire to own a bank account

Access more finances through credit to grow/expand businesses

Utilise transaction efficiencies of the modern financial system

Upward social mobility as a result of increased income - new horizons (geographical) beyond borders

A trajectory of the aspirations of VSLAs

• Getting closer to the customer

• Developing linkage partnerships

• Sustainable approaches• Methodology safeguards

Product Research

• Engaging development product specialists

• Compliance aspects• Training the branch

network in consultation with community partners

Product Development • Monitoring and Evaluation

• Working with the savings groups to refine what is on offer in line with their evolving needs

• Developing the next value add

Product enhancement

A framework for linkage to financial institutions

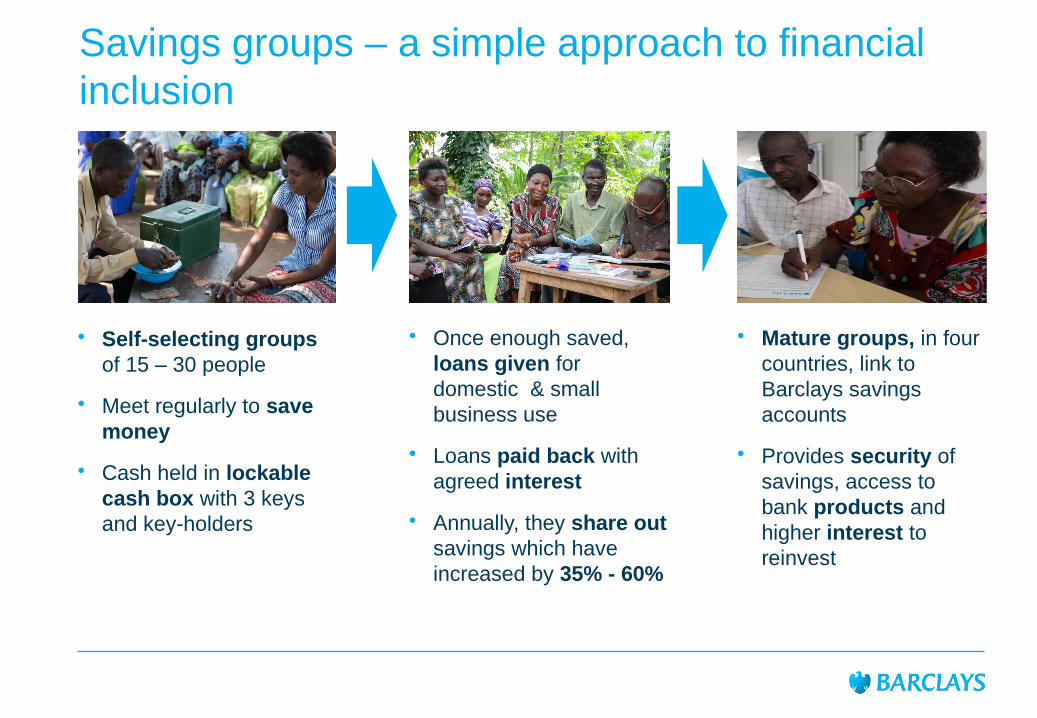

Savings groups – a simple approach to financial inclusion

Self-selecting groups of 15 – 30 people

Meet regularly to save money

Cash held in lockable cash box with 3 keys and key-holders

Once enough saved, loans given for domestic & small business use

Loans paid back with agreed interest

Annually, they share out savings which have increased by 35% - 60%

Mature groups, in four countries, link to Barclays savings accounts

Provides security of savings, access to bank products and higher interest to reinvest

Scalability and SustainabilityBanking on Change has developed financial products and services that meet the needs of savings groups in Uganda, Tanzania, Ghana and Kenya, and in doing so we are the first partnership between a global commercial bank and international NGOs to successfully link informal savings groups to the formal banking sector

Developing suitable products that meet the needs of poorer communities positively impacts on society but also makes good business sense

Savings groups save more when their savings are secure in a formal bank account

Higher and predictable deposits have great potential for scalability, supported by the 95% repayment rate

Banking on Change aims to see this model replicated by others, adhering to the linkage principles

In the long-term, this helps breaks the barriers to financial inclusion in a sustainable way

Click icon to add picture

Enablers: Digitizing DataA simple data collection tool on the secretary’s phone capturing key group or individual data points that enables a series of new offers for VSLAs. Barclays can then use the data to have greater insight into group and/or individual performance, which can enable:

Access toInformation

Developing a VSLA credit scoring mechanism

Tracking group performance

Identifying individuals who might be interested in banking with Barclays

Enablers: e-KeysVSLAs use a three-PIN system to access mobile money wallets linked to the bank, enabling groups to deposit and withdraw at agent locations

How Banking on Change supports Financial Inclusion now and in the future

Stella Tungaraza(Plan Tanzania)

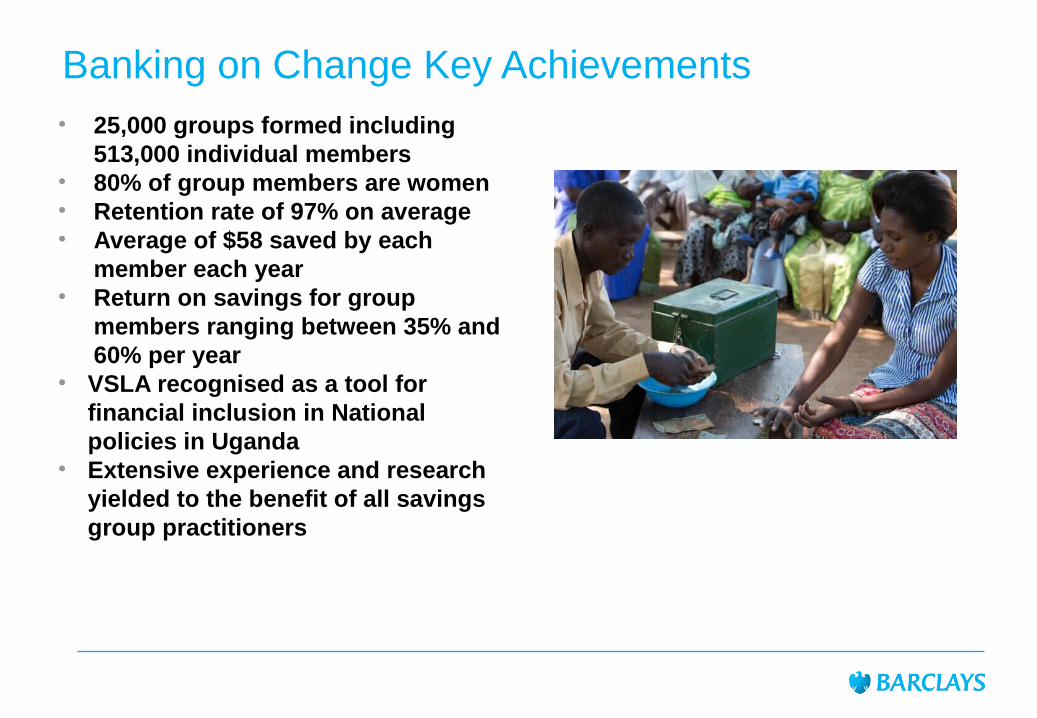

Banking on Change Key Achievements• 25,000 groups formed including

513,000 individual members • 80% of group members are women• Retention rate of 97% on average• Average of $58 saved by each

member each year• Return on savings for group

members ranging between 35% and 60% per year

• VSLA recognised as a tool for financial inclusion in National policies in Uganda

• Extensive experience and research yielded to the benefit of all savings group practitioners

Global Impact after three years

“The greatest impact of Banking on Change may have been an educational one– due to the programme over half a million people have increased their financial literacy”*

In Ghana, 60.4% of VSLA members have invested inproductive assets at the end of the project while they were only 45.3% at the beginning

In Peru, female group members increased their investment in small businesses by 47 per cent in three years

In Tanzania women who arestrongly denying that decision making in the household can be done by both men and Women decreased from18.3% to 9.9%

In Egypt while 12.5% of members were engaged in income generating activities at the beginning, there were 23.4% at the end

“Increase in education expenses: 63.9% to 67.5%Decrease in failure to access health due to lack of funds:17.5% to 14.5% This is impressive as such impact are only usually measurable after 5-8 years”*

Impact

*Final Evaluation of the Banking on Change Programme, Triodos Facet, February 2013

In Uganda, VSLA members’ monthly household income rose from $60 to $95

Global impact of Banking on Change

WHAT NEXT?

Building on phase 1, the three partners will continue working together

• For the next 3 years

• In 7 countries

• With a investment of £10 million

Increase focus on financial inclusion of young people

Target: 75% beneficiaries under 35; 10k youth groups

• Deepen enterprise training

Target: 41k small businesses; 7 countries

• Scale-up informal to formal bank links

Target: 5k groups linked; 800 Barclays colleagues engaged

Banking on Change Charter• Banking on Change aims to be a global leader in responsibly linking poor savers to

formal financial institutions and we want to share our model to encourage others to adopt it too.

• 2.5 billion people would benefit from access to financial services, to achieve this we need others to be involved

• We are building an alliance of individuals and institutions who can influence, facilitate or implement responsible linking poor people to formal financial institutions.

• We are creating a Banking on Change Charter which will include the principles for responsible linkage developed by CARE

• People can sign up to the charter either as supporters – endorsing the charter and showing their support to bank the unbanked, or as Members – agreeing to facilitate linkage (such as through scale, financial literacy, product development, policy development/implementation)

• We aim to get 100 signatures including from Banks, Microfinance practitioners, NGO’s, related private sector actors, government, and influential individuals

• The Charter will be launched later this year, and presented at various global conferences including the World Economic Forum Africa in 2014, and in Davos 2015

• If you are interested to find out more please ask Alice Allan - [email protected]

Conclusion…

From informal banking to formal banking:

Click icon to add pictureClick icon to add picture

…any questions