Embed Size (px)

Citation preview

Journal of Data Science 3(2005), 153-177

Influence Diagnostics for Linear Mixed Models

Temesgen Zewotir1 and Jacky S. Galpin2

1University of KwaZulu-Natal and2University of the Witwatersrand

Abstract: Linear mixed models are extremely sensitive to outlying responsesand extreme points in the fixed and random effect design spaces. Few diag-nostics are available in standard computing packages. We provide routinediagnostic tools, which are computationally inexpensive. The diagnosticsare functions of basic building blocks: studentized residuals, error contrastmatrix, and the inverse of the response variable covariance matrix. The ba-sic building blocks are computed only once from the complete data analysisand provide information on the influence of the data on different aspectsof the model fit. Numerical examples provide analysts with the completepictures of the diagnostics.

Key words: Case deletion, influential observations, random effects, statisticaldiagnostics, variance components ratios.

1. Introduction

The linear mixed model provides flexibility in fitting models with variouscombinations of fixed and random effects, and is often used to analyze data in abroad spectrum of areas. It is well known that not all observations in a data setplay an equal role in determining estimates, tests and other statistics. Sometimesthe character of estimates in the model may be determined by only a few caseswhile most of the data are essentially ignored. It is important that the dataanalyst be aware of particular observations that have an unusually large influenceon the results of the analysis. Such cases may be assessed as being appropriateand retained in the analysis, may represent inappropriate data and be eliminatedfrom the analysis, may suggest that additional data need to be collected, maysuggest the current modeling scheme is inadequate, or may indicate a data readingor data entry error. Regardless of the ultimate assessment of such cases, theiridentification is necessary before intelligent subject-matter-based decisions canbe drawn.

In ordinary linear models such model diagnostics are generally available instatistical packages and standard textbooks on applied regression, see for ex-ample, Cook and Weisberg (1982), Chatterjee and Hadi (1986, 1988). Oman

154 T. Zewotir and J. S. Galpin

(1995) notes that, for the mixed model, standard statistical packages generallyconcentrate on estimation of and testing hypotheses about various parametersand submodels without providing overall diagnostics of the model. There havebeen a limited number of studies in linear mixed model diagnostics. Fellner(1986) examined robust estimates of the variance components, focusing on find-ing outlier resistant estimates of the mixed model parameters by limiting theinfluence of the outliers on the estimates of the model parameters. Beckman,Nachtsheim and Cook (1987) applied the local influence method of Cook (1986)to the analysis of the linear mixed model. Although an assessment of the influenceof a model perturbation is generally considered to be useful, as Lawrance (1990)remarked, a practical and well established approach to influence analysis in sta-tistical modeling is based on case deletion. Christensen, Pearson and Johnson(1992) (hereafter CPJ) studied case deletion diagnostics, in particular the analogof Cook’s distance, for diagnosing influential observations when estimating thefixed effect parameters and variance components.

Some work has been done for special cases of the mixed model. In particularMartin (1992), Haslett and Hayes (1998) and Haslett (1999) considered the fixedeffect linear model with correlated covariance structure and Christensen, Johnsonand Pearson (1992, 1993) considered spatial linear models. But the approachesof Martin (1992), Haslett and Hayes (1998) and Haslett (1999) cannot be directlyapplied to a mixed model unless the entire focus of analysis is on the fixed effectsestimate. Similarly the spatial linear model where covariance matrix of the dataare determined by the locations at which observations are taken cannot be directlyapplied to the linear mixed model. We are also mindful that for fixed effect linearmodels with correlated error structure Haslett (1999) showed that the effects onthe fixed effects estimate of deleting each observation in turn could be cheaplycomputed from the fixed effects model predicted residuals. However, when theinterest of analysis is on the linear mixed model parameters (fixed effects andvariance components) and predictors and likelihood functions this is not sufficient.

The key to making deletion diagnostics useable is the development of efficientcomputational formulas, allowing one to obtain the case deletion diagnostics bymaking use of basic building blocks, computed only once for the full model. Thegoal of this paper is to supplement the work of CPJ with such information andextend the ordinary linear regression influence diagnostics approach to linearmixed models. A number of diagnostics are proposed, which are analogues of theCook’s distance (Cook, 1977), likelihood distance (Cook and Weisberg, 1982),the variance (information) ratio (Belsley, Kuh, and Welsch, 1980), the Cook-Weisberg statistic (Cook and Weisberg, 1980) and the Andrews-Pregibon statistic(Andrews and Pregibon, 1978). The diagnostics are applied to two examples.

Influence Diagnostics for Linear Mixed Models 155

2. Model Definition and Estimation

The general form of the linear mixed model is

y = Xβ + Zu + ε

where β is a p × 1 vector of unknown constants, the fixed effects of the model;X is an n × p known design matrix of fixed numbers associated with β; Z =[Z1|Z2| . . . , |Zr] , where Zi is an n× qi known design matrix of the random effectfactor i; u′ = [u′

1|u′2| . . . , |u′

r]], where ui is a qi × 1 vector of random variablesfrom N(0, σ2

i I), i = 1, 2, . . . , r; ε is an n× 1 vector of error terms from N(0, σ2eI);

and ui and ε are mutually independent. One may also write u ∼ N(0, σ2eD),

where D is block diagonal with the i-th block being γiIqi , for γi = σ2i /σ

2e , so that

y has a multivariate normal distribution with E(y) = Xβ and var(y) = σ2eH,

for H = I +∑r

i=1 γiZiZ′i .

No consensus exists on the best way to estimate the parameters (see, e.g.,Harville, 1977; Robinson, 1991 and Searle, Casella and McCulloch, 1992). Stan-dard methods for the linear mixed models are maximum likelihood, restrictedmaximum likelihood (REML) and minimum norm quadratic unbiased estimation(MINQUE). The discussion in this article focuses on maximum likelihood, butthe results can also be easily applied to REML and MINQUE.

If the γi’s (and hence H) are known, the maximum likelihood estimates ofβ, σ2

e and the realized value of u are given by β = W (X,X)−1W (X,y), σ2e =

W (d,d)/n, u = DZ′H−1(y − Xβ) = DW(Z,d) for d = y − Xβ, and whereW (A,B) = A′H−1B, in the notation of theW -operator of Hemmerle and Hartley(1973). Here β is the best linear unbiased estimator (BLUE) of β and u is the bestlinear unbiased predictor (BLUP) of u. If the γi’s are unknown, the maximumlikelihood estimates are substituted back into D (and/or H) to obtain β, σ2

e andu (see, e.g., Harville, 1977; Searle et al., 1992, SAS Institute, 1992 and McCullochand Searle, 2001).

Conventional optimization methods, which require first and second order par-tial derivatives, may be applied to obtain the maximum likelihood estimate ofγ′ = [γ1, . . . , γr]. The theoretical advantage of the Newton Raphson (NR) pro-cedure (quadratic convergence rate in the neighborhood of the solution) and thepractical advantage of the Fisher scoring procedure (robustness toward poor start-ing values) lead to the development of a hybrid NR and Fisher scoring algorithm(Jennrich and Sampson, 1976 and SAS Institute, 1992), used in this study.

Using minimum variance quadratic unbiased estimators with zero variancecomponents commonly called MIVQUE0 (Goodnight, 1978) as initial estimates ofthe variance components, the NR iterative procedure, γ(t+1) = γ(t)−(F(t))−1g(t),while for the Fisher scoring algorithm, γ(t+1) = γ(t) − (E(F(t)))−1g(t), where, g(t)

156 T. Zewotir and J. S. Galpin

and F(t) are the gradient (first derivative of the log-likelihood) and the Hessian(second derivative of the log -ikelihood) evaluated at γ(t), respectively. The t-thelement of the gradient vector g is

−12trace(W (Zi,Zi)) +

12σ2

e

W (d,Zi)W (Zi,d).

The (i, j)-th, i, j = 1, 2, . . . r, element of F is

12trace(W (Zi,Zj))W (Zj ,Zi)) − 1

σ2e

W (d,Zi)W (Zi,Zj)W (Zj ,d),

implying that the expected value of the (i, j)-th element of F is

−12trace(W (Zi,Zj)W (Zj,Zi)).

The fitted values of the response variable y are y = Xβ + Zu, giving theresiduals e = y − y. The symmetric matrix R = H−1−H−1XW (X,X)−1X′H−1

transforms the observations into residuals. That is, e = Ry, and if the γi’s (andhence H) are known e ∼ N(0, σ2

eR) and correlation between ei and ej is en-tirely determined by the elements of R, corr(ei, ej) = rij/

√riirjj. If the γi’s are

unknown and their estimates are used these results are useful only as an approx-imation. In fact such approximation is common in mixed model inference. Forinstance inference about β and u use similar approximation in the SAS proce-dure, PROC MIXED (Little, et al., 1996 and Verbeke and Molenberghs, 1997).The i-th Studentized residual is defined as ti = ei/(σe

√rii).

3. Background, Notation and Update Formulae

Without loss of generality, we partition the matrices as if the i-th omittedobservation is the first row; i.e., i = 1. Then

X =[

x′i

X(i)

], Zj =

[z′ji

Zj(i)

], Z =

[z′i

Z(i)

], y =

[yi

y(i)

],

and H =[hii h′

i

hi H[i]

].

For notational simplicity, A(i) denotes an n × m matrix A with the i-th rowremoved, ai denotes the i-th row of A, and aij denotes the (i, j)-th element of A.Similarly, a(i) denotes a vector a with the i-th element removed, and ai denotesthe i-th element of a. Moreover, using a similar notation to CPJ, we define

ai = ai − A(i)H[i]hi pii = x′iW (X,X)−1xi

Influence Diagnostics for Linear Mixed Models 157

mi = hii − h′H[i]hi, and W[i](A,B) = A′(i)H

−1[i] B(i).

Further, let β(i), σ2e(i), u(i) and γ(i) denote the estimates of β, σ2

e , u and γwhen the i-th observation is deleted, respectively.

Theorem 1: For fixed (or known) variance components ratios,

W[i](A,B) = W (A,B) − aib′i/mi.

The proof is given in the Appendix. The updating formulae for β, σ2e and u

then become

β(i) = β − 1mi − pii

W (X,X)−1x′i(yi − x′

iβ),

σe(i) =1

n− 1{nσ2

e − 1mi − pii

(yi − x′iβ)2} and

u(i) = u −D{zi −W (Z,X)−1xi} yi − x′iβ

(mi − pii)

Because of the iterative nature of estimation a simple analytical expressionfor the change in the variance components ratios when a case is deleted cannotbe obtained. However, we can derive analytic expressions for the change in γif we use γ as a starting value and perform a one step iteration with the i-thobservation omitted. In general, such one step diagnostics adequately estimatethe fully iterated change in the parameter with the i-th observation deleted, formodels with non linear parameters, see Pregibon (1981), who pioneered the idea.

Cox and Hinkley (1974, page 308) noted that, if started with a consistentestimate, the NR and Fisher scoring methods lead in one step to an asymptoticallyefficient estimate. Thus, since γ, the MLE of γ (obtained as the final iteratedestimate for the full model), is a consistent estimate (see Hartley and Rao, 1967)this leads in one step to an efficient estimate of γ(i).

Noting that at convergence γ(t+1) = γ(t) − (F(t))−1g(t) is equal to γ(t+1) =γ(t)−(E(F(t)))−1g(t) and making use of Theorem 1, the one step updating formulafor variance components ratios becomes

γ(i) = γ − (Q − G)−1g(i)

where

Q(j, k) = E(F(i, j)),

G(j, k) =1mi

{ 12mi

ssq(zjiz′ki) − z′jiW (ZjZk)zki}

158 T. Zewotir and J. S. Galpin

for j, k = 1, 2, . . . , r , and the j-th element of g(i) is

∂λ

∂γj(i)=

12ssq(W (Zj ,d))

(1

σ2e(i)

− 1σ2

e

)

+W (d,Zj){W (Zj ,X)W (X,X)−1xi − zji

} y − x′iβ

σ2e(i)(mi − pii)

+(y − x′

iβ)2

2σ2e(i)(mi − pii)

ssq(W (Zj,X)W (X,X)−1xi − zji) +1

2missq(zji),

where the notation ssq(A) is the sum of the squares of elements of A. Clearly, theone step estimate can only be obtained by explicitly recomputing and reinverting(Q − G) for each i. This is an r × r matrix, where r is the number of randomeffects in the model. In most practical cases r will not be large enough to implythat an r × r matrix inversion is expensive.

CPJ used xi, zi, zji, yi, pii and mi as the basic building blocks of the casedeletion statistics. All are a function of a row (or column) of H and H−1

[i] . But inthe iterative estimation process for the full model, it is not necessary to explicitlycompute and store H, an n×nmatrix. Moreover, H[i] is an (n−1)×(n−1) matrix,and its inversion and storage for each i, i = 1, 2, . . . , n, would be computationallyexpensive. Although CPJ, overcame this last problem to a certain extent bynoting that one can write H−1

[i] = C[i] − 1cii

cic′i, for

C = H−1 =[cii c′ici C[i]

],

it is still essential that xi, zi, zji, yi, pii and mi be computed using H−1[i] , for each

of the n cases deleted in turn. This is extremely time consuming. It is, therefore,important to find a solution to the problem, which we solve using other basicbuilding blocks.

Theorem 2: (Basic theorem on efficient updating): If C′i = [cii c′i], so that Ci

is the i-th column of H−1 and cii is the i-th diagonal element of H−1 then

(1) mi =1cii, (2) xi =

1cii

X′Ci

(3) zji =1cii

Z′jCi and (4) yi =

1cii

y′Ci.

The proof is given in the Appendix. In summary, once we have H−1 a veryefficient updating formula can be obtained by applying Theorem 2. Obtaining

Influence Diagnostics for Linear Mixed Models 159

H−1 seems to require inversion of an n × n matrix, but the formula H−1 =I − Z(D−1 + ZZ)−1Z′ reduces the work, and implies that there is no need tocompute and store either H−1

[i] or H.Making use of Theorem 2, C,R, and e the updating formulae become

β − β(i) = W (X,X)−1X′Cieirii,

σ2e(i) =

n

n− 1σ2

e − e2i(n − 1)rii

= σ2e

(n

n− 1− t2in− 1

),

u− u(i) = DZ′Rieirii

∂λ

∂γj(i)=

12σ2

e

(t2i − 1n− t2i

)ssq(Z′

je) − ti(n− 1)(n − t2i )

√riiσ2

e

e′ZjZ′jRi

+t2i (n− 1)

2rii(n− t2i )ssq(Z′

jRi) +1

2ciissq(C′

iZj),

and

G(j, k) =1cii

{1

2ciissq(Z′

jCiC′iZk) − C′

iZjW (Zj,Zk)Z′kCi

},

j, k = 1, 2, . . . , r.As it can be seen from Table 3.1, when the i-th case is deleted the number

of arithmetic operations involved is substantially reduced by (4n − 1)(n − 1) −2(p + q + 1), which is at least (2n − 1/2)(2n − 3) − 1/2, since p + q + 1 ≤ n.Thus, at least n{(2n− 1/2)(2n − 3) − 1/2} operations and the computation andstorage of H are reduced in the overall basic blocks construction for a case deletionupdating formulae. For large n, which is frequently the case, the improvementis substantial. Moreover, the rearrangement of the elements of H and H−1 inorder to compute H−1

[i] which creates a computational difficulty and defeats the

compactness of the updating formula is avoided. Note that H−1[i] hi is common for

mi, xi, zi and yi, and the number of arithmetic operations required to computeH−1

[i] hi is counted only once.Besides the computational advantage in a case deletion diagnostics, as it can

be seen from Section 4, a more general, compact and appealing diagnostic toolscan be easily obtained from our updating formulae.

For spatial linear models, y = Xβ + ε with var(ε) = σ20V, where the co-

variance matrix of the data is determined by the locations at which observationsare taken, mi, xi and yi were used as basic building blocks for the covariancefunction diagnostics (Christensen et al., 1993) and prediction (i.e., prediction offuture observation) diagnostics (Christensen et al., 1992). In such cases too the

160 T. Zewotir and J. S. Galpin

computational advantage of our method relative to Christensen et al. (1992,1993) is large by using V in place of H.

Table 3.1: The number of operations required to compute the basicbuilding blocks for ith case deletion updating

H−1[i] H−1

[i] hi mi xi

CPJ (n− 1)(2n − 1) 2(n− 1)2 (2n− 1) p(2n− 1)Ours − − 1 p(2n+ 1)

zi yi Total

CPJ q(2n− 1) (2n − 1) (2n − 1)(n+ p+ q + 1)+2(n− 1)2

Ours q(2n+ 1) (2n + 1) (2n+ 1)(p + q + 1) + 1

In the fixed effects models y = Xβ+ε with var(ε) = σ20V, the generalized least

squares estimate of β is given by β = (X′V−1X)−1X′V−1y. Noting that insteadof the commonly used residuals the predicted residuals could be easily obtained insuch a model, Haslett (1999) simplified the aspects of work discussed by Martin(1992) and Hayes and Haslett (1998) and showed that predicted residuals (whichthey referred to as “conditional residuals”) play a key role in the diagnostics. Butby making use of the two theorems (and using V in place of H), the simplicity androle of the natural residuals is pronounced and that gives more insight to ascribethe source of influence to easily interpretable components such as residuals andleverages. It must be also noted that conditional residual can be easily obtainedas e(i) = yi − x′

iβ(i) − z′iu(i) = ei/rii.The updating formulae assume that the variance components ratios are cor-

rect. CPJ, Banerjee and Frees (1997) and Haslett (1999) also make this assump-tion. Thus it seems important we first examine the variance components ratiosdiagnostics and take any necessary measure in order to build confidence that thevariance components ratios estimate are equally sensitive to each observation.However, since the maximum likelihood estimate of the variance components ra-tios and the maximum likelihood estimate of fixed effects are independent suchassessment might not be that essential. This is clearly demonstrated from our ex-amples (Section 5) that the inclusion or exclusion of variance components ratiosinfluential observations has no remarkable effect on the influence of fixed/randomeffects and the likelihood function.

Influence Diagnostics for Linear Mixed Models 161

4. Measures of Influence

We propose and investigate a number of diagnostics for the variance compo-nents ratios, fixed effects parameters, prediction of the response variable and ofrandom effects, and the likelihood function.

4.1 Influence on variance components ratios

The general diagnostic tools for variance components ratios are the analoguesof the Cook’s distance and the information ratio.

4.1.1 Analogue of Cook’s distance

The analogue of Cook’s distance measure for variance components γ, is

CDi(γ) = (γ(i) − γ)′[var(γ)]−1(γ(i) − γ)

= −g′(i)(Q − G)−1Q(Q− G)g(i)

= g′(i)(Ir + var(γ)G)−2var(γ)g(i).

Large values of CDi(γ) highlight points for special attention.

4.1.2 Analogue of the information ratio

The analogue of the information ratio measures the change in the determinantof the maximum likelihood estimate’s information matrix, giving

IR(γ) =det(Inf(γ(i)))det(Inf(γ))

=det(Q − G)

det(Q)

=det(Q) det(Ir −Q−1G)

det(Q)= det(Ir + var(γ)G),

where det(A) denotes the determinant of the square matrix A. Ideally whenall observations have equal influence on the information matrix, IR(γ) is ap-proximately one. Deviation from unity indicates that the i-th observation ispotentially influential. Since var(γ) and Ir are fixed for all i = 1, 2, . . . , n,we observe that IR(γ) will be a function of G which is a function of Ci andcii = 1− z′i(D

−1 +ZZ)−1zi. Since cii is a function of the number of observationsfalling in the random effect levels, the values of IR(γ) tend to be identical for afairly balanced data set.

162 T. Zewotir and J. S. Galpin

4.2 Influence on fixed effects parameter estimates

4.2.1 Analogue of Cook’s distance

The Cook’s distance can be extended to measure influence on the fixed effectsin the mixed models by defining

CDi(β) = (β(i) − β)′W (X,X)(β(i) − β)/(pσ2e)

= C′iXW (X,X)−1Cie

2i /(pr

2iiσ

2e)

=(cii − rii)t2i

riip.

Large values of CDi(β) indicate points for further consideration.

4.2.2 Analogue of the variance ratio

The variance ratio measures the change of the determinant of the variance ofβ when the i-th case is deleted:

V Ri(β) =det(var(β(i)))

det(var(β))=

det(σ2e(i)W[i](X,X)−1)

det(σ2eW (X,X)−1)

=(n− t2in− 1

)pcii

cii − CiXW (X,X)−1X′Ci

=(n− t2in− 1

)pciirii.

As this is close to 1 if the point is not influential, it seems sensible to use therelative measure |V Ri(β)− 1| as a criterion for assessing the influence of the i-thobservation on the variance of β. The larger the statistic |V Ri(β)−1|, the higherthe influence of the i-th observation.

If one uses the trace instead of the determinant, the V R becomes

V Ri(β) = trace{[var(β)]−1(var(β(i)))}

=σe(i)

σ2e

trace{W (X,X)W[i](X,X)−1}

=n− t2in− 1

trace{I + X′CiC′

iXW (X,X)−1 1rii

}

=n− t2in− 1

(ciirii

+ p− 1).

Since V Ri(β) will be close to p if removing the i-th point does not change thetrace, we could use the relative measure |V Ri(β) − p| as a criterion for assessing

Influence Diagnostics for Linear Mixed Models 163

the influence of the i-th observation on the variance of β. The larger the statistic|V Ri(β) − p|, the higher the influence of the i-th observation.

4.2.3 Analogue of the Cook-Weisberg statistic

Another statistic used to measure the change of the confidence ellipsoid vol-ume of β is the Cook-Weisberg statistic. Under the assumption y ∼ N(Xβ, σ2

eH),β ∼ N(β, σ2

eW (X,X)−1). The 100(1 − α)% confidence ellipsoid for β is thengiven by E = {β : (β − β)′W (X,X)(β − β)/(pσ2

e ) ≤ F (α, p, n − p)}. When thei-th observation is omitted E(i) = {β : (β − β(i))′W[i](X,X)(β − β(i))/(pσ2

e(i)) ≤F (α, p, n−p−1)}. Cook and Weisberg (1980) proposed the logarithm of the ratioE(i) to E as a measure of influence on the volume of confidence ellipsoid for inthe multiple linear regression model, namely

CWi =volume(E(i))volume(E)

, i = 1, 2, . . . , n.

Noting that the volume of the ellipsoid is proportional to the inverse of thesquare root of the determinant of the associated matrix of the quadratic form,the analogous measure for fixed effects β becomes

CWi = log

{det(W (X,X)1/2σp

e(i)(F (α, p, n − p))p/2)

det(W[i](X,X))1/2σpe(F (α; p, n − p− 1))p/2

}

=12

log(ciirii

)+p

2log(n− tin− 1

)+p

2log(

F (α; p, n − p)F (α; p, n − p− 1)

).

If CWi is negative (positive) then the volume of the confidence ellipsoid is de-creasing (increasing) and increases (decreases) precision after deleting the ithobservation. Regardless of CWi’s sign, a large |CWi| indicates a strong influenceon β or/and var(β). The constant (p/2) log(F (α; p, n − p)/F (α; p, n − p − 1))does not affect the detection of an influential observation, but it plays importantrole in determining the sign of CWi. Clearly the Cook-Weisberg statistic, CWi,can be simplified as

CWi =12

log(V Ri(β)) +p

2log(

F (α; p, n − p)F (α; p, n − p− 1)

).

Thus apart from the F values, CWi is identical to V Ri(β). In fact, for large n,the ratio of the F values is close to 1, and hence CWi ≈

12 log(V Ri(β)).

164 T. Zewotir and J. S. Galpin

4.2.4 Analogue of the Andrews Pregibon statistic

Yet another measure based on the volume of the confidence ellipsoid is theAndrews Pregibon statistic:

APi = −12

log

{e′(i)e(i) det(W[i](X,X))

e′edet(W (X,X))

}, i = 1, 2, . . . , n.

Note that

e(i) = y(i) − X(i)β(i) − Z(i)u(i)

= y(i) − X(i)β − Z(i)u

+ (X(i)W (X,X)−1X′Ci + Z(i)DZ′Ri)eirii.

For Ri(i) and Ci(i) the i-th column of R and H−1 without the i-th element,respectively,

Z(i)DZ′Ri = (H(i) − I(i))H−1(Ii − XW (X,X)−1X′Ci)

= −Ri(i) − X(i)W (X,X)−1X′Ci,

which then yields

e(i) = y(i) − X(i)β − Z(i)u− Ri(i)eirii, and

e′(i)e(i) = ssq(y(i) − X(i)β − Z(i)u− Ri(i)(ei/rii))

= e′e +e2ir2ii

ssq(Ri) − 2eirii

e′Ri = ssq(e − eirii

Ri).

It immediately follows that

APi =12

log(ciirii

)+

12

log(e′e) − 12

log(ssq(e − eirii

Ri)).

Obviously, the larger the statistic APi, the stronger the i-th observation’s influ-ence on the fit.

4.3 Influence on random effect prediction

The proposed diagnostic measure examines the squared distance from thecomplete data predictor of the random effects to the i-th case deleted predictor of

Influence Diagnostics for Linear Mixed Models 165

the random effects, relative to the variance of the random effects, var(u) = σ2eD.

This is the analogue to the Cook distance (Cook, 1977) and can be written as

CDi(u) = (u− u(i))′D−1(u− u(i))/σ

2e =

t2irii

R′iZDDZ′Ri

=t2irii

R′i(H − I)Ri = t2i

(1 − ssq(Ri)

rii

).

A large CDi(u) indicates that the i-th observation is influential in predicting therandom effects.

4.4 Influence on the likelihood function

Because of the computational intractability in estimating the variance com-ponents ratios, we consider the estimate of θ′ = [β′, σ2

e ], assuming γ fixed. Forθ(γ) and θ(i)(γ), the maximum likelihood estimates of θ based on n and n − 1observations, respectively, let λ(θ(γ)) and λ(θ(i)(γ)) be the log likelihood functionevaluated at θ(γ) and θ(i)(γ), respectively. The distance between the likelihoodfunctions measures the influence of the i-th observation on the likelihood function,giving the likelihood distance LDi (cf Cook and Weisberg, 1982) as

LDi = 2{λ(θ(γ)) − λ(θ(i)(γ)}

where

λ(θ(γ)) = −n2

log 2π − n

2log σ2

e − 12

log(det(H)) − n

2and

λ(θ(i)(γ)) = −n2

log 2π − n

2log σ2

e(i) −12

log(det(H))

−(y − Xβ(i))′H−1(y − Xβ(i))/(2σ

2e(i)).

Furthermore, since

(y − Xβ(i))′H−1(y − Xβ(i)) = nσ2

e +e2ir2ii

(cii − rii),

we obtain

LDi = n log(n− t2in− 1

)+

[n+ t2i (cii − rii)](n − 1)rii(n− t2i )

− n.

If LDi is large then the i-th observation is influential on the likelihood function.

166 T. Zewotir and J. S. Galpin

4.5 Influence on Linear Functions of β

In some cases we may be interested in assessing the influence of the i-thobservation on a given subset of β, or more generally, on s linearly independentcombinations of β namely ψ = L′β where L′ is s × p matrix with rank(L) =s, using the maximum likelihood estimate of ψ, ψ = L′β. Omitting the i-thobservation, the MLE of ψ is ψ(i) = L′β(i). Using the generalized Cook’s statisticas a measure of the influence of the i-th observation on ψ we obtain

CDi(ψ) = (ψ − ψ(i))′(L′W (X,X)L)−1((ψ − ψ(i))/(sσ

2e )

= (β(i) − β)′M(β(i) − β)/(sσ2e )

= C′iXW (X,X)−1MW (X,X)−1X′Cit

2i /(srii),

where M = L(L′W (X,X)−1L)−1L′. For positive definite M, we have

Ci′XW (X,X)−1X′Ci − C′

iXW (X,X)−1MW (X,X)−1X′Ci

= Ci′XW (X,X)−1/2[I −W (X,X)−1/2MW (X,X)−1/2]W (X,X)−1/2X′Ci

≥ 0

and

C′iXW (X,X)X′Cit

2i /(srii) ≥ C′

iXW (X,X)−1MW (X,X)−1X′Cit2i /(srii),

so that

CDi(β)p/s = (cii − rii)t2i /(srii)≥ C′

iXW (X,X)−1MW (X,X)−1X′Cit2i /(srii)

= CDi(ψ)

where p/s is fixed. This means that CDi(ψ) does not need to be calculated unlessCDi(β) is large.

One can further simplify CDi(ψ) by imposing some constraints on L. If ourinterest is centered on the influence of the i-th observation on t elements of β(which we assume, without loss of generality, to be the last t components of β)we have L′ = [0 | It] where 0 is a t× (p− t) matrix of zeros. Partitioning X intoX = [X1 |X2] we obtain

W (X,X)−1 =[W (X1,X1) W (X1,X2)W (X2,X1) W (X2,X2)

]−1

,

Influence Diagnostics for Linear Mixed Models 167

and using the standard matrix identity for the inverse of a partitioned matrix wefurther simplify

W (X,X)−1MW (X,X)−1

= W (X,X)−1L(L′W (X,X)−1L)−1L′W (X,X)−1

= W (X,X)−1 −[W (X1,X2)−1 0

0 0

]

from which it follows that

CDi(ψ) =t2itrii

(cii − rii − C′iX1W (X1,X1)−1X′

1Ci)

=p

tCDi(β)(1 − 1

cii − riiCi

′X1W (X1,X1)−1X′1Ci),

which measures the influence of the i-th observation on the last t elements of β.If our interest is centered on the influence of one particular effects’ level,

namely βk, t = 1,L′ = [0 | 1], X1 = X[k] and X2 = Xk and

CDi(ψ) = pCDi(β)(1 − 1cii − rii

Ci′X[k]W (X[k],X[k])

−1X′[k]Ci),

which measures the influence of the i-th observation on the k-th element of β.

5. Application

5.1 Aerosol dataBeckman et al. (1987) developed local influence diagnostics for the mixed

model and illustrated their methodology by using aerosol penetration data. CPJused the same data for comparison and illustration of their diagnostic methods.We use the same data.

The aerosol data involves high-efficiency particulate air filter cartridges usedin commercial respirators to prevent or reduce the respiration of toxic fumes,radionuclides, dusts, mists, and other particulate matter. The aim is to determinethe factors that contribute most to the variability in penetration of the filtersand to determine whether the standard aerosol can be replaced by an alternativeaerosol in quality assurance testing. Filters fail a quality test if the percentage ofpenetration of an aerosol is too large. Two aerosols were crossed with two filtermanufacturers. Within each manufacturer, three filters were used to evaluate thepenetration of the two aerosols. The aerosols and manufacturers were taken asfixed effects and the filters nested within manufacturers were taken as a randomeffect. The data are presented in Table 5.1.

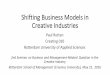

Figures 5.1-5.4 give the index plots of the influence measures. Cases 33 and31 stand out as the most influential on the filter variance ratio, CD(γ), with

168 T. Zewotir and J. S. Galpin

Table 5.1: Percent penetration of two aerosols using three filters from manu-facturers

Manufacturer 1 (j = 1) Manufacturer 2 (j = 2)Filter 1 Filter 2 Filter 3 Filter 1 Filter 2 Filter 3(k = 1) (k = 2) (k = 3) (k = 1) (k = 2) (k = 3)

Aerosol 1 (i = 1) 0.750 0.082 0.082 0.600 4.100 1.0000.770 0.085 0.076 0.680 5.000 1.8000.840 0.096 0.077 0.870 1.800 2.700

Aerosol 2 (i = 2) 0.910 0.660 2.170 1.120 0.160 0.1500.830 0.830 1.520 1.100 0.110 0.1200.950 0.610 1.580 1.120 0.260 0.120

0 3 6 9 12 15 18 21 24 27 30 33 36

0.00

0.05

0.10

0.15

0.20

0.25

0.300 3 6 9 12 15 18 21 24 27 30 33 36

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Figure 5.1 Index plot of CD(γ) and |IR-1|

CD(γ) |IR-1|

Diag

nost

ic va

lue

Index

0 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.2

0.4

0.6

0.8

1.0

1.20 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Figure 5.2 Index plot of CD(β), |VR-1|, |CW| and AP

CD(β) |VR-1| |CW| AP

Diag

nost

ic va

lue

Index

0 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.1

0.2

0.3

0.4

0.5

0 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.1

0.2

0.3

0.4

0.5

Figure 5.3 Index plot of CD(u)

Index

Diag

nost

ic Va

lue

0 3 6 9 12 15 18 21 24 27 30 33 36

0

2

4

6

8

0 3 6 9 12 15 18 21 24 27 30 33 36

0

2

4

6

8

Figure 5.4 Index plot of LD

LD

Index

cases 14 also being indicated as influential. However, Beckman et al. and CPJranked case 14 as the most influential observation on the filter variance, with cases13, 31, 32 and 33 regarded as somewhat less influential on the filter variance.

Influence Diagnostics for Linear Mixed Models 169

Table 5.2: Maximum likelihood filter variacneratio estimate for aerosol data

MLE % of change

Full data 0.21516832Case 33 deleted 0.34529161 60.475%Case 31 deleted 0.33581581 56.071%Case14 deleted 0.31175359 44.888%

0 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.2

0.4

0.6

0.8

1.0

1.20 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Figure 5.5 Index plot of CD(β), |VR-1|, |CW| and APwhen case 33 is deleted

CD(β) |VR-1| |CW| AP

Diag

nost

ic va

lue

Index0 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 3 6 9 12 15 18 21 24 27 30 33 36

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Figure 5.6 Index plot of CD(u) when case 33 is deleted

Index

Diag

nost

ic Va

lue

0 3 6 9 12 15 18 21 24 27 30 33 36

0

2

4

6

8

0 3 6 9 12 15 18 21 24 27 30 33 36

0

2

4

6

8

Figure 5.7 Index plot of LD when case 33 is deleted

LD

Index

Table 5.2 gives the variance ratio estimate for cases 33, 31 and 14 deleted.The result indicates that case 33 is the most influential point while case 14 is thethird most influential case.

Figures 5.2-5.4 show the index plots of the influence measures for fixed effects,prediction of random effects and the log-likelihood distance, respectively. In allof these, case 14 is by far the most influential point. Case 13 is clearly the secondmost influential case. In the overall analyses of aerosol data cases 13 and 14 havea large influence. However, before dealing with the influential cases on the

170 T. Zewotir and J. S. Galpin

Table 5.3: Metallic oxide analysis data

Raw Lot Sample 1 Sample 2material Chemist 1 Chemist 2 Chemist 1 Chemist 2

Type 1 1 4.1 4.0 4.3 4.3 4.1 4.0 4.1 4.12 4.1 4.0 4.0 3.9 4.2 4.2 3.7 4.63 3.5 3.5 3.4 3.6 3.4 3.3 4.0 3.54 4.2 4.2 4.2 4.3 4.1 3.7 4.1 4.65 3.7 3.8 3.3 3.3 3.2 3.1 3.1 3.26 4.0 4.2 3.8 4.2 4.1 4.3 4.2 4.17 4.0 3.8 3.8 4.0 3.6 3.8 3.9 3.88 3.8 3.9 4.0 3.9 4.0 4.0 4.2 4.09 4.2 4.5 4.3 4.1 3.8 3.7 3.8 3.810 3.6 4.0 4.0 3.7 3.9 4.1 4.2 3.711 4.6 4.6 4.0 3.4 4.4 4.5 3.9 4.112 3.3 2.9 3.2 3.9 2.9 3.7 3.3 3.413 4.5 4.5 4.0 4.2 3.7 4.0 4.0 3.914 3.8 3.8 3.5 3.6 4.3 4.1 3.8 3.815 4.2 4.1 3.8 3.8 3.8 3.8 3.9 3.916 4.2 3.4 3.7 4.1 4.4 4.5 4.0 4.017 3.3 3.4 3.9 4.0 2.2 2.3 2.4 2.7b

18 3.6 3.7 3.6 3.5 4.1 4.0 4.4 4.2

Type 2 1 3.4 3.4 3.6 3.5 3.7 3.5 3.1 3.42 4.2 4.1 4.3 4.2 4.2 4.2 4.3 4.23 3.5 3.5 4.2 4.5 3.4 3.7 3.9 4.04 3.4 3.3 3.5 3.1 4.2 4.2 3.3 3.15 3.2 2.8 3.1 2.7 3.0 3.0 3.2 2.76 0.2 0.7 0.8 0.7 0.3 0.4 0.2 −1.07 0.9 0.6 0.3 0.6 1.0 1.1 0.7 1.08 3.3 3.5 3.5 3.4 3.9 3.7 3.7 3.79 2.9 2.6 2.8 2.9 3.1 3.1 2.9 2.710 3.8 3.8 3.9 3.8 3.4 3.6 4.0 3.811 3.8 3.4 3.6 3.8 3.8 3.6 3.9 4.012 3.2 2.5 3.0 3.5 4.3 3.7 3.8 3.813 3.4 3.4 3.3 3.3 3.5 3.5 3.2 3.3

Note: Table value is metal content minus 80 in percent by weight

fixed/random effects and the log likelihood function, scrutinizing influential pointson the variance components ratio seems essential.

Accordingly, case 33 was deleted and Figures 5.5-5.7 present the diagnostic

Influence Diagnostics for Linear Mixed Models 171

Table 5.4: The Top 5 influential cases

ID CDi(γ) ID CDi(β)

(2,6,2, 2,1) 0.468932 (2,6,2,2,2) 0.00118(1,2,2,2,2) 0.129775 (2,12,1,1,2) 0.00041(1,11,1,2,2) 0.125141 (2,12,2,1,1) 0.00041(1,2,2,2,1) 0.117674 (1,11,1,2,2) 0.00029(2,12,2,1,1) 0.101159 (1,2,2,2,2) 0.00026

ID |CRi − 1| ID |CWi|(2,6,2,2,2) 0.26717 (2,6,2,2,2) 0.155420(2,12,1,1,2) 0.09283 (2,12,1,1,2) 0.048712(2,12,2,1,1) 0.09134 (2,12,2,1,1) 0.047890(1,11,1,2,2) 0.09103 (1,11,1,2,2) 0.047723(1,2,2,2,2) 0.07938 (1,2,2,2,2) 0.041354

ID APi ID CDi(u)

(2,6,2,2,2) 0.06554 (2,6,2,2,2) 3.15971(2,6,2,2,1) 0.03450 (2,12,1,1,2) 1.11102(1,2,2,2,1) 0.02850 (2,12,2,1,1) 1.09466(1,2,2,2,2) 0.02820 (1,11,1,2,2) 1.09466(2,12,2,1,1) 0.02475 (1,2,2,2,2) 1.0912

ID LDi

(2,6,2,2,2) 1.38359(2,12,1,1,2) 0.13386(2,12,2,1,1) 0.12939(1,11,1,2,2) 0.12803(1,2,2,2,2) 0.09615

The order in the ID is (raw material type, lot, sample, chemist, du-plicate analysis number).

measures for the fixed/random effects, the response variable and the log likelihoodfunction without case 33. Many of the general features of Figure 5.5 are similar tothe full data plot Figure 5.2. Likewise, Figure 5.6 and Figure 5.3, and Figure 5.7and Figure 5.4 are similar. It seems that case 33 has little effect on the influenceof each observation on the fixed/random effects and the log-likelihood function,while it has a noticeable effect on the variance components ratio.

172 T. Zewotir and J. S. Galpin

5.2 Metallic oxide data

Fellner (1987) introduced the robust estimation of variance components andillustrated his methodology by using metallic oxide data. The metallic oxideanalysis data given by Fellner (1987) were taken from a sampling study designedto explore the effects of process and measurement variation on the properties oflots of metallic oxide. The data are shown in Table 5.3. Two samples were drawnfrom each lot. Duplicate analyses were then performed by each of two chemists,with a pair of chemists being randomly selected for each sample.

A nested model was fitted, with raw material type considered fixed, and lot,sample and chemist considered random.

The top five influential points on variance components ratios, fixed effect pa-rameters, prediction of random effects and likelihood function are given in Tables5.4. The order in the identification is (raw material type, lot, sample, chemist,duplicate analysis number). Observation (2,6,2,2,1) is the most influential on thevariance components ratios estimate. On the other hand, observation (2,6,2,2,2)is by far the most influential on the fixed and random effects estimate and likeli-hood function. There is no large second most influential observation. Since in abalanced design the value of IRi(γ) is identical for all i, IRi(γ) did not indicateany influential point on the variance of variance components ratios estimate.

Table 5.5 gives the maximum likelihood variance components ratios estimateswith the full data and with case (2,6,2,2,1) removed. But case (2,6,2,2,2) is notinfluential on the variance components ratios, even if it is an outlier and influen-tial on the fixed and random effects estimate and the likelihood function. Outliersneed not necessarily be influential. In order to clear the doubt we also includethe estimates when case (2,6,2,2,2) is removed.

Table 5.5: Metallic oxide data: Maximum likelihood esti-mate of variance components ratios from full-data and thedata with cases (2,6,2,2,1) and (2,6,2,2,2) removed

Full data (a) % change (b) % change

Lot 13.0791 14.9490 14.30% 14.2893 9.25%Sample 1.0019 1.1538 15.17% 1.0774 7.54%Chemist 0.7379 1.0174 37.88% 0.8031 8.84%

(a)= case (2,6,2,2,1) deleted; (b)= case (2,6,2,2,2) deleted.

The estimates of the variance components ratios are small with the full data.Deleting case (2,6,2,2,1) results in an increase in the variance components ratios

Influence Diagnostics for Linear Mixed Models 173

of the lot effect, sample effect and chemist effect far larger than that due todeleting case (2,6,2,2,2). Undoubtedly the cumulative increase in the variancecomponents ratios will have a substantial effect on the overall fit. Thus case(2,6,2,2,1) should be put under scrutiny.

We further assessed if the inclusion or exclusion of case (2,6,2,2,1), whichis the most influential case on the variance components ratio, does have a re-markable effect on the influence measures of the fixed/random effects and thelog-likelihood function. The result shows that the top five influential cases underCDbeta), |V R − 1|, |CW |, CD(u) and LD remained as the top five influentialcases and case (2,6,2,2,2) is by far the most influential point on the fixed andrandom effects estimate and likelihood function. But under AP statistic cases(1,2,2,2,1), (1,2,2,2,2) and (2,12,2,1,1), become the top three influential pointsand case (2,6,2,2,2) becomes the seventh influential observation. This is, perhapsthe removed case and case (2,6,2,2,2) belongs in the same cell and the removedcase was also the second top influential case under AP statistic.

6. Concluding Remarks

We have presented various diagnostic measures that appear useful and canplay an important role in linear mixed model data analysis. All the diagnosticmeasures are a function of the basic building blocks: Studentized residuals, errorcontrast matrix, and the inverse of the response variable covariance matrix. Thebasic building blocks are computed only once from the complete data analysis.

Although no formal cutoff points are presented for these measures, it appearsthat relative comparisons such as rankings or simple index plots are a promisingand practical approach to pinpoint influential observations. The basic buildingblocks, particularly C, R and e play an important role in the mixed modeldiagnostics. Characterization of the distributions and properties of C and R arenot studied. This is a bottleneck for distributional properties and cutoff pointfor the diagnostic measures. This is an issue for future research.

Generally we fit a linear mixed model by specifying the covariance structureof u and ε. Here we have assumed that D is block diagonal with the i-th blockbeing γiIqi . In the case where D is a known unstructured covariance matrix, i.e.,the covariance of u is arbitrary positive definite matrix, the diagnostic measuresfor the fixed effects, random effects and likelihood function derived in this studywould be used as they are. However, if D is unknown, extending our diagnosticsto assess influence on such unstructured covariance estimates is an area of futureresearch.

174 T. Zewotir and J. S. Galpin

Acknowledgements

The work of the first author is supported by German Academic ExchangeService (DAAD) and is grateful for the support.

Appendix: Proof of Theorems

Proof of theorem 1

W (A,B) = [ai, bfA′(i)]H

−1[b′i,B(i)]′. Applying the standard matrix identity

for the inverse of a partitioned matrix H, we obtain

W (A,B) = [ai,A′(i)]

[1/mi −h′

iH−1[i] /mi

−h′iH

−1[i] /mi H−1

[i] + H−1[i] hih′

iH−1[i] /mi

][b′

i

B(i)

]

= aibi′/mi − A′

(i)H−1[i] hib′

i/mi − aih′iH

−1[i] B(i)/mi

+ A′(i)H

−1[i] B(i) + A′

(i)H−1[i] hih′

iH−1[i] B(i)/mi

= A′(i)H

−1[i] B(i) + ai(b′

i − h′iH

−1[i] B(i))/mi

− A′(i)H

−1[i] hi(b′

i − h′iH[i]B(i))/mi

= A′(i)H

−1[i] B(i) + (ai − A′

(i)H−1[i] hi)(b′

i − hi′H−1

[i] B(i))/mi

= A′(i)H

−1[i] B(i) + aib′

i/mi = W[i](A,B) + aib′i/mi �

Proof of theorem 2.

From the inverse of a partitioned matrix H and H−1, and the uniquenessproperty of the inverse of a positive definite matrix,

[cii c′ici C[i]

]=

[1/mi −h′

iH−1[i] /mi

−H−1[i] hi/mi H−1

[i] + H−1[i] hih′

iH−1[i] /mi

].

Then mi = 1/cii follows immediately. Further, ci = −H−1[i] hi/mi, ci/cii =

−H−1[i] hi,

xi = xi − X′(i)H

−1[i] hi = xi +

1cii

X′[i]ci

=1cii

(ciixi + X′[i]ci) =

1cii

[xi,X′[i]][ciici

]=

1cii

X′Ci.

Influence Diagnostics for Linear Mixed Models 175

Similarly,

zji = zji − Z′j(i)H

−1[i] hi =

1cii

Z′jCi, and

yi = yi − y′(i)H

−1[i] hi =

1cii

y′Ci . �

References

Andrews, D. F. and Pregibon, D. (1978). Finding outliers that matter. Journal of theRoyal Statistical Society, Series B 40, 85-93.

Banerjee, M. and Frees, E. W. (1997). Influence diagnostics for linear longitudinalmodels. Journal of the American Statistical Association 92, 999-1005.

Beckman, R. J., Nachtsheim, C. J. and Cook, R. D. (1987). Diagnostics for mixedmodel analysis of variance. Technometrics 29, 413-426.

Belsley, D. A., Kuh, E. and Welsch, R. E. (1980). Regression Diagnostics. Wiley.

Chatterjee, S. and Hadi, A. S. (1986). Influential observation, high leverage points, andoutliers in linear regression (with discussion). Statistical Science1, 379-416.

Chatterjee, S. and Hadi, A. S., (1988). Sensitivity Analysis in Linear Regression. Wiley.

Christensen, R., Johnson, W. and Pearson, L. M. (1992). Prediction diagnostics forspatial linear models. Biometrika79, 583-591.

Christensen, R., Johnson, W. and Pearson, L. M. (1993). Covariance function diagnos-tics for spatial linear models. Mathematical Geology 25, 145-160.

Christensen, R., Pearson, L. M. and Johnson, W. (1992). Case deletion diagnostics formixed models. Technometrics 34, 38-45.

Cook, R. D. (1977). Detection of influential observations in linear regression. Techno-metrics 19, 15-18.

Cook, R. D. (1986). Assessment of Local Influence (with discussion). Journal of theRoyal Statistical Society, Series B 48, 133-169.

Cook, R. D. and Weisberg, S. (1980). Characterization of an empirical influence functionfor detecting influential cases in regression. Technometrics 22, 495-508.

Cook, R. D. and Weisberg, S. (1982). Residual and Influence in Regression. Chapmanand Hall, London.

Cox, D. R. and Hinkley, D. V. (1974). Theoretical Statistics. Chapman and Hall,London.

Fellner, W. H. (1986). Robust estimation of variance components. Technometrics 28,51-60.

176 T. Zewotir and J. S. Galpin

Goodnight, J. H. (1978). Computing MIVQUE0 estimates of variance components.Technical Report R-105, SAS Institute Inc.

Hartley, H. O. and Rao, J. N. K. (1967). Maximum likelihood estimation of the mixedanalysis of variance model. Biometrika 54, 93-108.

Harville, D. A. (1977). Maximum likelihood approaches to variance component estima-tion and to related problems (with discussion). Journal of the American StatisticalAssociation 72, 320-340.

Haslett, J. and Hayes, K. (1998). Residuals for the linear model with general covariancestructure. Journal of the Royal Statistical Society, Series B 60, 201-215.

Haslett, S. (1999). A simple derivation of deletion diagnostics for the general linearmodel with correlated errors. Journal of the Royal Statistical Society, Series B61, 603-609.

Hemmerle, W. J. and Hartley, H. O., 1973. Computing maximum likelihood estimatesfor the mixed AOV model using the W transformation. Technometrics 15, 819-831.

Jennrich, R. I. and Sampson, P. F., 1976. Newton-Raphson and related algorithms formaximum likelihood estimation of variance components. Technometrics 18, 11-18.

Lawrance, A. J. (1990). Local and deletion influence. In Directions in Robust Statisticsand Diagnostics, Part I (Edited by W. A. Stahel and S. Weisberg), Springer Verlag.141-157.

Littell, R. C., Milliken, G. A., Stroup, W. W., and Wolfinger, R. D. (1996). SAS systemfor mixed models. SAS Institute Inc.

Martin, R. J. (1992). Leverage, influence and residuals in regression models whenobservations are correlated. Communications in Statistics, Theory and Methods21, 1183-1212.

McCulloch, C. E. and Searle, S. R. (2001). Generalized, Linear and Mixed Models.Wiley.

Oman, S. D. (1995). Checking the assumptions in mixed model analysis of variance:A residual analysis approach. Computational Statistics and Data Analysis 20,309-330.

Pregibon, D. (1981). Logistic regression diagnostics. Annals of Statistics 9, 705-724.

Robinson, G. K. (1991). That BLUP is a good thing: The estimation of random effects(with discussion). Statistical Science 6, 15-51.

SAS Institute Inc. (1992). SAS Technical Report, p. 229. SAS Institute, Cary, NC.

Searle, S. R., Casella, G. and McCulloch, C. E. (1992). Variance Components. Wiley.

Verbeke G. and G. Molenberghs (1997). Linear Mixed Models in Practice: A SASOriented Approach. Springer-Verlag.

Influence Diagnostics for Linear Mixed Models 177

Received February 4, 2004; accepted May 2, 2004.

Temesgen Zewotir (corresponding author)School of Statistics and Actuarial ScienceUniversity of KwaZulu-NatalPietermaritzburg CampusPrivate Bag X01, Scottsville 3209, SOUTH [email protected]

Jacky S GalpinSchool of Statistics and Actuarial ScienceUniversity of the WitwatersrandPrivate Bag 3, P. O. Wits 2050, SOUTH [email protected]