Embed Size (px)

Citation preview

Inheritance Tax P.X

in association with

Inheritance Tax planning:protecting your estate and familyProvided by Skipton Financial Services Limited

P.2 Telegraph Inheritance Tax Service

the last 20 years, people have generally become better off as their assets have risen in value – most notably house prices, which have climbed considerably over the past two decades. Yet there have been only small changes made to thresholds over that time, especially since 2009.

The idea of what constitutes an extremely wealthy person has changed, but the tax rules around inheritance have broadly remained the same.

When you die, if your estate’s value is higher than your Inheritance Tax threshold, 40% of everything you own above it will be taxed. That could easily run into thousands of pounds. It’s not just that your loved ones would miss out on a large slice of their inheritance; they would be left with the task of paying this tax bill during what would clearly be a difficult time. It is not a legacy that anyone wants to leave behind.

IntroductionMore than £4 billion will be raised through Inheritance Tax during the 2015/16 tax year, according to HMRC forecasts. That’s four times more than 30 years ago – demonstrating just how wide-reaching this tax has become.

In total, approximately 40,000 estates are expected to trigger a 40% tax bill over this year – with deceased’s family, friends and other loved ones missing out on that £4 billion. It is no wonder that Inheritance Tax has become so deeply unpopular in the UK. According to July 2015 research by NFU Mutual, nearly half of Brits believe that Inheritance Tax is the most unfair out of all taxes.

That so many people have an opinion about Inheritance Tax is testament to its growing impact. Traditionally, it has been considered a problem that only affected the richest people in society. Yet an increasing number of estates have incurred a liability. This is because, over

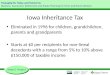

No children

Total £1 million:£675k subject to IHT

£270k IHT liability

Single person

Estate left to a friend

House:£500k

Assets:£500k

Total £1 million:No IHT liability

to be paid

Married /Civil partners

Estate left totwo children

House:£500k

Assets:£500k

Recent Government changes

The good news is that the Government is making changes to the rules, which will benefit those people who want to pass on their home to a direct descendant, such as a child or grandchild. From April 2017, this new ‘main residence’ nil rate band will be gradually introduced. It will mean that many will either see their Inheritance Tax liability significantly reduced, or face no problem at all.

However, not everyone will be able to take advantage of this rule. By HMRC’s own forecasts, even when the ‘main residence’ nil rate band is fully introduced for the 2020/21 tax year, 37,000 estates will be liable every year – roughly the same amount as there are today.

Telegraph Inheritance Tax Service P.3

This special Telegraph guide has been put together to steer you through the rules around Inheritance Tax, assist you in identifying if you might have a liability, and outline potential ways you can address it. It is not intended as a replacement for financial or tax advice.

It has been produced by the Telegraph’s recommended financial services partner, Skipton Financial Services Limited (SFS). Since 2004, SFS has helped thousands of readers put suitable plans in place towards reducing or, in some cases, even eliminating their Inheritance Tax liability. Some areas of Inheritance Tax planning are not regulated by the Financial Conduct Authority.

Married /Civil partners

Estate left toniece and nephew

No children

Total £1 million:£350k subject to IHT

£140k IHT liability

House:£500k

Assets:£500k

First things first, what exactly is Inheritance Tax?The origins of Inheritance Tax in the UK can be traced back to 1796 – although many countries around the world have their own version of the tax.

The original thinking behind it was to protect the poorest people in society – by taxing the richest people’s estates on death, and redistributing their wealth to the rest of the population. In 1857 the Inheritance Tax threshold was £20. It’s certainly come a long way since.

The thresholds

The current rules are that each person has an individual Inheritance Tax threshold of £325,000.

• If you are married or in a civil partnership, your allowances are added together, meaning you have an overall threshold of £650,000.

• If you are widowed, your threshold could be up to £650,000, depending on how much allowance was used when your partner passed away.

• Should you and your partner divorce, you will both once again have a threshold of £325,000 each.

When you die, everything you own above your threshold will be taxed at 40%. So if, for example, you are single and your estate is valued at £500,000, you will have an Inheritance Tax liability of £70,000 (£500,000 - £325,000 = £175,000. 40% of £175,000 = £70,000).

As we explain on page 7, from April 2017 a new ‘main residence’ nil rate band will be gradually introduced that, if applicable to you, could eventually mean your individual threshold is £500,000 or jointly £1 million.

P.4 Telegraph Inheritance Tax Service

Telegraph Inheritance Tax Service P.5

This is a really important point when you come to assess whether your estate has an Inheritance Tax liability. It will ultimately be calculated at the point you die, and over the coming years the value of your assets could climb considerably. Should house prices, for example, continue their general upwards trend since 2009, it could have a huge impact on the value of your estate.

Settling an Inheritance Tax liability

In the majority of cases, it will fall upon your loved ones to pay the Inheritance Tax bill – and, in some cases, they would have to settle it before they can inherit what you want them to have. At what would already be a very difficult time, this problem could cause a significant level of anxiety and stress.

Under the rules, the executor of your estate would be required to pay the Inheritance Tax bill within six months of your death. After that point, interest will be charged on top.

2014 research by UHY Hacker Young found that the UK and Ireland have the highest Inheritance Tax rates in the world.

For example, whilst the UK threshold is £325,000/£650,000, in the US it is £3.2 million. Several developed countries, such as Australia, New Zealand and Israel, have abolished Inheritance Tax altogether.

Your estate

Everything that you own is considered part of your estate. It includes obvious assets such as your home and any other property that you have (such as a holiday home or buy-to-let house).

Your car(s) is also included, as are your savings and investments. Furthermore, other items of notable value – from jewellery to antiques, and even your furniture – will be part of it too.

So although £325,000/£650,000 might sound like a large amount, when you actually add up everything that you own, you might be surprised by how much your estate is actually worth.

Your estate’s value isn’t fixed

The current £325,000/£650,000 thresholds have been in place since April 2009 – yet the amount of revenue raised over the 2014/15 tax year was 60% higher than in 2009/10. This is largely because people’s estates have climbed in value over the years, either triggering an Inheritance Tax bill or substantially increasing their existing liability.

Looking for help assessing the value of your estate?

The Telegraph website includes an interactive Inheritance Tax calculator, which can help you to work out the current – and potential future – value of your estate. Simply input details of the value of your assets, and you will receive an answer over whether you currently, or in future may, have an Inheritance Tax liability.

Visit telegraph.co.uk/iht to find out more.

No more Inheritance Tax on family homesFor eight years, the subject of Inheritance Tax thresholds has been at the centre of a major political debate – one that has influenced who is leading the country.

Back in October 2007 – with the Conservatives in opposition to a Labour Government – George Osborne made a pledge that, should his party win the next general election, they would increase Inheritance Tax thresholds to £1 million. It caused significant headlines, and it is said that the-then Prime Minister, Gordon Brown, delayed calling a snap general election that at the time polls strongly suggested he would win.

Ultimately, the next election wasn’t until 2010, which resulted in a coalition Government being formed by the Conservatives and the Liberal Democrats. No agreement could be made on Inheritance Tax policy, so the rules remained unchanged over the term of parliament. However, in the 2015 election the Conservatives surprisingly won a majority vote – meaning they could finally act on their 2007 promise.

During the election campaigning, David Cameron and Osborne both reaffirmed their pledge, and an extraordinary Budget announcement in July 2015 offered them the platform to announce new measures.

As part of his Budget speech, Osborne stated,

“You can pass up to £1 million on to your children free of Inheritance Tax. No more Inheritance Tax on family homes. Aspiration supported. The tax paid only by the rich. The security of home ownership restored. Promise made – promise delivered.”

P.6 Telegraph Inheritance Tax Service

Will you benefit?

Whilst there is no doubt this new rule will boost thousands of families, not everyone will be able to take advantage of the new allowance.

For example, it only applies if you leave your main property to a direct beneficiary, such as a child or grandchild. If you planned to pass on your home to a nephew or niece, for instance, you can’t benefit from this new rule.

In addition, whilst you can use your £175,000 per person additional allowance on your main home, any further property you own (such as buy-to-let) would be treated separately, in line with the existing rules, and will be counted within your £325,000 per person threshold.

Will the new allowance be enough?

Although a married couple or widower will have a combined additional £350,000 allowance from 2020, the value of your family home may climb above this amount before you die, if it isn’t already.

According to July 2015 forecasts by Centre for Economics and Business Research, average UK property prices will climb by 4.7% over 2015, to reach £261,000. This year-on-year rise is predicted to continue over the next five years, meaning that by 2020 the average UK house will be worth £321,000 – that’s only just below the £350,000 allowance.

And don’t forget, property prices in the South East and London areas are well above the UK average. If you live in these regions, the new ‘main residence’ nil rate band will help ease your potential Inheritance Tax burden, but it might not be enough to eliminate it.

‘Main residence’ nil rate band

From April 2017, the Government will phase in the new ‘main residence’ nil rate band. Initially it will be worth £100,000 per person, rising to £125,000 in April 2018, £150,000 in April 2019, and finally £175,000 in April 2020. The ‘main residence’ nil rate band will be available on estates worth up to

£2 million. It will be tapered away by £1 for every £2 an estate value is above £2 million.

This £175,000 per person allowance can be added to your existing threshold. So in effect, single or divorced people will have an overall threshold of £500,000, and for married couples or civil partnerships – and widowers – the threshold will be £1 million (jointly).

Telegraph Inheritance Tax Service P.7

The table below illustrates how even the new ‘main residence’ nil rate band might not be enough to eliminate your Inheritance Tax liability.

As an example, currently if a married couple’s home was worth £450,000 and other assets were worth £750,000, they would currently leave behind a £220,000 tax bill. Assuming the estate grows 5% compound per year, the liability would be £321,000 in 10 years’ time.

Value of Main Residence Value of Other IHT Now IHT 2020 IHT 2025

1 £150,000 £100,000 £0.00 £0.00 £0.00

2 £225,000 £250,000 £60,000 £39,000 £79,000

3 £300,000 £450,000 £170,000 £179,000 £258,000

4 £375,000 £550,000 £240,000 £268,000 £372,000

5 £450,000 £750,000 £350,000 £409,000 £551,000

Value of Main Residence

Value of Other IHT Now IHT 2020 IHT 2025

1 £150,000 £100,000 £0.00 £0.00 £0.00

2 £225,000 £250,000 £0.00 £0.00 £0.00

3 £300,000 £450,000 £40,000 £0.00 £0.00

4 £375,000 £550,000 £110,000 £65,000 £142,000

5 £450,000 £750,000 £220,000 £206,000 £321,000

Figures assume assets and house increase of 5% p/a, that the threshold increases 2.5% p/a from April 2020. Property allowance receives full benefit from 2020 with gradual increase from 2017. All figures rounded down to the nearest £1,000.

Married/Widowed Client

Mark Butterworth, head of technical services at SFS, explained,

“Naturally, no one wants to contemplate their own death. But if the collective value of your estate is above your threshold and therefore an element is going to be liable for a 40% Inheritance Tax bill, failure to take appropriate steps could leave your loved ones with the added burden of finding the money to pay it during what would already be a difficult time.

“It’s therefore recommended that you don’t leave it too late. If you are unsure whether your estate is going to have an Inheritance Tax liability, it’s at least worth finding out now. You can total up the value of all your possessions yourself to get a rough idea, or receive specialist, financial advice for a firmer picture.”

P.8 Telegraph Inheritance Tax Service

Single Client

Inheritance Tax is often nicknamed “the voluntary tax” – simply because there are, in fact, a number of options available to tackle any potential liability.

It does require careful planning. There is no doubt that the rules are complicated, and some of the options available might not be right for your circumstances. This is why it is strongly recommended you speak to an expert.

It is also really important that you address the issue as a priority. Leaving it too long can result

The Telegraph recommends the services of Skipton Financial Services Limited (SFS) for this reason. They are experts on Inheritance Tax planning and since 2004 have helped thousands of readers put plans in place to reduce or even eliminate their potential 40% tax bill.

There are a number of things you can do to address an Inheritance Tax liability

in a reduced level of options and potentially greater expense. This is because many of the potential solutions available require you to live at least seven years in order to be fully effective.

Beyond that, taking a proactive approach now can offer you peace of mind that you have plans in place that will help your loved ones. It will mean they aren’t faced with needless headaches during what would already be a difficult time.

Telegraph Inheritance Tax Service P.9

Things you can’t do if you don’t leave a Will:

• Pass your estate to an unmarried partner.

• Decide how much money and other assets each of your family members receive.

• Specify who will become the guardians of your children.

• Give a memento – e.g. a piece of jewellery to a treasured friend or a family member.

• Leave something to charity.

• Potentially minimise Inheritance Tax.

What are your options?There are a number of simple, cost-effective options available.

The importance of a Will

Using a Will is one of the most effective and convenient ways to reduce the amount of Inheritance Tax payable – by making the best possible use of the allowances available to both spouses.

There is a misconception that, when you die, your whole estate would be passed on to your spouse without the need for a Will. In reality, depending on the size of your estate, your partner may only inherit the first £250,000 plus your personal possessions and half of the remainder of the estate outright. Your children will receive the rest. An unmarried or unregistered civil partner has no automatic right to your estate at all.

Without a Will, you are deemed to have died ‘intestate’ which means the law – rather than you – dictates who will inherit your estate. A Will not only provides legal ways of helping to reduce or avoid Inheritance Tax, but helps ensure as much of your wealth as possible is retained by your family and that your ‘wishes’ are carried out.

P.10 Telegraph Inheritance Tax Service

Redstone Wills are members of The Society of Will Writers and Estate Planning Practitioners and abides by their code of practice, copies of which can be found on the Society of Will Writers website or by writing to them at Chancery House, Whisby Way, Lincoln LN6 3LQ. Redstone Wills Limited, Windmill Road, St Leonards-on-Sea, East Sussex TN38 9BY. Company no. 3673190. Will writing is not regulated by the Financial Conduct Authority.

Will Writing ServiceThere are many different types of Wills to allow for different circumstances – including Wills that seek to mitigate an Inheritance Tax liability and provide full estate planning solutions.

One of the reasons why the Telegraph recommends SFS for your Inheritance Tax planning needs is because they offer a Will Writing Service. As most Wills can be drawn up without the need for a face-to-face consultation

with a solicitor, SFS can provide you with the facility to have a simple Will drawn up at your own convenience; in your home and whenever you are ready to do so.

This service is provided in partnership with Redstone Wills Limited. You’ll have access to a direct helpline to Redstone who can help you complete your instruction form and guide you through the process. Will writing is not regulated by the Financial Conduct Authority.

Telegraph Inheritance Tax Service P.11

Redstone Wills are members of The Society of Will Writers and Estate Planning Practitioners and abides by their code of practice, copies of which can be found on the Society of Will Writers website or by writing to them at Chancery House, Whisby Way, Lincoln LN6 3LQ. Redstone Wills Limited, Windmill Road, St Leonards-on-Sea, East Sussex TN38 9BY. Company no. 3673190.

P.12 Telegraph Inheritance Tax Service

Gifts and trust planningThere is no Inheritance Tax applied on transfers between married couples or registered partners – whatever the value. Beyond that, there are a number of gift allowances available to every individual, where you can transfer your money and thereby reduce the value of your estate on which Inheritance Tax can be levied.

• Annual gift allowance – everyone can give away £3,000 exempt from Inheritance Tax, per tax year. It doesn’t have to go to a specific person, but the total must not exceed this figure. If you have not previously used it, you can backdate your previous year’s exemption and gift £6,000 to begin with.

• Marriage gifts exemption – if you’re feeling generous, you and your partner can each give a wedding gift of up to £5,000 to each child when they get married, at any time before their wedding day. If it is your grandchild, you can gift them up to £2,500. For other family members or friends, you can give up to £1,000. This can be combined with your annual exemption.

• Small gifts exemption – any number of gifts to different people, up to the value of £250 each, can be made in a tax year. Should the gift exceed £250, it must be deducted from your £3,000 annual exemption instead.

• Charitable donations exemption – all manner of gifts are exempt, and in addition – should you be willing to donate at least a tenth of your net wealth (estate above your threshold) to good causes – the Government will reduce your Inheritance Tax rate from 40% to 36%. This includes national institutions such as the British Museum, recognised political parties, universities and other gifts for the national benefit.

These gift exemptions include:

Telegraph Inheritance Tax Service P.13

Period of years before death

% Reduction (Taper Relief) % of Tax payable

0-3 years Nil 40%

3-4 years 20% 32%

4-5 years 40% 24%

5-6 years 60% 16%

6-7 years 80% 8%

More than 7 years No tax 0%

The table below shows you how this works

Other gifts

You can give bigger financial gifts, but in order for these to be exempt you must survive seven years from the date of the gift (although the £3,000 annual gift allowance can be offset against this). If you wish to consider this route, you must first ensure that you will have sufficient money left over to maintain your quality of life during your later years.

You can make unlimited direct gifts of cash, shares or other items of value – known as

Potentially Exempt Transfers (PETs) – and they will be deducted from your estate.

• If you die within the seven-year period, your estate may still have to pay tax on these PETs, on any part of the gift that is in excess of your Inheritance Tax threshold.

• However, the tax payable will reduce after the first three years (known as ‘Taper Relief’), and then fall further each year on a sliding scale.

Making giftsThere are four main ways of making gifts.

P.14 Telegraph Inheritance Tax Service

For a variety of reasons, you may not want your beneficiary to immediately receive a gift. Gifts to Trust allow you to place money into a suitable investment, which is then wrapped in a Trust. You can choose who you want to be the

2. Gifts to Trust

As the name suggests, this is handing the gift directly to a beneficiary for their immediate benefit.

1. Direct gift

Advantage Disadvantage

• Growth outside estate from day 1

• All IHT Free After 7 Years

• Annual Gift Allowance available

• Retain element of control as trustees

• Settlor has No Access to Capital or Growth

• Can’t be used to provide an income to Settlor

• Must survive 7 years for it to be fully outside of the estate

trustees, including yourself and the trustees are responsible for distributing the capital of the trust. The two more commonly used types of Trust are Flexible Trust and Discretionary Trust.

Advantage Disadvantage

• Growth outside estate from day 1

• All IHT Free After 7 Years

• Annual Gift Allowance available

• Settlor has No Access to Capital or Growth

• Can’t be used to provide an income to Settlor

• Must survive 7 years for it to be fully outside of the estate

• Loss of control

How we can help

Our Adviser will invest your money for you and assist you to complete the relevant paperwork

to reflect your wishes.

If you wish to retain access to your original capital rather than gift it away, a Loan Trust plan could be suitable. Again you place the money inside a suitable investment, and any growth belongs to the Trust – making it free from Inheritance Tax – whilst the original investment belongs to you and remains within your estate.

A Loan Trust is not the most efficient way of minimising an Inheritance Tax liability, as only the investment gains are free from Inheritance Tax. However, it is an ideal method of boosting your income and keeping control of your capital – as any amount can be taken from the loan until the original capital invested is exhausted.

Telegraph Inheritance Tax Service P.15

3. Loan Trust

This is another method of giving money away (and it is outside of your estate after seven years) whilst still having access to a regular, pre-determined income. In addition to this – based on a number of factors including age,

Making gifts can be complex, which is why financial advice is strongly recommended. The Telegraph recommends Skipton Financial Services Limited (SFS) to offer readers personalised advice on making suitable plans. They can discuss these options in greater detail, and offer you advice that is personalised to your specific circumstances. Trusts are not regulated by the Financial Conduct Authority.

Advantage Disadvantage

• Any growth is outside estate from day 1

• Allows access to original capital

• Only original loan comes back into the estate

• Retain element of control as trustees

• Any Outstanding Loan falls within the Settlor’s estate

• No Access to Growth

• If an income is provided this is exhausted once the original capital is exhausted

Advantage Disadvantage

• All IHT Free After 7 Years

• Annual Gift Allowance available

• You are able to receive a fixed income

• Potential for an element of Gift to be IHT free immediately

• Growth outside estate from day 1

• No Capital Access by the Settlor or beneficiaries during Settlor’s lifetime

• Can’t amend the level of income

• Must survive 7 years for whole amount to be outside of the estate

4. Discounted Gift Schemes

health and the level of income selected – there is usually an immediate ‘discount’ to Inheritance Tax. This means that an investment into this scheme usually results in an immediate saving in Inheritance Tax.

Life insuranceSometimes, despite all other methods of trying to eliminate or reduce Inheritance Tax, there is no option but to simply insure the liability. This can be done by taking out life insurance to cover the cost of the tax bill that your heirs will have to pay when you die.

You can choose from:

• A Whole of Life policy – which has a sum assured, paid to the beneficiaries on death. It is written under Trust and it will not be added to your estate, as the money in the Trust doesn’t belong to you, it belongs to the trustees whom you choose.

• A Level Term Assurance is designed to provide a lump sum in the event of death during the term of policy. This makes it a useful option to cover a potential Inheritance Tax liability that would arise should a donor die within seven years of having made a Potentially Exempt Transfer (PET) or Chargeable Lifetime Transfer (CLT).

As with other potential Inheritance Tax solutions, it’s recommended you don’t delay putting a plan into place.According to data provided by Iress on 18 August 2015 – for a £100,000 sum to cover a liability for the rest of their life, with premiums guaranteed – it would cost a 65-year-old male £216 a month to take out a suitable policy. However, if you waited until 80-years-old to take out such a policy, it would cost you £576 a month.

It’s also worth mentioning that these figures are based on a person in standard health. If your health circumstances were to change over the years, these costs could prove even higher.

P.16 Telegraph Inheritance Tax Service

Receive personalised financial advice on tackling your Inheritance Tax liability

As this guide has emphasised there is a lot to think about when it comes to Inheritance Tax. It is such a complex area, and the consequences of ignoring the problem, or getting it wrong, could prove extremely costly and upsetting to your loved ones.

There are a number of ways you could tackle your Inheritance Tax liability, and in some cases you may even be able to eliminate your potential bill altogether. However, the sooner you act, the greater the flexibility you will have.

The first step is to find out if you are likely to be affected – financial advice is strongly recommended.

The Telegraph has recommended the services of Skipton Financial Services Limited (SFS) to our readers since 2004. SFS can provide free, telephone-based information. Should there be a potential liability, you need to decide if you wish to take things further by arranging a face-to-face appointment with an SFS Adviser.

With nearly three decades’ experience, SFS are experts at Inheritance Tax planning. They have Advisers based nationwide who are able to discuss your personal situation and look at the options available to you to mitigate this tax – this includes the new ‘main residence’ nil rate band. You could still retain control of your estate, whilst ensuring the taxman does not take a large slice of what you have spent your lifetime acquiring.

Over the years, SFS has helped thousands of Telegraph readers make suitable plans to address their Inheritance Tax liability – why not see what they can do for you?

Telegraph Inheritance Tax Service P.17

Inheritance Tax planning solutions may put your capital at risk so you may get back less than you originally invested. Inheritance Tax thresholds depend on your individual circumstances and may change in the future. Some areas of Inheritance Tax planning are not regulated by the Financial Conduct Authority.

• An initial telephone-based consultation. They will help you to total up the value of your estate and ask you a few questions about your circumstances. By doing so you can gain an initial idea over whether you might have an Inheritance Tax liability.

• A face-to-face appointment. With SFS Advisers based nationwide, you can meet up with your nearest Adviser at a time and location convenient for you. During this first meeting your SFS Adviser will take the time to get to know you, your full circumstances and your estate aspirations. If they feel that they can help you, they will arrange a second appointment.

• Personalised recommendations. In-between your first and second appointments, your SFS Adviser will spend time researching potential solutions to your Inheritance Tax liability, so they can present you with advice

What an SFS Inheritance Tax review entails:

and recommendations that are tailored to your situation and needs. They can also answer any questions you may have.

• Expertise. SFS Advisers work closely with the Head Office-based Technical team, who are experts in helping clients make suitable plans. Over the years SFS has aided thousands of clients with their Inheritance Tax needs.

• Time and space. You will then be given all the time you need to decide whether to act on this advice. There is no rush, or pressure, to do anything.

• All charges for acting on SFS’s advice will be outlined to you, in writing, before you make any decisions over whether to act. You will never face an unexpected bill for the advice you receive and choose to act upon.

P.18 Telegraph Inheritance Tax Service

For more information about how SFS can help you, either:

Call a member of the Skipton Inheritance Tax Team on

0800 389 8395*

Lines open 9am-7pm, Monday to Thursday, and 9am-5pm on Friday

Complete and detach the reply-slip opposite and return (no stamp required) to:

FREEPOST SFS

Visit telegraph.co.uk/iht

*Service and quality are important to us, that’s why some of our calls are recorded and monitored. Calls are free from a BT landline, costs from other networks and mobiles may vary.

Telegraph Inheritance Tax Service P.19

Inheritance Tax ServicePlease complete all your details below and place in an envelope (no stamp required) and return to FREEPOST SFS.

Name

Address

Postcode

Telephone Number

Email Address~

Mobile~

~Only provide your email address or your mobile number if you would like to be contacted by either of these media.

Marital Status Single Married Widowed Registered Civil Partnership

Date of Birth / /

Total number of Children/Grandchildren

Have you or your partner taken any previous steps to help with your Inheritance Tax planning?

Yes No

Have you or your partner made a Will?

Self Yes No Partner Yes No

How do you rate your need to take definite action to help reduce your eventual Inheritance Tax bill, payable by your beneficiaries?

Wish to take definite action urgently May consider action in the future

Wish to discuss further

IHT2015

Inheritance Tax P.X

Please complete the details of your current estate value below (including your partner’s assets if applicable)

House Value (main residence only) £

Personal Possessions and Valuables + £ i.e. Home contents

Savings and Investments + £ i.e. Banks, Building Societies, National Savings, ISAs, Bonds, Shares etc.

Other Assets + £ i.e. Holiday Home(s)/Investment Property(ies) in the UK/Abroad, Cars, Boats etc.

Business Assets + £ i.e. Part Share in Company/Business, Estimate Value of Holding

Life Assurance + £

Subtract Amount of these Death Benefits Under Trust – £

Total Gross Assets = £

Have you included all joint assets with your partner? Yes No

Subtract Debts – £ i.e. Mortgages, Credit Cards etc.

TOTAL NET ASSETS = £

We respect your privacy and with your permission, Skipton Financial Services Limited would like to send you special offers from time to time. Please tick the relevant boxes if you would like to receive future offers from us by Phone , Letter , Email or SMS .Skipton Financial Services Limited will not pass your details to companies outside the Skipton Group of companies without your consent. If you would like to receive offers from other carefully selected organisations by Phone, Letter, Email or SMS, please tick here .If, at any time you wish to change your marketing contact preferences, or would like a copy of Skipton Financial Services Limited’s Privacy Policy, please contact us on 0800 137 832*, or write to us at Skipton Financial Services Limited, The Bailey, PO Box 101, Skipton, North Yorkshire, BD23 1XT.Skipton Financial Services Limited offers Restricted advice. Registered office: The Bailey, Harrogate Road, Skipton BD23 1DN. Registered in England No. 2061788. Skipton Financial Services Limited is authorised and regulated by the Financial Conduct Authority under register number 100013. Skipton Financial Services Limited is a wholly owned subsidiary of Skipton Building Society.

IHT2015

Inheritance Tax P.X

Telegraph Inheritance Tax Service is provided by Skipton Financial Services Limited who offers Restricted advice. Skipton Financial Services Limited is authorised and regulated by the Financial Conduct Authority under register number 100013 and is a wholly owned subsidiary of Skipton Building Society. Registered office: The Bailey, Harrogate Road, Skipton, North Yorkshire BD23 1DN. Registered in England number 2061788. Telegraph Media Group Limited is an introducer appointed representative of Skipton Financial Services Limited.

TELIHTGUIDE/08/15

*Service and quality are important to us, that’s why some of our calls are recorded and monitored. Calls are free from a BT landline, costs from other networks and mobiles may vary.

For more information about how SFS can help you, either:

Call a member of the Skipton Inheritance Tax Team on

0800 389 8395*

Lines open 9am-7pm, Monday to Thursday, and 9am-5pm on Friday

Complete and detach the reply-slip opposite and return (no stamp required) to:

FREEPOST SFS

Visit telegraph.co.uk/iht