Embed Size (px)

Citation preview

Ingra d.d.

Standalone Financial Statements as at 31 December

2008 together with the Independent Auditors’ Report

Ingra d.d. 31 December 2008

CONTENT

Management’ Report 1 - 2

Responsibility for the financial statements

3

Independent Auditors' report

4-5

Financial statements:

Income statement for the period from 1 January to 31 December 2008 6 Balance sheet for the period from 1 January to 31 December 2008 7

Cash Flow Statement for the period from 1 January to 31 December 2008 8

Statement of changes in equity for the period from 1 January to 31 December 2008

9

Notes to the financial statements 10 - 54

Ingra d.d. 31 December 2008

1

Management' Report

INGRA is a company established in the year 1955, as an export association of industrial manufacturers from ex-

Yugoslavia, with the goal of organising their export activities and commercial development. In 50 years of its

existence, INGRA participated in over 700 investment projects in more than 30 countries worldwide; whose total

value exceeds USD 10 billion.

In cooperation with its members, INGRA was the first company from Central and East Europe to start operating

in Germany 35 years ago. During the eighties, INGRA participated in the construction of two hydroelectric

power plants in the USA. Adapting to market needs and changes of political, economic and legal system in

general, INGRA experienced numerous transformations in the course of its existence.

In the transformation proceedings of INGRA d.d., the Issuer’s share capital was estimated at DEM (German

Mark) 4,000,000.00. Pursuant to the Resolution of the General Meeting of 16 July 2004, by applying the fixed

exchange rate of German Mark and Euro (DEM 1.95583 for EUR 1), the Issuer’s share capital of DEM

4,000,000.00 was converted to equal the sum of EUR 2,045,167.5248, which amounts to equivalent value of

HRK 15,059,503.13 in accordance with the midpoint exchange rate for euro currency of the Croatian National

Bank, valid on the day of adopting the resolution at the General Meeting held on 1 June 2004.

Pursuant to the Resolution of the General Meeting of 16 July 2004, the share capital is increased from HRK

15,059,503.13, for the amount of HRK 44,940,496.87, to HRK 60,000,000.00, divided in 40 000 shares without

par value, fully paid from the Company’s own resources.

In accordance with the Companies’ Act, on 12 January 2006 INGRA’s ordinary shares were enlisted in the

Public Joint Stock Companies Listing of the Zagreb Stock Exchange (JSC market), where they are traded under

the symbol INGR-R-A. Until the mentioned date, trading of INGRA’s shares was limited to official market of

Varaždin Stock Exchange d.d.

Operative and financial review of the financial year

Within the scope of its various present business activities, INGRA has expanded its primary activity of exporting

investment projects for known clients to the marketing of self-funded investment projects. Capital construction

takes the form of “turnkey construction”, and includes construction works, energetic, industry, assembly,

shipbuilding, as well as tourism. Works are performed in cooperation with more than 40 companies.

Apart from the foreign markets, which today include Germany, Algiers, Libya, Middle East, Russia and Niger,

INGRA increasingly participates in large infrastructural projects in Croatia, such as road construction, residential

construction, construction of buildings such as public institutions (hospitals, hotels, embassies etc.) or mobile

networks infrastructure.

In its record year, INGRA rounded up investment cycle started in the year 2006 in the most significant part. in

the three-year-period involving the years 2006, 2007 and 2008, INGRA achieved total revenues above HRK 2.1

billion, while during the year 2008 invested in own investment projects and acquisitions more than HRK 300

million.

4

Independent Auditors’ report

To the Management Board and Shareholders of Ingra d. d.

We have audited the accompanying standalone financial statements of Ingra d.d. Zagreb (hereinafter: the

Company), which comprise the balance sheet as of 31 December 2008, and the income statement,

statements of changes in equity and cash flow for the year then ended, and a summary of significant

accounting policies and other explanatory notes as presented on pages 6 to 54. The standalone financial

statements of the Company as of the year ended 31 December 2007 were audited by another auditor who

issued qualified opinion on 28 May 2008.

Management’s Responsibility for the financial statem ents

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with International Financial Reporting Standards. This responsibility includes: designing,

implementing and maintaining internal control relevant to the preparation and fair presentation of financial

statements that are free from material misstatement, whether due to fraud or error; selecting and applying

appropriate accounting policies; and making accounting estimates that are reasonable in the

circumstances.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted

our audit in accordance with International Standards on Auditing. Those standards require that we comply

with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the

financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

financial statements. The procedures selected depend on the auditor's judgment, including the assessment

of the risks of material misstatement of the financial statements, whether due to fraud or error. In making

those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair

presentation of the financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal

control. An audit also includes evaluating the appropriateness of accounting policies used and the

reasonableness of accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our

audit opinion.

Basis for the Qualified Opinion

a) At the recognition of income and expenses related to construction for other investors, except for its

most significant project – Arena Zagreb, the Company has not complied with the requirements of

International Accounting Standard 11 Construction contracts ("IAS 11"), which include a

requirement for an assessment of contract revenue and expenses to be performed, and for these

to be recognised in profit or loss based on the stage of completion of the contract. IAS 11 also

requires full provision to be made immediately upon identification of any losses expected to arise

on long-term contracts currently in progress, irrespective of their stage of completion.

The Company also did not apply IAS 11 in prior years. Any resulting misstatement of the balance

sheet as at 31 December 2007 would have a consequential impact on the result in 2008.

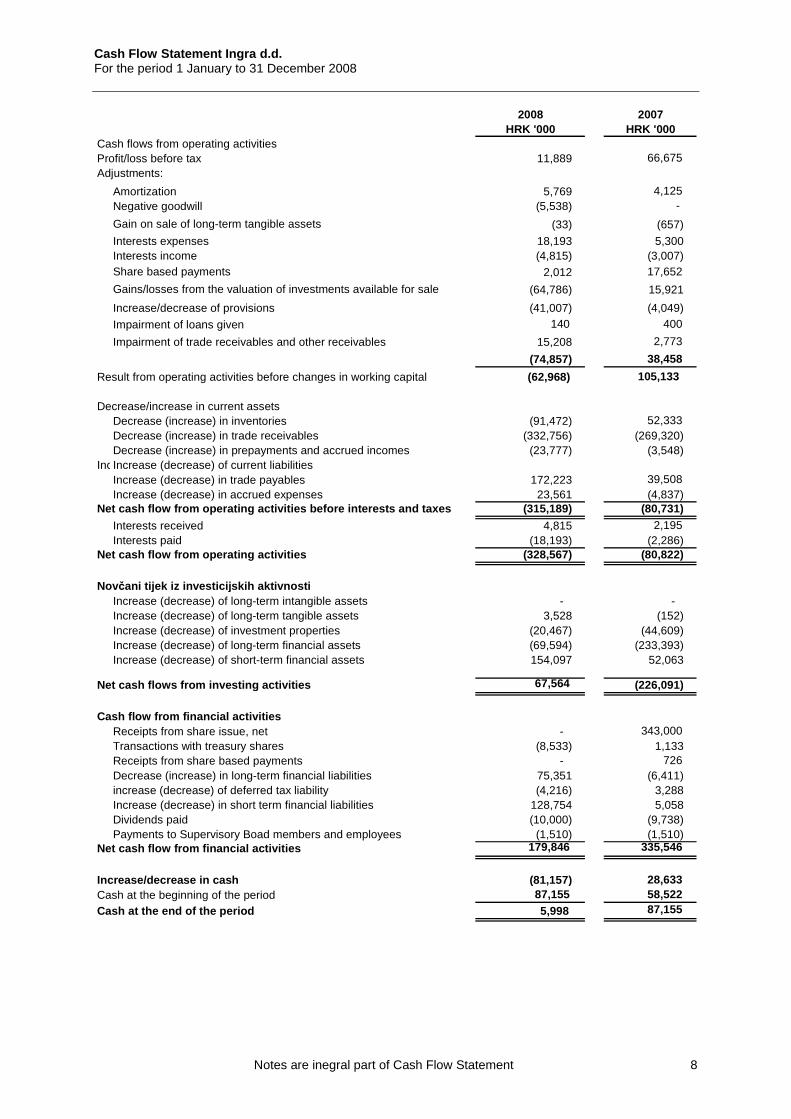

Cash Flow Statement Ingra d.d. For the period 1 January to 31 December 2008

Notes are inegral part of Cash Flow Statement 8

2008 2007HRK '000 HRK '000

Cash flows from operating activitiesProfit/loss before tax 11,889 66,675 Adjustments:

Amortization 5,769 4,125 Negative goodwill (5,538) -

Gain on sale of long-term tangible assets (33) (657)

Interests expenses 18,193 5,300Interests income (4,815) (3,007)Share based payments 2,012 17,652

Gains/losses from the valuation of investments available for sale (64,786) 15,921

Increase/decrease of provisions (41,007) (4,049)

Impairment of loans given 140 400

Impairment of trade receivables and other receivables 15,208 2,773

(74,857) 38,458

Result from operating activities before changes in working capital (62,968) 105,133

Decrease/increase in current assetsDecrease (increase) in inventories (91,472) 52,333 Decrease (increase) in trade receivables (332,756) (269,320)Decrease (increase) in prepayments and accrued incomes (23,777) (3,548)

Increase (decrease) of current liabilitiesIncrease (decrease) of current liabilitiesIncrease (decrease) in trade payables 172,223 39,508 Increase (decrease) in accrued expenses 23,561 (4,837)

Net cash flow from operating activities before inte rests and taxes (315,189) (80,731)

Interests received 4,815 2,195 Interests paid (18,193) (2,286)

Net cash flow from operating activities (328,567) (80,822)

Novčani tijek iz investicijskih aktivnostiIncrease (decrease) of long-term intangible assets - - Increase (decrease) of long-term tangible assets 3,528 (152)Increase (decrease) of investment properties (20,467) (44,609)Increase (decrease) of long-term financial assets (69,594) (233,393)Increase (decrease) of short-term financial assets 154,097 52,063

Net cash flows from investing activities 67,564 (226,091)

Cash flow from financial activitiesReceipts from share issue, net - 343,000 Transactions with treasury shares (8,533) 1,133Receipts from share based payments - 726 Decrease (increase) in long-term financial liabilities 75,351 (6,411)increase (decrease) of deferred tax liability (4,216) 3,288Increase (decrease) in short term financial liabilities 128,754 5,058Dividends paid (10,000) (9,738)Payments to Supervisory Boad members and employees (1,510) (1,510)

Net cash flow from financial activities 179,846 335,546

Increase/decrease in cash (81,157) 28,633 Cash at the beginning of the period 87,155 58,522 Cash at the end of the period 5,998 87,155

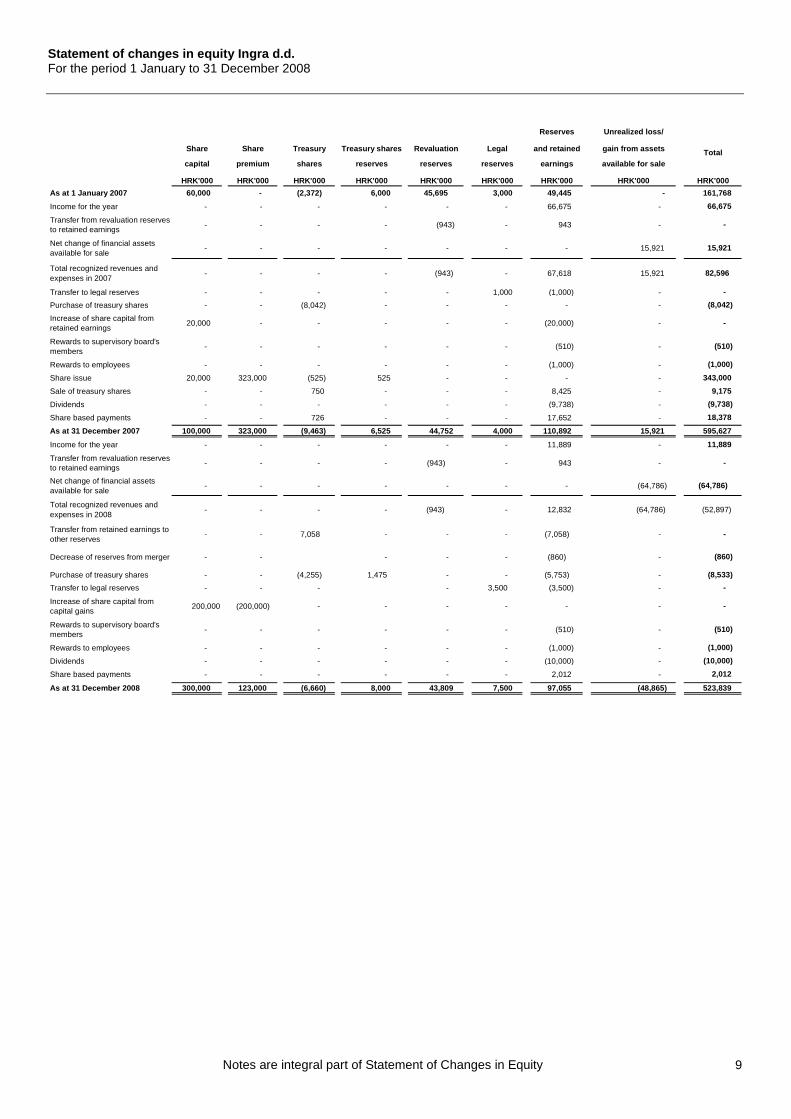

Statement of changes in equity Ingra d.d. For the period 1 January to 31 December 2008

Notes are integral part of Statement of Changes in Equity 9

Reserves Unrealized loss/

Share Share Treasury Treasury shares Revaluation Legal an d retained gain from assets

capital premium shares reserves reserves reserves earning s available for sale

HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HRK'000 HR K'000 HRK'000

As at 1 January 2007 60,000 - (2,372) 6,000 45,695 3,000 49,445 - 161,768

Income for the year - - - - - - 66,675 - 66,675

Transfer from revaluation reserves to retained earnings

- - - - (943) - 943 - -

Net change of financial assets available for sale

- - - - - - - 15,921 15,921

Total recognized revenues and expenses in 2007

- - - - (943) - 67,618 15,921 82,596

Transfer to legal reserves - - - - - 1,000 (1,000) - -

Purchase of treasury shares - - (8,042) - - - - - (8,042)

Increase of share capital from retained earnings

20,000 - - - - - (20,000) - -

Rewards to supervisory board's members

- - - - - - (510) - (510)

Rewards to employees - - - - - - (1,000) - (1,000)

Share issue 20,000 323,000 (525) 525 - - - - 343,000

Sale of treasury shares - - 750 - - - 8,425 - 9,175

Dividends - - - - - - (9,738) - (9,738)

Share based payments - - 726 - - - 17,652 - 18,378

As at 31 December 2007 100,000 323,000 (9,463) 6,525 44,752 4,000 110,892 15,921 595,627

Income for the year - - - - - - 11,889 - 11,889

Transfer from revaluation reserves to retained earnings

- - - - (943) - 943 - -

Net change of financial assets available for sale

- - - - - - - (64,786) (64,786)

Total recognized revenues and expenses in 2008

- - - - (943) - 12,832 (64,786) (52,897)

Transfer from retained earnings to other reserves

- - 7,058 - - - (7,058) - -

Decrease of reserves from merger - - - - - (860) - (860)

Purchase of treasury shares - - (4,255) 1,475 - - (5,753) - (8,533)

Transfer to legal reserves - - - - 3,500 (3,500) - -

Increase of share capital from capital gains

200,000 (200,000) - - - - - - -

Rewards to supervisory board's members

- - - - - - (510) - (510)

Rewards to employees - - - - - - (1,000) - (1,000)

Dividends - - - - - - (10,000) - (10,000)

Share based payments - - - - - - 2,012 - 2,012

As at 31 December 2008 300,000 123,000 (6,660) 8,000 43,809 7,500 97,055 (48,865) 523,839

Total

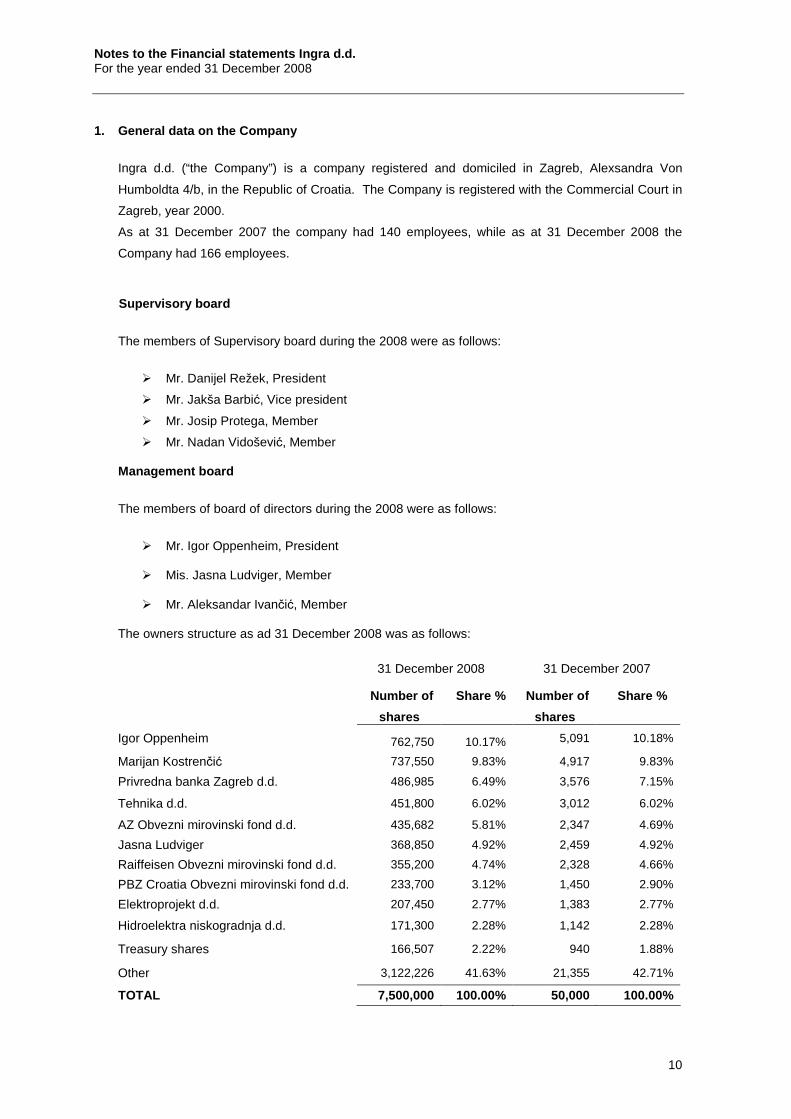

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

10

1. General data on the Company

Ingra d.d. (“the Company”) is a company registered and domiciled in Zagreb, Alexsandra Von

Humboldta 4/b, in the Republic of Croatia. The Company is registered with the Commercial Court in

Zagreb, year 2000.

As at 31 December 2007 the company had 140 employees, while as at 31 December 2008 the

Company had 166 employees.

Supervisory board

The members of Supervisory board during the 2008 were as follows:

� Mr. Danijel Režek, President

� Mr. Jakša Barbić, Vice president

� Mr. Josip Protega, Member

� Mr. Nadan Vidošević, Member

Management board

The members of board of directors during the 2008 were as follows:

� Mr. Igor Oppenheim, President

� Mis. Jasna Ludviger, Member

� Mr. Aleksandar Ivančić, Member

The owners structure as ad 31 December 2008 was as follows:

31 December 2008 31 December 2007

Number of

shares

Share % Number of

shares

Share %

Igor Oppenheim 762,750 10.17% 5,091 10.18%

Marijan Kostrenčić 737,550 9.83% 4,917 9.83%

Privredna banka Zagreb d.d. 486,985 6.49% 3,576 7.15%

Tehnika d.d. 451,800 6.02% 3,012 6.02%

AZ Obvezni mirovinski fond d.d. 435,682 5.81% 2,347 4.69%

Jasna Ludviger 368,850 4.92% 2,459 4.92%

Raiffeisen Obvezni mirovinski fond d.d. 355,200 4.74% 2,328 4.66%

PBZ Croatia Obvezni mirovinski fond d.d. 233,700 3.12% 1,450 2.90%

Elektroprojekt d.d. 207,450 2.77% 1,383 2.77%

Hidroelektra niskogradnja d.d. 171,300 2.28% 1,142 2.28%

Treasury shares 166,507 2.22% 940 1.88%

Other 3,122,226 41.63% 21,355 42.71%

TOTAL 7,500,000 100.00% 50,000 100.00%

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

11

2. Summary of accounting policies

General

The financial statements have been prepared in accordance with the requirements of the

International Financial Reporting Standards (IFRS) issued by the International Accounting Standards

Committee (IASB). The financial statements for the year 2008 have been prepared using the

historical cost convention except for any financial assets and liabilities stated at fair value in

accordance with IAS 39 “Financial Instruments: Recognition and Measurement”. The accounting

policies have been consistently applied, except where disclosed otherwise. The financial statements

are prepared on a going concern basis.

The Company's consolidated financial statements and its subsidiaries that the Company has to

provide in accordance with IFRS and the Croatian law, will be issued as a separate document shortly

after the publication of these unconsolidated financial statements.

These financial statements were authorised for issue by the Management Board on 18 May 2009.

The financial statements are denominated in Croatian Kuna (HRK). At 31 December 2008, the

exchange rate for USD 1 and EUR 1 was HRK 5.16 and HRK 7.32, respectively (31 December 2007:

HRK 4.99 and HRK 7.33 respectively).

Estimates and judgements

In the preparation of financial statements the managements used certain judgements, estimations

and assumptions which affect reporting amounts of assets and liabilities, disclosure of contingent

items at the reporting date and income and expenses for the period then ended.

Estimates and associated assumptions are used, but not limited to, for: calculation and depreciation

period and residual values for property, plant and equipment and intangible assets, impairment,

value adjustments for inventory and doubtful receivables and provisions. More details on the

accounting policies for there estimates are presented in the other parts of this note as well in other

parts of notes to financial statements. Future events and their influence cannot be predicted with the

certainty. Therefore accounting estimates and underlying assumptions require judgement, and those

used in the preparation of the financial statements are subject to changes due to occurrence of new

events, gaining of additional experience, new information and changes in environment in which the

Company operates. Actual results may differ from these estimates.

The basic of Company's financial statements

The basic accounting policies used for the preparation of the financial statements are presented in

the following items:

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

12

a) Property, plant and equipment

Items of property, plant and equipment, except for land, are measured at cost less accumulated

depreciation and accumulated impairment losses. Cost includes expenditure that is directly attributable

to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and

direct labour, any other costs directly attributable to bringing the asset to a working condition for its

intended use, and the costs of dismantling and removing the items and restoring the site on which they

are located.

Gains and losses on disposal of an item of property, plant and equipment are recognised net within

“other operating income” in profit or loss. When revaluated assets are sold, the amounts included in

the revaluation surplus reserve are transferred to retained earnings

The cost of replacing part of an item of property, plant and equipment is recognised in the carrying

amount of the item if it is probable that the future economic benefits embodied within the part will flow to

the Company and its cost can be measured reliably. The costs of the day-to-day servicing of property,

plant and equipment are recognised in profit or loss as incurred.

Following initial recognition at cost, land is carried at a revaluated amount which is the fair value at the

date of the revaluation less any subsequent accumulated impairment losses.

Independent evaluation of land value is performed when carrying value significantly differ from fair

value.

Any revaluation surplus is credited to the revaluation reserve included in the equity unless, and limited

to the amount in which, it cancels the decrease in the value of the same asset which was previously

recognized as and expenses and then it is recognized as income.

If the carrying amount of the item decreased as a result of revaluation, this decrease should be

recognized as an expense. An annual transfer from the asset revaluation reserve is made to retained

earnings for the depreciation relating to the revaluation surplus. Related part of revaluation reserves

created from the earlier asset revaluation is transferred from revaluation reserves directly to retained

earnings, after asset derecognition.

Depreciation is recognised in profit or loss on a straight-line basis over the estimated useful lives of

each part of an item of property, plant and equipment. Depreciation of an asset starts when the assets

are available for use. Land and assets in the course of construction are not depreciated. The estimated

useful lives are as follows:

Buildings 40 years

Plant and equipment 2-10 years

Vehicles, furniture and office equipment 4 years

Depreciation is calculated on the separate asset items until they are fully depreciated.

Following initial recognition at cost, buildings are carried at a revaluated amount which is the fair value

at the date of the revaluation less any subsequent accumulated depreciation on buildings and

accumulated impairment losses.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

13

Fair value is determined by reference to market-based evidence, which is the amount for which the

assets could be exchanged between a knowledgeable willing buyer and a knowledgeable willing seller

in an arm’s length transaction as at the valuation date.

Any revaluation surplus is credited to the asset revaluation reserve included in the equity section of the

balance sheet. If the carrying amount of the item increased as a result of revaluation, this increase

should be recognised as an income in the amount for which it cancels revaluation decrease of the

same asset, which was previously recognized as an expense.

If the carrying amount of the item decreased as a result of revaluation, this decrease should be

recognized as an expense. Revaluation decrease is recognised directly in the revaluation reserve

unless it exceeds the revaluation reserve of the same asset.

An annual transfer from the asset revaluation reserve is made to retained earnings for the depreciation

relating to the revaluation surplus. In addition, any accumulated depreciation at revaluation date is

eliminated against the gross carrying amount of the asset and the net amount is restated to the

revaluated amount of the asset.

Upon derecognition of an asset or disposal, any revaluation reserve relating to the particular asset is

transferred to retained earnings.

Impairment of tangible and intangible assets excluding goodwill

At each balance sheet date, the Company reviews the carrying amount of its tangible and intangible

assets to determine whether there is any indication that those assets have suffered an impairment loss.

If any such indication exists, the recoverable amount of the asset is estimated in order to determine the

extent of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of the

individual asset, the Company estimated the recoverable amount of the cash-generating unit to which

the asset belongs. Where a reasonable and consistent basis of allocation can be identified, corporate

assets are also allocated to individual cash-generating units, or otherwise they are allocated to the

smallest Company’s cash-generating units for which a reasonable and consistent allocation basis can

be identified.

Intangible assets with indefinite useful lives and intangible assets not yet available for use are tested for

impairment annually, and when ever there is an indication that the asset may be impaired.

Recoverable amount is higher of fair value less costs to sell and value in use. In assessing value in

use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate

that reflects current market assessments of the time value of money and the risks specific to the asset

for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying

amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable

amount. An impairment loss is recognized immediately in profit or loss, unless the relevant asset is

carried at a revaluated amount, in which case the impairment loss is treated as a revaluation decrease.

b) Investment property

Investment property is property held either to earn rental income or for capital appreciation or both.

Investment property is initially measured at cost. After initial recognition, investment property is

measured at cost less accumulated depreciation and accumulated impairment losses.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

14

Cost includes purchase price and expenditure that is directly attributable to the acquisition of the asset.

Investment property in progress is classified as property, plant and equipment, except land which is

immediately recognised as investment property. Land is not amortised. After putting into use,

investment property will be depreciated over the useful economic life.

c) Investment in subsidiares

Subsidiaries are entities in which the Company has the power, directly or indirectly, to exercise control

over their operations. Control is achieved where the Company has the power to govern the financial

and operating policies of an entity so as to obtain benefit from its activities. Investments in subsidiaries

are stated at cost.

d) Investment in associates

Associates are those entities in which the Company has significant influence, but not control. Significant

influence is presumed to exist when the Company has influence over the financial and operating

policies of the associate, but does not have control or joint control on chosen policies. Associates are

initially recognised at cost.

e) Inventories

Inventories are stated at the lower of cost and net realisable value. Raw materials, spare parts and

small tools are stated at purchase price. The cost of materials is based on the weighted average

method. Small tools are written off as they are put into use.

Inventories of work in progress and trading goods are stated at the lower of cost, or net realisable

value. Cost includes expenditure incurred in acquiring the inventories and bringing them to their existing

condition and location.

f) Receivables

Receivables represent the right to collect determined amounts from customers or other debtors with

regard to the company's operations. Receivables are reported in the total amount and decreased by the

provisions for doubtful and bad debts. Bad debt provisions are made when collection of a part or a total

of this receivable is uncertain based on the Management’s estimation.

g) Cash and cash equivalents

Cash and cash equivalents consist of deposits, balances in banks and similar institutions and cash on

hand. This item includes cash immediately available and utilizable and is characterized by its absence

of collection risk and collection accessory charges.

h) Revenue recognition

Sales, which are reported net of returns, discounts and bonuses, as well as net of taxes directly

connected with the sale of products and services rendered, represent amounts invoiced to third parties.

Revenue is recognized at the time delivery has taken place and transfer of risks and rewards has been

completed.

Sale of goods

Revenue from the sale of goods is recognized when all the following conditions are satisfied:

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

15

� The company has transferred to the buyer the significant risks and rewards of ownership of the

goods;

� The company retains neither continuing managerial involvement to the degree usually associated

with ownership nor effective control over the goods sold;

� The amount of revenue can be measured reliably;

� It is probable that the economic benefits associated with the transaction will flow to the entity; and

� The costs incurred in respect of the transaction can be measured reliably.

i) Use of estimates and judgements

The preparation of financial statements in conformity with IFRSs requires management to make

judgements, estimates and assumptions that affect the application of policies and reported amounts of

assets and liabilities, income and expenses.

The estimates and associated assumptions are based on historical experience and various other

factors that are believed to be reasonable under the circumstances, the results of which form the basis

of making the judgements about carrying values of assets and liabilities that are not readily apparent

from other sources. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting

estimates are recognised in the period in which the estimate is revised if the revision affects only that

period or in the period of revision and future periods if the revision affects both current and future

periods.

Judgements made by management in the application of IFRS that have significant effect on the

amounts recognised in the financial statements and judgements which involve a risk of causing a

material adjustment within the next financial year are high, are also disclosed in Note 39.

j) Foreign currency translation

Assets and liabilities reported in foreign currencies are translated into Kuna’s by using Croatian

National Bank’s mid exchange rate as of the end of the year. Foreign exchange gains or losses are

included in the profit and loss statement as incurred.

k) Loans received

Interest-bearing bank loans and overdrafts are recorded on the basis of received amount decreased for

direct cost needed for their approval. Financial costs, including premium paid on the settlement or

withdrawals are recorded on accrual basis and added to the carrying value of the instrument, only for

the un-settled amount in period in which they occurred.

l) Provisions

Provisions are recognized when the Company has a present obligation (legal or constructive) as a

result of a past event, it is probable that the Company will be required to settle the obligation, and a

reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimated of the consideration required to settle the

present obligation at the balance sheet date, taking into account the risks and uncertainties surrounding

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

16

the obligation. Where a provision is measured using the cash flows estimated to settle the present

obligation, its carrying amount is the present value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered

from a third party, the receivable is recognized as an asset if it is virtually certain that reimbursement

will be received and the amount of the receivable can be measured reliably.

m) Employee benefits

(i) Defined pension fund contributions

Obligations for defined contributions to pension funds are recognised as an expense in the income

statement when incurred.

(ii) Bonus plans

A liability for employee benefits is recognised in provisions based on the Company’s formal plan and

when past practice has created a valid expectation by the Management Board/key employees that they

will receive a bonus and the amount can be determined before the time of issuing the financial

statements.

Liabilities for bonus plans are expected to be settled within 12 months of the balance sheet date and

are measured at the amounts expected to be paid when they are settled.

(iii) Share based payment transactions

The Company operates a number of equity-settled, share-based compensation plans. The total amount

to be expensed over the vesting period and the amount that is credited to the share capital is

determined by reference to the fair value of the options granted. The fair value of the equity accounted

instruments is measured at the grant date. At each balance sheet date, the entity revises its estimates

of the number of options that are expected to vest.

n) Taxes

The Company provides for taxation liabilities in accordance with Croatian law. Corporate tax for the

year comprises current and deferred tax.

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted at

the balance sheet date.

Deferred tax reflects the net tax effect of the temporary differentials between the book values of the

assets and the liabilities for the purpose of the financial reporting and the values used for the purpose

of establishing profit tax. A deferred tax asset for the carry-forward of unused tax losses and unused tax

credits is recognized to the extent that it is probable that future taxable profit will be available against

which the unused tax losses and unused tax credits can be utilized. Deferred tax assets and liabilities

are calculated using the tax rate applicable to the taxable profit in the years in which these assets and

liabilities are expected to be collected or paid.

Current and deferred tax are recognized as an expense or income in profit or loss, except when they

relate to items credited or debited directly to equity, in which case the tax is also recognized directly in

equity.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

17

o) Earnings per share

The Company presents basic earnings per share data for its ordinary shares. Basic earnings per share

is calculated by dividing the profit or loss attributable to ordinary shareholders of the Company by the

weighted average number of ordinary shares outstanding during the period.

p) Segment reporting

A segment is a distinguishable component of the Company that is engaged either in providing related

products or services (business segment), or in providing products or services within a particular

economic environment (geographical segment), which is subject to risks and rewards that are different

from those of other segments. The Company’s primary format for segment reporting is based on

geographical segments.

q) Leases

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the

risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

Assets held under finance leases are initially recognised as assets of the Company at their fair value at

the inception of the lease or, if lower, at the present value of the minimum lease payments. The

corresponding liability to the lessor is included in the balance sheet as a finance lease obligation.

Lease payments are apportioned between finance charges and reduction of the lease obligations so as

to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are

charged directly to profit or loss.

Operating lease payments are recognized as an expense on a straight-line basis over the lease term.

r) Finance income and expenses

Finance income and expenses comprises interest income on loans and borrowings using the effective

interest method, interest income on funds invested, dividend income, foreign currency losses and

gains, gains and losses from changes in the fair value of financial assets at fair value through profit or

loss.

Interest income is recognised as it accrues in profit or loss, using the effective interest method.

Dividend income is recognised on the date that the Company’s right to receive payment is established.

Finance expenses comprise interest expense on borrowings, foreign currency losses, changes in the

fair value of financial assets at fair value through profit or loss and impairment losses recognised on

financial assets. All borrowing costs are recognised in profit or loss using the effective interest method.

s) Dividends

Dividends are recognised in the statement of changes in equity and recorded as liabilities in the period

in which they are approved by the Company’s shareholders.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

18

t) Financial assets and financial liabilities

Financial assets

Investments are recognized and derecognized on trade date where the purchase or sale of an

investment is under a contract whose terms require delivery of the investment within the timeframe

established by the market concerned, and are initially measured at fair value, plus transaction costs,

except for those financial assets classified as at fair value through profit or loss, which are initially

measured at fair value.

Financial assets are classified into the following specified categories:

• “At fair value through profit or loss” (FVTPL)

Financial assets are classified as at FVTPL where the financial asset is either held for trading or it is

designated as at FVTPL. A financial asset is classified as held for trading if:

1. it has been acquired principally for the purpose of selling in the near future; or

2. it is a part of identified portfolio of financial instruments that the Company manages

together and has a recent actual pattern of short-term profit-taking; or

3. it is a derivative that is not designated and effective as a hedging instrument.

Financial assets at FVTPL are stated at fair value, with any resultant gain or loss recognized in profit or

loss. The net gain or loss recognized in profit or loss incorporates any dividend or interest method less

any impairment, with revenue recognized on an effective yield basis.

• “Held-to-maturity”

Bills of exchange and debentures with fixed or determinable payments and fixed maturity dates that the

Company has the positive intent and ability to hold to maturity are classified as held-to-maturity

investments. Held-to-maturity investments are recorded at amortized cost using the effective interest

method less any impairment, with revenue recognized on an effective yield basis.

• “Available for sale” (AFS)

Unlisted shares and listed redeemable notes held by the Company that are traded in an active market

are classified as being AFS and are stated at fair value. Gains and losses arising from changes in fair

value are recognized directly in equity in the investments revaluation reserve with the exception of

impairment losses, interest calculated using the effective interest method and foreign exchange gains

and losses on monetary assets, which are recognized directly in profit or loss. Where the investment is

disposed of or is determined to be impaired, the cumulative gain or loss previously recognized in the

investment revaluation reserve is included in profit or loss for the period.

Dividends on AFS equity instruments are recognized in profit or loss when the Company’s right to

receive the dividends is established.

The fair value of AFS monetary assets denominated in a foreign currency is determined in that foreign

currency and translated at the spot rate at the balance sheet date. The change in fair value attributable

to translation differences that result from a change in amortised cost of the asset is recognized in profit

or loss, and other changes are recognized in equity.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

19

• “Loans and receivables”

Trade receivables, loans, and other receivables that have fixed or determinable payments that are not

quoted in an active market are classified as loans and receivables. Loans and receivables are

measured at amortised cost using the effective interest method, less any impairment. Interest income is

recognized by applying the effective interest rate, except for short-term receivables when the

recognition of interest would be immaterial.

Impairment of financial assets

Financial assets, other than those at FVTPL, are assessed for indicators of impairment at each balance

sheet date. Financial assets are impaired where there is objective evidence that, as a result of one or

more events that occurred after the initial recognition of the financial asset, the estimated future cash

flows or the investment have been impacted.

For unlisted shares classifies as AFS a significant or prolonged decline in the fair value of the security

below its cost is considered to be objective evidence of impairment.

For all other financial assets, including redeemable notes classifies as AFS and finance lease

receivables, objective evidence of impairment could include:

• Significant financial difficulty of the issuer or counterparty; or

• Default or delinquency in interest or principal payments; or

• It becoming probable that the borrower will enter bankruptcy or financial re-organisation.

For certain categories of financial asset, such as trade receivables, assets that are assessed not to be

impaired individually are subsequently assessed for impairment on a collective basis. Objective

evidence of impairment for a portfolio of receivables could include the Company’s past experience of

collecting payments, an increase in number of delayed payments in the portfolio past the average credit

period of 60 days, as well as observable changes in national or local economic conditions that correlate

with default on receivables.

For financial assets carried at amortised cost, the amount of the impairment is the difference between

the asset’s carrying amount and the present value of estimated future cash flow, discounted at the

financial asset’s original effective interest rate.

The carrying amount of the financial assets is reduced by the impairment loss directly for all financial

assets with the exception of trade receivables, where the carrying amount is reduced through the use of

an allowance account. When a trade receivable is considered uncollectible, it is written off against the

allowance account. Subsequent recoveries of amounts previously written off are credited against the

allowance account. Changes in the carrying amount of the allowance account are recognised in profit

or loss.

With the exception of AFS equity instruments, if in a subsequent period, the amount of the impairment

loss decreases and the decrease can be related objectively to an event occurring after the impairment

was recognised, the previously recognised impairment loss is reversed trough profit or loss to the

extent that the carrying amount of the investment at the date the impairment is reversed does not

exceed what the amortised cost would have been had the impairment not been recognised.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

20

In respect of AFS equity securities, impairment losses previously recognised through profit or loss are

not reversed trough profit or loss. Any increase in fair value subsequent to an impairment loss is

recognised directly in equity.

De-recognition of financial assets

The Company derecognises a financial asset only when the contractual rights to the cash flows from

the asset expire; or it transfers the financial asset and substantially all the risks and rewards of

ownership of the asset to another entity. If the Company neither transfers nor retains substantially all

the risks and rewards of ownership and continues to control the transferred asset, the Company

recognises its retained interest in the asset and an associated liability for amounts it may have to pay. If

the Company retains substantially all the risks and reward ownership of a transferred financial asset,

the Company continues for recognise the financial asset and also recognises a collateralised borrowing

for the proceeds received.

Financial liabilities and equity instruments issued by the Company

Classification as debt or equity

Debt and equity instruments are classified as either financial liabilities or as equity in accordance with

the substance of the contractual arrangement.

Equity instruments

An equity instruments is any contract that evidences a residual interest in the assets of an entity after

deducting all of its liabilities. Equity instruments issued by the Company are recorded at the proceeds

received, net of direct issue costs.

Compound instruments

The component parts of compound instruments issued by the Company are classified separately as

financial liabilities and equity in accordance with the substance of the contractual arrangement. At the

date of issue, the fair value of the liability component is estimated using the prevailing market interest

rate for a similar non-convertible instrument. This amount is recorded as a liability on an amortised cost

basis using the effective interest method until extinguished upon conversion or at the instrument’s

maturity date. The equity component is determined by deducting the amount of the liability component

from the fair value of the compound instrument as a whole. This is recognised and included in equity,

net of income tax effects, and is not subsequently remeasured.

Share capital

a. Ordinary shares

Incremental costs directly attributable to issue of ordinary shares are recognised as a deduction

from equity.

b. Repurchase of share capital

When share capital recognised as equity is repurchased, the amount of the consideration paid,

including directly attributable costs, is recognised as a deduction from equity. Repurchased shares

are classified as treasury shares and are presented as a deduction from total equity.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

21

Financial guarantee contract liabilities

Financial guarantee contract liabilities are measured initially at their fair values and are subsequently

measured at the higher of:

• the amount of the obligation under the contract, as determined in accordance with IAS 37

Provisions, Contingent Liabilities and Contingent Assets; and

• the amount initially recognised less, where appropriate, cumulative amortisation recognised in

accordance with the revenue recognition policies (dividend and interest revenue).

Financial liabilities at FVTPL

Financial liabilities are classified as at FVTLP where the financial liability is either held for trading or it is

designated as at FVTPL.

A financial liability is classified as held for trading if:

• it has bees incurred principally for the purpose of repurchasing in the near future: or

• it is a part of an identified portfolio of financial instruments that the Company manages together

and has a recent actual pattern of short-term profit-taking; or

• it is derivative that is not designated and effective as a hedging instrument.

A financial liability other than a financial liability held for trading may be designated as at FVTPL upon

initial recognition if:

• Such designation eliminates or significantly reduces a measurement or recognition

inconsistency that would otherwise arise; or

• The financial liability forms part of a group of financial assets or financial liabilities or both,

which is managed and its performance is evaluated on a fair value basis, in accordance with

the Company’s documented risk management or investment strategy, and information about

the grouping is provided internally on that basis; or

• It forms part of a contract containing one or more embedded derivatives, and IAS 39 Financial

Instruments: Recognition and Measurement permits the entire combined contract (asset or

liability) to be designated as at FVTPL.

Financial liabilities at FVTPL are stated at fair value, with any resultant gain or loss recognised in profit

or loss. The net gain or loss recognised in profit or loss incorporates any interest paid on the financial

liability.

Other financial liabilities

Other financial liabilities, including borrowings, are initially measured at fair value, net of transaction

cost.

Other financial liabilities are subsequently measured at amortised cost using the effective interest

method, with interest expense recognised on an effective yield basis.

The effective interest method is a method of calculating the amortised cost of a financial liability and of

allocating interest expense over the relevant period. The effective interest rate is the rate that exactly

discounts estimate future cash payments through the expected life of the financial liability, or, where

appropriate, a shorter period.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

22

De-recognition of financial liabilities

The Company derecognise financial liabilities when, and only when, the Company’s obligations are

discharged, cancelled or they expire

u) Contingent assets and liabilites

Contingent liabilities are not recognised in financial statements. They are published in notes only if cast

of economical benefits isn't possible.

Contingent assets isn't expressed in financial statement, already is expressed when the intakes of

economical benefits is possible.

v) Subsequent events

Post-year-end events that provide additional information about the Company’s position at the balance

sheet date (adjusting events) are reflected in the financial statements.

Post-year-end events that are not adjusting events are disclosed in the notes when material.

w) Comparatives

Comparative figures have been adjusted to conform to presentation in the current year, where

necessary.

x) Adoption of International Financial Reporting Sta ndards (IFRS) during the year

The Company has applied in the year 2008 the following amendments and interpretations issued which

are or have become effective during the year and presented, in accordance with the requirements,

comparative data. The application of the new standards had no effect on the capital as at 1 January

2008:

• IAS 39 (amendments) „Financial instruments: Recognition and measurement“ and IFRS 7

(amendments) „Financial instruments: Disclosure – Reclassification of Financial Assets“ (by

those amendments reclassification of financial assets made before 1 November 2008 is

permitted, with the earliest application starting from 1 July 2008)

The following three interpretations issued by International Financial Reporting Interpretations

Committee – IFRIC are effective for the current reporting period: IFRIC 11 “Group and Treasury

Transactions”, IFRIC 12 “Service concession Arrangements”, IFRIC 14 “The limit on a Defined Benefit

Asset, Minimum Funding Requirements and their Interaction“. Application of these interpretations has

not effected Company' accounting policies.

The Company reclassified part of its financial assets “At fair value through profit and loss” from that

position to the balance sheet position “Available for sale” financial assets. Reclassification effect

amounted to HRK 5,476 thousand (income before tax would be lower for that amount).

y) Standards and interpretations which are not appl ied yet

On the date of the Financial Statements' approval the following new and revised standards,

amendments and interpretations have been issued but were not effective yet for the financial year

ended 31 December 2008:

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

23

New standard:

• IFRS 8 “Operating Segments” (effective for accounting periods beginning on or after 1 January

2009),

Amendments to standards:

• Improvements to IFRSs (effective for accounting periods beginning on or after 1 January 2009,

except for the amendment to IFRS 5 „Non-current Assets Held for Sale and Discontinued

Operations“ which is effective for annual periods beginning on or after 1 July 2009).

Improvements include 35 amendments which can be divided as follows:

• 1st part – amendments that result in accounting changes for presentation, recognition and

measurement purposes, and

• 2nd part – amendments that are terminology or editorial changes only, that have no or minimal

effect on accounting.

• IFRS 1 (amended) „First-time Adoption of IFRSs (effective for the accounting periods

beginning on or after 1 January 2009),

• IFRS 2 (amended) „Share-based Payment“, (effective for the accounting periods beginning on

or after 1 January 2009),

• IAS 27 (amended) „Consolidated and Separate Financial Statements“ (effective for the

accounting periods beginning on or after 1 January 2009)

• IAS 32 (amended) „Financial Instruments: Presentation – Puttable Financial Instruments and

Obligations Arising on Liquidation“ (effective for accounting periods beginning on or after 1

January 2009)

• IAS 39 (amended) „Financial Instruments: Recognition and Measurement – Eligible Hedged

Items“ (effective for accounting periods beginning on or after 1 July 2009)

Revised standards:

• IFRS 3 (revised) „Business Combinations“ (effective for accounting periods beginning on or

after 1 July 2009)

• IAS 1 (revised) „Presentation of Financial Statements“ (effective for accounting periods

beginning on or after 1 January 2009)

• IAS 23 (revised) “Borrowing Costs” (effective for the accounting periods beginning on or after 1

January 2009)

• IAS 27 (revised) „Consolidated and Separate Financial Statements“ (effective for the

accounting periods beginning on or after 1 July 2009)

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

24

New interpretations:

� IFRIC 13 “Customer Loyalty Programmes” (effective for accounting periods beginning on or

after 1 July 2008),

� IFRIC 15 „Agreements for the Construction of Real Estate“ (effective for accounting periods

beginning on or after 1 January 2009)

� IFRIC 16 „Hedges of a Net Investment in a Foreign Operation“ (effective for accounting periods

beginning on or after 1 October 2009)

� IFRIC 17 „Distribution of Non-cash Assets to Owners“ (effective for accounting periods

beginning on or after 1 July 2009)

The Management anticipate that the application of the above mentioned standards and interpretations

will be applied in the Company' Financial Statements for the periods for which they become effective,

and that this application will have no material impact on the Company's Financial Statements in the

periods for which they are applied

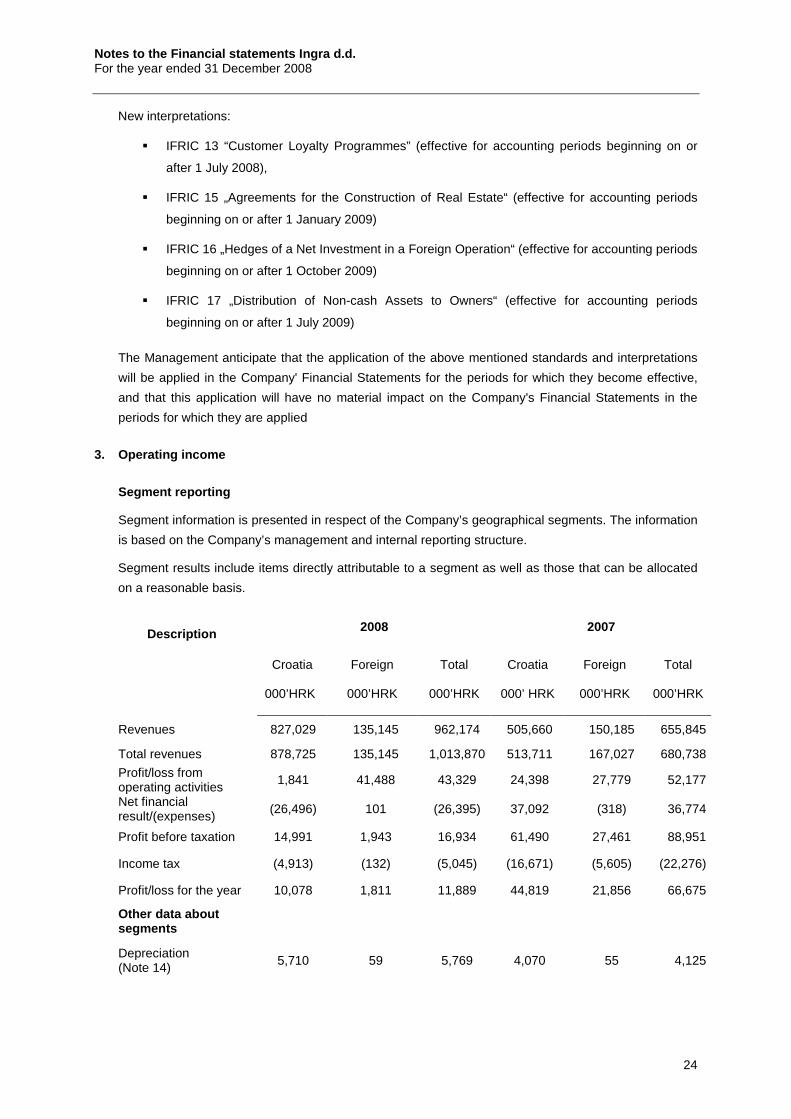

3. Operating income

Segment reporting

Segment information is presented in respect of the Company’s geographical segments. The information

is based on the Company’s management and internal reporting structure.

Segment results include items directly attributable to a segment as well as those that can be allocated

on a reasonable basis.

Description 2008

2007

Croatia

000’HRK

Foreign

000’HRK

Total

000’HRK

Croatia

000’ HRK

Foreign

000’HRK

Total

000’HRK

Revenues 827,029 135,145 962,174 505,660 150,185 655,845

Total revenues 878,725 135,145 1,013,870 513,711 167,027 680,738

Profit/loss from operating activities

1,841 41,488 43,329 24,398 27,779 52,177

Net financial result/(expenses)

(26,496) 101 (26,395) 37,092 (318) 36,774

Profit before taxation 14,991 1,943 16,934 61,490 27,461 88,951

Income tax (4,913) (132) (5,045) (16,671) (5,605) (22,276)

Profit/loss for the year 10,078 1,811 11,889 44,819 21,856 66,675

Other data about segments

Depreciation (Note 14) 5,710 59 5,769 4,070 55

4,125

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

25

Since the Company does not allocate assets and liabilities based on individual business segments, the

Management Board has not presented information on assets and liabilities based on geographical

segments.

4. Other operating income

2008

HRK’000

2007

HRK’000

Rental income 2,824 2,544

Excess of fair value of acquired assets over the consideration given (negative goodwill) 5,538 -

Income from contingent assets recognised - 14,956

Collection of previously impaired trade receivables - 590

Release of provision for court cases 41,007 4,581

Net gain on sale of property, plant and equipment 33 657

Other 2,294 1,565

51,696 24,893

Excess of the fair value of acquired assets over the consideration given (negative goodwill) in the

amount of HRK 5,538 thousand is the result of merger of the related company Carbonarius d.o.o. as at

29 December 2008.

Release of provision for court cases relates to release of provision in relation of court case with the

company Meñimurje d.d. Visokogradnja in bankruptcy. In accordance with the assessment of

Company’s lawyer the Company will not have losses in relation to this case and it is certain that the

case will be solved in Company’s favour.

5. Costs of materials and services

2008

HRK’000

2007

HRK’000

Costs of materials

Raw materials and materials 14,823 1,199

Energy 1,251 1,040

Small inventory 153 190

16,227 2,429

Costs of services

Subcontractors 911,749 374,279

Maintenance 1,522 1,232

Rental fee 2,672 2,265

Other services 7,533 5,272

923,476 383,048

939,703 385,477

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

26

6. Personnel costs

2008

HRK’000

2007

HRK’000

Net salaries and wages 24,629 42,733

Taxes and contributions 21,558 21,019

46,187 63,752

The average number of employees in Company in 2008 was 143 (2007: 140)

Personnel expenses for the Company include HRK 7,110 thousand (2007: HRK 5,459 thousand) of

defined pension contributions paid into obligatory pension funds.

Contributions are calculated as a percentage of employees' gross salaries.

7. Depreciation

2008

HRK’000

2007

HRK’000 Depreciation of property, plant and equipment

- ordinary rates 4,590 2,946

- release of revaluation reserves 1,179 1,179

5,769 4,125

8. Other operating expenses

2008

HRK’000

2007

HRK’000

Non-production services 38,775 37,012

Remunerations 3,873 2,770

Entertainment costs 2,178 2,066

Insurance premiums 2,946 1,944

Other taxes 5,268 5,459

Bank services 5,731 2,818

Bad debt provisions 15,207 3,173

Severance payments and scholarships 665 935

Provisions for court cases - 531

Other taxes and contributions 814 499

Other expenses 5,947 9,344 81,404 66,551

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

27

9. Financial incomes and expenses

2008

HRK’000

2007

HRK’000

Financial income

Interest income on investments not held at fair value through profit or loss 4,815 3,007

Net gain on disposal of available-for-sale financial assets released from equity 2,671 217

Foreign exchange gains 2,901 642 Net change in investments at fair value through profit or loss 1,458 4,725

Net profit on sale of financial asset trough profit or loss 12,959 33,483

Total financial income 24,804 42,074

Financial expenses

Interest expense 18,193 5,300

Foreign exchange losses 5,248 -

Realized losses on financial assets available for sale 15,399 -

Unrealised loss on financial asset trough profit or loss 8,199 -

Other financial expenses 4,160 -

Total financial expenses 51,199 5,300

Financial result (26,395) 36,774

10. Income tax

Recognized in the income statement

2008

HRK’000

2007

HRK’000

Current tax 5,045 22,968

Deferred tax - (692)

Income tax in the income statement 5,045 22,276

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

28

Reconciliation of effective tax rate

A reconciliation of tax expense per the income statement and taxation at the statutory rate is detailed in

the table below:

2008.

HRK’000

2007.

HRK’000

Profit before taxation 16,934 88,951

Gain taxed abroad (4,236) -

Corrected gain 12,698 88,951

Tax calculated at the statutory rate of 20% (2007: 20%) 2,540 17,790

Expenses not allowable for income tax purposes 3,392 4,647

Tax on depreciation calculated on revaluated amount 236 236

Non-taxable income (1,079) (12)

Incentives (44) (36)

Income tax from previous periods - (349)

Income tax 5,045 22,276

Effective tax rate 39.72% 25.04%

Tax regulations in Croatia are subject to changes. There is also inconsistency in the application of tax

regulations and significant uncertainty in the area of tax laws interpretations of various taxes and

transactions which result in tax effects. Tax positions of the Company are subject to examination by

regulatory bodies and possible disputes, and accordingly the potential tax effect is uncertain in case the

tax authorities apply interpretations different from the Company’s interpretations.

In accordance with local regulations, Tax authorities can review the Company’s business books and

documentation and additional tax liabilities and potential penalties can be imposed to the Company.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

29

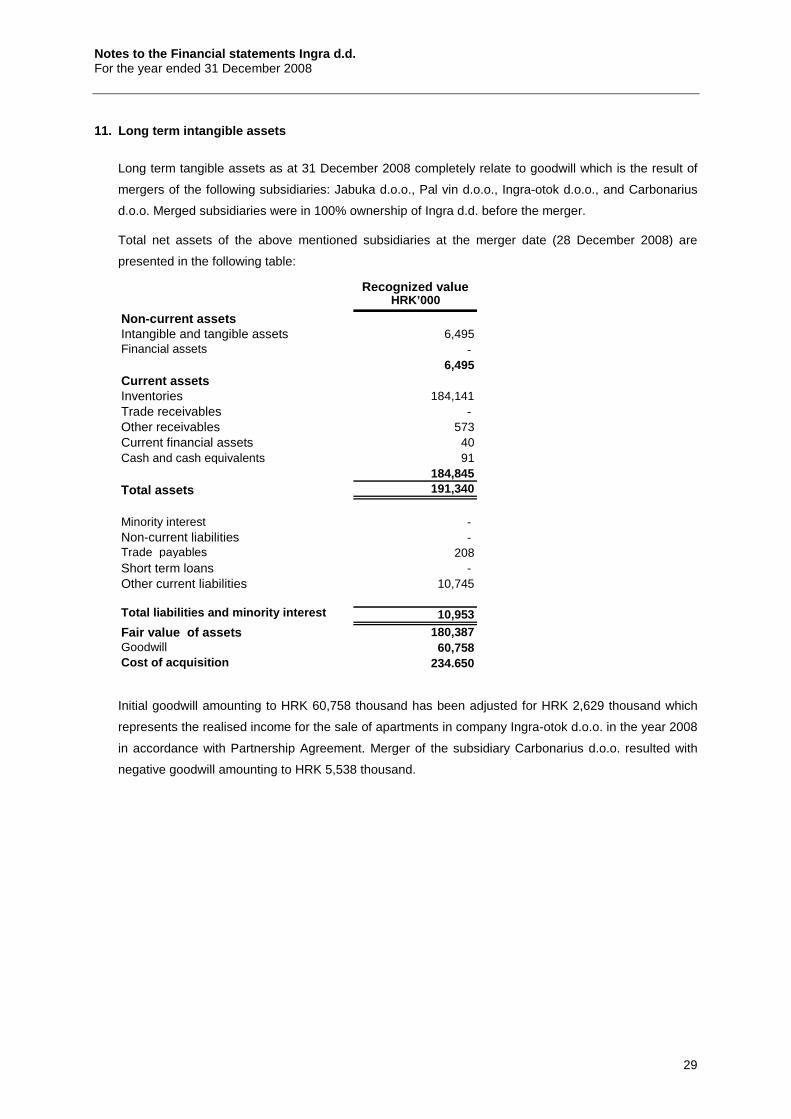

11. Long term intangible assets

Long term tangible assets as at 31 December 2008 completely relate to goodwill which is the result of

mergers of the following subsidiaries: Jabuka d.o.o., Pal vin d.o.o., Ingra-otok d.o.o., and Carbonarius

d.o.o. Merged subsidiaries were in 100% ownership of Ingra d.d. before the merger.

Total net assets of the above mentioned subsidiaries at the merger date (28 December 2008) are

presented in the following table:

Initial goodwill amounting to HRK 60,758 thousand has been adjusted for HRK 2,629 thousand which

represents the realised income for the sale of apartments in company Ingra-otok d.o.o. in the year 2008

in accordance with Partnership Agreement. Merger of the subsidiary Carbonarius d.o.o. resulted with

negative goodwill amounting to HRK 5,538 thousand.

Recognized value HRK’000

Non-current assets Intangible and tangible assets 6,495Financial assets -

6,495Current assets Inventories 184,141Trade receivables - Other receivables 573Current financial assets 40 Cash and cash equivalents 91

184,845Total assets 191,340

Minority interest - Non-current liabilities - Trade payables 208Short term loans - Other current liabilities 10,745

Total liabilities and minority interest 10,953

Fair value of assets 180,387Goodwill 60,758Cost of acquisition 234.650

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

30

12. Property, plant and equipment

Description Land Buildings Plant and equipment

Vehicles and other

assets Total

HRK'000 HRK'000 HRK'000 HRK'000 HRK'000

Purchase value

As at 1 January 2007 12,060 105,142 4,687 7,438 129 ,327

Additions - - 1,562 1,815 3,377

Disposals - (2,713) (365) (1,559) (4,637)

As at 31 December 2007 12,060 102,429 5,884 7,694 12 8,067

Additions - - 1,088 949 2,037

Disposals - - (375) (235) (610) _______ _______ _______ _______ _______

As at 31 December 2008 12,060 102,429 6,597 8,408 129,494 _______ _______ _______ _______ _______

Accumulated depreciation

As at 1 January 2007 - 14,676 3,678 5,758 24,112

Additions - 2,561 891 673 4,125

Disposals - (170) (523) (1,375) (2,068)

As at 31 December 2007 - 17,067 4,046 5,056 26,169

Additions - 2,561 1,204 1,023 4,788

Disposals - - (369) (213) (582) _______ _______ _______ _______ _______

As at 31 December 2008 - 19,628 4,881 5,866 30,375 _______ _______ _______ _______ _______

Carrying value

As at 31 December 2007 12,060 85,362 1,838 2,638 101,898

As at 31 December 2008 12,060 82,801 1,716 2,542 99,119

Revaluation

Lands and buildings were revaluated for the first time during the September 2006 based on current

market value for current purpose. The valuation has made independent assessor.

Leased assets

Total area of the building is 4,700 m2 and it includes an area of 1,132 m2 that is rented to third parties.

Total book value of the building is HRK 85,363 thousand (2006: HRK 99,003 thousand). An asset under

lease has been rented under non-cancellable operating lease during the period of two to six years.

Subsequent renewals are negotiated with the lessee. No contingent rents are charged. Future minimal

payments according to non-cancellable operating lease in the whole amount for every upcoming period

is presented in Note 31.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

31

Total value of pledged assets as a security for loans amounted to HRK 166,229 thousand.

As at 31 December 2008 the Company uses completely depreciated assets with the purchase cost

amounting to HRK 7,161 thousand.

13. Investment property

Description Land Buildings Total

HRK'000 HRK'000 HRK'000

Purchase cost

As at 1 January 2007 - 9,312 9,312

Additions 10,082 34,527 44,609

Disposals - - -

As at 31 December 2007 10,082 43,839 53,921

Reclassification 5,127 (5,127) -

Additions 14,019 7,429 21,448

Disposals - - - _______ _______ _______

As at 31 December 2008 29,228 46,141 75,369 _______ _______ _______

Accumulated depreciation

As at 1 January 2007 - 776 776

Charge for the period - - -

Disposals - - -

As at 31 December 2007 - 776 776

Charge for the period - 981 981

Disposals - - - _______ _______ _______

As at 31 December 2008 - 1,757 1,757 _______ _______ _______

Carrying value

As at 31 December 2007 10,082 43,063 53,145

As at 31 December 2008 29,228 44,384 73,612

The fair value of the investment property does not significantly differ from the cost of acquisition.

Part of the building relating to office space sized 1,100 m2 and warehouse space sized 300 m2 is rented

to third parties. Remaining land and building is not rented to third parties.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

32

14. Investment in subsidiaries

31 December 2008 Ownership 31 December 2007 Ownership

HRK'000 % HRK'000 %

1. Ingra Mar d.o.o. 10 51% 10 51%

2. Ingra M.E. d.o.o. 20 100% 20 100%

3. Ingra Italija s.r.l., Italy 51 67% 51 67%

4. Bioadria d.o.o. 91 64% 91 64%

5. Ingra Bioren d.o.o. 12 60% 12 60%

6. Tiha nekretnine d.o.o. - - 1,879 100%

7. Ingra gradnja d.o.o. 20 100% 20 100%

8. Pal Vin d.o.o. - - 79,742 100%

9. Ingra Mont d.o.o. - - 15 75%

10. Posedarje Rivijera 160 100% 160 100%

11. Jabuka d.o.o. - - 67,385 100%

12. Ingra Energo d.o.o. 7 100% 7 100%

13. Mavrovo adg 54,213 79% - -

14. Južni Jadran Nautika

d.o.o.

255 51% 255 51%

15. Sarl Alžir 39 99% 39 99%

16. Mavrovo inženjering dooel 9,644 50% - -

17. Intel d.o.o. 12,463 100% 12,463 100%

18. Geotehnika Sudan d.o.o. 1,443 100% 1,443 100%

19. Opatija nekretnine d..o.o 190 51% 190 51%

20. Geotehnika d.o.o. 20 100% 20 100%

21. Lanište d.o.o. 93,967 100% 58,433 50%

22. Domovi dalmatinske

rivijere d.o.o.

13,214 100% 13,214 100%

23. Ingra otok d.o.o. - - 5,144 100%

24. P.B. Žitnjak d.o.o. - - 24,250 51%

25. Primani d.o.o. 2,200 51% 2,200 51%

26. Marina Slano d.o.o. 49 62% 49 62%

188,068 267,092

During 2008 the Company acquired two Macedonian construction companies: Mavrovo ADG (in April

2008) and Mavrovo Inženjering dooel (in June 2008). Request for bankruptcy procedure has been

initialized in March 2009 for the company Mavrovo ADG.

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

33

15. Investment in associates

31 December

2008 Ownership 31 December 2007 Ownership

HRK'000 % HRK'000 %

Dubrovačke Lučice d.o.o. 45 49% 45 49%

Ingra Pro d.o.o. 8 40% 8 40%

Hotel Lapad d.d. 13,308 11% 13,052 19%

13,361 13,105

16. Other financial assets

31 December 2008

HRK’000

31 December 2007

HRK’000

Non-current

Investments in affiliates 10,860 10,860

Held to maturity investments 4,093 4,317

Financial assets at fair value through profit or loss - 363

Other non-current investments 2,056 1,056

17,009 16,596

Current

Available for sale financial assets 47,561 121,586

Deposits and guarantees 46 326

Financial assets at fair value through profit or loss 17,823 85,977

65,430 207,889

Investments in affiliates not publicly traded refer to investments in Lipik Glas d.o.o. (17.54%) and

Adriastar hotels and resorts d.o.o. (19.5%).

A financial asset available for sale refers to holdings in an investment fund.

Financial assets at fair value through profit and loss refer to holdings in cash funds. Financial assets at

fair value through profit and loss which were reclassified as at 1 July 2008 from this balance sheet

position to Available for sale financial assets amounted to HRK 7,798 thousand as at 31 December

2008. As stated in note 2x) reclassification effect amounted to HRK 5,476 thousand (income before tax

would be lower for that amount).

Notes to the Financial statements Ingra d.d. For the year ended 31 December 2008

34

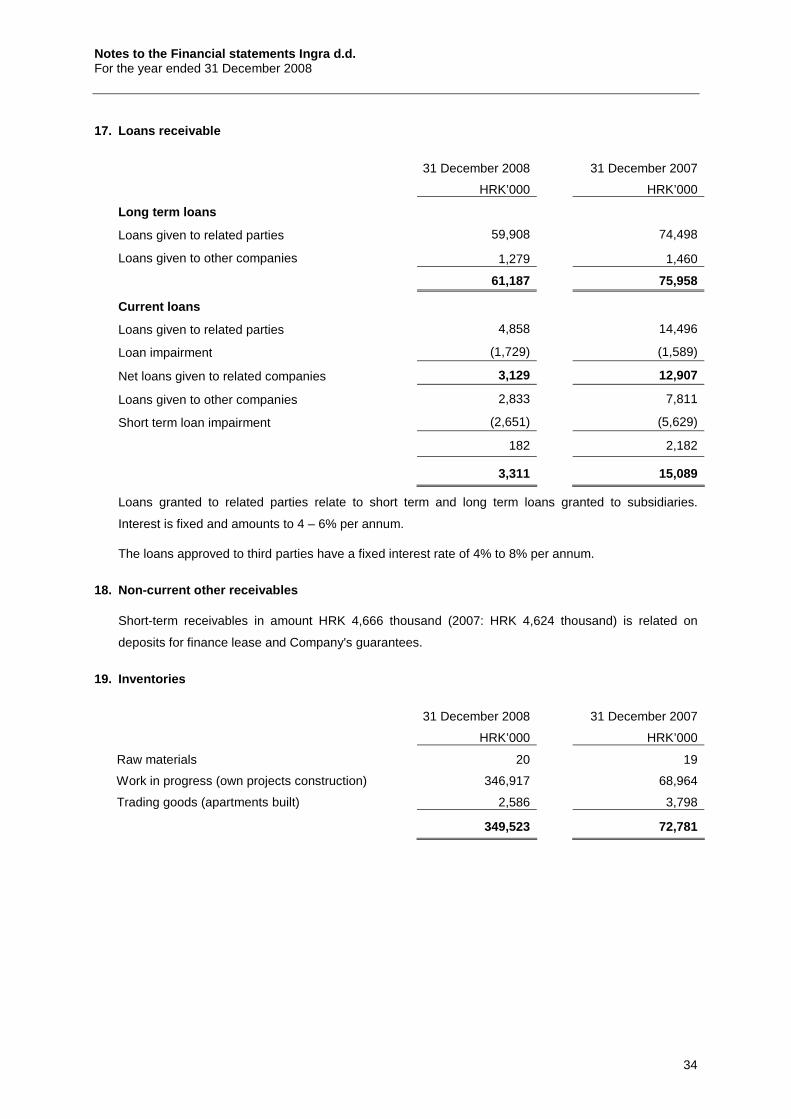

17. Loans receivable

31 December 2008

HRK’000

31 December 2007

HRK’000

Long term loans

Loans given to related parties 59,908 74,498

Loans given to other companies 1,279 1,460

61,187 75,958

Current loans

Loans given to related parties 4,858 14,496

Loan impairment (1,729) (1,589)

Net loans given to related companies 3,129 12,907

Loans given to other companies 2,833 7,811

Short term loan impairment (2,651) (5,629)

182 2,182

3,311 15,089

Loans granted to related parties relate to short term and long term loans granted to subsidiaries.

Interest is fixed and amounts to 4 – 6% per annum.

The loans approved to third parties have a fixed interest rate of 4% to 8% per annum.

18. Non-current other receivables

Short-term receivables in amount HRK 4,666 thousand (2007: HRK 4,624 thousand) is related on

deposits for finance lease and Company's guarantees.

19. Inventories

31 December 2008

HRK’000

31 December 2007

HRK’000

Raw materials 20 19

Work in progress (own projects construction) 346,917 68,964

Trading goods (apartments built) 2,586 3,798

349,523 72,781

Notes to the financial statements Ingra d.d. For the year ended 31 December 2008

35

20. Trade and other receivables

31 December 2008

HRK’000

31 December 2007

HRK’000

Receivables from related parties

Trade receivables from related parties 466,230 171,901

Loans given to related parties 5,810 4,314

Receivables from key shareholders 2,195 6,192

474,235 182,407

Receivables from third parties

Trade receivables 128,718 124,269

Advances given 31,162 51,615

Receivable for VAT 19,222 10,553

Other receivables for taxes 22,530 243

Other receivables 17,107 5,726

218,739 192,406

692,974 374,813

21. Cash and cash equivalents

31 December 2008

HRK’000

31 December 2007

HRK’000

Cash at bank 39,692 96,174

Petty cash 104 1,335

Total cash at bank and petty cash 39,796 97,509

Granted overdraft on bank account (33,798) (10,354)

Cash in the cash flow statement 5,998 87,155

Cash in banks bear interest at a variable rate between 0.50% and 3% per annum.

Granted overdraft on bank account amounts to HRK 35,000 thousand and has variable interest rate

based on one month ZIBOR increased by 1.8% per annum. Interest rate range in 2007 was from 7.05%

to 10.47%.

22. Prepaid expenses and accrued income

31 December 2008

HRK’000

31 December 2007

HRK’000

Accrued income 27,184 6,098

Prepaid expenses 2,693 80

Interest and other receivables 114 36

29,991 6,214

Accrued income in the amount of HR 27,184 thousand mostly refer to accrued income from the

construction of Arena Zagreb performed in the year 2008.

Notes to the financial statements Ingra d.d. For the year ended 31 December 2008

36

23. Share capital and reserves

31 December 2008

HRK’000

31 December 2007

HRK’000

Share capital 300,000 100,000

By the Decision of the General Assembly held on 26 June 2007 share capital was increased by HRK 20

million from HRK 60 million to HRK 80 million. This was allocated to 40,000 shares without the nominal

value and was transferred from retained earnings. This decision was recorded in the court register of

the Commercial court in Zagreb on 27 June 2007. In accordance with the General Assembly decision of

the Company held on 26 June 2007 related to the share capital increase by issuing new shares, the

Company has increased share capital by issuing non-redeemable non transferable ordinary shares in

an initial public offering through cash payment.

Share capital was increased by HRK 20 million, from HRK 80 million to HRK 100 million through the

issue and payment of 10,000 non transferable ordinary shares, without nominal value. The price of the

initial public offer was HRK 35,000 per share and the Company collected the amount of HRK 350

million, paid into the separate Company’s bank account on 22 August 2007. Following the implemented

recapitalization and issuance of new shares, share capital of the Company amounted to HRK 100

million which was divided into 50,000 non transferable ordinary shares, without nominal value.

Increase of share capital resulted in the creation of a share premium in the amount of HRK 330,000

thousand. Fee charge in the amount of HRK 7,000 thousand incurred during the initial public offering

was recognised as a change in capital and reserves as a decrease in the share premium.

Increase in share capital was recorded into the court register of Commercial court in Zagreb on 7

September 2007

Furthermore, the Company increased the share capital by HRK 200,000 thousand in 2008 from share

premium account in accordance with the Decision made on General meeting held on 21 July 2008.

Also, in accordance with the Decision of the General Assembly the share split has been made in a way

that one ordinary share on the name INGR-R-A, without the nominal value, has been split to 150

shares without nominal amount. Total sum of ordinary shares on the name INGR-R-A after this

corporate action is 7,500,000 shares without nominal value.

Treasury shares

As at 31 December 2008 the Company held 166,507 own shares (31 December 2007: 940). Treasury

shares represent 2.22% of the share capital (2007: 1.88%). During 2008 the Company purchased

25,507 (2007: 230) own shares for the amount of HRK 4,255 thousand (2007: 230 thousand). The

shares have been fully paid.

Retained earnings contain HRK 6,660 thousand (2007: HRK 2,946 thousand ) which represent

reserves for treasury shares that together with the stated reserves for treasury shares cannot be

distributed to shareholders.

Notes to the financial statements Ingra d.d. For the year ended 31 December 2008

37

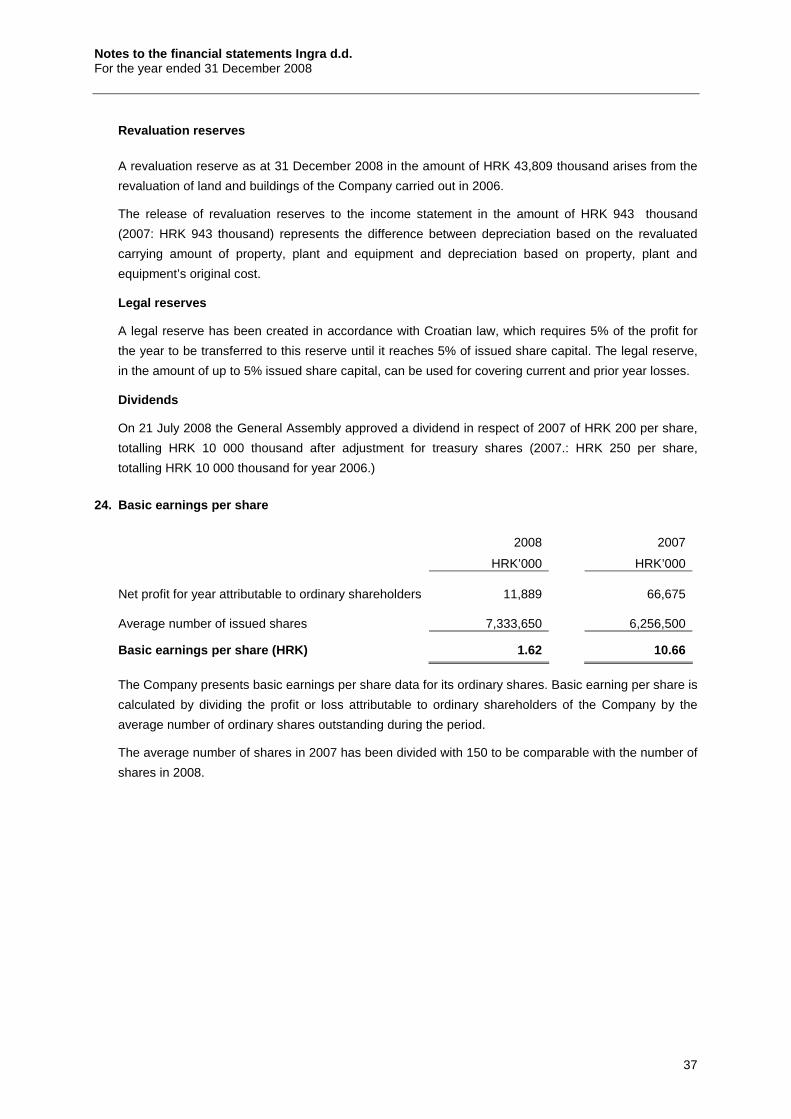

Revaluation reserves

A revaluation reserve as at 31 December 2008 in the amount of HRK 43,809 thousand arises from the

revaluation of land and buildings of the Company carried out in 2006.

The release of revaluation reserves to the income statement in the amount of HRK 943 thousand

(2007: HRK 943 thousand) represents the difference between depreciation based on the revaluated

carrying amount of property, plant and equipment and depreciation based on property, plant and

equipment’s original cost.

Legal reserves

A legal reserve has been created in accordance with Croatian law, which requires 5% of the profit for

the year to be transferred to this reserve until it reaches 5% of issued share capital. The legal reserve,

in the amount of up to 5% issued share capital, can be used for covering current and prior year losses.

Dividends

On 21 July 2008 the General Assembly approved a dividend in respect of 2007 of HRK 200 per share,

totalling HRK 10 000 thousand after adjustment for treasury shares (2007.: HRK 250 per share,

totalling HRK 10 000 thousand for year 2006.)

24. Basic earnings per share

2008

HRK’000

2007

HRK’000

Net profit for year attributable to ordinary shareholders 11,889