Embed Size (px)

Citation preview

Industrial mineralsOur world is made of them, our future too

Dr. Michalis StefanakisIMA-Europe

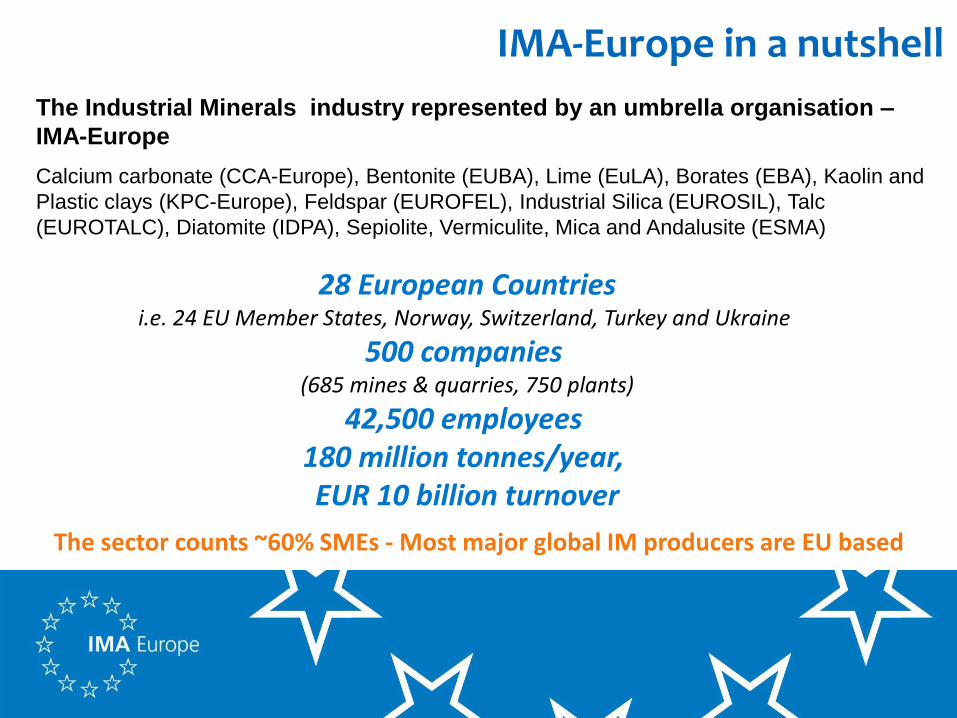

IMA-Europe in a nutshell

The Industrial Minerals industry represented by an umbrella organisation –

IMA-Europe

Calcium carbonate (CCA-Europe), Bentonite (EUBA), Lime (EuLA), Borates (EBA), Kaolin and

Plastic clays (KPC-Europe), Feldspar (EUROFEL), Industrial Silica (EUROSIL), Talc

(EUROTALC), Diatomite (IDPA), Sepiolite, Vermiculite, Mica and Andalusite (ESMA)

28 European Countriesi.e. 24 EU Member States, Norway, Switzerland, Turkey and Ukraine

500 companies (685 mines & quarries, 750 plants)

42,500 employees 180 million tonnes/year, EUR 10 billion turnover

The sector counts ~60% SMEs - Most major global IM producers are EU based

3Critical Raw

Materials 10.09.10

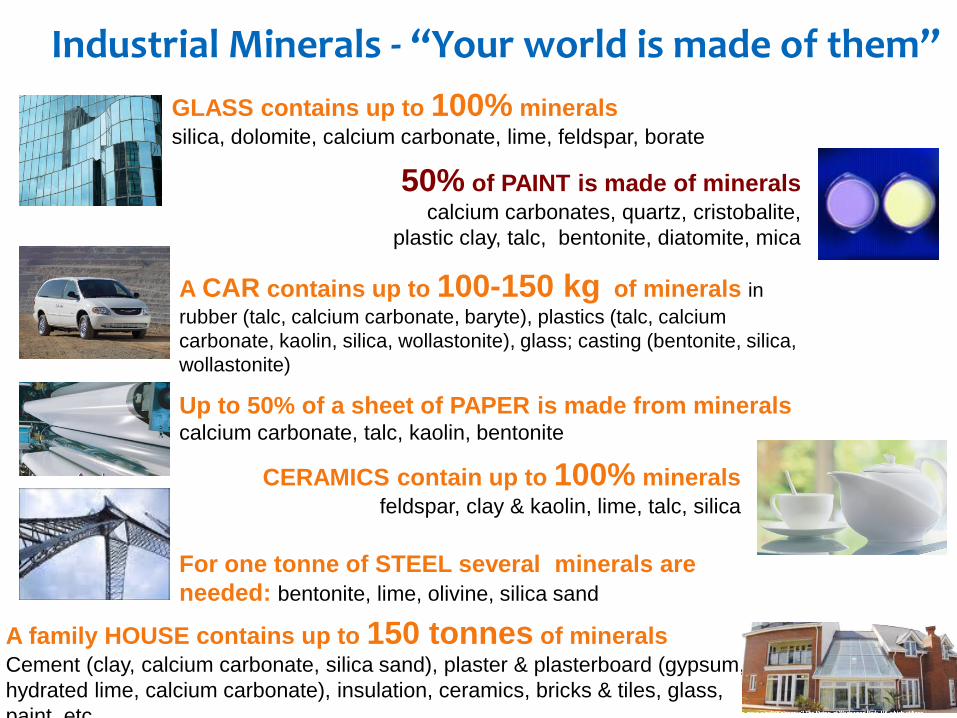

Industrial Minerals - “Your world is made of them”

50% of PAINT is made of mineralscalcium carbonates, quartz, cristobalite,

plastic clay, talc, bentonite, diatomite, mica

CERAMICS contain up to 100% minerals feldspar, clay & kaolin, lime, talc, silica

Up to 50% of a sheet of PAPER is made from mineralscalcium carbonate, talc, kaolin, bentonite

A family HOUSE contains up to 150 tonnes of mineralsCement (clay, calcium carbonate, silica sand), plaster & plasterboard (gypsum,

hydrated lime, calcium carbonate), insulation, ceramics, bricks & tiles, glass,

paint, etc.

GLASS contains up to 100% mineralssilica, dolomite, calcium carbonate, lime, feldspar, borate

A CAR contains up to 100-150 kg of minerals in

rubber (talc, calcium carbonate, baryte), plastics (talc, calcium

carbonate, kaolin, silica, wollastonite), glass; casting (bentonite, silica,

wollastonite)

For one tonne of STEEL several minerals are

needed: bentonite, lime, olivine, silica sand

23.01.144

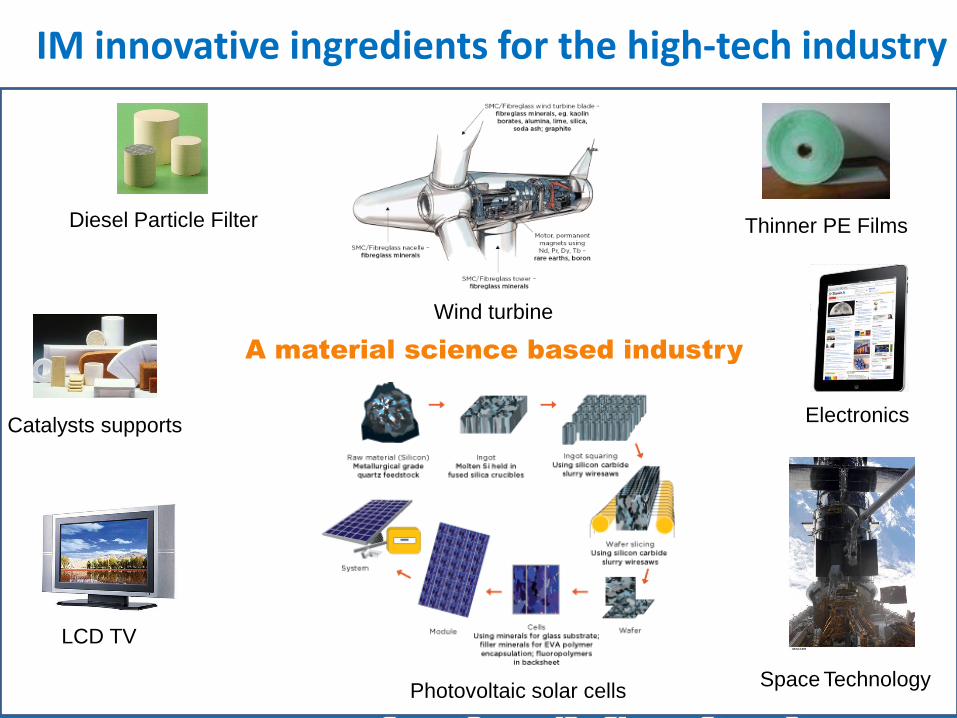

IM innovative ingredients for the high-tech industry

A material science based industry

Diesel Particle Filter Thinner PE Films

Space Technology

ElectronicsCatalysts supports

Photovoltaic solar cells

Wind turbine

LCD TV

5Critical Raw

Materials 10.09.10

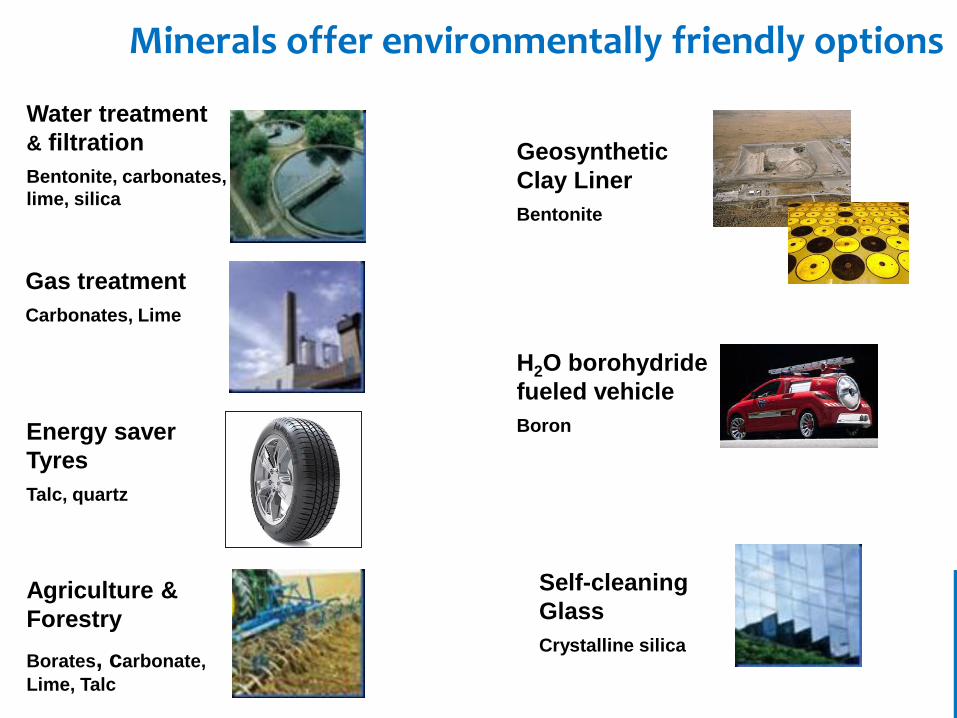

Water treatment

& filtration

Bentonite, carbonates,

lime, silica

Gas treatment

Carbonates, Lime

Agriculture &

Forestry

Borates, carbonate,

Lime, Talc

Geosynthetic

Clay Liner

Bentonite

Self-cleaning

Glass

Crystalline silica

Minerals offer environmentally friendly options

H2O borohydride

fueled vehicle

BoronEnergy saver

Tyres

Talc, quartz

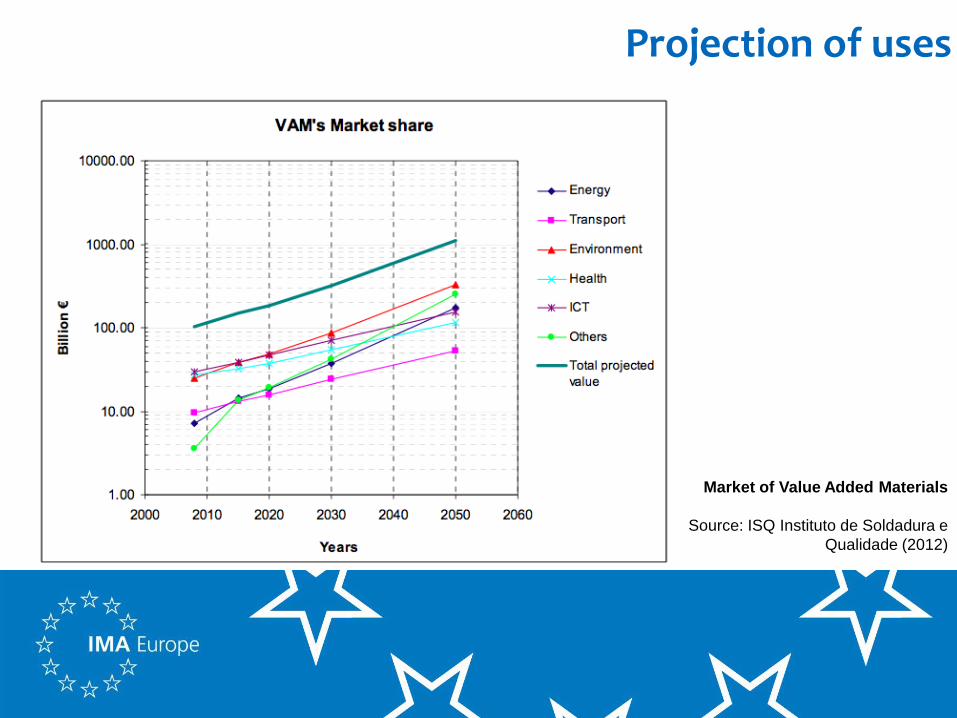

Projection of uses

Market of Value Added Materials

Source: ISQ Instituto de Soldadura e

Qualidade (2012)

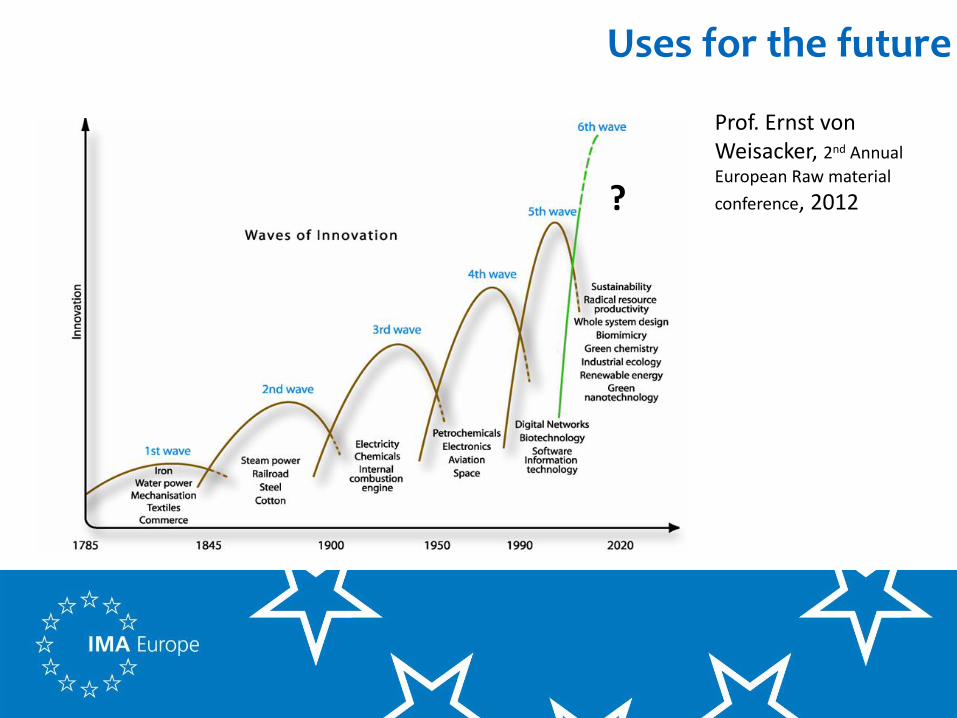

Uses for the future

Prof. Ernst von Weisacker, 2nd Annual

European Raw material

conference, 2012?

Mineral properties for high value applications

• Nano size• High Purity• Customized surface properties• Low weight• Recyclability• Innocuous to human health and the environment

Need for expanding material science skills

9Critical Raw

Materials 10.09.10

Value creation through innovation

Innovation Union

Facts

• Under-investing in our knowledge base, spending every year

0.8% of GDP less than the US and 1.5% less than Japan in R&D – with major

gaps in business R&D, venture capital investments; too much fragmentation

and costly duplication.

• European universities do not attract or retain enough top

global talent, with relatively few in leading positions in existing

international rankings.

• Unsatisfactory framework conditions, ranging from poor

access to finance, high costs of IPR to slow standardization and ineffective

use of public procurement.

• …

Innovation Union

Actions

• Create an excellent, modern education system in all Member

States.

• Innovation partnership : Ensuring a secure supply chain and achieve efficient

and sustainable management and use of non-energy

raw materials along the entire value chain

• Spend our resources more efficiently and achieve critical mass.

• …

Skills & Training for the Industrial Minerals industry

• Match skills supply to skills demand; shortage of skills for mining-

minerals expertise.

• Process know-how in all industry segments is the winning factor, i.e.

value of multidisciplinary approach; reconsider education curricula.

• Continual training of professionals and low ranking workforce ;

Learning at job and validation of learning; reinforce incremental

innovation on the shop floor.

• Respond to increasing need for massive data handling and internet

domination even at shop floor.

The European Innovation Partnership on Raw Materials (EIP RM)

• Member of the High Level Group, of the Sherpa and the Operational Groups

Involved in three approved EIP RM commitments

• European Minerals Day, European Minerals Year,

IMA-Europe is a founding member of SPIRE public private partnership

IMA-Europe is part of several research projects

• FP7 STOICISM: Sustainability, Efficiency & better Functionality for three IM

• FP7 Minerals4EU: EU Mineral intelligence network structure – member of the

Industrial Consultation Committee

• H2020: involved in multiple calls’ development as partner or supporter

Contribution of IMA-Europe to Innovation

Contribution of IMA-Europe to Innovation (2)

Developing LCI for IM products

• Life Cycle Inventory data are compiled & submitted to the EU data base (ELCD)

Contributing to Product Environmental Footprint studies relevant for

the sector

• Plastics, paints, paper, etc.

Participating in EU Chemical Agency (ECHA) & EU Committees on

Nanomaterials

• Improving the legal framework for nanomaterials

Industrial Minerals Resource efficiency

1. Primary resource efficiency: efficient sourcing through sustainable

mining and processing

1. Efficiency of usage: by improving the performance of the many end-use

applications in which they are used, contribute to savings in downstream

sectors

1. Secondary resource efficiency: by-products and waste valorisation,

allowing waste streams reduction

1. Recycling from end-use applications: industrial minerals are recovered

through the recycling of the products in which they are used; the average

IM recycling is 60% (silica 73, lime 68, feldspar 67, talc 60, calcium carbonate 58,

bentonite 50, kaolin & clay 49%)

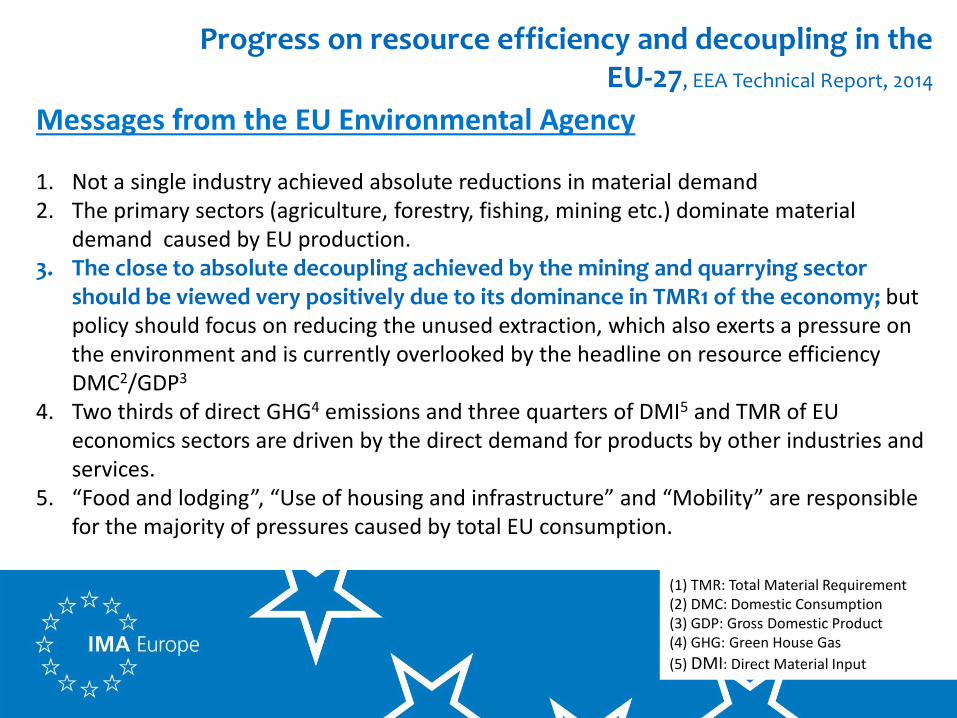

Progress on resource efficiency and decoupling in the EU-27, EEA Technical Report, 2014

Messages from the EU Environmental Agency

1. Not a single industry achieved absolute reductions in material demand2. The primary sectors (agriculture, forestry, fishing, mining etc.) dominate material

demand caused by EU production. 3. The close to absolute decoupling achieved by the mining and quarrying sector

should be viewed very positively due to its dominance in TMR1 of the economy; but policy should focus on reducing the unused extraction, which also exerts a pressure on the environment and is currently overlooked by the headline on resource efficiency DMC2/GDP3

4. Two thirds of direct GHG4 emissions and three quarters of DMI5 and TMR of EU economics sectors are driven by the direct demand for products by other industries and services.

5. “Food and lodging”, “Use of housing and infrastructure” and “Mobility” are responsible for the majority of pressures caused by total EU consumption.

(1) TMR: Total Material Requirement(2) DMC: Domestic Consumption(3) GDP: Gross Domestic Product(4) GHG: Green House Gas

(5) DMI: Direct Material Input

17Critical Raw

Materials 10.09.10

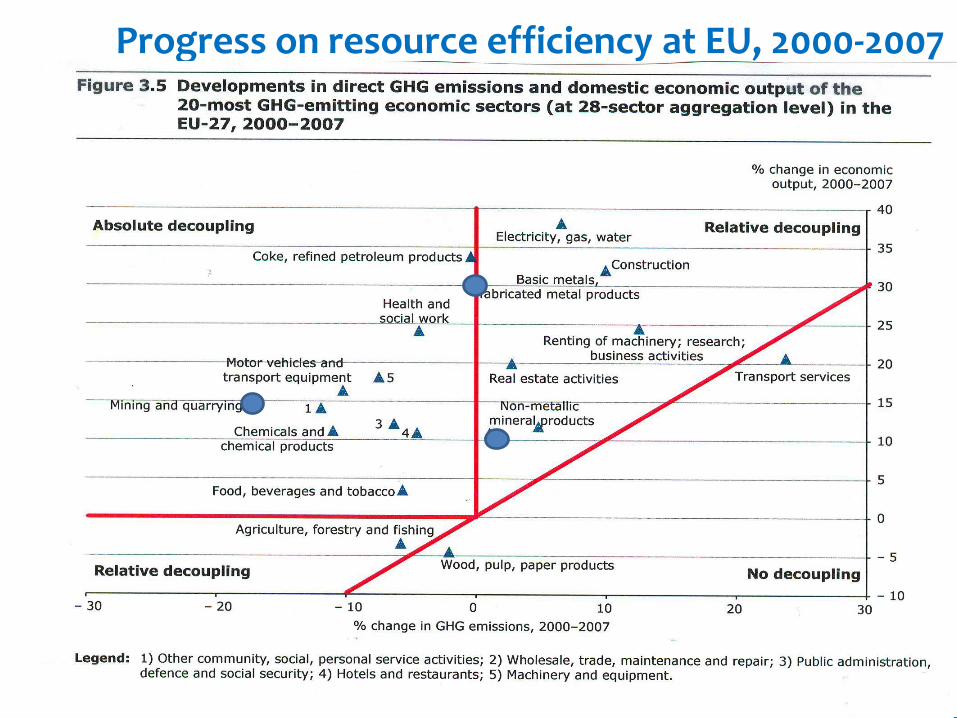

Progress on resource efficiency at EU, 2000-2007

18Critical Raw

Materials 10.09.10

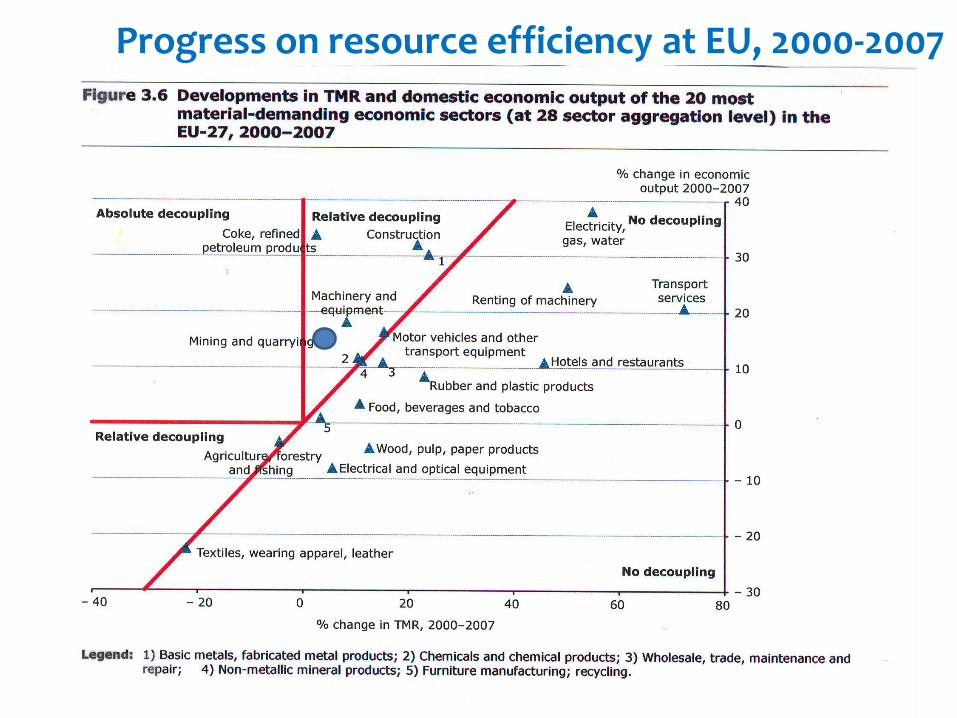

Progress on resource efficiency at EU, 2000-2007

Resource efficiency - Conclusion

Resource Efficiency should not be limited to “using less”, it should promote to ….

“Using better,

Living better”!

Thank you for your attention

IMA-Europe S&B Industrial [email protected] [email protected]: +32 2 210 44 10http://www.ima-europe.eu http://www.sandb.com

![Minerals [Most] rocks are [mostly] made of minerals, so ___________identification and interpretation depends on recognizing ____________________________________](https://img.dokumen.tips/doc/110x75/56649e165503460f94b01715/minerals-most-rocks-are-mostly-made-of-minerals-so-identification.jpg)