Embed Size (px)

Citation preview

Way2WealthWay2Wealthmaking investing simpler, more understandable and profitablemaking investing simpler, more understandable and profitable..

Indian Economy Indian Economy UpdateUpdateApril 2010April 2010

Agenda

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Sector Contribution & Growth

3

Indian economy – Sector Contribution

Over the last 8-9 years the composition of the Indian GDP moving towards manufacturing and services sector

Share of agriculture in total Indian GDP is declining from 25 percent in early 2000-01 to 18 percent 2008-09

Reforms (privatization) amid sustainable internal demand helped manufacturing grow sharply during 2000-2009

Last but not the least, services occupy major portion in GDP, as the share stand more than 50 percent driven by IT and ITES

Despite declining share the agriculture & allied still provided huge employment opportunities and play a pivotal role with strong backward and forward linkages

GDP Contribution - Sectors (%)

20 18

62

15

20

65

0

10

20

30

40

50

60

70

Agriculture & Allied Industry Services & Allied Sector

2002-032009-10 E

Source:RBI

4

Indian economy – Sector Growth

After peaking in Q3-07 Indian agriculture showed relatively slower & negative growth

After bottoming out in Dec’08 Indian Industrial growth gained strong momentum

Unlike the volatile Agri and Industry, Indian Services sector held their forte well

Despite strong rebound in Industry, weaker Agri and Services weigh on Indian Economy going forward

Agriculture Sector Growth Rate (%)

4.0

2.0

0.0

2.0

4.0

6.0

8.0

10.0

Oct'06-Dec'06 Oct'07-Dec'07 Oct'08-Dec'08 Oct'09-Dec'09

Agriculture

Indistrial Sector Growth Rate (%)

4.0

0.0

4.0

8.0

12.0

16.0

Oct'06-Dec'06 Oct'07-Dec'07 Oct'08-Dec'08 Oct'09-Dec'09

Industry

Services Sector Growth Rate (%)

2.0

6.0

10.0

14.0

Oct'06-Dec'06 Oct'07-Dec'07 Oct'08-Dec'08 Oct'09-Dec'09

Services

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Key Characteristics of Indian Economy

6

Indian economy – Key Characteristics

Agriculture Though the absolute contribution to GDP is declining but more than 65 percent of population depend on agriculture and allied activities

India stand second in total global Arable & Irrigated land and largely depend upon the monsoon (natural rains) for taking up agricultural activities

Potential improvements include seed technology, improved water management & infra and encouraging allied activities like dairy, poultry and processed food industry

Industry Unlike the rest of the emerging economies Indian industry is skewed to domestic needs than export markets

Few sectors like Gems & jewelry, leather and cotton depend heavily on export markets and face quality restrictions

There is a lot of scope for the industrial activity to pick up especially in automobile, technology and food processing

ServicesAftermath of liberalization saw banking, trade, community and business services to boom on the back of IT & ITES

Increased use of services sector edge in manufacturing can create increased productivity in manufacturing and also create self sustaining demand for services sector

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Agriculture sector

8

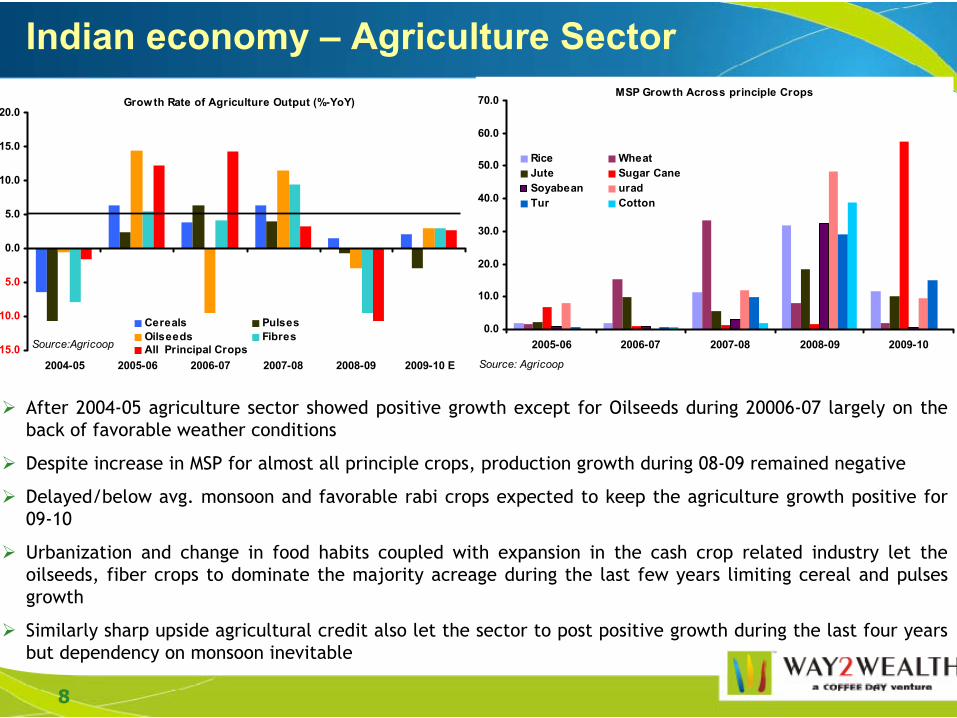

Indian economy – Agriculture Sector

After 2004-05 agriculture sector showed positive growth except for Oilseeds during 20006-07 largely on the back of favorable weather conditions

Despite increase in MSP for almost all principle crops, production growth during 08-09 remained negative

Delayed/below avg. monsoon and favorable rabi crops expected to keep the agriculture growth positive for 09-10

Urbanization and change in food habits coupled with expansion in the cash crop related industry let the oilseeds, fiber crops to dominate the majority acreage during the last few years limiting cereal and pulses growth

Similarly sharp upside agricultural credit also let the sector to post positive growth during the last four years but dependency on monsoon inevitable

Growth Rate of Agriculture Output (%-YoY)

15.0

10.0

5.0

0.0

5.0

10.0

15.0

20.0

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 E

Cereals PulsesOilseeds FibresAll Principal CropsSource:Agricoop

MSP Growth Across principle Crops

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2005-06 2006-07 2007-08 2008-09 2009-10

Rice WheatJute Sugar CaneSoyabean uradTur Cotton

Source: Agricoop

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Manufacturing Sector

10

Indian economy – Manufacturing Sector

Strong domestic as well as external demand let the Indian manufacturing grow steadily higher during 2002-07

Onset of global credit crisis (preceded by rate hikes) let the sentiments as well as the growth move sharply lower

Driven by the stimulus and steady domestic demand the manufacturing growth surged sharply higher

Mining, key manufacturing and Chemicals continue to post positive growth, while the Food and allied segments show marginal growth

A sharp upswing caught the industry surprised and show strong signs of pressure on the existing capex to add volumes and finally inflation

IIP Index Growth (%-YOY)

2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

IIP Index Growth

Source:MOSPI

IIP Index Growth-Key Components (%-YoY)

40

30

20

10

0

10

20

30

40

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-104

2

0

2

4

6

8

10

12

14

Food Prod Mining Electricity

Source:MOSPI

As indicated earlier the Capital goods sectors continue to grow strongly, while consumer goods remain shaky

Forward looking PMI suggest positivism moving ahead but the slower pace of export orders may weigh

Indian economy – Manufacturing Sector

Purchasing Managers Index-India

35

40

45

50

55

60

65

70

75

31/05/2005 28/02/2006 30/11/2006 31/08/2007 31/05/2008 28/02/2009 30/11/2009

PMI Index PMI-Export Orders PMI-New OrdersSource:Mospi

Capital Goods Production Growth (YoY-%)

15

10

5

0

5

10

15

20

25

30

35

40

Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Source:Mospi

Consumer Goods Production Growth (YoY-%)

5

0

5

10

15

20

Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

Source:Mospi

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Services Sector

13

Indian economy – Services Sector

Backed by IT & ITES, services sector contribution to overall GDP grew strongly over 2000-009

In line with the rapid urbanization contribution from Hotel & Restaurant, Transport and Banking sectors continued to grow and dominate the contribution to the total service sector

However, the YoY growth rate show that the community and personal services showed steady growth with rest of the three showing a more cyclical pattern

Demographic advantages, Urbanization along with scope for rapid industrialization the future growth prospects lie strongly in Trade, Communication and Financial Services

Weaker consumerism & business investment at matured economies stabilize overall services sector in the near future

Services Sector Componenets Growth

2

4

6

8

10

12

14

16

18

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 E

Trade, Hotels & Rest TransP & Commu Banking & Finance Community & Personal ServSource:RBI

Services Sector Contribution to GDP

656967

30

40

50

60

70

80

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 EServices & Allied SectorSource:RBI

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Indicators

15

Indian economy – Trade

After contracting during early 2009 the trade deficit continue to grow as rate of imports outpace exports

Since Q1-09 imports surged faster than the exports with oil imports accounting for 28 percent and the rest with non-oil imports

Higher raw material prices internationally, weaker consumer at matured economies and steady INR let the trade balance remain largely negative despite slowdown in economic activity

Despite no immediate threat, untimely policy (exchange rate intervention & trade tariffs) and global commodity prices may spoil the party in the medium term

Indian Trade Balance (Mln USD)

20000

16000

12000

8000

4000

0

4000

Jun-99 Oct-00 Feb-02 Jun-03 Oct-04 Feb-06 Jun-07 Oct-08 Feb-10

Trade Balance (mln USD)Source:RBI

Deficit

Surplus

Indian Trade Scenario (YoY-%)

60

40

20

0

20

40

60

80

Jun-99 Oct-00 Feb-02 Jun-03 Oct-04 Feb-06 Jun-07 Oct-08 Feb-10

Import Growth (YoY-%) Export Growth (YoY-%)Source:RBI

16

Indian economy – Fiscal Status Balance of payment (Quaterly in USD billion)

30

20

10

0

10

20

30

40

Mar-05 Sep-05 Mar-06 Sep-06 Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09

Balance of payment (Quaterly in USD billion)

Current & Capital A/C - India

40.0

20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 E

Current A/C (bln USD) Capital A/C (bln USD)

Source: RBI

After contracting during 2008-09, Indian BoP turning positive with capital A/C moving sharply higher (later flows)

Despite weaker economic environment current A/C is not improving similarly as imports remain higher, resulting current A/C balance to GDP remain above 3 percent

Similar to trade A/C though the BoP is neither heartening nor threatening, sharp swings in capital flows may pose a threat to smoother execution of the monetary policy

17

Indian economy – Funds Flow

As indicated earlier the capital flows remained stronger with FDI, FII and ECB turning positive since Q1 - FY09-10

Though FDI and ECB remained below the previous peaks the hot money FII scaled close to the Sep’07 highs

Until the matured economies signal rate hike the capital flow remain intact thereby pushing the benchmark indices higher

Foreign Direct Investments - Monthly

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Jan-06 Nov-06 Sep-07 Jul-08 May-09 Mar-10

FDI (Mln USD)

Source:RBI

Net Foreign Insti Investments Monthly

2000

1500

1000

500

0

500

1000

1500

2000

2500

3000

Jan-06 Nov-06 Sep-07 Jul-08 May-09 Mar-10

Net FII (Mln USD)

Source:RBI

External Commercial Barrowings - Monthly

0

1000

2000

3000

4000

Jan-06 Nov-06 Sep-07 Jul-08 May-09 Mar-10

ECB (M ln USD)

Source:RBI

18

Indian economy – Inflation

Weaker Agri sector performance amid strong upswing in domestic consumption pushed the inflation sharply higher

Both CPI and WPI indices now remain close/above double digit mark leaving pre-emptive monetary action by RBI

From food & primary related price rise recent weeks showed inflation moving to rest of the sub sections like power, fuel etc

Though the fortunes of the monsoon debatable, much of the inflation’s strength lie in narrow gap between potential/actual output or simply capacity constraints

Inflation & Components Growth (YoY) -CPI

0.0

5.0

10.0

15.0

20.0

25.0

31/01/2007 31/10/2007 31/07/2008 30/04/2009 31/01/2010

CPI TotalInd Food CompInd Fuel & light Rural HH Infla

Source:Mospi

Inflation & Components Growth (YoY) - WPI

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

31/01/2007 31/10/2007 31/07/2008 30/04/2009 31/01/2010

WPI TotalWPI Prim ArtiWPI ManfWPI Fuel & power

Source:Mospi

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

Forward Looking Indicators

20

Indian economy – Forward Looking IndicatorsFixed Capital Formation (%-YoY)

0

10

20

30

40

50

60

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Total

Public sector

Private Corporate

Credit Growth (%-MoM)

6

4

2

0

2

4

6

8

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-100

1

1

2

2

3

3

4

Total Food Non Food

Unlike the rest of the emerging Asia, India largely depend on domestic economic agents for capital as well as consumption

Gross Fixed capital formation though slowed down in last two years remain strong when compared to rest of Emerging Asia

After moving lower during the crisis, over all credit growth picking up strongly in the recent months suggesting increased activity

Better banking system, education, higher savings etc keep the Indian growth story robust in the medium term

21

Indian economy – Forward Looking Indicators

Highlighting the urgent need to capacity expansion the GoI set an ambitious spend plan during 11th FY

By 2011-12 total infrastructure (road, port and electricity) investments expected to touch ~10 pct of GDP

Power, irrigation and roadways expected to see increased allocation and also private sector participation

Investment in Infrastrucure (as a % of GDP)

4.23

1.2

5.43

6.45

2.89

9.43

0

2

4

6

8

10

Public Sector Private Sector Total

2007-082011-12 E

Source:11 FYP

Planned Expansion of roads (kms)

0

20000

40000

60000

80000

2005-06 2006-07 2007-08 2008-09 2009-10 E 2010-11 FSource:11 FYP

Power Generation (MWh)

0

5000

10000

15000

20000

25000

2008-09 2009-10 E 2010-11 F 2011-12 F

Thermal Hydro

Nuclear Total

Source:11 FYP

Agenda

Sector Contribution & Growth

Key Characteristics of Indian Economy

Agriculture Sector

Manufacturing Sector

Services Sector

Indicators

Forward Looking Indicators

GDP & Other Variables

India Economy Update

GDP & Other Variables

23

Indian economy – GDP

After witnessing steady growth during 2008-10 Indian economy set to grow by 7.9 percent (expecting normal monsoon)

Rebound in agriculture followed by buoyant manufacturing expected to push the economic growth during FY10-11

However, inflation, weaker matured economies and failure of the monsoon remain as greatest risk to the economy in the medium term

Indian GDP

9.69.0

6.7 6.9

7.9

2

4

6

8

10

2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 E 2010-11 FSource:RBI, W2W Estimates

Source: RBI, W2W Estimates

87.27.610 Yr G Sec Yield

4.5-5.53.53-4.337.09-7.1591-181 TB Yield

1311.8412.76PLR

10.2511.858.93CPI

6.903.178.46WPI

9.108.502.75IIP

7.856.856.70Real GDP

2010-11 F2009-102008-09

Thank you

Research Department

Premise A, 15th Floor, Chandramukhi Building, Backbay Reclamation, Nariman Point (near Inox Theatre), MUMBAI : 400021

Phone: 022 4019 2900, Fax: 022 40192939