Embed Size (px)

Citation preview

The “United States” of India?

India Strategy India Strategy (Politics)(Politics)

Nikhil Vora / Nikhil SalviIDFC Securities Ltd(Dir) +91-22-6622 2567(M) +91 –98211 32471Email: [email protected]

March 2012

Centre‘&’State OR Centre‘vs’State

India Strategy (Politics)India Strategy (Politics)

“In the happiness of his subjects lies the King’s happiness;

In their welfare his welfare,

He shall not consider as good, only that which pleases him,

but treat as beneficial to him, whatever pleases his subjects”

--- Chanakya, Arthashastra

…Are today’s ‘Kings’ (read politicians) rediscovering this maxim….at least at the state level?

Today’s ‘Kings’ are increasingly being reminded of this maxim, as evinced from state level assembly elections in past two years, in which regional parties that promised better governance were awarded with majority mandate (irrespective of incumbency factor!). With the Central coalition in power faltering in spite of clear mandate in last general elections, and regional parties reading recent political winds correctly, we hazard a guess that the next general elections may see a fragmented Parliament with coalition government of smaller regional parties having little in common. Does this entail economic growth taking a backseat as the future Parliament labors to arrive at consensus over reforms?

We think otherwise, not because we believe coalition parties will put reforms over politics (unlikely, as history shows us), but because state governments are increasingly using their constitutionally allocated powers to drive economic progress demanded by a ‘younger’ electorate. Post liberalization, the centre has limited to policy making, while investment function is increasingly taken up by private sector. Private investments gravitate towards states with better infrastructure and policies conducive for business, thereby fuelling competition between states to attract capital and investments that accelerate economic activity. Looking ahead, we believe this competition will only intensify and with increasing decentralization of powers, tomorrow’s India, although in letter will still be a ‘Union of States’ as envisaged in the Constitution, but in spirit will more resemble ‘The United States of India’!.

This reminds me of something that VS Naipaul, the Nobel winning author once commented, “Bihar…a place where civilization ends…”

Clearly, we don’t agree…!!!

3

‘‘United States of IndiaUnited States of India’’? Better or Worse?? Better or Worse?

The First Article of Constitution describes India as a ‘Union of States’, although the nature of constitution is federal in structure

“…what is important is that the use of the word 'Union' is deliberate…Though the country and the people may be divided into different States for convenience of

administration, the country is one integral whole, its people a single people living under a single imperium derived from a single source”

– Dr B R Ambedkar , Chairman, Drafting Committee of the Indian Constitution

“It is the Union of India which is the basis of our nationality…States are but limbs of the Union, and while we recognize that the limbs must be healthy and strong…it is the strength and stability of the Union and its capacity to develop and evolve that should be governing consideration of all

changes in the country“

- The State Reorganisation Committee

Questions we seek to answerQuestions we seek to answer……

But how close is the reality of Centre-State relations to that envisaged?

And what does that mean for economic growth of the country?

We revisit this idea in the backdrop of increasing strain in Centre-State relations and results of recent assembly elections

4

5

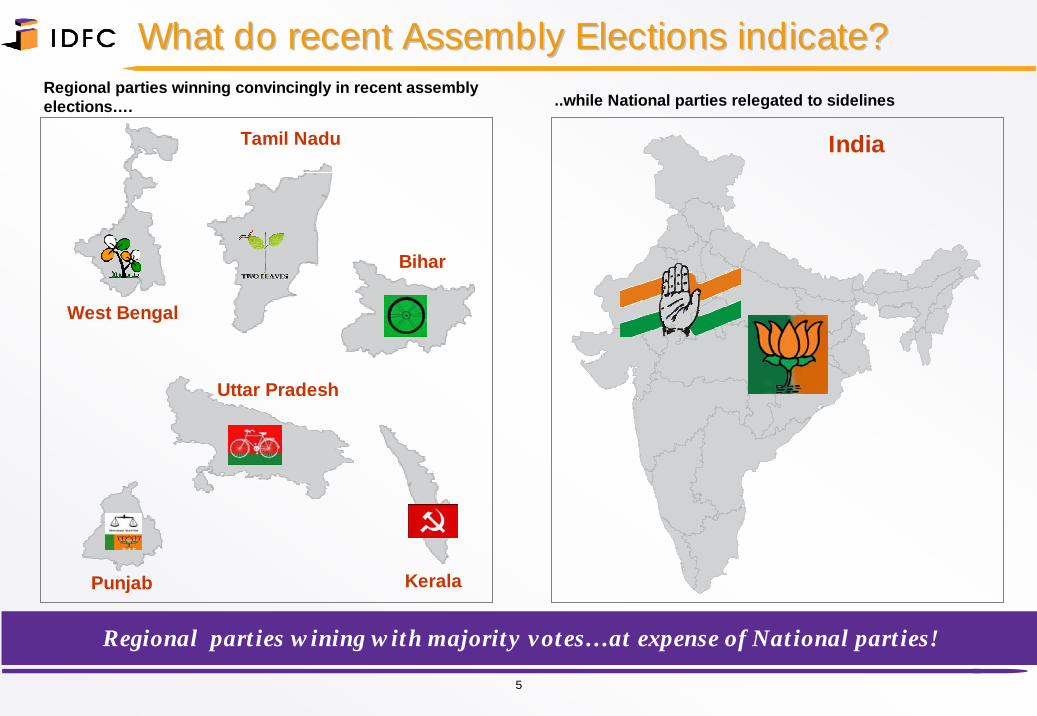

What do recent Assembly Elections indicate?What do recent Assembly Elections indicate?

West Bengal

Tamil Nadu

Uttar Pradesh

Punjab

Bihar

Kerala

India

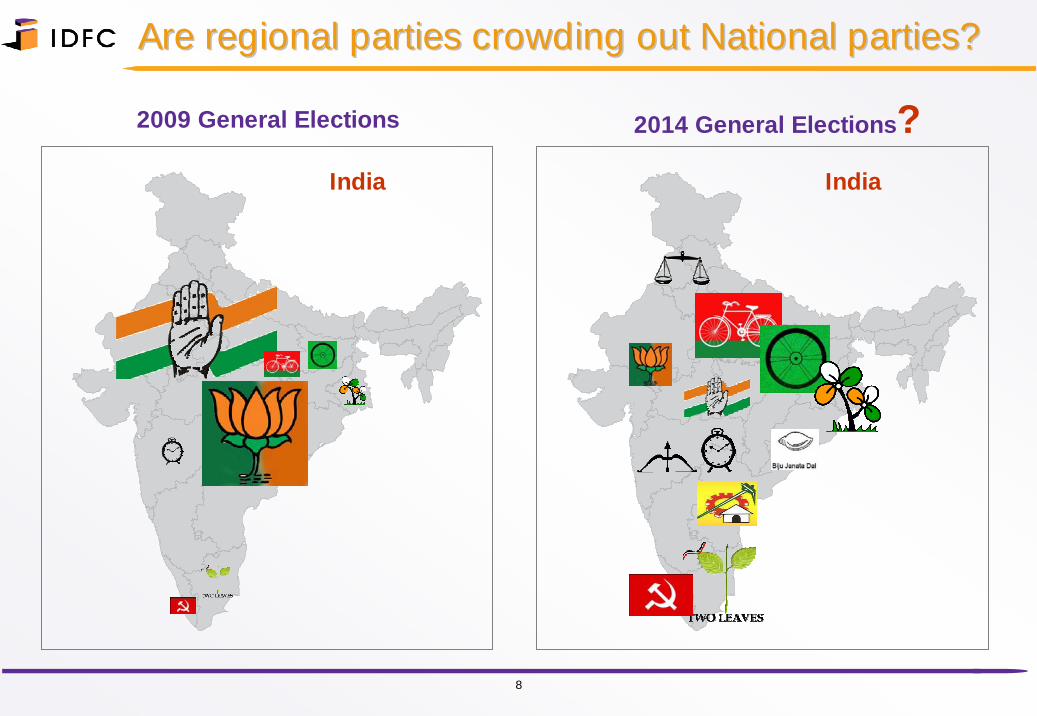

Regional parties winning convincingly in recent assembly elections…. ..while National parties relegated to sidelines

Regional parties wining with majority votes…at expense of National parties!

6

What do recent Assembly Elections indicate? What do recent Assembly Elections indicate? ““MMOORREE””

Onus towards better governance (voting even to incumbent)!

Move away from narrow caste / religion politics?

Economic aspiration demanding better politics/governance?

Regional parties gaining at expense of National parties!

What do the recent assembly elections

portend for 2014?

7

Are regional parties crowding out National parties?Are regional parties crowding out National parties?

2014 General Elections?India

2009 General Elections

8

India

9

DDééjjàà vu 1996vu 1996--99?99?

…plus ça change, plus c'est la même chose…(the more things change, the more they stay the same)

- Jean-Baptiste Alphonse Karr, in the Les Guêpes, January 1849

1010

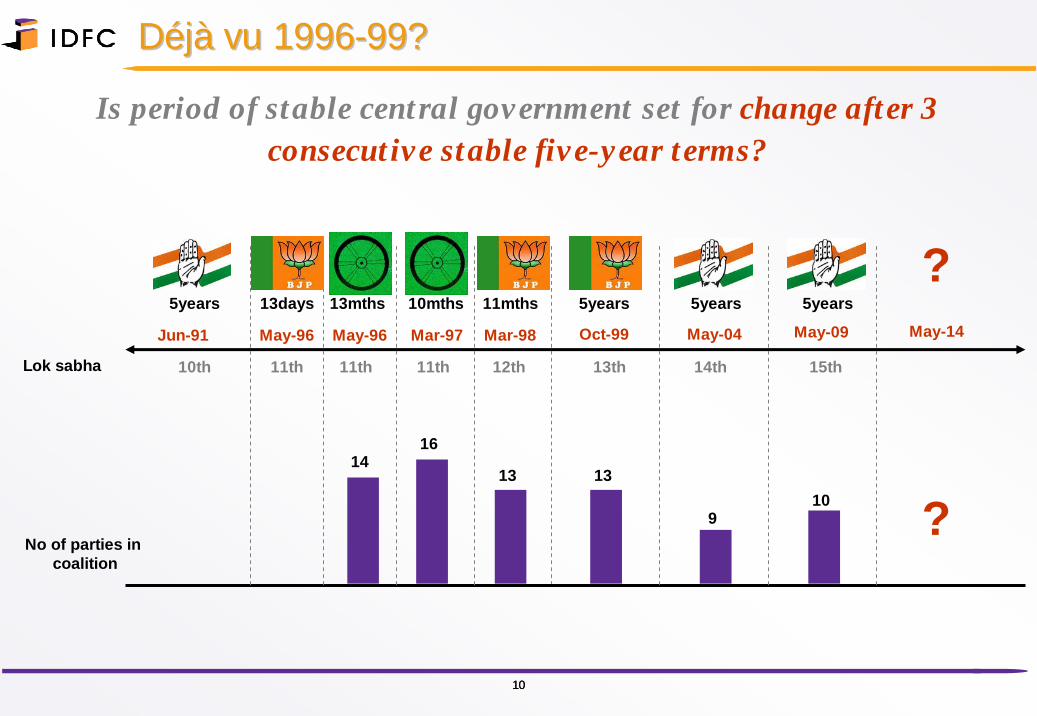

DDééjjàà vu 1996vu 1996--99?99?

Is period of stable central government set for change after 3 consecutive stable five-year terms?

Jun-91 May-96 May-96 Mar-97 Mar-98 Oct-99 May-04 May-09

5years 13days 13mths 10mths 11mths 5years 5years 5years

Lok sabha 10th 11th 11th 11th 12th 13th 14th 15th

No of parties in coalition

1416

13 13

910

May-14

?

?

0%

25%

50%

75%

100%

1980 1984 1989 1991 1996 1998 1999 2004 2009 … 2014

Seats won - National Parties Seats won - Regional Parties

1111

National parties ceding ground to regional parties?National parties ceding ground to regional parties?

?

1212

What can fragmented mandate in 2014 can mean to reforms?What can fragmented mandate in 2014 can mean to reforms?

Can coalition governments (15+ parties) provide political stability?Can a fractured Parliament arrive at a consensus on reforms?

Reforms Parliament Act/LawCabinet Key measures

FDI in single brand retail

Land acquisition bill

Mining bill

Goods & services tax

Direct Tax code

Jan Lokpal bill

Not requiredFDI of 100% in single brand retail has come into effect; For FDI > 51%, mandatory sourcing of at least 30% from the domestic small and cottage industries!

Companies to pay at least 2x market price in urban and 6x in rural areas; Companies shall provide for rehabilitation and resettlement

Tax of 26% of profit of coal miners and 100% royalty for others;Also, central and state cess to be levied on mining companies

Move towards a common indirect tax regime across the country; According to CII, GST could add 1-1.5% to GDP growth

Move towards a simplified direct tax structure and lower tax rates; To improve tax collections due to lower evasions

It would enable filing of complaints against politicians and bureaucrats without prior government approval

Not required

FDI in aviation Not required FDI of 49% in aviation is on the cards! Not required

1313

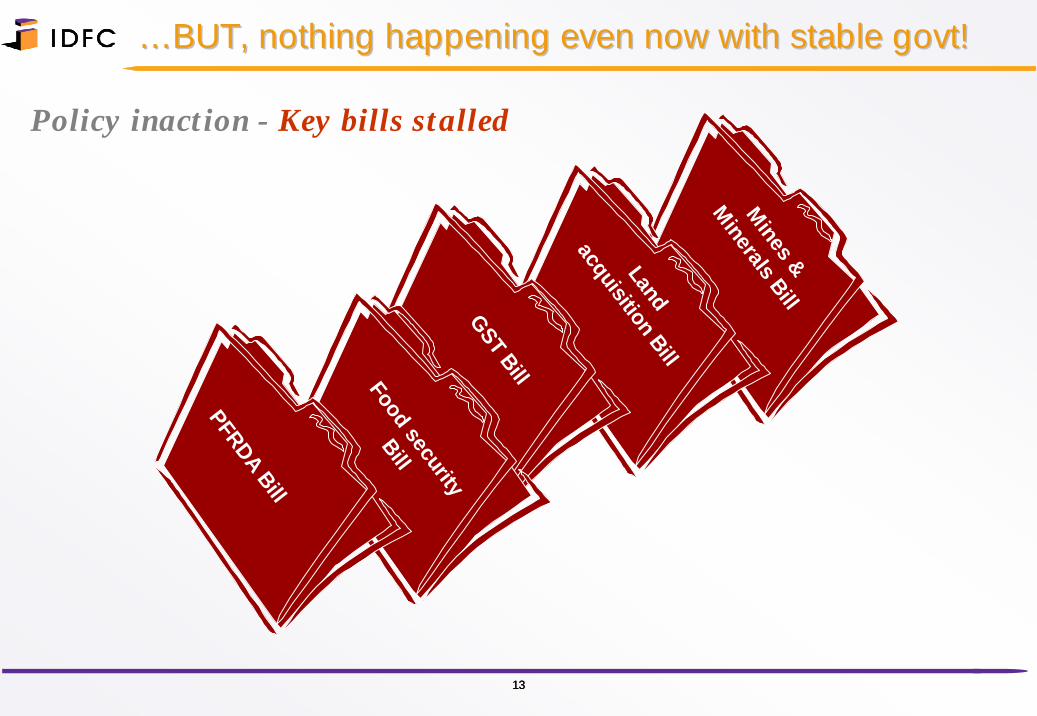

……BUT, nothing happening even now with stable BUT, nothing happening even now with stable govtgovt!!

Policy inaction - Key bills stalled

PFRDA Bill

Food security

Bill

GST Bill

Land

acquisition Bill

Mines &

Minerals Bill

1414

……BUT, nothing happening even now with stable BUT, nothing happening even now with stable govtgovt!!

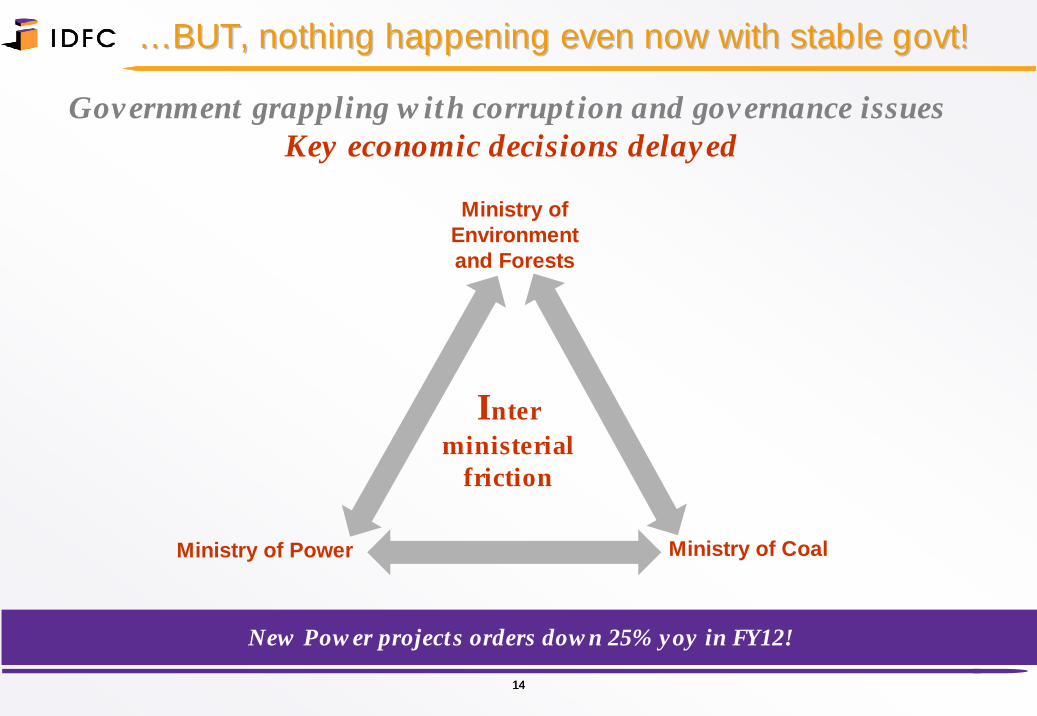

Government grappling with corruption and governance issues Key economic decisions delayed

Inter ministerial

friction

Ministry of Environment and Forests

Ministry of CoalMinistry of Power

New Power projects orders down 25% yoy in FY12!

Corporate India sums it up bestCorporate India sums it up best……

“There’s a sense that the bureaucracy has stopped taking decisions as they fear that action might be taken against them

in future even for honest mistakes.”

- Sunil Bharti Mittal

Is ‘Intent to govern’ more important than majority in legislative bodies?

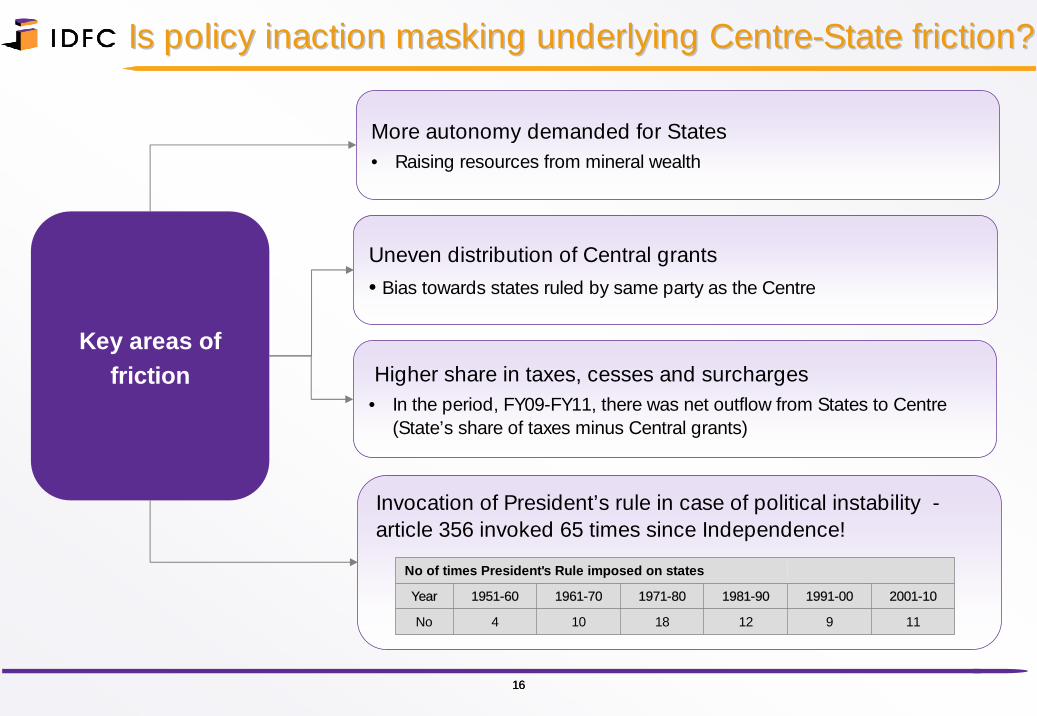

Invocation of President’s rule in case of political instability -article 356 invoked 65 times since Independence!

1616

Is policy inaction masking underlying CentreIs policy inaction masking underlying Centre--State friction?State friction?

Key areas of friction

No of times President's Rule imposed on states

Year 1951-60 1961-70 1971-80 1981-90 1991-00 2001-10

No 4 10 18 12 9 11

More autonomy demanded for States • Raising resources from mineral wealth

Higher share in taxes, cesses and surcharges • In the period, FY09-FY11, there was net outflow from States to Centre

(State’s share of taxes minus Central grants)

Uneven distribution of Central grants

• Bias towards states ruled by same party as the Centre

17

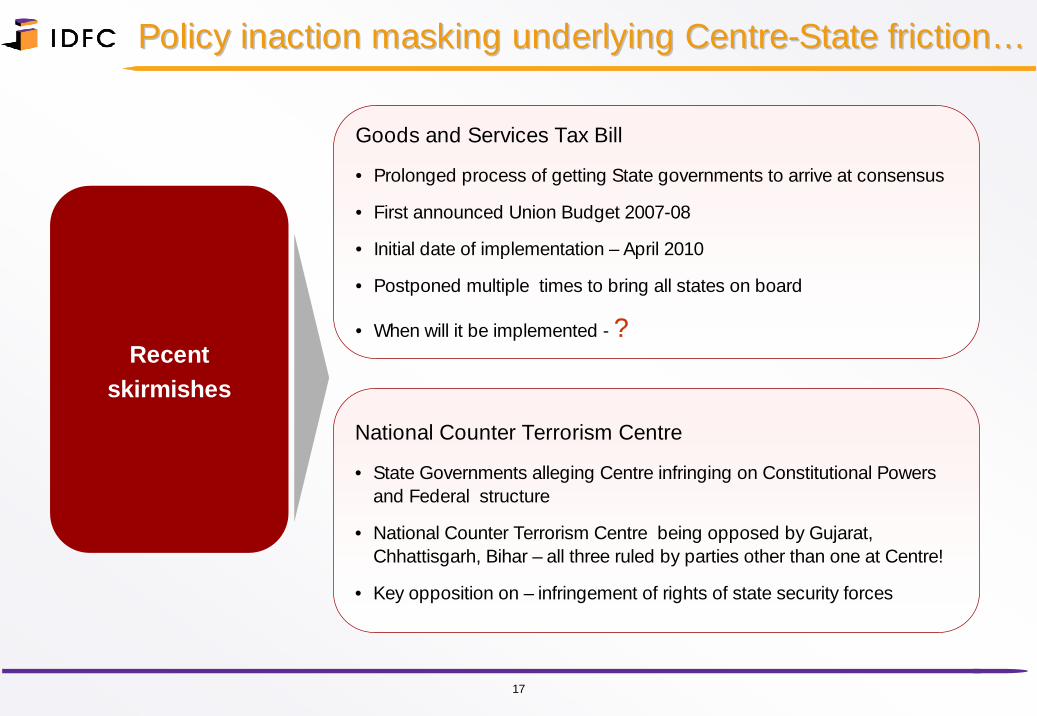

Policy inaction masking underlying CentrePolicy inaction masking underlying Centre--State frictionState friction……

Recent skirmishes

Goods and Services Tax Bill

• Prolonged process of getting State governments to arrive at consensus

• First announced Union Budget 2007-08

• Initial date of implementation – April 2010

• Postponed multiple times to bring all states on board

• When will it be implemented - ?

National Counter Terrorism Centre

• State Governments alleging Centre infringing on Constitutional Powers and Federal structure

• National Counter Terrorism Centre being opposed by Gujarat, Chhattisgarh, Bihar – all three ruled by parties other than one at Centre!

• Key opposition on – infringement of rights of state security forces

1818

Economic OutlookEconomic Outlook

So Is there hope for

the economy??

1919

Changes in Indian economy post Changes in Indian economy post liberalisationliberalisation……

• Economy no longer solely driven by Central policy

• States competing against each other for economic development

• Competition between States for attracting

Capital

Investments

Creation of employment opportunities

Increased economic activities

• Private sector investment gravitates towards states offering better infrastructure and governance

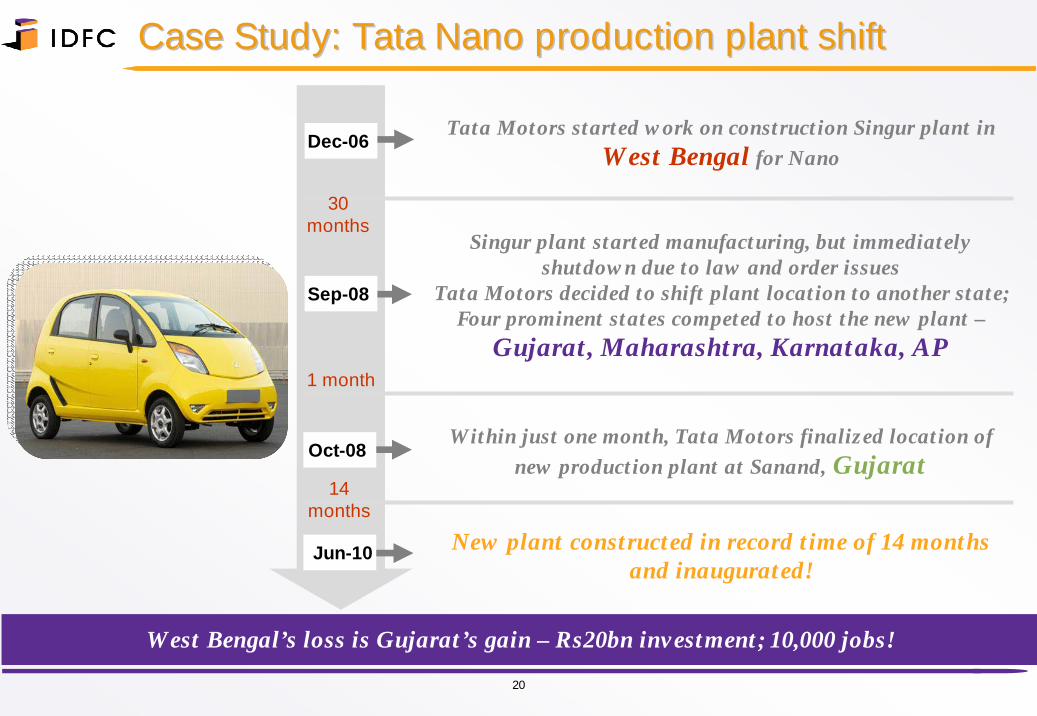

Case Study: Tata Case Study: Tata NanoNano production plant shiftproduction plant shift

20

Tata Motors started work on construction Singur plant in West Bengal for Nano

Dec-06

Sep-08

Oct-08

Jun-10

Within just one month, Tata Motors finalized location of new production plant at Sanand, Gujarat

Singur plant started manufacturing, but immediately shutdown due to law and order issues

Tata Motors decided to shift plant location to another state; Four prominent states competed to host the new plant –

Gujarat, Maharashtra, Karnataka, AP

New plant constructed in record time of 14 months and inaugurated!

30 months

1 month

14 months

West Bengal’s loss is Gujarat’s gain – Rs20bn investment; 10,000 jobs!

2121

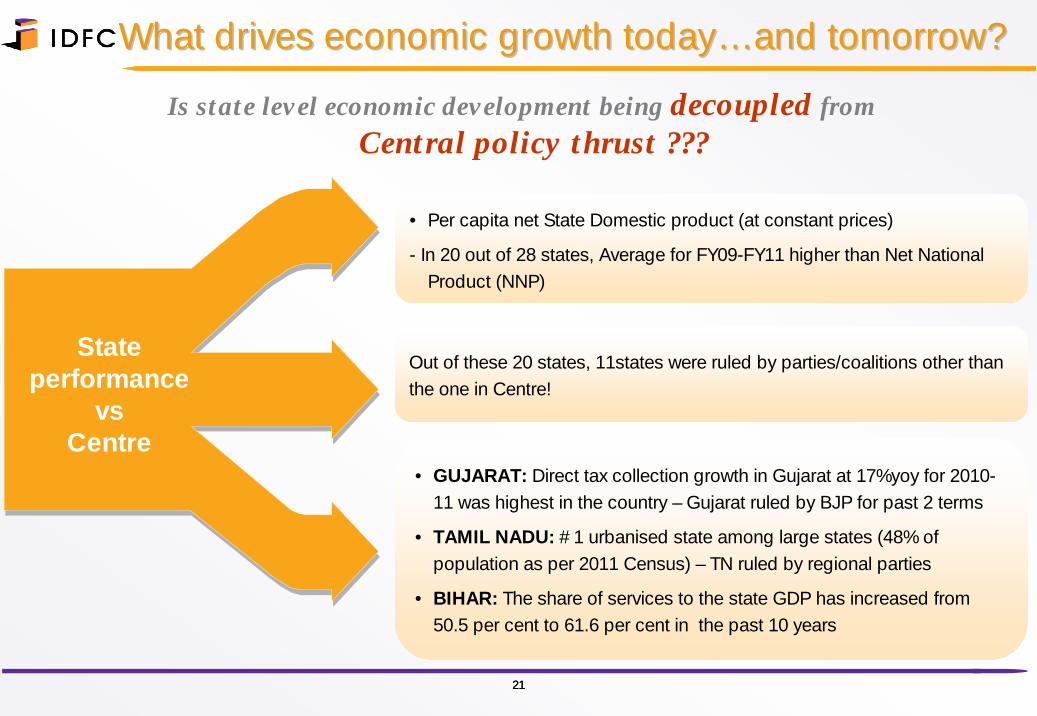

Is state level economic development being decoupled from Central policy thrust ???

What drives economic growth todayWhat drives economic growth today……and tomorrow?and tomorrow?

State performance

vsCentre

• Per capita net State Domestic product (at constant prices)

- In 20 out of 28 states, Average for FY09-FY11 higher than Net National Product (NNP)

Out of these 20 states, 11states were ruled by parties/coalitions other than the one in Centre!

• GUJARAT: Direct tax collection growth in Gujarat at 17%yoy for 2010-11 was highest in the country – Gujarat ruled by BJP for past 2 terms

• TAMIL NADU: #1 urbanised state among large states (48% of population as per 2011 Census) – TN ruled by regional parties

• BIHAR: The share of services to the state GDP has increased from 50.5 per cent to 61.6 per cent in the past 10 years

2222

“In the happiness of his subjects lies the King’s happiness; In their welfare his welfare,

He shall not consider as good, only that which pleases him,but treat as beneficial to him, whatever pleases his subjects”

What drives economic growth today..&.. tomorrow?What drives economic growth today..&.. tomorrow?

Are today’s ‘Kings’ (politicians) rediscovering this maxim….at least at the state level?

“The root of wealth is economic activity and lack of it brings material distress. A king can achieve the desired objectives and abundance of riches by undertaking productive economic activity, in the absence of which, both current prosperity and

future growth are in danger of destruction. ”

– Chanakya, Arthashastra

– Chanakya, Arthashastra

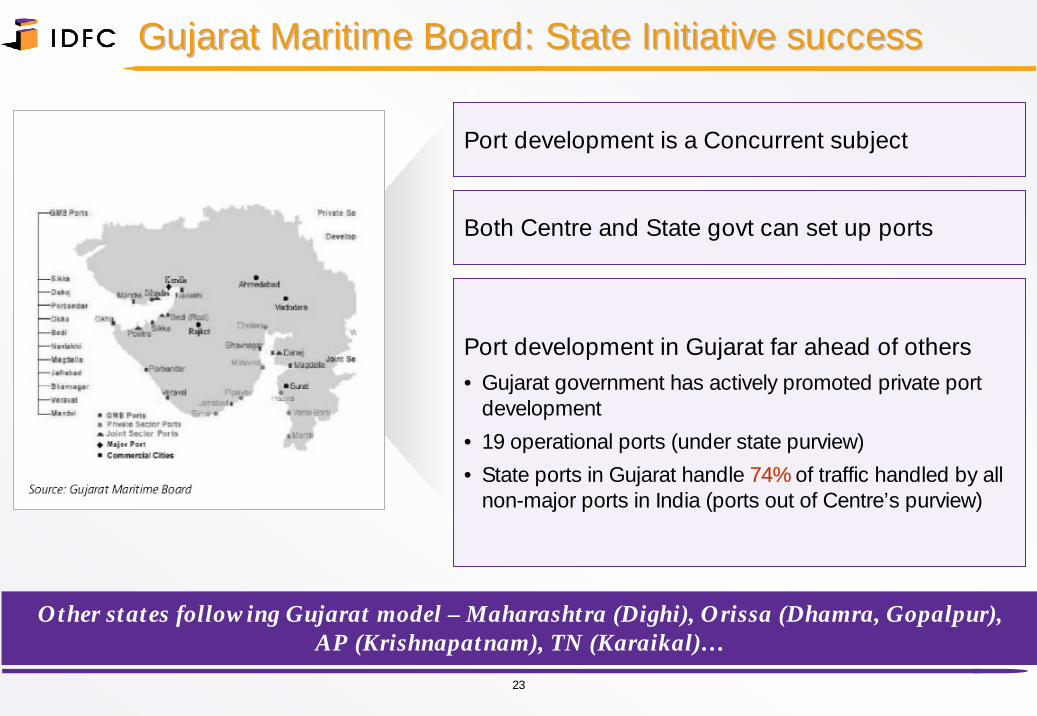

Gujarat Maritime Board: State Initiative successGujarat Maritime Board: State Initiative success

23

Other states following Gujarat model – Maharashtra (Dighi), Orissa (Dhamra, Gopalpur), AP (Krishnapatnam), TN (Karaikal)…

Port development is a Concurrent subject

Both Centre and State govt can set up ports

Port development in Gujarat far ahead of others• Gujarat government has actively promoted private port

development

• 19 operational ports (under state purview)

• State ports in Gujarat handle 74% of traffic handled by all non-major ports in India (ports out of Centre’s purview)

Bihar policy decisions: State Initiative successBihar policy decisions: State Initiative success

24

The UN gave $30,000 award to Bihar for its simplified taxation model!

Once upon a time ….

“Bihar…a place where civilization ends…” - V S Naipaul, Nobel-prize winning author

Today….• Only state with 50% seats in municipal bodies reserved for women

• Fast track courts – fastest judgment delivered in 13 days

• 5,000 ex-soldiers recruited into ‘special auxilliary force’ to check crime

• New and simplified ‘Patna model of taxation’

• Property taxes based on local area and use of property

• Other states following similar model

• 50% decline in girl students’ dropout rate – after the state government spent Rs2bn providing bicycles to girl students reaching 9th standard

• Innovative means of tackling corruption – attach properties of corrupt bureaucrats

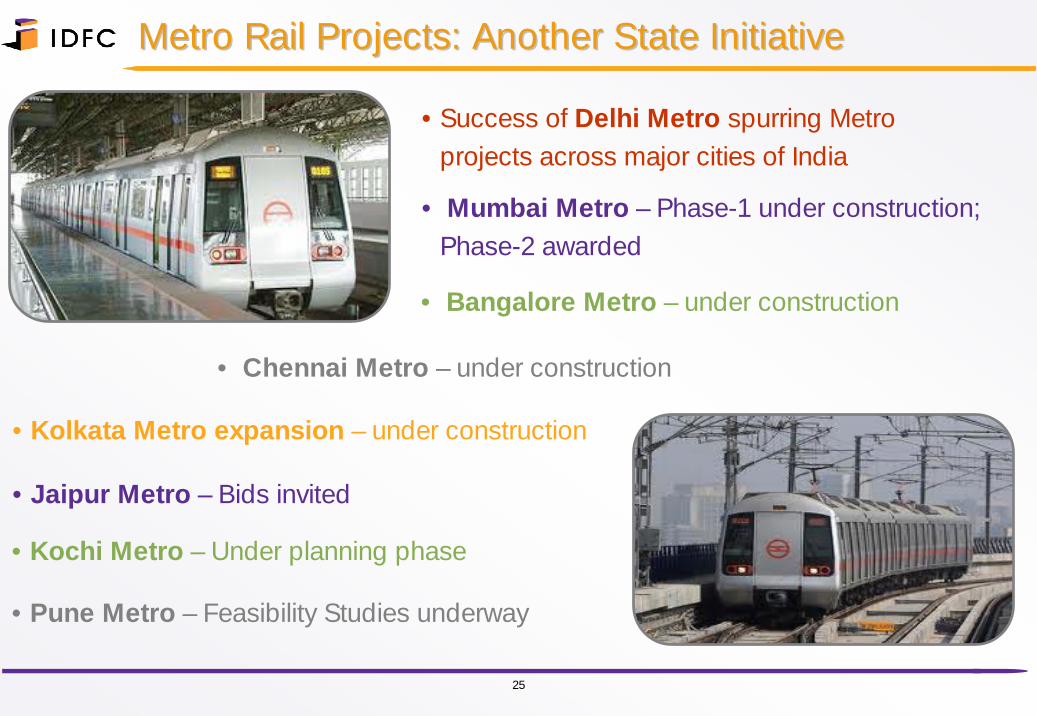

Metro Rail Projects: Another State InitiativeMetro Rail Projects: Another State Initiative

25

•Success of Delhi Metro spurring Metro projects across major cities of India

• Mumbai Metro – Phase-1 under construction; Phase-2 awarded

• Bangalore Metro – under construction

• Chennai Metro – under construction

•Kolkata Metro expansion – under construction

•Jaipur Metro – Bids invited

•Kochi Metro – Under planning phase

•Pune Metro – Feasibility Studies underway

(12)

-

12

24

36

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12

FII Net investment ($bn) FDI Investment ($bn)

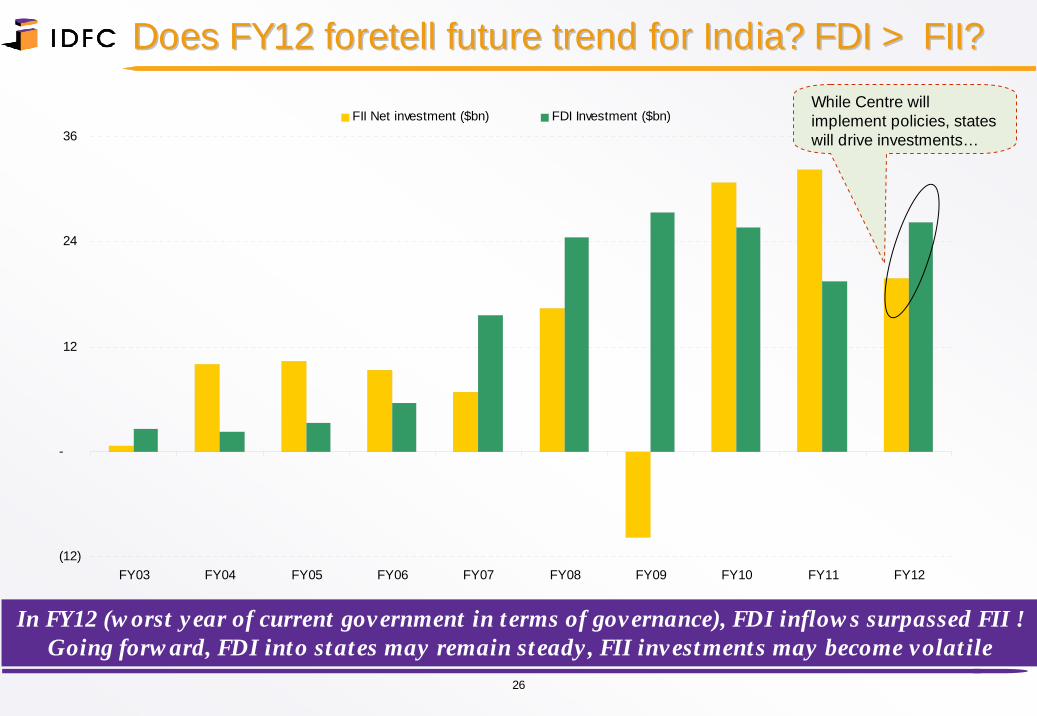

Does FY12 foretell future trend for India? FDI > FII? Does FY12 foretell future trend for India? FDI > FII?

26

In FY12 (worst year of current government in terms of governance), FDI inflows surpassed FII !Going forward, FDI into states may remain steady, FII investments may become volatile

While Centre will implement policies, states will drive investments…

Crystal gazingCrystal gazing…….Weak Centre.Weak Centre…….Stronger states?.Stronger states?

27

Is local economic growth giving State governments leverage over Centre?

…increasingly ‘younger’ electorate forcing governments to focus on economic growth …

…reality increasingly accepted by regional parties….

Major policy decisions still in Centre’s purview…

…and enforced by recent election results…

…but increasing autonomy to be given to States…

Competition for showcasing economic growth to voters a reality…

E.g. FDI in retail, Land Bill, Environmental policies

Development focused parties re-elected in Gujarat (BJP), Bihar (JD)

Difficulty in administering geographically large and populous country like India

Election manifestos of winning parties focusing on economic growth rather than freebies

Political Political power power shifting shifting to to statesstates??

Crystal gazingCrystal gazing…….But what can go wrong?.But what can go wrong?

28

Will State Governments pick up the gauntlet of economic development within their scope?

State Governments squandering away mandate for economic development….

.…by pandering to populist (read money-losing) policies; E.g. no increase in power tariffs in Tamil Nadu for past five years, delays in power tariff increase in WB

…State fiscal position deteriorating due to political largess'…

Crystal gazing...What will CentreCrystal gazing...What will Centre--State relation be like?State relation be like?

29

How will the Centre-State relationship appear in the future of India?

Even if one State Government falters on economic development, others waiting to capture the opportunity…case in point – Tata Nano production shift to Gujarat

Stronger economic growth will embolden states to oppose Central dictats…..case in point – NCTC Bill

…Increasing decentralisation of economic policy making

…States to be the ‘ground zero’ for both politics and economics, shifting focus away from Centre…

In letter, In letter, ““Union of StatesUnion of States””, but in spirit , but in spirit ““United States of IndiaUnited States of India””??

30

3232

DisclaimerDisclaimer

Our research is also available on Bloomberg and Thomson Reuters

This document has been prepared by IDFC Securities Ltd (IDFC SEC). IDFC SEC and its subsidiaries and associated companies are a full-service, integrated investment banking, investment management and brokerage group. Our research analysts and sales persons provide important input into our investment banking activities.

This document does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

The information contained herein is from publicly available data or other sources believed to be reliable. While we would endeavor to update the information herein on reasonable basis, the opinions and information in this report are subject to change without notice and IDFC SEC, its subsidiaries and associated companies, their directors and employees (“IDFC SEC and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent IDFC SEC and affiliates from doing so. Thus, the opinions expressed herein should be considered those of IDFC SEC as of the date on this document only. We do not make any representation either express or implied that information contained herein is accurate or complete and it should not be relied upon as such.

The information contained in this document has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. The investment discussed or views expressed in the document may not be suitable for all investors. Investors should make their own investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved) and investment decisions based upon their own financial objectives and financial resources. Investors assume the entire risk of any use made of the information contained in the document. Investments in general involve some degree of risk, including the risk of capital loss. Past performance is not necessarily a guide to future performance and an investor may not get back the amount originally invested.

Foreign currency-denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or the price of, or income derived from, the investment. In addition, investors in securities, the values of which are influenced by foreign currencies, effectively assume currency risk.

Affiliates of IDFC SEC may have issued other reports that are inconsistent with and reach different conclusions from, the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject IDFC SEC and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this document may come are required to inform themselves of, and to observe, such applicable restrictions.

Reports based on technical analysis centers on studying charts of a stock's price movement and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

IDFC SEC and affiliates, their directors, officers, and employees may from time to time have positions in, purchase or sell, or be materially interested in any of the securities mentioned or related securities. IDFC SEC and affiliates may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall IDFC SEC, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind including but not limited to any direct or consequential loss or damage, however arising, from the use of this document. Any comments or statements made herein are those of the analyst and do not necessarily reflect those of IDFC SEC and affiliates.

This document is subject to changes without prior notice and is intended only for the person or entity to which it is addressed and may contain confidential and/or privileged material and is not for any type of circulation. Any review, retransmission, or any other use is prohibited.

Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. IDFC SEC will not treat recipients as customers by virtue of their receiving this report.IDFC Capital (USA) Inc. has reviewed the report and, to the extent that it includes present or past information, it is believed to be reliable, although its correctness cannot be assured.

Additional Disclosures of interest:1. IDFC SEC and its affiliates (i) may have received compensation from the company covered herein in the past twelve months for investment banking services; or (ii) may expect to receive or intends to seek compensation for investment-banking services from the subject company in the next three months from publication of the research report.

2. Affiliates of IDFC SEC may have may have managed or co-managed in the previous twelve months a private or public offering of securities for the subject company.

3. IDFC SEC and affiliates collectively do not hold more than 1% of the equity of the company that is the subject of the report as of the end of the month preceding the distribution of the research report.

4. IDFC SEC and affiliates are not acting as a market maker in the securities of the subject company.

Explanation of Ratings:

1. Outperformer : More than 5% to Index 2. Neutral : Within 0-5% (upside or downside) to Index3. Underperformer : Less than 5% to Index

Copyright in this document vests exclusively with IDFC Securities Ltd.