Embed Size (px)

Citation preview

‘India, NCR: Development potential, Competitive advantage and Costs of a

booming Automotive sector’

Lorenza Monaco, PhD Candidate, SOAS, University of London

c.MET 05, Ancona - June 2012

A research work in progress...

� Research work started for the University of Naples, ‘L’Orientale’, in 2009 (LS)

� Here, overall picture of first findings and remarks from a field research carried out in India, National Capital Region (NCR) from Nov 2011 to April 2012

� Fieldwork part of a PhD programme in Development Studies at SOAS, University of London, UK

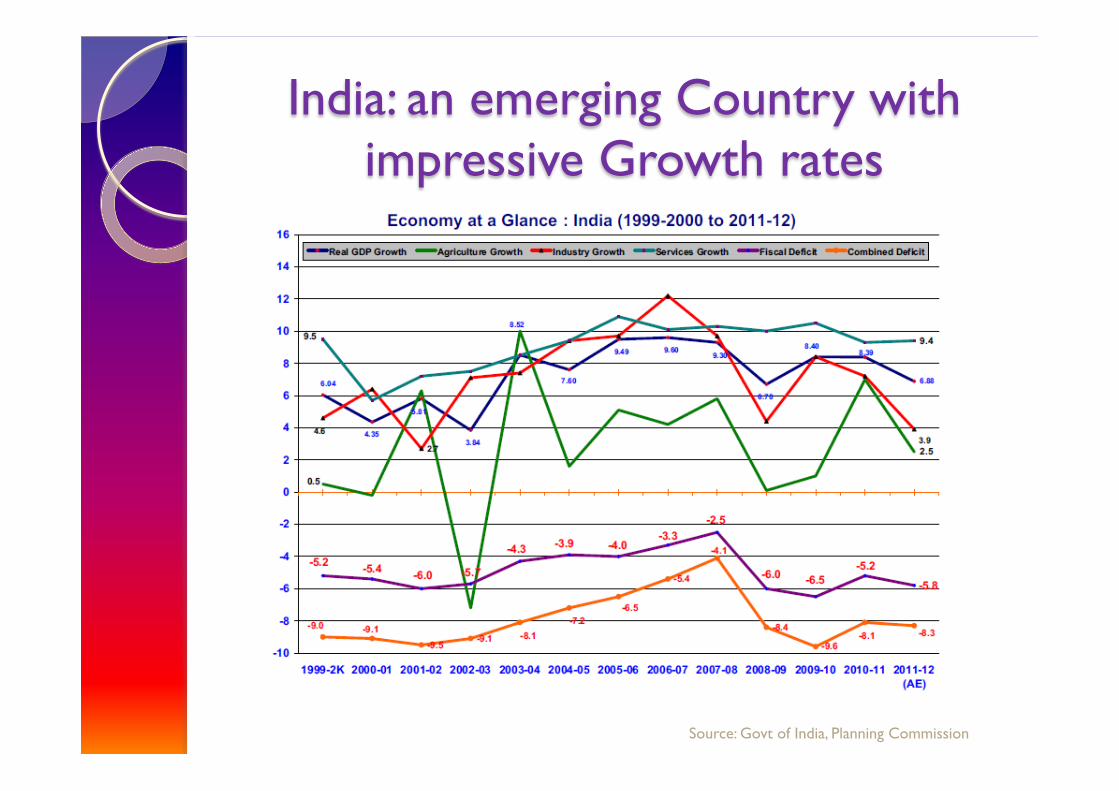

India: an emerging Country with impressive Growth rates

Source: Govt of India, Planning Commission

World GDP Growth per group of Countries

Source: Govt of India, Planning Commission

Automotive: a booming sector � Production: - In March-April 2011 production growth of 27.45% was recorded

(cumulative production); - In the same year, the Industry produced 17,916,035 vehicles (75% 2-

wheelers, 17% passenger vehicles, 4% 3-wheelers, 4% commercial vehicles);

� Domestic Sales: - In 2010/11 Domestic Sales grew at 26.17% (15,513,156 vehicles);

- Passenger vehicles segment grew by 29.16%, Commercial vehicles by 26.97%, 2-wheelers by 25.82%, 3-wheelers by 19.44%;

� Exports:

- During March-April 2011, overall automobile exports registered a growth rate of 29.64%;

- Passenger vehicles grew by 1.64%, Commercial vehicles by 69.51%, 2-wheelers by 35.04%, 3-wheelers by 55.86%.

Source: SIAM, Industry Profile 2010-11

Indian Automobile: a statistical profile

Source: SIAM, 2009-11 Statistical Profile

Auto Policies in Globalising India � Until 1991, highly protected sector and strong incentives to domestic

supply – Phased Manufacturing Programme (PMP) – only few Indian OEMs dominated the market – timid steps towards liberalisation (Ranawat and Tiwari, 2009);

� Through the 1991 New Industrial Policy, partial easing of market access (increasing number of JVs with foreign Companies, but limited share), expansion of range, technology and number of component suppliers (Narayanan and Vashisht, 2008);

� Auto Policy 2002: complete liberalisation - full abolition of QRs, licences and import duties, compliance with WTO rules, allowance of foreign participation upto 100%, incentives for investment in R&D (Narayanan and Vashisht, 2008; Ranawat and Tiwari, 2009);

� 2005/2006 – progressive steps towards integration on world markets – FTAs;

� Automotive Mission Plan 2006 – 2016: markedly investor–friendly, policies targeted on encouraging growth, domestic competition and innovation, stress on output and employment increase, infrastructure improvement, environment, safety regulations & certification systems (MHI&PE, Govt of India, 2006).

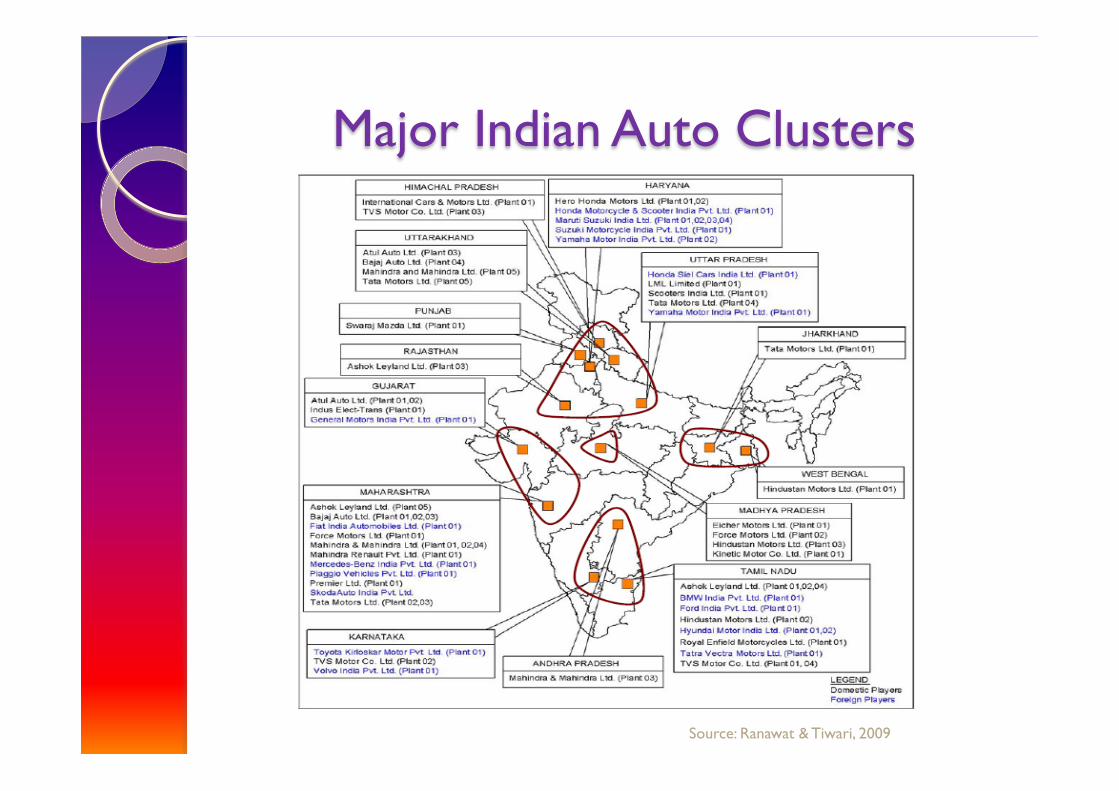

Major Indian Auto Clusters

Source: Ranawat & Tiwari, 2009

OEMs distribution on Indian territory

Chenglepet

Chennai

Hesur

Bangalore

Zaheerabad Pune

Mumbai

Nashik

Rajkot

Panchmahal

Aurangabad Bhandara

Pithampur • Force Motors/

MAN

Jamshedpur

Kolkata Jabalpur

Lucknow

Faridabad

Guatam Budh Nagar

New Delhi

Punjab

Alwar

Rewari

Gurgaon

Source: ANFIA, Italy

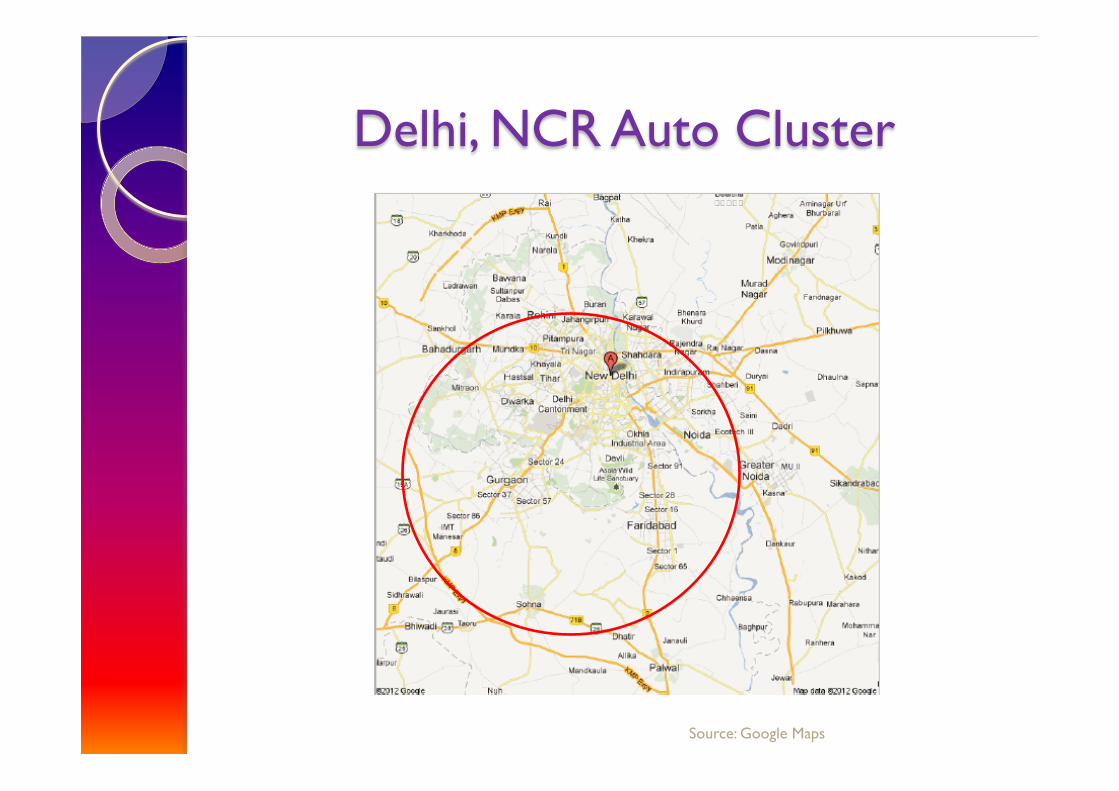

Delhi, NCR Auto Cluster

Source: Google Maps

NCR: Competitiveness... � Basic advantages of Indian Manufacturing: average product

quality at affordable prices (Narayanan & Vashisht, 2008), good engineering and IT skills + language proficiency in English among workers, low production and labour costs (Noble, 2006; Ranawat & Tiwari, 2009);

� Relative advantages of being located in the NCR: largest pool of young, skilled and educated workers hired directly through Colleges, proximity to services, institutions, business associations based in Delhi, better transport system and infrastructure provision than in other clusters (except Mumbai – Pune), important export centre, strong vendor base linked to big and old players (Maruti, Hero, Honda), closer access to retail market (NCR largest car market in the Country), until recently, weak labour movement, due to a newly industrialised area, management-friendly local Government (Haryana).

...and Costs

Lately, the following ‘disadvantages’ have emerged in the NCR:

� Clogged roads and transports; � Government taking rather weak positions; � Strong and prolonged Labour unrest ->

massive protests at Maruti (2000), Honda (2005), Rico (2009), Maruti – Suzuki (2011), over issues concerning political representation, minimum wage, contracts and working conditions.

Research Questions � Research questions formulated after the initial literature review have

undergone frequent changes and evolutions while experiencing the ‘field reality’ -> even more queries now!

� Some broad points, still under assessment are: - What kind of role is the Auto sector playing within Indian Industrial

Development? Is it really leading its Manufacturing Growth? Can this sector have spill-over/ multiplying effects over other Industrial sectors? Is this Growth producing benefits in terms of Employment?

- What kind of Corporate Strategies have been pursued by OEMs operating in the NCR, in the name of ‘flexibility’ and ‘competitiveness’? How have these shaped the Industrial Relations system in the area?

- What is the meaning of the recent Labour unrest? What is really at stake, in particular at Maruti? To what extent Labour disputes will affect local Corporate Strategies?

- Costs and Benefits of an undeniably Competitive Growth: are benefits outweighing its costs, or the latter represent a too high price to pay, especially for Labour?

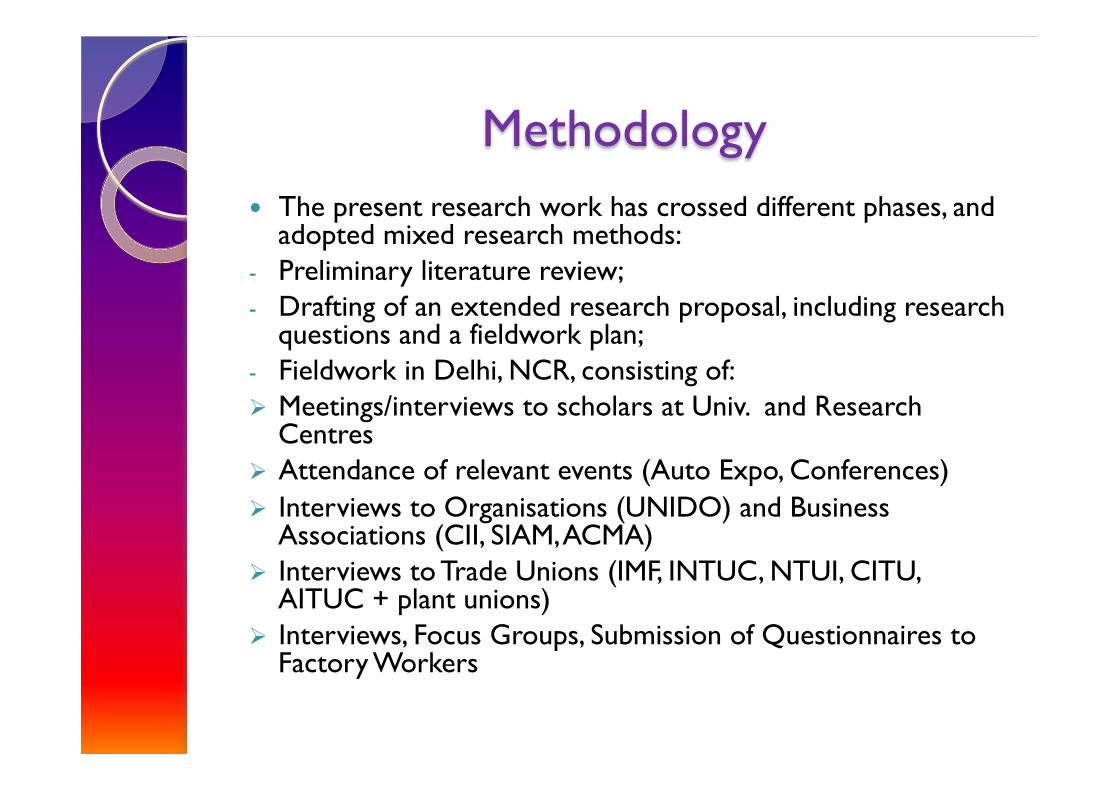

Methodology � The present research work has crossed different phases, and

adopted mixed research methods: - Preliminary literature review; - Drafting of an extended research proposal, including research

questions and a fieldwork plan; - Fieldwork in Delhi, NCR, consisting of: Ø Meetings/interviews to scholars at Univ. and Research

Centres Ø Attendance of relevant events (Auto Expo, Conferences) Ø Interviews to Organisations (UNIDO) and Business

Associations (CII, SIAM, ACMA) Ø Interviews to Trade Unions (IMF, INTUC, NTUI, CITU,

AITUC + plant unions) Ø Interviews, Focus Groups, Submission of Questionnaires to

Factory Workers

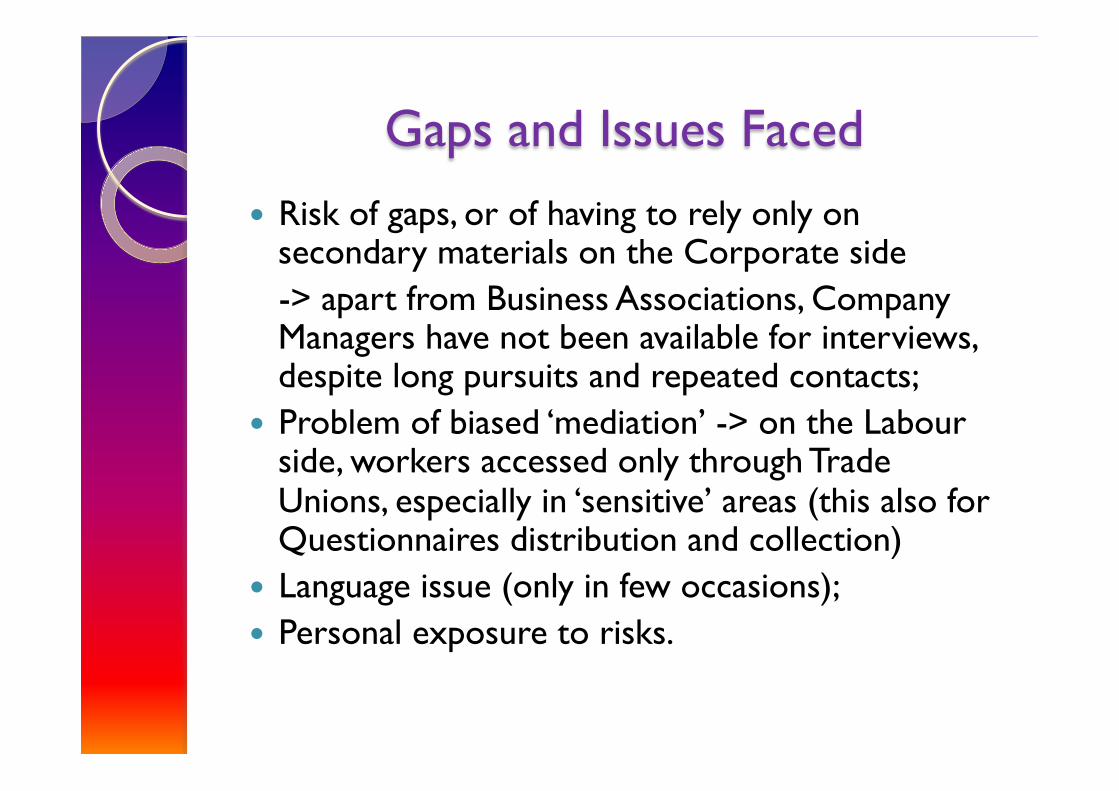

Gaps and Issues Faced � Risk of gaps, or of having to rely only on

secondary materials on the Corporate side -> apart from Business Associations, Company

Managers have not been available for interviews, despite long pursuits and repeated contacts;

� Problem of biased ‘mediation’ -> on the Labour side, workers accessed only through Trade Unions, especially in ‘sensitive’ areas (this also for Questionnaires distribution and collection)

� Language issue (only in few occasions); � Personal exposure to risks.

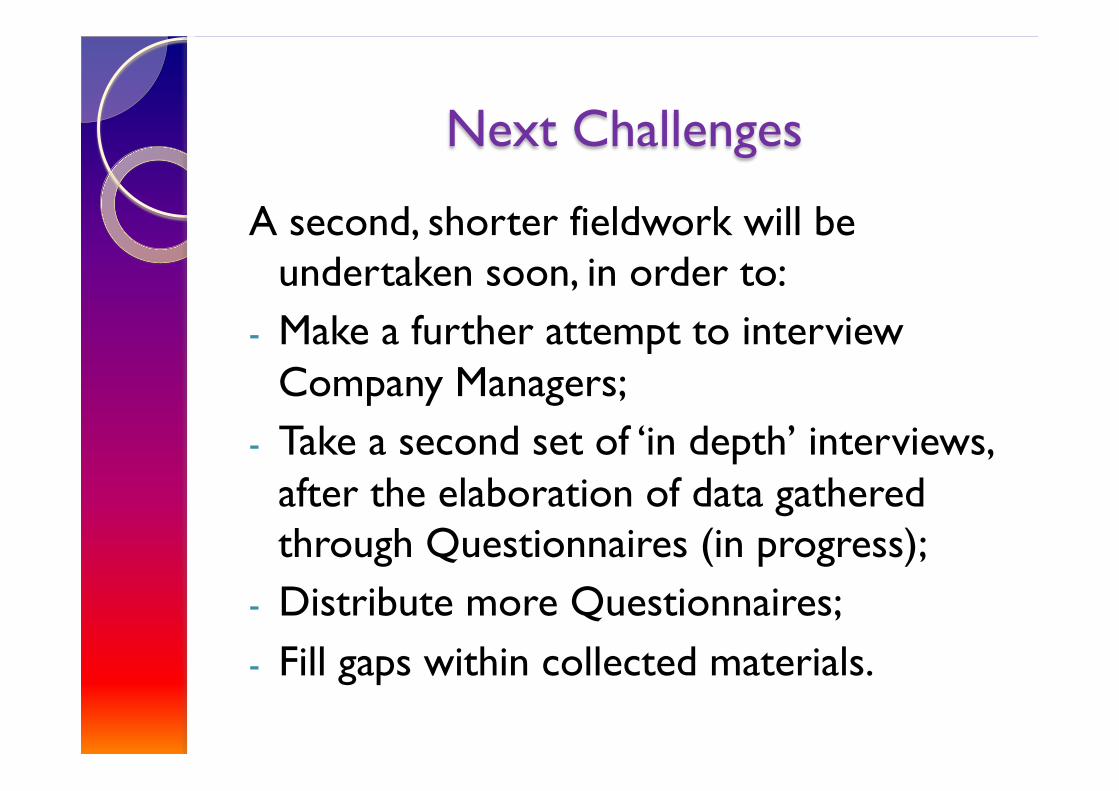

Next Challenges

A second, shorter fieldwork will be undertaken soon, in order to:

- Make a further attempt to interview Company Managers;

- Take a second set of ‘in depth’ interviews, after the elaboration of data gathered through Questionnaires (in progress);

- Distribute more Questionnaires; - Fill gaps within collected materials.

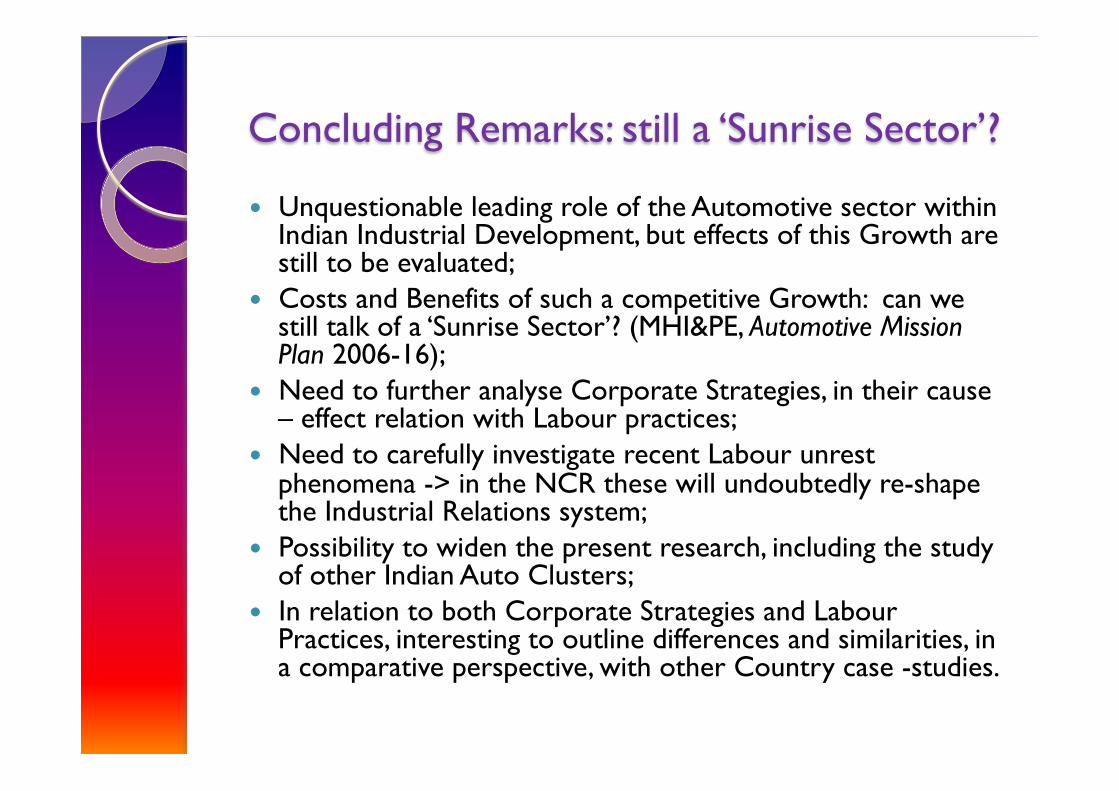

Concluding Remarks: still a ‘Sunrise Sector’?

� Unquestionable leading role of the Automotive sector within Indian Industrial Development, but effects of this Growth are still to be evaluated;

� Costs and Benefits of such a competitive Growth: can we still talk of a ‘Sunrise Sector’? (MHI&PE, Automotive Mission Plan 2006-16);

� Need to further analyse Corporate Strategies, in their cause – effect relation with Labour practices;

� Need to carefully investigate recent Labour unrest phenomena -> in the NCR these will undoubtedly re-shape the Industrial Relations system;

� Possibility to widen the present research, including the study of other Indian Auto Clusters;

� In relation to both Corporate Strategies and Labour Practices, interesting to outline differences and similarities, in a comparative perspective, with other Country case -studies.

Thank you!

Lorenza Monaco, BA, MA University of Naples ‘L’ Orientale’

PhD Candidate SOAS, University of London [email protected]