Embed Size (px)

DESCRIPTION

INDIA Inc. Opportunities Unlimited. Information Communication and Technology. Presented By :. Dr. Ajay Data. Key Messages. As a rapidly growing market and a key sourcing destination, India is increasingly becoming the center of global commercial interest and economic activity - PowerPoint PPT Presentation

Citation preview

This material was used by Data Infocom Limited during an oral presentation; it is not a complete record of the discussion. No part of this document may be circulated, quoted, or reproduced for distribution without prior written approval from Data Infocom Limted, India.

Presented By :

Key Messages

• As a rapidly growing market and a key sourcing destination, India is increasingly becoming the center of global commercial interest and economic activity

• IT-ITES, a poster-child for the new Indian economy, has grown by 25% (CAGR) over the past decade; exports alone have grown by over 36% (CAGR) over the same period

• Sector growth driven by sustained demand, and increasing service line depth and supply-side maturity based on strong fundamentals of abundant talent/skill, quality and service delivery expertise at a sustained cost-value proposition - reflecting India’s growing importance in the new world IT order

• The future holds significant opportunity for India – much larger than the aggressive targets set by the industry for itself; key stakeholders are undertaking several initiatives to ensure that Indian IT-ITES achieves its full potential

India is not just a land of mystics and wonders…

• India’s GDP has grown at nearly twice the global rate over past 20 years

• Steady annual growth in real GDP, industrial production and domestic demand of 5-6%

• Sustained real growth in foreign investment inflows (FDI and FII) since economic liberalization (1991)

• Cumulative forex reserves of ~USD 140bn

FY06 GDP Growth in India is Amongst the Fastest in the Region

Source: JM Morgan Stanley

Source: Citigroup

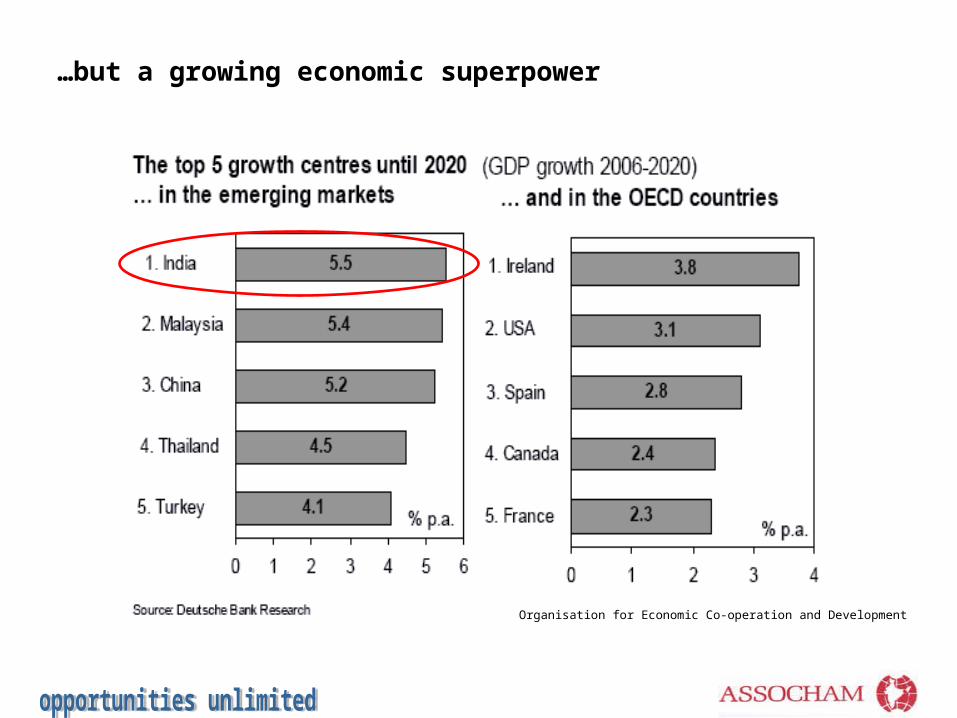

…but a growing economic superpower

Organisation for Economic Co-operation and Development

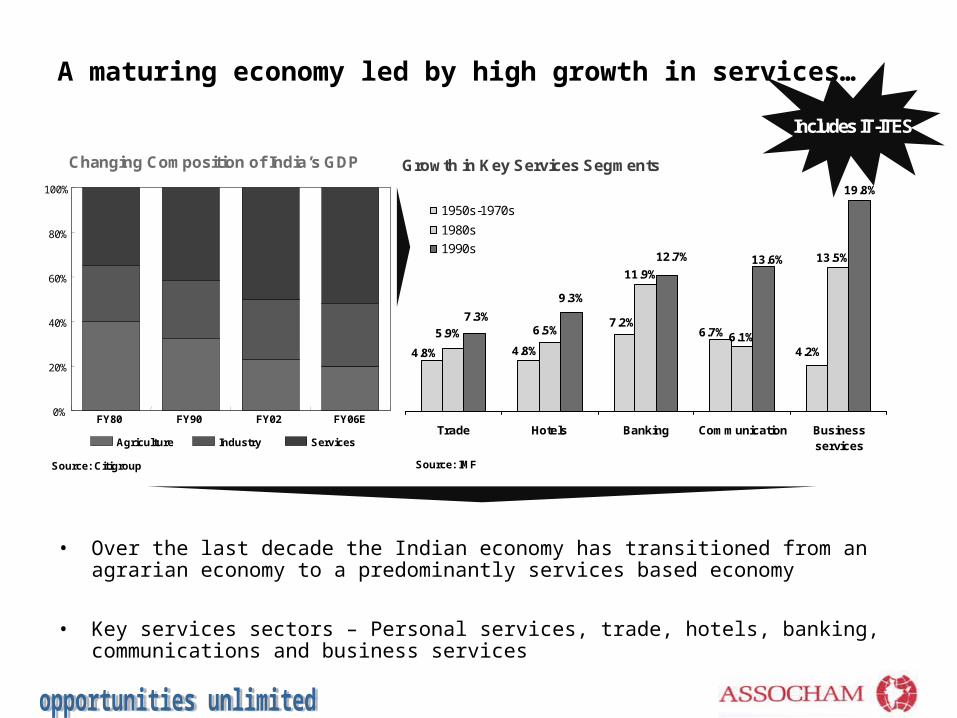

A maturing economy led by high growth in services…

• Over the last decade the Indian economy has transitioned from an agrarian economy to a predominantly services based economy

• Key services sectors – Personal services, trade, hotels, banking, communications and business services

Growth in Key Services Segments

4.2%

6.7%7.2%

4.8%4.8%

13.5%

6.1%

11.9%

6.5%5.9%

19.8%

13.6%12.7%

9.3%

7.3%

Trade Hotels Banking Communication Businessservices

1950s-1970s

1980s

1990s

Source: IMFSource: Citigroup

Changing Composition of India’s GDP

Includes IT-ITES

0%

20%

40%

60%

80%

100%

FY80 FY90 FY02 FY06E

Agriculture Industry Services

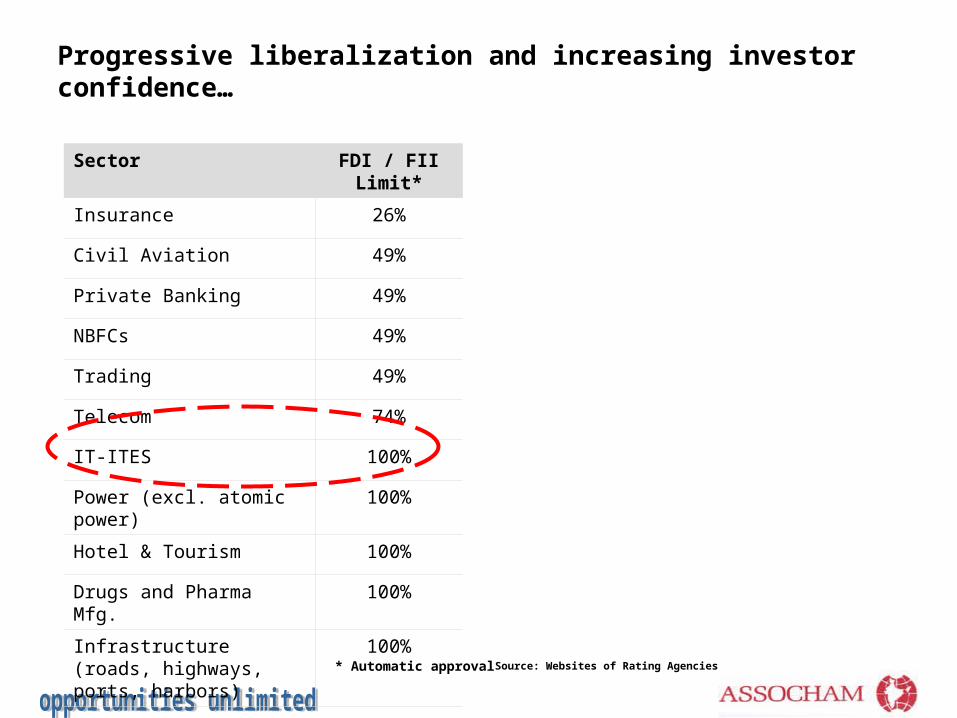

Progressive liberalization and increasing investor confidence…

Sector FDI / FII Limit*

Insurance 26%

Civil Aviation 49%

Private Banking 49%

NBFCs 49%

Trading 49%

Telecom 74%

IT-ITES 100%

Power (excl. atomic power) 100%

Hotel & Tourism 100%

Drugs and Pharma Mfg. 100%

Infrastructure (roads, highways, ports, harbors)

100%

* Automatic approval Source: Websites of Rating Agencies

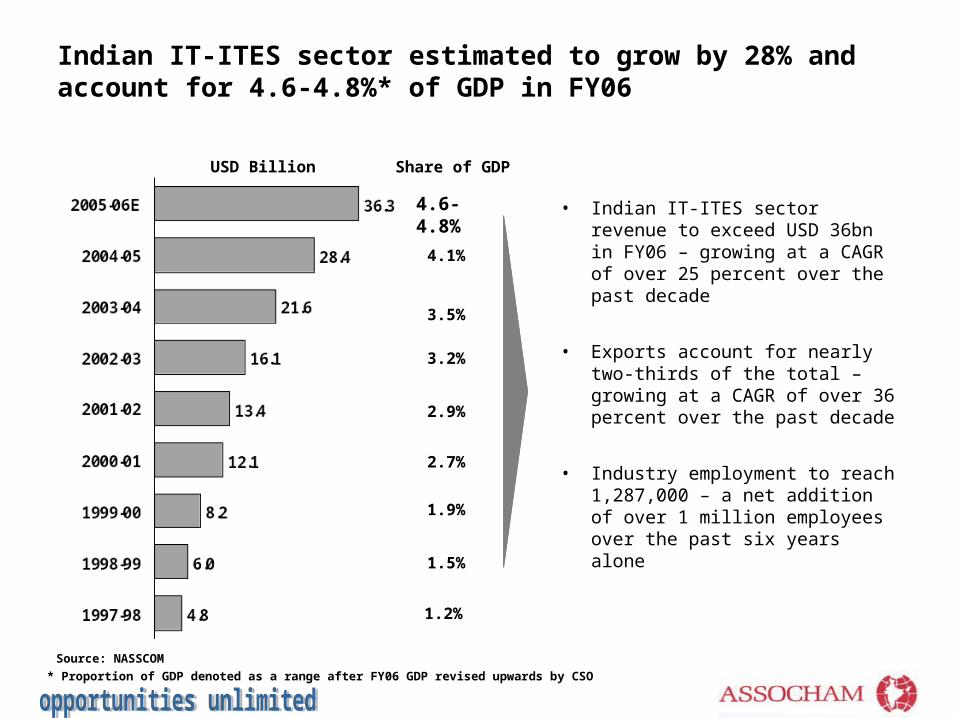

Indian IT-ITES sector estimated to grow by 28% and account for 4.6-4.8%* of GDP in FY06

• Indian IT-ITES sector revenue to exceed USD 36bn in FY06 – growing at a CAGR of over 25 percent over the past decade

• Exports account for nearly two-thirds of the total – growing at a CAGR of over 36 percent over the past decade

• Industry employment to reach 1,287,000 – a net addition of over 1 million employees over the past six years alone

4.6-4.8%

4.1%

3.5%

3.2%

2.9%

1.2%

1.5%

1.9%

2.7%

USD Billion Share of GDP

Source: NASSCOM

* Proportion of GDP denoted as a range after FY06 GDP revised upwards by CSO

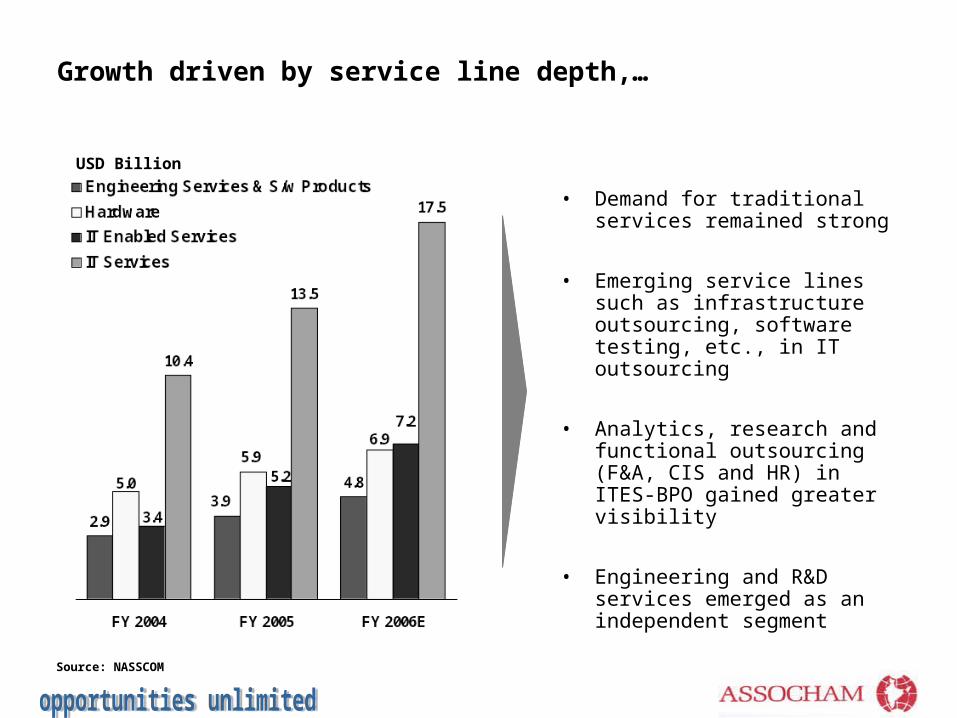

Growth driven by service line depth,…

• Demand for traditional services remained strong

• Emerging service lines such as infrastructure outsourcing, software testing, etc., in IT outsourcing

• Analytics, research and functional outsourcing (F&A, CIS and HR) in ITES-BPO gained greater visibility

• Engineering and R&D services emerged as an independent segment

USD Billion

Source: NASSCOM

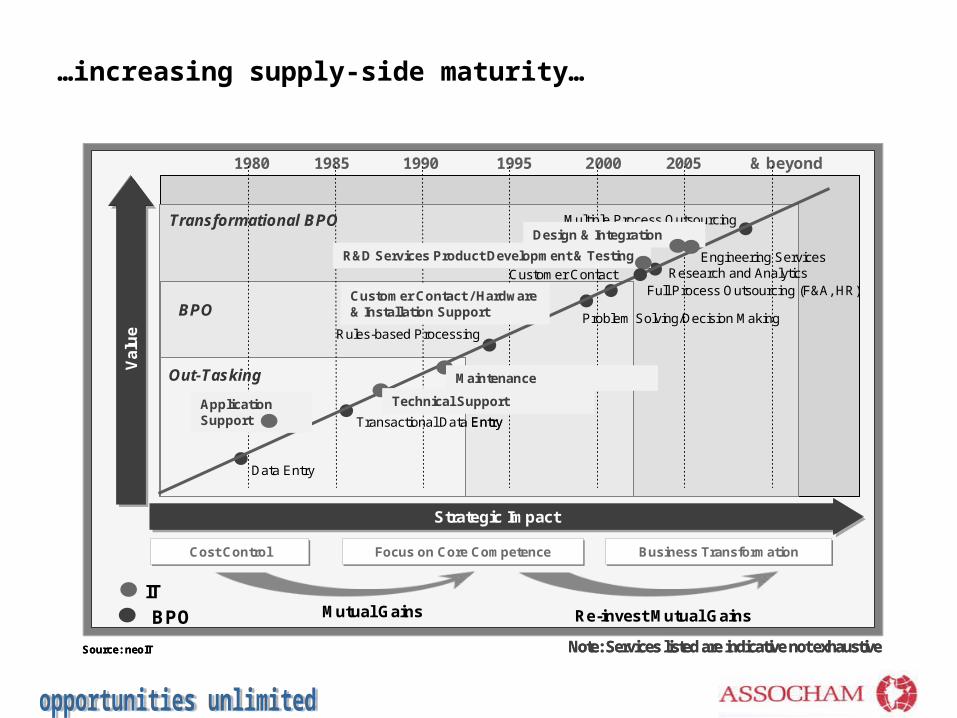

…increasing supply-side maturity…

1980 1985 1990 1995 2000 2005 & beyond

Mutual Gains Re-invest Mutual Gains

Strategic ImpactStrategic Impact

Va

lue

Va

lue

Full Process Outsourcing (F&A, HR)

Multiple Process Outsourcing

Rules-based ProcessingProblem Solving/Decision Making

Customer Contact

Transactional Data Entry

Data Entry

Cost ControlCost Control Focus on Core CompetenceFocus on Core Competence Business TransformationBusiness Transformation

Out-Tasking

BPO

Transformational BPO

Application Support

Technical Support

Customer Contact / Hardware & Installation Support

Maintenance

R&D Services Product Development & Testing

Design & Integration

ITBPO

Source: neoIT

Research and AnalyticsEngineering Services

Note: Services listed are indicative not exhaustive

1980 1985 1990 1995 2000 2005 & beyond

Mutual Gains Re-invest Mutual Gains

Strategic ImpactStrategic Impact

Va

lue

Va

lue

Full Process Outsourcing (F&A, HR)

Multiple Process Outsourcing

Rules-based ProcessingProblem Solving/Decision Making

Customer Contact

Transactional Data Entry

Data Entry

Transactional Data Entry

Data Entry

Cost ControlCost Control Focus on Core CompetenceFocus on Core Competence Business TransformationBusiness Transformation

Out-Tasking

BPO

Transformational BPO

Application Support

Technical Support

Customer Contact / Hardware & Installation Support

Maintenance

R&D Services Product Development & Testing

Design & Integration

ITBPO

Source: neoIT

Research and AnalyticsEngineering Services

Note: Services listed are indicative not exhaustive

IT services exports lead, accounting for 35% of the total, growing at 32-33% (FY06E)

Source: NASSCOM

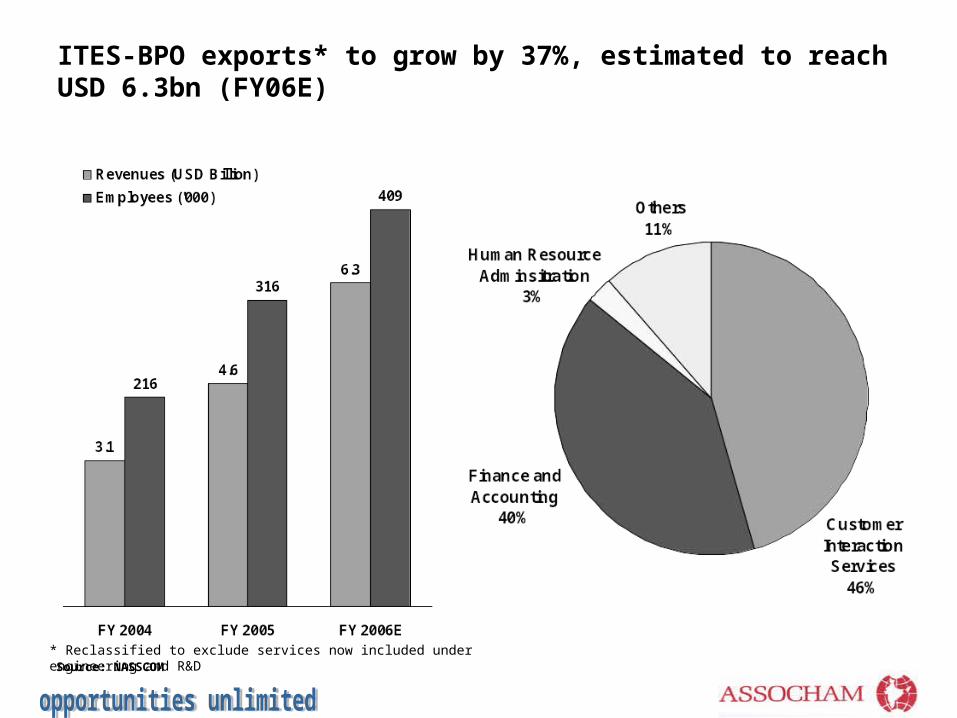

ITES-BPO exports* to grow by 37%, estimated to reach USD 6.3bn (FY06E)

* Reclassified to exclude services now included under engineering and R&D Source: NASSCOM

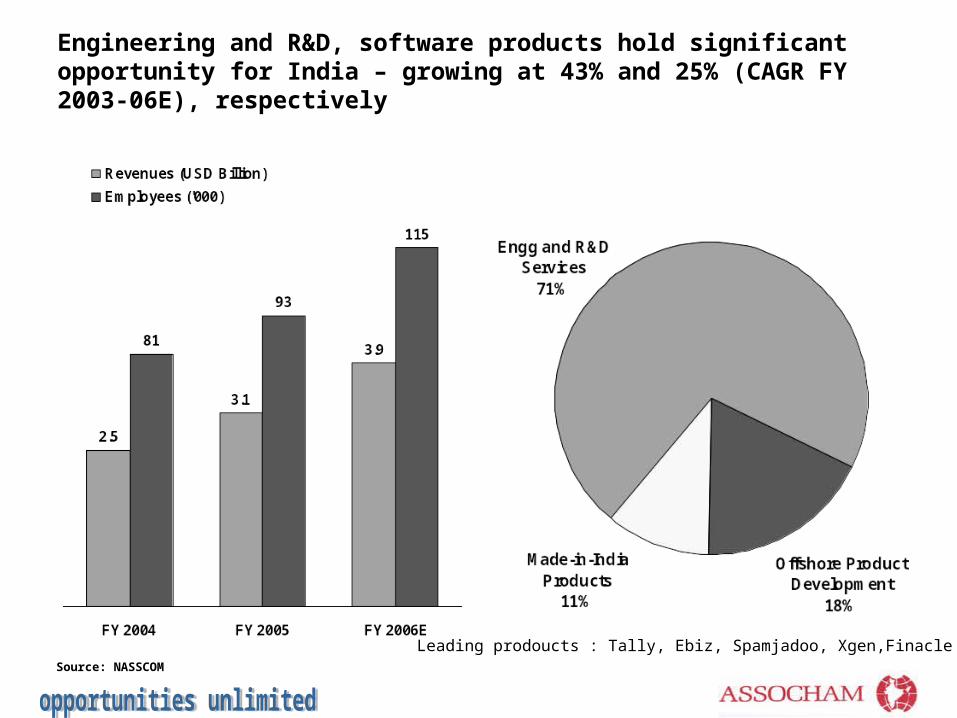

Engineering and R&D, software products hold significant opportunity for India – growing at 43% and 25% (CAGR FY 2003-06E), respectively

Source: NASSCOM

Leading prodoucts : Tally, Ebiz, Spamjadoo, Xgen,Finacle

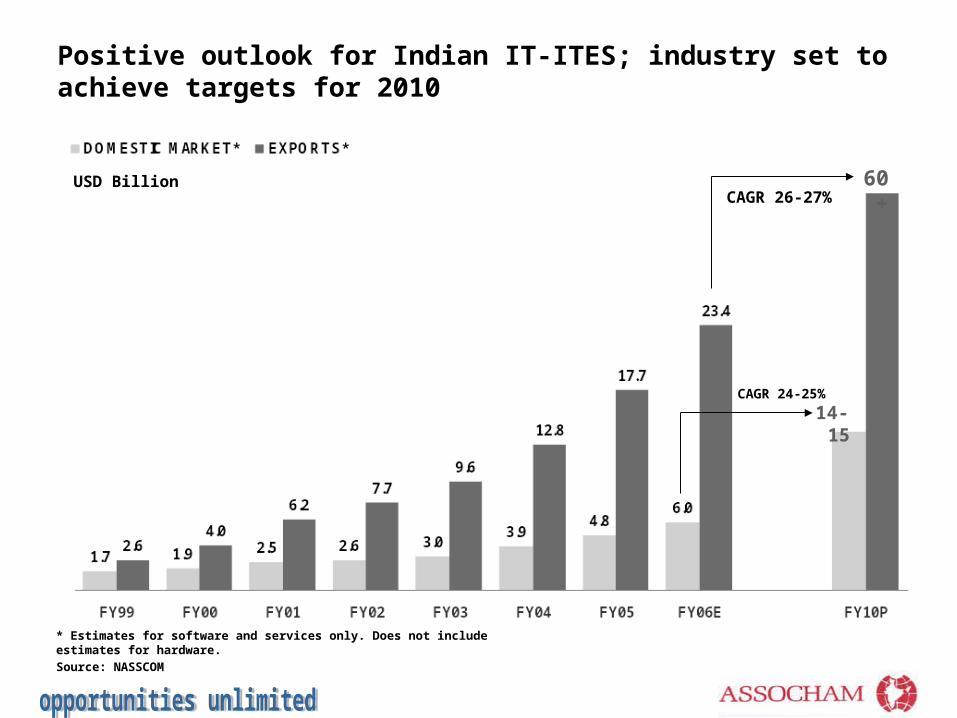

Positive outlook for Indian IT-ITES; industry set to achieve targets for 2010

14-15

60+USD BillionCAGR 26-27%

CAGR 24-25%

Source: NASSCOM

* Estimates for software and services only. Does not include estimates for hardware.

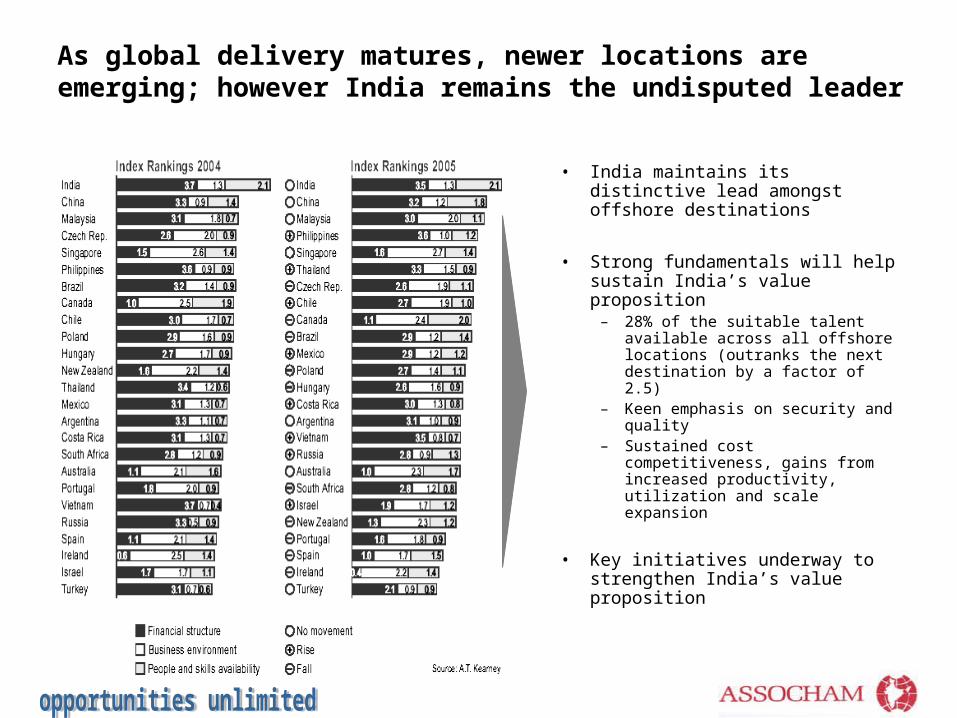

As global delivery matures, newer locations are emerging; however India remains the undisputed leader

• India maintains its distinctive lead amongst offshore destinations

• Strong fundamentals will help sustain India’s value proposition

– 28% of the suitable talent available across all offshore locations (outranks the next destination by a factor of 2.5)

– Keen emphasis on security and quality

– Sustained cost competitiveness, gains from increased productivity, utilization and scale expansion

• Key initiatives underway to strengthen India’s value proposition

India’s pillars of success – You can use this opportunity.

• Access to a large, growing pool of highly qualified talent

• A high degree of quality orientation and demonstrated service delivery expertise

• Keen emphasis on information security reflected in the comprehensive legal framework and elaborate security practices supplemented by enabling intervention

• World class telecommunication infrastructure

• International standards in real estate and office facilities

• Enabling (and progressively improving) business environment through strong government support; incentives, favorable regulations and policy

…delivered at a sustained and compelling cost-value proposition

Five key areas that India is focused on, to sustain its lead

• Enhancing the talent pool advantage – focus on skill development to better leverage the worlds largest working population

• Strengthening urban infrastructure in existing and emerging cities and emphasis on proactive regulatory reform to facilitate greater ease of doing business

• Driving a philosophy of operational excellence amongst industry players to ensure that India based delivery sustains world leading benchmarks in performance

• Catalyzing domestic market development

• Actively promoting an uncompromised agenda towards global free trade