Embed Size (px)

Citation preview

Ind AS Ind AS 1212Income TaxesIncome TaxesIncome TaxesIncome Taxes

ObjectivesObjectives

• Calculate taxes under Ind AS 12.

• Describe the recognition criteria for deferred tax liabilities and

assets.

• Explain the deferred tax effects on business combinations.

• Detail the recognition of deferred tax assets arising from unused tax • Detail the recognition of deferred tax assets arising from unused tax

losses or credits.

• Detail presentation and disclosure requirements of income taxes

ScopeScope

Ind AS 12 defines “income taxes” as including all domestic and foreign taxes, which are based on taxable profits.

Included in scope

– withholding tax (tax payable by components on distributions to parent)

Excluded from scope

– Other taxes (e.g. VAT, Business Tax) that are levied on another basis (e.g. on gross revenue)

– Methods of Accounting for Government grants

QuestionQuestion

• How should interest and penalties on income tax deficiencies be presented?

AnswerAnswer

• Interest and penalties assessed on income tax deficiencies should be presented based on their nature (i.e., either as a finance cost (interest) or operating expense (penalties)) because those items do not meet the definition of current or deferred income tax expense the definition of current or deferred income tax expense as defined in Ind AS 12.

Some DefinitionsSome Definitions

• Accounting Profit

– Profit or loss for a period per the books of account.

• Taxable Profit

– The profit (loss) for a period, determined in accordance with the rules established by the taxation authorities, upon which income taxes are payable (recoverable)payable (recoverable)

• Tax expense

– The aggregate amount included in the determination of profit or loss for the period in respect of current tax and deferred tax

• Current tax

– The amount of income taxes payable (recoverable) in respect of the taxable profit (tax loss) for a period.

Some Definitions (contd.)Some Definitions (contd.)

• Tax base

– It is the amount attributable to that asset or liability for tax purposes.

• Deferred tax assets

– The amounts of income taxes recoverable in future periods in respect of;

• Deductible temporary differences• Deductible temporary differences

• The carryforward of unused tax losses and credits

• Deferred tax liabilities

– The amounts of income taxes payable in future periods in respect of taxable temporary differences.

Measurement of Current and Deferred TaxMeasurement of Current and Deferred Tax

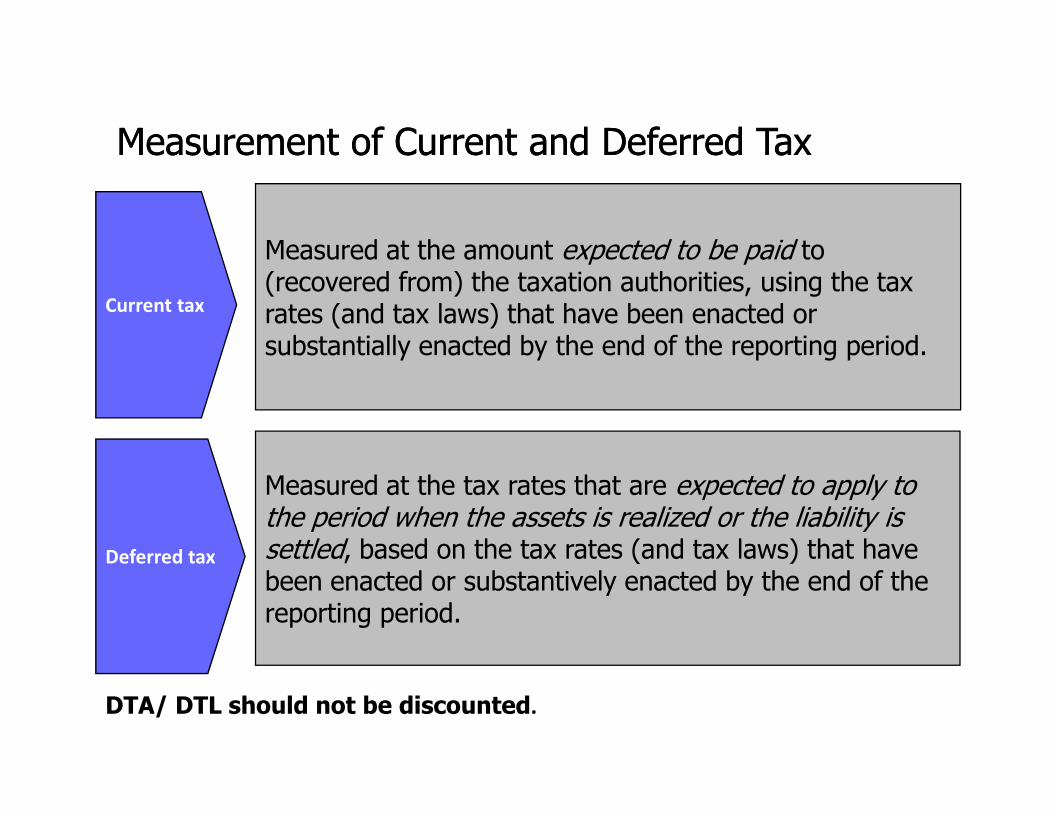

Current tax

Measured at the amount expected to be paid to (recovered from) the taxation authorities, using the tax rates (and tax laws) that have been enacted or substantially enacted by the end of the reporting period.

Deferred tax

Measured at the tax rates that are expected to apply to the period when the assets is realized or the liability is settled, based on the tax rates (and tax laws) that have been enacted or substantively enacted by the end of the reporting period.

DTA/ DTL should not be discounted.

Current TaxCurrent Tax

• Current tax for current and prior period, to the extent unpaid, should be recognized as a liability. Payment in excess of the amount due should be recognized as an asset.

• The benefit relating to a tax loss that can be carried • The benefit relating to a tax loss that can be carried back to recover current tax of a previous period should be recognized as an asset.

Deferred tax

• General Principle

– Balance sheet liability method

– Deferred taxes are recognized for temporary differences:

• Differences between the carrying amount of an asset or liability in the balance sheet and its tax base.the balance sheet and its tax base.

Temporary differencesTemporary differences

• Temporary differences are differences between the carrying amount of an asset or liability in the balance sheet and its tax base

- Taxable temporary differences

- Deductible temporary differences

Accounting for deferred tax Accounting for deferred tax ––a fivea five--step approachstep approach

1.Calculate tax base

2.Calculate temporary difference

3.Identify the temporary differences that give rise to deferred tax assets or liabilitiesdeferred tax assets or liabilities

4.Calculate deferred tax balances using appropriate tax rate

5.Recognise deferred tax in income, equity or as an adjustment to goodwill

Tax Base Tax Base

• Tax base of an asset is the amount that will bedeductible for tax purposes against any taxableeconomic benefits that will flow to an entity when itrecovers the carrying amount of the asset. If thoseeconomic benefits will not be taxable, the tax base ofeconomic benefits will not be taxable, the tax base ofthe asset is equal to its carrying amount.

• Tax base of an liability is its carrying amount, less anyamount that will be deductible for tax purposes inrespect of that liability in future periods.

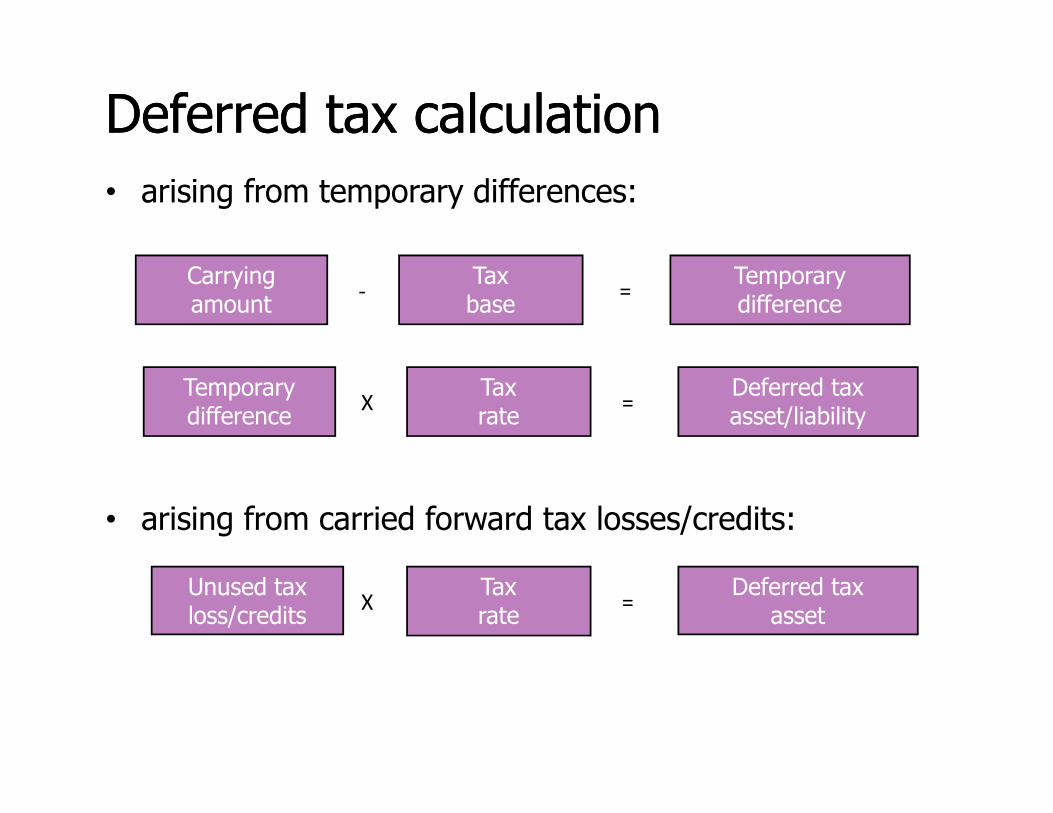

Deferred tax calDeferred tax calculationculation

• arising from temporary differences:

Carrying amount

Tax base

Temporary difference

– =-

Temporary difference

Tax rate

Deferred tax asset/liability

X =

• arising from carried forward tax losses/credits:

difference rate asset/liabilityX =

Unused tax loss/credits

Tax rate

Deferred tax asset

X =

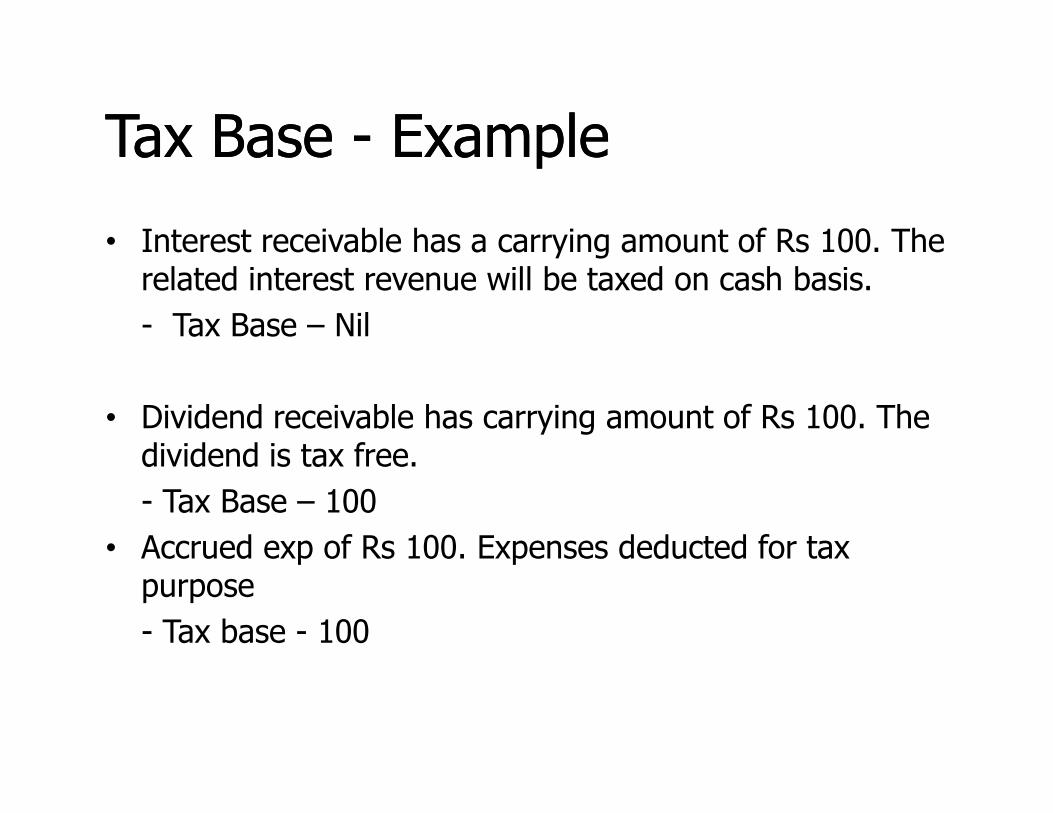

Tax Base Tax Base -- ExampleExample

• Interest receivable has a carrying amount of Rs 100. The related interest revenue will be taxed on cash basis.

- Tax Base – Nil

• Dividend receivable has carrying amount of Rs 100. The • Dividend receivable has carrying amount of Rs 100. The dividend is tax free.

- Tax Base – 100

• Accrued exp of Rs 100. Expenses deducted for tax purpose

- Tax base - 100

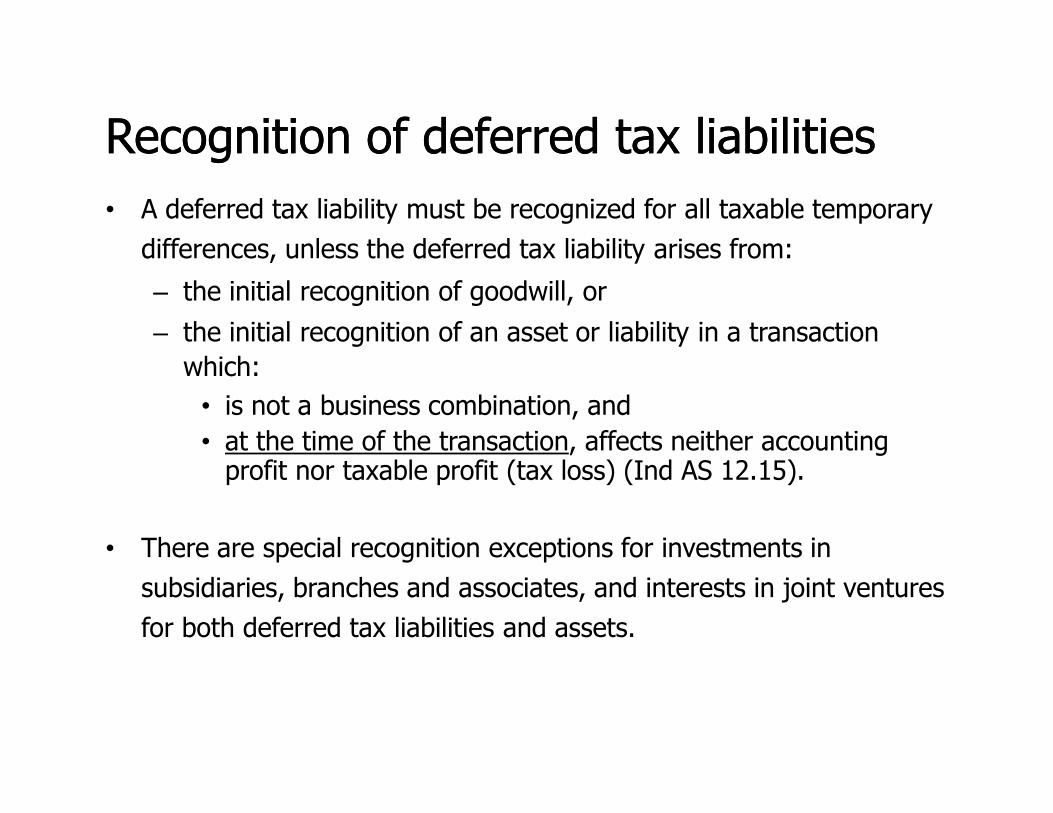

Recognition of deferred tax liabilitiesRecognition of deferred tax liabilities

• A deferred tax liability must be recognized for all taxable temporary

differences, unless the deferred tax liability arises from:

– the initial recognition of goodwill, or

– the initial recognition of an asset or liability in a transaction

which:

• is not a business combination, and• is not a business combination, and

• at the time of the transaction, affects neither accounting profit nor taxable profit (tax loss) (Ind AS 12.15).

• There are special recognition exceptions for investments in

subsidiaries, branches and associates, and interests in joint ventures

for both deferred tax liabilities and assets.

Consolidated Financial StatementConsolidated Financial Statements

• In consolidated financial statements (CFS), temporarydifferences are determined by comparing the carryingamounts of assets and liabilities in the CFS with theappropriate tax base.

• The tax base is determined by reference to aconsolidated tax return in those jurisdictions in whichsuch a return is filed. In other jurisdictions, the tax baseis determined by reference to the tax returns of eachentity in the group.

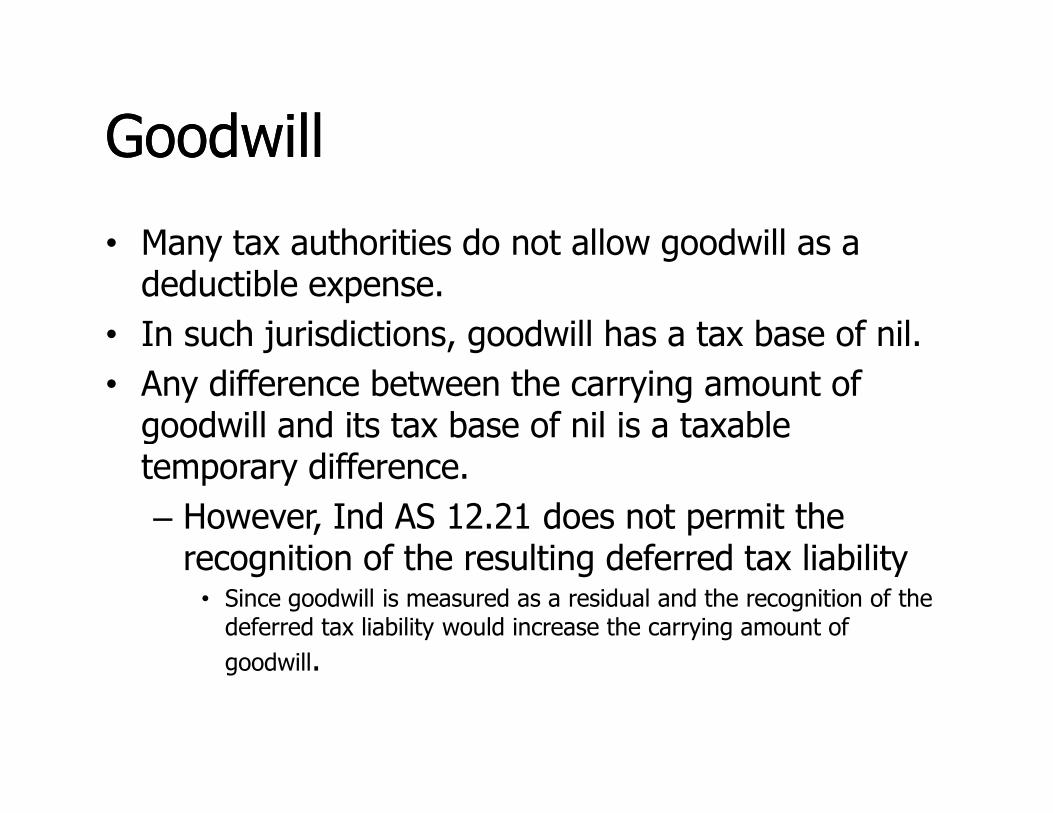

GoodwillGoodwill

• Many tax authorities do not allow goodwill as a deductible expense.

• In such jurisdictions, goodwill has a tax base of nil.

• Any difference between the carrying amount of goodwill and its tax base of nil is a taxable goodwill and its tax base of nil is a taxable temporary difference.

– However, Ind AS 12.21 does not permit the recognition of the resulting deferred tax liability • Since goodwill is measured as a residual and the recognition of the deferred tax liability would increase the carrying amount of

goodwill.

Goodwill contd.Goodwill contd.

• Deferred tax liabilities for taxable temporary differencesrelating to goodwill are, however, recognised in certaincases.

– For example, if goodwill acquired Rs 100 in a businesscombination has a cost of Rs 100 that is deductiblefor tax purposes at a rate of 20% p.a. starting in thefor tax purposes at a rate of 20% p.a. starting in theyear of acquisition, the tax base of the goodwill is Rs100 on initial recognition and Rs 80 at the end of theyear of acquisition. If the carrying amount of goodwillper the books at the end of the year of acquisitionremains unchanged at Rs 100, a taxable temporarydifference of Rs 20 arises at the end of that year.

Recognition of deferred tax assetsRecognition of deferred tax assets• Deferred tax assets must be recognized only to the extent that it is

‘probable’ that future taxable profits will be available.

– ‘Probable’ not defined, Ind AS 12 contains guidance

• Factors to consider for recognition of DTA arising from unused losses:

• Existence of sufficient taxable temporary difference

• Convincing other evidence that sufficient taxable profits will be availableavailable

• Losses resulted from identifiable causes, which are unlikely to recur

• Availability of tax planning opportunities

• At the end of each reporting period, an entity should reassess unrecognized DTAs.

– The entity should recognize a previously unrecognized DTA to the extent that it has become probable that future taxable profit will allow the DTA to be recovered.

Tax Planning OpportunitiesTax Planning Opportunities

• When there are insufficient taxable temporary differencesrelating to the same taxation authority and the sametaxable entity, the deferred tax asset is recognized to theextent that tax planning opportunities are available to theentity that will create taxable profit in appropriateentity that will create taxable profit in appropriateperiods.

• Tax planning opportunities are actions that the entitywould take in order to create or increase taxable incomein a particular period before the expiry of a tax loss or taxcredit carryforward.

QuestionQuestion

• When assessing the recoverability of deferred tax assetsarising from the carry forward of unused tax losses andunused tax credits, should a deferred tax asset berecognised where the amount of probable future taxableprofit available is sufficient only for a portion, rather thanthe total, of the unused tax losses or unused tax credits?the total, of the unused tax losses or unused tax credits?

Answer• Yes. Ind AS 12.34 states the following:

• A deferred tax asset shall be recognised for thecarryforward of unused tax losses and unused tax creditsto the extent that it is probable that future taxable profitwill be available against which the unused tax losses andunused tax credits can be utilised.unused tax credits can be utilised.

• When assessing the probability that taxable profit will beavailable against which unused tax losses or unused taxcredits can be utilised, an entity assesses whether it isprobable that it will have any taxable profits before anyportion of the unused tax losses or unused tax creditsexpire.

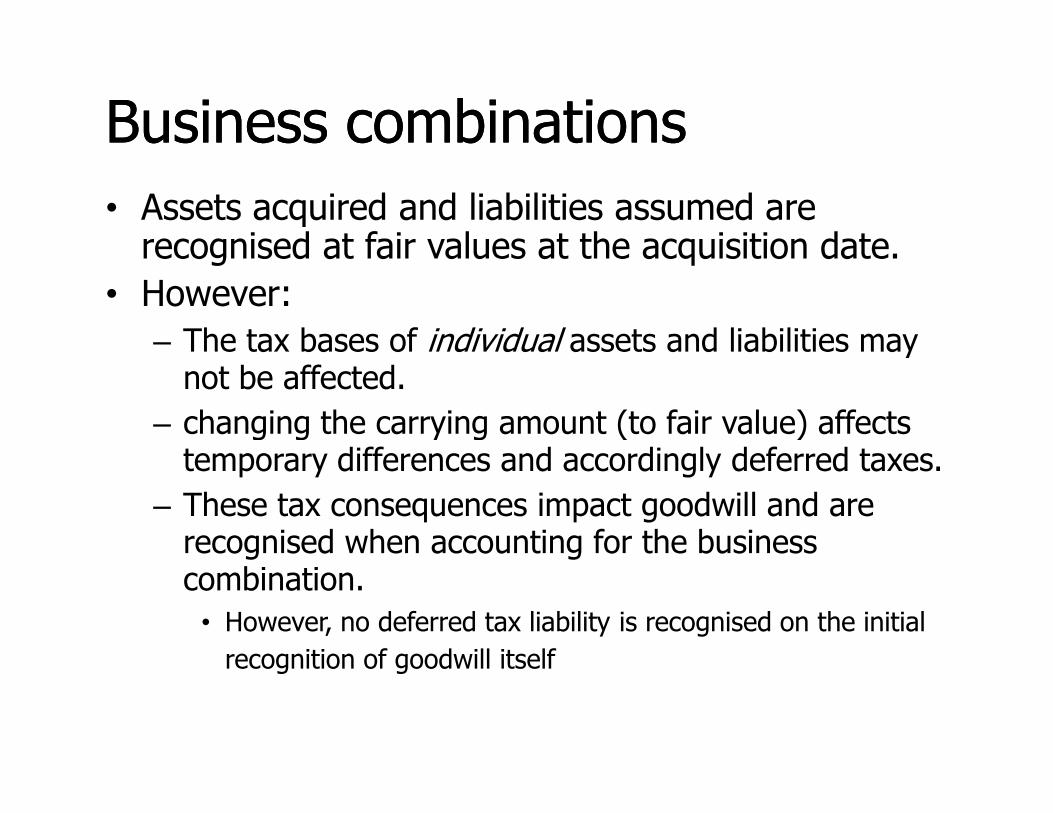

Business combinationsBusiness combinations

• Assets acquired and liabilities assumed are recognised at fair values at the acquisition date.

• However:

– The tax bases of individual assets and liabilities may not be affected.

– changing the carrying amount (to fair value) affects – changing the carrying amount (to fair value) affects temporary differences and accordingly deferred taxes.

– These tax consequences impact goodwill and are recognised when accounting for the business combination.

• However, no deferred tax liability is recognised on the initial

recognition of goodwill itself

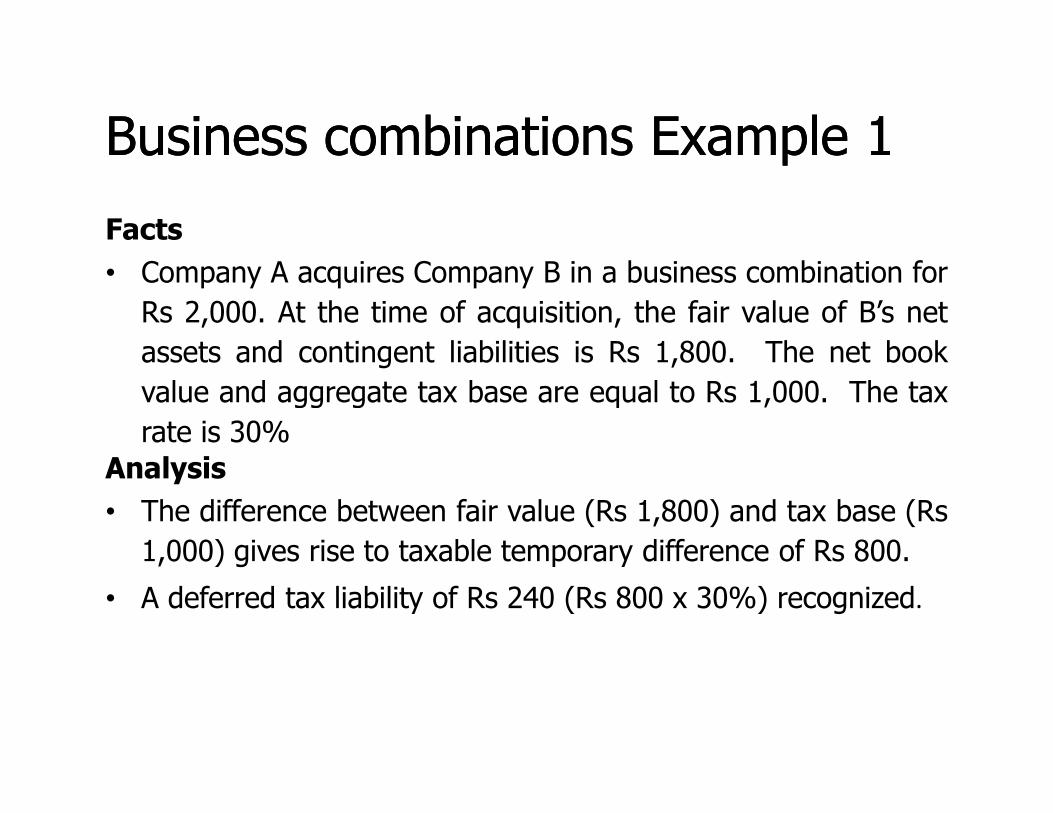

Business combinations Example 1Business combinations Example 1

Facts

• Company A acquires Company B in a business combination for

Rs 2,000. At the time of acquisition, the fair value of B’s net

assets and contingent liabilities is Rs 1,800. The net book

value and aggregate tax base are equal to Rs 1,000. The taxvalue and aggregate tax base are equal to Rs 1,000. The tax

rate is 30%

Analysis

• The difference between fair value (Rs 1,800) and tax base (Rs

1,000) gives rise to taxable temporary difference of Rs 800.

• A deferred tax liability of Rs 240 (Rs 800 x 30%) recognized.

Business combinations Example 1 (cont.)

Accounting for the business combination

Fair value of assets 1,800

Deferred tax liability (240)Deferred tax liability (240)

Goodwill 440

Total consideration 2,000

PostPost--acquisition recognition of DTA acquisition recognition of DTA of acquireeof acquiree

• Recognizes DTA’s of acquiree once the ‘probability’ criterion is met, even post acquisition.– No time limit.

– If within the measurement period and resulting from new information about facts and circumstances that new information about facts and circumstances that existed at the acquisition date - Adjust goodwill and reassess impairment for goodwill

• If goodwill is nil – recognise the deferred tax benefits in

profit or loss

– If not - Recognised in profit or loss.

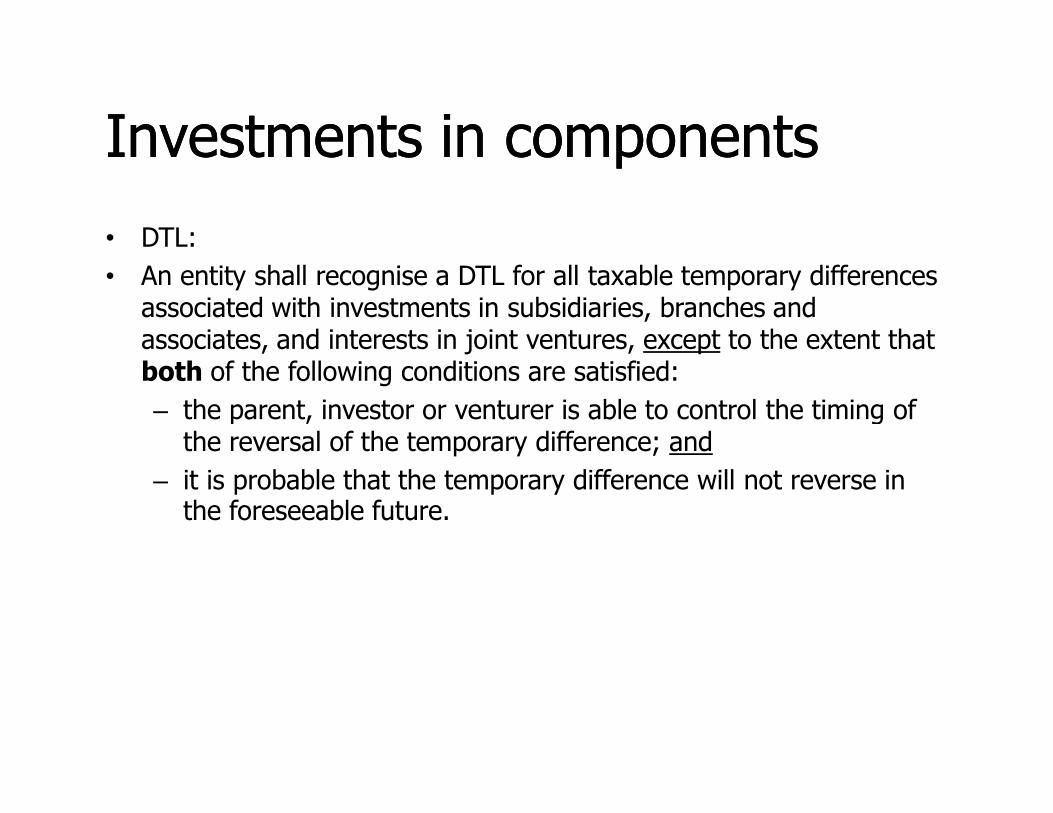

Investments in componentsInvestments in components

• DTL:

• An entity shall recognise a DTL for all taxable temporary differences associated with investments in subsidiaries, branches and associates, and interests in joint ventures, except to the extent that both of the following conditions are satisfied:

– the parent, investor or venturer is able to control the timing of – the parent, investor or venturer is able to control the timing of the reversal of the temporary difference; and

– it is probable that the temporary difference will not reverse in the foreseeable future.

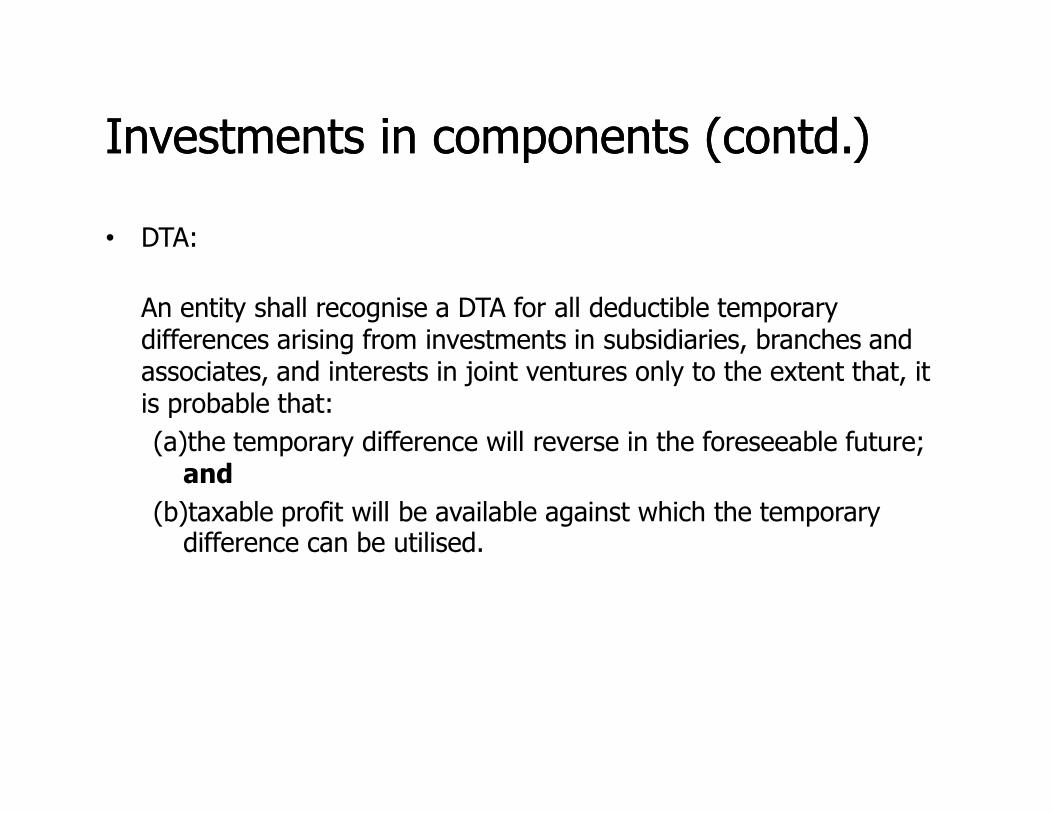

Investments in components (contd.)Investments in components (contd.)

• DTA:

An entity shall recognise a DTA for all deductible temporary differences arising from investments in subsidiaries, branches and associates, and interests in joint ventures only to the extent that, it is probable that:is probable that:

(a)the temporary difference will reverse in the foreseeable future; and

(b)taxable profit will be available against which the temporary difference can be utilised.

QuestionQuestion

• A deferred tax liability is not required for an excess ofthe amount for financial reporting over the tax basis ofan investment in a subsidiary, branch, associate orinterest in a joint venture when the investor is able tocontrol the timing of the reversal of the temporarycontrol the timing of the reversal of the temporarydifference, and it is probable that the temporarydifference will not reverse in the foreseeable future.

• In the circumstance where such an exception relates toundistributed profits and an entity requires its subsidiaryto remit only a portion of undistributed earnings, wouldthe entity be required to recognise a deferred tax liabilityonly for a portion of the undistributed earnings to beremitted in the future?

AnswerAnswer

• Yes. Ind AS 12.39 is not an "all-or-nothing" requirement.If circumstances change and it becomes probable thatsome or all of the undistributed earnings of a subsidiarywill be remitted in the foreseeable future but incometaxes have not been recognised, the investor shouldtaxes have not been recognised, the investor shouldaccrue as an expense of the current period, incometaxes attributable to that remittance.

Current and Deferred Tax Recognized Current and Deferred Tax Recognized outside P&Loutside P&L

• If the underlying item is recognized outside profit or loss, the current and deferred tax is also recognized outside the profit or loss

• If the underlying item is recognized in:

– Other comprehensive income, the current and deferred tax is also recognized in other comprehensive incomerecognized in other comprehensive income

– Directly in equity, the current and deferred tax is also recognized directly in equity

Current and Deferred Tax Recognized Current and Deferred Tax Recognized outside P&L(contd.)outside P&L(contd.)

• Example of items recognized in “other comprehensive income”

– a change in carrying amount arising from the revaluation of property, plant and equipment

• Example of items recognized directly in “equity”

an adjustment to the opening balance of retained earnings – an adjustment to the opening balance of retained earnings resulting from either a change in accounting policy that is applied retrospectively or the correction of an error

PresentationPresentation

– Tax expense

• Tax Expense (Income) related to profit or loss from ordinary activities

– shall be presented in the statement of profit and loss.

– Exchange differences on deferred foreign tax liabilities or assets

• Where exchange differences on deferred foreign tax liabilities or assets are recognised in the statement of profit and loss, such differences may be classified as deferred tax expense (income)

– if that presentation is considered to be the most useful to financial statement users.

PresentationPresentation

Offset– current tax assets and current tax liabilities

• Offset if, and only if, the entity:– has a legally enforceable right to set off the recognisedamounts; and

– intends either to settle on a net basis, or to realise the assetand settle the liability simultaneouslyAn entity will normally have a legally enforceable right to setoff a current tax asset against a current tax liability when theyAn entity will normally have a legally enforceable right to setoff a current tax asset against a current tax liability when theyrelate to income taxes levied by the same taxation authorityand the taxation authority permits the entity to make or receivea single net payment.

– In consolidated financial statements, a current tax asset of oneentity in a group is offset against a current tax liability ofanother entity in the group if, and only if, the entitiesconcerned have a legally enforceable right to make or receive asingle net payment and the entities intend to make or receivesuch a net payment.

Presentation (contd.)Presentation (contd.)

– deferred tax assets and liabilities

• Offset if, and only if:

– the entity has a legally enforceable right to set off current tax assets against current tax liabilities; and

– the deferred tax assets and liabilities relate to income taxes levied by the same taxation authority on either:levied by the same taxation authority on either:

» the same taxable entity; or

» different taxable entities which intend either to settle current tax liabilities and assets on a net basis or to realise the asset and settle the liability simultaneously.

Certain DisclosuresCertain Disclosures

• The major components of tax expense (income) need to be disclosed separately.– Major Components of tax expense (income) may include:

• current tax expense (income);

• prior period adjustments;

• deferred tax expense (income);• deferred tax expense (income);

• amount of the benefit arising from a previously unrecognised tax loss, tax credit or temporary difference of a prior period that is used to reduce current tax or deferred tax expense;

• Aggregate current and deferred tax relating to items charged or credited directly to equity;

Certain Disclosures (contd.)Certain Disclosures (contd.)

• Income tax relating to each component of other comprehensive income;

• An explanation of the relationship between tax expense (income) and accounting profit in either or both of the following forms:

a numerical reconciliation between tax expense (income) and the – a numerical reconciliation between tax expense (income) and the product of accounting profit multiplied by the applicable tax rate, disclosing also the basis on which the applicable tax rate is computed; or

– a numerical reconciliation between the average effective tax rate andthe applicable tax rate, disclosing also the basis on which the applicable tax rate is computed;

• An explanation of changes in the applicable tax rate compared to the previous accounting period;

Certain DisclosuresCertain Disclosures

• Amount (and expiry date, if any) of deductible temporary differences, unused tax losses, and unused tax credits for which no deferred tax asset is recognised;

• Aggregate amount of temporary differences associated with investments in subsidiaries, branches and associates and interests in joint ventures, for which deferred tax liabilities have not been joint ventures, for which deferred tax liabilities have not been recognised;

• In respect of discontinued operations, the tax expense relating to:

– the gain or loss on discontinuance; and

– the profit or loss from the ordinary activities of the discontinued operation for the period, and corresponding amounts for each prior period presented;

Certain Disclosures (contd.)Certain Disclosures (contd.)

• Change in the amount recognised for pre-acquisition deferred tax asset

• Description of the event or change in circumstances that cause deferred tax benefits to be recognised after the acquisition date

• Amount of deferred tax asset recognised and evidence supporting its recognition, when:

– the utilisation of the deferred tax asset is dependent on future taxable profits in excess of the profits arising from the reversal of existing taxable temporary differences; and

– the entity has suffered a loss in either the current or preceding period

THANK YOUTHANK YOU