Embed Size (px)

Citation preview

ITA36Vo11.doc 25/08/2003 10:22 am

Income Tax Assessment Act 1936

VOLUME 11

Part IIIA—Capital gains and capital losses

Income Tax Assessment Act 1936 iii

Contents Part IIIA—Capital gains and capital losses i

Division 18—Principal residence 1 160ZZQ Principal residence............................................................................ 1

Division 19—Goodwill 28 160ZZR Exemption of part of gain attributable to goodwill ......................... 28 160ZZRAA Calculation of exemption threshold for purposes of

section 160ZZR............................................................................... 31 Division 19A—Transfers of assets between companies under

common ownership 33 Subdivision A—Outline and interpretation 33

160ZZRAAAOutline of Division ......................................................................... 33 160ZZRA Interpretation................................................................................... 33 160ZZRB When companies under common ownership................................... 35 160ZZRBA Cost base etc. of certain assets ........................................................ 35 160ZZRBB Meaning of indexed common ownership market value................... 36 160ZZRC Underlying interest ......................................................................... 36

Subdivision B—Application of Division 37 160ZZRD Transfers of assets between companies under common

ownership........................................................................................ 37 160ZZRDA How Division applies to grouped assets ......................................... 37 160ZZRDB How Division applies to depreciable assets .................................... 37 160ZZRDC Application of Subdivision E.......................................................... 38 160ZZRDD Application of Subdivision F .......................................................... 38

Subdivision C—Grouped assets 39 160ZZRDE Transferor may elect to group assets............................................... 39 160ZZRDF Depreciable property groups........................................................... 39 160ZZRDG Pre-common ownership groups ...................................................... 41 160ZZRDH Post-common ownership groups..................................................... 42 160ZZRDI Shares or loans created after first asset in group is disposed

of..................................................................................................... 43 Subdivision D—Depreciable assets 43

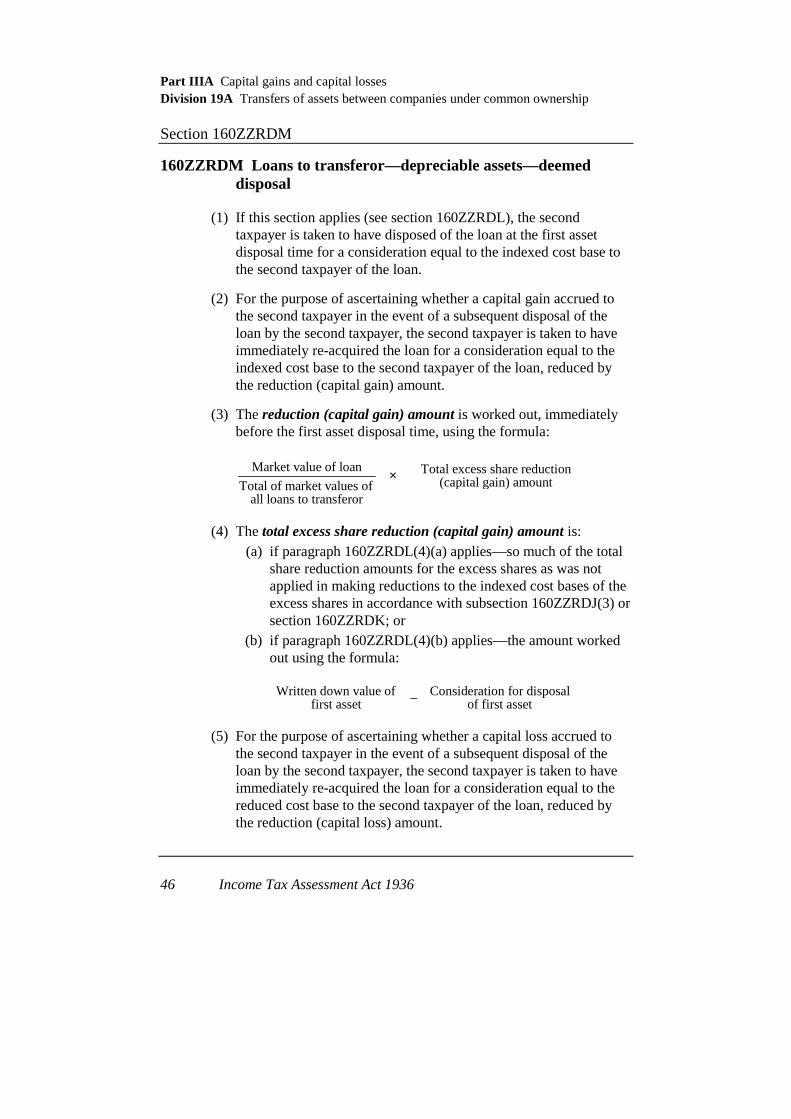

160ZZRDJ Shares in, and loans to, transferor—depreciable assets—deemed disposal.............................................................................. 43

160ZZRDK Shares of different classes............................................................... 44 160ZZRDL Loans to transferor—depreciable assets.......................................... 45 160ZZRDM Loans to transferor—depreciable assets—deemed disposal............ 46 160ZZRDN More than one loan ......................................................................... 47

iv Income Tax Assessment Act 1936

Subdivision E—Other assets 48 160ZZRE Shares in, and loans to, transferor—deemed disposal and

re-acquisition .................................................................................. 48 160ZZRF First asset acquired before transferor and transferee came

under common ownership—shares in, and loans to, transferor—reduction in cost base etc. ............................................ 54

160ZZRFA First asset acquired when transferor and transferee under common ownership—shares in, and loans to, transferor—reduction in cost base etc. ............................................................... 56

Subdivision F—Other adjustments 57 160ZZRG Indirect equity or debt interests in transferor—reduction in

cost base etc. ................................................................................... 57 160ZZRH Equity interests in transferee—compensatory increase in cost

base etc. .......................................................................................... 57 Division 19B—Share value shifting arrangements 59

160ZZRI Object.............................................................................................. 59 160ZZRJ Simplified outline ........................................................................... 59 160ZZRK List of definitions............................................................................ 60 160ZZRL Requirements for Division to apply ................................................ 61 160ZZRM Share value shift under an arrangement .......................................... 62 160ZZRN Controller of a company etc............................................................ 64 160ZZRO Material decrease, material increase and total market value

increase........................................................................................... 65 160ZZRP Consequences of value shift to pre-CGT share ............................... 67 160ZZRQ Consequences of value shift to post-CGT share.............................. 68

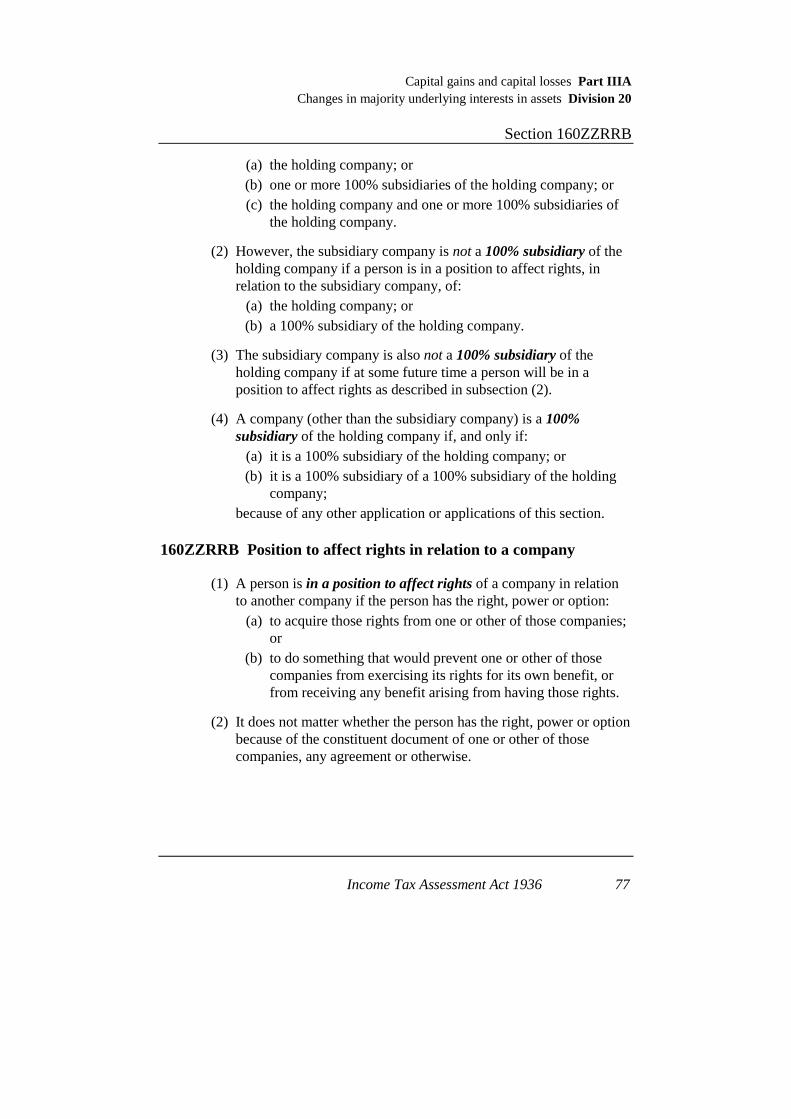

Division 20—Changes in majority underlying interests in assets 72 Subdivision A—Preliminary 72

160ZZRR Interpretation................................................................................... 72 160ZZRRA What is a 100% subsidiary.............................................................. 76 160ZZRRB Position to affect rights in relation to a company............................ 77 160ZZRS Indirect beneficial interest in asset .................................................. 78 160ZZRT Indirect beneficial interest in income derived from asset................ 78 160ZZRU Acquisition of percentage of underlying interests as a result

of death ........................................................................................... 78 Subdivision B—Provisions applying to taxpayers other than

public entities 79 160ZZS Changes in majority underlying interests in assets of

taxpayers other than public entities................................................. 79

Income Tax Assessment Act 1936 v

Subdivision C—Provisions applying to public entities 80 160ZZSA Public entities to determine at identified times whether

changes have occurred since 19 September 1985 in majority underlying interests in assets of the entities .................................... 80

160ZZSB Date of acquisition of asset if failure to make determination on time ............................................................................................ 81

160ZZSC If no continuity of majority underlying interests found at first test time........................................................................................... 82

160ZZSD If no continuity of majority underlying interests at later test time ................................................................................................. 83

Subdivision D—Abnormal trading 84 160ZZSE Abnormal trading in shares in a public company or units in a

publicly traded unit trust ................................................................. 84 160ZZSF Abnormal trading: general provision .............................................. 85 160ZZSG Abnormal trading: 5% of shares or units in one transaction ........... 85 160ZZSH Abnormal trading: suspected acquisition or merger........................ 85 160ZZSI Abnormal trading—20% of shares or units traded over 60

day period ....................................................................................... 85 Subdivision E—How holdings of shares or units of less than 1% in

certain public entities may be treated 86 160ZZSJ What this Subdivision is about........................................................ 86 160ZZSK Holdings of less than 1% in public company or publicly

traded unit trust ............................................................................... 86 160ZZSL Holdings of less than 1% in interposed public company or

interposed publicly traded unit trust................................................ 87 160ZZSM Notional single shareholder or unitholder....................................... 88 160ZZSN Capital shareholding and dividend shareholding of less than

1%................................................................................................... 90 160ZZSO Capital unitholding and income unitholding of less than 1%.......... 91 160ZZSP Shares that are part of a substantial shareholding ........................... 91

Subdivision F—How interposed superannuation funds, approved deposit funds, special companies and government bodies may be treated 92

160ZZSR What this Subdivision is about........................................................ 92 160ZZSS When fund, special company or government body is taken to

have rights to capital, dividends or other income............................ 93

vi Income Tax Assessment Act 1936

Subdivision G—Determination of underlying interests if mutual insurance organisation with more than 50 members ceases to be such an organisation but continues to be a public entity 95

160ZZST Members of former mutual insurance organisation taken to hold underlying interests in assets since base time ......................... 95

Division 20A—Special provisions relating to disposals of certain pre-20 September 1985 assets 96

160ZZT Disposal of shares or interest in trust .............................................. 96 Division 21—Miscellaneous 100

160ZZU Keeping of records........................................................................ 100

Part IIIB—Australian branches of foreign banks 105

Division 1—Preliminary 105 160ZZVA Object............................................................................................ 105 160ZZVB Application ................................................................................... 105 160ZZV Definitions .................................................................................... 106 160ZZW Certain provisions to apply as if Australian branch of foreign

bank were a separate legal entity .................................................. 107 Division 2—Provisions relating to income tax 109

160ZZX Income of branch to have Australian source ................................. 109 160ZZY Deduction for foreign tax.............................................................. 109 160ZZZ Notional borrowing by branch from bank..................................... 109 160ZZZA Notional payment of interest by branch to bank ........................... 110 160ZZZC Offshore banking units.................................................................. 111 160ZZZE Notional derivative transactions between branch and bank .......... 111 160ZZZF Notional foreign exchange transactions between branch and

bank .............................................................................................. 112 160ZZZG Losses ........................................................................................... 112 160ZZZH Net capital losses .......................................................................... 112 160ZZZI Certain transactions to be disregarded .......................................... 113

Division 3—Provisions relating to withholding tax 114 160ZZZJ Withholding tax on interest paid by branch to bank...................... 114

Part IV—Returns and assessments 115 161 Annual returns .............................................................................. 115 161A Form and content of returns .......................................................... 115 161AA Contents of returns of full self-assessment taxpayers ................... 116 161G Tax agent to give taxpayer copy of notice of assessment.............. 116 162 Further returns and information .................................................... 116 163 Special returns .............................................................................. 117

Income Tax Assessment Act 1936 vii

163A Late lodgement penalty—relevant entities, instalment taxpayers and full self-assessment taxpayers ................................ 117

163AA General interest charge on unpaid penalty .................................... 119 163B Late lodgment of returns by persons other than relevant

entities, instalment taxpayers and full self-assessment taxpayers ....................................................................................... 120

164 Returns deemed to be duly made .................................................. 122 166 Assessment ................................................................................... 123 166A Deemed assessment ...................................................................... 123 167 Default assessment........................................................................ 124 168 Special assessment ........................................................................ 125 169 Assessments on all persons liable to tax ....................................... 125 169A Reliance by Commissioner on returns and statements .................. 125 170 Amendment of assessments .......................................................... 126 170A Power to amend assessment not to limit other powers to

amend assessment ......................................................................... 136 170AA Liability of taxpayer where assessment amended ......................... 136 170BA Effect of public ruling on tax other than withholding tax ............. 142 170BB Effect of private rulings on tax other than withholding tax........... 142 170BCA Effect of oral ruling on tax other than withholding tax ................. 143 170BC Assessment of tax other than withholding tax if public or

private rulings conflict .................................................................. 144 170BDA Assessment of tax other than withholding tax if public and

oral rulings conflict ....................................................................... 144 170BDB Assessment of tax other than withholding tax if private and

oral rulings conflict ....................................................................... 145 170BDC Assessment of tax other than withholding tax if public,

private and oral rulings conflict .................................................... 146 170BD Effect of public ruling on withholding tax .................................... 147 170BE Effect of private ruling on withholding tax................................... 147 170BF Withholding tax where conflicting rulings.................................... 148 170BG Final Tribunal decision about private ruling conclusive ............... 149 170BH Final court order about private ruling conclusive.......................... 149 170BI Final court order about Commissioner discretion ......................... 150 170C Power of Commissioner to reduce amount of tax payable in

certain cases .................................................................................. 151 171 Where no notice of assessment served.......................................... 151 172 Refunds of amounts overpaid ....................................................... 152 173 Amended assessment to be an assessment .................................... 152 174 Notice of assessment..................................................................... 152 175 Validity of assessment .................................................................. 153 175A Objections against assessments..................................................... 153 176 Judicial notice of signature ........................................................... 153

viii Income Tax Assessment Act 1936

177 Evidence ....................................................................................... 153

Part IVA—Schemes to reduce income tax 155 177A Interpretation................................................................................. 155 177B Operation of Part........................................................................... 156 177C Tax benefits .................................................................................. 156 177CA Withholding tax avoidance ........................................................... 161 177D Schemes to which Part applies...................................................... 161 177E Stripping of company profits ........................................................ 162 177EA Creation of franking debit or cancellation of franking credits ...... 164 177EB Cancellation of franking credits—consolidated groups ................ 172 177F Cancellation of tax benefits etc. .................................................... 175 177G Amendment of assessments ......................................................... 179 177H Amendment of foreign tax credit determinations.......................... 179

Part VA—Tax file numbers 181

Division 1—Preliminary 181 202 Objects of this Part........................................................................ 181 202A Interpretation................................................................................. 183 202AA Definition of eligible PAYG payment ........................................... 187

Division 2—Issuing of tax file numbers 188 202B Application for tax file number..................................................... 188 202BA Issuing of tax file numbers............................................................ 188 202BB Current tax file number................................................................. 189 202BC Deemed refusal by Commissioner ................................................ 189 202BD Interim notices .............................................................................. 189 202BE Cancellation of tax file numbers ................................................... 190 202BF Alteration of tax file numbers ....................................................... 191

Division 3—Quotation of tax file numbers by recipients of eligible PAYG payments 192

202C TFN declarations by recipients of eligible PAYG payments ........ 192 202CA Operation of TFN declaration ....................................................... 192 202CB Quotation of tax file number in TFN declaration.......................... 193 202CC Making a replacement TFN declaration in place of an

ineffective declaration................................................................... 194 202CD Sending of TFN declaration to Commissioner.............................. 195 202CE Effect of incorrect quotation of tax file number............................ 196 202CF Payer must notify Commissioner if no TFN declaration by

recipient ........................................................................................ 197

Income Tax Assessment Act 1936 ix

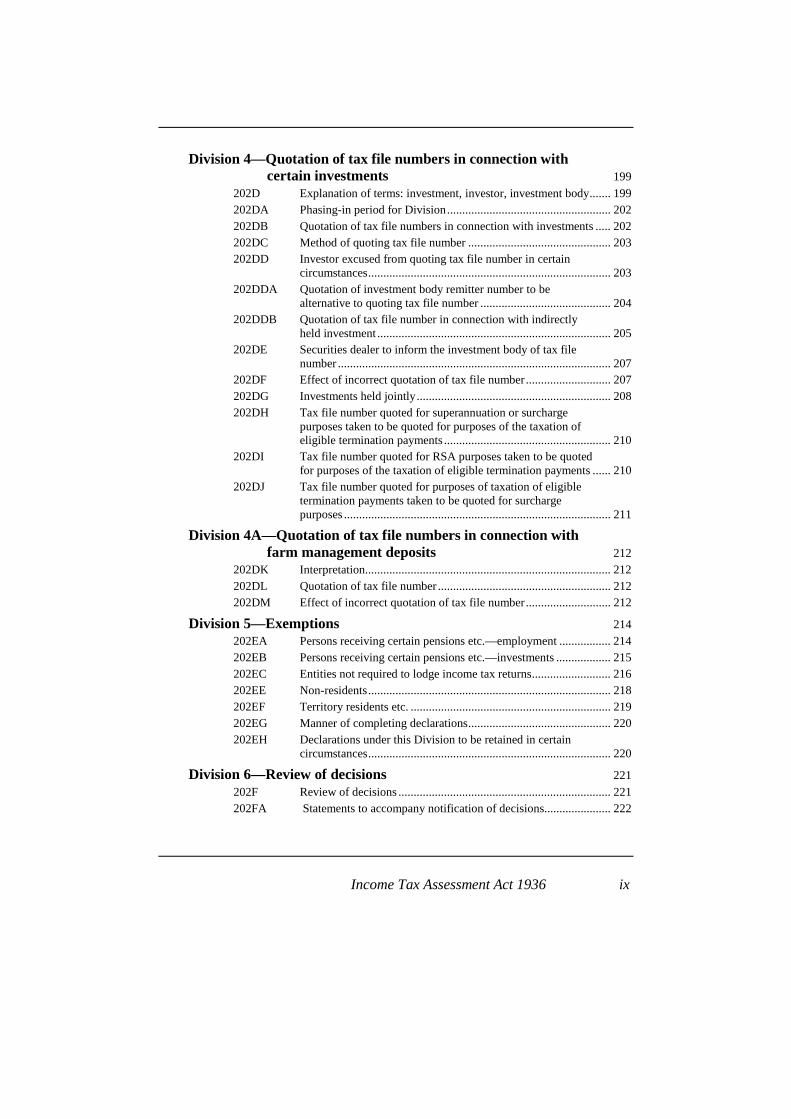

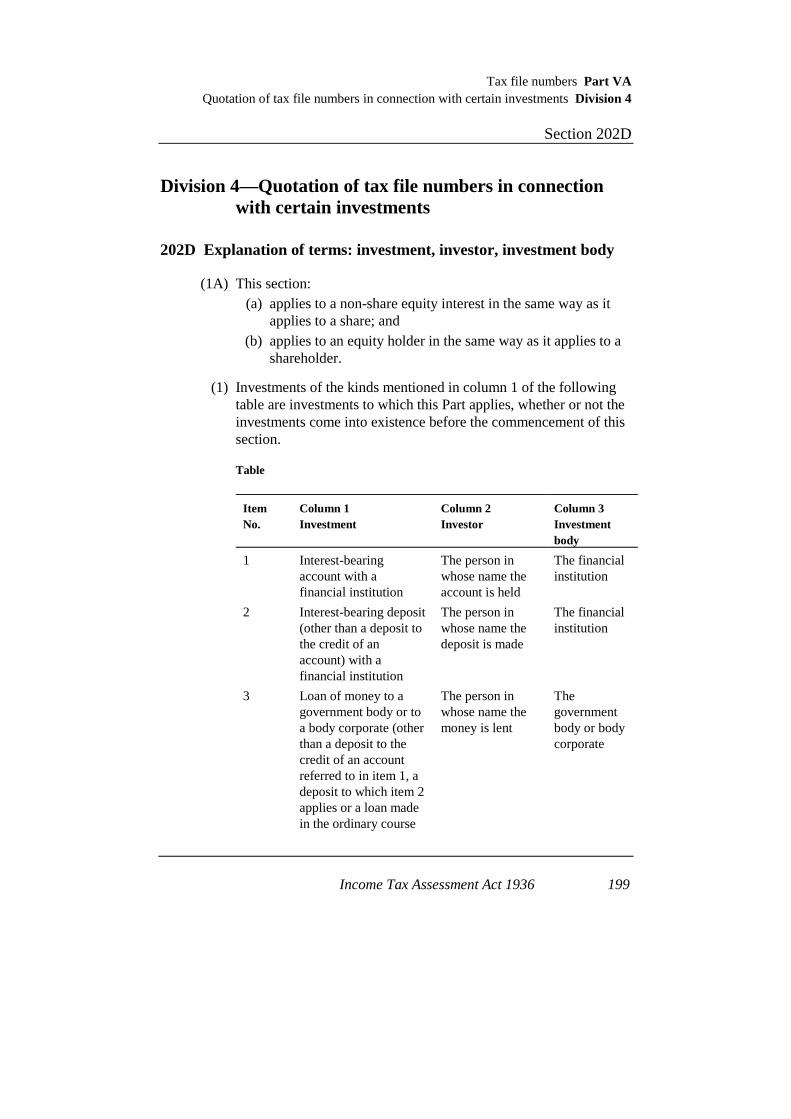

Division 4—Quotation of tax file numbers in connection with certain investments 199

202D Explanation of terms: investment, investor, investment body....... 199 202DA Phasing-in period for Division...................................................... 202 202DB Quotation of tax file numbers in connection with investments ..... 202 202DC Method of quoting tax file number ............................................... 203 202DD Investor excused from quoting tax file number in certain

circumstances................................................................................ 203 202DDA Quotation of investment body remitter number to be

alternative to quoting tax file number ........................................... 204 202DDB Quotation of tax file number in connection with indirectly

held investment ............................................................................. 205 202DE Securities dealer to inform the investment body of tax file

number .......................................................................................... 207 202DF Effect of incorrect quotation of tax file number............................ 207 202DG Investments held jointly................................................................ 208 202DH Tax file number quoted for superannuation or surcharge

purposes taken to be quoted for purposes of the taxation of eligible termination payments ....................................................... 210

202DI Tax file number quoted for RSA purposes taken to be quoted for purposes of the taxation of eligible termination payments ...... 210

202DJ Tax file number quoted for purposes of taxation of eligible termination payments taken to be quoted for surcharge purposes ........................................................................................ 211

Division 4A—Quotation of tax file numbers in connection with farm management deposits 212

202DK Interpretation................................................................................. 212 202DL Quotation of tax file number ......................................................... 212 202DM Effect of incorrect quotation of tax file number............................ 212

Division 5—Exemptions 214 202EA Persons receiving certain pensions etc.—employment ................. 214 202EB Persons receiving certain pensions etc.—investments .................. 215 202EC Entities not required to lodge income tax returns.......................... 216 202EE Non-residents................................................................................ 218 202EF Territory residents etc. .................................................................. 219 202EG Manner of completing declarations............................................... 220 202EH Declarations under this Division to be retained in certain

circumstances................................................................................ 220 Division 6—Review of decisions 221

202F Review of decisions ...................................................................... 221 202FA Statements to accompany notification of decisions...................... 222

x Income Tax Assessment Act 1936

Division 7—Manner of providing information 223 202G Transmission of information in accordance with

specifications ................................................................................ 223

Part VI—Collection and recovery of tax 225

Division 1—General 225 204 When tax payable.......................................................................... 225 205 Taxpayer leaving Australia ........................................................... 226 206 Extension of time and payment of tax by instalments................... 227 208 Tax a debt due to the Commonwealth........................................... 227 209 Recovery of tax............................................................................. 228 213 Temporary business ...................................................................... 229 214 Substituted service ........................................................................ 229 214A Interest rates.................................................................................. 230 215 Liquidators, receivers and certain agents ...................................... 230 216 When tax not paid during lifetime ................................................ 233 218 Commissioner may collect tax from person owing money to

taxpayer ........................................................................................ 235 219 Consolidated assessments ............................................................. 238 220 Assessment where no administration ............................................ 238

Division 1AAA—Payment of RPS, PAYE and PPS deductions to Commissioner 241

Subdivision A—Outline of Division 241 220AAA Outline of Division ....................................................................... 241

Subdivision B—Large remitters 241 220AAB Who is a large remitter—general .................................................. 241 220AAC Who is a large remitter—determination by Commissioner........... 243 220AAD Application to cease to be a large remitter .................................... 244 220AAE When amounts must be remitted................................................... 244 220AAF How amounts must be paid........................................................... 245 220AAG What else must be sent.................................................................. 245 220AAGA Commissioner must be notified of amounts.................................. 246 220AAH Variation of requirements ............................................................. 246 220AAI Grouping of companies................................................................. 247

Subdivision C—Medium remitters 248 220AAJ Who is a medium remitter—general ............................................. 248 220AAK Who is a medium remitter—determination by Commissioner...... 249 220AAL Application to cease to be a medium remitter ............................... 250 220AAM When amounts must be remitted................................................... 250 220AAN How amounts must be paid........................................................... 251

Income Tax Assessment Act 1936 xi

220AAO What else must be sent.................................................................. 251 220AAOA Commissioner must be notified of amounts.................................. 251 220AAP Variation of requirements ............................................................. 252

Subdivision D—Small remitters 253 220AAQ Who is a small remitter ................................................................. 253 220AAR When amounts must be remitted................................................... 253 220AAS How amounts must be paid........................................................... 253 220AAT What else must be sent.................................................................. 254 220AATA Commissioner must be notified of amounts.................................. 254 220AAU Variation of requirements ............................................................. 255

Subdivision E—Offences and penalties 255 220AAW Large remitters—non-electronic payment..................................... 255 220AAZ Failure to send statements to Commissioner—offence ................. 256

Subdivision F—Recovery of amounts by Commissioner 256 220AAZA Recovery of amounts by Commissioner ....................................... 256

Subdivision G—Miscellaneous 259 220AAZB Power of Commissioner to obtain information ............................. 259 220AAZC Declarations .................................................................................. 259 220AAZD Application of this Division to partnerships.................................. 259 220AAZE Application of this Division to unincorporated companies ........... 260 220AAZF Review of decisions ...................................................................... 260 220AAZG Interpretation................................................................................. 261

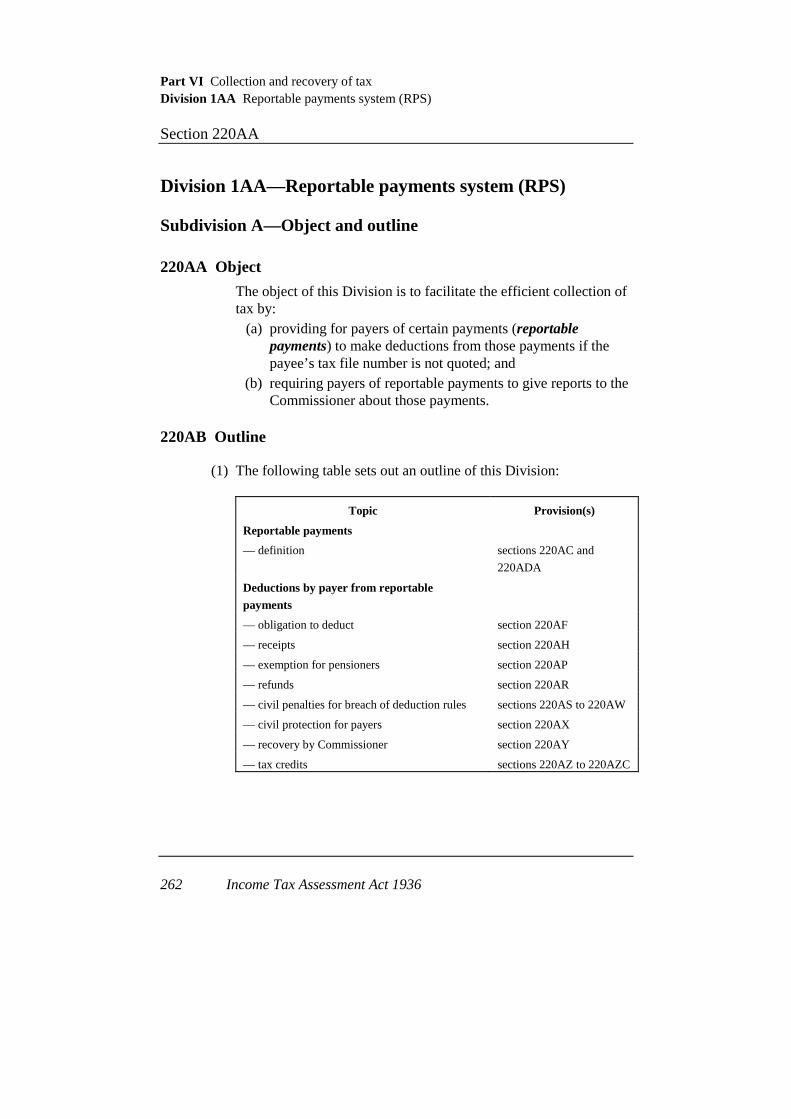

Division 1AA—Reportable payments system (RPS) 262 Subdivision A—Object and outline 262

220AA Object............................................................................................ 262 220AB Outline .......................................................................................... 262

Subdivision B—Interpretation 263 220AC Interpretation................................................................................. 263 220AD Money not actually paid to a person ............................................. 265 220ADA Transfer of reportable payment debts............................................ 265 220AE Signing of documents ................................................................... 265

Subdivision C—Payer of reportable payment must make deduction if payee’s tax file number not quoted 266

220AF Deduction from reportable payment if payee’s tax file number not quoted ........................................................................ 266

Subdivision D—Payers’ reporting and record-keeping obligations 267 220AH Obligation to issue receipt for deduction ...................................... 267

xii Income Tax Assessment Act 1936

220AJ Annual report ................................................................................ 268 220AK Retention of annual report............................................................. 269

Subdivision E—How payees can quote their tax file numbers 269 220AL Method of quoting tax file number ............................................... 269 220AM Meaning of tax file number declaration........................................ 269 220AN When tax file number declaration in force.................................... 270 220AO Commissioner may correct tax file number set out in tax file

number declaration form............................................................... 271 Subdivision F—Making of pensioner exemption declaration to be

alternative to quotation of tax file number 272 220AP Making of pensioner exemption declaration to be alternative

to quotation of tax file number...................................................... 272 Subdivision G—Payer to send tax file number declaration form or

pensioner exemption declaration form to Commissioner 275

220AQ Obligations of payer—tax file number declaration form or pensioner exemption declaration form.......................................... 275

Subdivision H—Refund of deductions in special circumstances 277 220AR Commissioner may refund deductions.......................................... 277

Subdivision I—Civil penalties for failure to make deductions from reportable payments and for failure to send deductions to the Commissioner 278

220AS Failure to make deduction from reportable payment .................... 278 220AU Commissioner may remit penalty for failure to deduct................. 279

Subdivision J—Payers to have civil protection for making deductions 279

220AX Payers to have civil protection for making deductions.................. 279 Subdivision K—Recovery of amounts payable under this Division 279

220AY Recovery of amounts by Commissioner ....................................... 279 Subdivision L—Tax credits for deductions from reportable

payments 281 220AZ Entitlement to credit—payee neither a partnership nor a

trustee............................................................................................ 281 220AZA Entitlement to credit—payee a partnership................................... 281 220AZB Entitlement to credit—payee a trustee .......................................... 282 220AZC Application of credits.................................................................... 285

Subdivision M—Miscellaneous 285 220AZD Power of Commissioner to obtain information ............................. 285

Income Tax Assessment Act 1936 xiii

220AZE Declarations .................................................................................. 286 220AZF Application of this Division to partnerships.................................. 286 220AZG Application of this Division to unincorporated companies ........... 286 220AZH Review of decisions ...................................................................... 287

Division 1A—Collection by instalments of tax on companies in respect of years of income before the year of income ending on 30 June 1990 288

221AAA Application ................................................................................... 288 221AA Interpretation................................................................................. 288 221AB Modified application of Division for early balancing

companies ..................................................................................... 289 221AC Liability to pay instalments of tax................................................. 289 221AD Amount of notional tax ................................................................. 290 221AE Amount of instalment of tax ......................................................... 292 221AF When instalment of tax payable.................................................... 295 221AG Estimated income tax.................................................................... 296 221AH Notice of alteration of amount of instalment................................. 302 221AI Application of payments of instalments of tax.............................. 303 221AJ Notice of instalment of tax to be prima facie evidence................. 304

Division 1B—Collection of Tax on Companies and Trustees of certain Funds 306

221AK General interpretative provisions .................................................. 306 221AKA Termination of operation of this Division..................................... 308 221AL Net capital gains to be disregarded in making certain

calculations ................................................................................... 309 221AM When income tax becomes due and payable................................. 310 221AN Modified application of Division for certain entities with

substituted accounting periods ...................................................... 310 221AO Liability to make payments under this Division............................ 312 221AP When initial payment to be made.................................................. 312 221AQ Amount of initial payment ............................................................ 313 221AR Power of relevant entity to revise estimate in certain

circumstances................................................................................ 314 221AS Statement as to basis of estimate................................................... 315 221AT Circumstances in which initial payment not required ................... 315 221AU Election to make single payment .................................................. 316 221AV Power of Commissioner to reduce amount of initial payment

or waive initial payment................................................................ 318 221AW Power of Commissioner to vary estimate of income tax............... 319 221AX Initial payment avoidance arrangements...................................... 320 221AY Additional tax if income or deduction transferred under

avoidance scheme ......................................................................... 326

xiv Income Tax Assessment Act 1936

221AZ Additional payments to form part of initial payment .................... 328 221AZA Refund to reduce initial payment of tax ........................................ 328 221AZB Notional tax .................................................................................. 329

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 1

Division 18—Principal residence

160ZZQ Principal residence

(1) In this section:

dependent child, in relation to a taxpayer, means a child of the taxpayer who is under the age of 18 years and is dependent on the taxpayer for economic support.

dwelling includes: (a) a unit of accommodation constituted by, or contained in, a

building, being a unit that consists, in whole or in substantial part, of residential accommodation; and

(b) a caravan, houseboat or other mobile home.

relevant period, in relation to the disposal of a dwelling by a taxpayer other than a taxpayer in the capacity of a trustee, means the period after 19 September 1985 during which the dwelling was owned by the taxpayer and includes any period during which land acquired after that date on which the dwelling is erected was owned by the taxpayer before the erection of the dwelling.

(1AA) For the purposes of this section, if: (a) land or a dwelling is acquired or disposed of under a contract

entered into at a particular time; and (b) legal ownership of the land or dwelling does not pass until a

later time; then, in spite of any other provision of this Part, the ownership of the land or dwelling is to be worked out on the basis of the legal ownership.

(1AB) If, under the contract mentioned in subsection (1AA) or another contract entered into in relation to it, the person to whom the legal ownership is to pass has a right or licence to occupy the land or dwelling before legal ownership passes, then that subsection has effect in relation to that person as if the legal ownership began when the licence or right was first exercisable.

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

2 Income Tax Assessment Act 1936

(1A) For the purposes of this section, where: (a) an asset was disposed of by a company or a trustee of a trust

estate to a taxpayer; (b) the asset was acquired by the company or the trustee on or

after 20 September 1985; and (c) because of section 160ZZMA, this Part (other than that

section) does not apply in respect of the disposal; the following provisions have effect:

(d) the taxpayer shall be treated as having owned the asset at all times during the period (in this subsection called the prior ownership period) commencing at the time when the company or trustee acquired the asset and ending at the time of the disposal of the asset;

(e) a dwelling to which the asset relates shall not be treated as the sole or principal residence of the taxpayer during the prior ownership period.

(2) For the purposes of this section, a person shall be taken to own, or to have acquired, a dwelling constituted by or contained in a building if the person owns or has acquired, as the case may be:

(a) in the case of a dwelling other than a flat or home unit: (i) a legal or equitable estate or interest in the land on

which the dwelling is erected; or (ii) a licence or right to occupy the dwelling; or (b) in the case of a flat or home unit: (i) a legal or equitable estate or interest in a stratum unit in

relation to the flat or home unit; (ii) a licence or right to occupy the flat or home unit; or (iii) a share in a company that owns a legal or equitable

estate or interest in the land on which the building containing the flat or home unit is erected, being a share that entitles the holder to a right of occupancy of the flat or home unit.

(3) For the purposes of this section, a dwelling owned by a person shall be deemed to include:

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 3

(a) any land owned by the person that is adjacent to the dwelling to the extent that:

(i) that land is used by the person primarily for private or domestic purposes in association with the dwelling; and

(ii) the sum of the area of that land and the area of the land on which the dwelling is situated does not exceed 2 hectares; and

(b) in the case of a dwelling being a flat or home unit—a garage, storeroom or other structure owned by the person that forms part of or is attached to or otherwise associated with the building containing the flat or home unit and is used by the person primarily for private or domestic purposes.

(4) If: (a) land that by virtue of paragraph (3)(a) forms part of a

dwelling owned by a person is disposed of by the person separately from the rest of the dwelling; or

(b) a garage, storeroom or other structure that forms part of a dwelling owned by a person is disposed of by the person separately from the rest of the dwelling;

this section does not apply in respect of the disposal.

(5) Where: (a) a taxpayer has at any time (in this subsection called the

relevant time), whether before or after the commencement of this subsection, acquired a legal or equitable estate or interest (other than a life interest) in land; and

(b) one of the following subparagraphs is applicable: (i) no dwelling or partly erected dwelling was on the land

at the relevant time and, after that time, the taxpayer: (A) erected a dwelling on the land; or (B) commenced to erect a dwelling on the land but

died before the erection of the dwelling was completed;

(ii) a partly erected dwelling was on the land at the relevant time and, after that time, the taxpayer:

(A) completed the erection of the dwelling; or

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

4 Income Tax Assessment Act 1936

(B) commenced to complete the erection of the dwelling but died before the erection of the dwelling was completed;

(iii) a dwelling or partly erected dwelling was on the land at the relevant time and, after that time, the taxpayer demolished the dwelling or partly erected dwelling and:

(A) erected a new dwelling on the land; or (B) commenced to erect a new dwelling on the land

but died before the erection of the dwelling was completed;

(iv) a dwelling was on the land at the relevant time and, after that time, the taxpayer:

(A) repaired or renovated the dwelling; or (B) commenced to repair or renovate the dwelling

but died before the repairs or renovations were completed; and

(c) if sub-subparagraph (b)(i)(A), (ii)(A), (iii)(A) or (iv)(A) applies:

(i) the dwelling became the sole or principal residence of the taxpayer for the purposes of this Part as soon as practicable after the dwelling was erected, the erection of the dwelling was completed or the repair or renovation of the dwelling was completed, as the case requires and continued to be the sole or principal residence of the taxpayer for the purposes of this Part for not less than 3 months; or

(ii) the taxpayer died after the dwelling was erected, the erection of the dwelling was completed or the repair or renovation of the dwelling was completed, as the case requires and the taxpayer’s death occurred:

(A) before it was practicable for the dwelling to become the taxpayer’s sole or principal residence; or

(B) during the period of 3 months referred to in subparagraph (i); and

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 5

(d) an election that this subsection is to apply in relation to the dwelling is made in accordance with subsection (5A) or (5B) by:

(i) in a case where subparagraph (ii) does not apply—the taxpayer; or

(ii) in a case where sub-subparagraph (b)(i)(B), (ii)(B), (iii)(B) or (iv)(B) or subparagraph (c)(ii) applies or any other case where the taxpayer died before the end of the period allowed for making an election without having made an election:

(A) if the taxpayer held the estate or interest as a joint tenant—the surviving joint tenant; or

(B) otherwise—the trustee of the estate of the taxpayer;

the following provisions have effect: (e) if subparagraph (c)(i) applies: (i) the period during which the dwelling was the sole or

principal residence of the taxpayer for the purposes of this Part includes:

(A) the period on and from the relevant commencing date to and including the date on which the dwelling was erected, the erection of the dwelling was completed or the repair or renovation of the dwelling was completed, as the case requires (other than any part of that period during which the taxpayer was the dependent child of another taxpayer); or

(B) the period of 4 years immediately before the dwelling became the sole or principal residence of the taxpayer (other than any part of that period during which the taxpayer was the dependent child of another taxpayer);

whichever period (in this paragraph called the construction period) is the shorter period; and

(ii) no other dwelling is to be treated as having been the sole or principal residence of the taxpayer during the construction period;

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

6 Income Tax Assessment Act 1936

(f) if sub-subparagraph (b)(i)(B), (ii)(B), (iii)(B) or (iv)(B) or subparagraph (c)(ii) applies:

(i) this Part has effect as if the dwelling was the sole or principal residence of the taxpayer at the time of his or her death; and

(ii) the period during which the dwelling was the sole or principal residence of the taxpayer for the purposes of this Part includes:

(A) the period on and from the relevant commencing date to and including the date of the death of the taxpayer (other than any part of that period during which the taxpayer was the dependent child of another taxpayer); or

(B) the period of 4 years immediately before the death of the taxpayer (other than any part of that period during which the taxpayer was the dependent child of another taxpayer);

whichever period (in this paragraph called the construction period) is the shorter period; and

(iii) no other dwelling is to be treated as having been the sole or principal residence of the taxpayer during the construction period.

(5AA) For the purposes of subsection (5): (a) a reference to the relevant commencing date is a reference to: (i) if subparagraph (5)(b)(iii) applies and the dwelling, or

partly completed dwelling, that was demolished was occupied by the taxpayer or another person after the relevant time—the date on which the dwelling ceased, or last ceased, to be so occupied; or

(ia) if: (A) subparagraph (5)(b)(iv) applies; and (B) the dwelling was occupied by the taxpayer or

another person after the relevant time; and (C) the dwelling ceased to be so occupied for the

purpose of allowing the repairs or renovations to be carried out;

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 7

the date on which the dwelling ceased, or last ceased, to be so occupied; or

(ii) otherwise—the date on which the taxpayer acquired the estate or interest in the land; and

(b) a taxpayer who has, whether before or after the commencement of this subsection, entered into a contract or contracts for the erection of, or for the completion of the erection of, a dwelling is taken to have commenced to erect, or to have commenced to complete the erection of, the dwelling at the time when the contract or the first contract was entered into; and

(c) a taxpayer who has, whether before or after the commencement of this paragraph, entered into a contract or contracts for the repair or renovation of a dwelling is taken to have commenced to repair or renovate the dwelling at the time when the contract or the first contract was entered into.

(5A) An election for the purposes of subsection (5) does not have any effect unless it is made on or before the date of lodgment of the taxpayer’s return of income of the later of the following years of income:

(a) the year of income in which the dwelling first became the sole or principal residence of the taxpayer for the purposes of this Part;

(b) the year of income in which this subsection commenced; or within such further period as the Commissioner allows.

(5B) An election by a surviving joint tenant, or a trustee, in relation to a deceased taxpayer for the purposes of subsection (5) does not have any effect unless it is made on or before whichever is the later of the following dates:

(a) the date of lodgment of the return of income of the deceased taxpayer’s estate for the year of income in which the taxpayer died;

(b) the last day of the year of income in which the Act that inserted this subsection received the Royal Assent;

or within such further period as the Commissioner allows.

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

8 Income Tax Assessment Act 1936

(6) A reference in this section to a taxpayer having acquired a dwelling as a beneficiary in the estate of a deceased person is a reference to a taxpayer having acquired a dwelling:

(a) under the will of a deceased person, or under such a will as varied by an order of a court; or

(b) by operation of a law as a result of the intestacy of a deceased person, or by operation of law as a result of such an intestacy as the operation of the law is varied by an order of a court; or

(c) under a deed of arrangement where: (i) the deed was entered into in settlement of a claim to

participate in the distribution of the estate of the deceased person; and

(ii) the consideration (if any) given by the taxpayer for the dwelling consisted of the variation or waiver of a claim to one or more other assets that formed part of that estate;

whether the dwelling was transmitted directly to the taxpayer or was transferred to the taxpayer by the executor of the will, or by the administrator of the estate, of the deceased person.

(6A) Where: (a) a taxpayer and another person owned a dwelling as joint

tenants; and (b) the other person died;

this section applies according to its tenor to the acquisition by the taxpayer of the dwelling as a result of the death of the other person as it applies to a taxpayer who acquired the dwelling as a beneficiary in the estate of a deceased person.

(7) A reference in this section to the acquisition or disposal by a person of a dwelling or to the transmission or transfer of a dwelling to a person includes a reference to the acquisition or disposal by a person or to the transmission or transfer to a person, as the case may be, of the asset the ownership of which, by virtue of subsection (2), constitutes ownership of the dwelling.

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 9

(8) For the purposes of this section: (a) a dwelling shall be deemed to be the sole or principal

residence of a person at a particular time notwithstanding that it is used at that time both for that purpose and another purpose or other purposes; and

(b) where: (i) a taxpayer disposes of a dwelling that: (A) was the sole or principal residence of the

taxpayer for a continuous period of not less than 3 months included in the period of 12 months ending at the time of disposal; and

(B) the dwelling was not used for gaining or producing assessable income in any part of that period of 12 months other than the part of that period in which the dwelling was also the sole or principal residence of the taxpayer; and

(ii) before disposing of the dwelling, the taxpayer acquired another dwelling and that other dwelling became the next sole or principal residence of the taxpayer;

each of those dwellings shall be deemed to be the sole or principal residence of the taxpayer during:

(iii) in a case where the taxpayer acquired that other dwelling more than 3 months before the time of disposal—the period of 3 months ending at the time of disposal; or

(iv) in any other case—the period commencing on the day on which the taxpayer acquired that other dwelling and ending at the time of disposal.

(9) Where: (a) a dwelling is the sole or principal residence of a taxpayer at a

particular time; and (b) at that time, another dwelling is the sole or principal

residence of the taxpayer’s spouse or of a dependent child of the taxpayer;

whichever of those dwellings is nominated by the taxpayer and the taxpayer’s spouse, or by the taxpayer, as the case may be, shall, for

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

10 Income Tax Assessment Act 1936

the purposes of this section, be deemed to be the sole or principal residence of the taxpayer and the taxpayer’s spouse, or the taxpayer and the dependent child of the taxpayer, as the case may be, at that time.

(10) Where, under subsection (9), a taxpayer nominates a dwelling, and the taxpayer’s spouse nominates a different dwelling, in relation to the same period:

(a) in the case of the dwelling nominated by the taxpayer: (i) if the interest of the taxpayer in the dwelling throughout

that period did not exceed one-half of the total of all the interests in the dwelling—the dwelling shall, for the purposes of this section, be deemed to have been the sole or principal residence of the taxpayer during that period; or

(ii) in any other case—the dwelling shall, for the purposes of this section, be deemed to have been the sole or principal residence of the taxpayer during one-half of that period; or

(b) in the case of the dwelling nominated by the taxpayer’s spouse:

(i) if the interest of the spouse in the dwelling throughout that period did not exceed one-half of the total of all the interests in the dwelling—the dwelling shall, for the purposes of this section, be deemed to have been the sole or principal residence of the spouse during that period; or

(ii) in any other case—the dwelling shall, for the purposes of this section, be deemed to have been the sole or principal residence of the spouse during one-half of that period.

(11) Where: (a) at a particular time (in this subsection called the cessation

time), a dwelling owned by a taxpayer ceases to be the sole or principal residence of the taxpayer (disregarding subsection (20D)); and

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 11

(b) an election that this subsection is to apply in relation to the taxpayer and in relation to the dwelling is made in accordance with subsection (11A) by:

(i) if the taxpayer died before the end of the period allowed for making an election without having made an election:

(A) if the taxpayer and another person owned the dwelling as joint tenants—the surviving joint tenant; or

(B) otherwise—the trustee of the estate of the taxpayer; or

(ii) in any other case—the taxpayer; then, for the purposes of this section (other than this subsection and subsection (20D)), during the period:

(c) commencing at the cessation time; and (d) ending at the earliest of the following later times: (i) the time when the dwelling again became the sole or

principal residence of the taxpayer; (ii) the end of the relevant period; (iii) the end of the period of 6 years (whether that period is

continuous or represents the aggregation of 2 or more periods):

(A) commencing at or after the cessation time; and (B) during which the part of the dwelling that was

the sole or principal residence of the taxpayer before the cessation time was used for the purpose of gaining or producing assessable income;

the following provisions have effect: (e) the dwelling is taken to have been the sole or principal

residence of the taxpayer; (f) no other dwelling is taken as having been the sole or

principal residence of the taxpayer; (g) any use for the purpose of gaining or producing assessable

income of the part of the dwelling that was the sole or principal residence of the taxpayer before the cessation time is to be disregarded.

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

12 Income Tax Assessment Act 1936

(11A) An election for the purposes of subsection (11) must be made: (a) in the case of an election by a taxpayer—on or before the

date of lodgment of the taxpayer’s return of income for the later of the following years of income:

(i) the year of income in which the disposal of the dwelling takes place;

(ii) the year of income in which this subsection commenced; or

(b) in the case of an election by a surviving joint tenant, or a trustee, in relation to a deceased taxpayer—on or before whichever is the later of the following dates:

(i) the date of lodgment of the return of income of the deceased taxpayer’s estate for the year of income in which the taxpayer died;

(ii) the last day of the year of income in which this subsection commenced;

or, in either case, within such further period as the Commissioner allows.

(12) Subject to subsection (21), where: (a) a dwelling owned by a taxpayer, being a natural person other

than: (i) a person who acquired the dwelling as a beneficiary in

the estate of a deceased person; or (ii) a person in the capacity of a trustee; is disposed of; and (b) the dwelling was, throughout the relevant period, the sole or

principal residence of the taxpayer; a capital gain shall not be deemed to have accrued to the taxpayer, and a capital loss shall not be deemed to have been incurred by the taxpayer, as the case requires, in respect of the disposal of the dwelling.

(13) Subject to subsection (21), where: (a) a dwelling owned by a taxpayer, being a natural person who

acquired the dwelling as a beneficiary in the estate of a deceased person, is disposed of;

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 13

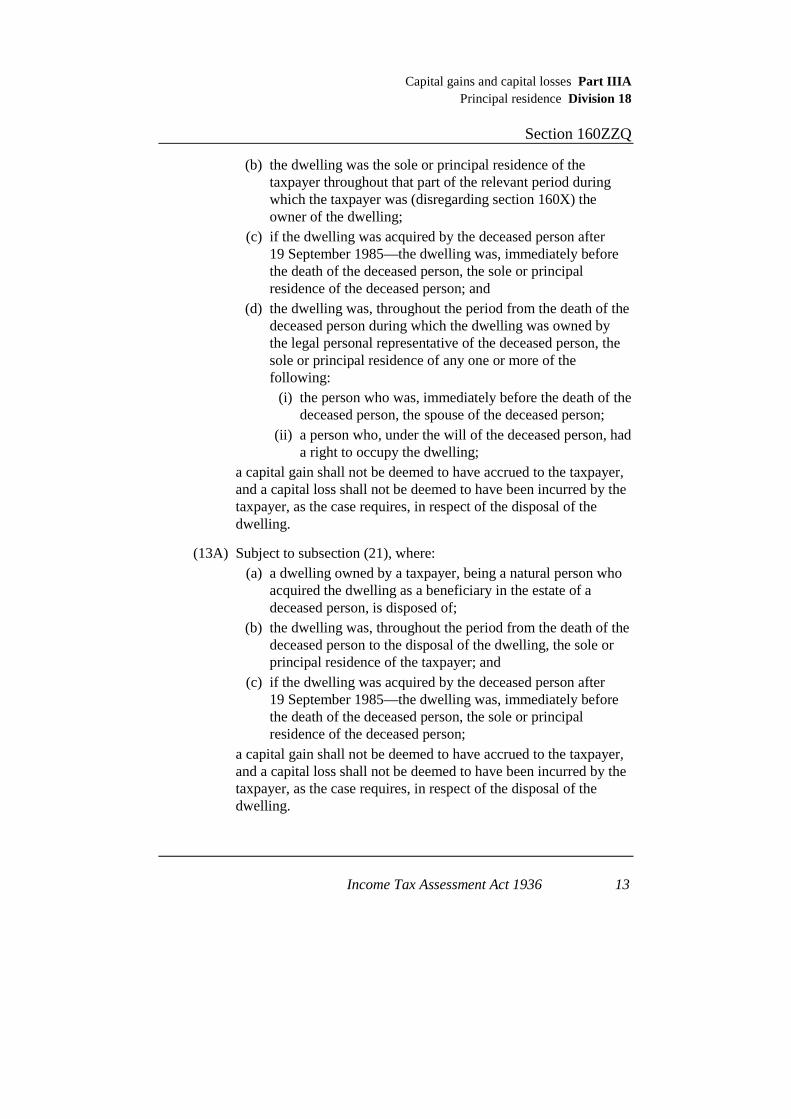

(b) the dwelling was the sole or principal residence of the taxpayer throughout that part of the relevant period during which the taxpayer was (disregarding section 160X) the owner of the dwelling;

(c) if the dwelling was acquired by the deceased person after 19 September 1985—the dwelling was, immediately before the death of the deceased person, the sole or principal residence of the deceased person; and

(d) the dwelling was, throughout the period from the death of the deceased person during which the dwelling was owned by the legal personal representative of the deceased person, the sole or principal residence of any one or more of the following:

(i) the person who was, immediately before the death of the deceased person, the spouse of the deceased person;

(ii) a person who, under the will of the deceased person, had a right to occupy the dwelling;

a capital gain shall not be deemed to have accrued to the taxpayer, and a capital loss shall not be deemed to have been incurred by the taxpayer, as the case requires, in respect of the disposal of the dwelling.

(13A) Subject to subsection (21), where: (a) a dwelling owned by a taxpayer, being a natural person who

acquired the dwelling as a beneficiary in the estate of a deceased person, is disposed of;

(b) the dwelling was, throughout the period from the death of the deceased person to the disposal of the dwelling, the sole or principal residence of the taxpayer; and

(c) if the dwelling was acquired by the deceased person after 19 September 1985—the dwelling was, immediately before the death of the deceased person, the sole or principal residence of the deceased person;

a capital gain shall not be deemed to have accrued to the taxpayer, and a capital loss shall not be deemed to have been incurred by the taxpayer, as the case requires, in respect of the disposal of the dwelling.

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

14 Income Tax Assessment Act 1936

(14) Subject to subsection (21), where: (a) a taxpayer, being a natural person, disposes of a dwelling that

the taxpayer acquired as a beneficiary in the estate of a deceased person;

(b) the disposal took place within 2 years after the date of the death of the deceased person; and

(c) if the dwelling was acquired by the deceased person after 19 September 1985, the dwelling was, immediately before the death of the deceased person, the sole or principal residence of the deceased person;

a capital gain shall not be deemed to have accrued to the taxpayer, and a capital loss shall not be deemed to have been incurred by the taxpayer, as the case requires, in respect of the disposal of the dwelling.

(15) Subject to subsection (21), where: (a) a dwelling owned by a taxpayer in the capacity of the trustee

of the estate of a deceased person is disposed of; (b) either of the following subparagraphs is applicable: (i) the disposal took place within 2 years after the date of

the death of the deceased person; or (ii) the dwelling was, throughout the period from the death

of the deceased person to the time of disposal of the dwelling by the taxpayer, the sole or principal residence of any one or more of the following:

(A) the person who was, immediately before the death of the deceased person, the spouse of the deceased person;

(B) a person who, under the will of the deceased person, had a right to occupy the dwelling; and

(c) if the dwelling was acquired by the deceased person after 19 September 1985, the dwelling was, immediately before the death of the deceased person, the sole or principal residence of the deceased person;

a capital gain shall not be deemed to have accrued to the taxpayer, and a capital loss shall not be deemed to have been incurred by the

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 15

taxpayer, as the case requires, in respect of the disposal of the dwelling.

(16) Subject to subsection (21), where: (a) a dwelling owned by a taxpayer referred to in

paragraph (12)(a) is disposed of; (b) the dwelling was the sole or principal residence of the

taxpayer during part only of the relevant period; and (c) but for this section and subsection 160ZA(1), a capital gain

would have accrued to the taxpayer, or the taxpayer would have incurred a capital loss, in respect of the disposal;

a capital gain shall be deemed to have accrued to the taxpayer, or the taxpayer shall be deemed to have incurred a capital loss, as the case may be, in respect of the disposal of the dwelling, of an amount calculated in accordance with the formula:

AB

C,

where:

A is the amount of the capital gain or of the capital loss, as the case may be, referred to in paragraph (c);

B is the number of days in the part of the relevant period during which the dwelling was not the sole or principal residence of the taxpayer; and

C is the number of days in the relevant period.

(17) Subject to subsections (20A) and (21), where: (a) a dwelling owned by a taxpayer referred to in

paragraph (13)(a) is disposed of; (aa) the disposal is not covered by subsection (13), (13A) or (14); (b) any one or more of the following subparagraphs is or are

applicable: (i) the dwelling was the sole or principal residence of the

taxpayer during the whole or a portion of the part of the relevant period referred to in paragraph (13)(b);

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

16 Income Tax Assessment Act 1936

(ii) in a case to which paragraph (13)(c) applies—the dwelling was the sole or principal residence of the deceased person referred to in that paragraph during the whole or part of the period during which the deceased person owned the dwelling;

(iii) in a case to which paragraph (13)(d) applies—the dwelling was the sole or principal residence of any one or more of the persons referred to in subparagraphs (13)(d)(i) and (ii) during the whole or part of the period referred to in that paragraph; and

(c) but for this section and subsection 160ZA(1), a capital gain would have accrued to the taxpayer, or the taxpayer would have incurred a capital loss, in respect of the disposal;

a capital gain shall be deemed to have accrued to the taxpayer, or the taxpayer shall be deemed to have incurred a capital loss, as the case may be, in respect of the disposal of the dwelling, of an amount calculated in accordance with the formula:

AB

C,

where:

A is the amount of the capital gain or of the capital loss, as the case may be, referred to in paragraph (c).

B is the sum of the following: (d) the number of days (if any) in the relevant period during

which the taxpayer owned the dwelling (disregarding section 160X), but the dwelling was not the taxpayer’s sole or principal residence;

(e) if the deceased person acquired the dwelling on or after 20 September 1985—the number of days (if any) in the period during which the deceased person owned the dwelling, but the dwelling was not the deceased person’s sole or principal residence;

(f) the number of days (if any) in the period mentioned in paragraph (13)(d) during which the dwelling was not the sole or principal residence of any of the persons mentioned in subparagraphs (13)(d)(i) and (ii).

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 17

C is: (h) in a case where the dwelling was acquired by the deceased

person before 20 September 1985—the number of days in the period from and including the date of the death of the deceased person to and including the day immediately before the date of the disposal; or

(j) in a case where the dwelling was acquired by the deceased person on or after 20 September 1985—the number of days in the period from and including the date on which the dwelling was acquired by the deceased person to and including the day immediately before the date of disposal.

Note: The number of days worked out under paragraphs (e) and (j) is modified in some cases: see subsection (20AA).

(17A) Subject to subsections (20A) and (21), where: (a) a dwelling owned by a taxpayer referred to in

paragraph (13A)(a) is disposed of; (aa) the disposal is not covered by subsection (13), (13A) or (14); (b) either or both of the following subparagraphs is or are

applicable: (i) the dwelling was the sole or principal residence of the

taxpayer during the whole or part of the period referred to in paragraph (13A)(b);

(ii) in a case to which paragraph (13A)(c) applies—the dwelling was the sole or principal residence of the deceased person referred to in that paragraph during the whole or part of the period during which the deceased person owned the dwelling; and

(c) but for this section and subsection 160ZA(1), a capital gain would have accrued to the taxpayer, or the taxpayer would have incurred a capital loss, in respect of the disposal;

a capital gain shall be deemed to have accrued to the taxpayer, or the taxpayer shall be deemed to have incurred a capital loss, as the case may be, in respect of the disposal of the dwelling, of an amount calculated in accordance with the formula:

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

18 Income Tax Assessment Act 1936

AB

C,

where:

A is the amount of the capital gain or of the capital loss, as the case may be, referred to in paragraph (c).

B is the sum of the following: (d) the number of days (if any) in the period from the deceased

person’s death to the disposal of the dwelling during which the dwelling was not the taxpayer’s sole or principal residence;

(e) if the deceased person acquired the dwelling on or after 20 September 1985—the number of days (if any) in the period during which the deceased person owned the dwelling, but the dwelling was not the deceased person’s sole or principal residence.

C is: (g) in a case where the dwelling was acquired by the deceased

person before 20 September 1985—the number of days in the period from and including the date of the death of the deceased person to and including the day immediately before the date of the disposal; or

(h) in a case where the dwelling was acquired by the deceased person on or after 20 September 1985—the number of days in the period from and including the date on which the dwelling was acquired by the deceased person to and including the day immediately before the date of disposal.

Note: The number of days worked out under paragraphs (e) and (h) is modified in some cases: see subsection (20AA).

(18) Subject to subsections (20A) and (21), where: (a) a dwelling owned by a taxpayer referred to in

paragraph (14)(a) is disposed of; (b) the disposal took place within 2 years after the date of death

of the deceased person; (c) the dwelling was the sole or principal residence of the

deceased person referred to in paragraph (14)(a) during part

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 19

only of the period during which the deceased person owned the dwelling; and

(d) but for this section and subsection 160ZA(1) a capital gain would have accrued to the taxpayer, or the taxpayer would have incurred a capital loss, in respect of the disposal;

a capital gain shall be deemed to have accrued to the taxpayer, or the taxpayer shall be deemed to have incurred a capital loss, as the case may be, in respect of the disposal of the dwelling, of an amount calculated in accordance with the formula

AB

C,

where:

A is the amount of the capital gain or of the capital loss, as the case may be, referred to in paragraph (d);

B is the number of days in the part of the period during which the deceased person owned the dwelling during which the dwelling was not the sole or principal residence of the deceased person; and

C is the number of days in the period during which the deceased person owned the dwelling.

(19) Subject to subsections (20A) and (21), where: (a) a dwelling owned by a taxpayer in the capacity of the trustee

of the estate of a deceased person is disposed of; (aa) the disposal is not covered by subsection (15); (b) either or both of the following subparagraphs is or are

applicable: (i) the dwelling was the sole or principal residence of any

one or more of the persons referred to in sub-subparagraphs (15)(b)(ii)(A) and (B), during the whole or part of the period referred to in subparagraph (15)(b)(ii);

(ii) in a case to which paragraph (15)(c) applies—the dwelling was the sole or principal residence of the deceased person during the whole or part of the period

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

20 Income Tax Assessment Act 1936

during which the deceased person owned the dwelling; and

(c) but for this section and subsection 160ZA(1), a capital gain would have accrued to the taxpayer, or the taxpayer would have incurred a capital loss, as the case may be, in respect of the disposal;

a capital gain shall be deemed to have accrued to the taxpayer, or the taxpayer shall be deemed to have incurred a capital loss, as the case may be, in respect of the disposal of the dwelling, of an amount calculated in accordance with the formula:

AB

C,

where:

A is the amount of the capital gain or of the capital loss, as the case may be, referred to in paragraph (c).

B is the sum of the following: (d) the number of days (if any) in the period mentioned in

subparagraph (15)(b)(ii) during which the dwelling was not the sole or principal residence of any of the persons mentioned in sub-subparagraphs (15)(b)(ii)(A) and (B);

(e) if the deceased person acquired the dwelling on or after 20 September 1985—the number of days (if any) in the period during which the deceased person owned the dwelling, but the dwelling was not the deceased person’s sole or principal residence.

C is: (g) in a case where the dwelling was acquired by the deceased

person before 20 September 1985—the number of days in the period from and including the date of the death of the deceased person to and including the day immediately before the date of the disposal; or

(h) in a case where the dwelling was acquired by the deceased person on or after 20 September 1985—the number of days in the period from and including the date on which the

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 21

dwelling was acquired by the deceased person to and including the day immediately before the date of disposal.

Note: The number of days worked out under paragraphs (e) and (h) is modified in some cases: see subsection (20AA).

(20) Subject to subsections (20A) and (21), where: (a) a dwelling owned by a taxpayer referred to in

paragraph (15)(a) is disposed of; (b) the disposal took place within 2 years after the date of death

of the deceased person; (c) the dwelling was the sole or principal residence of the

deceased person referred to in paragraph (15)(a) during part only of the period during which the deceased person owned the dwelling; and

(d) but for this section and subsection 160ZA(1) a capital gain would have accrued to the taxpayer, or the taxpayer would have incurred a capital loss, in respect of the disposal;

a capital gain shall be deemed to have accrued to the taxpayer, or the taxpayer shall be deemed to have incurred a capital loss, as the case may be, in respect of the disposal of the dwelling, of an amount calculated in accordance with the formula:

AB

C,

where:

A is the amount of the capital gain or of the capital loss, as the case may be, referred to in paragraph (d);

B is the number of days in the part of the period during which the deceased person owned the dwelling during which the dwelling was not the sole or principal residence of the deceased person; and

C is the number of days in the period during which the deceased person owned the dwelling.

(20A) Where both subsections (17) and (18), both subsections (17A) and (18) or both subsections (19) and (20) would, but for this subsection, apply to a taxpayer in respect of the disposal of a dwelling owned by the taxpayer:

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

22 Income Tax Assessment Act 1936

(a) if each of the subsections that would so apply has the effect of deeming a capital gain to have accrued to the taxpayer in respect of the disposal—only that subsection applies which deems the smaller capital gain to have accrued; or

(b) if each of the subsections that would so apply has the effect of deeming the taxpayer to have incurred a capital loss in respect of the disposal—only that subsection applies which deems the larger capital loss to have been incurred.

(20AA) For the purposes of subsections (17), (17A) and (19), if, immediately before the death of the deceased person concerned, the dwelling concerned:

(a) was the deceased person’s sole or principal residence; and (b) was not being used for the purpose of gaining or producing

assessable income; then:

(c) the number of days mentioned in paragraphs (17)(e), (17A)(e) or (19)(e) (as appropriate) is taken to be nil; and

(d) the number of days mentioned in paragraphs (17)(j), (17A)(h) or (19)(h) (as appropriate) is worked out from and including the date of the death, instead of the date on which the deceased person acquired the dwelling.

(20B) Where: (a) but for this subsection a capital gain would be deemed to

have accrued to a taxpayer, or a taxpayer would be deemed to have incurred a capital loss, in respect of the disposal of a dwelling by the taxpayer; and

(b) the taxpayer owned the dwelling as the trustee of, or acquired the dwelling as a beneficiary in, the estate of a deceased person (in this subsection called the relevant deceased person); and

(ba) subparagraph 160X(5)(a)(ii) does not apply to the taxpayer’s acquisition of the dwelling;

then: (c) in the case of a dwelling disposed of on or before 15 August

1989—that capital gain is to be reduced or that capital loss is to be increased; or

Capital gains and capital losses Part IIIA Principal residence Division 18

Section 160ZZQ

Income Tax Assessment Act 1936 23

(d) in the case of a dwelling disposed of after that date—that capital gain is to be increased or reduced or that capital loss is to be increased or reduced;

by such amount as the Commissioner considers appropriate to take into account the extent to which the dwelling was, during any period that occurred after 19 September 1985 and before the dwelling was acquired by the relevant deceased person, the sole or principal residence of any one or more of the following:

(e) any person who owned the dwelling at the time of his or her death;

(f) any person who, immediately before the death of a person referred to in paragraph (e), was the spouse of that person;

(g) any person who, under the will of a person, had a right to occupy the dwelling;

(h) any person who acquired the dwelling as a beneficiary in the estate of a deceased person.

(20C) Subject to subsection (21), where, pursuant to the will of a deceased person, a taxpayer in the capacity of a trustee of the estate of the deceased person acquired a dwelling after 19 September 1985 for occupation by another person (in this subsection called the beneficiary):

(a) if the taxpayer disposes of the dwelling to the beneficiary for no consideration:

(i) the taxpayer is not taken for the purposes of this Part other than this subsection to have disposed of the dwelling; and

(ii) the beneficiary is taken for the purposes of this Part to have acquired the dwelling on the date on which it was acquired by the taxpayer; and

(iii) the cost base, the indexed cost base or the reduced cost base to the beneficiary of the dwelling for the purposes of this Part includes any amount that would, if the taxpayer had disposed of the dwelling for the purposes of this Part at the time when ownership of the dwelling passed to the beneficiary, have been included in the cost base, the indexed cost base or the reduced cost base, as the case may be, of the dwelling to the taxpayer as a

Part IIIA Capital gains and capital losses Division 18 Principal residence Section 160ZZQ

24 Income Tax Assessment Act 1936

result of the taxpayer having incurred expenditure in respect of the dwelling; or

(b) if the taxpayer disposes of the dwelling to a person otherwise than as mentioned in paragraph (a):

(i) if the dwelling was the sole or principal residence of the beneficiary during the whole of the period from the time when the dwelling was acquired by the taxpayer to the time when it was so disposed of—a capital gain is not to be deemed to have accrued to the taxpayer, and a capital loss is not to be deemed to have been incurred by the taxpayer, as the case requires, in respect of the disposal of the dwelling; or