Embed Size (px)

Citation preview

Discussion Papers

Regional Program on Enterprise Development

Incentives and Obstacles to Growth: Lessons from Manufacturing Case Studies in Madagascar

Olivier Cadot and John Nasir

Edited by Linda Cotton

November 2001

RPED Paper No. 117

The views and interpretations expressed in this study are solely those of the authors. They do not necessarily represent the views of the World Bank or its member countries and should not be attributed to the World Bank or its affiliated organizations

Abstract

Since the mid-1980s the Malagasy government has pursued fiscal and administrative reform along with economic and financial liberalization. These efforts have contributed to steady GDP growth rates since 1995, averaging 4.1 percent between 1997 and 1999. Manufacturing has been keeping pace with GDP, its share hovering around 12 percent. Firms located in Export Processing Zones (EPZs) have experienced tremendous growth, (19% a year between 1995 and 1999), but their production still represents a relatively small share of value added. Most of the growth in the Malagasy economy has occurred in transportation, construction and other non-tradable sectors. By contrast, the development of import-substituting (IS) firms has been considerably slower. In the past, IS firms became accustomed to producing for the domestic market under the protection of high import barriers. These companies are stagnating as they find themselves unprepared for the stiff competition from imports unleashed by recent liberalization.

The present market structure has created distortions, pulling resources into the EPZs (and to

some extent, the non-tradables sector) from the rest of the economy. Given the right environment, all segments of the economy can thrive, contributing to a faster overall growth rate with a much broader base. Despite the dramatic growth of recent years, EPZs also face constraints and there is considerable room for improvement. Firm-level studies allow for distinguishing the impediments and challenges faced by these disparate groups. Madagascar must address these issues to improve productivity and competitiveness both inside and outside EPZs, as trade barriers fall around the world and the country becomes more integrated into the global economy.

Incentives and Obstacles to Growth: Lessons from Manufacturing Case Studies in Madagascar

Introduction.............................................................................................................................. 1 Growth and Structure of the Industrial Sector ................................................................. 2 Reform and Restructuring................................................................................................ 4

Export Processing Zones.......................................................................................................... 5

Textiles and Garments ..................................................................................................... 6 Information Technology ................................................................................................ 12 Handicrafts ..................................................................................................................... 16

The Common Law Sector ...................................................................................................... 22

Infrastructure.................................................................................................................. 28 Taxes .............................................................................................................................. 29 Market and Industry Structure ....................................................................................... 30 Barriers to Entry............................................................................................................. 31 Conclusion ..................................................................................................................... 32

Cross-Cutting Issues .............................................................................................................. 33

Infrastructure.................................................................................................................. 33 Finance and Banking...................................................................................................... 34 Training and Education.................................................................................................. 37 Business Environment.................................................................................................... 40

Conclusion ............................................................................................................................. 42 References .............................................................................................................................. 44 Abbreviations ......................................................................................................................... 45

Introduction In recent years Madagascar has undertaken numerous economic reforms and instituted new

liberalization policies. However, while macro-economic policies are important and getting the prices �right� is necessary for international competitiveness, this is not sufficient. It is also necessary to have a supporting micro-economic environment that lowers transactions costs and facilitates trade. Barriers to entry must be removed and the incentive system structured so that capital can be deployed to the most efficient sectors. Market failures, especially in the financial sector, that inhibit investment to improve competitiveness and to acquire new technology must be minimized. Government administrative and regulatory requirements that discourage both foreign and domestic investment must also be eliminated.

An inspection of the incentive system and the regulatory framework gives a general idea of

the supportiveness of the business environment. However, this alone is not adequate to determine the effects of the overall environment on firm incentives and profitability. Nor does it allow us to differentiate between obstacles that are peculiar to individual firms or sectors and those that are �cross cutting,� i.e. those that affect all firms in all sectors.

This type of analysis is particularly important to Madagascar where the industrial sector

appears to be splitting into two distinct segments, poised on unique growth trajectories. In one group are enterprises focusing on the export market, enjoying the privileges of Export Processing Zones (EPZ) and growing rapidly. In the other group are Common Law (CL) companies, which do not enjoy the favorable treatment accorded EPZ firms but are accustomed to being protected by high barriers while producing for the domestic market in the past. However, these common law companies are now stagnating as they find themselves unprepared for the stiff competition from imports unleashed by liberalization.

Firm-level studies such as this one are capable of deciphering the impediments and challenges faced by these disparate groups. The micro-economic firm level approach allows us to determine which problems are firm and sector specific, which are limited to one group and which are cross cutting-issues that reduce profitability and competitiveness across all sectors.

This paper examines the results of firm interviews in representative industrial sectors

conducted in July 2001 as a part of the Integrated Framework program established by the World Trade Organization ministers in 1996. This program is designed to promote the integration of the least developed countries into the global economy. Following a brief review of the overall characteristics of the industrial sector, the remainder of the paper is devoted to identifying sources of competitiveness and impediments to growth. The manufacturing firms interviewed are separated into the two distinct divisions mentioned above, EPZs and Common Law sector firms, (in particular, the lagging import-substituting sector) and are considered in turn. Cross-cutting issues are covered in the final section which also forms the basis of recommendations for reforms and motivation for more detailed analysis to be carried out elsewhere.

To anticipate, this paper�s overall conclusions are as follows:

2

• The rapid growth of firms in the Export Processing Zone (EPZ) demonstrates that Malagasy industry can be internationally competitive and has the potential to spur growth and lead Madagascar�s integration into the world economy.

• However, growth in EPZ firms is still fragile and dependent upon footloose investment. Its continuation requires a stable and favorable regulatory environment and substantial improvements in the provision of infrastructure and public services.

• Common Law (CL) firms producing for the local market have been protected by formal and informal barriers to entry and have not yet fully restructured to face competition from imports.

• These CL firms face a more difficult business environment than EPZ firms. For them to survive and be able to stand up to increased competition, investment incentives must be improved through a lighter and more stable fiscal regime, improved access to credit, and better domestic infrastructure.

Growth and Structure of the Industrial Sector This background section provides an introductory overview of the Malagasy economy in

terms of recent growth trends in the primary, secondary and tertiary sectors. In the primary sector, agriculture accounts for about 55 percent of value added, while livestock and fisheries represent about 28 percent and forestry about 18 percent. Real growth in the primary sector fell from 2.5 percent in 1996 to 1.9 percent in 1997, driven by a decline in agriculture, as a result of bad weather. Agriculture has also been severely affected by locust infestations. The share of agro-processing has declined steadily; production fell by 11 percent in 1999 and by 23 percent in 2000. However, this decline has been somewhat offset by increasing investment in shrimp production. Shrimp producers have restructured their operations in anticipation of the removal of a trade embargo by the European Union in the late 1990s. Since then, shrimp production (particularly aquaculture) has grown at a healthy pace. Shrimp exports are now the largest source of export revenues in Madagascar.

The IMF (2000) estimates that growth in the secondary sector increased from 1.9 percent on

average in 1995-96 to about 4.7 percent in the period 1997-99, largely because of the performance of the beverage and tobacco industries, both essentially non-tradables. The food and beverage industry contributes about 6 percent to total value added and represents about half the output in the secondary sector. Also, the Export Processing Zone is an important contributor to exports and a significant source of employment in the manufacturing sector. It still represents a fairly small share of value added (less than 5 percent), but has grown rapidly in terms of size and significance in the Malagasy economy. It is expected that EPZ-led growth will continue to be high over the next several years.

Madagascar�s exports are still dominated by agricultural products, although their share has

fallen. Exports of food and agricultural raw materials accounted for over 75 percent of exports in 1990, by 1999 this figure had dropped to 42.5 percent. Much of this change was driven by the increase in EPZ exports. In the same time period the share of textiles in exports rose from 4.5 percent to over 29 percent. Madagascar is also developing exports in other areas such as handicrafts and services such as data processing. The change in the composition of exports has been accompanied by a change in the destination. In 1999, exports to Japan and the United

3

States fell to 1.4 percent and 5.4 percent of total exports respectively, down from 6.9 percent and 17.8 percent in 1990. The process of shifting resources toward more efficient production has begun but is moving slowly. So far, most of the investment in the EPZ has come from abroad. But our survey revealed that more indigenous investors, recognizing that competition in the domestic market is increasing and that the business environment is not improving, are switching investment into export sectors such as fresh vegetables, textiles, services and handicrafts

The tertiary sector, primarily transport and services, has been the highest source of growth

overall. Together with retail and wholesale trade, these sectors are perhaps the most important contributors to value added in the past few years. While the tourism sector continues to grow, it is also important to note that the government�s role in this and other private sector activity has diminished considerably (in keeping with its commitment to liberalization). According to the IMF (2000), rising incomes and the expansion of capacity in the tourism industry have also contributed to annual growth rates of over 10 percent in the construction industry in the late 1990s.

Table 1: Average growth by sector (as percentage of GDP) Branches 1995 1996 1997 1998 1999 Food Industry 2.8 1.4 -3.9 10.2 -4 Drinks and Tobacco 9.3 22.5 9.6 7.5 16 Textiles and Clothing 1.8 -14.2 6.2 -6.3 7.1 Industry of Wood 3.4 5.4 0.3 11.9 8.7 Paper and Publishing -5 -41.8 -11.1 -4.4 -19.4 Leather Articles -19.7 2.9 -56.9 -11.8 12.8 Electric Equipment 13.3 0 7.5 -1.6 -1.4 Metal Product 31.1 -8 6.8 6.8 3.1 Chemicals -16.8 3.3 3.7 1.3 5.9 Energy 12.9 8.4 17.3 -1.6 4.5 Construction Material 10.9 0.9 15 1.8 3.1 Transport Equipment -6.1 3.1 4 5.5 5.5 Mining Products 15.3 -6.6 8.5 5.5 -31.5 TOTAL 6.5 2.6 8.4 1.5 2.3 Source: Instat

4

Reform and Restructuring Since the mid 1980s, the Malagasy government has pursued fiscal and administrative reform

as well as economic and financial liberalization. It took a while for these reforms to take effect, but real GDP growth has been steady since 1995, averaging 4.1 percent per year between 1997 and 1999. The fastest growth has been among firms registered under the Export Processing Zone (EPZ) regime. However, EPZ firms still represent a relatively small share of value added in the economy. Most of the recent growth has occurred in non-tradable sectors: construction, transport, beverages and tobacco, while other sectors have stagnated. Traditional import-substituting firms, accustomed to high levels of protection, have not restructured or invested enough to withstand the growing competition from imports. Consequently, resources have been flowing out of traditional import substituting industries and toward non-tradables.

Malagasy firms producing for the domestic market find it difficult to compete with imports

not just because they failed to fully restructure, but also because they face a substantially more difficult business environment than do EPZ firms. Unlike EPZ firms, they receive few tax incentives or duty exemptions, (although their inputs have generally lower import tax rates than their outputs). In addition, because the informal sector is de facto out of taxation�s reach, traditional import-substituting firms find themselves shouldering a disproportionate share of the economy�s fiscal burden, both direct and indirect. Moreover, they bear the brunt of government regulations and administrative procedures, many of which contribute significantly to the difficulties firms face in restructuring. For example, import duties and difficulties getting expatriate work permits make it harder to adopt new technologies.

Growth cannot come only from sectors where there is limited international competition such

as construction and transportation. In order for a developing country to fully integrate into the world market and grow out of poverty, conditions must be created that allow investors to successfully compete against imports or to export. The extraordinary success of EPZ firms in light manufacturing, agri-food, data processing and other labor or natural-resource intensive industries is testimony to this statement.

5

Export Processing Zones Madagascar has been actively promoting its exports since the early 1990s, focusing on the

development of Export Processing Zones (EPZs) in order to attract foreign direct investment. The World Trade Organization estimates that about 50 percent of companies licensed to operate within EPZs are concentrated in the apparel and textile industries, with the remainder focused on food processing, footwear, jewelry, and information technology, (Table 2 gives an illustration).

Table 2: EPZ Production Industrial Free Zone (Agglomeration of Tana and Antsirabe), 2000

DIVISION Production

in billions FMG (% of total)

Value Added in billions FMG (% of total)

Average Value Added in billions FMG

Textile manufacture 690.7(50.3) 122.6(32.4) 3 Manufacture of article of clothing, making and dyeing of fur

546.1(39.8) 213.3(56.3) 4.5

Manufacture of leather and shoes 11.2(0.8) 3.9(1) 0.8 Wood manufacture(except furniture) 15.2(1.1) 3.1(0.8) 0.6 Manufacture of precision medical instruments and optics and clocks

25.2(1.8) 10.8(0.6) 3.6

Furniture manufacturing 52.8(3.8) 12.7(3.6) 2.1

Others 32.4(2.4) 12.3(2.1) 1.8

Total 1373.6(100) 378.7(100) 3.3 Source: INSTAT

Investment in Malagasy EPZs comes primarily from six countries: France, Mauritius, India,

Hong Kong, China and Malaysia. In 1999, EPZs employed an estimated 50,000 people. That same year, it was estimated that there were 126 textile firms, 31 agro-processing firms, 26 data-processing firms, 21 wood firms and 15 handicrafts firms located in EPZs. In 1999, entrepreneurs invested about FMG 328 billion, (around $US 51 million) in textile firms, while investment in agro-processing amounted to FMG 58 billion (around $US 9 million). Wood-processing and data-processing firms invested FMG 39 billion and FMG 20 billion respectively.

Eligibility. Eligibility requirements for location within EPZs are based on the firm�s

activities. Firms are allowed into EPZs if they are exported-oriented manufacturers, develop or manage EPZs, provide services to EPZ companies, produce inputs used by EPZ firms, or export at least 95 percent of their output. Customs duties are levied on the 5 percent of production allowed to be sold domestically. Firms in EPZs pay a refundable VAT of 20 percent on imported inputs. The refund should be completed within one month, upon proof of exports, thereby preventing leakage of cheaper imported goods into the domestic market. Implementation of the VAT drawback scheme has been difficult and remains an area of ongoing concern.

6

Incentives. The Malagasy government offers several incentives to firms located in EPZs. These include a grace period on corporate tax for the first 2-15 years of operations; a post-grace period tax rate reduced by an amount based on 75 percent of non-initial investment, exemption from customs duties and taxes on imported equipment, inputs, spare parts, packaging, and building materials; taxation of dividends at only 10 percent rather than 25 percent; 99 year leases for investment in land; free repatriation of profits after payment of taxes and 100 percent foreign ownership.

Box 1. EPZ Provisions and Qualifying Requirements Incentives offered to qualifying firms: • Corporate tax holiday of 5 years • Duty free importation of capital equipment and machinery for EPZ operations. • Duty free importation of all raw materials and intermediate goods required in the production process and in

construction. • Exemption from withholding tax on dividends • Exemption from fringe benefits tax on EPZ employees • Exemption from withholding taxes on interest-earned, fees, remittances and royalties. • Exemption from branch profits tax for a branch of a foreign registered company operating in EPZs. • Sales taxes refund on goods of services purchased from customs territory.

Qualifying requirements: • New investment • Export at least 95% of annual sales • Create employment opportunities and undertake human resource development • Undertake value-addition activities • Provide adequate environmental safeguards • Strive to achieve significant technical know-how and technological transfer • Ministry of Industry approval

Textiles and Garments In the past several years, garment and textile firms have been flocking to Madagascar.

Encouraged by the effective implementation of the EPZ legislation, firms have taken advantage of some of the lowest labor costs in the world and preferential access to United States and European Union markets. Output by EPZ-registered firms has more than doubled between 1995 and 2000. The fastest growth has occurred in the garment and textile sector. Currently, the sector accounts for almost 90 percent of the value of EPZ production in Antananarivo and Antsirabe, where most EPZ firms are located. This trend was given an additional boost by Madagascar�s recent certification under the US government�s Africa Growth and Opportunities Act (AGOA) that allows firms to export garments to the US duty and quota free, without any restrictions on fabric origin. All of the firms we interviewed confirmed their plans to expand production for the US market and we encountered numerous buyers seeking production facilities in Madagascar for export to the US market.1

Mauritian companies, in particular, have led the expansion of the Malagasy garment

industry. Seeking relief from steadily rising wages rates at home, their strategy has been to move

1 The fact that few people speak English deters some US buyers, especially small ones. This issue is discussed in detail in the Cross-Cutting Issues section.

7

production of low-value mass produced garments such as jeans, shirts and chinos, to Madagascar. Meanwhile, operations in Mauritius are directed toward higher value, top-quality clothing. Also, much of the production for the US was moved to Madagascar in response to quota barriers imposed on Mauritius. Managers of these firms consistently reported that they selected Madagascar over other countries because of its proximity to Mauritius, the ability to use the French language and the high productivity of the workforce compared to other Sub-Saharan African countries. One major buyer illustrated part of this perception about productivity by stating that �Malagasy workers have an innate dexterity that is more Asian that African.� Nonetheless, managers also stated that despite these advantages, they would not have been interested in Madagascar without the effective implementation of EPZ provisions permitting them to import and export duty free and affording them a tax holiday.

Low-Cost Labor. Along with preferential market access, the Malagasy garment industry�s

main competitive advantage is low-cost labor. The average monthly salary of a machine operator is less than one-third of that in Mauritius and only about 60 percent of the average salary in India.2 Of course, low wages are only part of the story. If worker productivity is too low, as is often the case in Africa, it will offset the advantages of low labor costs. Firms we interviewed reported that productivity of an average machine operator ranges from only 50 to 80 percent of Chinese workers, (generally considered the most productive in the world). However, wage rates in Madagascar are low enough to compensate for lower productivity. Therefore, unit labor costs compare favorably with major competitor countries. Table 3 gives an index of unit labor costs for a representative company producing men�s shirts. Though task-level efficiency is low -- the average machine operator produces 14.2 shirts a day -- wages are also low, giving a unit labor index of 0.023. This suggests that it takes just over 2 cents of direct labor to earn one dollar in revenue, less than any other country in the table, except Ghana.3 In this particular firm, the manager believes he can become even more competitive. With additional experience, the productivity of an average machine operator should improve to around 16-17 shirts a day, a rate which some workers already achieve. Even at 14 shirts a day, this company is more efficient than firms surveyed in Mozambique in 1998, where managers reported the average at 8-10 shirts a day or in Nepal, where estimates in 1999 ranged from 12-14 shirts per day.

Table 3. Unit Labor Cost in Standardized Garment Production (Men's Casual Shirts)

Mada-gascar

Kenya

Ghana

Mozam-bique

Lesotho

South Africa

India

EPZ China

Task Level Efficiencya 14-15 12-15 12 10-11 18 15 16 18-22 Monthly Wageb $55-65 $60-65 $30-45 $40-50 $82-95 $255 $70-75 $150 Index of Unit Labor Costc 0.023 0.026 0.022 0.029 0.035 0.050 0.027 0.040

a The average number of shirts a machine operator can produce in a workday b Wage for a semi-skilled sewing machine operator in the garments industry

2 A recent survey in the industry puts the average wage at $0.37 an hour in Madagascar, $0.58 in India and $1.47 in Mauritius. Our interviews confirmed that these are generally accurate. 3 This measures direct labor used in production. Actual labor input is higher because of management, service staff, laborers and other indirect labor.

8

c Unit labor cost calculations are based on assumed 26-day work month and FOB prices of shirts in each factory, except for Madagascar, where a 21-day month is used.

lp

qwULC •=

Source: Interviews with African garment producers, 1996, 1998 and in Madagascar in 2001

Managers also reported that productivity is improving and given proper management and training, they expect that Malagasy workers can approach the productivity levels of workers in India and Mauritius, which are only slightly below those in China. Today, task-level efficiency is highly variable within the same factory. One jeans producer said that some days they can meet their goal of 20 standard minutes per pair of jeans but on other days the time can rise to 35 minutes. This is a relatively new company, however, and its management is confident that with more experience they will be able to consistently reach high task-level efficiency, something they felt unable to do in other African countries. In conclusion, while worker productivity in Madagascar is low by international standards, it is improving and low wages more than compensate for it.

Productivity Factors. Average productivity is lowered by high employee turnover and absenteeism. Firms in Madagascar report a wide range of worker turnover figures, ranging from a low of 8-10 percent to a high of over 17 percent. One reason for high turnover is that in the rapidly growing market, new firms have poached trained workers from existing ones. But, the wide dispersion of turnover rates suggest that some firms have not yet learned to effectively manage Malagasy workers who have not yet become accustomed to the rigid discipline required in factories. Several managers of older firms explained how they went through a period of high turnover when they first arrived, and that their firms had similar experiences during initial operations in Mauritius.

Absenteeism is more difficult to quantify. Most firms in Madagascar indicated that

absenteeism averaged around three to six percent. However, this does not include workers who report for work and then go to the clinic. Other studies have estimated absenteeism between 12.5 and 15 percent and stated that this is not an uncommon rate for a largely female work force.4 The absenteeism rate does appear to be significantly higher than in Mauritius.

Table 4. Absenteeism and Turnover Rates in Madagascar and Mauritius

Madagascar Mauritius Absenteeism as % of Employment 12-15 5-10 Worker Turnover as a % of Employment 15-17 5

Source: UNIDO 2001 and Integrated Framework Interviews 2001 Another important factor lowering average worker productivity is the fact that an unusually

high proportion of the workforce is not directly involved in production. Many employees are hired to perform duties such as moving bundles, rectify mistakes and generally helping production. For example, in the shirt factory discussed above only around 40 percent of the work force is directly involved in production. Such a use of labor could not be tolerated in a

4 UNIDO (2001): Sector Study of the Textile and Clothing Industry in Madagascar.

9

high or medium wage country, but for now it is acceptable in Madagascar. If labor becomes more expensive in the future, there is scope to reduce the use of labor in the production process.

Cost Structure. The share of labor in total costs is small. For most garments it accounts for

only about 15 percent of total FOB costs. Consequently, operating in a low-wage country confers only a limited cost advantage. The most important cost is fabric, which usually comprises around 65 percent of total costs. Today almost all fabric used in Madagascar comes from East Asia where exceptionally efficient production leads to the cheapest fabric in the world. Transportation costs for this fabric are relatively low; firms estimate that it adds less than 10 percent to the costs, still making it cheaper than fabric from any other location. For example, one firm reported that the landed price in Madagascar for 14 ounce Denim used in the production of blue jeans is $2.30 a square meter from Mauritius and $1.80 from Hong Kong. Similar fabric can be obtained in South Africa for $1.90, close to the price of East Asian fabric, but firms say that the lead time is longer and the quality less consistent. Thus, major buyers purchase huge quantities of fabric and ship them to their manufacturing facilities world wide, ensuring the quality and reliability of their supply.

Transportation costs from Madagascar to its major markets are substantially higher than

from East Asia and the shipping schedules are less regular. One firm reported that the average cost of shipping a 40-foot container from Madagascar to the East Coast of the US is around $3600 and takes about 30 days, compared to around $1200 and less than two weeks from Singapore to the US West Coast. Air freight, which many firms use for small shipments, is also very expensive. However, the transportation infrastructure is improving. Costs are falling and the frequency and reliability of shipping is increasing. Though it will never reach the efficiency of East Asia, it should certainly allow Madagascar�s textile and garment firms to be competitive.

Table 5 provides a cost analysis for a typical low-cost men�s casual shirt. The FOB price of

around $6.00 is close to the value found in previous studies. The majority of costs come from overhead, management fees and margin and the cost of fabric. The overhead and management fees are paid, for the most part, to the parent company and will probably not vary much regardless of the firm�s location. The fabric is imported from East Asia and transportation costs are so low that fabric from anywhere else will have similar costs. The location-specific costs are therefore, labor and shipping. As discussed above, labor in Madagascar is already exceedingly cheap. The company referred to in Table 5 estimates that the same shirt made in Mauritius would use $.70 in labor, adding almost four percent to the FOB price and increasing the cost of production by almost seven percent.

Table 5. Cost Analysis: Typical Casual Men’s Long-Sleeve Shirt Item Cost (US$) Fabric 2.26 Accessories/labels/packaging 0.36 Washing 0.14 Labor 0.47 Transport to port 0.10 Sub Total 3.33 Overhead, Mgt. Fee and Margin 2.67 Total 6.00

10

Source: Integrated Framework Interviews 2001 Future Potential and Impediments. Overall production costs for most garments are probably

higher in Madagascar than in other countries, especially those in East Asia. Labor costs are some of the lowest in the world, but worker productivity is also lower than in East Asia and labor makes up a small proportion of overall costs. The cost of imported fabric is slightly higher than in East Asia and transportation costs are substantially more. However, these cost disadvantages are more than offset by the preferential access into the US and EU markets.

Under current AGOA provisions, Madagascar can only maintain its duty-free access after

2004 if firms use locally-produced fabric, fabric from the US or fabric from other AGOA beneficiary countries. Currently, there is just one major producer of cotton cloth in Madagascar and it can supply only a tiny portion of the EPZ market. While productivity in its plant is low -- less than 25 percent of a similar plant in Mauritius-- its labor costs are so low that it is still competitive, even though it is a highly capital-intensive industry. Its major drawback appears to be its inability to consistently produce high-quality fabric. However, the company demonstrates the feasibility of establishing competitive spinning and weaving operations in Madagascar. The potentially large supply of cotton means it is conceivable that a fully-integrated textile and garment industry could eventually develop. Several private sector groups have studied the possibility but none have invested to date. There is also possibility of using fabric from South Africa, Mauritius and other AGOA beneficiaries. Though fabric from these countries costs more than that from East Asia, the lack of a US tariff may compensate for this.

The implications of local content requirements in 2004 is just one of the questions on the

minds of firm managers. Quotas under the Multi-Fiber Agreement are set to be eliminated in 2005, and as China enters the WTO it will have the same tariff barriers as other countries. Will garments from Madagascar be competitive enough to maintain an industry not firmly rooted in the country? In Madagascar, investment has been even more tentative than in other countries. There is little vertical integration and few firms have made major capital investments. Start-up garment production requires little investment relative to other industries. Most firms are leasing facilities, performing only the final assembly of low-cost items and not even investing in important labor-saving devices such as over-head conveyors. Thus, they can easily move if Madagascar loses its preferential access and is no longer competitive.

While there is no clear answer, most buyers for large clothing distributors interviewed for

this paper are relatively optimistic and believe that Madagascar is one of the few African countries that will be able to compete with China. They believe that wage rates in China will continue to increase, while wages in Madagascar will stabilize. Transportation costs and turnaround times will fall rapidly.5 Managers also expect that the productivity of Malagasy workers will continue to rise until it matches Asian levels.6 One large buyer argues that low wages will give the garment industry in Madagascar a life span of 20 years.

5 There is already evidence of this. Mast Company has used its buying power to have Maersk schedule a ship every week to make its last stop in Madagascar on its way to New York. This has dropped shipping times to the US East coast from around 45 days to 30 days. 6 Much of the confidence derives from the fact that people throughout the industry expect some type of preferential access to continue. Many believe that the AGOA exemption from local or US content requirements will be

11

But the survival of the Malagasy garment industry is not assured. It depends upon its ability

to reduce overhead, lower transportation costs and increase the advantage of cheap labor by improving productivity. This will require increased training, better infrastructure, and easing the burden of governmental administrative procedures and regulatory requirements.

Training. The lack of trained workers is a critical problem for the garments sector.

Currently most managers, quality control experts, supervisors and technicians are who must do most worker training in-house. There are few skilled garment or textile workers in Madagascar and the sole training institution, FORMACO, is ineffective. It is too small one firm said that it only has capacity for 60 workers every three weeks and it does not teach skills that are appropriate for the industry in Madagascar. The shortage of skilled workers will drive up costs and become increasingly problematic as the industry expands. It will also severely limit the industry�s ability to move up the value chain.

Infrastructure. Infrastructure is also a serious constraint that will only increase with growth.

In Antananarivo, few firms have standby generators but many indicate that they are planning to add them as power fluctuations are becoming more frequent and shortages are expected to increase. All enterprises outside of the capital are forced to have expensive generators. The poor infrastructure in outlying regions was often cited as the reason firms cluster around a few cities. In particular, the road network is congested and poorly laid out. It costs as much to ship a container from Antananarivo to the port at Tamatave as it does to send a container by sea to Mauritius, (which is about one quarter of the cost of shipping a container to the East coast of the US). Any disruption of the one road leading to the port will prevent exporting, making adherence to shipping schedules difficult.

Bureaucratic Burden. Firm managers stated that the EPZ legislation is relatively well

implemented. However, government bureaucracy is still a source of increased costs and there are indications that it is becoming more of a problem, not less. Customs clearance is the subject of most complaints. Interviews revealed that on average, it takes four to five days to clear an incoming or outgoing container and that this time has risen in the past few months. It is possible to clear a container in substantially less time but that requires large unofficial payments and the cost of these payments has also been increasing. Managers believe that there is an adversarial relationship between the customs inspectors and shippers and that customs officials seem uninterested in helping Malagasy industry become more competitive. Recent attempts to organize a stop to unofficial payments broke down. Managers say that customs officials have retaliated against the leaders of this effort by subjecting their firms to more inspections and delayed clearing. The Integrated Framework study contains a section that considers the customs regime in great detail, but it is important to note the impact that faster customs clearance can have. One major garments exporter estimated that reducing clearance times to one day, as is the case in some East Asian countries, would have the same effect as a three tofive percent cost savings.

extended or another preference granted but none of the managers we interviewed could articulate exactly how they thought this would happen.

12

The decision to force EPZ firms to pay VAT and then reclaim it has had a particularly negative impact upon the garments industry. Firms report that reimbursement takes two to three months and that the time is growing. For large firms this ties up hundreds of thousands of dollars in working capital and puts a strain on their cash management system. The VAT refund scheme was particularly problematic in Mahajanga. VAT receipts, collected by the local customs office must be refunded by the Treasury in Antananarivo. During these transactions, the money often becomes unaccounted for. Currently, firms tell us that over 17 billion MGF are owed to firms in Mahajanga. The requirement to pay VAT has encouraged most firms to engage in Cut Make and Trim (CMT) operations where they never take ownership of the fabric and accessories but merely cut and assemble parts provided by large buyers or their parent companies. Since value added and profits are less in CMT, this reduces the profits that are reported in Madagascar. The reliance on CMT may also discourage development of a domestic primary textile industry.

Firm interviews revealed that there are many other bureaucratic burdens but that most are

minor. Yet several firms said that these smaller problems are growing. They are beginning to worry about the deterioration of the business environment, just when they should be using the breathing space provided by the remaining trade preferences to become more competitive. For example, it has become much more time consuming to obtain expatriate work permits, sometimes taking up to six months or a year. So far, expatriates have not been stopped from working while they wait for approval but they feel insecure knowing that they are not in compliance with the law which is sending the wrong signal to investors. In addition, the establishment of provincial governments has led to worries about the creation of a new level of bureaucracy with its own demands for taxes, fees and regulatory barriers.

In conclusion, the garment industry has grown rapidly and appears set to continue, at least

for the next two or three years. It is unclear how competitive Madagascar will be once quotas are ended and local content rules become binding. The industry is not yet heavily invested and can move easily if other countries are more competitive. Most managers and buyers are optimistic that Madagascar will be able to remain competitive by increasing productivity and cutting costs. However, this depends upon reducing many constraints including the shortage of trained workers, the poor infrastructure, the heavy bureaucratic burden and the lack of local inputs. Until these issues are resolved, many firms appear to be waiting to make major, irreversible investments.

Information Technology Madagascar�s low wage rates and relatively productive, French-speaking workers suggest

that it has the ability to become an exporter of services to the Francophone world and beyond. This mostly untapped potential is well illustrated by the small, but growing information technology (IT) sector that has developed in recent years. Firms in this industry fall broadly into two categories. The first employs relatively skilled workers to design web sites and Internet applications. Many of these firms were started by local entrepreneurs and are small; most have less than 50 workers. Though there are no exact figures available, managers in the industry estimate that there are 10-15 small firms designing websites and applications for export markets,

13

and that these firms employ close to 200 people. The second group consists of firms performing data entry or providing Internet content for the export market. Most of these firms were started with foreign capital, have EPZ status and are relatively large, averaging around 100 workers. Currently there are 23 known EPZ data processing firms, employing between 3000 and 3500 workers. Though the IT industry is still small, it has grown rapidly. With the right policies, there is every expectation that this sector will continue to grow at a healthy rate.

On average, labor accounts for more than one third of costs for firms engaged in data entry.

Therefore, large foreign firms are attracted by Madagascar�s very low labor costs for literate, French-speaking workers. The majority of exports are directed to France, but some go to Belgium and other Francophone countries. The industry�s growth has been spurred by the rapid increase in demand for Internet content and the EU requirement for most administrative documents to be digitized.

In addition to the low labor costs compared to Europe and other countries (see Table 6),

firms cited the productivity of Malagasy workers as the reason they located in Madagascar. One company recently established in Antananarivo considered Tunisia, Morocco, and other Francophone African countries but selected Madagascar because of the quality of the work force. It is the general impression in the industry that Malagasy workers are disciplined and productive, but lack the creativity found in Europe. However, this is not a major consideration for firms doing data entry or producing Internet content.

Table 6. Average Wage for IT Employees Madagascar France India

Data Entry Clerk $39-$160 $890-$1100 $30-$180 Programmer/Software Engineer $200-$555 $1500-$4800 $250-$500 Graphic Designer $66-$266 $1200-$3500 $110-$180 Source: Integrated Framework Interviews 2001

Low labor costs are also the foundation of the small firms designing web sites and writing

applications. Many of these firms were founded by local entrepreneurs who studied or worked abroad and often rely, at least partly, on foreign sources for funding. But because these firms are basically Malagasy, finance is restricted and they remain small. A small portion of output from this type of firm is directed toward the local market, but the vast majority of the services are sold to France and Belgium. Managers indicated that at times the Malagasy designers have difficulty understanding the needs of European clients because of cultural differences, but this is becoming less of a problem as they gain experience. Overall, the European clients were satisfied with the performance of Malagasy designers. As the Malagasy designers become more adept, they have been able to move up and create more complicated, and thus higher value, applications.

Growth in the IT sector has been encouraging, indicating Madagascar�s ability to export

services. Whether the industry will continue to prosper and fulfill its promise depends critically on resolving problems in three major areas: extraordinarily high cost of connection due to the lack of bandwidth, shortage of skilled designers and engineers and impediments to operation created by government bureaucracy.

14

Bandwidth. The most severe problem is the lack of bandwidth. Because Madagascar lacks fiber optic connections, all Internet links are via satellite through a few suppliers. Consequently, connectivity is many times more expensive than in Europe, India or other competing countries. High communications costs force firms to make large shipments of data via courier. Since flights are limited and air freight expensive, this creates long turnaround times, eliminating the opportunity to compete for time-sensitive operations. The high cost of connectivity also keeps the demand for Internet services low, reducing the size of the domestic market. Finding accurate information on the demand for telecommunications services is almost impossible. One manager opined that telecommunications firms greatly underestimate their sales in order to avoid the five percent tax. But interviews with enterprises in all sectors of the economy made it clear that the extremely high cost of service and connectivity prevents Madagascar from taking full advantage of the global market.

Today, almost all Malagasy Internet sites are hosted on servers in France or the US so that

foreign clients can more easily access them. This makes it prohibitively expensive for most firms to maintain complex web sites with the capacity for customer interaction, such as online shopping or reservation sites. One IT manager estimates that a complex site maintained in France for a Malagasy firm could cost almost $400 a month compared to only $65-$70 for a firm in France. This high cost prevents many firms from using web sites to reach their customers and limits the growth of the market for web designers.

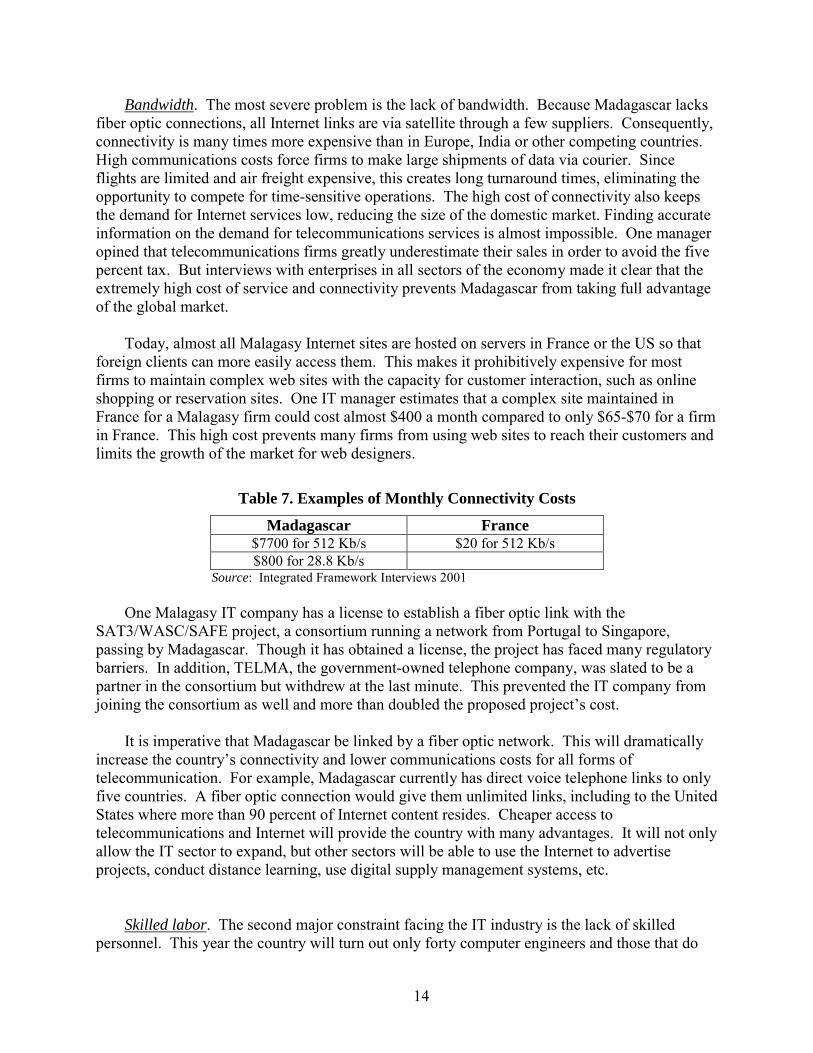

Table 7. Examples of Monthly Connectivity Costs

Madagascar France $7700 for 512 Kb/s $20 for 512 Kb/s $800 for 28.8 Kb/s

Source: Integrated Framework Interviews 2001 One Malagasy IT company has a license to establish a fiber optic link with the

SAT3/WASC/SAFE project, a consortium running a network from Portugal to Singapore, passing by Madagascar. Though it has obtained a license, the project has faced many regulatory barriers. In addition, TELMA, the government-owned telephone company, was slated to be a partner in the consortium but withdrew at the last minute. This prevented the IT company from joining the consortium as well and more than doubled the proposed project�s cost.

It is imperative that Madagascar be linked by a fiber optic network. This will dramatically

increase the country�s connectivity and lower communications costs for all forms of telecommunication. For example, Madagascar currently has direct voice telephone links to only five countries. A fiber optic connection would give them unlimited links, including to the United States where more than 90 percent of Internet content resides. Cheaper access to telecommunications and Internet will provide the country with many advantages. It will not only allow the IT sector to expand, but other sectors will be able to use the Internet to advertise projects, conduct distance learning, use digital supply management systems, etc.

Skilled labor. The second major constraint facing the IT industry is the lack of skilled

personnel. This year the country will turn out only forty computer engineers and those that do

15

not go abroad will quickly be taken up by local companies. One company reports that salaries for application designers have already more than doubled this year and that if this continues, his company will go out of business. Monthly wages for software developers are now almost equivalent to India. Today a developer with average experience in Madagascar is paid more than a beginner in India $300 as compared to $200. Experienced developers can earn almost $600 a month. If this continues, soon Madagascar�s advantage in labor cost will disappear. In addition to a shortage of highly skilled engineers and designers, the industry also faces a shortage of literate data entry personnel, especially those who can blind-type.

Table 8. Changes in Monthly Wages for New Entrant Software Developers in Madagascar

Year Monthly Wage 1997 $75-$112 1998 $112-$180 1999 $180-$224 2000 $224-$277 2001 $277-$298

Source: Estimated by GOTICOM Members There are several factors leading to a shortage of workers with the necessary skills for the IT

sector. There are few good training institutions in Madagascar and those that do exist suffer from a number of problems. Computer hardware is subject to import taxes of around 30 percent with no exemption for schools and training institutions. These taxes make computer equipment even more expensive for people to afford on their own. The high taxes have led to the growth of an informal sector providing both hardware and training. But the training is of very low quality. Many of the best instructors from the formal training institutions have left teaching for the private sector. On a positive note, GOTICOM, the industry association, hopes to set up training programs for graphic designers, computer engineers, and other IT workers. A further consideration is the lack of English-speaking workers. Most of the IT business in the world is in Anglophone countries and to be able to fully expand and take advantage of the world market, it is necessary to speak English.

Bureaucracy. In addition to the lack of connectivity and skilled workers, government

bureaucracy is the other major impediment to the IT industry�s expansion. Firms report that it is a constant battle to obtain basic services from government offices and that many officials do not seem interested in helping firms solve problems or overcome the difficult business environment. For example, companies report that it is extremely difficult to obtain work permits for expatriates. One French investor has been waiting over six months to obtain a permit even though he has already invested over $300,000 in a company. In addition, after almost six months the government still owes him a VAT refund of close to $60,000. This is a large burden on the cash flow of a new start-up company. The lack of bandwidth prevents firms from making timely delivery of data. Instead of facilitating delivery by courier to help overcome this obstacle, customs officials make it difficult and time-consuming to clear computer equipment and data. One small local firm employing 35 workers was denied the ability to get EPZ status, even though it exports most of its services. They were told they did not employ enough workers to qualify as an EPZ. Other firms have been told by customs that software and web development firms do not

16

qualify for EPZ status, though as we understand it, this is a misinterpretation of the law. This is not an exhaustive list of government barriers but amply illustrates that although the government has not stopped the industry from developing, it has done little to support growth.

The relative success of the IT sector points the way for many potential service exporters

such as accounting data entry, tele-translation services and call centers. It relies on the very low cost of productive labor, which is Madagascar�s proven comparative advantage. At the same time, the IT industry provides many opportunities to move up the value chain as the country develops. It also offers a valuable source of employment for Madagascar. The large data entry firms provide many high-paying jobs, a large percentage of which (up to 75 percent in some companies) go to women. The smaller applications firms provide needed employment for skilled workers, supplying a return for education and providing opportunities that help keep badly needed skilled workers from emigrating. However, the future of the industry depends upon the ability to overcome the critical obstacles described above.

Handicrafts Madagascar has developed a strong and growing handicrafts industry based upon

inexpensive labor and the country�s rich cultural heritage. It is only partially correct to categorize the handicrafts sector as an �EPZ sector.� Not all handicraft firms have EPZ status and information on firms operating under Common Law status or in the informal sector is largely absent. While larger handicrafts firms are generally located in EPZs, most of the numerous small firms are not.

There are no authoritative figures on the importance of handicrafts in the overall economy.

However, by 1999 well over 2,000 workers were directly employed in handicraft firms operating within EPZs. Still, this is only a fraction of total employment in this sector. Many thousands of workers in the informal sector support the industry by providing raw material and doing piecework at home. The handicrafts sector is highly labor intensive and is capable of providing a vast number of jobs for rural communities, women and other groups often bypassed by the growth of the exporting sector. It is clear that, given the appropriate policy environment, handicrafts production for export, the tourist market, and even the local market can make a significant contribution to poverty alleviation.

In order to investigate the handicrafts industry, we focused most (though not all) of our

interviews on two types of firms exporters of raffia items and producers of hand embroidery.7 While Madagascar also exports hand-made silk, wood carvings, jewelry and other handicrafts items, the raffia and embroidery firms examined here are among the largest handicraft firms and provide a good illustration of the sector�s challenges. The market for raffia products began to take off when rabanne (fabric made from woven raffia) became popular in France several years ago. Since then, the trend has continued to grow and spread to other parts of Europe and does not appear to be slowing down. Also, Madagascar has a long tradition of hand embroidery, thanks to the training provided to generations of Malagasy women by religious orders. These Malagasy workers have thus gained a reputation of having a high level of dexterity. As wage 7 Raffia is the fiber of leaves taken from the raffia palm, a tree native to Madagascar. Raffia is used in the production of ties and various woven items (mats, baskets, hats, etc.).

17

rates continue to rise around the world, there are fewer and fewer places where high-quality hand embroidery can be profitably produced.

18

Table 9. Scale and Competitiveness of African Handicrafts Exporters

Leading Exporters Average Sales (US$) Output per Worker (US$) Madagascar 244,250 1,376 Ghana 150,714 1,494 Kenya 194,806 1,249 Burkina Faso 184,425 N/A Philippines 700,000 5,000

Source: Tyler Associates and firm interviews in Madagascar

Scale of Companies. Most if the handicrafts enterprises that were interviewed are small, ranging from between $100,000 to $300,000 in annual sales with less than 100 permanent and temporary workers. One firm had over $500,000 in turnover, demonstrating the potential for well-managed firms with adequate resources. The firms we spoke with are already larger than those studied recently in Ghana, but they do not yet approach the scale of firms in the Philippines. However, they have been growing rapidly so it is conceivable that the best handicrafts firms in Madagascar could one day approach the average size of those in the Philippines. Some handicrafts experts believe that firms in Africa usually hit a sales limit of around US$200,000 compared to those in the Philippines, where the upper bound is about US$750,000.

Various impediments to growth are examined in greater detail below, however, firms stated

that growth appears to be limited in part by the fact that the enterprises are typically run by one family that is sometimes hesitant to employ outside managers. Labor productivity is also a likely factor limiting the growth of firms. In Filipino handicraft firms, productivity is up to four times that of Sub-Saharan African firms (including Madagascar) leading to higher sales revenues. This is true even though Filipino firms operate under many of the same constraints as African firms. However, some Malagasy firms believe that firms in the sector can continue to expand and still maintain control if they rely on a �putting-out� system.

Labor and Training. The amount of time workers devote to their jobs is difficult to

calculate for the handicrafts sector. The bulk of workers are temporary and paid a certain amount per piece produced. Some of them work at home under a putting-out system. While some firms estimate that their employees work almost full time, others suggest that they work half that. In addition, because the European demand for raffia is seasonal, most temporary employees in this industry do not work during the months of May through August. The ratio of permanent to temporary workers varies widely by firm and by type of industry. Every firm, however, has a permanent core of their most skilled workers. In contrast, most of the large exporting firms run factories in order to maintain quality and only contract out work to make up shortfalls in production.

Since most handicraft firms pay per piece, determining average monthly wages is difficult.

However, wages in the handicraft sector appear to be lower than wages in other types of large EPZ firms. Firms estimate that an employee working the equivalent of full time earns between $26 and $35 a month depending on his productivity and skill level. In contrast, the larger garment-producing firms we interviewed estimated their average monthly wages to be around

19

$54. The very best full-time workers can earn up to $60 dollars a month - to keep them from leaving for jobs in the large EPZ firms - and supervisors can earn up to $90 a month. Wages have been rising in the handicrafts industry because of competition for labor coming from the large garment firms. Some firms have increased their wages by as much as 20 percent in the last year, but most say that their increases were around 10 percent, only slightly ahead of inflation.

The handicrafts industry has the potential to substantially impact poverty. Women dominate

employment in most handicrafts firms; many work at home. Jobs in this industry can provide women with an opportunity to earn a good income while still caring for their families. Many of the jobs in this sector are also created in rural areas producing raffia, rabanne, silk and other raw materials.

While generally the tasks associated with handicrafts require a relatively low level of skills,

some tasks require exceptional ability. For example, the best employees in the hand-embroidery industry must carefully create high-quality embroidered children�s clothes, tablecloths and other items. Such delicate work requires years of experience and practice. Experienced seamstresses in embroidery enterprises regularly conduct on-the-job training for new employees. In other handicraft enterprises as well, almost all training takes place inside the firm. Raffia dealers intensively train workers during slow months and jewelry firms bring in trainers from Europe.

Perhaps in-house training is used because there are few institutions that train workers for the

handicrafts sector. SYMA is one such institution and firms reported that it was, in fact, quite good for teaching embroidery. However, it is too expensive for most firms to send many workers and the institute has limited capacity in any event. An equivalent institution exists for sewing rabanne (fabric made from raffia) called EMSF (Espace Métier Solidarité Firaisankina) but it is not considered useful, as it does not teach skills appropriate to the way the enterprises operate. While firms are currently able to train their own workers, many expressed worries that they would not be able to keep pace with growth and mentioned the need for improved training facilities. The lack of training facilities appears to be a more significant problem for embroidery firms than for other manufacturers in the handicrafts sector because they require employees to have relatively higher skills.

Impediments to Growth. Most of the firms we interviewed are optimistic. Among raffia

producers, expected sales growth over the next three years ranges from 50 to 400 percent. Embroidery firms expect lower growth than that, averaging around 100 percent over the next three years. However, several impediments to growth undoubtedly need to be addressed before these optimistic predictions can become reality.

Market Information: Foremost among major impediments to growth for all handicrafts firms is the need for more information on potential buyers. Most handicrafts are exported to France or Belgium and only a small fraction is directed to the US or Japan. Entrepreneurs believe that there is a large market for their products outside of Europe but they have no contact with prospective buyers and little knowledge of marketing. Few non-Europeans ever visit the country, either for business or tourism. All handicraft firms we questioned repeatedly requested help marketing their products. Expensive telephone and Internet services rates are particularly burdensome. One fast-growing raffia firm reported that in its first year of operations, its

20

telecommunications costs were about 5 percent of turnover, an exceptionally large burden for a start-up company. Costly Internet and telephone service, lack of English proficiency, as well as high transport costs, all conspire to make it difficult to reach non-European markets.

Finance: To take advantage of the US market, handicrafts firms must be able to

consistently meet deadlines for large orders while maintaining high quality. Most firms believe that access to raw materials is not a problem in this regard, but access to finance is particularly worrisome. None of the handicraft firms with whom we spoke were ever able to access bank finance in Madagascar. One firm, unable to borrow money from local banks, successfully obtained a loan in France. Another company was refused a loan of working capital by local banks, even though it was secured by a letter of credit from a large, reputable French buyer. The usual explanation provided by banks for the strictness in loan provision is that the risk of non-shipment is too great. Many of the companies, however, claim to never have missed a shipment. They believe that commercial banks exclude handicrafts firms as a rule. Currently, some producers are operating with advance payments from European buyers. But Japanese and US customers are loath to do this. Firms therefore point to the lack of working capital, along with poor market contacts, as the main constraints hindering expansion into the North American and Japanese markets.

When the handicrafts sector took off in Ghana, firms reported similar problems with

working capital. The Ghana Export Promotion Council and Aid to Artisans assisted firms by providing assurances to lenders. In addition, donor agencies provided funds that were mixed with bank funds in order to help provide working capital. Now Ghanaian firms report no problems obtaining finance, although they do complain of high interest rates.8 Ghana has also successfully introduced export insurance, further assuring lenders. Producers in Madagascar have also mentioned the need for export insurance. Ghana appears to provide a useful model for how trade finance might be made more accessible in Madagascar.

Raw Material Supplies: The supply of raw materials is not a major concern of Malagasy

handicraft enterprises. Most raffia and rabanne fabric is delivered to producers in Antananarivo from the Mahajanga area and from specific villages in the highlands including Ambohimiadana and Fandriana where the raw material is initially gathered and processed. Even during the rainy season when roads are difficult to negotiate, producers can usually get the required supplies. However, during the season when farmers are fully engaged in planting rice, rabanne prices can rise by almost 50 percent. Prices can also increase due to the large amounts of raffia being exported to East Asia and the smaller amounts going to Europe, where it is used in the agricultural sector as well as in handicrafts. Because raffia is a renewable resource some concerns have been raised that if harvesting is not properly managed, shortages could result. However, none of the raffia producers interviewed considered the supply threatened nor had they experienced shortages. Regardless, last year increased demand drove the price of raffia up 30 percent.

Embroidery companies import much of their fabric. However, those that rely on Cotona, the

main local producer of cotton fabric, are worried that it may not be able to fill their orders, thus 8 The World Bank (2001): Ghana: International Competitiveness Opportunities and Challenges Facing Non-Traditional Exports (Report No. 22421-GH).

21

forcing them to use more expensive imported cloth. Other handicrafts firms, such as silk producers and jewelry companies, did not feel that materials were an issue.

Transport: The majority of firms sell on FOB (freight-on-board) terms, thus transportation

costs are the customer�s responsibility. With shipping costs so high, these terms undoubtedly affect firm competitiveness. The cost of air freight is especially high, putting handicrafts firms at a disadvantage. Embroidery, jewelry, and other items are often shipped by air but raffia is too bulky for this to be cost effective. This is less of a problem when firms have time to plan bulk seasonal shipments. However, the cost of quickly filling small raffia orders by air is particularly prohibitive. Transportation is a significant hindrance to market expansion. Firms are currently unable to make regular on-time shipments due to the high cost of air freight, the infrequent maritime shipping departures and long transit times between ports.

Government Bureaucracy: Many handicraft firms operate with little government scrutiny

due to their small size. Firm complaints generally do not include tax collection nor labor regulations. Handicraft companies do make the standard criticisms about customs however, but since these companies make few shipments which are usually not time sensitive, customs is not cited as a major impediment. Firms also find the requirement to repatriate foreign exchange within three months to be a burden. This forces them to incur the enormously high costs associated with transferring foreign exchange. Some banks charge as much as 2-3 percent to deposit foreign currency. Moreover, if a shipment is not accepted, in order to account for the foreign exchange, the company must pay to have the cargo shipped back to Madagascar. This is, of course, in addition to bearing the loss of the sale and the original charges for shipping the cargo to the purchaser.

Most of the small firms do not locate within EPZs because it can be a complicated process

involving a considerable amount of official procedures and red tape. In fact, one EPZ embroidery firm established a non-EPZ sister company to avoid the regulations and facilitate selling domestically, even though the sister company still exports almost 60 percent of its output. The advantages of EPZ status are limited for most handicrafts firms. They import little and make most purchases in cash, avoiding VAT draw-back procedures. Even tax holidays are of little use since most firms pay a minimum of taxes in any event. As firms grow, they must decide not only whether to establish formal factories, but also whether to apply for EPZ status.

Recommendations. The handicrafts industry has enormous potential for creating jobs and

growth. This growth depends on maintaining Madagascar�s main competitive advantage - exceptionally low wages relative to production. Firms in this industry demand relatively little capital and put less stress on infrastructure than other exporters like large garments firms. The handicrafts industry also has backward and forward linkages with other sectors, such as agriculture and tourism. Employment creation in this sector is thus not confined to a certain geographic area.

To assure continued growth, efforts must be made to provide training, better access to

finance, and most importantly information on new markets. One way that this could be done is by fostering links between large buyers and individual firms. In the garments industry, close cooperation between buyers and producers has been instrumental to growth. The garment buyers

22

use their market power to purchase low-cost inputs, keep shipping costs down and help new firms develop. For example, one firm reported that The Gap company allowed it to produce the same style of garment for two years, until its workers had gained enough experience to be competitive. An added advantage is that the large garment buyers enforce minimum labor standards, in keeping with their company strategy. In the handicrafts sector, similar arrangements might be possible. Large new buyers could provide needed finance, technical expertise and assistance with design. In return, the buyers would be able to secure a supply of high quality handicrafts, not easily available elsewhere.

A few companies producing high-quality embroidery and other such items have been able to

obtain contracts with high-end buyers, including world renowned department stores. However, they have been unable to sustain these relationships due to lack of finance. Capital is needed to improve their production facilities and bring them into compliance with buyers� labor standards. These small enterprises also struggle to find funds for inputs and to train enough labor to consistently make large shipments of the required quality. While buyers may be willing to purchase large orders, they appear less willing to invest in capacity building. Well-planned interventions on the part of the donors may help to develop relationships with buyers and consequently expand the capabilities of the handicrafts sector.

The Common Law Sector Malagasy industry, which accounts for slightly more than 12 percent of GDP, has grown

moderately in the second half of the 1990s. Between 1994 and 1999, growth in the industrial sector averaged about 4 percent, just keeping ahead of the average annual population growth of 3 percent. Much of this growth can be attributed to the EPZ sector, which grew at 19 percent a year between 1995 and 1999. If the growth of industries with EPZ status is excluded, it is then obvious that the growth of Common Law (CL) industries was quite weak.

Imports, by contrast, have grown vigorously. Imports grew 15.7 percent a year in volume

between 1995 and 1999 and have maintained that rate between 1999 and 2000.9 Expressed in SDR (Special Drawing Rights), import growth averaged 7 percent annually in the second half of the 1990s, (IMF, 2000). This lower rate reflects the reduction in the price of some imported goods expressed in SDRs due to the dollar�s appreciation.

The fact that imports have grown substantially suggests that the weak growth of Malagasy

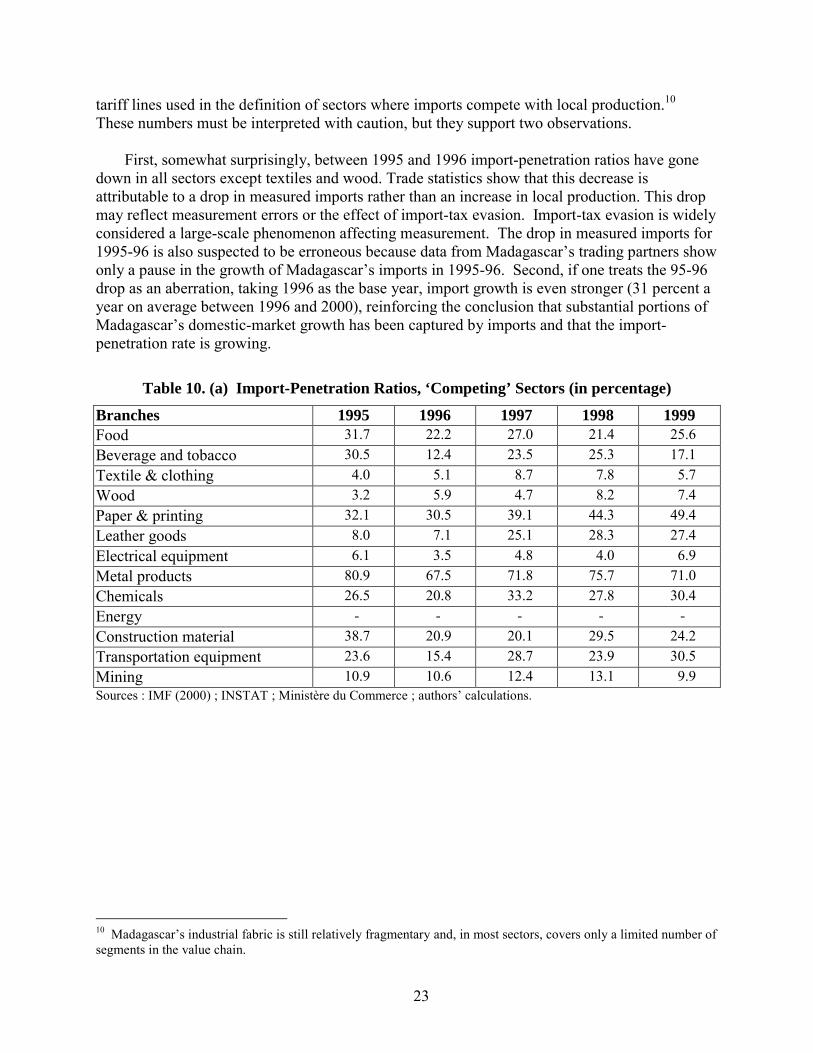

industrial production outside of the EPZ may be due more to import competition than to domestic-market stagnation. This hypothesis is confirmed by observing the evolution of import-penetration ratios in sectors where imports compete with domestic production. Table 5.10 (a) shows the evolution of import-penetration ratios in those sectors and Table 5.10 (b) gives the

9 The aggregate volume growth is approximated by multiplying volume growth at the tariff-line level by the weight of each tariff line in total import value for the terminal year.

23

tariff lines used in the definition of sectors where imports compete with local production.10 These numbers must be interpreted with caution, but they support two observations.

First, somewhat surprisingly, between 1995 and 1996 import-penetration ratios have gone

down in all sectors except textiles and wood. Trade statistics show that this decrease is attributable to a drop in measured imports rather than an increase in local production. This drop may reflect measurement errors or the effect of import-tax evasion. Import-tax evasion is widely considered a large-scale phenomenon affecting measurement. The drop in measured imports for 1995-96 is also suspected to be erroneous because data from Madagascar�s trading partners show only a pause in the growth of Madagascar�s imports in 1995-96. Second, if one treats the 95-96 drop as an aberration, taking 1996 as the base year, import growth is even stronger (31 percent a year on average between 1996 and 2000), reinforcing the conclusion that substantial portions of Madagascar�s domestic-market growth has been captured by imports and that the import-penetration rate is growing.

Table 10. (a) Import-Penetration Ratios, ‘Competing’ Sectors (in percentage)

Branches 1995 1996 1997 1998 1999 Food 31.7 22.2 27.0 21.4 25.6 Beverage and tobacco 30.5 12.4 23.5 25.3 17.1 Textile & clothing 4.0 5.1 8.7 7.8 5.7 Wood 3.2 5.9 4.7 8.2 7.4 Paper & printing 32.1 30.5 39.1 44.3 49.4 Leather goods 8.0 7.1 25.1 28.3 27.4 Electrical equipment 6.1 3.5 4.8 4.0 6.9 Metal products 80.9 67.5 71.8 75.7 71.0 Chemicals 26.5 20.8 33.2 27.8 30.4 Energy - - - - - Construction material 38.7 20.9 20.1 29.5 24.2 Transportation equipment 23.6 15.4 28.7 23.9 30.5 Mining 10.9 10.6 12.4 13.1 9.9 Sources : IMF (2000) ; INSTAT ; Ministère du Commerce ; authors� calculations.

10 Madagascar�s industrial fabric is still relatively fragmentary and, in most sectors, covers only a limited number of segments in the value chain.

24

Table 10. (b) Tariff Lines, ‘Competing’ Sectors Branches HS2 categories Food 101, 102,103,199,201,202,203,204, 205,206, 299,301,

302,299,401,402,405,406,407 Beverage and tobacco 408;411;412;499;501;502;599 Textile & clothing 1201-1206;1301,1302,1304,1305 Wood 1001;1099 Paper & printing 1101-1199 Leather goods 999;1401;1499 Electrical equipment 2301; Metal products 2101;2199 Chemicals 701;702;705 Energy Construction material 601; Transportation equipment 2404; Mining 699;

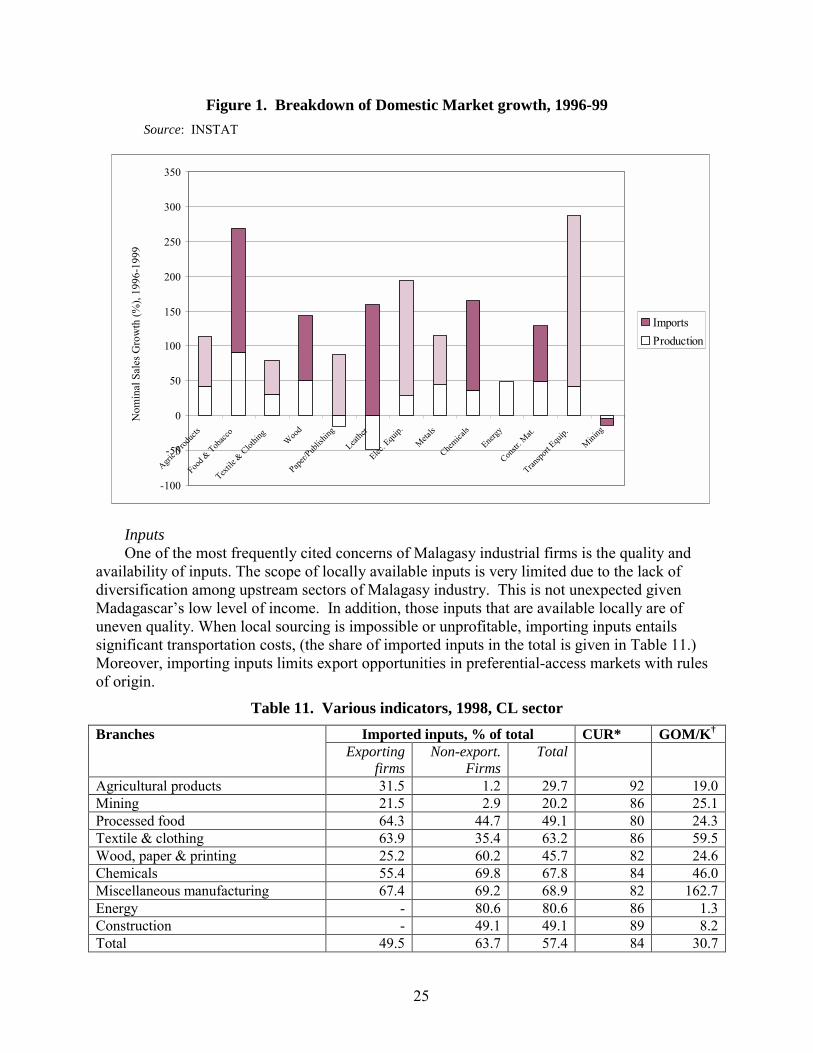

Figure 1. shows the split of nominal domestic-market growth between domestic production

and imports revealing that much of the growth was captured by imports. For the paper/printing and leather industries, domestic output fell (by 15 percent and 47 percent respectively) whereas imports increased strongly (by 88 percent and 159 percent, respectively). In agri-food, beverages, and textiles, three important sectors in Malagasy industry, less than 40 percent of the market�s growth was captured by domestic production; the rest was attributed to imports.11 This is all the more noteworthy since in 1996, imports represented only 22 percent of consumption in agri-food products, 12 percent in beverages and 5 percent in textiles.

These preliminary observations portray a growing gap between two segments of the

Malagasy economy poised on different trajectories. On one hand, the dynamic export sector centered around the EPZ is expanding rapidly. On the other hand, the domestic sector is struggling to compete with imports and gradually loosing steam. Given that the latter still accounts for more than 10 percent of GDP (five times more than the EPZ sector) and provides between 150,000 and 200,000 jobs,12 its difficulties should not be taken lightly. We now turn to an analysis of the obstacles to growth in the domestic sector, or non-EPZ, Common Law firms.

11 The agri-food and beverage industries, taken together, account for about half of industrial production. 12 Employment in individual companies and in corporations outside of the textile/garment sector was, in 1997, 146,000 employees (Madio 1999, Table 3). Employment in the textile/garment sector, of which a large part is in the EPZ, was 47,000 people. Most of the employment gains since 1997 have been recorded in the EPZ sector.

25

Figure 1. Breakdown of Domestic Market growth, 1996-99 Source: INSTAT

Inputs One of the most frequently cited concerns of Malagasy industrial firms is the quality and

availability of inputs. The scope of locally available inputs is very limited due to the lack of diversification among upstream sectors of Malagasy industry. This is not unexpected given Madagascar�s low level of income. In addition, those inputs that are available locally are of uneven quality. When local sourcing is impossible or unprofitable, importing inputs entails significant transportation costs, (the share of imported inputs in the total is given in Table 11.) Moreover, importing inputs limits export opportunities in preferential-access markets with rules of origin.

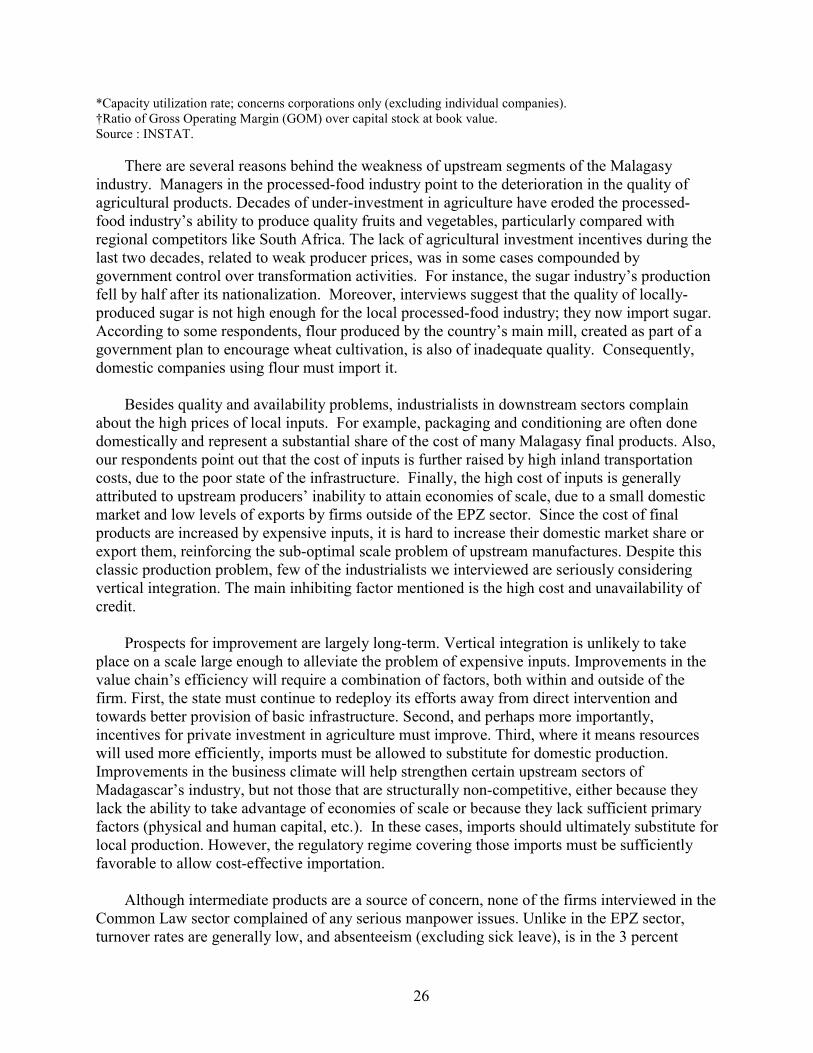

Table 11. Various indicators, 1998, CL sector Imported inputs, % of total CUR* GOM/K† Branches

Exporting firms

Non-export. Firms

Total