Embed Size (px)

Citation preview

STUDY ON PRIVATE-INITIATIVE INFRASTRUCTURE PROJECTS

IN DEVELOPING COUNTRIES IN FY2011

STUDY ON THE NEW CEBU CONTAINER PORT AND THE

REDEVELOPMENT OF THE EXISTING CEBU PORT

IN THE REPUBLIC OF THE PHILIPPINES

FINAL REPORT

February 2012

Prepared for:

The Ministry of Economy, Trade and Industry

Prepared by:

Oriental Consultants Co., Ltd.

Ides Co., Ltd.

PREFACE

This report shows the results of the “Study on Private-Initiative Infrastructure Projects in Developing Countries in

FY2011” contract awarded by The Ministry of Economy, Trade and Industry to Oriental Consultants Co., Ltd and

Ides Co., Ltd.

This study, “Study on the New Cebu Container Port and the Redevelopment of the Existing Cebu Port in the

Republic of the Philippines” deals with the issue of a new container terminal development project to cope with the

problems caused by the congestion of the existing Cebu port and the shallow water depth of the Cebu international

container berths. The feasibility to realize the project for construction of the New Cebu Container Port and for

Redevelopment of the Existing Cebu Port are studied to ensure the success of this Project. The total cost of the

project is estimated as Japanese Yen 17.8 billion (equivalent 9.9 billion pesos) including VAT.

We, all members of the Study Team, hope this study will contribute to putting the plan into practice, and will be

gratified if the result helps the relevant government officials understand and drive the Project forward.

February 2012

Oriental Consultants Co., Ltd.

Ides Co., Ltd.

Project Site Map (1)

Manila

Key Plan of Philippines

Cebu Base Port Mactan Island

Location Map

Cebu Island

0 25 50 km

(Source: Study Team)

Project Site Map (2)

Proposed Site of New Port

(Consolacion)

Mactan North Mactan South

Cebu South

Minglanilla

Cebu Baseport

(Source: Study Team)

0 5km 10km

List of Abbreviations Abbreviation Description

AASHTO American Association of State Highway and Transportation Officials

ADB Asian Development Bank

AO Presidential Administration Order

APL American President Lines

ARMM Autonomous Region in Muslim Mindanao

ATI Asian Terminal Incorporation

BLT Build Lease Transfer

BOD Biochemical Oxygen Demand

BOO Build Own Operate

BOT Build Operate Transfer

BTO Build Transfer Operate

BT Build Transfer

CAR Cordillera Administrative

CENRO Community Environment and Natural Resource Office

CFS Container Freight Station

CIA Cebu Integrated Arrastre

CIP Cebu International Port

COD Chemical Oxygen Demand

CPA Cebu Port Authority

CY Container Yard

dB Decibel

DAO Department Administration Order

DENR Department of Environmental and Natural Resources

DMC Department Memorandum Circular

DO Dissolved Oxygen

DOTC Department of Transportation and Communications

DPI Dubai Port International

DPWH Department of Public Works and Highways

DWT Dead Weight Tonnage

ECA Environmentally Critical Area

ECC Environmental Compliance Certificate

EIA Environmental Impact Assessment

EIRR Economic Internal Rate of Return

EIS Environmental Impact Statement

EMB Environmental Management Bureau

EN Exchange of Note

EO Presidential Executive Order

EPRMP Environmental Performance Report and Management Plan

ERIA Economic Research Institute for Asean and East Asia

FIRR Financial Internal Rate of Return

FS Feasibility Study

GDP Gross Domestic Products

GRDP Gross Regional Domestic Products

GRT Gross Registered Tonnage

GWEN Good Roads and Bridges, Water and Electrification Now Program

GWT Gross Weight Ton

HSH High Standard Highway

ICC Investment Coordination Committee

ICTSI International Container Terminal Service Incorporation

IMF International Monetary Fund

IRR Internal Rate of Return

JBIC Japan Bank for International Corporation

JETRO Japan External Trade Organization

JICA Japan International Cooperation Agency

JICA Study The Study on the Cebu Integrated Port Development Plan

LA Loan Agreement

LOA Length of Overall

MC EMB Memorandum Circular

METI Ministry of Economy, Trade and Industry

MICT Manila International Container Terminal

MO Management Office

MO Memorandum Order

MOF Ministry of Finance

MOFA Ministry of Foreign Affairs

MPN Most Probable Number

NCR National Capital Region

NEDA National Economic and Development Authority

NEPC National Environmental Protection Council

NEPC National Environmental Protection Council (Now DENR)

NGO Non-Governmental Organization

NPPD National Plan for Port Development

NPV Net Present Value

ODA Official Development Assistance

OECD Organization for Economic Cooperation and Development

OPASCOR Oriental Port & Allied Services Corporation

Panamax Panama Maximum size

PDP Philippine Development Plan

PD Presidential Decree

PDPFD Provincial Development and Physical Framework Plan

PEISS Philippine Environmental Impact Statement System

PENRO Provincial Environment and Natural Resource Office

PEZA Philippine Economic Zone Authority

PMO Project Management Office

PMO Port Management Office

Post-Panamax Post-Panama Maximum size

PPA Philippine Ports Authority

PPOSS Philippine Port System Strategy

PPP Public Private Partnership

PSA PSA international

PSP Private Sector Participation

QC Quay Gantry Crane

RA Regional Act

RGDP Regional Gross Domestic Products

RORO Roll On / Roll Off

ROO Rehabilitate Own Operate

ROT Rehabilitate Operate Transfer

RRTS Road Ro-Ro Terminal System

RTG Rubber Tire Mounted Gantry Crane

SCMB Subic, Clark, Manila and Batangas Corridor

SER Shadow Exchange Rate

SPS Salala Port Service

STEP Special Term for Economic Partnership

SWR Shadow Wage Rate

TEU Twenty Foot Equivalent Unit

TOS Terminal Operation System

USDI United South Dock Handlers Incorporated

WACC Weighted Average Cost of Capital

WEO World Economic Outlook

Table of Contents

Executive Summary

(1) Background and Necessity of the Project .......................................................................................... 1

(2) Basic Policy Concerning Decisions on Project Content .................................................................... 3

(3) Description of the Project .................................................................................................................. 18

(4) Implementation Schedule ................................................................................................................... 25

(5) Feasibility of Implementation ............................................................................................................ 27

(6) Possible Japanese Firms’ Participation in the Proposed Project ........................................................ 29

(7) Concrete Schedule for Realizing the Project and Risks Inhibiting Its Realization ................................ 30

(8) Project Location Map ......................................................................................................................... 32

Chapter 1 Overview of the Host Country and Sectors

(1) Economic and Financial Conditions of Republic of Philippines ....................................................... 1-1

(2) Overview of Port Sector ..................................................................................................................... 1-3

(3) Present Situation of Cebu Region and Port ........................................................................................ 1-5

Chapter 2 Study Methodology

(1) Contents of the Study ......................................................................................................................... 2-1

(2) Method of Study / Organization ......................................................................................................... 2-4

(3) Schedule of the Study ............................................................................................................................ 2-7

Chapter 3 Justification, Objectives and Technical Feasibility of the Project

3.1 Demand Forecast ............................................................................................................................... 3-1

3.2 Cebu New Port ..................................................................................................................................... 3-9

(1) Background of the Project .................................................................................................................. 3-9

(2) The Study for Determination of the Project Contents ........................................................................ 3-11

(3) Description of the Project .............................................................................................................. 3-17

3.3 Cebu Existing Port ................................................................................................................................. 3-38

(1) Background of the Project .............................................................................................................. 3-38

(2) The Study for Determination of the Project Contents ........................................................................ 3-40

(3) Description of the Project .............................................................................................................. 3-62

3.4 Public-Private Partnership (PPP) of the Project ................................................................................. 3-77

Chapter 4 Evaluation of Environmental and Social Impacts

(1) Environmental and Social Considerations ......................................................................................... 4-1

(2) Environmental Effects Due to Project Implementation ..................................................................... 4-8

(3) Social Impacts of Project Implementation ..................................................................................... 4-12

(4) Governing Laws of the Philippines on Environmental and Social Impacts ....................................... 4-15

(5) Action Plan for the Government of Philippines ................................................................................. 4-19

Chapter 5 Financial and Economic Evaluation

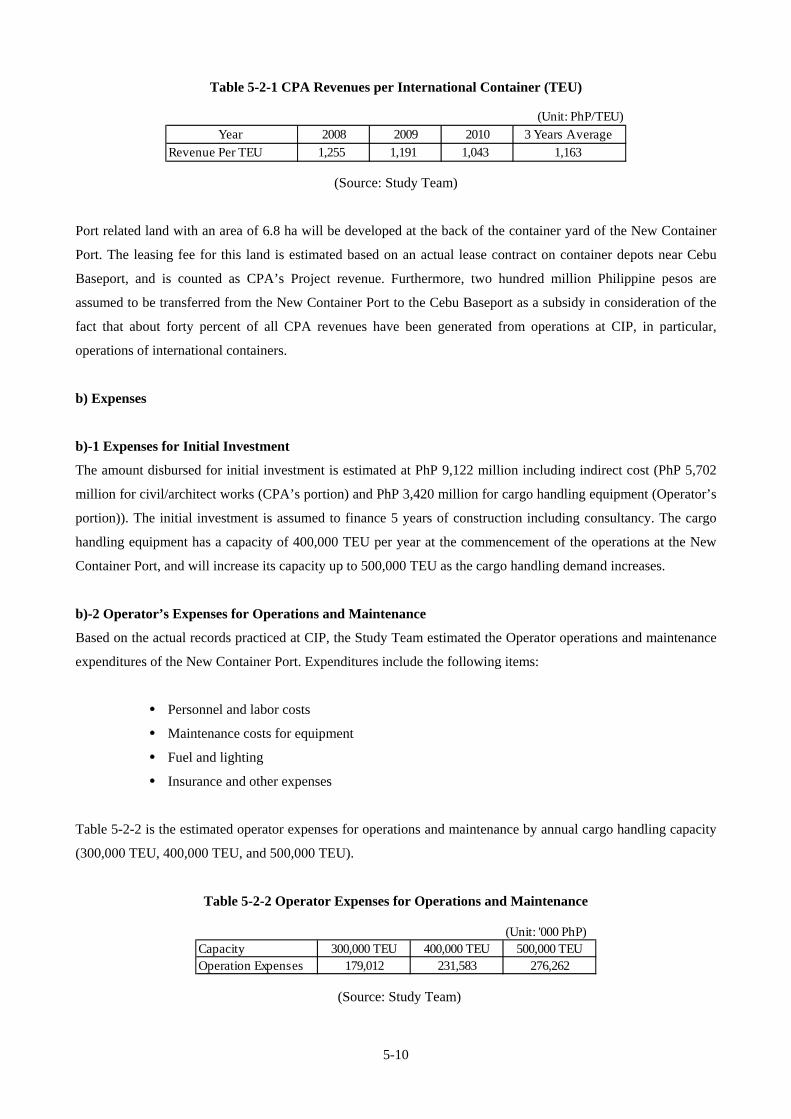

(1) Cost Estimate for New Cebu Container Port and Redevelopment of Existing Port ........................... 5-1

(2) Outline of Preliminary Financial and Economic Analysis ................................................................. 5-7

Chapter 6 Planned Project Schedule

(1) New Cebu Container Terminal ........................................................................................................ 6-1

(2) Cebu Baseport .................................................................................................................................... 6-3

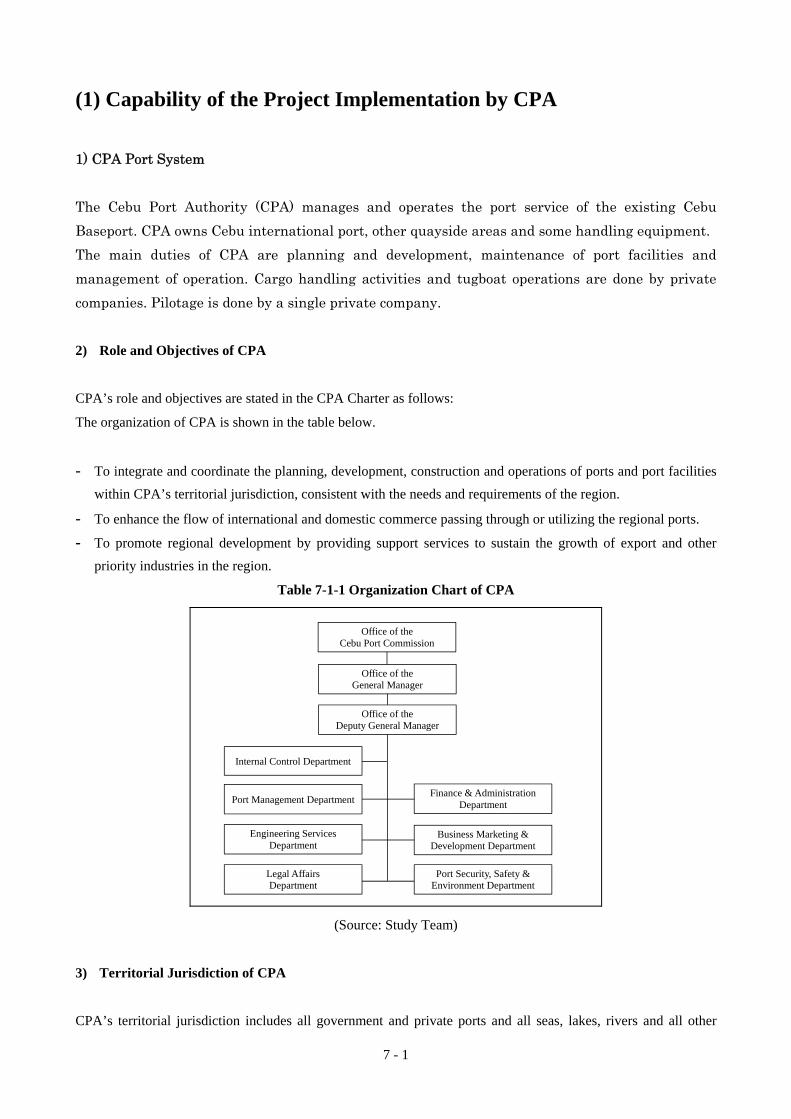

Chapter 7 Implementation Organization

(1) Capability of the Project Implementation by CPA ............................................................................. 7-1

Chapter 8 Technical Advantages of Japanese Companies

(1) Possible Japanese Firms’ Participation in the Proposed Project ........................................................ 8-1

(2) Advantages for Japanese Private Firms on the Project ...................................................................... 8-5

(3) Necessary Measures to Promote Participation of Japanese Firms ..................................................... 8-6

Chapter 9 Financial Outlook

(1) Analysis of Financing Plan ................................................................................................................ 9-1

(2) Possibility and Availability of Funds ............................................................................................. 9-2

(3) Cash Flow Analysis ............................................................................................................................... 9-3

Chapter 10 Action Plan and Issues

(1) Actions of Private Sectors .................................................................................................................. 10-1

(2) Actions of Public Sector .................................................................................................................... 10-5

(3) Legal and Financial Constraints of CPA ............................................................................................ 10-7

(4) Requirement of Additional Detailed Studies ..................................................................................... 10-10

Executive Summary

1

(1) Background and Necessity of the Project

The Study of the development of Cebu Port was started with the JICA report, ”The Study on the Cebu Integrated

Port Development Plan in the Republic of the Philippines” in 2002 In the JICA Study the short-term and

long-term development plans were proposed including preliminary design, cost estimate, economical/financial

analysis and environmental and social impacts assessment.

After the JICA report in 2002, a study on the feasibility of Japan’s ODA loan, which focused particularly on

STEP ODA in 2003, was conducted by the study group which was commissioned by the Ministry of Economy,

Trade and Industry in Japan.

In the study report made by JICA in 2004, “The Study on the Master Plan for the Strategic Development of the

National Port System in the Republic of the Philippines,” PPOSS (Philippine Port System Strategy) worked out a

strategic national port master plan with the target year 2024 and an urgent development plan with the target year

2009. Cebu Port is designated as one of six major national gateway ports (major ports for international container

trade) in this national plan.

In addition, Economic Research Institute for ASEAN and East Asia (ERIA) issued a report in 2010, “The

Comprehensive Asia Development Plan,” in which Cebu Port is also identified as the major port of the Philippines

that needs to be developed urgently.

However, due to a policy change by the proponent of CPA, a proposal for development by a private investor and

no agreement by the local government, development of the New Cebu Port has not materialized.

Ten years have passed since the JICA study in 2002. Nowadays, the congestion has become more serious due to

increasing cargo volume. The congestion of the international and domestic container terminals is remarkable. In

order to handle the increasing container cargo, two quayside gantry cranes installed in 2003 were increased to four

gantry cranes in 2010 and will increase to five gantry cranes in 2012 with seventeen RTGs. For other

cargoesexcept containers, due to the very narrow apron area, congestion during the loading and unloading is much

more serious. Therefore, the efficiency of cargo handling decreases and the safety of port operations will become

an issue.

According to information from the shipping companies, the water depth in front of the wharf is too shallow for

efficient and economical international shipping operation from/to Kaohsiung, Pusan, Hong Kong and Singapore.

They have a lease contract for empty container stocking in the city proper because of the lack of available land in

the terminal. Deepening of the berth to accommodate bigger container ships is very difficult because of the

structure of the berth, pier type with a retaining wall. Expansion of the wharf into the sea is also difficult due to

the narrow strait between Cebu Island and Mactan Island.

2

The Aquino Government started in 2010, announced that national projects should utilize a PPP scheme in order to

reduce the governmental burden by introducing private investment. DOTC follows the same policy and is

examining their handling projects on the practicality of introducing PPP schemes.

In this Study, the past study JICA 2002 is reviewed taking into account the recent economy and port surrounding

conditions. Then, the Project will be renewed applying a PPP scheme, i.e., survey how we can introduce private

investment to the Project considering finance methods and procedures.

On the other hand, the cooperating proponent, Mitsubishi Corporation, intends to participate in the operation of

the new container terminal as one of the Japanese groups considering partnership with Filipino companies and to

confirm the realization of the Project. Another proponent, Nippon Steel Corporation, intends to participate in the

supply and construction of the large steel pipe sheet pile type structure for the New Cebu Port. This Study

examines and evaluates the various procedures for construction of the New Cebu Container Terminal and for port

development and shall provide a proposal with action plans from the viewpoints of the private firms in order to

ensure implementation.

3

(2) Basic Policy Concerning Decisions on Project Content

The Study comprises the following steps:

1) Selection of the Site for the New Cebu Container Port

In the 2002 JICA Report, five candidate sites were proposed as shown in Figure 1. As the PPP scheme is

assumed for this project, the estimated construction cost is used as the most important factor for evaluation of the

site selection even though other factors such as ease of access to the New Port and safe navigation of the ships are

also important. To compare the sites, rough port planning was done to calculate the major volume of quantity such

as dredging, reclamation, container berth and breakwaters to estimate the construction cost. The Consolacion site

is the most economical and recommendable considering evaluation factors as shown in Figure 2. Therefore, the

preliminary design, cost estimate of the Project implementation, and economical and financial analysis were made

based on the Consolacion site.

Figure 1 Candidate Sites of New Cebu Container Port

Consolacion

Mactan North Mactan South

Cebu South

Minglanilla

Cebu Baseport

(Source: JICA Report 2002)

4

Figure 2 Comparison of Construction Cost for Candidate Sites

83%

111%

83%

166%

97%

29%

92%

28%

51%

24%

71%

142%

5%

47%

4%

12%

0% 100% 200% 300% 400%

A1Consolacion

A2Mactan-North

A3Mactan South

A4Cebu-South

A5Minglanilla

Assume 1.0

1.4

2.5

2.7

3.0

Reclamation Dredging

Breakwater

Road

(Source: Study Team)

2) Technical Review

The technical items are studied as mentioned below.

a) Cargo Demand Forecast

- Economic Framework

The Government of the Philippines formulated the basic strategic policy on national economic development

entitled, “The Philippine Development Plan 2011 – 2016.” In this Plan, the Government sets the corresponding

targets of a high economic growth rate of 7 to 8% per year for at least 6 years. On the other hand, considering

growth rate forecast of the International Monetary Fund (IMF), an annual growth rate of 4.9% until 2016 and

5.0% after 2016 has been established in this study as a conservative estimate.

- Cargo Demand

The actual annual growth rate of the total cargo volume was over 3% after 2000 at Cebu Baseport. A high

correlation (coefficient of determination=0.8297) has been observed between total cargo volume and GRDP.

Based on the above growth rate of the economic framework, total cargo volumes are estimated as 16 million tons

and 24 million tons in 2020 and 2030 respectively.

- Forecast by type of trade

Cargo volume of import, export, domestic loading, and domestic unloading are forecasted either through

correlation analysis or elasticity analysis with GRDP. Import growth rate is the biggest among all cargoes from

2010 to 2030 and import cargo will reach 7.9 million MT around 2030, which exceeds the domestic unloading

volume of 7.8 million MT.

- Forecast by Package Type

5

Four package types of bulk cargo, break-bulk cargo, container cargo, and rolling were forecasted. Shares by

package type are set for each trade type taking into account the past achievements and recent development. Thus,

cargo volume by trade type and by package type can be estimated.

- Demand Forecast for International Containers (TEU)

To forecast the future foreign container volume, a correlation analysis between container volume (TEU) and

GRDP of Region VII is implemented. A high correlation between the two variables is confirmed with a

determination coefficient of 94.0%. Resultant foreign container volume is estimated at 343,000 TEU in 2020, and

594,000 TEU in 2030.

Cargo volume by trade type by package type can be estimated as shown in Table 1.

Table 1 Summary of Demand Forecast by Trade Type and by Package Type

(Source: Study Team)

b) Port Planning

- New Cebu Port

Among international container, domestic container, international bulk and international general cargo, the rate of

increase in the international container demand forecast is 5.5% per year and the others are 2.5%. The tariff of

domestic container handling is set at 60 - 70% of the international container value. Therefore, the priority to move

international containers to the New Port is thought to be highest from the viewpoint of financial feasibility for the

private terminal operator.

The timing of opening the New Port should be adjusted to the time the cargo volume of the existing port reaches

Foreign Trade

Container Import Bulk Export Bulk Container Passenger

TEU MT MT TEU Pax

2000 103,944 48,203 14,338 372,268 2,651 299,630 1,366,913 1,494,780 0 0 10,059,048

2001 112,700 70,971 5,542 417,270 2,647 310,845 32,255 2,332 1,741,965 2,251,422 0 0 10,156,654

2002 103,139 53,912 20,000 406,547 2,484 337,370 42,507 6,824 1,696,717 2,611,269 0 0 10,738,198

2003 115,246 73,986 10,027 259,359 3,520 335,092 45,060 9,625 1,913,186 2,143,714 0 0 10,934,435

2004 120,281 60,931 6,000 192,140 31,735 311,282 78,396 99,700 1,852,455 2,255,197 0 0 11,785,915

2005 128,803 44,206 2,000 333,910 21,254 317,317 70,573 37,200 1,740,712 2,146,086 0 0 11,945,178

2006 146,459 75,648 7,800 276,922 30,177 279,442 10,666,071

2007 169,191 42,056 0 350,477 30,100 292,548 10,921,179

2008 157,634 93,287 0 423,989 32,062 295,155 10,321,278

2009 178,879 125,543 0 411,523 8,335 257,469 122,699 71,662 1,780,891 2,421,876 269,250 314,158 9,784,977

2010 202,213 156,373 0 358,674 0 247,295 273,754 194,678 2,030,300 2,303,575 279,634 366,817 10,993,921

2011 202,454 174,708 0 382,455 2,279 278,904 266,807 187,470 2,089,791 2,349,794 291,742 381,172 11,195,1372012 215,129 195,129 0 408,142 4,648 294,434 259,636 180,064 2,153,060 2,398,818 304,562 396,248 11,396,3532013 228,425 217,245 0 434,623 7,109 301,115 251,954 172,295 2,218,174 2,448,861 317,834 411,768 11,597,5682014 242,372 241,163 0 461,922 9,664 307,946 243,739 164,153 2,285,186 2,499,945 331,575 427,745 11,798,7842015 257,003 266,998 0 490,061 12,317 325,429 234,970 155,625 2,354,150 2,552,090 345,798 444,190 12,000,0002016 272,351 294,871 0 519,063 15,070 332,810 225,626 146,700 2,425,122 2,605,319 360,519 461,115 12,000,0002017 288,779 325,344 0 549,681 17,933 340,523 215,787 137,419 2,499,377 2,660,698 375,937 478,721 12,000,0002018 306,029 358,190 0 581,264 20,905 348,414 205,316 127,708 2,575,830 2,717,250 391,900 496,846 12,000,0002019 324,142 393,560 0 613,836 23,988 356,486 194,187 117,554 2,654,543 2,774,999 408,427 515,505 12,000,0002020 343,160 431,616 0 647,424 27,186 364,744 182,372 106,942 2,735,582 2,833,972 425,535 534,712 12,000,0002021 363,128 460,195 0 690,292 27,730 373,863 186,931 109,081 2,803,972 2,890,651 436,173 545,406 12,000,0002022 384,096 490,202 0 735,304 28,285 383,209 191,605 111,263 2,874,071 2,948,464 447,078 556,314 12,000,0002023 406,111 521,710 0 782,566 28,850 392,790 196,395 113,488 2,945,923 3,007,433 458,255 567,440 12,000,0002024 429,228 554,794 0 832,191 29,427 402,609 201,305 115,758 3,019,571 3,067,582 469,711 578,789 12,000,0002025 453,500 589,532 0 884,298 30,016 412,675 206,337 118,073 3,095,060 3,128,934 481,454 590,365 12,000,0002026 478,986 626,006 0 939,010 30,616 422,992 211,496 120,434 3,172,436 3,191,512 493,490 602,172 12,000,0002027 505,746 664,305 0 996,457 31,229 433,566 216,783 122,843 3,251,747 3,255,343 505,827 614,216 12,000,0002028 533,845 704,518 0 1,056,777 31,853 444,405 222,203 125,300 3,333,041 3,320,449 518,473 626,500 12,000,0002029 563,348 746,742 0 1,120,113 32,490 455,516 227,758 127,806 3,416,367 3,386,858 531,435 639,030 12,000,0002030 594,326 791,077 0 1,186,615 33,140 466,904 233,452 130,362 3,501,776 3,454,596 544,721 651,810 12,000,000

Exportbrkbulk (MT)

InboundBrkbulk (MT)

OutboundBrkbulk (MT)

Foreign Trade Year

Domestic Trade Inbound Bulk

(MT)Outbound

Bulk (MT)Inbound

Rolling (MT)Outbound

Rolling (MT)Import

Brkbulk (MT)

6

its full capacity. The handling capacity of the international container terminal of the existing port is estimated as

approximately 300,000 TEU per year. Referring to the result of the demand forecast curve, the time of opening

the New Port is proposed to be the year 2018. The initial capacity of container handling of the New Port is

expected to be 400,000 TEU per year and is scheduled to increase to 500,000 TEU per year by 2023 by installing

additional QCs and RTGs. The demand forecast of international container and New Port development are shown

in Figure 3.

Figure 3 Demand Forecast of International Container and New Port Development

0

100

200

300

400

500

600

700

2000

2005

2010

2015

2020

2025

2030

Year

Thr

ough

put (

1,00

0 T

EU

)

Phase 1 New Port = 400,000TEU

Additional QC/RTG = 500,000TEU

Existing Terminal Capacity = 300,000TEU

ForecastPast Record

2018

2023

Phase 2 Expansion

(Source: Study Team)

The berth length of the New Port is considered as two berths in order to prevent ship-waiting time. With a long

berth one next generation container ship of 3,000 TEU and one present average sized ship of 1,000 TEU can berth

at the same time. Also, the long berth can accommodate two ships of the present maximum size of 2,000 TEU at

the same time as shown Figure 4.

Figure 4 Berth Length of New Port

LOA 240m (3,000 TEU)LOA 150m (1,000TEU)

LOA 180m (2,000TEU)LOA 180m (2,000TEU)

Full Loaded Draft = 12.1mFull Loaded Draft =8.8m

Full Loaded Draft = 11.0m Full Loaded Draft = 11.0m

Future Maximum Size Present Average Size

Presenyt Maximum Size Present Maximum Size

Berth Length 450m

(Source: Study Team)

The location of the reclamation area has been decided to be the area where sea level is around 0.00 m in order to

7

minimize reclamation and dredging volume and the location of the berth to be the area where sea level is around

-13.0 m. The reclamation area is moved 200 m to the south from the JICA study. The reclamation area is located

approximately 250 m from the shoreline so that the mangrove plants can be saved by water exchange through tide

flow. The access road is planned to be an elevated bridge-way for the same reason. The layout plan of New Cebu

Port is shown in Figure 5.

Figure 5 Layout Plan of Phase 1 Development (New Port)

(Source: Study Team)

The container terminal layout is planned with consideration of the maximum handling capacity of 500,000 TEU

containers. Four gantry cranes (initially three) with a capacity of 15 container rows, a 450 m long berth, a terminal

area, and a back yard for port operation facilities have been studied as shown Figure 6.

Cebu North Coastal Road is one of the major development projects of the DPWH in the Metro Cebu area to

develop Cebu province. A length of 1.39 km out of 6 km of Cebu North Coastal Road was completed in 2009 by

DPWH. The new access road of the New Cebu Container Port will be connected to Cebu North Coastal Road.

Two traffic lanes are required for each direction based on the traffic forecast and an elevated bridge-way on the

shoreline and a cutting mound type road near Cebu North Coastal Road has been designed. A trumpet type

interchange near Cebu North Coastal Road will be constructed by DPWH. The terminal layout and bird’s eye

view are shown in Figures 6 and 7.

Turning Basin

Reclamation 350m x 600m

Berth Length 450m

8

Figure 6 Terminal Layout Plan of New Cebu Port

(Source: Study Team)

Figure 7 Bird’s Eye View of New Cebu Port

(Source: Study Team)

9

- Cebu Baseport

A study must be done on reorganizing the existing port functions after shifting the international container terminal

from the existing port to the New Port. In addition, in redevelopment of the existing port, it is also important to

establish a safe and convenient port station and to create commercial space closely related to the people’s life

activities.

The background and necessity of the redevelopment Project are explained from following points:

- CPA has to reshuffle the layout of the existing port based on the future port demand forecast.

- Income from the international container terminal will vanish for the existing port. It is considered that the

Project is a financially closed unit in which the financial aspects of the New Port are separate from those of

the existing port. In order to raise the feasibility of the Project, cost saving and introduction of alternative

income sources will be required.

- It has been observed that the high risk of accidents in the cargo handling operation and passenger traffic is

mainly due to the narrowness of the cargo yard in the vicinity of the quay-wall. It is essential that CPA ensure

improvement of the safety.

- The guarantee of a safe and comfortable trip is important for passengers who use the port to depart to / arrive

from Manila, Mindanao, etc. using a ferry or RORO.

- To improve the financial status of regional citizens, a strategy must be developed where the port, as a center

of commercial activities, will activate the economy. The PPP policy introducing private finance for

development is based on this activation of the economy.

- Taking advantage of the location close to the urban core of Cebu, a part of the Cebu Baseport area will be

redeveloped for commercial and business use. Thereby, a combination of town and open space is created and

will contribute to the promotion of redevelopment in the urban core.

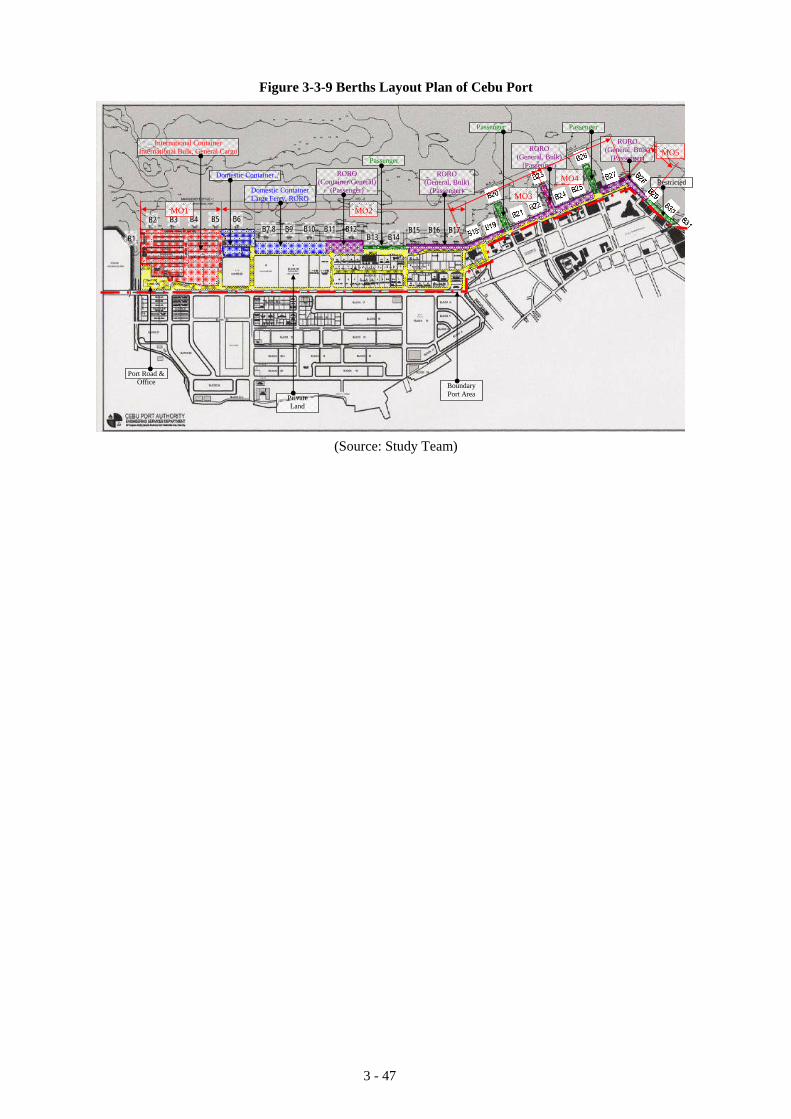

The Present Conditions of the Existing Port

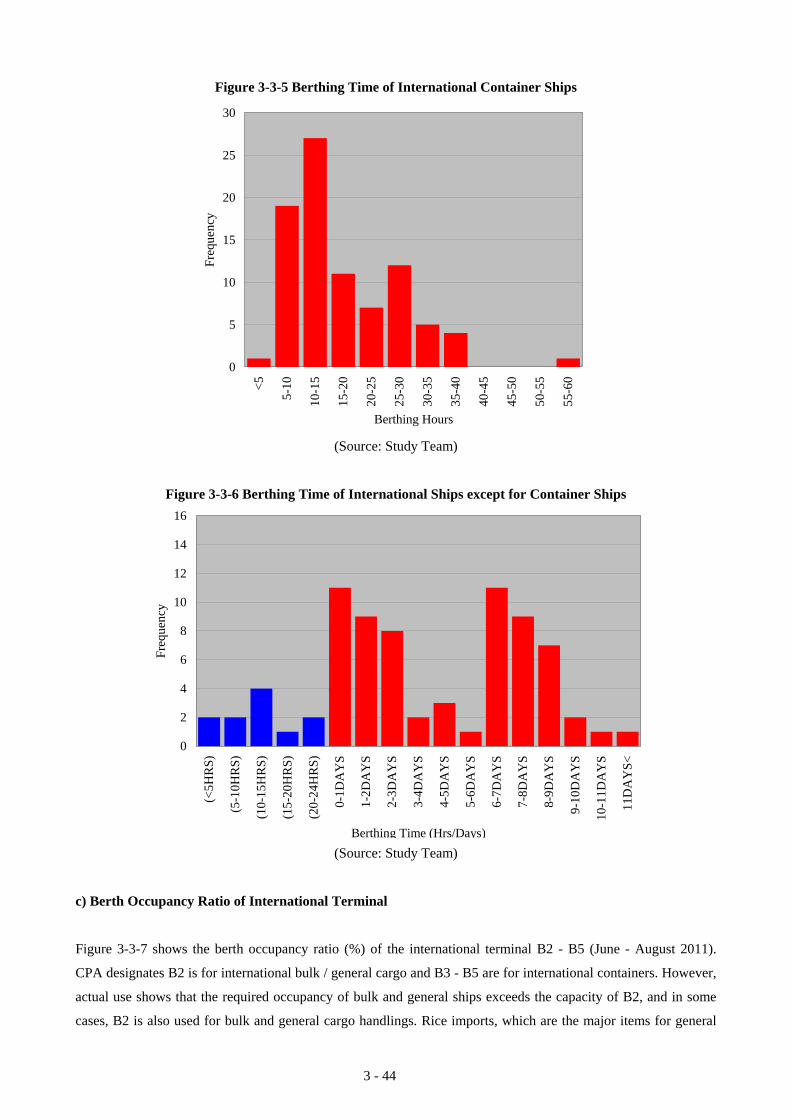

In order to clarify the present condition of the existing port, the berthing time of each berth, berth occupancy ratio,

cargo operation (in and out), yard operation, handling capacity, etc. should be observed and analyzed. One of the

most important factors in port planning is the berth occupancy ratio, which is shown in Figure 8 for international

container and bulk berth.

10

Figure 8 Berth Occupancy Ratio of International Terminal

14%20%23%

8%57%

13%5%

23%

8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

B2(L=130.5m)

B3(L=128.0m)

B4(L=128.0m)

B5(L=128.5m)

Berth No.

Ber

th O

ccup

ancy

Others

Rice

Container67%

54%

25% 27%

(Source: Study Team)

Port Planning of the Existing Port

The basic plan of the Project is as follows:

- International container terminal will be moved to the New Port according to the increase in port demand

(scheduled by 2018).

- Evaluate whether the capacity of the existing port is adequate or not before opening of the New Port.

- After commencement of operation of the New Port, study is required on facility investment of the existing

port as the short-term development plan 2020.

- Minimum required development on the existing port should be recommended. A PPP scheme should be

introduced on redevelopment by leasing the CPA owned port land so that the gained income will complement

the budget of the existing port.

- For the middle-term development plan targeted in 2030, some port functions should be relocated section by

section to the New Port when the capacity of the existing port is saturated.

- For the further long-term plan after 2030, only the passenger terminal should remain at the existing port and

all cargo functions should be moved to the New Port.

Degrees of Congestion of International Terminal

The international terminal handles both container and bulk / general cargo and it is not easy to evaluate congestion

separating these functions. Therefore, it is assumed that all international cargoes will be handled at the berths B2 -

B5 (4 berths, 515 m long) by 2018 as discussed. The limit capacity of the berth occupancy is assumed at 65%. The

following figures show the curve of demand for international container and international bulk/general cargo

11

calculated by the commodity-wise demand forecast.

Figure 9 Demand Forecast of International Container and Rate of Increase from Present Year 2011

International Container (TEU)

306

343

594

202

0

100

200

300

400

500

600

700

2000

2005

2010

2015

2020

2025

2030

Year

Thr

ough

put (

1,00

0 T

EU

)

51% Increase

70% Increase

(Source: Study Team)

Figure 10 Demand Forecast of Bulk / General Cargo and Rate of Increase from Present Year 2011

Import/Export Bulk (MT)

960

559

1,106

0

500

1,000

1,500

2,000

2,500

2000

2005

2010

2015

2020

2025

2030

Year

Thr

ough

put (

1,00

0MT

)

72% Increase

98% Increase

(Source: Study Team)

From these figures, international containers are estimated to increase 51% over the present throughput volume,

while international bulk / general cargo will increase 72% by 2018. On the other hand, the current berth

occupancy ratios of international container and bulk / general cargo berths (B2 - B5) are estimated at 15%

(container) and 29% (bulk / general). From this information, berth occupancy before New Port opening (2018) is

calculated as shown in Figure 11. It is foreseen that the occupancy ratio will increase to 71% (B2 - B5 total),

which will nearly reach the maximum capacity.

12

Figure 11 Forecast of Berth Occupancy Ratio before Opening New Port (2018)

BerthOccupancyContainer

BerthOccupancy

Bulk/Brkbulk

Total BerthOccupancy

At present 2011 15% 29% 43%

2018年 22% 49% 71%

51% Increase 72% Increase

(Source: Study Team)

The same calculations were made for other domestic containers, bulk, general cargoes and passengers to prepare

the short-term development plan in 2020.

The Suitable Location of Commercial and Public Spaces for Development

The location of commercial development sites by private sectors or public space sites such as a parks, etc. at Cebu

Baseport, is considered from the following viewpoints:

- Requirement of facilities and equipment as renewal port

- Appropriate location, function and scale as a commercial/public area in consideration of surrounding land

use and the city master plan

- Circulation of port-related traffic and other traffic

- Intention of redevelopment by private landowners in the port zone

- Private developer’s view on redevelopment

- Profitability of CPA land by sale or lease.

Regarding the location of the commercial development sites or public sites at Cebu Baseport, the following three

places are assumed as proposed sites with the Existing International Container Port area recommended as the most

feasible space.

- Existing International Container Port area

- Existing private lots in Port area

- The area around Fort San Pedro

13

Figure 12 Proposed Sites for Commercial Development or Public Space

Sites proposed for

(Source: Study Team)

Based on the above study, the Redevelopment Plan of the Baseport and Bird’s Eye View are shown Figures 13

and 14.

Figure 13 Redevelopment Plan of Cebu Baseport (2020)

Sky-Walk for Passenger

Superferry

Port Commercial Center

Bulk/General

Container Yard

Parking Parking

International Bulk/General

Domestic Container

Passenger

DomesticFerry/RORO/General

Commercial Development

Convert Terminal (Pier 1 & 3) Passenger → General Cargo

(Source: Study Team)

Site for Commercial or Public Spaces

14

Figure 14 Bird’s Eye View of Cebu Baseport (2020)

(Source: Study Team)

Port Plan 2030

The proposed port layout plan for 2030 is shown in Figure 15. In this plan, parts of port functions are moved to

the New Port when the capacities of each function are saturated due to an increase in demand. According to the

demand forecast study, initially, congestion of the international bulk / general cargo terminal will become serious

followed by the domestic container terminal. The proposed plan is dependent on these port functions (part of the

international bulk / general and the entire domestic container will be moved to New Port) being moved from the

existing port.

15

Figure 15 Proposed Layout Plan of Existing Port 2030

International Bulk/General

Passenger

Domestic Ferry/RORO/General

Commercial Development

Sky-Walk for Passenger

Superferry

Port Commercial Center

Bulk/General

Parking Parking

(Source: Study Team)

Port Plan after 2030

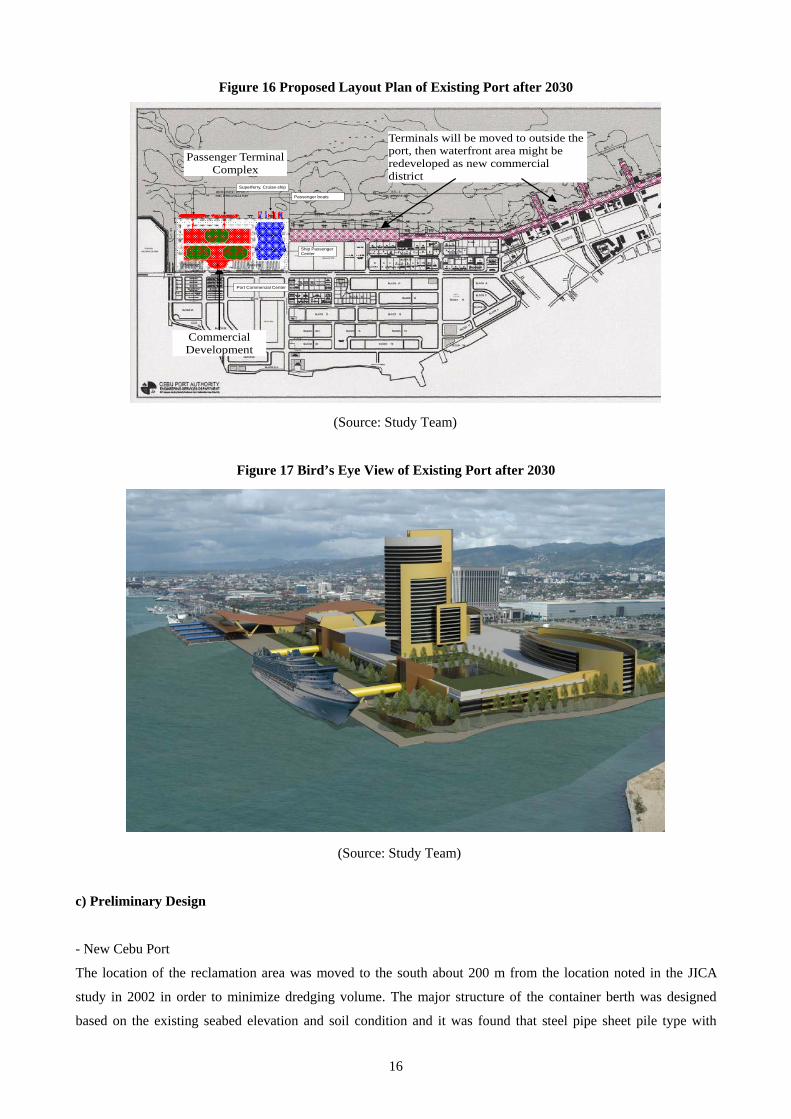

The proposed port layout plan after 2030 is shown in Figure 16. Port related parties have suggested that most of

the cargo terminals should eventually be moved to the newly developed port outside the downtown area of the city

in view of the social environment as well as the safety and efficiency of port operation as the present port space is

quite narrow. This study follows the same concept; thus, the plans of 2020 and 2030 represent the vision in the

process of this final port development strategy. Bird’s Eye View is shown in Figure 17.

16

Figure 16 Proposed Layout Plan of Existing Port after 2030

Terminals will be moved to outside the port, then waterfront area might be redeveloped as new commercial district

Commercial Development

Ship PassengerCenter

Passenger boats

Superferry, Cruise-ship

Port Commercial Center

Parking Parking

Passenger Terminal Complex

(Source: Study Team)

Figure 17 Bird’s Eye View of Existing Port after 2030

(Source: Study Team)

c) Preliminary Design

- New Cebu Port

The location of the reclamation area was moved to the south about 200 m from the location noted in the JICA

study in 2002 in order to minimize dredging volume. The major structure of the container berth was designed

based on the existing seabed elevation and soil condition and it was found that steel pipe sheet pile type with

17

anchor pile is the most economical and suitable for the new container port. Two traffic lanes are required for each

direction based on the traffic forecast and a bridge type superstructure in the coastline area and a cutting mound

type road near Cebu North Coastal Road is recommended. The typical substructure type will be multi-column

with a pier-head type pier and a bored pile foundation. The column section will be a circular shape, especially in

the seashore area, to minimize the streaming inhibition because it is the most economical and widely used in the

Philippines.

- Existing Cebu Port

For the structural type of pontoons, several options are available such as steel, fiberglass, concrete or

hybrid-concrete, etc. Considering the cost, durability, ease of local procurement and construction capabilities,

concrete type pontoons are proposed. For the foundation of the building, precast concrete piles are proposed

because they have good durability, low cost and are easy to procure in the local market. The structure of the

building is to be made of RC beam and slab.

d) Construction Cost

The Project cost estimated for the construction of New Cebu Port and the redevelopment of Existing Cebu Port

separately. The Project cost consists of civil work, building, utilities, container handling equipment, detailed

engineering cost, construction supervision cost, right of way acquisition cost and administration cost. Based on the

plan of New Cebu Port (Figure 6) and the redevelopment plan of Existing Cebu Port (Figure 13), rough quantities

were calculated for the facilities and estimated the cost. Cost of right of way for the access road is estimated using

the current price of the public works.

e) Environmental and Social Impacts

For the assessment of environmental issues, dredged materials from the New Cebu Port will be disposed in the

deep sea. In order to mitigate seawater contamination, a silt protector should be provided during the disposal of

the dredged material. There is small area of mangrove trees in the proposed site. It is assured that the number of

new mangrove trees that are planted will exceed the numbers that are cut down during the construction as

instructed by DENR.

3) Justification of the Project

The justification of the Project is evaluated by studying the following items.

a) Study of Investment Demarcation between Public and Private

In general, in the Philippines, fundamental facilities are the responsibility of the public while operation is the

responsibility of private companies. Firstly, construction costs, which should be kept as low as possible,

reclamation costs, which need an application to the central government for approval, berth cost and pavement

18

costs, which are relatively high, should be burdened by the public. Private institutions should shoulder the over

investments and expenditures as much as possible. Whether funds for facilities are to be provided by public or

private sectors, should be studied through pattern analysis.

b) Implementation Schedule

Based on the above demarcation, the implementation schedule is verified by each demarcation and reviewed for

expected completion and commencement of operation based on the demand forecast.

c) Evaluation of Finance

The possibilities to realize the both project for construction are studied including the case study of the facilities to

be shouldered by public or private.

d) Contributed Economic Effectiveness

The contribution to economic effectiveness is considered and verified in the cases with execution and without

execution.

4) Proposal toward Implementation of the Project

The proposals of the Study Team are compiled based on the above verifications.

a) Appropriate Demarcation of Public/Private Investments in View of Commencement of Operation and

Profitability

The timing of commencement and appropriate demarcation is proposed in consideration of the implementation

schedule and financial evaluation.

b) Utilization of Japan ODA Finance Program

The amount and investment objectives are proposed for the Japan ODA.

19

(3) Description of the Project

New Cebu Container Port will be constructed to cope with the congestion of the existing Cebu port and the

shallow water depth of the container berths. The redevelopment of the existing Cebu port will be implemented

including vacant area of the container terminal. The component of the new Cebu port is to construct international

container berths, container terminal and port related facilities and existing port is to construct expansion of berth,

floating passenger berths, domestic container terminal and passenger terminal.

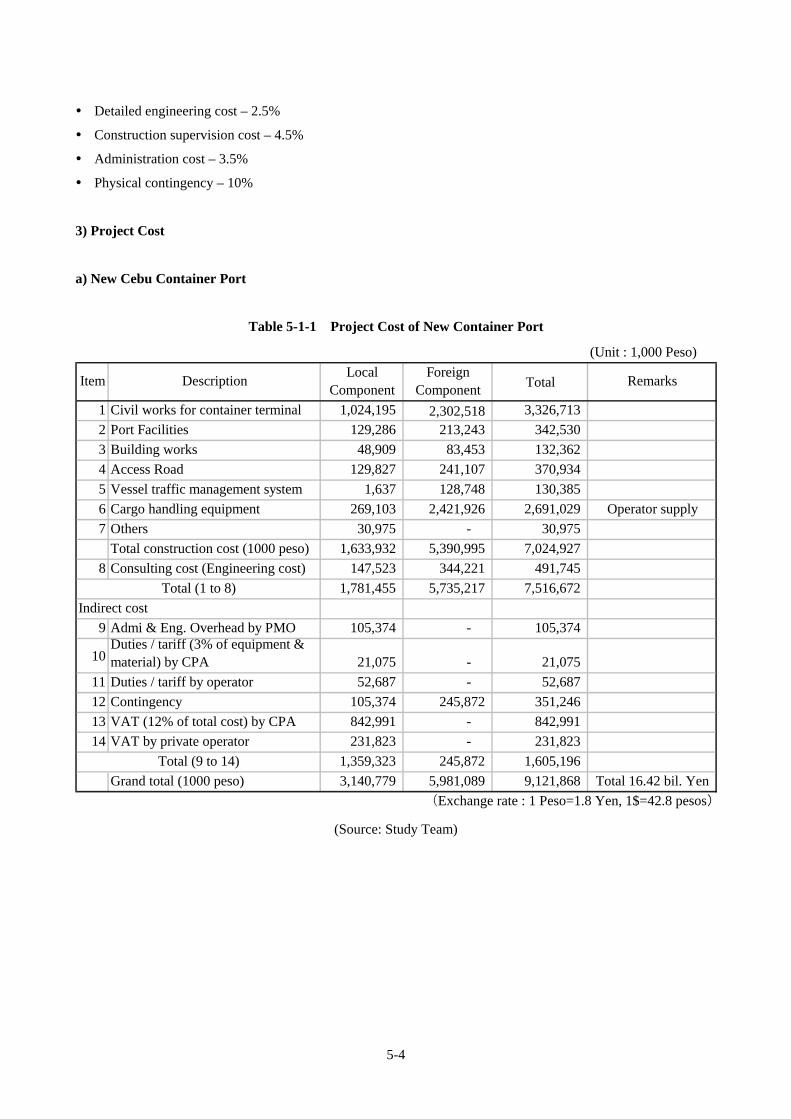

1) Implementation Project Cost

The Project cost has been estimated for the New Cebu Port and the redevelopment of the existing Baseport.

The Project cost consists of civil work, building, utilities, container handling equipment, detailed engineering cost,

construction supervision cost, ROW acquisition cost, and administration cost.

a) Implementation Cost of New Cebu Port

Table 2 New Cebu Port

(Unit : 1,000 Peso)

LocalComponent

ForeignComponent

Total

1 Civil works for container terminal 1,024,195 2,302,518 3,326,713

2 Port Facilities 129,286 213,243 342,530

3 Building works 48,909 83,453 132,362

4 Access Road 129,827 241,107 370,934

5 Vessel traffic management system 1,637 128,748 130,385

6 Cargo handling equipment 269,103 2,421,926 2,691,029 Operator supply

7 Others 30,975 - 30,975

Total construction cost (1000 peso) 1,633,932 5,390,995 7,024,927

8 Consulting cost (Engineering cost) 147,523 344,221 491,745

1,781,455 5,735,217 7,516,672

Indirect cost

9 Admi & Eng. Overhead by PMO 105,374 - 105,374

10Duties / tariff (3% of equipment &material) by CPA 21,075 - 21,075

11 Duties / tariff by operator 52,687 - 52,687

12 Contingency 105,374 245,872 351,246

13 VAT (12% of total cost) by CPA 842,991 - 842,991

14 VAT by private operator 231,823 - 231,823

1,359,323 245,872 1,605,196

Grand total (1000 peso) 3,140,779 5,981,089 9,121,868 Total 16.42 bil. Yen

(Exchange rate : 1 Peso=1.8 Yen, 1$=42.8 pesos)

Total (9 to 14)

Total (1 to 8)

RemarksItem Description

(Source: Study Team)

20

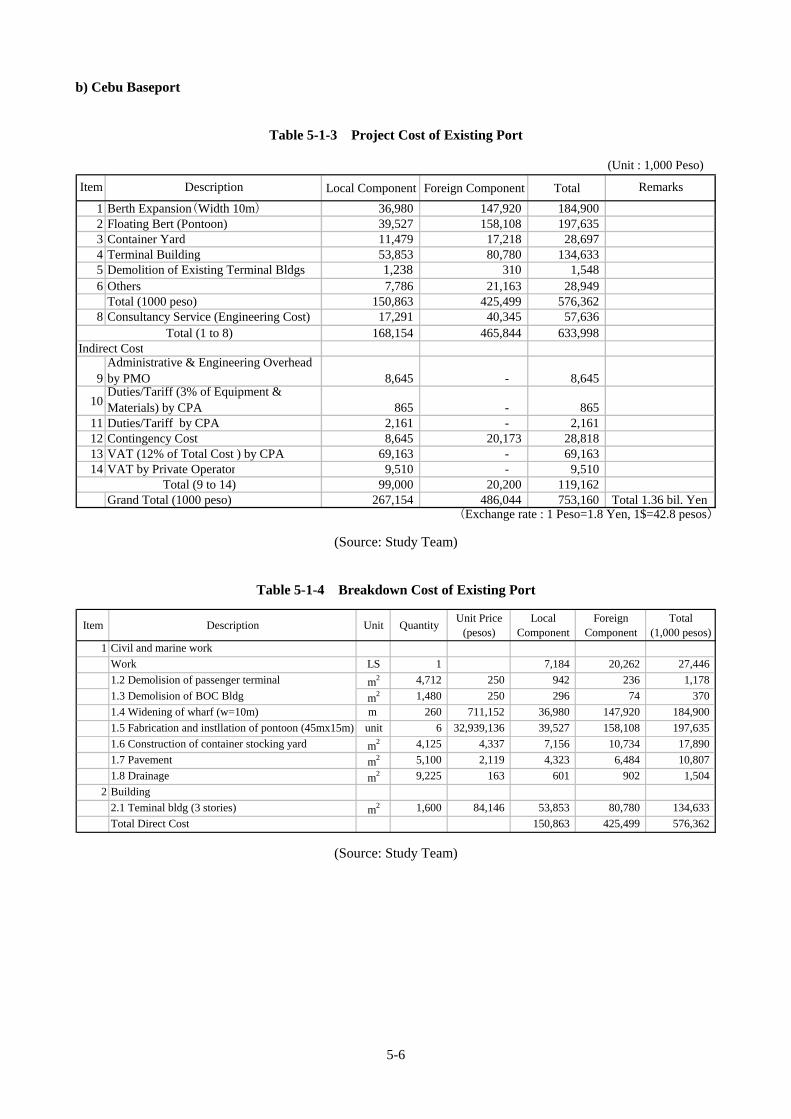

b) Existing Baseport

Table 3 Existing Baseport

(Unit : 1,000 Peso)

Local Component Foreign Component Total

1 Berth Expansion(Width 10m) 36,980 147,920 184,900 2 Floating Bert (Pontoon) 39,527 158,108 197,635 3 Container Yard 11,479 17,218 28,697 4 Terminal Building 53,853 80,780 134,633 5 Demolition of Existing Terminal Bldgs 1,238 310 1,548 6 Others 7,786 21,163 28,949

Total (1000 peso) 150,863 425,499 576,362 8 Consultancy Service (Engineering Cost 17,291 40,345 57,636

168,154 465,844 633,998 Indirect Cost

9Administrative & EngineeringOverhead by PMO 8,645 - 8,645

10Duties/Tariff (3% of Equipment &Materials) by CPA 865 - 865

11 Duties/Tariff by CPA 2,161 - 2,161 12 Contingency Cost 8,645 20,173 28,818 13 VAT (12% of Total Cost ) by CPA 69,163 - 69,163 14 VAT by Private Operator 9,510 - 9,510

99,000 20,200 119,162 Grand Total (1000 peso) 267,154 486,044 753,160 Total 1.36 bil. Yen

(Exchange rate : 1 Peso=1.8 Yen, 1$=42.8 pesos)

Item Description Remarks

Total (9 to 14)

Total (1 to 8)

(Source: Study Team)

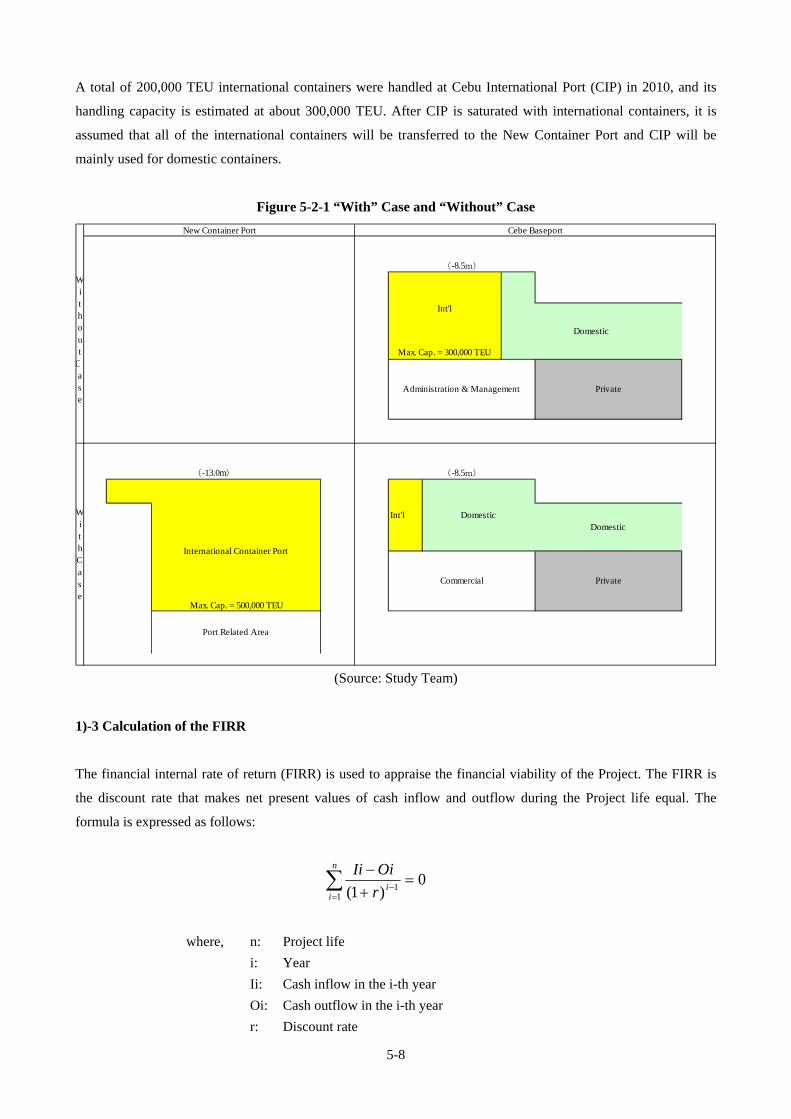

2) Outline of Preliminary Financial and Economic Analysis

a) Cebu New Port

a)-1 Financial Evaluation of the Project

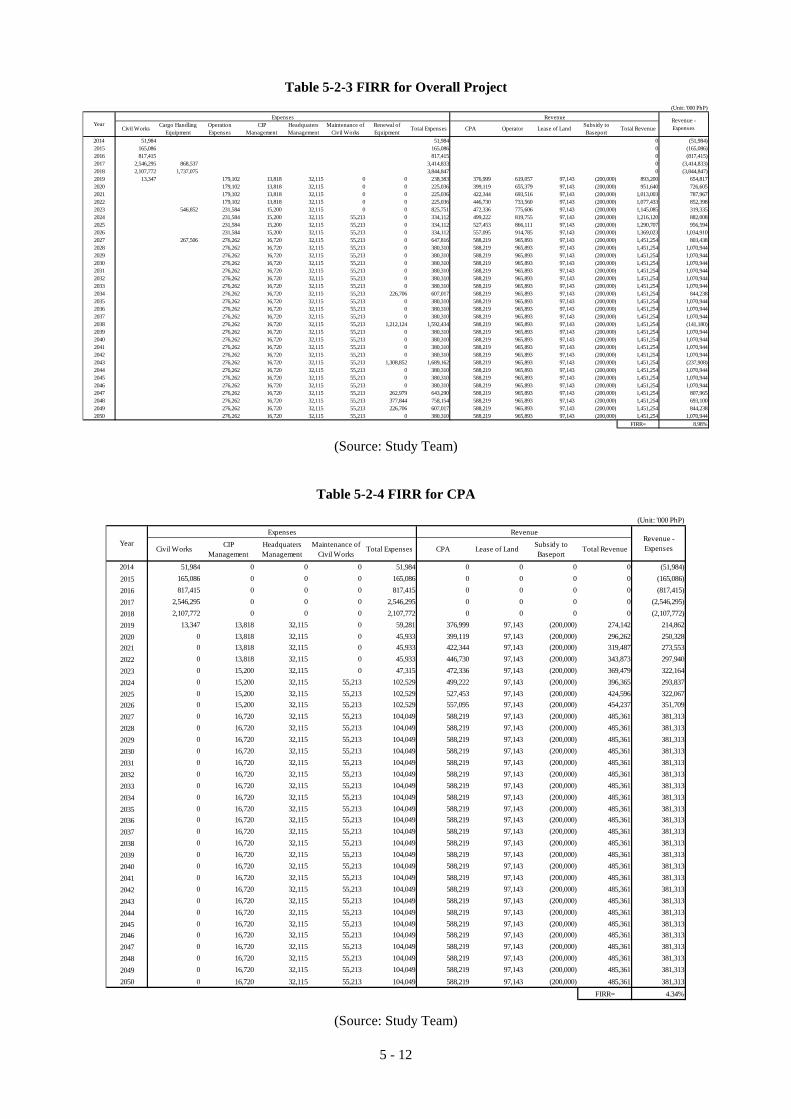

- FIRR (Base Case): Overall Project 8.98%, CPA 4.34%, Operator 18.01%

- Sensitivity Analysis

Sensitivity analysis was carried out for a total of 6 cases: cost increase (Case I), revenue decrease (Case II), and

both cost increase and revenue decrease (Case III). In the case of 10% cost and revenue variance for the Overall

Project, the FIRR are 7.62% (Case I), 7.48% (Case II), and 6.13% (Case III) as shown below.

21

Table 4 Financial Evaluation of the Project

Overall Project CPA Operator Overall Project CPA Operator7.62% 3.51% 15.61% 6.39% 2.76% 13.48%

Overall Project CPA Operator Overall Project CPA Operator7.48% 3.42% 15.36% 5.81% 2.41% 12.48%

Overall Project CPA Operator Overall Project CPA Operator6.13% 2.60% 13.03% 3.16% N.A 7.98%

Case IIICost Increase & Revenue Decrease By 10% Cost Increase & Revenue Decrease By 20%

Case ICost Increase By 10% Cost Increase By 20%

Case IIRevenue Decrease By 10% Revenue Decrease By 20%

(Source: Study Team)

Assuming a Weighted Average Cost of Capital (WACC) of 2.16% for CPA and 6.43% for TO, both of which are

derived from financial plans, the resulting NPVs are PHP 2,087 million and PHP 3,366 million, respectively.

Further, B/C Ratios are 1.29 for CPA and 1.59 for TO under the same discount rates.

a)-2 Economic Evaluation

- EIRR (Base Case): 20.02%

- Sensitivity Analysis

As shown in the table below, the New Cebu Port Project has an EIRR of more than 15% for all of the cases in the

sensitivity analysis except for the worst scenario case.

Table 5 Economic Evaluation of the Project

Cost Increase By 10% Cost Increase By 20%18.03% 16.32%

Benefit Decreases By 10% Benefit Decreases By 20%17.82% 15.55%

Cost Increase & Benefit Decrease By 10% Each Cost Increase & Benefit Decrease By 20% Each15.97% 12.36%

Case I

Case II

Case III

(Source: Study Team)

Assuming the social discount rate of 15%, the Benefit Cost ratio (B/C) for the Base Case is 1.29. On the other

hand, the NPV of the Project is calculated at PHP 1,860 million.

b) Cebu Baseport

b)-1 Financial Evaluation of the Project

- FIRR (Base Case): 5.81%

- Sensitivity Analysis

22

Sensitivity analysis was carried out for the same 6 cases as the financial evaluation. In the case of a 10% cost and

revenue variance for the Project, FIRRs are 4.86% (Case I), 4.76% (Case II), and 3.81% (Case III) as shown

below.

Table 6 Financial Evaluation of the Project

Case IIICost Increase & Revenue Decrease By 10% Cost Increase & Revenue Decrease By 20%

3.81% N.A

Case IIRevenue Decrease By 10% Revenue Decrease By 20%

4.76% 3.59%

Case ICost Increase By 10% Cost Increase By 20%

4.86% 4.00%

(Source: Study Team)

Assuming the WACC is 7.0%, the NPV of the Cebu Baseport Project is calculated at PHP -85 million and the B/C

ratio is 0.89.

b)-2 Economic Evaluation of the Project

EIRR (Base Case): 20.97%

Sensitivity Analysis

As shown in the table below, the Cebu Baseport Project has an EIRR of more than 15% for all of the cases in the

sensitivity analysis except for the worst scenario case.

Table 7 Economic Evaluation of the Project

(Source: Study Team)

Assuming the social discount rate of 15%, the Benefit Cost ratio (B/C) for the Base Case is 1.24. On the other

hand, the NPV of the Project is calculated at PHP 105 million.

In general, the New Cebu Port Project has both high FIRR and EIRR values except for the worst scenario case in

the sensitivity analysis. On the other hand, there is a possibility that the FIRR of the Cebu Baseport Project is less

than the WACC of the Project while the EIRR of the Project is expected to be higher than 20%. It should be noted

however, the FIRR of the Baseport Project will improve and the financial problems mentioned above will be

resolved if the CPA plot is sold instead of leased or if a project fund with lower interest is secured through ODA

assistance. Taking these circumstances into consideration, both Projects can be judged to be sound and feasible.

Case ICost Increase By 10% Cost Increase By 20%

19.18% 17.65%

16.96%

Cost Increase & Revenue Decrease By 20%

14.09%

Benefits Decrease By 20%

19.00%Case II

Benefits Decrease By 10%

Case IIICost Increase & Revenue Decrease By 10%

17.34%

23

3) Evaluation of Environmental and Social Impacts

3)-1 General

This Study focuses on the environmental and social impacts in the area of the New Cebu Port about 10 km north

of the existing Baseport and the redevelopment area in the existing Baseport.

- Seawater Quality

Dissolved oxygen content and chemical oxygen level are much higher than the DENR limits. The levels of

cadmium in the New Port and arsenic at the Cebu Port site are critical. Other heavy metals are below the DENR

limits but excessive levels of total coliform and fecal coliform, both indicators of pollution from anthropogenic

sources, were observed to be very high in the New Port and existing Baseport.

- Sea Bottom Sediment Quality

Lead pollution in Baseport and New Port is significantly higher at ten times the Japan limit. Other heavy metals

are below the DENR limits. The chemical oxygen level is far higher than the DENR limits in both ports.

- Air and Noise

All levels of air quality parameters fall below the maximum limits set by DENR. This indicates relatively good air

quality at these sites.

- Marine Ecology

In the existing Baseport, the absence of marine vegetation and macrobenthos, which fish feed on, and regular

dredging in the harbor limit the survival of fishes in the area. The mangroves along the shoreline near the New

Port site showed the characteristic features of the substrate in the study area. Corals and associated macrobenthos

were observed near the Baseport site. The sea grasses provide nutrients for juvenile fishes and other marine

organisms in the area. No rare, threatened or endangered species of algae have been encountered.

Magnitude of development is as follows:

- New Port : 23 ha reclamation, 450 m berth, 16,000 m³ dredging and 600 m access road

- Baseport : 270 m pontoon, 4,800 m² passenger terminal, 4,000 m² yard, 8.5 ha business center by PPP.

3) -2 Positive Environmental and Social Impacts of the Project

With implementation of the New Cebu Port and redevelopment of Cebu Baseport, environmental improvement

around the Project site is expected as follows:

- By construction of the New Cebu Port, larger-sized vessels with emission control systems can use the port.

Reduction of CO₂ emission per TEU is expected. Due to construction of the New Cebu Port, the access

distance from Mactan Island will be shortened and the congestion around the existing Baseport will thus be

reduced.

- With construction of the New Cebu Port and redevelopment of the Baseport, cargo volumes will increase and

industrial/regional development in the hinterland and surrounding areas will follow. An increase in job

opportunities and local economic development is expected.

24

3)-3 Negative Environmental and Social Impacts of the Project

All impacts on the environment and society are relatively good at both sites.

The remarkable environmental and social impacts for the both sites are indicated below;

New Cebu Port

Land acquisition for the new access road before the construction of new port may cause a rise in land prices in

Consolacion, but considering the acquired land is small area and not located in the center of Consolacion, the

impact to the land price will be limited compared with the common national road construction.

A negative impact on marginal fishing is irreversible, but minimal in magnitude because the few who catch fish

nearby only get a small quantity of small-sized anchovies and small roundscads.

Operation-phase impacts of the Project will mainly be positive and highly probable, i.e., increased land values,

improved opportunities for livelihood, employment and income, economy and growth, enhanced port productivity,

efficiency and berth capacity and improved welfare of women and children. All these are reversible and vary in

terms of duration ranging from short to long-term.

Baseport

Operation of constructed facilities is expected to generate mainly positive impacts including: improvement in the

overall CPA efficiency in handling of cargoes and passengers, increase in space for business and recreation,

increased employment and livelihood opportunities, improved CPA financial resources, improvement in workers’

living standards and increased business and tourism activities and importantly.

3)-4 Study of Findings and Action Plan

a) New Cebu Port

- According to DENR, an EIA shall be prepared to apply for ECC because of the New Port.

- Land acquisition for construction of the access road is necessary. Coordination with DPWH and Consolacion

town is necessary to adjust the intersection and transition area to the Cebu North Coastal Road designed by

DPWH.

- EIA should provide legal proof to show its authority to reclaim and develop the New Cebu Port site. This

should be done together with an application for a special land patent from the Land Management Bureau of

DENR and a Presidential Proclamation for reservation of the Project site as a container port zone.

- CPA must consult with DENR Provincial Environment and Natural Resource Office (PENRO) and/or the

Community Environment and Natural Resource Office (CENRO) as well as the Protected Area, Wildlife and

Coastal Zone Management Service of DENR-7 to obtain clearance to acquire and develop the port site.

- CPA must also coordinate with the Philippine Reclamation Authority on its plan to carry out offshore

reclamation of Consolacion town.

- CPA must coordinate with DENR and Philippine Coast Guard Regional Office – Region 7 for confirmation of

designated/approved disposal site for dredged materials during port construction.

25

b) Cebu Baseport

Since the Cebu Baseport involves redevelopment including expansion/modification of the existing port facility,

existing DENR guidelines indicate that the EPRMP document must be prepared by CPA.

26

(4) Implementation Schedule

1) New Cebu Port

After the authorization and approval of the New Cebu container Port by the Philippine government, the following

will be done: the application for a soft loan, employment of the consultant, conduction of detailed design,

preparation of PQ and tender documents, selection of contractor of the civil works and implementation of

construction of the works. It is estimated the period of implementation of detailed design and preparation of tender

documents, construction of civil works and fabrication/installation of container handling equipment are one year,

two and a half years, and one year respectively.

Table 8 Implementation Schedule of New Cebu Port (PPP Scheme)

Month

Container Terminal Development 1 Implementing Public Portion by CPA

(1) Study on New Cebu Container Port by METI 6

(2) Submission and Review of New Cebu Container Port to NEDA by DOTC 3

(3) Preparation of EIA and Obtain ECC by CPA 3

(4) Financial Arrangement and Requests for Project Loan by CPA/DOTC 12

(5) Procurement of Consultants for the engineering study 3

(6) DD - PQ + T/D Preparation by Consultant 12

(7) PQ for procurement of contractor by CPA 3

(8) Tendering for procurement of contractor by CPA 6

(9) Contract negotiation and signing the contract with CPA 3

(10) Construction works 30

1) Dredging works 4

2) Container berth construction 18

3) Revetment construction 12

4) Reclamation works 12

5) Road and pavement construction 15

6) Building works construction 10

7) Utility works construction 12

8) Access road construction 18

2 Procurement of Private Investor (Concessioner)(1) Project Resolution by Government DOTC/CPA

1) Preparation and Submission of PPP Scheme by CPA 3

2) Evaluation and approval by CPA Board 3

(2) Transaction (Procurement ) of Private Investor

1) Document Preparation of PQ and Tender Documents 6

2) PQ process for short list investors for tendering 4

3) Procurement by Tendering 8

4) Contract negotiation and Signing the contract with CPA/DOTC 5

(3) Installation of the Equipment and Auxiliary Facility

1) Engineering study of facilities 3

2) Fabrication and Installation of the Equipment 12

3) Supply and preparatory work of Auxiliary Facility 6

3 Commencement of Operation of Container Terminal

Description of Works 2011 2012 2013 2014 2015 2016 2017 2018

(Source: Study Team)

2) Existing Baseport

After the authorization and approval of the New Cebu container Port by the Philippine government, the following

will be done: application for a soft loan, employment of consultant, conduction of detailed design, preparation of

PQ and tender documents, selection of contractor of the civil works and implementation of construction of the

works. It is estimated the period of implementation of detailed design and preparation of tender documents,

construction of marine works and construction of business/commercial center are eight months, fifteen months

and two years respectively.

27

Table 9 Implementation Schedule of Cebu Baseport (PPP Scheme)

Month

Redevelopment of Baseport1 Implementing Public Portion by CPA

(1) Study on New Cebu Container Port by METI 6

(2) Submission and Review of New Cebu Container Port to NEDA by DOTC 3

(3) Preparation of EIA and Obtain ECC by CPA 3

(4) Financial Arrangement and Requests for Project Loan by CPA/DOTC 12

(5) Procurement of Consultants for the engineering study 3

(6) DD - PQ + T/D Preparation by Consultant 6

(7) PQ for procurement of contractor by CPA 3

(8) Tendering for procurement of contractor by CPA 4

(9) Contract negotiation and signing the contract with CPA 3

(10) Construction works 15

1) Demolision of Bldgs 4

2) Widening of wharf (w=10m) 10

3) Fabrication and instllation of pontoon (45mx15m) 12

4) Yard Construction 4

5) Teminal bldg (3 stories) 10

2 Procurement of Private Investor (Concessioner)(1) Project Resolution by Government DOTC/CPA

1) Preparation and Submission of PPP Scheme by CPA 3

2) Evaluation and approval by CPA Board 3

(2) Transaction (Procurement ) of Private Investor

1) Document Preparation of PQ and Tender Documents 3

2) PQ process for short list investors for tendering 3

3) Procurement by Tendering 4

4) Contract negotiation and Signing the contract with CPA/DOTC 3

(3) Construction of Business and Commercial Center 24

3 Commencement of Operation of Redevelopment Plan of Baseport

Description of Works 2011 2012 20132014 to

20172018 2019 2020 2021

(Source: Study Team)

28

(5) Feasibility of Implementation

The purpose of this section of the report is to evaluate both the Cebu New Port and Baseport Projects from

financial and economic, technological, capability of the project implementation by CPA and advantages for

Japanese private firms.

1) Cebu New Port

- Regarding the Base Case, the Project is judged to be financially viable because the FIRR are expected to be

higher than WACC both for CPA portion and TO portion. In addition, EIRR of the Project is expected to be

about 20%, which is higher than the cut-off rate of 15% currently adopted in the Philippines. The Project is

judged to be healthy from a national economic viewpoint. Cash balance will be minus from 2018, but turns to

be plus after the two years of operation. Taking these circumstances into consideration, the Project can be

judged to be sound and feasible.

- A comparative study of five proposed sites was done to select the most appropriate port in the JICA study in

2002. Specific port planning was done for the main facility such as berth, reclamation, dredging and

breakwater to calculate rough quantities for the proposed sites and the cost estimate in this study. Based on the

comparison, the Consolacion site is the most recommendable from the economical aspects, accessibility to the

Baseport, future expansion, adjustability to the airport and environmental conditions.

- The port function of the Baseport is international cargoes (container, bulk and general cargo) and domestic

cargoes (container, ferry and RORO) and passengers. Maintaining this function, international container should

be transferred to the New Port considering a PPP scheme. The rate of increase in the international container

demand forecast is 5.5% per year. The rate is not very high compared to the rates of other major ports in Asia.

Therefore, if we assume the international container terminal should be moved to the New Port, the initial

investment share for the public sector should be set at a high level in order to reduce the burden encountered

by the private sector.

- The timing of opening the New Port should be adjusted to the time the cargo volume of the existing port

reaches capacity. The handling capacity of the international container terminal of the existing port is estimated

as approximately 300,000 TEU per year. The capacity of container handling should be increased step by step

considering the efficiency and feasibility of the New Port.

- CPA became independent of PPA in 1992 and operates and maintains all ports in Cebu province. CPA is

financially sound and designates the new PMO to operate the new project. A financial specialist and lawyer

should be employed for the Project because CPA has no experience with PPP schemes.

29

2) Cebu Baseport

- Regarding the Base Case, FIRR of the Project is estimated at 5.81%, which is less than WACC. The FIRR of

the Project will however, become higher than WACC if a project fund with a lower interest rate such as an

ODA loan and CPA’s retained earning can be used. In addition, EIRR of the Project is expected to be about

20%, which is higher than the cut-off rate of 15% currently adopted in the Philippines. Therefore, the Project is

judged to be healthy from a national economic viewpoint. Cash flow of CPA Re-Development Project was

calculated based on the assumption that CPA will borrow a long-term loan from Treasury Bank. The cash

balance of CPA was minus for almost all of the period, and the minus in cash balance will be accumulated.

Selling or leasing the port land should be considered carefully giving comprehensive consideration for the best

use of the port land.

- Based on the movement of international container to the New Port, Baseport redevelopment should be planned

to use the vacant area of the international container yard for mitigation of the congestion of the port area for

target year 2020. The cargo operation is carried out in a way that the cargo transported from private storage by

trucks is directly loaded onto the ship; therefore, berth occupancy is taken into account quantitatively for the

port planning method.

- Income from the international container terminal will vanish due to the Baseport Redevelopment Project. In

order to raise the feasibility of the Project, cost saving and introduction of alternative income sources will be

required.

- Regarding the port layout of 2030, overflow cargo from the port capacity should be moved to the New Port.

Port related parties have suggested that most of the cargo terminals should eventually be moved to the newly

developed port outside the downtown area of the city.

Taking the variety of elements mentioned above into consideration, both the Cebu New Port and Baseport

Projects are judged to be feasible for implementation from financial, economic, technological, and social and

environmental aspects.

30

(6) Possible Japanese Firms’ Participation in the Proposed Project

1) Cebu New Port

Regarding the participation in the terminal operation, all Japanese operating oversea terminals are efficiently and

satisfactorily managed in Indonesia and Vietnam. As Japanese construction firms and suppliers have also acquired

knowledge in international competitive bidding, there is a high possibility of participation in the construction of

the New Cebu Container Terminal because of their experience in the Philippines.

2) Cebu Baseport

Japanese consulting firms have extensive experience in redevelopment of Japanese ports; therefore, there is an

advantage for Japanese Consulting Firms to participate in the Study for Redevelopment of the Baseport. Japanese

consulting firms have the intension to participate in redevelopment of the large scale business/commercial and

tourist area in the Baseport in 2030.

31

(7) Concrete Schedule for Realizing the Project and Risks Inhibiting

Its Realization

1) Implementation Schedule

The following stages are generally applied for processing PPP scheme projects. The master plan will be

implemented in four (4) stages for the Partnership Project, “Planning of Partnership Projects,” “Preparation of

Feasibility Study of the Partnership Projects,” “Transaction for Partnership Project” and “Management for

Implementation of the Partnership Project.”

Stage1:Planning and Selection of PPP Scheme Project

- CPA will be required to authorize the draft master plan as reviewed and updated by the current Study.

- CPA will identify and select the Project components to be implemented by PPP scheme based on the draft

master plan.

- CPA shall apply for Project resolution by the government and permit the implementation of the proposed

Project by PPP Scheme.

Stage 2:Preparation of full scale Feasibility Study of PPP Scheme Project

- CPA shall review the suggestion, recommendation and proposal of the full scale feasibility study.

- CPA will check and confirm the full scale feasibility study such as assessment, evaluation, the readiness of the

Project implementation, scope and cost of the public and private responsible portions, the financial returns of

the Project by CPA and private concessionaire, traffic demands, and implementing schedule of operation.

- CPA shall conduct the environmental survey by updating the previous EIA study carried out in 2002 under the

JICA study in order to obtain the approval of the EIA from the regional environmental agency.

Step 3: Transaction for Partnership Project (Procurement of private investor, concessionaire)

- CPA shall prepare the documents required for procurements of concessionaire, such as prequalification

documents, tender documents, draft partnership agreement documents, PQ and tender evaluation criteria for

selection of concessionaire in coordination with DOTC, MOF and Agencies responsible for PPP.

- CPA shall prepare the financial arrangement of the Project components responsible by CPA.

- CPA may procure a consultant for the engineering study of the Project and a contractor for the construction

works of the CPA portion.

32

Stage 4:Management for Implementation of Partnership Project

- CPA will prepare a management plan of partnership contract.

- CPA shall report periodically on the results of management activities to the higher authority responsible for the

Partnership Project Responsible agency in the Government of the Philippines.

- Management unit of CPA manages the fulfillment of preliminary requirements by Business Entity and

monitoring in the pre-construction stage as follows:

- Manages the performance of the partnership Project and monitor commercial operation.

- Manage various issues stemming from construction works in the construction stage.

- Conduct asset appraisal and management in the expiration of partnership agreement stage.

2) Risks to be Encountered for PPP Scheme

The types of risks in PPP projects for infrastructure provision are categorized as “political risk,” “project

performance risk” and “demand risk.” The executing agency and its supervisory ministry will be responsible for

checking and supervising the following aspects:

- Evaluation of Project feasibility and prioritization with regard to national development priorities are undertaken

by DOF and NEDA. DOTC and CPA shall prepare all documents carefully and assist DOF and NEDA to

clarify the all issues.

- Political Risk: To provide compensation to an asset owner/business enterprise based on a risk-sharing scheme

between the Government and Business Enterprise.

- Demand Risk: When demand becomes lower revenue than the minimum total revenues guaranteed by the

Government on which the agreement was based, extension of contract and/or other financial compensation may

be granted.

- If there is a delay of land acquisition or increase in land price, CPA will compensate the cost.

- If there is a delay in approval of commencement of commercial operation, delay in tariff adjustment and

changes, there will be an extension of contract and/or other financial compensation.

33

(8) Project Location Map

Figure 18 Location Map of the Project

(Source: Study Team)

Project Location

Chapter 1

Overview of Republic of Philippines and Port Sector

1 - 1

(1) Economic and Financial Conditions of Republic of Philippines

1) Population Changes in Past Years

This section describes the socio-economic conditions in the county and Central Visayas designated as Region

VII. The population in the Philippines was about 19 million in 1948, and it increased to about 88.5 million in

2007 (4.6 times). The annual average rate of population growth has fallen gradually from a peak of 3.08% for

the ten years from 1960 to 1970 to 2.04% from 2000 to 2007.

Table 1-1-1 Population Change in Past Years

Year 1948 1960 1970 1975 1980

Population 19,234,182 27,087,685 36,684,486 42,070,660 48,098,460

Growth Rate (%) 2.89% 3.08% 2.78% 2.71%

Year 1990 1995 2000 2007

Population 60,703,206 68,616,536 76,506,928 88,566,732

Growth Rate (%) 2.35% 2.32% 2.36% 2.04%

(Source: Philippine Statistical Yearbook 2000, 2010)

The population in 1980 in Central Visayas was less than 4 million but increased to about 6.4 million in 2007

(1.69 times) accounting for 7.2% of the Philippine population. The population growth rate of Central Visayas

from 1980 is less than the growth rate of the whole country except for the five years from 1995 to 2000.

Table 1-1-2 Change of Population Growth Rate by Region

Region 1980-1990 1990-1995 1995-2000 2000-2007NCR 2.98% 3.31% 1.06% 2.12%CAR 2.28% 1.71% 1.82% 1.50%Region 1 1.96% 1.30% 2.15% 1.10%Region 2 2.01% 1.52% 2.25% 1.13%Region 3 2.59% 2.13% 3.17% 2.35%Region 4 3.06% 3.55% 3.75% 2.92%Region 5 1.18% 1.91% 1.68% 1.22%Region 6 1.77% 1.30% 1.56% 1.35%Region 7 1.95% 1.66% 2.81% 1.59%Region 8 0.88% 1.84% 1.51% 1.12%Region 9 2.29% 2.75% 2.12% 1.83%Region 10 2.36% 2.44% 1.99% 1.67%Region 11 2.93% 2.17% 2.41% 1.72%Region 12 3.37% 3.25% 2.69% 2.41%Region 13 2.55% 1.82% 1.63% 1.25%ARMM 2.89% 2.46% 3.73% 5.46%Others - 3.66% 0.16% -3.04%Philippines 2.35% 2.32% 2.36% 2.04%

(Source: Philippine Statistical Yearbook 2010)

1 - 2

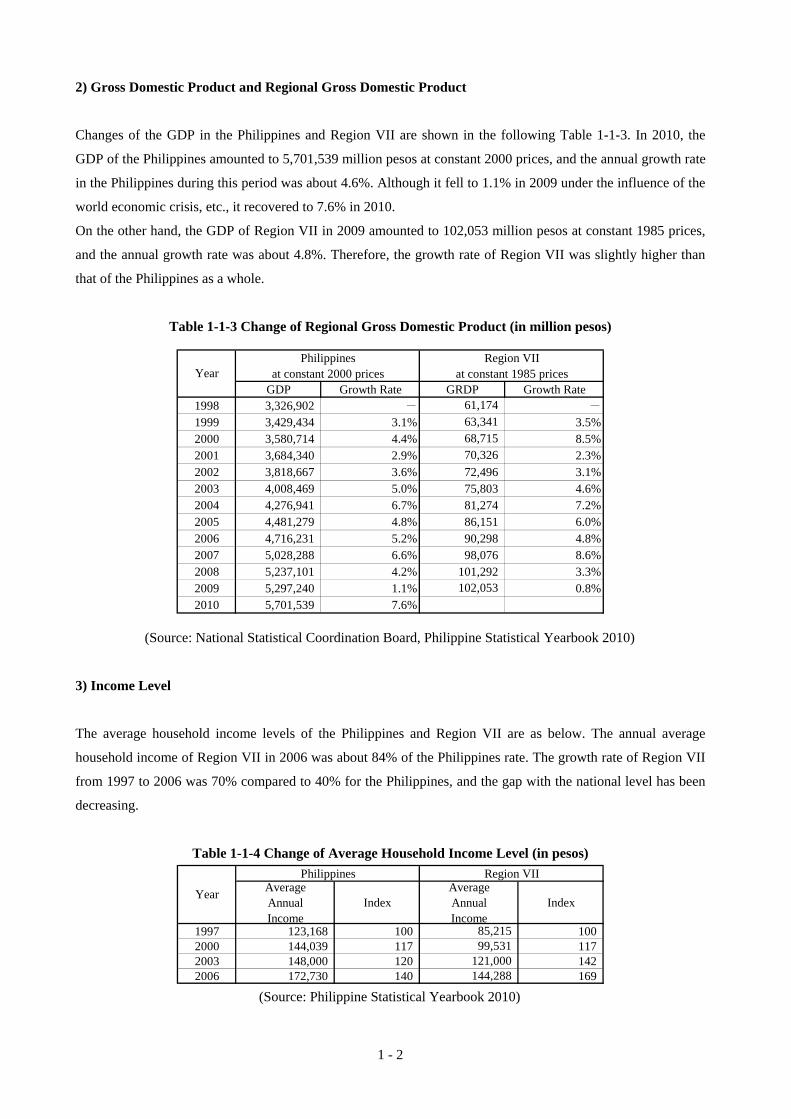

2) Gross Domestic Product and Regional Gross Domestic Product

Changes of the GDP in the Philippines and Region VII are shown in the following Table 1-1-3. In 2010, the

GDP of the Philippines amounted to 5,701,539 million pesos at constant 2000 prices, and the annual growth rate

in the Philippines during this period was about 4.6%. Although it fell to 1.1% in 2009 under the influence of the

world economic crisis, etc., it recovered to 7.6% in 2010.

On the other hand, the GDP of Region VII in 2009 amounted to 102,053 million pesos at constant 1985 prices,

and the annual growth rate was about 4.8%. Therefore, the growth rate of Region VII was slightly higher than

that of the Philippines as a whole.

Table 1-1-3 Change of Regional Gross Domestic Product (in million pesos)

Philippines Region VIIat constant 2000 prices at constant 1985 prices

GDP Growth Rate GRDP Growth Rate1998 3,326,902 - 61,174 -

1999 3,429,434 3.1% 63,341 3.5%2000 3,580,714 4.4% 68,715 8.5%2001 3,684,340 2.9% 70,326 2.3%2002 3,818,667 3.6% 72,496 3.1%2003 4,008,469 5.0% 75,803 4.6%2004 4,276,941 6.7% 81,274 7.2%2005 4,481,279 4.8% 86,151 6.0%2006 4,716,231 5.2% 90,298 4.8%2007 5,028,288 6.6% 98,076 8.6%2008 5,237,101 4.2% 101,292 3.3%2009 5,297,240 1.1% 102,053 0.8%2010 5,701,539 7.6%

Year

(Source: National Statistical Coordination Board, Philippine Statistical Yearbook 2010)

3) Income Level

The average household income levels of the Philippines and Region VII are as below. The annual average

household income of Region VII in 2006 was about 84% of the Philippines rate. The growth rate of Region VII

from 1997 to 2006 was 70% compared to 40% for the Philippines, and the gap with the national level has been

decreasing.