Embed Size (px)

Citation preview

IMPROVING THE SUPPLY CHAIN OF TILAPIA INDUSTRY IN THE PHILIPPINES

Wilfred E. Jamandre, Central Luzon State University (CLSU)

Upton Hatch, North Carolina State University (NCSU)

Remedios B. Bolivar, Central Luzon State University (CLSU)

Russell Borski, North Carolian State University (NCSU)

OBJECTIVES

1. Develop tilapia supply chain maps

2. Analyze tilapia supply chain performance

3. Identify areas for improvement in supply chain

4. Provide recommendations

METHODOLOGY

PROCESS INPUT OUTPUT

The Philippine Tilapia

Industry

Chain actors, key

activities and roles,

Flows of product,

information and

payments

Costs and margins

associated with each

practice

External influences

SCM

New Institutional

Economics:

Relationship Marketing

Operations

Management and

Logistics

Supply Chain Maps

Performance of tilapia

supply chain

Areas for improvement

in the supply chain

(Other recommendations)

STUDY AREAS AND COVERAGE

• Regions I, III, IV, CAR and NCR

• 5 hatchery and nursery operators

• 28 farmers

• 4 processors

• 24 traders/consolidators/shippers

• 11 institutional buyers

Routes of SC mapped Supply Chain Players Number of Respondents

Bicol-Laguna-Batangas-Manila-

Baguio (Chain 1):

Hatchery and Nursery Operators 3

Fish farmers 15

Processors 2

Traders/consolidators 8

Institutional buyers 5

Pampanga-Pangasinan-Ilocos and

Isabela - Baguio and Manila

(Chain 2):

Hatchery and Nursery Operators 2

Fish farmers 13

Processors 2

Traders/consolidators 16

Institutional buyers 6

DATA GATHERED

• key players, their roles/activities/services

• product grades and standards

• product, information and payment flows

• logistics issues

• production and marketing

• external influences

DATA PROCESSING AND ANALYSIS Objectives Methods of Analysis

(1) Provide an overview of the tilapia industry

Synthesis of relevant studies and trends

(2) Map out specific supply chains Flowchart analysis from downstream to upstream

(3) Analyze the performance of the supply chains

Descriptive statistics, and relevant performance metrics (qualitative and quantitative)

(4) Identify areas for improvement in the supply chain

(5) Provide specific policy recommendations

Results and Findings

HIGHLIGHTS OF THE PHILIPPINE TILAPIA INDUSTRY

• 12% of aquaculture GDP

• 1.4 million workforce and fish producers

• source of food and animal protein

• 3.81 kgs per capita consumption

• 10% average annual growth rate (2005-2008)

• 14% of the total food expenditure

BAS (2010) and Rodriguez et.al. (2009)

Tagaytay

HIGHLIGHTS OF THE PHILIPPINE TILAPIA INDUSTRY

• 258,663MT production (BAS 2010).

• 80% from Regions III and IV

• Top 5 provinces: – Pampanga (37.68%), Batangas (21.06%), Laguna (4.64%), Rizal

(4.06%) and Bulacan (3.58%).

• Culture environments: – 57% freshwater fishponds

– 38% freshwater fish cages

– 7% brackishwater fishpond

– 1% freshwater fishpen (BFAR, 2004)

HIGHLIGHTS OF THE PHILIPPINE TILAPIA INDUSTRY

• Types of tilapia: – Nile Tilapia

• 87% of total tilapia production in 2010 (BFAR, 2010)

– Mozambique tilapia – GET Excel

– GIFT - CLSU

– FAST

HIGHLIGHTS OF THE PHILIPPINE TILAPIA INDUSTRY

• Industry’s growth drivers: – genetic improvement

– stock management and cultural practices

• Market niches: – product forms - fillet, dried, whole fish

– outlets - supermarkets, food chains

Tagaytay

Hatchery

Operators

Nursery

Operators

Fish Producers

Small-scale

trader

Retailer

Improved

quality tilapia

Institutional

buyers

Ponds

Cages

Pens Supermarkets

Specialty shops

Food Chains

Restaurants

Bars, canteens, etc. Live Form

Fillet

Grilled

Barbecued

Specialty menus

Traders

(Wholesaler, Consignacion,

Viajero, Retailer)

Improved brood

stocks

End-users Processors

Live Form/Frozen

TILAPIA SUPPLY CHAIN MAJOR PLAYERS

KEY CUSTOMERS

• Institutional Buyers (Supermarkets, Specialty Shops, Food

Chains, Restaurants)

• Household consumers

PRODUCT FORMS

• Preferred by household customers

– live form tilapia

– size of 4-5 pieces per kg (200 - 250 g per fish)

– Northern Luzon markets prefer darker-skinned tilapia

– The common food recipes are charcoal grilled, fried, boiled and stew

• Preferred by hypermarkets – live form tilapia – size of 3-4 pieces per kg (250 – 350 g per fish)

PRODUCT FORMS

• Specialty shops and food chains in major urban centers – tilapia fillet (350 g per pack) – whole frozen fish (2-3 pieces per kg) – dried fish (100 g per pack or 30-35 g per fish) – by-products of filleting - fish soups, tilapia belly and deep

fried tilapia skin

PRODUCT FORMS

VOLUME REQUIREMENTS

• Major customers in Luzon

– 5,335 kg average daily or 1, 947,275 kg (or ~ 1,947.28MT) yearly

• Annual national consumption requirement:

– 323,850 MT (~ 1% )

MAJOR PLAYERS AND THEIR ACTIVITIES

• Processors

– Fillet, dried, whole, frozen and choice portions or trimmings

– Dressing recovery: • 1 kg raw tilapia (2-3 pieces) yields 30-35%

fillet, 18% belly, 25% innards, 21% head and 1% skin

MAJOR PLAYERS AND THEIR ACTIVITIES

• Wholesalers – shippers or viajeros

• Retailers – Resellers – Handle 100-150 kg of live form, daily

(5-6 pieces per kg)

MAJOR PLAYERS AND THEIR ACTIVITIES

Traders

- buy, sell and distribute

Consolidators

- Supply supermarkets

- Facilitators

- Price monitor

- Small-scale trading

- Gatekeepers

MAJOR PLAYERS AND THEIR ACTIVITIES

• Fish producers

– produce marketable tilapia

• 2.5 – 3 months (4-5 pieces per kg)

• 3.5-4.5 months (2-3 pieces per kg)

MAJOR PLAYERS AND THEIR ACTIVITIES

• Nursery operators • Maintain fry up to marketable

sizes:

- 22-20 on-season months (May, June, July, August)

- 14-12 off-season (September, October, November, December)

• Nile tilapia – better species

Bicol

MAJOR PLAYERS AND THEIR ACTIVITIES

• Hatchery operators

Supply fry and fingerlings (400 thousand fry every 18 days)

Provide techno-guides to fish producer – customers

Handle about 3,000 breeders • GIFT –CLSU, GET -Excel)

Maintain nursery ponds

MAJOR ROUTES

MAJOR ROUTES

Pampanga

Laguna

Batangas

Metro Manila

Angeles

Baguio City

Dagupan City

Cagayan

Valley

Cordillera

Administrative

Region

MAJOR SUPPLY

CENTERS

MAJOR

TRANSSHIPMENT

POINT

MAJOR DEMAND

CENTERS

Camarines Sur

Tilapia Fry

Isabela

Ilagan

La Union &

Ilocos Provinces

Fry

Hatcheries

Malabon

Marketable

fish

Marketable

fish

PRODUCT FLOW (BICOL-LAGUNA/BATANGAS-MANILA/BAGUIO ROUTE)

(frozen)

(live form)

FRY

FRY

(live form)

(frozen)

Hatchery/Nursery

Batangas

Hatchery

Nursery

Laguna

Hatchery

Camarines Sur

F

i

n

g

e

r

l

n

g

s

Cage operator

Batangas/Taal

Grow-out pond

Semi-intensive

Laguna/Rizal

Processors

3 months conditioning Consolidator/Trader

Trader Local market

(live form

Specialty shop - Monterrey

(Manila, Tuguegarao)

Fastfood shop

Supermarket

Trader

Wholesale shipper

“viajero”

Local market

(live form)

Central fish

market

(Malabon)

Local market

Supermarket

Manila

Pangasinan

Baguio

(live form)

(live form/frozen)

(live form)

(frozen)

(live form)

FRY/FINGERLINGS

- Direct stocking

Grow-out

pond

Pampanga

Central fish market

Dagupan

(live form)

Consolidator/T

rader

Local

market

Baguio

Supermarket

Pampanga

Manila

(live form) Ilocos

Isabela

Trader

(live form)

PRODUCT FLOW (PAMPANGA – PANGASINAN - BAGUIO ROUTE)

Hatchery/

Nursery

Pampanga

TILAPIA SUPPLY CHAIN: INFORMATION FLOW Hatchery

Nursery

Producers

Processor

Trader

/Consolidator

Wholesaler

/”Viajero”

Specialty

Shop

MARKETABLE SIZE

-Volume

-Price

-Weight

-Quality

Supermarket

Local market

-Source of fish

-Volume

-Delivery schedule

-Size

Wholesaler-Retailer

MARKETABLE SIZE

-Volume

-Delivery schedule

-Size

-Price

FINGERLINGS

-Quantity

-Delivery schedule

-Cost

-Strain/Sex

FRY

-Volume

-Delivery schedule

-Size

-Strain/Sex

Hatchery

Nursery

Producers

Processor

Trader/Consolidator

Wholesaler/”Viajero”

Specialty Shop

Supermarket

Local

market

Wholesaler-

Retailer

Terminal Market

CASH

CASH

Cash, net after feed

loan (1-2 days)

CASH

Producers

(non feed-borrowers)

Trader/Retailer

(small-scale)

Sales remittances, net

after trading capital

CASH

Advanced cash

Post-dated

checks,7 days

Retailer

Sales remittances

CASH

Cash

Cash

CASH

TILAPIA SUPPLY CHAIN: PAYMENT FLOW

CASH

MAJOR CONCERNS TRANSACTION COSTS

HATCHERIES/ NURSERIES

FISH FARMERS

• High cost of outbound logistics

• High competition with mixed sex fingerlings

• High mortality rates

• Expensive inputs • Mislabeld inputs

• Low fish recovery - 25% in lakes and

cages/pens - 60% in pond systems

• Unpredictable climate patterns

•Overstocking

• Prolonged grow-out period (8-10 months )

• Lack of cold storage facilities

FISH FARMERS

• Cost of waiting •Harvest delays

• Limited opportunities for value-adding & processing

• 4% shrinkage allowance required by traders

HATCHERIES/ NURSERIES

• In-transit mortality losses • Toll fees (“goodwill”)

MAJOR CONCERNS TRADERS

• “Uncalibrated” weighing scale of fish farmers

• Disrupted delivery schedules due to defaulting “contract growers”

• Lag responses to price changes

• Absence of product grades and standards

TRADERS

• High logistics and transaction costs:

• Search

• Assembly

• Distribution

TRANSACTION COSTS

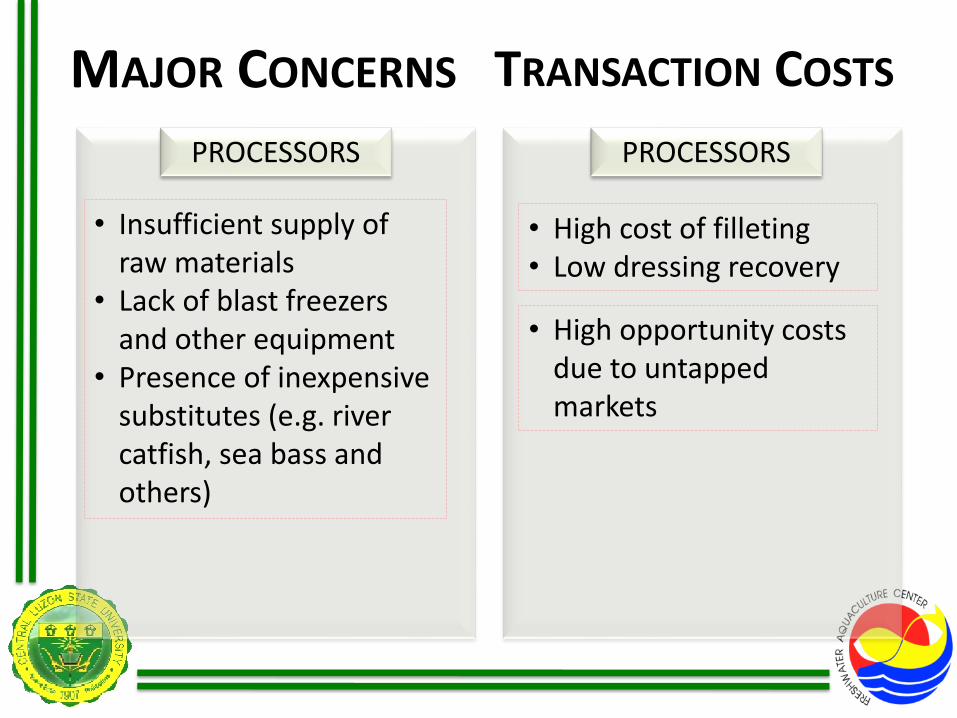

MAJOR CONCERNS

PROCESSORS

• Insufficient supply of raw materials

• Lack of blast freezers and other equipment

• Presence of inexpensive substitutes (e.g. river catfish, sea bass and others)

• High opportunity costs due to untapped markets

TRANSACTION COSTS

• High cost of filleting • Low dressing recovery

PROCESSORS

MAJOR CONCERNS

INSTITUTIONAL BUYERS

• Off-season stock-outs from regular suppliers

TRANSACTION COSTS

• High cost of product search

• High opportunity cost

INSTITUTIONAL BUYERS

RECOMMENDATIONS

(1) Encourage the establishment of more nursery and hatchery farms

(2) Conduct market promotion

(3) Motivate participation of small farmers in supply chains

(4) Institutionalize an accreditation/certification program for feed manufacturers, hatcheries and processors

(5) Strengthen farmers’ organizations

Thank you.

Funding for this research was provided by the

COLLABORATIVE RESEARCH SUPPORT

PROGRAM

The AquaFish CRSP is funded in part by United States Agency for International Development (USAID) Cooperative Agreement No. EPP-A-00-06-00012-00 and by US and Host Country partners.

The contents of this presentation do not necessarily represent an official position or policy of the United States Agency for International Development

(USAID). Mention of trade names or commercial products in this presentation does not constitute endorsement or recommendation for use on the part of USAID or the AquaFish Collaborative Research Support Program. The accuracy, reliability,

and originality of the work presented are the responsibility of the individual authors.

MARKET REQUIREMENTS FOR TILAPIA Specialty shops Supermarkets

Description Size (g/pc) Volume (kg/day)

Price (PhP/kg)

Size (g/pc) Volume (kg/day)

Price (PhP/kg)

Live form

Large 400-500 100 83 400-500 1000 112

Medium 300-400 100 77 300-400 1000 95

Fish fillet 250 -350 any amount 280 250 -350 g/pack any amount 312

Smoked 250-350g/pack any amount 209 250-350 g/pack any amount 330

Dried 30 any amount 150 X X X

Butterfly

fillet 70 any amount 250 X X X

Fillet by-products: X X X

Head I kg any amount 30 X X X

Belly I kg any amount 50 X X X

Skin I kg any amount 350 X X X

TILAPIA SUPPLY AND UTILIZATION ACCOUNTS

SUPPLY (MT) UTILIZATION (MT) CONSUMPTION

Production Imports Gross Supply Exports

Feeds

and Waste

Processing

Net Food Disposable

Per Capita

kg/yr

Per Capita

g/day

2001 135,627 0 135,627 0 4,069 0 131,558 1.69 4.63

2002 152,985 0 152,985 0 4,590 0 148,395 1.87 5.12

2003 168,132 0 168,132 0 5,044 0 163,088 2.01 5.51

2004 177,790 0 177,790 0 5,334 0 172,456 2.09 5.73

2005 195,504 0 195,504 0 5,865 0 189,639 2.22 6.08

2006 241,775 0 241,775 0 7,253 0 234,522 2.7 7.4

2007 278,819 20 278,839 52 8,365 0 270,422 3.05 8.36

2008 299,813 20 299,833 300 8,994 0 290,539 3.21 8.79 Source: Bureau of Agricultural Statistics, 2009

RETAIL AND WHOLESALE PRICES SPREADS, MEANS AND COVARIATIONS, 2001-2008

Month Prices Covariation

Retail Wholesale R-W Spread Retail (%) Wholesale

(%)

R-W Spread

(%)

January 66.04 50.61 15.42 12.30 12.60 16.61

February 65.20 50.96 14.25 13.55 12.81 19.53

March 65.59 49.99 15.60 12.41 11.86 17.82

April 66.00 49.70 16.29 11.44 12.54 15.31

May 65.97 49.99 15.98 11.33 12.19 12.77

June 66.67 51.45 15.22 10.48 9.68 22.40

July 67.71 51.97 15.73 11.18 10.26 28.60

August 68.18 52.39 15.78 11.62 13.30 7.44

September 68.29 51.79 16.50 12.68 15.72 7.71

October 68.59 52.04 16.56 12.99 16.52 11.01

November 68.23 51.79 16.44 13.52 15.69 9.38

December 69.76 54.70 15.06 13.51 16.29 10.02

Means 67.18 51.45 15.74 12.25 13.29 14.88 Source: Bureau of Agricultural Statistics, Department of Agriculture (Various Issues)

VALUE OF TILAPIA PRODUCTION

1991-1999 Mean 55.2777778 Standard Error 2.6509143 Median 57.02 Mode #N/A Standard Deviation 7.95274289 Sample Variance 63.2461194 Kurtosis 1.35249253 Skewness -0.5399786 Range 28.49 Minimum 39.78 Maximum 68.27 Sum 497.5 Count 9 covariation 14.39%

2000-2008 Mean 66.2111111 Standard Error 2.70703941 Median 67.38 Mode #N/A Standard Deviation 8.12111822 Sample Variance 65.9525611 Kurtosis -0.94247877 Skewness 0.49269906 Range 22.69 Minimum 57.71 Maximum 80.4 Sum 595.9 Count 9

12.27%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Mean SD Covariation

1990 45.12 46.05 42.02 63.67 42.42 42.32 41.90 41.76 39.75 39.63 43.88 44.54 44.42 6.37 14.34 1991 49.62 48.66 50.76 51.51 50.05 50.99 50.09 50.15 50.05 48.46 48.99 48.74 49.84 0.98 1.96 1992 65.93 63.21 64.02 64.99 63.46 63.19 60.38 59.94 57.71 53.98 59.72 59.81 61.36 3.41 5.56 1993 67.74 69.76 68.10 68.60 60.02 64.00 62.53 60.90 58.86 59.58 60.27 61.65 63.50 3.99 6.29 1994 72.49 75.98 75.39 75.12 73.90 73.66 68.46 67.07 65.30 62.86 65.74 65.82 70.15 4.72 6.73 1995 77.84 80.47 77.60 78.93 75.64 73.04 69.10 66.77 64.36 61.42 63.61 65.47 71.19 6.81 9.57 1996 77.41 76.09 75.72 78.25 74.46 75.09 72.40 69.62 66.93 65.50 67.41 67.35 72.19 4.58 6.34 1997 75.77 77.86 78.79 79.82 78.43 77.61 72.26 70.48 66.75 66.04 66.91 67.67 73.20 5.40 7.38 1998 76.29 74.56 74.68 79.62 78.10 76.71 73.05 69.57 68.15 69.07 73.84 78.32 74.33 3.79 5.10 1999 96.44 98.69 98.02 95.41 103.59 87.80 82.86 78.28 74.89 71.35 71.10 71.20 85.80 12.30 14.33 2000 81.68 80.12 79.40 80.29 78.14 76.40 71.44 69.25 66.85 65.23 65.82 64.56 73.27 6.71 9.16 2001 72.80 73.71 71.72 78.99 77.40 77.61 75.35 74.81 71.36 70.09 69.78 70.59 73.68 3.15 4.28 2002 77.16 68.77 75.39 74.93 74.46 75.51 73.11 72.07 69.76 69.42 68.06 67.66 72.19 3.33 4.62 2003 75.95 75.84 73.96 74.92 73.99 75.54 73.03 71.74 70.62 70.88 71.17 70.96 73.22 2.08 2.84 2004 82.28 84.07 86.72 89.56 88.86 88.44 85.34 83.05 80.01 81.66 79.05 78.60 83.97 3.84 4.57 2005 91.36 90.79 90.55 91.28 88.69 89.73 85.04 83.68 81.25 81.25 81.86 81.57 86.42 4.34 5.02 2006 92.89 92.24 90.67 92.91 90.00 87.22 86.05 85.39 83.46 83.67 84.65 85.27 87.87 3.64 4.15 2007 98.30 97.25 95.50 98.00 95.32 93.83 89.94 89.09 86.92 87.62 88.81 88.50 92.42 4.35 4.70 2008 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 100.00 Mean 77.74 77.59 77.32 79.83 77.21 76.25 73.28 71.77 69.63 68.83 70.04 70.44

SD 14.67 14.89 14.90 12.61 15.72 14.12 13.71 13.53 13.53 14.09 13.19 13.15 Covariation

18.87 19.19 19.27 15.79 20.36 18.52 18.71 18.85 19.43 20.47 18.83 18.66

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Mean SD

covariation

1990 34.51 35.19 32.21 47.98 32.51 32.81 33.98 34.52 33.75 33.74 37.23 38.65 35.59 4.33 0.12 1991 37.95 37.18 38.91 38.82 38.35 39.53 40.62 41.45 42.50 41.25 41.56 42.29 40.03 1.80 0.04 1992 50.42 48.30 49.07 48.98 48.63 48.99 48.97 49.55 49.00 45.95 50.67 51.90 49.20 1.44 0.03 1993 51.81 53.30 52.20 51.70 45.99 49.62 50.71 50.34 49.98 50.72 51.13 53.49 50.92 1.97 0.04 1994 55.44 58.06 57.79 56.61 56.63 57.11 55.52 55.44 55.45 53.51 55.77 57.11 56.20 1.26 0.02 1995 59.53 61.49 59.48 59.48 57.96 56.63 56.04 55.19 54.65 52.29 53.97 56.81 56.96 2.71 0.05 1996 59.20 58.14 58.04 58.97 57.06 58.22 58.72 57.55 56.83 55.76 57.19 58.44 57.84 1.00 0.02 1997 57.95 59.49 60.39 60.15 60.10 60.17 58.60 58.26 56.68 56.22 56.77 58.72 58.63 1.49 0.03 1998 58.35 56.97 57.24 60.00 59.85 59.47 59.24 57.51 57.87 58.80 62.65 67.96 59.66 3.04 0.05 1999 73.76 75.41 75.13 71.90 79.38 68.07 67.20 64.71 63.59 60.74 60.32 61.78 68.50 6.48 0.09 2000 62.47 61.22 60.86 60.51 59.88 59.23 57.94 57.24 56.76 55.53 55.84 56.02 58.63 2.37 0.04 2001 55.68 56.32 54.97 59.53 59.31 60.17 61.11 61.84 60.59 59.67 59.20 61.25 59.14 2.27 0.04 2002 59.01 52.55 57.79 56.47 57.06 58.54 59.29 59.57 59.23 59.10 57.74 58.71 57.92 1.95 0.03 2003 58.09 57.95 56.69 56.46 56.70 58.57 59.23 59.30 59.96 60.34 60.38 61.57 58.77 1.65 0.03 2004 62.93 64.24 66.47 67.49 68.09 68.57 69.21 68.65 67.94 69.52 67.07 68.20 67.37 1.98 0.03 2005 69.87 69.37 69.41 68.79 67.96 69.57 68.97 69.17 68.99 69.17 69.45 70.78 69.29 0.67 0.01 2006 71.04 70.48 69.50 70.02 68.97 67.62 69.79 70.58 70.87 71.23 71.82 73.99 70.49 1.57 0.02 2007 75.18 74.31 73.2 73.85 73.04 72.75 72.94 73.64 73.8 74.59 75.35 76.79 74.12 1.20 0.02 2008 76.48 76.41 76.65 75.36 76.63 77.53 81.1 82.66 84.91 85.13 84.84 86.77 80.37 4.28 0.05

Mean 59.46 59.28 59.26 60.16 59.16 59.11 59.43 59.32 59.12 58.59 59.42 61.12 SD 11.22 11.38 11.42 9.50 12.05 10.95 11.12 11.18 11.49 11.99 11.19 11.41 Covariation

0.19 0.19 0.19 0.16 0.20 0.19 0.19 0.19 0.19 0.20 0.19 0.19

TILAPIA AVERAGE RETAIL PRICES (NOMINAL), 1990-2008

END

CONSIGNACION

Dagupan and Malabon

TRADERS

Wholesaler/Viajero Retailer

FISH FARMS

Laguna

Batangas

• Bicol

PRODUCT FLOW

HATCHERY

NURSERY

FARMS

18 days fry

COMMERCIAL

FARMS

BACKYARD

FARMS CONSOLIDATOR

30-45 days

fingerlings

Grow-out periods

• 2.5 - 3 months

• 3.5-4.5 months

MANILA MARKET

DISTRIBUTION ARM

INSTITUTIONAL ACCOUNTS CONSUMERS

Fishcage operators

Laguna –Batangas

live form (250 – 300 g/fish or 4-5

pieces/kg)

Tilapia fillet (450 – 750 g/fish

or 2-3 pieces/kg

Department

store

Wet

market

Malabon / Navotas

consignacion

WHOLESALER