Embed Size (px)

Citation preview

0

IMPLEMENTING TALLY SHEETS INTERNAL PAY EQUITY AUDITS AND OTHER ESSENTIAL TOOLS

Jesse Brill, Moderator - NASPP

Douglas Friske - Towers Perrin

Myrna Hellerman - Sibson Consulting

Michael S. Kesner -Deloitte Consulting LLP

Joseph Rich - Pearl Meyer & Partners

1

Discuss the challenges of responsible management of executive pay

Describe Tally Sheets, Internal Pay Equity Audits and Accumulated and Future Realizable Wealth Calculations and their role in an evolving framework of responsible analyses and actions to restore (establish?) sound governance and decision making, fiscal responsibility, and transparency with respect to executive pay

Objectives for Today’s Discussion

EvolvingFrameworks

Discussion

The Obviousand Beyond

Discuss how you can make these tools actionable inside of YOUR company

2

TALLY SHEETS (go to Tally Sheets will evolve document)

3

… more on TALLY SHEETS(no visuals for Mike Kesner Presentation)

4

INTERNAL PAY EQUITY AUDIT

5

The “Holy Cow” moments caused by Tally Sheets have raised important questions…

How much is enough?

What’s fair and equitable? To/For whom?

How did this happen? Who’s responsible?

6

The “fairness” question is influenced by what is going on inside our companies -- cost risk has been passed like a “hot potato” to everyone, EXCEPT THOSE AT THE TOP

ToMeritocracy

Variable pay

Welfare self-management

Consumer education

Defined contribution

Self-service

Employability

FromEntitlement

Fixed pay

Welfare security

Indemnity coverage

Defined benefit

Full service

Employment security

Everyone Else

6

Top Executives

Economic and Employment Security

7

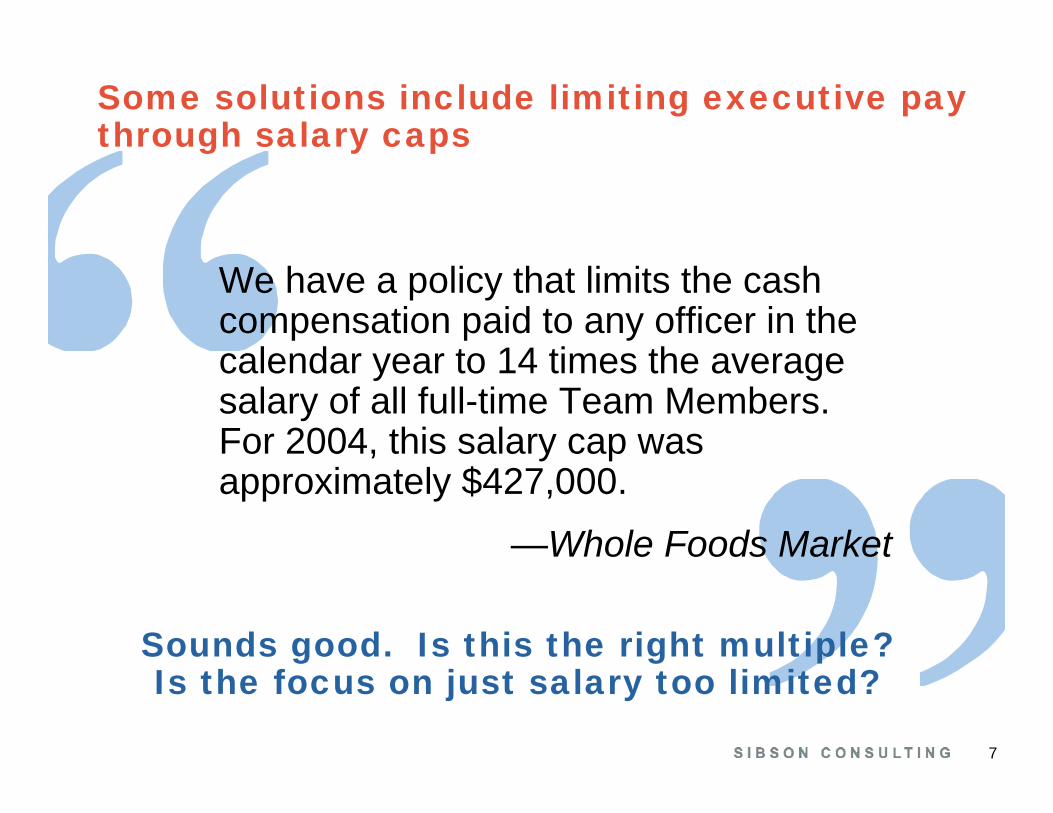

Some solutions include limiting executive pay through salary caps

We have a policy that limits the cash compensation paid to any officer in the calendar year to 14 times the average salary of all full-time Team Members. For 2004, this salary cap was approximately $427,000.

—Whole Foods Market

Sounds good. Is this the right multiple?Is the focus on just salary too limited?

8

Salary caps don’t tell the whole story about the “fairness” of an executive’s pay…

John P. Mackey, Chairman & CEO, Whole FoodsIn 2004, John P. Mackey raked in $885,216 in total compensation including stock option grants from Whole Foods Market.

From previous years’ stock grants the Whole Foods Market executive cashed out $1,013,893 in stock option exercises.

And, John P. Mackey has another $4,370,735 in unexercised stock options from previous years.

—AFL-CIO Executive Pay Watch Database

Is this package still “fair”and internally equitable?

9

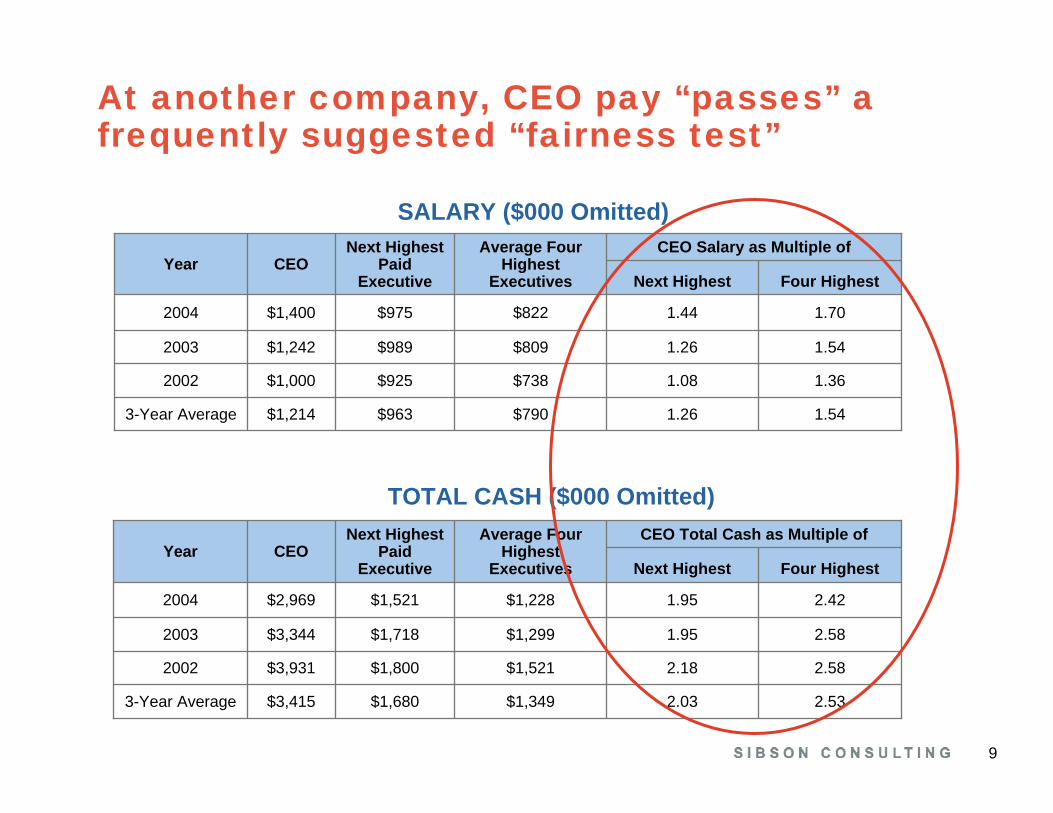

At another company, CEO pay “passes” a frequently suggested “fairness test”

3-Year Average

2002

2003

2004

Year

$1,214

$1,000

$1,242

$1,400

CEO

1.541.26$790$963

1.361.08$738$925

1.541.26$809$989

1.701.44$822$975

Four HighestNext Highest

Next Highest Paid

Executive

CEO Salary as Multiple ofAverage Four Highest

Executives

3-Year Average

2002

2003

2004

Year

$3,415

$3,931

$3,344

$2,969

CEO

2.532.03$1,349$1,680

2.582.18$1,521$1,800

2.581.95$1,299$1,718

2.421.95$1,228$1,521

Four HighestNext Highest

Next Highest Paid

Executive

CEO Total Cash as Multiple ofAverage Four Highest

Executives

SALARY ($000 Omitted)

TOTAL CASH ($000 Omitted)

10

Even looking at all cash payments plus grant date PV of equity, the “fairness test” is met

Is this package still “fair”and internally equitable?

How much more is there in the economic package?

2.002.00$330$330$660Grant Date PV Restricted Shares

Total

Grant Date PV Options

Other Cash

Total Cash

Compensation Components

$8,106

$4,342

$135

$2,969

CEO

2.231.60$3,634$5,062

2.151.40$2,016$3,102

2.261.24$60$109

2.421.95$1,228$1,521

Four HighestNext

Highest

Next Highest Paid

Executive

CEO Total as Multiple ofAverage Four Highest Executives

2004 ALL CASH PAYMENTS PLUS EQUITY(Grant Date PV) ($000 Omitted)

11

…YES, there’s more … for the CEO

…and for others

12

What happened at H-P has happened at many companies. A rewards package like this…

ALPHA CORP 1995 PAY PROGRAM (Excerpt)

StaffManagementExecutivesSenior Executives

Program

Cash

Equity

CEO 4 Proxy EVP

Base Salary

SVP VPs Director Mgr Other Exempt

Annual Incentive

Pension

Enhanced Pension

Stock Options

Other

13

Over time became a rewards package like this…

StaffManagementExecutivesSenior Executives

Program

Cash

Equity

CEO 4 Proxy EVP

Base Salary

SVP VP Director Mgr Other Exempt

Annual Incentive

Long-Term Cash

Pension

Enhanced Pension

Stock Options

Restricted Stock

Severance/COC

Other

Discretionary Cash Award

Discretionary Awards

Matched Deferral

Special Grants

ALPHA CORP 2005 PAY PROGRAM (Excerpt)

14

…And the accumulated financial exposure associated with a (never expected) “breakup”had not been made transparent to shareholders

15

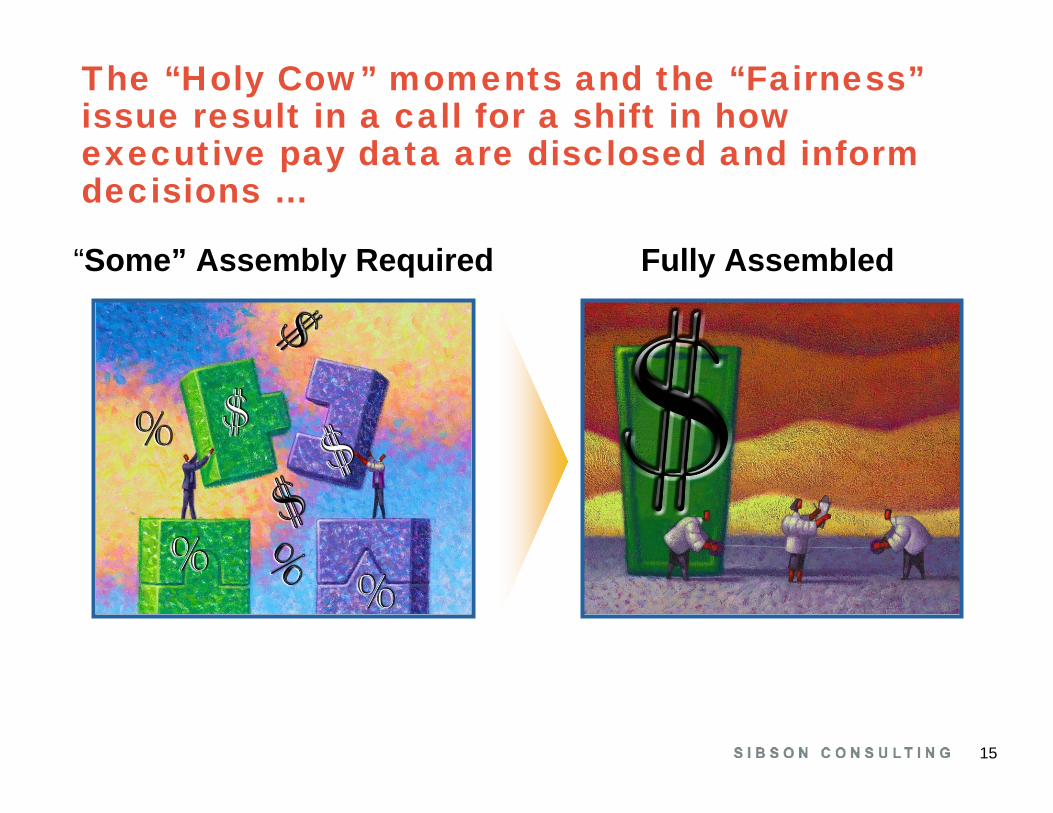

The “Holy Cow” moments and the “Fairness”issue result in a call for a shift in how executive pay data are disclosed and inform decisions …

“Some” Assembly Required Fully Assembled

16

“Some” Assembly Required Fully Assembled

…and unambiguous accountability

17

Evolving tools provide the data needed by the Board/Compensation Committee to step up to this stewardship responsibility

Internal Equity Audit. Documents the historical evolution of the components of the total economic package provided by the company to its CEO and to each of its (key) employee segments

Specifically: How and why has the differential between the total rewards paid (and payable) to the CEO and other executive and employee levels changed over time?

Tally Sheet. Documents the value of the total economic package provided (past and current) and the potential liability for the economic package to be provided in the future

Accumulated and Future Realizable Wealth Calculations.

18

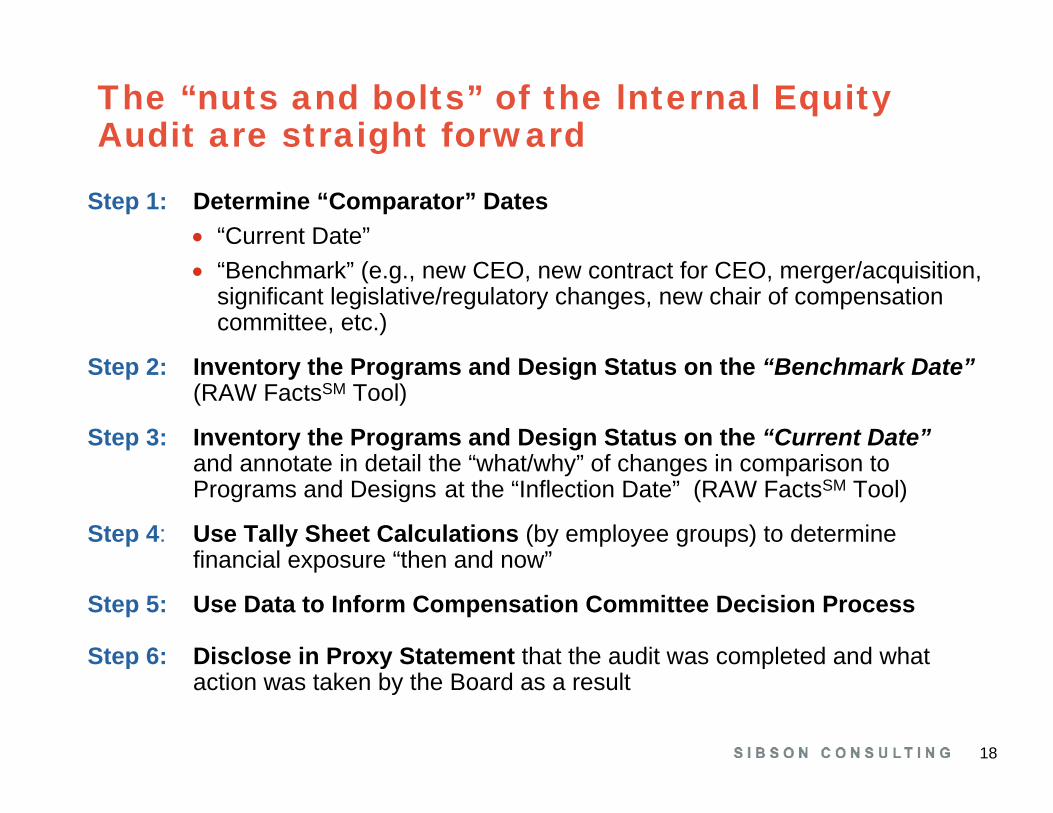

The “nuts and bolts” of the lnternal Equity Audit are straight forward

Step 1: Determine “Comparator” Dates• “Current Date”• “Benchmark” (e.g., new CEO, new contract for CEO, merger/acquisition,

significant legislative/regulatory changes, new chair of compensation committee, etc.)

Step 2: Inventory the Programs and Design Status on the “Benchmark Date”(RAW FactsSM Tool)

Step 3: Inventory the Programs and Design Status on the “Current Date”and annotate in detail the “what/why” of changes in comparison to Programs and Designs at the “Inflection Date” (RAW FactsSM Tool)

Step 4: Use Tally Sheet Calculations (by employee groups) to determine financial exposure “then and now”

Step 5: Use Data to Inform Compensation Committee Decision Process

Step 6: Disclose in Proxy Statement that the audit was completed and what action was taken by the Board as a result

19

Organization of the Internal Equity Audit Tool

Divides fact finding process into three “timeframes”

• Entry “Fees” programs and policies that come into play when there is a new entrant to the organization

• Cost of Maintenance programs and policies that impact the employee during his/her active employment

• Exit “Fees” programs and policies that deliver post-termination compensation and benefits

Within each “timeframe” identifies (a) the existence of a given program and (b) key design characteristics

Identifies the eligibility by distinct employee groups for a given program or design feature

Identifies what has changed since the prior evaluation period

20

Current Date

Prior Evaluation Date

Compensation Committee Members (Name, Affiliation) 1

Other Board Committees with Governance Rights over Rewards (Stock Plan, Benefits Plan, Succession) Employee Group

CEO 20 Next Highest Paid Executives

Group #1

Group #2 Change1 Comments

Number of Employees

Employment Contract Change of Control Protection Severance Protection “Parachute” Cash Signing Grant Welcome Equity Grant Prior Er Equity Buy-outs Relocation Allowance Perquisite Allowance Other

Other

1st Year AI Guarantee LTI Guarantee Service/Vesting Enhancement Tax Gross-ups Other Other

Other

Prog

ram

s

Entry

“Fee

s”

Desig

n

Gove

rnan

ce

1 Check circle if different from prior evaluation.

211 Check circle if different from prior evaluation.2 As a percent of base salary.

Employee Group

CEO 20 Next Highest Paid Executives

Group #1

Group #2 Change1 Comments

Base Salary Annual Variable Pay Commissions Current Dividends (e.g., on deferred RS)

Deferral of Base Salary/Bonus Other

Vacation Supplemental Sick/Disability Supplemental Health Care Perquisite Allowance Car Allowance Financial Counseling Tax Preparation Other Transportation Club Membership Supplemental Benefits

Other

Total Cash Comp Mix (Base/AI) Base/AI Pay Positioning AI Range2 (threshold, target, max) Annual Incentive (AI) Metrics Base Salary Increase Guarantee Match on Deferred Base Salary/AI Tax Gross-ups

Other

Prog

ram

s

Cost

of M

ainte

nanc

e (An

nual

Cash

)

Desig

n

22

1 Check circle if different from prior evaluation.2 TDC = Total Direct Comp (Base + Annual Incentive + Long-Term Incentive).3 As a percent of base salary.

Employee Group

CEO 20 Next Highest Paid Executives

Group #1

Group #2 Change1 Comments

Cash Settled LTI Carried Interest Deferral of Cash LTI Other Other

Incentive Stock Options NQSO RS (time) RS (performance) Performance Units SARs Other

Other

TDC2 Mix (Base/AI/LTI) TDC Positioning LTI Range3 (threshold, target, max) LTI Metrics Cashless Exercise Match on Deferred LTI Tax Gross-ups Front-loaded Equity Grants Ownership Guidelines Require Equity Hold to Ret. Dividend Deferral

Other

Prog

ram

s

Cost

of M

ainte

nanc

e (Lo

ng-T

erm

Cas

h/Eq

uity

)

Desig

n

23

1 Check circle if different from prior evaluation.2 As a percent of base salary.

Employee Group

CEO 20 Next Highest Paid Executives

Group #1

Group #2 Change 1 Comments

DB Qualified Pension Frozen DB Pension DB SERP 401(k) SERP/401(k) Profit Sharing Savings Plan AI / LTI Payouts Stock Plan Deferred Cash/Dividends Change of Control Severance “Parachute” Benefit Continuation Other

Other

DB Target Benefit Amount 2

Enhanced DB SERP Amount 2

401(k) Match/Maximum Match

DC SERP

Match on Deferred Cash

Interest on Def Cash/Dividends

Tax Gross-ups

Accelerated Vesting

Enhanced Exercise Period

Prog

ram

s De

sign

Exit

“Fee

s”

24

In partnership with the other essential tools, the Internal Pay Equity Audit serves to “corral”relevant facts about executive pay…but needs to be applied within the context of several guiding principles

25

1. Seek no “magic multiples” or specific financial comparisons that establish a “safe harbor” for executive pay levels and designs

…and the survey says…

26

2. Broaden definition of “executive” and “pay” and “economic impact”

27

TOTAL

Compensation Component

Other2

Annual Incentive CashLong-Term Incentive Cash PaidEquity Grant Date PV• Plan #1• Plan #2• Plan #3

Salary

Cash Amounts DeferredMatches (e.g., Sup 401(k), on deferred amounts)

Benchmark YearCurrent YearBenchmark YearCurrent YearCEO

Benchmark YearCurrent Year

20 Next HighestPaid Executives1

TOTAL AS A % OF FULLY DILUTED EARNINGS

• Credited/Reinvested• Paid CurrentlyDividends

CEO as Multiple of20 Next Highest Paid Executives

ANNUAL EXECUTIVE “COST OF MAINTENANCE”

1 Footnote to include names of 20 individuals included in the top 20.2 Includes all W-2 items (e.g., financial counseling, tax preparation, company provided transportation, facilities for personal use at net operating cost, perk

allowance, car allowance, clubs, gross ups, other reimbursements, etc.). Also includes director’s fees from company or affiliated entities and payments related to special arrangements between company and executive.

3. Act as if proxy disclosure was required

28

Benchmark YearCurrent YearCompensation Component

TOTAL

PV of Other Welfare Benefits/InsurancePV of Other Compensation Continuation/Commitment

Company Lost Deductions

PV Defined Benefit (Pension + SERP)Defined Contribution (e.g., 401k + SERP)Other Savings/Profit SharingDeferred Cash + MatchesEquity Payouts• Plan #1

Severance Pay [e.g., PV of (base + bonus) x # years]

• Plan #2• Plan #3

PV Amounts Payable

TOTAL AS A % OF FULLY DILUTED EARNINGS

PV Welfare Benefit Commitments

Gross-up Payments

CEO “EXIT FEES”1

3. Act as if proxy disclosure was required continued

1 Company’s financial exposure if CEO terminated at end of fiscal year under the most favorable conditions for the executive.

29

?

4. Make compensation decisions informed by a thorough understanding of how/why compensation plans and their associated costs have evolved over time

ExecutivesSenior ExecutivesProgram

Cash

Equity

CEO 4 Proxy EVP

Base Salary

SVP VPs

Annual Incentive

Pension

Enhanced Pension

Stock Options

Other

ExecutivesSenior ExecutivesCEO 4 Proxy EVP

Base Salary

SVP VP

Annual Incentive

Long-Term Cash

Pension

Enhanced Pension

Stock Options

Restricted Stock

Severance/COC

Matched Deferral

Special Grants

30

“Some” Assembly Required Fully Assembled

5. Unambiguously disclose decisions

31

ACCUMULATED AND FUTURE REALIZABLE WEALTH CALCULATIONS

(go to NASPP Tools Panel document)

32