Embed Size (px)

Citation preview

(IMPACT OF FORTIGN INSTITUTIONAL INVESTORS ON INDIAN MARKET)

1

2

PREFACE

The Indian capital markets may appear mysterious and puzzling to many foreign

investors and even to domestic Indian investor. To my knowledge, however, there is no

current information material that comprehensively addresses invertors’ concerns about

this rapidly growing market. I have no power to solve its inherent problems; but what I

have tried to do is shed some light on practices and rules in the Indian market, including

problematic ones, so that foreign as well as Indian investors can look at the market more

rationally for their portfolio investments in Indian securities.

The Indian financial system is a vast universe. This universe is regulated and supervised

by two government agencies under the Ministry of Finance.

(i). The Reserve bank of India, India’s Central Bank, and

(ii). The Securities Exchange Board of India, the country’s capital market regulator.

All parts of the system are interconnected with one another, and the jurisdictions of the

central bank and the capital market regulator overlap in some fields of Indian financial

activities. This research focuses on the FII (foreign institutional investor) flows to Indian

capital market, its portfolio investment and determinants of investing in Indian market

and deciding the portfolio preferences. This research also gives the suggestions on the

investment avenues available for the FII in Indian with the help of Gap analysis.

The Indian capital market changes amazingly quickly. Some part of this research may be

out-of-date by the time of completion. Therefore, please do not assume that the

information in this research continues to be correct or remains unchanged. This research

is originally focused on foreign investor and its role and impact on Indian capital market.

3

SYNOPSIS

TITLE OF THE PROJECT: - Foreign institutional investors and Indian capital

market (its determinants and avenues of investment).

OBJECTIVE OF THE RESEARCH: - To study the role and impact foreign institutional

investor on Indian capital market and find out the factors that determines the flow of FIIs.

CHAPTER 1: INTRODUCTION

Since the beginning of the liberalization of investment policies. Flows FIIs in India

steadily grown in importance. Paper covers the flow of FII in India and their relationship

with other economic variables. In this paper I’m particularly covering the relationship

between FII and stock market. It covers the investment trend of FII and the various

issues related to the FII investment in the domestic market.

BACKGROUND: -

The national common minimum programmed of the present UPA government envisages policies, which encourage foreign institution investors (FIIs), but reduce exposure to the Indian financial system to speculative capital flows

An FII means an entity established or incorporated outside India, which proposes to

undertake investment in India; while an FII sub-account includes those foreign corporate,

foreign individuals, institutions, funds or portfolios established or incorporated outside

India on whose behalf investments are proposed to be made in India by an FII

4

CHAPTER II: RESEARCH METHODOLOGY

Research is often described as active; diligent and systematic process of inquiry aimed at

discovering, interpreting and revising facts. This intellectual investigation produces a

greater understanding of events, behaviors or theories and makes practical application

through laws and theories. In other words we can say, the purpose of research is to

discover answers to the questions through the application of scientific procedures. The

main aim of research is to find out the truth which is hidden and which has not been

discovered as yet.

Research methodology is a way to systematically solve the research problem. It may be

understood as a science of studying how research is done scientifically. In it we study the

various steps that are generally adopted by a researcher in studying his research problem

along with the logic behind them.

OBJECTIVE: -The main objective of the research is to show that Supply Chain

Management is the key tool in the brand building of any company. Especially in the

sectors like retailing, FMCG, consumer durables etc. it is the key differentiator among

strong brands and weak brands.

To carry out my project I have used the exploratory research.

Exploratory research includes surveys and fact-finding enquiries of different kinds. The

major purpose of exploratory research is to explore the facts which are existing but new

for everyone.The main characteristic of this method is that the researcher has no control

over the variables; he can only report what has happened or what is happening. It is also

called as ex post facto research. Most ex post facto research projects are used for

descriptive studies in which researcher seeks to measure such items as, for example,

frequency of shopping, preferences of people, or similar data.

DATA SOURCE: - To carry out the project work I have consulted the various secondary

sources of data such as Magazines, Journals and websites.

SCOPE OF THE STUDY: - The research will be covering whole capital market and

investment made by FIIs. This research is helpful for investors who made the large

investment in the market and too much bothered about the volatility because of FII.

5

CHAPTER IV: DESCRIPTIVE WORK

The subtopics, which will be covered as a part of the study can be given in the following

points:

Flow of FII in India.

Regulatory information about FII.

Liberalization of foreign investment policy.

Flow of FII: its nature and causes.

Determinants of flow of FII.

CHAPTER III: DATA ANALYSIS AND INTERPRETATION

To analyze the data that are collected from the various secondary sources, I have

implemented some statistical tools. I am using two model, one is for analyzing the

determinants of FII flow and second is for analyzing the avenues of investment for FII

through Cap and Gap analysis.

CHAPTER V: SUGGESTIONS AND CONCLUSION

This section of the report will show all the conclusions and suggestions that I will be

drawing from the above analysis.

6

CONTENTS

i) CERTIFICATE………………………………………………….2

ii) ACKNOWLEDGEMENT ……………………………………...3

iii) PREFACE ……………………………………………………….4

iv) SYNOPSIS ………………………………………………………5

V) CONTENT……………………………………………………….8

CHAPTER 1: INTRODUCTION ……………………………………………….9

i) Background

ii) Research Review

CHAPTER II: RESEARCH METHODOLOGY .………………………...18

i) Research Process

ii) Scope of the study

CHAPTER III: DESCRIPTIVE WORK ……..…………………………….26

i) Regulatory information.

ii) FII flow to India: nature and causes.

iii) Liberalization of foreign institutional investor in India.

iv) Foreign institutional investment in India.

v) Determinants of foreign institutional investor.

CHAPTER IV: DATA ANALYSIS AND INTERPRETATION ……78

i) Conceptual model for analysis

ii) Gap analysis for investment avenues

iii) Findings

CHAPTER V: SUGGESTIONS AND CONCLUSION ……………..94

BIBLIOGRAPHY……………………………………………………….98

ANNEXURE..…………………………………………………………..100

7

CHAPTER – 1

INTRODUCTION OF THE TOPIC

8

INTRODUCTIONForeign investment refers to investments made by the residents of a country in the

financial assets and production processes of another country. After the opening up of the

borders for capital movement, these investments have grown in leaps and bounds. The

effect of foreign investment, however, varies from country to country. It can affect the

factor productivity of the recipient country and can also affect the balance of payments.

In developing countries there has been a great need for foreign capital, not only to

increase the productivity of labor but also because foreign capital helps to build up the

foreign exchange reserves needed to meet trade deficits. Foreign investment provides a

channel through which developing countries can gain access to foreign capital. It can

come in two forms: foreign direct investment (FDI) and foreign institutional investment

(FII). Foreign direct investment involves in direct production activities and is also of a

medium- to long-term nature. But foreign institutional investment is a short-term

investment, mostly in the financial markets. FII, given its short-term nature, can have

bidirectional causation with the returns of other domestic financial markets such as

money markets, stock markets, and foreign exchange markets. Hence, understanding the

determinants of FII is very important for any emerging economy as FII exerts a larger

impact on the domestic financial markets in the short run and a real impact in the long

run. The present study examines the role, impact and relationship of FII’s and Indian

capital market, and also determinants of foreign institutional investment in India, a

country that opened its economy to foreign capital following a foreign exchange crisis.

India, being a capital scarce country, has taken many measures to attract foreign

investment since the beginning of reforms in 1991. Up to the end of January 2003, India

succeeded in attracting a total foreign investment of around U.S.$48 billion out of which

U.S.$12 billion was in the form of FII. These figures show the importance of FII in the

overall foreign investment program. India is in the process of liberalizing its capital

account, and this has a significant impact on foreign investment and particularly on FII,

which affects short-term stability in the financial markets.

Hence, there is a need to determine the push and pull factors behind any change in the

FII, so that we can frame our policies to influence the variables that attract foreign

9

investment. Also, FII has been the subject of intense discussion, as it is held to be

responsible for having intensified the currency crises of the 1990s in East Asia and

elsewhere in the world.

The present study aims to examine the role, impact, determinants and avenues of

investment for FII in the Indian context.

We attempt to analyze the effect of return, risk, and inflation, which in the research are

considered to be the major determinants of FII. The proposed relationship among the

factors (discussed in detail later) is that inflation and risk in the domestic country and

return in the foreign country adversely affect the FII flowing to the domestic country,

whereas inflation and risk in the foreign country and return in the domestic country have

a favorable effect on the flow of FII. In the next section we will briefly consider the

existing studies of this topic. In Section III, we discuss the theoretical model. Section IV

briefly assesses the trends in FII in India. The database and methodology adopted in this

study are explained in Section V. In Section VI, we discuss the estimated results of the

study, and appropriate conclusions are drawn in the last section.

There is another concept called “foreign portfolio investments” (FPI), which is a broader

one compared to FII. Foreign portfolio investments include FII and other components

like GDR (Global Depositary Receipts), ADR (American Depositary Receipts), and off-

shore funds and others. As the components in FPI other than FII are not dependent on

market forces and they are not volatile, we consider only FII in this study.

10

THE BACKGROUND

An FII means an entity established or incorporated outside India, which proposes to

undertake investment in India; while an FII sub-account includes those foreign corporate,

foreign individuals, institutions, funds or portfolios established or incorporated outside

India on whose behalf investments are proposed to be made in India by an FII

The national common minimum programmed of the present UPA government envisages

policies, which encourage foreign institution investors (FIIs), but reduce exposure to the

Indian financial system to speculative capital flows.

The character of global capital flows to developing countries underwent significant

changes on many counts during the 'nineties. By the time the East Asian financial crisis

surfaced, the overall size of the flows more than tripled. It stood at US$ 100.8 bn. in 1990

and rose to US$ 308.1 bn. by 1996. The increase was entirely due to the sharp rise in the

flows under private account that rose from US$ 43.9 bn. to 275.9 billion during the same

period. In relative terms the percentage of private account capital flows increased from

43.55 to 89.55 per cent. Simultaneously, the Official Development Assistance (ODA),

declined both in relative and absolute terms. All the main components of the private

account capital transfers, namely, (a) commercial loans, (b) foreign direct investments

(FDI), and (c) foreign portfolio investments (equity and bonds) (FPI) recorded significant

increases. Portfolio flows increased at a faster rate than direct investments on private

account. As a result, starting with a low level of 11.16 per cent, the share of capital flows

in the form of portfolio investments quadrupled to reach 37.22 per cent in 1996 reflecting

the enhanced emphasis on private capital flows with portfolio investments forming the

second important constituent of the flows during the 'nineties. In this process multilateral

bodies led by the International Finance Corporation (IFC) played a major role.

Following the East Asian financial crisis, initially there was a slow down followed, by a

decline in private capital flows. While bonds and portfolio equity flows reacted quickly

and declined in 1997 itself, loans from commercial banks dropped a year later in 1998.

Decline in FDI was also delayed. But the fall in FDI was quite small compared to the

11

other three major forms of private capital flows. While flows on official account

increased, following the crisis, they continue to constitute only a small portion of the total

flows. Thus, starting with the resolve by the developed countries to provide one per cent

of their GNP as developmental aid, the industrialised world preferred to encourage

private capital transfers through direct investments instead of official assistance. The

declining importance of official development finance is attributed to budgetary

constraints in donor countries and the optimism of private investors in the viability of the

developing countries.

12

Portfolio investments spread risk for foreign investors, and provide an opportunity to

share the fruits of growth of developing countries, which are expected to grow faster.

Investing in emerging markets is expected to provide a better return on investments for

pension funds and private investors of the developed countries. For developing countries,

foreign portfolio equity investment has different characteristics and implications

compared to FDI. Besides supplementing domestic savings, FDI is expected to facilitate

transfer of technology, introduce new management and marketing skills, and helps

expand host country markets and foreign trade. Portfolio investments supplement foreign

exchange availability and domestic savings but are most often not project specific. FPI,

are welcomed by developing countries since these are non-debt creating. FPI, if involved

in primary issues, provides critical risk capital for new projects. Since FPI takes the form

of investment in the secondary stock market, it does not directly contribute to creation of

new production capabilities. To enable FPI flows which prefer easy liquidity, multilateral

bodies, led by the International Finance Corporation (IFC), have been encouraging

establishment and strengthening of stock markets in developing countries as a medium

that will enable flow of savings from developed countries to developing countries.

FPI, it is expected, could help achieve a higher degree of liquidity at stock markets,

increase price-earning (PE) ratios and consequently reduce cost of capital for investment.

FPI is also expected to lead to improvement in the functioning of the stock market, as

foreign portfolio investors are believed to invest on the basis of well-researched strategies

and a realistic stock valuation. The portfolio investors are known to have highly

competent analysts and access to a host of information, data and experience of operating

in widely differing economic and political environments. Host countries seeking foreign

portfolio investments are obliged to improve their trading and delivery systems, which

would also benefit the local investors. To retain confidence of portfolio investors’ host

countries are expected to follow consistent and business friendly liberal policies. Having

access to large funds, foreign portfolio investors can influence developing country capital

markets in a significant manner especially in the absence of large domestic investors.

Portfolio investments have some macroeconomic implications. While contributing to

build-up of foreign exchange reserves, portfolio investments would influence the

13

exchange rate and could lead to artificial appreciation of local currency. This could hurt

competitiveness. Portfolio investments are amenable to sudden withdrawals and therefore

these have the potential for destabilizing an economy.

The volatility of FPI is considerably influenced by global opportunities and flows from

one country to another. Though it is sometime argued that FDI and FPI are both equally

volatile, the Mexican and East Asian crises brought into focus the higher risk involved in

portfolio investments. The present paper has two objectives. One, to assess the

importance of different types of foreign portfolio investments in capital flows to India.

And two, to understand the investment behaviour of foreign portfolio investors through

an analysis of the portfolios of US-based India specific funds. Such an exercise, it is

hoped, would explain the relationship between foreign institutional investments and

trading pattern in the Indian stock market better than aggregate level analysis.

14

RESEARCH REVIEW

There have been several attempts to explain FII behavior in India. All the existing studies

have found that equity return has a significant and positive impact on FII (Agarwal 1997;

Chakrabarti 2001; Trivedi and Nair 2003). But given the huge volume of investments,

foreign investors can play the role of market makers and book their profits, that is, they

can buy financial assets when the prices are declining, thereby jacking-up the asset

prices, and sell when the asset prices are increasing (Gordon and Gupta 2003). Hence,

there is a possibility of a bidirectional relationship between FII and equity returns.

Following the Asian financial crisis and the bursting of the info-tech bubble

internationally in 1998/99, net FII declined by U.S.$61 million. This, however, exerted

little effect on equity returns. This negative investment might possibly disturb the long-

term relationship between FII and other variables such as equity returns, inflation, and so

on. Chakrabarti (2001) has perceived a regime shift in the determinants of FII following

the Asian financial crisis and found that in the pre–Asian crisis period, any change in FII

had a positive impact on equity returns. But it was found that in the post–Asian crisis

period, a reverse relationship has been the case, namely, that change in FII is mainly due

to change in equity returns. This is a fact that needs to be taken into account in any

empirical investigation of FII. Investments, either domestic or foreign, depend heavily on

risk factors. Hence, while studying the behavior of FII, it is important to consider the risk

variable. Further, realized risk can be divided into ex-ante and unexpected risk. Ex-ante

risk is an observed component and is negatively related to FII. But the relationship

between unexpected risk and FII is obscure. Therefore, while examining the impact of

risk on FII, one needs to separate the unobserved component from the realized risk.

Trivedi and Nair (2003) have used only the realized risk. Another possible determinant of

FII is the operation of foreign factors such as returns in the source country’s financial

markets and other real factors in the source economy. So far, however, studies have

found that both return in the source country stock market and the inflation rate have not

exerted any impact on FII. Agarwal (1997) found that world stock market capitalization

had a favorable impact on the FII in India.

15

A survey of the literature shows that existing studies do not account for volatility, which

can be expected in most of the monthly financial time series data. Yet given the increase

in financial market integration, both domestically and in foreign financial markets,

accounting for volatility is unavoidable. Further, the existing studies either do not

incorporate risk in foreign and domestic markets or make use of realized risk, an

approach that does not always yield robust results.

This is because standard deviation/variance (realized risk variable) increases irrespective

of the direction in which stock returns move, while movement of FII is determined by

bull/bear phases. It is preferable, therefore, to divide the realized risk into ex-ante risk

and unpredictable risk. Since investment in stock markets is sentiment driven, and is

affected more or less by everything, the crucial task is to identify a few critical

determinants. This research makes a modest attempt to explore the relation between FII

and its pivotal determinants, for the particular case of India. More specifically, a few

important variables believed to be affecting FII are chosen and then a theoretical model is

built and empirically tested for India. The focus of this research is the study of the critical

determinants of FII, so as to provide a better understanding of FII behavior that helps

while liberalizing the capital account and investment avenues for FII in Indian capital

market. We hope that the study will be important from a policy perspective, as FII

constitutes an important element for the smooth functioning of domestic financial

markets.

16

CHAPTER – 2

RESEARCH MATHEDOLOGY

17

RESEARCH MATHEDOLOGY

The purpose of research is to discover answers to the questions through the application of

scientific procedures. The main aim of research is to find out the truth which is hidden

and which has not been discovered as yet. Though each research study has its own

specific purpose, we may think of research objectives as falling into a number of

following broad categories:

1) To gain familiarity with a phenomenon or to achieve new insights into it.

2) To portray accurately the characteristics of a particular individual, situation or

a group.

3) To determine the frequency with which something occurs or with which it is

associated with something else.

4) To test a hypothesis of a casual relationship between variables.

Research methodology is a way to systematically solve the research problem. It may be

understood as a science of studying how research is done scientifically. In it we study the

various steps that are generally adopted by a researcher in studying his research problem

along with the logic behind them.

Research methodology has many dimensions and research methods do constitute a part of

the research methodology. The scope of research methodology is wider than that of

research methods. Thus, when we talk of research methodology we not only talk of the

research methods but also consider the logic behind the methods we use in the context of

our research study and explain why we are using a particular method or technique and

why we are not using others so that research results are capable of being evaluated either

by the researcher himself or by others. Why a research study has been undertaken, what

data have been collected and what particular method has been adopted, why particular

technique of analyzing data has been used and a host of similar other question are usually

answered when we talk of research methodology concerning a research problem or study.

18

Research Process

Research process consists of series of actions or steps necessary to effectively carry out

research and the desired sequencing of these steps.

Review theLiterature Feed forward

Feed back

A brief description of the above steps is stated below:

1) Formulating the research problem

At the very outset the researcher must single out the problem he wants to study,

i.e. that is he must decide the general area of interest or aspect of a subject matter that he

would like to inquire into. Initially the problem may be stated in a broad general way and

then the ambiguities, if any, relating to the problem be resolved. Then the feasibility of a

particular solution has to be considered before a working formulation of the problem can

be set up. In fact, formulation of the problem often follows a sequential pattern where a

number of formulations are set up, each formulation more specific than the preceding

one, each one phrased in more analytical terms, and each more realistic in terms of the

available data and resources. In this research the problem that I have formulated is ‘role

and impact of foreign institutional investor on Indian capital market.’

19

Define research problem

Review concepts & theories

Review previous research & findings

Formulate hypotheses Design

research

Interpret and report

Analyze data

Collect data

2) Extensive literature survey

Once the problem is formulated, a brief summary of it should be written down. At

this juncture I have undertaken extensive literature survey connected with the problem.

The earlier studies, which are similar to the study in hand have been carefully studied.

3) Development of the working hypothesis

After extensive literature survey, researcher should state in clear terms the

working hypothesis or hypotheses. Working hypothesis is tentative assumption made in

order to draw out and test its logical or empirical consequences. The manner in which

research hypothesis are developed is particularly important since they provide the focal

point for research. They also affect the manner in which tests must be conducted in the

analysis of the data and indirectly the quality of data, which is required for the analysis.

4) Preparing the research design

The research problem having been formulated in clear-cut terms, the researcher will be

required to prepare a research design i.e. he will have to state the conceptual structure

within which research would be conducted. In other words the function of research

design is to provide for the collection of relevant evidence with minimal expenditure of

effort, time and money.

The preparation of the research design, involves usually the consideration of the

following:

a) The means of obtaining the information:

b) The availability and skills of the researcher and his

staff;

c) Explanation of the way in which selected means of

obtaining information will

be organized and the reasoning leading to the selection;

20

d) The time available for research; and

e) The cost factor relating to research.

5) Determining sample design

All the items under consideration in any field of inquiry constitute a ‘universe’ or

‘population’. Quite often we select only a few items from the universe for our study

purposes. The items so selected constitute what is technically called a sample.

The researcher must decide the way of selecting a sample or what is popularly known as

the sample design. In other words, a sample design is a definite plan determined before

any data are actually collected for obtaining a sample from a given population

6) Collecting the data

In dealing with any real life problem it becomes necessary to collect data that are

appropriate. There are several ways of collecting the appropriate data.

Primary data can be collected either through experiment or through survey.but in case of

survey; data can be collected by any one of the following ways:

a) By observation.

b) Through personal interview.

c) Through telephone interview.

d) By mailing of questionnaires.

e) Through schedules.

The researcher should select one of these methods of collecting the data taking into

consideration the nature of investigation, objective and scope of the inquiry.

21

7) Execution of the project

Execution of the project is a very important step in the research process. The researcher

should see that the project is executed in a systematic manner and in time. A careful

watch should be kept for unanticipated factors in order to keep the survey as much

realistic as possible.

8) Analysis of the data

After the data have been collected, the researcher turns to the task of analyzing them.the

analysis of data requires a number of closely related operations such as establishment of

categories, the application of these categories to raw data through coding, tabulation and

then drawing statistical inferences.

Analysis work after tabulation is generally based on the computation of various

percentages, coefficients, etc. in brief the researcher can analyse the collected data with

the help of various statistical tools.

9) Hypothesis-testing

After analyzing the data, the researcher is in a position to test the hypothesis, if any, he

had formulated earlier. Do the facts support the hypothesis or they happen to be contrary?

This is the usual question, which should be answered while testing the hypothesis.

10) Generalisations and interpretation

If a hypothesis is tested and upheld several times, it may be possible for the

researcher to arrive at generalization, i.e., to build a theory. As a matter of fact, the real

value of research lies in its ability to arrive at certain generalization.

22

11) Preparation of the report

Finally the researcher has to prepare the report of what has been done by him.

Writing of report must be done with great care keeping in view the following:

1) In its preliminary pages the report should carry the title and data

followed by acknowledgements and foreword.

2) Report should be written in a concise and objective style.

3) Charts and illustrations in the main report should be used only if

they present the information more clearly and forcibly.

23

SCOPE OF THE STUDY

A number of studies in the past have observed that investments by FIIs and the

movements of Sensex are quite closely correlated in India and FIIs wield significant

influence on the movement of sensex. There is little doubt that FII inflows have

significantly grown in importance over the last few years. In the absence of any other

substantial form of capital inflows, the potential ill effects of a reduction in the FII flows

into the Indian economy can be severe. From the point of attracting foreign capital, the

initial expectations have not been realised. Investment by FIIs directly in the Indian stock

market did not bring significantly large amount compared to the GDR issues. GDR

issues, unlike FII investments, have the additional advantage of being project specific and

thus can contribute directly to productive investments. FII investments, seem to have

influenced the Indian stock market to a considerable extent.

Results of this study show that not only the FIIs are the major players in the domestic

stock market in India, but their influence on the domestic markets is also growing. Data

on trading activity of FIIs and domestic stock market turnover suggest that FII’s are

becoming more important at the margin as an increasingly higher share of stock market

turnover is accounted for by FII trading. Moreover, the findings of this study also indicate

that Foreign Institutional Investors have emerged as the most dominant investor group in

the domestic stock market in India. Particularly, in the companies that constitute the

Bombay Stock Market Sensitivity Index (Sensex), their level of control is very high. Data

on shareholding pattern show that the FIIs are currently the most dominant non-promoter

shareholder in most of the Sensex companies and they also control more tradable shares

of Sensex companies than any other investor groups.

24

CHAPTR – 3

DESCRIPTIVE WORK ON SUBTOPICS

25

REGULATORY INFORMATION

FII flows to India formally began in September 1992 under the foreign portfolio

investment (FPI) scheme, when the Government of India issued the Guidelines for

Foreign Institutional Investment. In November 1995, the Securities and Exchange Board

of India (SEBI) 6 enforced the Securities and Exchange Board of India (Foreign

Institutional Investors) Regulations, 1995 (henceforth, referred to as SEBI FII

Regulations) to regulate matters relating to FII investment flows. At present, investment

by FIIs is jointly regulated by this and Regulation 5(2) of the Foreign Exchange

Management Act (FEMA), 1999. The SEBI regulations require FIIs to register with the

SEBI and also obtain approval from the Reserve Bank of India (RBI) under the FEMA

for securities trading, operating foreign currency and rupee bank accounts and remitting

and repatriating funds. In the entire process of FII registration and regulation, the SEBI

acts as the nodal authority and once SEBI registration has been obtained, an FII does not

require any further permission for trading securities or for transferring funds into or out

of India. The SEBI FII Regulations and RBI policies are amended and modified from

time to time in response to the gradual maturing of the Indian financial market and

changes taking place in the global economic scenario. Such modification, needless to

mention, is required to be done to ensure quantitative as well as qualitative improvements

in the portfolio flows through the FII route, as India has to compete with other Asian

nations and other emerging markets of the world for global capital inflows.

In India, FII investment (in shares and debentures) started in January 1993. FII

regulations by the SEBI were first introduced on November 14, 1995 in the form of the

SEBI FII Regulations. Over the years, the SEBI and the RBI together, through a variety

of measures, are trying to improve the scope, coverage and quality of FII investment.

These measures include (a) widening the array of instruments in which

FIIs are allowed to trade, (b) expanding the list of the types of funds that can be

registered as FIIs in India and the entities on behalf of whom they can invest, (c) raising

the caps for FII investment in different sectors and companies, (d) easing the norms for

26

FII registration, reducing procedural delays, lowering fees, etc., and (e) mandating stricter

disclosure norms, etc. A summary of the major regulatory changes relating

to FIIs along with their reference dates is presented in Table 1.

The hypothesis underlying the present empirical analysis is essentially that

both strengthening of the regulatory infrastructure by the SEBI and the RBI

on the one hand and further liberalisation and easing of regulatory curbs for

FIIs at various time points in history on the other have had a positive impact

on the flows to the national stock markets.

27

28

29

30

31

THE PRE- AND POST-FII REGULATION PERIODS

The SEBI FII Regulations, introduced in mid-November 1995, formally set forth in

detail:

• Conditions and procedures for grant or renewal of certificates to FIIs (and their sub-

accounts) permitting them to operate directly in the Indian stock market. (This includes

the eligibility criteria for being permitted to be registered as an FII in India; verification

of whether it is legally permissible for the applicant to invest in securities outside the

country of its incorporation; whether the applicant has been registered with any statutory

authority in that country; and whether any legal proceeding has been initiated by any

statutory authority against the applicant.)

• Conditions for and restrictions on investment, which include the type of instruments an

FII is allowed to invest in, and the applicable caps or ceilings in respect of different types

of instruments (or sectors), etc.

• General obligations and responsibilities, which include appointment of a domestic

custodian; appointment of a branch of a bank approved by the RBI for opening of foreign

currency denominated accounts and special non-resident rupee accounts; maintenance of

proper books of accounts, records, etc.

• Procedure for action in case of default and suspension/cancellation of certificate.

• The fees and taxes to be paid.

• Provisions for appeal in case of any grievances.

32

It is obviously of interest to see whether the introduction of the SEBI FII Regulations had

any immediate repercussions on FII equity investments, causing a major gap between the

pre- and post- regulation flows. We use the monthly data series of FII net equity inflows

(FIINM) to study this impact. However, in the post-regulation period, the Asian currency

crisis had a very strong negative effect on global capital flows, particularly to emerging

Asian economies. In order to filter out this effect, we compare our pre-regulation period

with the post-regulation period up to the beginning of the Asian crisis (which is taken to

be up to June 1997). Comparing the monthly inflows prior to the introduction of the SEBI

Regulations with the corresponding post regulation (pre-Asian crisis) period inflows, it is

easy to see that the average (and median) monthly inflows during these two sub-periods

were quite different, with the post-regulation period having a much higher average (and

median) inflow. A research confirms that the difference between the means (and

medians) of the two sub-periods are indeed statistically significant with the post-

regulation period experiencing much higher flows on an average. Next we consider the

result of a Chow break point test, which helps us detect any significant shift in the flows

immediately after the introduction of the SEBI FII Regulations. To carry out this test, we

regress the monthly net equity flows (FIINM) (for the 54-month preceding the Asian

crisis) on returns on the BSE Sensex (BSER). The result of the Chow test strongly

suggests existence of a structural break in the time series data on FII flows under

consideration at the time point of the introduction of the SEBI Regulations in November

1995, thus confirming that the introduction of a comprehensive set of laws to govern FII

flows had definitely helped to attract more foreign portfolio investment flows into the

country until the onset of the Asian financial crisis.

33

FII FLOWS TO INDIA: NATURE AND CAUSES

Portfolio investment flows from industrial countries have become increasingly important

for developing countries in recent years. The Indian situation has been no different. In the

year 2000-01 portfolio investments in India accounted for over 37% of total foreign

investment in the country and 47% of the current account deficit. The corresponding

figures in the previous year were 59% and 64% respectively. A significant part of these

portfolio flows to India comes in the form of Foreign Institutional Investors’ (FIIs’)

investments, mostly in equities. Ever since the opening of the Indian equity markets to

foreigners, FII investments have steadily grown from about Rs. 2600 crores in 1993 to

over Rs.11,000 crores in the first half of 2001 alone. Their share in total portfolio flows

to India grew from 47% in 1993-94 to over 70% in 1999-20001. The nature of the foreign

investor’s decision-making process, which lies at the heart of the portfolio flows, is

briefly described bellow.

The International Portfolio Investor’s decision-making problem

International portfolio flows, as opposed to foreign direct investment (FDI) flows, refer to

capital flows made by individuals or investors seeking to create an internationally

diversified portfolio rather than to acquire management control over foreign companies.

Diversifying internationally has long been known as a way to reduce the overall portfolio

risk and even earn higher returns. Investors in developed countries can effectively

enhance their portfolio performance by adding foreign stocks particularly those from

emerging market countries where stock markets have relatively low correlations with

those in developed countries. For instance, according to Morgan Stanley Capital

International’s estimates, between 1985 and 1990, an investor holding an all-US portfolio

could improve her returns by over 25% by holding the MSCI world index instead and at

the same time, reduce her risk by about 2%.

The portfolio investor’s problem may be thought of as deciding upon appropriate country

weights in the portfolio so as to maximize portfolio returns subject to a risk constraint, or

in the absence of a pre-specified risk level, to reach the optimum portfolio, that which has

the highest Sharpe ratio, S where the Sharpe ratio is the ratio of expected excess return

(excess over the risk-free rate) to the dispersion (standard deviation) of the return.

34

While it is generally held that portfolio flows benefit the economies of recipient

countries, policy-makers worldwide have been more than a little uneasy about such

investments. Portfolio flows – often referred to as “hot money” – are notoriously volatile

compared to other forms of capital flows. Investors are known to pull back portfolio

investments at the slightest hint of trouble in the host country often leading to disastrous

consequences to its economy. They have been blamed for exacerbating small economic

problems in a country by making large and concerted withdrawals at the first sign of

economic weakness. They have also been held responsible for spreading financial crises

– causing ‘contagion’ in international financial markets. In the wake of the Asian crisis,

prominent economists have, for these reasons, expressed doubts about the wisdom of the

IMF view of promoting free capital mobility among countries.

International capital flows and capital controls have emerged as an important policy

issues in the Indian context as well. The danger of Mexico-style ‘abrupt and sudden

outflows’ inherent with FII flows and their destabilizing effects on equity and foreign

exchange markets have been stressed. Some authors have argued that FII flows have, in

fact, had no significant benefits for the economy at large.

While these concerns are all well-placed, comparatively less attention has been paid so

far to analyzing the FII flows data and understanding their key features. A proper

understanding of the nature and determinants of these flows, however, is essential for a

meaningful debate about their effects as well as predicting the chances of their sudden

reversals. In an attempt to address this lacuna, this paper undertakes an empirical analysis

of FII investment flows to India.

The broad objective of the present paper is to gain a better understanding of the nature

and determinants of FII flows. Towards this end we first take a look at the FII investment

flow data to bring out the key features of these flows. Next we study the relationship

between FII flows and the stock market returns in India with a close look at the issue of

causality. Finally we study the impact of other factors identified in the portfolio flows

literature on the FII flows to India. In all of these investigations we make a distinction

between the pre-Asian crisis period and the post-Asian crisis period to check

if there was a regime shift in the relationships owing to the Asian crisis.

35

The paper is arranged as follows. The next section sketches a brief review of the recent

literature in the area. The third section provides an overview of the nature and sources of

portfolio flows in India pointing out their main characteristics. The fourth section probes

into the possible determinants of FII flows to India. The fifth and final section concludes

with a summary of the major findings and their policy implications.

International Portfolio Flows

International portfolio flows are, as opposed to foreign direct investment, liquid in nature

and are motivated by international portfolio diversification benefits for individual and

institutional investors in industrial countries. They are usually undertaken by institutional

investors like pension funds and mutual funds. Such flows are, therefore, largely

determined by the performance of the stock markets of the host countries relative to

world markets. With the opening of stock markets in various emerging economies to

foreign investors, investors in industrial countries have increasingly sought to realize the

potential for portfolio diversification that these markets present. While the Mexican crisis

of 1994, the subsequent ‘Tequila effect’, and the widespread ‘Asian crisis’ have had

temporary dampening effects on international portfolio flows, they have failed to counter

the long-term momentum of these flows. Indeed, several researchers5 have found

evidence of persistent ‘home bias’ in the portfolios of investors in industrial countries in

the 90’s. This ‘home bias’ – the tendency to hold disproportionate amounts of stock from

the ‘home’ country – suggests substantial potential for further portfolio flows as global

market integration increases over time.

It is important to note that global financial integration, however, can have two distinct

and in some ways conflicting effects on this ‘home bias’. As more and more countries –

particularly the emerging markets – open up their markets for foreign investment,

investors in developed countries will have a greater opportunity to hold foreign assets.

However, these flows themselves, along with greater trade flows will tend to cause

different national markets to increasingly become parts of a more unified ‘global’ market,

reducing their diversification benefits. Which of these two effects will dominate is, of

36

course, an empirical issue, but given the extent of the ‘home bias’ it is likely that for quite

a few years to come, FII flows would increase with global integration.

In recent years, international portfolio flows to developing countries have received the

attention of scholars in the areas of finance and international economics alike. In the 90’s

several papers have explored the causes and effects of cross-border Portfolio investment.

While papers in the finance tradition have focused on the nature and determinants of

portfolio flows from the perspective of the diversifying investors, those from the

international macroeconomics perspective have focused on the recipient country’s

situation and appropriate policy response to such flows. For the present purposes, we

shall focus only on papers that address the issue of portfolio flows exclusively.

Previous research has also attempted to identify the factors behind these capital flows.

The main question is whether capital flew in to these countries primarily as a result of

changes in global (largely US) factors or in response to events and indicators in the

recipient countries like its credit rating and domestic stock market return. The question is

particularly important for policy makers in order to get a better understanding of the

reliability and stability of such flows. The answer is mixed – both global and country-

specific factors seem to matter, with the latter being particularly important in the case of

Asian countries and for debt flows rather than equity flows.

As for the motivation of US equity investment in foreign markets, recent research8

suggest that US portfolio managers investing abroad seem to be chasing returns in

foreign markets rather than simply diversifying to reduce overall portfolio risk. The

findings include the well-documented ‘home bias’ in OECD investments, high turnover

in foreign market investments and that, in general, the patterns of foreign equity

investment were far from what an international portfolio diversification model would

recommend. The share of investments going to emerging markets has been roughly

proportional to the share of these markets in global market capitalization but the volatility

of US transactions were even higher in emerging markets than in other OECD countries.

Furthermore there was no relation between the volume of US transactions in these

markets and their stock market volatility.

The Mexican and Asian crises and the widespread outcry against international portfolio

investors in both cases have prompted analyses of short-term movements in international

37

portfolio investment flows. The question of ‘feedback trading’ has received For the

related literature on international capital flows in general (comprising both FDI and

portfolio flows) considerable attention. This refers to investors’ reaction to recent

changes in equity prices. If a gain in equity values tends to bring in more portfolio

inflows, it is an instance of ‘positive feedback trading’ while a decline in flows following

a rise in equity values is termed ‘negative feedback trading’. Between 1989 and 1996

unexpected equity flows from abroad raised stock prices in Mexico with at the rate of 13

percentage points for every 1% rise in the flows. There has been, however, no evidence

of ‘feedback trading’ among foreign investors in Mexico. In the period leading to the

Asian crisis, on the other hand, Korea witnessed positive feedback trading and significant

‘herding’ among foreign investors. Nevertheless, contrary to the belief in some segments,

these tendencies actually diminished markedly in the crisis period and there has been no

evidence of any ‘destabilizing role’ of foreign equity investors in the Korean crisis. While

FII flows to the Asian Crisis countries dropped sharply in 1997 and 1998 from their pre-

crisis levels, it is generally held that the flows reacted to the crisis (possibly exacerbating

it) rather than causing it.

More recent studies find that the effect of ‘regional factors’ as determinants of portfolio

flows have been increasing in importance over time. In other words portfolio flows to

different countries in a region tend to be highly correlated. Also the flows are more

persistent than returns in the domestic markets. Feedback trading or return-chasing

behavior is also more pronounced. The flows appear to affect contemporaneous and

future stock returns positively, particularly in the case of emerging markets. Finally stock

prices seem to behave on the assumption of persistent portfolio inflows. It is commonly

argued that local investors possess greater knowledge about a country’s financial markets

than foreign investors and that this asymmetry lies at the heart of the observed ‘home

bias’ among investors in industrialized countries. A key implication of recent theoretical

work in this area is that in the presence of such information asymmetry, portfolio flows to

a country would be related to returns in both recipient and source countries. In the

absence of such asymmetry, only the recipient country’s returns should affect these

flows.

38

FOREIGN INSTITUTIONAL INVESTMENT IN INDIA: AN

OVERVIEW

India opened its stock markets to foreign investors in September 1992 and has, since

1993, received considerable amount of portfolio investment from foreigners in the form

of Foreign Institutional Investor’s (FII) investment in equities. This has become one of

the main channels of international portfolio investment in India for foreigners. In order to

trade in Indian equity markets, foreign corporations need to register with the SEBI as

Foreign Institutional Investors (FII). SEBI’s definition of FIIs presently includes foreign

pension funds, mutual funds, charitable/endowment/university funds etc. as well as asset

management companies and other money managers operating on their behalf.

39

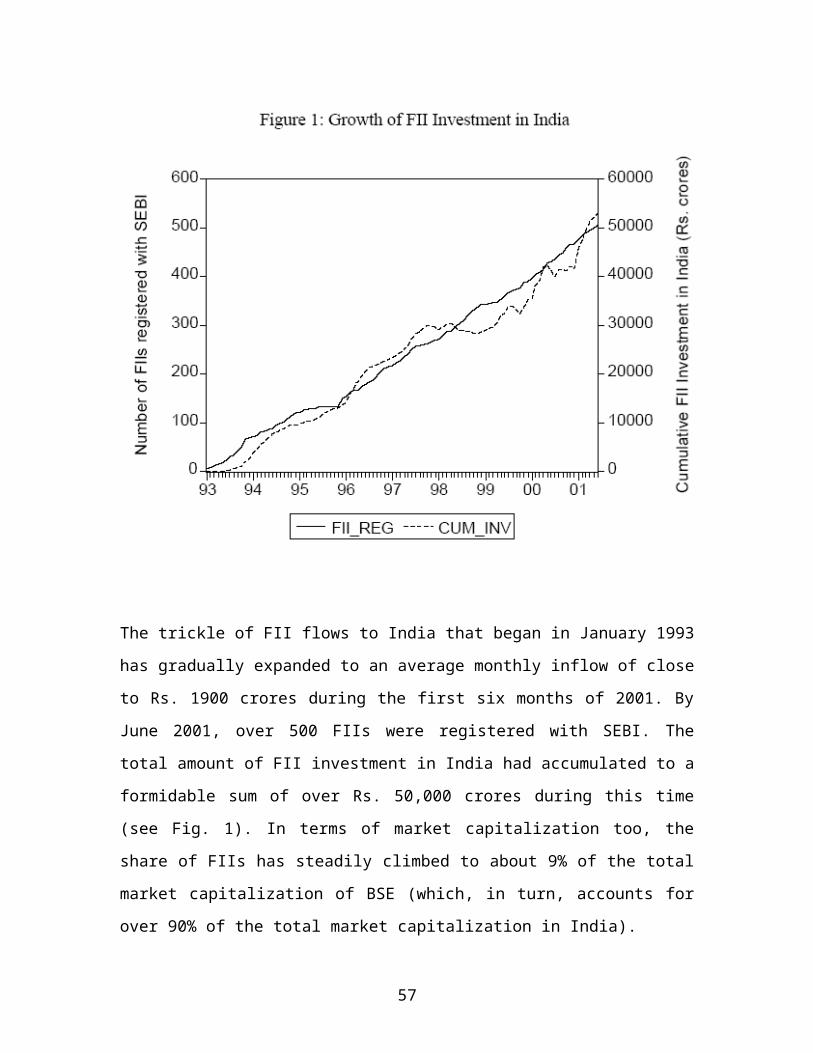

The trickle of FII flows to India that began in January 1993 has gradually expanded to an

average monthly inflow of close to Rs. 1900 crores during the first six months of 2001.

By June 2001, over 500 FIIs were registered with SEBI. The total amount of FII

investment in India had accumulated to a formidable sum of over Rs. 50,000 crores

during this time (see Fig. 1). In terms of market capitalization too, the share of FIIs has

steadily climbed to about 9% of the total market capitalization of BSE (which, in turn,

accounts for over 90% of the total market capitalization in India).

40

The sources of these FII flows are varied. The FIIs registered with SEBI come from as

many as 28 countries (including money management companies operating in India on

behalf of foreign investors). US-based institutions accounted for slightly over 41%, those

from the UK constitute about 20% with other Western European countries hosting

another 17% of the FIIs (Fig. 2). It is, however, instructive to bear in mind The closed-

end country fund, “The India Fund” launched in June 1986 provided a channel for

portfolio investment in India before the stock market liberalization in 1992. Global

Depository Receipts, American Depository Receipts, Foreign Currency Convertible

Bonds and Foreign Currency Bonds issued by Indian companies and traded in foreign

exchanges provide other routes for portfolio investment in India by foreign investors. It is

also possible for foreigners to trade in Indian securities without registering as an FII but

such cases require approval from the RBI or the Foreign Investment Promotion Board.

that these national affiliations do not necessarily mean that the actual investor funds come

from these particular countries. Given the significant financial flows among the industrial

countries, national affiliations are very rough indicators of the ‘home’ of the FII

investments. In particular institutions operating from Luxembourg, Cayman Islands or

Channel Islands, or even those based at Singapore or Hong Kong are likely to be

investing funds largely on behalf of residents in other countries. Nevertheless, the

regional breakdown of the FIIs does provide an idea of the relative importance of

different regions of the world in the FII flows.

41

FACTORS AFFECTING FII FLOWS

In this section we shall study the relationship between FII flows and possible economic

factors affecting it, particularly stock returns in the Indian market.

FII flows and stock returns – determining the cause and the effect

FII flows and contemporaneous stock returns are strongly correlated in India. The

correlation coefficients between different measures of FII flows and market returns on the

Bombay Stock Exchange during different sample periods are shown in the different

panels of Table 1. While the correlations are quite high throughout the sample period,

they exhibit a significant rise since the beginning of the Asian crisis.

42

These positive correlations have often been held as evidence of FII actions determining

Indian equity market returns. However, correlation itself does not imply causality. A

positive relationship between portfolio inflows and stock returns is consistent with at

least four distinct theories: 1) the “omitted variables” hypothesis; 2) the “downward

sloping demand curve” view; 3) the “base-broadening” theory; and 4) the “positive

feedback strategy” view.

The “omitted variables” view is the classic case of spurious correlation – that the

correlated variables, in fact, have no causal relationship between them but are both

affected by one or more other variables missed out in the analysis. The “downward

sloping demand curve” view contends that foreign investment creates a buying pressure

for stocks in the emerging market in question and causes stock prices to rise much in the

same way as suddenly higher demand for a commodity would cause its price to rise. The

‘base-broadening’ argument contends that once foreigners begin to invest in a country,

the financial markets in that country are now no longer moved by national economic

factors alone but rather begin to be affected by foreign market movements as well. As the

market itself is now affected by more factors than before, its exposure to domestic shocks

decline. Consequently the ‘risk’ of the market itself falls, people demand a lower risk

premium to buy stocks, and stock prices rise to higher levels. Finally the ‘positive

feedback view’ asserts that if investors ‘chase’ returns in the immediate past (like the

previous day or week) then aggregating their fund flows over the month can lead to a

positive relationship in the contemporaneous monthly data. In the present context, both

directions of causation are equally plausible.

Further returns on the BSE Index explain close to a third of the total variation in FII

flows during the entire period. They also indicate, however, that the Asian crisis marked

a regime shift in the relationship between FII flows and Indian stock market return.

During and after the crisis, the returns explained about 40% of the total variation in FII

flows. The positive relationship between market return and FII flows, however, serves

only as a first-pass in understanding the nature of such flows and their implications for

the Indian markets. Since the FII flows essentially serve to diversify the portfolio of

foreign investors, it is only normal to expect that several factors – both domestic as well

43

as external to India – are likely to affect them along with the expected stock returns in

India. Past research suggests that the declining world interest rates have been among the

important “push” factors for international portfolio flows in the early 90’s. The “usual

suspects” in the literature include US and world equity returns, changes in interest rates,

stock market volatility, some measure of the country risk and the exchange rate. In the

Indian case, however these factors do not appear to have had a prominent role in

motivating FII flows. Finally it also appears that there has been no significant

informational disadvantage for FIIs vis-à-vis the local investors in the Indian market.

Other factors that may affect FII flows

Country risk measures, that incorporate political and other risks in addition to the usual

economic and financial variables, may be expected to have an impact on portfolio flows

to India though they are likely to matter more in the case of FDI flows. In order to check

the impact of such country risk on FII flows, semi-annual country risk scores for India

were taken from the Institutional Investor magazine, an important country-rating agency.

These raw ratings were then divided by the world average rating to obtain normalized

ratings. The intuition behind this normalization is as follows. If

India’s credit rating improves but that of other countries improve even more, then India

may not improve its relative attractiveness as a destination of investment flows. The

relation between the normalized country rating and the average monthly FII flows (as a

proportion of the preceding month’s BSE capitalization) is shown in Figure 5. The

correlation between the two variables is –0.15. No relationship is evident from the figure

itself and statistical testing confirms this view. Thus we can conclude that broadly

speaking there is no evidence of India’ credit rating affecting FII flows.

44

It is also conceivable that the extent to which the Indian market moves out of step with

the world market is a factor in determining its attractiveness to foreign investors.

The lower the co-movement, the greater the protection that investment in India provides

to investors against world market shocks.

45

LIBERALISATION OF FOREIGN INSTITUTIONAL INVESTMENT

Following the announcement by the Government in the Budget 2002-03 that suggested

those foreign institutional investors’ (FII) portfolio investments would not be subject to

the sectoral limits for foreign direct investment except in specified sectors, a Committee

was constituted with representation from the Department of Economic Affairs as well as

the Department of Industrial Policy and Promotion.

The Committee was reconstituted twice. After the second reconstitution, the Committee

had 5 meetings, the last being held on June, 24, 2004. The report gives an evolution of

FII policy in India, examines the pros and cons of FII investment, especially in an era

with no balance of payment pressures, and also provides a perspective on FII investment

restrictions in peer countries in Asia. The recommendations are as follows:

A. (i) In general, FII investment ceilings, if any, may be reckoned over and above

prescribed FDI sectoral caps. The 24 per cent limit on FII investment imposed in 1992

when allowing FII inflows was exclusive of the FDI limit. The suggested measure will be

in conformity with this original stipulation.

(ii) Special procedure for raising FII investments beyond 24per cent upto the FDI limit in

a company may be dispensed with by amending the relevant SEBI (FII) Regulations.

(iii) In order to provide dispersed investments and prevent concentration, the existing

limit of 10per cent by a FII in a single company may continue.

B Recommendations in para A above would apply, in general, to all sectors.

Specific recommendations are being made for the following sectors with overall

composite caps :

a. Telecom services.

b. Defence production

c. Public sector banks.

d. Insurance companies.

FII investments are currently not permitted in print media, sectors which are not yet

opened for private investment and in gambling, betting, lottery. The Committee

recommends the same may continue.

46

FDI investment in retail trading is prohibited. FII investments, however, are permitted up

to 24 per cent in all listed companies, except in print media companies. The Committee

recommends the same may continue as this would help in developing supply chains in a

wide range of products including that of agriculture.

In his Budget Speech on February 28, 2002, the Finance Minister announced that:

“Foreign Institutional Investors (FIIs) can invest in a company under the portfolio

investment route beyond 24 per cent of the paid-up capital of the company with the

approval of the general body of the shareholders by a special resolution. I propose that

now FII portfolio investments will not be subject to the sectoral limits for foreign direct

investment except in specified sectors. Guidelines in this regard will be issued

separately.”

2. Following this announcement, with the approval of Finance Minister, a committee was

set up on March 13, 2002 to identify the sectors in which FIIs’ portfolio investments will

not be subject to the sectoral limits for Foreign Direct Investment (FDI).

Evolution of FII Investment Policy

India embarked on a gradual shift towards capital account convertibility with the launch

of the reforms in the early 1990s. Although foreign natural persons – except NRIs – are

prohibited from investing in financial assets, such investments were permitted by FIIs

and Overseas Corporate Bodies (OCBs) with suitable restrictions. Ever since September

14, 1992, when FIIs were first allowed to invest in all the securities traded on the primary

and secondary markets, including shares, debentures and warrants issued by companies

which were listed or were to be listed on the Stock Exchanges in India and in the schemes

floated by domestic mutual funds, the holding of a single FII and of all FIIs, Non-resident

Indians (NRIs) and OCBs in any company were subject to the limit of 5 per cent and 24

per cent of the company’s total issued capital, respectively. Furthermore, funds invested

by FIIs had to have at least 50 participants with no one holding more than 5 per cent to

ensure a broad base and preventing such investment acting as a camouflage for individual

investment in the nature of FDI and requiring Government approval.

47

Initially the idea of allowing FIIs was that they were broad-based, diversified funds,

leaving out individual foreign investors and foreign companies. The only exceptions were

the NRI and OCB portfolio investments through the secondary market, which were

subject to individual ceilings of 5 per cent to prevent a possible “take over.” Individuals

were left out because of the difficulties in checking on their antecedents, and of their lack

of expertise in market matters and relatively short-term perspective. OCB investments

through the portfolio route have been banned since November, 2001.

In February, 2000, the FII regulations were amended to permit foreign corporates and

high net worth individuals to also invest as sub-accounts of Securities and Exchange

Board of India (SEBI)-registered FIIs. Foreign corporates and high net worth individuals

fall outside the category of diversified investors. FIIs were also permitted to seek SEBI

registration in respect of sub-accounts for their clients under the regulations. While

initially FIIs were permitted to manage the sub-account of clients, the domestic portfolio

managers or domestic asset management companies were also allowed to manage the

funds of such sub-accounts and also to make application on behalf of such sub-accounts.

Such sub-accounts could be an institution, or a fund, or a portfolio established or

incorporated outside India, or a broad-based fund, or a proprietary fund, or even a foreign

corporate or individual. So, in practice there are common categories of entities, which

could be registered as both FIIs and sub-accounts. However, investment in to a sub

account is to be made either by FIIs, or by domestic portfolio manager or asset

Management Company, and not by itself directly.

In view of the recent concerns of some unregulated entities taking positions in the stock

market through the mechanism of Participatory Notes (PNs) issued by FIIs, the issue was

examined by the Ministry of Finance in consultation with the Reserve Bank of India

(RBI) and SEBI. Following this consultation, in January 2004, SEBI stipulated that PNs

are not to be issued to any non-regulated entity, and the principle of "know your clients”

may be strictly adhered to. SEBI has indicated that the existing non-eligible PNs, will be

permitted to expire or to be wound-down on maturity, or within a period of 5 years,

whichever is earlier. Besides, reporting requirement on a regular basis has been imposed

on all the FIIs.

48

The following entities, established or incorporated abroad, are eligible to be registered as

FIIs:

(a)Pension Funds,

(b)Mutual Funds,

(c)vestment Trusts,

(d) Asset Management Companies,

(e) Nominee Companies,

(f) Banks,

(g) Institutional Portfolio Managers,

(h) Trustees, (i) Power of Attorney holders,

(j) University funds, endowments, foundations or charitable trusts or charitable societies.

Besides the above, a domestic portfolio manager or domestic asset management

company is now also eligible to be registered as an FII to manage the funds of

subaccounts.

The FIIs can also invest on behalf of sub-accounts. The following entities are entitled to

be registered as sub-accounts: i) an institution or fund or portfolio established or

incorporated outside India, ii) a foreign corporate or a foreign individual.

FIIs registered with SEBI fall under the following categories:

(a) Regular FIIs – those who are required to invest not less than 70 per cent of their

investment in equity-related instruments and up to 30 per cent in non-equity instruments.

(b) 100 per cent debt-fund FIIs – those who are permitted to invest only in debt

instruments.

A Working Group for Streamlining of the Procedures relating to FIIs constituted in April,

2003 by the Government, inter alia, recommended streamlining of SEBI registration

procedure, and suggested that dual approval process of SEBI and RBI be changed to a

single approval process of SEBI. This recommendation has since been implemented.

Forward cover in respect of equity funds for outstanding investments of FIIs over and

above such investments on June 11, 1998 was permitted. Subsequently, forward cover up

to a maximum of 15 per cent of the outstanding position on June 11, 1998 was also

49

permitted. This 15 per cent limit was liberalized to 100 per cent of portfolio value as on

March 31, 1999 in January 2003.

Like in other countries, the restrictions on FII investment have been progressively

liberalized. From November 1996, any registered FII willing to make 100 per cent

investment in debt securities were permitted to do so subject to specific approval from

SEBI as a separate category of FIIs or sub-accounts as 100 per cent debt funds. Such

investments by 100 per cent debt funds were, however, subject to fund-specific ceilings

specified by SEBI and an overall debt cap of US$ 1-1.5 billion. Moreover, investments

were allowed only in debt securities of companies listed or to be listed in stock

exchanges. Investments were free from maturity limitations.

From April 1998, FII investments were also allowed in dated Government securities.

Treasury bills being money market instruments were originally outside the ambit of such

investments, but were subsequently included from May, 1998. Such investments, which

are external debt of the Government denominated in rupees, were encouraged to deepen

the debt market. From April, 1997, the aggregate limit for all FIIs, which was 24 per cent,

was allowed to be increased up to 30 per cent by the Indian company concerned by

passing a resolution by its Board of Directors followed by a special resolution to that

effect by its General Body.

While permitting foreign corporates/high net worth individuals in February, 2000 to

invest through SEBI registered FII/domestic fund managers, it was noted that there was a

clear distinction between portfolio investment and FDI. The basic presumption is that

FIIs are not interested in management control. To allay fears of management control

being exercised by portfolio investors, it was noted that adequate safety nets were in

force, for example, (i) transaction of business in securities on the stock exchanges are

only through stock brokers who have been granted a certificate by SEBI, (ii) every

transaction is settled through a custodian who is under obligation to report to SEBI and

RBI for all transactions on a daily basis, (iii) provisions of SEBI (Substantial Acquisition

of Shares and Takeovers) Regulations, 1997 (iv) monitoring of sectoral caps by RBI on a

daily basis.

50

In 1998, the aggregate portfolio investment limits of NRIs/PIOs/OCBs and FIIs were

enhanced from 5 per cent to 10 per cent and the ceilings of FIIs and NRIs/OCBs were

declared to be independent of each other.

Aggregate FII portfolio investment ceiling was enhanced from 30 per cent to 40 per cent

of the issued and paid up capital of a company [March 01 2000]. The enhanced ceiling

was made applicable only under a special procedure that required approval by the

Board of Directors and a Special Resolution by the General Body of the relevant

company. The FII ceiling under the special procedure was further enhanced [March 08

2001] from 40 per cent to 49 per cent. Subsequently, the FII ceiling under the special

procedure was raised up to the sectoral cap in September, 2001.

Sectoral Caps

Quite apart from the ceilings on FII investment, there were and are ceilings on FDI, and

in some cases, unified ceilings for nonresident investments. There are two types of

ceilings on FII investment: statutory and administrative.

Currently non-resident investments in public sector banks and insurance sector are

capped under Acts at 20 per cent and 26 per cent respectively. Accordingly, FDI plus

portfolio investments by FIIs and NRIs are capped at 20 per cent and 26 per cent under

the above statutes.

There are also sectors where administrative caps for non-resident investments have been

prescribed. In these sectors (viz. telecom services, media, private sector 10 banks) FDI

plus portfolio investments by FIIs and NRIs cannot exceed the administrative caps fixed.

Caps can be of three types:

i) a separate cap on FDI,

ii) a separate cap on FII, and

iii) a composite caps on FDI and FII combined together.

51

Separate caps on FDI and FII, in turn, can be of five types:

I) ban on both FDI and FII (e.g. lottery business, gambling and betting),

II) non-zero separate caps on both FDI and FII ([e.g., DTH-broadcasting]), [DTH has

composite ceiling with a sub-ceiling for FDI at 20 per cent]

III) a composite non-zero cap on FDI and FII (banking, insurance, telecom)

IV) ban on FDI with a non-zero cap on FII (e.g.,Terrestrial broadcasting FM,

retail trading), and

V) ban on FII with a non-zero cap on FDI (e.g. print media).

For example, for private sector banks falling within the purview of the RBI’s regulatory

jurisdiction, no distinction is made either between different categories of nonresident

investors or the nature of foreign investment, whether portfolio or FDI.

Similarly, no distinction is made either between different categories of sub-sectors of FM

radio broadcasting and satellite uplinking, cable network and Direct-to-home. The

sectoral equity caps as of May 13, 2004 are given in Table 1 (at annex1).

In August, 2002, the Steering Group on Foreign Direct Investment headed by Shri

N.K.Singh, Member, Planning Commission, submitted its report.1 In this report, six

reasons given for imposing caps and bans on FDI national security, culture and media,

natural monopolies, monopoly power, natural resources, and transition costs, were

discussed in some detail.

The Steering Group observed that while all governments prefer vital defence industries to

be controlled by their own resident nationals, there was not much justification for

restrictions on the production of civilian goods used by the defence forces, and

production of those goods that are either imported or are banned for exports from

developed countries for strategic reasons. On culture and media, the Steering Group

observed that there was a need for true cultural globalization – not a one-way process of

only India having access to the culture of the rest of the world but a two-way street – and

in the field of current affairs and news programmes, editorial control must vest with

52

Indian nationals and eventually could be replaced by limits on aggregate market share (25

– 49 per cent) that can accrue to foreign controlled news/current affairs companies taken

together.

As regards natural monopolies, the Steering Group observed that in the absence of a